∎

22email: peter.richtarik@kaust.edu.sa 33institutetext: Majid Jahani 44institutetext: Industrial and Systems Engineering, 200 West Packer Avenue, Bethlehem, PA 18015, USA 44email: majidjahani89@gmail.com 55institutetext: Selin Damla Ahipaşaoğlu 66institutetext: Engineering Systems and Design, Sing. Univ. Tech. & Design, 8 Somapah Road, Singapore 66email: ahipasa@gmail.com 77institutetext: Martin Takáč 88institutetext: Industrial and Systems Engineering, 200 West Packer Avenue, Bethlehem, PA 18015, USA 88email: takac.mt@gmail.com

Alternating maximization: unifying framework for 8 sparse PCA formulations and efficient parallel codes††thanks: MT was partially supported by National Science Foundation grants CCF-1618717, CMMI-1663256 and CCF-1740796.

Abstract

Given a multivariate data set, sparse principal component analysis (SPCA) aims to extract several linear combinations of the variables that together explain the variance in the data as much as possible, while controlling the number of nonzero loadings in these combinations. In this paper we consider 8 different optimization formulations for computing a single sparse loading vector: we employ two norms for measuring variance (L2, L1) and two sparsity-inducing norms (L0, L1), which are used in two ways (constraint, penalty). Three of our formulations, notably the one with L0 constraint and L1 variance, have not been considered in the literature. We give a unifying reformulation which we propose to solve via the alternating maximization (AM) method. We show that AM is equivalent to GPower for all formulations. Besides this, we provide 24 efficient parallel SPCA implementations: 3 codes (multi-core, GPU and cluster) for each of the 8 problems. Parallelism in the methods is aimed at i) speeding up computations (our GPU code can be 100 times faster than an efficient serial code written in C++), ii) obtaining solutions explaining more variance and iii) dealing with big data problems (our cluster code can solve a 357 GB problem in a minute).

Keywords:

sparse PCA alternating maximization GPower big data analytics unsupervised learning1 Introduction

Principal component analysis (PCA) is an indispensable tool used for dimension reduction in virtually all areas of science and engineering, from machine learning, statistics, genetics and finance to computer networks (Jollife, 1986). Let denote a data matrix encoding samples (observations) of variables (features). PCA aims to extract a few linear combinations of the columns of , called principal components (PCs), pointing in mutually orthogonal directions, together explaining as much variance in the data as possible. If the columns of are centered, the problem of extracting the first PC can be written as

| (1.1) |

where is a suitable norm for measuring variance. The solution of this optimization problem is called the loading vector, (normalized) is the first PC. Further PCs can be obtained in the same way with replaced by a new matrix in a process called deflation (Mackey, 2008). Classical PCA employs the norm in the objective; using the norm instead may alleviate problems caused by outliers in the data and hence leads to a robust PCA model (Kwak, 2008). Robust formulations using objective functions that are not functions of the covariance matrix (as in Croux et al. (2013)) are also possible, but these are beyond our investigation.

As normally there is no reason for the optimal loading vectors defining the PCs to be sparse, they are usually combinations of all of the variables. In some applications, however, sparse loading vectors enhance the interpretability of the components and are easier to store, which leads to the idea to induce sparsity in the loading vectors. This problem and approaches to it are known collectively as sparse PCA (SPCA); for some fundamental work, refer to Zou et al. (2006); Moghaddam et al. (2006); d’Aspremont et al. (2007, 2008); Shen and Huang (2008); Lu and Zhang (2012); Journée et al. (2010); Luss and Teboulle (2013); Meng et al. (2012). Recent reviews on the subject can be found in Trendafilov (2016) and Hastie et al. (2015). In addition, recently, there has been great interest in establishing theoretical properties of sparse PCA including consistency, rates of convergence, minimax risk bounds for estimating eigenvectors and principal subspaces and detection under various and usually high-dimensional statistical models. See (Amini and Wainwright, 2009), (Vu and Lei, 2013), (Vu et al., 2013), and (Lei and Vu, 2015). The importance of robust and sparse models is getting more attention from various communities. For example, Robust Principal Component Analysis (RPCA), sometimes referred to as the Principal Component Pursuit (PCP), which decomposes a data matrix in a low-rank matrix and a sparse matrix has been investigated for video and signal processing (Candès et al., 2011; Hubert et al., 2016; Aravkin and Becker, 2016; Bouwmans et al., 2017) and inducing sparsity into robust estimators has been successful in robust outlier detection (Hubert et al., 2016). A popular way of incorporating a sparsity-inducing mechanism into optimization formulation (1.1) is via either a sparsity-inducing constraint or penalty. Two of the most popular functions for this are the and norm of the loading vector (the “norm” of , denoted by , is the number of nonzeros in ).

1.1 Eight optimization formulations

In this paper we consider 8 optimization formulations for extracting a single sparse loading vector (i.e., for computing the first PC) arising as combinations of the following three modeling factors: we use two norms for measuring variance (classical and robust ) and two sparsity-inducing (SI) norms (cardinality and ), which are used in two different ways (as a constraint or a penalty). All have the form

| (1.2) |

with and detailed in Table 1. Note that if we set in the constrained or in the penalized versions, the sparsity-inducing functions stop having any effect111In the penalized formulations this can be seen from the inequality . and we recover the classical and robust PCA (1.1). Choosing , will have the effect of directly enforcing or indirectly encouraging sparsity in the solution .

| # | Variance | SI norm | SI norm usage | ||

|---|---|---|---|---|---|

| 1 | constraint | ||||

| \hdashline 2 | constraint | ||||

| \hdashline 3 | constraint | ||||

| \hdashline 4 | constraint | ||||

| \hdashline5 | penalty | ||||

| \hdashline 6 | penalty | ||||

| \hdashline 7 | penalty | ||||

| \hdashline8 | penalty |

All 4 SPCA formulations of Table 1 involving variance were previously studied in the literature and are very popular. One of the earliest work, the well-known SCoTLASS (Simplified Component Technique-LASSO) method in Jolliffe et al. (2003), was for the penalized formulation. Although the original method is quite slow, faster numerical algorithms using projected gradient (Trendafilov and Jolliffe, 2006) and penalized matrix composition (Witten et al., 2009) was developed for SCoTLASS. The later one is an application of the conditional gradient algorithm as noted in (Luss and Teboulle, 2013). Qi et al. (2013) considered a generalization of the problem with penalty, in which a mixed norm of and penalties is used. d’Aspremont et al. (2007) solved a series of convex relaxations, based on semidefinite programming of the constrained variance problem, while d’Aspremont et al. (2008) considered the penalized and constrained formulations. While, Journée et al. (2010) studied the and penalized versions, Luss and Teboulle (2013) looked at all four. Enforcing sparsity directly with an constrained formulation is NP-hard and it can’t be approximated by an efficient approximation algorithm as shown in Magdon-Ismail (2017). Therefore, there are only a few works that attempt to solve this problem exactly; one recent notable study is Berk and Bertsimas (2019), which developed a branch and bound algorithm for this problem. In addition, Beck and Vaisbourd (2016) discussed a hierarchy of optimality conditions for this problem.

The constrained variance formulation was first proposed by Meng et al. (2012). To the best of our knowledge, the remaining three variance formulations were not considered in the literature before. In particular, the constrained variance formulation is new—and is perhaps preferable as it directly constraints the cardinality of the loading vector without using any proxies.

1.2 Reformulation and alternating maximization (AM) method

In all 8 formulations we introduce an additional (dummy) variable , which allows us to propose a generic alternating maximization method for solving them: i) for a fixed loading vector, find the best dummy variable (one maximizing the objective), then ii) fix the dummy variable and find the best loading vector; repeat steps i) and ii). This and the resulting algorithms are described in detail in Section 2. The generic AM method is not limited to our choice of SPCA formulations. Indeed, it is applicable, for instance, if instead of measuring the variance using either the or the norm, we use any other norm. One critical feature shared by the formulations in Table 1 is that steps i) and ii) of the AM method can be performed efficiently, in closed form, with the main computational burden in each step being a matrix-vector multiplication ( in step i) and in step ii)). Our method produces a sequence of loading vectors , with monotonically increasing values .

Our approach of introducing a dummy variable and using AM is similar to that of Journée et al. (2010), where it is done implicitly, but mainly to that of Richtárik (2011), where it is fully explicit, albeit used for different purposes.

Besides providing a conceptual unification for solving all 8 formulations using a single algorithm (AM), the main theoretical result of this paper is establishing that, perhaps surprisingly, in all 8 cases, the AM method is equivalent to the GPower method (Journée et al., 2010) applied to a certain derived objective function, with iterates being either the loading vectors or the dummy variables, depending on the formulation. This result is stated and proved in Section 3.

1.3 Parallelism

Besides giving a new unifying framework and a generic algorithm for solving a number of SPCA formulations, 5 of which were previously proposed in the literature and 3 not, our further contribution is in providing efficient strategies for parallelizing AM at two different levels: i) running AM in parallel from multiple starting points in order to obtain a solution explaining more variance and ii) speeding up the linear algebra involved. This is described in detail in Section 4.

Moreover, we provide parallel open-source code222Open source code with efficient implementations of the algorithms developed in this paper is published here: https://github.com/optml/24am. implementing these parallelization strategies, for each of our 8 formulations, on 3 computing architectures: i) multi-core machine, ii) GPU-enabled computer, and iii) computer cluster. We also provide a serial code; however, as nearly all modern computers are multi-core, the serial implementation only serves the purpose of a benchmark against which once can measure parallelization speedup. Hence, we provide a total of parallel sparse PCA codes based on AM. Numerical experiments with our multi-core, GPU and cluster codes are performed in Section 5.

Parallelism in our codes serves several purposes:

-

1.

Speeding up computations. As described above, the AM method computes a matrix-vector multiplication at every iteration; this can be parallelized. We find that our GPU implementations are faster than our multi-core implementations, which are, in turn, considerably faster than the benchmark single-core codes.

-

2.

Obtaining solutions explaining more variance. In some applications, such as in the computation of RIP constants for compressed sensing (Bah and Tanner, 2010), it is critical that a PC is computed with as high explained variance as possible. The output of our 8 subroutines depends on the starting point used; it only finds stationary solutions. Running them repeatedly from different starting points and keeping the solution with the largest objective value results in a PC explaining more variance. There are several ways in which this can be done, we implement 4 (NAI = “naive”, SFA = “start-from-all”, BAT = “batches” and OTF = “on-the-fly”); details are given in Section 4. A naive (NAI) approach is to do this sequentially; a different possibility is to run the method from several or all starting points in parallel (BAT, SFA), possibly asynchronously (OTF). This way at each iteration we need to perform a matrix-matrix multiplication which, when computed in parallel, is performed significantly faster compared to doing the corresponding number of parallel matrix-vector multiplications, one after another.

-

3.

Dealing with big data problems. If speed matters, for problems of small enough size we recommend using a GPU, if available. Since GPUs have stricter memory limitations than multi-core workstations (a typical GPU has 6GB RAM, a multi-core machine could have 20GB RAM), one may need to use a high-memory multi-core workstation if the problem size exceeds the GPU limit. However, for large enough (=big data) problems, one will need to use a cluster. Our cluster codes partition , store parts of it on different nodes, and do the computations in a distributed way.

Notation. By and we denote column vectors in and , respectively. The coordinates of a vector are denoted by subscripts (eg., ) while iterates are denoted by superscripts in brackets (eg., , , ). We reserve the letter for the iteration counter. By we refer to the cardinality (number of nonzero loadings) of vector . The and norms are defined by , and , respectively. For a scalar , we let and by we denote the sign of .

2 Alternating Maximization (AM) Method

As outlined in the previous section, we will solve (1.2) by introducing a dummy variable into each of the 8 formulations and apply an AM method to the reformulation. First, notice that for any pair of conjugate norms and , we have, by definition,

| (2.3) |

In particular, and .

Now, let for the variance formulations and for the variance formulations. Further, let be the function obtained from after replacing with (resp. with ). Then, in view of the above, (1.2) takes on the equivalent form

| (2.4) |

That is, the 8 problems from Table 1 can be reformulated into the form (2.4); the details can be found in Table 2.

| # | |||

|---|---|---|---|

| 1 | |||

| \hdashline 2 | |||

| \hdashline 3 | |||

| \hdashline 4 | |||

| \hdashline 5 | |||

| \hdashline 6 | |||

| \hdashline 7 | |||

| \hdashline 8 |

2.1 Solving the subproblems

All 8 problems of Table 2 enjoy the property that both of the steps (subproblems) of Algorithm 1 can be computed in closed form. In particular, each of these subproblems is of one of the 6 forms listed in Table 3.

| Subproblem # | ||||

|---|---|---|---|---|

| S1 | or | or | ||

| \hdashlineS2 | ||||

| \hdashlineS3 | ||||

| \hdashlineS4 | ||||

| \hdashlineS5 | ||||

| \hdashlineS6 |

The proofs of these elementary results, many of which are of folklore nature, can be found, for instance, in (Luss and Teboulle, 2013) (and partially in (Journée et al., 2010)). The columns of Table 3, from left to right, correspond to the objective function, feasible region, maximizer (optimal solution) and maximum (optimal objective value). The first result will be used both with and , the second result with and the remaining four results with .

Table 3 is brief at the cost of referring to a number of operators (, and ), which we will now define. For a given vector and integer , by we denote the vector obtained from by retaining only the largest components of in absolute value, with the remaining ones replaced by zero. For instance, for and we have . For , we define operators and element-wise for as follows:

| (2.5) |

| (2.6) |

Furthermore, we let

which is the solution of the one-dimensional dual of the optimization problem in line 4 of Table 3.

2.2 The AM method for all 8 SPCA formulations

Combining Algorithm 1 with the subproblem solutions given in Table 3, the AM method for all our 8 SPCA formulations can be written down concisely; see Algorithm 2.

Note that in the methods described in Algorithm 2 it is (in theory) not necessary to normalize the vector (resp. , , and ) when computing since clearly the iterate , which depends on , is invariant under positive scalings of , and is being either normalized, or is computed using function. We have to remember, however, to normalize the output. When the matrix is not well conditioned, it is still recommended to normalize vectors , , , and ) to eliminate the effect of limited floating point precision.

The method is terminated when a maximum number of iterations is reached or when

whichever happens sooner.

3 Equivalence of AM and GPower

GPower (generalized power method) (Journée et al., 2010) is a simple algorithm for maximizing a convex function on a compact set , which works via a “linearize and maximize” strategy. If by we denote an arbitrary subgradient of at , then GPower performs the following iteration:

| (3.7) |

The following theorem, our main result, gives a nontrivial insight into the relationship of AM and GPower, when the former is applied to solving any of the 8 SPCA formulations considered, and GPower is applied to a derived problem, as described by the theorem.

Theorem 1 (AM = GPower)

The AM and GPower methods are equivalent in the following sense:

- 1.

-

2.

For the 4 penalized sparse PCA formulations of Table 1, the iterates of the AM method applied to the corresponding reformulation of Table 2 are identical to the iterates of the GPower method as applied to the problem of maximizing the convex function

on , started from a feasible (we assume that , or are chosen such that ).

Proof

Recall that we wish to solve the problem

We will now prove the equivalence for all 8 choices of given in Tables 1 and 2. In the proofs we will also refer to the closed form solutions of the subproblem (S1)–(S6), as detailed in Table 3.

Consider first the constrained formulations: and . By induction assume that the -th -iterate () of AM is identical to the -th iterate of GPower (for this is enforced by the assumption that GPower is started from ). By considering all 4 formulations individually, we will show that produced by AM and GPower are also identical.

-

Formulation 1: Here we have

First, note that

the gradient of which is given by

(3.8) Given , in the AM method we have

(3.9) One iteration of GPower started from will thus produce the iterate

Observe that this is precisely how is computed in the AM method.

-

Formulation 2: Here we have

First, note that

the subgradient of which is given by

(3.10) Given , in the AM method we have

(3.11) One iteration of GPower started from will thus produce the iterate

Observe that this is precisely how is computed in the AM method.

-

Formulation 3: Here we have

First, note that

the gradient of which is given by

(3.12) Given , in the AM method we have

(3.13) One iteration of GPower started from will thus produce the iterate

Observe that this is precisely how is computed in the AM method.

-

Formulation 4: Here we have

First, note that

the subgradient of which is given by

(3.14) Given , in the AM method we have

(3.15) One iteration of GPower started from will thus produce the iterate

Observe that this is precisely how is computed in the AM method.

Consider now the penalized formulations: and . By induction assume that the -th -iterate () of AM is identical to the -th iterate of GPower (for this is enforced by the assumption that GPower is started from ). By considering all 4 formulations individually, we will show that produced by AM and GPower are also identical. Let , i.e., the -th column of is .

-

Formulation 5: Here we have

First, note that

the subgradient of which is given by

(3.16) Given , in the AM method we have

(3.17) One iteration of GPower started from will thus produce the iterate

Observe that this is precisely how is computed in the AM method.

-

Formulation 6: Here we have

First, note that

the subgradient of which is given by

(3.18) Given , in the AM method we have

(3.19) One iteration of GPower started from will thus produce the iterate

Observe that this is precisely how is computed in the AM method.

-

Formulation 7: Here we have

Note that the functions are linear and that, by definition, . Moreover, note that the gradient of at is equal to . Hence, if is any vector that maximizes over , then is a subgradient of at . Note that this is precisely how is defined in the AM method: . Hence, is a subgradient of at and one iteration of GPower started from will produce the iterate

Observe that this is precisely how is computed in the AM method.

-

Formulation 8: Here we have

Note that the functions are linear and that, by definition, . Moreover, note that the gradient of at is equal to . Hence, if is any vector that maximizes over , then is a subgradient of at . Note that this is precisely how is defined in the AM method: . Hence, is a subgradient of at and one iteration of GPower started from will produce the iterate

Observe that this is precisely how is computed in the AM method.

4 Embedding AM within a Parallel Scheme

In this section we describe several approaches for embedding Algorithm 2 (AM) within a parallel scheme for solving identical SPCA problems, started from a number of starting points, . This is done in order to obtain a loading vector explaining more variance and will be discussed in more detail in Section 4.1.

As we will see, it may not necessarily be most efficient to solve all problems simultaneously. Instead, we consider a class of parallelization schemes where we divide the problems into “batches” of problems each, and solve each batch of problems simultaneously. In this setting at each iteration we need to perform identical operations in parallel, notably matrix-vector multiplications and . It is useful to view the sequence of matrix-vector products as a single matrix-matrix product, e.g., in the first case, and use optimized libraries for parallelization. This simple trick leads to considerable speedups when compared to other approaches. We use similar ideas for the parallel evaluation of the operators. Note that even in the case, i.e, if we wish to run SPCA from a single starting point only, there is scope for parallelization of the matrix-vector products and function evaluations. Hence, parallelization in our method serves two purposes:

-

1.

to obtain solutions explaining more variance by solving the problem from several starting points (we choose ),

-

2.

to speed up computations by parallelizing the linear algebra involved (this applies to both and cases).

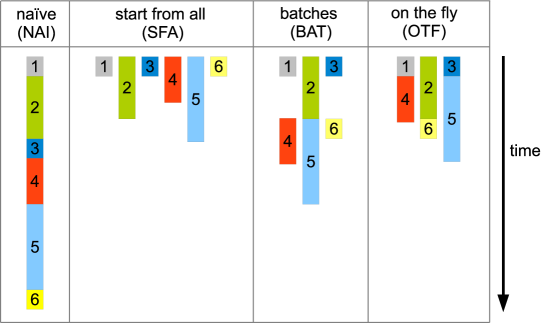

In particular, in this section we describe 4 parallelization approaches:

-

•

NAI = “naive” (),

-

•

SFA = “start-from-all” (),

-

•

BAT = “batches” ()

-

•

OTF = “on-the-fly” (BAT improved by a dynamic replacement strategy to reduce idle time).

The working of these 4 approaches is illustrated in Figure 1 in a situation with . In what follows we describe the methods informally, in a narrative style, with a suitable choice of numerical experiments illustrating the differences between the ideas.

4.1 The hunt for more explained variance

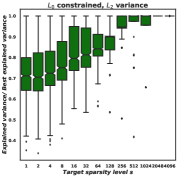

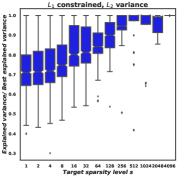

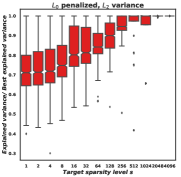

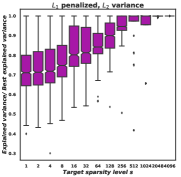

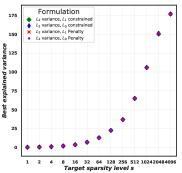

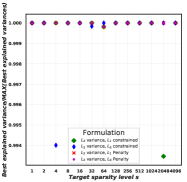

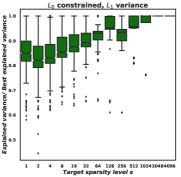

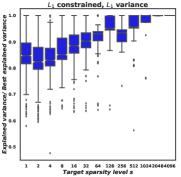

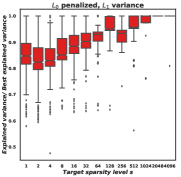

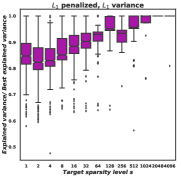

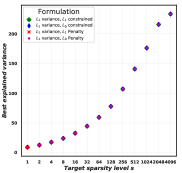

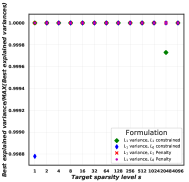

As shown by Journée et al. (2010) and Luss and Teboulle (2013) for GPower, and due to our equivalence theorem (Theorem 1), we know that Algorithm 2 (AM) is only able to converge to a stationary point rather than a global solution. Moreover, quality of the solution will depend on the starting point (SP) used. When the algorithm is run just once, the quality of the obtained solution, in terms of the objective value (or explained variance), can be poor. Hence, if the amount of explained variance is important, it will be useful to run the method repeatedly from a number of different SPs. We considered “AT&T Database of Faces” data set333https://www.kaggle.com/kasikrit/att-database-of-faces/data, which contains 400 images, and the size of each image is 92x112 pixels. After reshaping the data set, the data matrix has 400 rows and 10304 columns. We normalized each row of the matrix, and centralized each column of the normalized matrix and solved the corresponding SPCA problems described in Table 2 with . For each we run AM from randomly generated SPs with and . It is noteworthy to mention that the explained variance for the cases with and variance are considered as and , respectively. The results are given in Figures 2 and 3. In the first two rows of Figures 2 and 3, the vertical axis corresponds to the amount of explained variance of a particular solution compared to the best solution found with respect to the target sparsity level (horizontal axis) with the above setting. For the cases with constrained, we considered to be updated for some predefined iterations (let’s say 10), and would be fixed afterwards in order to have a stable . The same trick can be applied to the cases with penalty (cases 5-8). That is, we control sparsity level by for some predefined iterations; to do so, in order to reach the sparsity level of , first, we sort the vector “” based on its squared and absolute value for the operators and , respectively. Then, we set to be the element of the new sorted vector, and by doing so we can guarantee the sparsity level of the output vector to be for the predefined iterations, and we make fixed afterwards. Overall, it means that there is no need to tune in the aforementioned cases. In the third rows of the Figures 2 and 3, the left ones show the best explained variance for the formulations with and variances among 1000 runs; and the right ones highlight that the best explained variance for all formulations are close to each other.

Clearly, for small it is easy to obtain a bad solution if we run the method only a few times; this effect is milder for large but may be substantial nevertheless in real life problems. Hence, especially when is small, it is necessary to employ a globalization strategy such as rerunning AM from a number of different starting points. This experiment illustrates that the simple strategy of running the method from a number of randomly generated starting points can be effective in finding solutions with more explained variance. A “naive” (NAI) approach would be to do this sequentially: solve the problem with one starting point first before solving it for another starting point.

4.2 Economies of scale

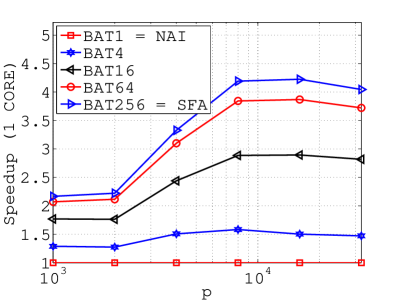

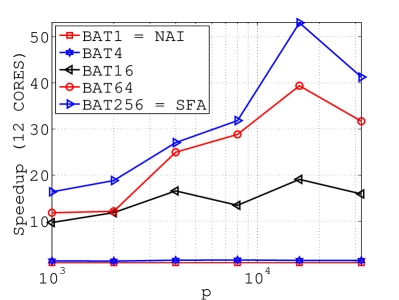

Running AM in parallel, started from a number of SPs, increases the utilization of computer resources, especially on parallel architectures. In order to demonstrate this, we generated 6 data matrices with and run the AM method for the penalized variance SPCA formulation with SPs (and ). By BAT we denote the approach with batches of size . Hence, SFA = BAT and NAI = BAT. Besides these two basic choices, we look at BAT, BAT and BAT as well. The results can be found in Figure 4.

Different problem sizes appear on the horizontal axis; on the vertical axis we plot the speedup obtained by applying a particular batching strategy compared to NAI. Note that even on a single-core computer (LEFT plot) we benefit from running the methods in parallel (“economies of scale”) rather than running them one after another. Indeed, we can obtain a speedup with BAT across the whole range of problem sizes, and speedup with SFA for large enough . With cores (RIGHT plot) the effect is much more dramatic: the speedup for BAT is consistently in the range, and can even reach for SFA.

4.3 Dynamic replacement

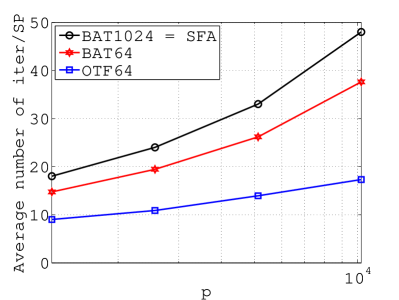

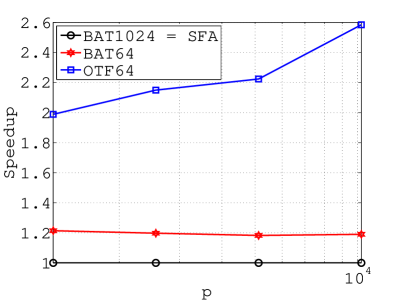

It often happens, especially when batch size is large, that some problems within a batch converge sooner than others. The vanilla BAT approach described above does nothing about it, and continues through matrix-matrix multiplies, updating the already converged iterates, until the last problem in the batch converges. A minor but not negligible speedup is possible by employing an “on-the-fly” (OTF) dynamic replacement technique, where whenever a certain problem converges, it is replaced by a new one. Hence, no predefined batches exist—OTF can be viewed as a greedy list scheduling heuristic. We used starting points and compare SFA with BAT and OTF–the dynamic replacement variant of BAT.

Looking at the LEFT plot in Figure 5, we see that the average number of iterations per starting point is much smaller for OTF. This results in speedup of more than when compared with SFA (RIGHT plot). Notably, SFA is slower than both BAT64 and OTF64, which shows that it may not be optimal to choose .

5 Multi-core Processors, GPUs and Clusters

Accompanying this paper is the open source software package “24am”444 https://github.com/optml/24am. implementing parallelization strategies described in Section 4, all with Algorithm 2 (AM) used as the underlying solution method, with the option of using any of the 8 optimization formulations of SPCA described in Table 1. The name 24am comes from the fact that we implement the solver for 3 different parallel architectures: multi-core processors, GPUs and computer clusters, leading to methods based on AM.

In the rest of this section we first perform several numerical experiments illustrating the speedups obtained by parallelization on these three computing architectures. We then conclude with a real-life numerical example (large text corpora) and a few implementation remarks.

5.1 Multi-core speedup

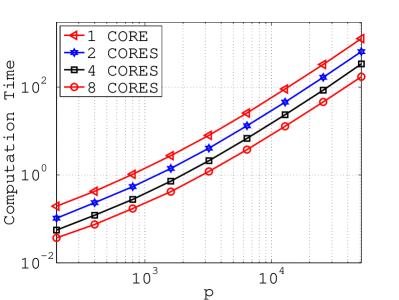

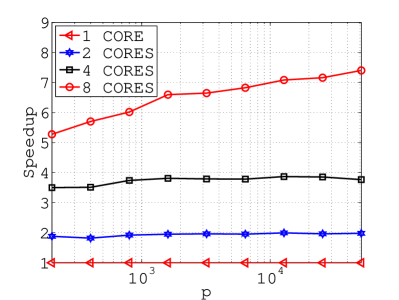

Here we solve 9 random constrained variance SPCA instances of sizes , , , with SPs each, on a machine using and cores; see Figure 6.

The plot on the LEFT shows the total computational time; the plot on the RIGHT shows the speedup of multi-core codes compared to the single-core code. Note that the speedup is consistently close to the number of cores for the 2 and 4-core setups across all problem sizes, and is growing with from to about in the -core setup.

5.2 GPU speedup

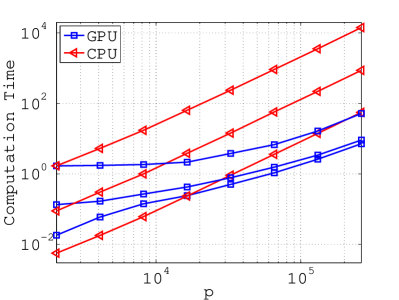

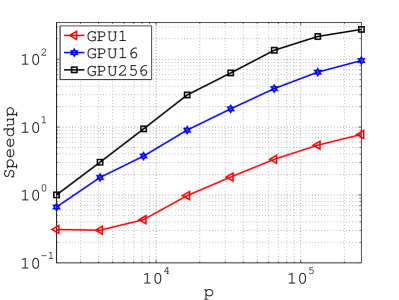

Here we solve 8 random penalized variance SPCA instances with varying roughly between and , and . We solved all formulations with SPs on a single-core CPU and a GPU; the results are shown in Figure 7.

The plot on the LEFT shows the total computational time. The red lines with triangle markers correspond to the single-core setup, the “higher” the line, the more starting points were used. The blue lines with square markers correspond to our GPU codes. While the runtime increases linearly with problem size for the single-core codes, it grows slowly for the GPU codes. Note that the GPU code may actually be slower for small problem sizes. Looking at the RIGHT plot, we see that the GPU code is capable of a - speedup; this happens for large problem sizes and SPs. The speedup can reach for SPs as well.

5.3 Cluster code

In this experiment we solved several penalized variance SPCA problems with a fully dense matrix ; the results are in Table 4. We focus our discussion on the largest of the problems only (last three lines of the table), one with and . We used a cluster of 800 CPUs; storage of the data matrix required 357.6 GB of memory. The matrix was first loaded from files to memory; this process took seconds. Subsequently, the loaded data was distributed to CPUs where needed, which took additional seconds. Finally we run the AM method with , and starting points and measured the average time of a single iteration; the results are , and seconds, respectively. When using a single starting point, the method would converge in about a minute. The column of Table 4 depicts the time it takes for the solver to perform iterations. We treated the problem directly, without using any safe feature elimination techniques (Zhang and El Ghaoui, 2011). Such preprocessing could, however, be able to expand the reach of our cluster code to even larger problem sizes.

| memory | # CPUs | GRID | SP | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 14.9 GB | 20 | 1 | 42.68 | 0.86 | 0.56 | 2.06 | 8.48 | ||

| 14.9 GB | 20 | 32 | - | - | 4.60 | 18.89 | 87.84 | ||

| 14.9 GB | 20 | 64 | - | - | 10.47 | 37.88 | 166.60 | ||

| \hdashline | 17.8 GB | 40 | 1 | 26.89 | 86.33 | 0.78 | 3.15 | 9.96 | |

| 17.8 GB | 40 | 32 | - | - | 7.39 | 27.72 | 125.14 | ||

| 17.8 GB | 40 | 64 | - | - | 13.19 | 58.36 | 201.51 | ||

| \hdashline | 44.7 GB | 100 | 1 | 49.22 | 104.26 | 0.45 | 2.44 | 11.62 | |

| 44.7 GB | 100 | 32 | - | - | 6.37 | 29.72 | 115.73 | ||

| 44.7 GB | 100 | 64 | - | - | 14.14 | 52.64 | 219.8 | ||

| \hdashline | 178.8 GB | 400 | 1 | 129.69 | 611.69 | 1.24 | 5.12 | 31.46 | |

| 178.8 GB | 400 | 32 | - | - | 17.50 | 61.36 | 255.80 | ||

| 178.8 GB | 400 | 64 | - | - | 31.36 | 141.61 | 525.08 | ||

| \hdashline | 357.6 GB | 800 | 1 | 92.12 | 713.45 | 4.14 | 15.82 | 95.51 | |

| 357.6 GB | 800 | 32 | - | - | 51.11 | 324.26 | 619.45 | ||

| 357.6 GB | 800 | 64 | - | - | 134.89 | 690.06 | - |

| NYT 1st PC | NYT 2nd PC | NYT 3rd PC | NYT 4th PC | NYT 5th PC |

|---|---|---|---|---|

| game | companies | campaign | children | attack |

| \hdashlineplay | company | president | program | government |

| \hdashlineplayer | million | al gore | school | official |

| \hdashlineseason | percent | bush | student | US |

| \hdashlineteam | stock | george bush | teacher | united states |

| PubMed 1st PC | PubMed PC | PubMed PC | PubMed 4th PC | PubMed 5th PC |

|---|---|---|---|---|

| disease | cell | activity | cancer | age |

| \hdashlinelevel | effect | concentration | malignant | child |

| \hdashlinepatient | expression | control | mice | children |

| \hdashlinetherapy | human | rat | primary | parent |

| \hdashlinetreatment | protein | receptor | tumor | year |

5.4 Large text corpora

In the first experiment we tested the AM method with constrained variance formulation (with ) on two medium-size data sets from the Machine Learning Repository555http://archive.ics.uci.edu/ml/datasets/Bag+of+Words: news articles appeared in New York Times and abstracts of articles published in PubMed. Each data set is formatted as a matrix , where the rows of correspond to news articles in the NYTimes data set and to abstracts in PubMed, and the columns correspond to words. The number of appearances of word in article or abstract is the -th entry of ; the matrices are hence clearly sparse. The NYTimes data set has 300,000 articles, 102,660 words, and approximately 70 million nonzero entries. The PubMed data set contains 8.2 million articles, 141,043 words, and approximately 484 million nonzeroes. The matrices can be stored in 0.778 GB and 5.42 GB memory space, respectively. We have customized the AM method to exploit sparsity as much as possible. In Table 5 we present the first 5 sparse principal components (5 words each). Clearly, the first PC for NYT is about sports, the second about business, the third about elections, the fourth about education and the fifth about United States. Similar interpretations can be given to the PubMed PCs. We also tested the AM method with other formulations reported in Table 2 for the NYTimes data set. Table 8 illustrates the first 5 sparse principal components regarding the formulations with variance666Note that the different colors in tables 8 and 9 are corresponding to the formulations with the same color in Table 2.. We also provided the nonzero values of sparse principal components corresponding to each word, and sort each principal component based on the values for each word. Furthermore, Table 9 presents the first 5 sparse principal components regarding the formulations with variance. For each formulation, we ran AM method by starting from random starting points with and . Moreover, Tables 6 and 7 show the best variances (among 20 runs) with respect to the first 5 sparse PCs for the NYTimes data set for the formulation with and variances, respectively.

| NYT 1st PC | NYT 2nd PC | NYT 3rd PC | NYT 4th PC | NYT 5th PC |

|---|---|---|---|---|

| 2000778.58 | 1912905.67 | 1560637.32 | 1429685.36 | 1193802.56 |

| \hdashline 2000778.59 | 1912905.66 | 1560637.45 | 1429685.37 | 1193803.32 |

| \hdashline2000778.60 | 1912906.01 | 1560637.21 | 1429685.37 | 1193838.99 |

| \hdashline 1912905.56 | 2000778.59 | 1560636.59 | 1429685.34 | 1193792.20 |

| NYT 1st PC | NYT 2nd PC | NYT 3rd PC | NYT 4th PC | NYT 5th PC |

|---|---|---|---|---|

| 486843.78 | 462445.23 | 386907.51 | 320581.40 | 315784.42 |

| \hdashline486843.78 | 462445.23 | 384622.40 | 336912.52 | 347835.82 |

| \hdashline486843.78 | 462391.75 | 387579.36 | 309628.15 | 295577.97 |

| \hdashline486843.78 | 462445.23 | 387901.14 | 319704.28 | 306050.47 |

| NYT 1st PC | NYT 2nd PC | NYT 3rd PC | NYT 4th PC | NYT 5th PC |

|---|---|---|---|---|

| team | percent | al gore | school | official |

| (0.6118) | (0.6768) | (0.6115) | (0.8143) | (0.7183) |

| \hdashline game | company | george bush | student | government |

| (0.4499) | (0.5117) | (0.4710) | (0.5139) | (0.4570) |

| \hdashline season | million | bush | program | US |

| (0.4368) | (0.3497) | (0.4539) | (0.1616) | (0.3208) |

| \hdashline player | companies | campaign | teacher | united states |

| (0.3833) | (0.2868) | (0.3284) | (0.1549) | (0.3064) |

| \hdashline play | stock | president | children | attack |

| (0.2921) | (0.2746) | (0.3002) | (0.1499) | (0.2796) |

| team | percent | al gore | school | official |

| (0.6119) | (0.6768) | (0.6123) | (0.8144) | (0.7185) |

| \hdashline game | company | george bush | student | government |

| (0.4498) | (0.5117) | (0.4728) | (0.5138) | (0.4567) |

| \hdashline season | million | bush | program | US |

| (0.4369) | (0.3497) | (0.4509) | (0.1617) | (0.3208) |

| \hdashline player | companies | campaign | teacher | united states |

| (0.3833) | (0.2868) | (0.3285) | (0.1549) | (0.3064) |

| \hdashline play | stock | president | children | attack |

| (0.2920) | (0.2746) | (0.3001) | (0.1499) | (0.2796) |

| team | percent | al gore | school | official |

| (0.6119) | (0.6771) | (0.6115) | (0.8144) | (0.7184) |

| \hdashline game | company | george bush | student | government |

| (0.4498) | (0.5114) | (0.4710) | (0.5138) | (0.4567) |

| \hdashline season | million | bush | program | US |

| (0.4368) | (0.3495) | (0.4540) | (0.1616) | (0.3209) |

| \hdashline player | companies | campaign | teacher | united states |

| (0.3833) | (0.2867) | (0.3284) | (0.1549) | (0.3065) |

| \hdashline play | stock | president | children | attack |

| (0.2920) | (0.2746) | (0.3003) | (0.1500) | (0.2796) |

| percent | team | al gore | school | official |

| (0.6767) | (0.6119) | (0.6114) | (0.8144) | (0.7183) |

| \hdashlinecompany | game | george bush | student | government |

| (0.5118) | (0.4498) | (0.4708) | (0.5139) | (0.4571) |

| \hdashlinemillion | season | bush | program | US |

| (0.3497) | (0.4368) | (0.4543) | (0.1615) | (0.3208) |

| \hdashlinecompanies | player | campaign | teacher | united states |

| (0.2868) | (0.3833) | (0.3284) | (0.1549) | (0.3064) |

| \hdashline stock | play | president | children | attack |

| (0.2746) | (0.2920) | (0.3003) | (0.1500) | (0.2796) |

| NYT 1st PC | NYT 2nd PC | NYT 3rd PC | NYT 4th PC | NYT 5th PC |

|---|---|---|---|---|

| percent | team | official | school | united states |

| (0.6047) | (0.5557) | (0.5846) | (0.6433) | (0.4945) |

| \hdashline company | game | government | book | country |

| (0.4915) | (0.4780) | (0.4789) | (0.4421) | (0.4631) |

| \hdashline million | season | bush | al gore | attack |

| (0.4900) | (0.4499) | (0.4446) | (0.3809) | (0.4353) |

| \hdashline companies | player | president | student | US |

| (0.2926) | (0.3615) | (0.3975) | (0.36535) | (0.4308) |

| \hdashline market | play | george bush | children | leader |

| (0.2585) | (0.3598) | (0.2701) | (0.3348) | (0.4072) |

| percent | team | official | campaign | school |

| (0.6047) | (0.5557) | (0.5936) | (0.5413) | (0.6643) |

| \hdashline company | game | government | george bush | women |

| (0.4915) | (0.4780) | (0.4955) | (0.4812) | (0.4544) |

| \hdashline million | season | bush | al gore | student |

| (0.4900) | (0.4499) | (0.4511) | (0.4702) | (0.3919) |

| \hdashline companies | player | president | election | children |

| (0.2926) | (0.3615) | (0.3699) | (0.3905) | (0.3578) |

| \hdashline market | play | political | palestinian | tax |

| (0.2585) | (0.3598) | (0.2481) | (0.3189) | (0.2654) |

| percent | team | official | school | billion |

| (0.6047) | (0.5741) | (0.5487) | (0.5814) | (0.5698) |

| \hdashline company | game | government | group | business |

| (0.4915) | (0.4711) | (0.4936) | (0.5362) | (0.5134) |

| \hdashline million | season | bush | program | fund |

| (0.4900) | (0.4432) | (0.4408) | (0.3838) | (0.4105) |

| \hdashline companies | player | president | george bush | money |

| (0.2926) | (0.3562) | (0.4100) | (0.3473) | (0.4093) |

| \hdashline market | play | group | student | stock |

| (0.2585) | (0.3534) | (0.2775) | (0.3261) | (0.2747) |

| percent | team | official | school | group |

| (0.6047) | (0.5557) | (0.5856) | (0.6527) | (0.5768) |

| \hdashline company | game | government | program | united states |

| (0.4915) | (0.4780) | (0.4788) | (0.4523) | (0.4750) |

| \hdashline million | season | bush | student | US |

| (0.4900) | (0.4499) | (0.4463) | (0.3628) | (0.3903) |

| \hdashline companies | player | president | family | american |

| (0.2926) | (0.3615) | (0.3951) | (0.3458) | (0.3861) |

| \hdashline market | play | al gore | children | attack |

| (0.2585) | (0.3598) | (0.2690) | (0.3435) | (0.3742) |

5.5 Implementation details

For single and multi-core architectures we developed our codes using the CBLAS interface. In particular, we use both the GSL BLAS and the Intel MKL777http://software.intel.com/en-us/articles/intel-mkl/ implementations (single-core) and the GotoBLAS2888https://www.tacc.utexas.edu/research-development/tacc-software/gotoblas2 and Intel MKL implementations (multi-core). Parallelization in the multi-core case is performed by the OpenMP interface. When comparing the performance of single-core and multi-core architectures, we use Intel MKL library for both serial and parallel versions of the same algorithm for consistency. Nevertheless, in our experience, GotoBLAS2 implementation of these algorithms are faster than the Intel MKL implementation. We use CuBLAS999http://developer.nvidia.com/cublas, version 4.0, on GPU (and make use of Thrust whenever possible for operations such as sorting, memory arrangements and data allocation on GPU). For comparisons between single-core and GPU architectures, we use the GSL BLAS implementation on the single-core. On a cluster, linear algebra is done with Intel MKL’s PBLAS, while communication between nodes is via MPI.

6 Conclusion

We propose a unifying framework for solving 8 SPCA formulations in which all have the same form and are solved by the same algorithm: the alternating maximization (AM) method. We observed that AM is in all cases equivalent to the GPower method applied to a suitable convex function. Five of these formulations were previously studied in the literature and three were not; notably the constrained (robust) variance seems to be new. For each of these formulations we have written 4 efficient codes—one serial and three parallel—aimed at single-core, multi-core and GPU workstations and a cluster. All these codes are enabled with efficient parallel implementations of a multiple-starting-point globalization strategy which aims to find PCs explaining more variance; with speedup per starting point achieving up to two orders of magnitude. The most efficient of these implementations is “on-the-fly”. We demonstrated that our cluster code is able to solve a very large problem with a 357 GB fully dense data matrix.

References

- Amini and Wainwright (2009) Amini AA, Wainwright MJ (2009) High-dimensional analysis of semidefinite relaxations for sparse principal components. Annals of Statistics 37:2877–2921

- Aravkin and Becker (2016) Aravkin A, Becker S (2016) Dual smoothing and value function techniques for variational matrix decomposition. Handbook of Robust Low-Rank and Sparse Matrix Decomposition: Applications in Image and Video Processing

- Bah and Tanner (2010) Bah B, Tanner J (2010) Improved bounds on restricted isometry constants for gaussian matrices. SIAM Journal on Matrix Analysis and Applications 31:2882–2898

- Beck and Vaisbourd (2016) Beck A, Vaisbourd Y (2016) The sparse principal component analysis problem: optimality conditions and algorithms. Journal of Optimization Theory and Algorithms 170:119–143

- Berk and Bertsimas (2019) Berk L, Bertsimas D (2019) Certifiably optimal sparse principal component analysis. Mathematical Programming Computations 11:381–420

- Bouwmans et al. (2017) Bouwmans T, Sobral A, Javed S, Jung SK, Zahzah EH (2017) Decomposition into low-rank plus additive matrices for background/foreground separation: A review for a comparative evaluation with a large-scale dataset. Computer Science Review 23:1–71

- Candès et al. (2011) Candès EJ, Li X, Ma Y, Wright J (2011) Robust principal component analysis? Journal of the ACM (JACM) 58:Article 11

- Croux et al. (2013) Croux C, Filzmoser P, Fritz H (2013) Robust sparse principal component analysis. Technometrics 55:202–214

- d’Aspremont et al. (2007) d’Aspremont A, El Ghaoui L, Jordan MI, Lanckriet G (2007) A direct formulation for sparse PCA using semidefinite programming. SIAM Review 49:434–448

- d’Aspremont et al. (2008) d’Aspremont A, Bach F, El Ghaoui L (2008) Optimal solutions for sparse principal component analysis. Journal of Machine Learning Research 9:1269–1294

- Hastie et al. (2015) Hastie T, Tibshirani R, Wainwright M (2015) Statistical Learning with Sparsity: The Lasso and Generalizations. Chapman and Hall/CRC

- Hubert et al. (2016) Hubert M, Reynkens T, Schmitt E, Verdonck T (2016) Sparse PCA for high-dimensional data with outliers. Technometrics 58:424–434

- Jollife (1986) Jollife I (1986) Principal component analysis. Springer Verlag, NY

- Jolliffe et al. (2003) Jolliffe IT, Trendafilov NT, Uddin M (2003) A modified principal component technique based on the LASSO. Journal of Computational and Graphical Statistics 12(3):531–547

- Journée et al. (2010) Journée M, Nesterov Y, Richtárik P, Sepulchre R (2010) Generalized power method for sparse principal component analysis. Journal of Machine Learning Research 11:517–553

- Kwak (2008) Kwak N (2008) Principal component analysis based on norm maximization. IEEE Transactions on Pattern Analysis and Machine Intelligence 30:1672–1680

- Lei and Vu (2015) Lei J, Vu VQ (2015) Sparsity and agnostic inference in sparse pca. The Annals of Statistics 43:299–322

- Lu and Zhang (2012) Lu Z, Zhang Y (2012) An augmented Lagrangian approach for sparse principal component analysis. Mathematical Programming, Series A 135:149–193, DOI DOI:10.1007/s10107-011-0452-4

- Luss and Teboulle (2013) Luss R, Teboulle M (2013) Conditional gradient algorithms for rank-one matrix approximations with a sparsity constraint. SIAM Review 55:65–98

- Mackey (2008) Mackey L (2008) Deflation methods for sparse PCA. In: Advances in Neural Information Processing Systems (NIPS), vol 21, pp 1017–1024

- Magdon-Ismail (2017) Magdon-Ismail M (2017) Np-hardness and inapproximability of sparse PCA. Information Processing Letters 126:35–38

- Meng et al. (2012) Meng D, Zhao Q, Xu Z (2012) Improve robustness of sparse PCA by -norm maximization. Pattern Recognition 45:487–497

- Moghaddam et al. (2006) Moghaddam B, Weiss Y, Avidan S (2006) Spectral bounds for sparse PCA: Exact and greedy algorithms. In: Weiss Y, Schölkopf B, Platt J (eds) Advances in Neural Information Processing Systems, MIT Press, Cambridge, MA, vol 18, pp 915–922

- Qi et al. (2013) Qi X, Luo R, Zhao H (2013) Sparse principal component analysis by choice of norm. Journal of Multivariate Analysis 114:127–160

- Richtárik (2011) Richtárik P (2011) Finding sparse approximations to extreme eigenvectors: generalized power method for sparse PCA and extensions. In: Proceedings of Signal Processing with Adaptive Sparse Structured Representations

- Shen and Huang (2008) Shen H, Huang JZ (2008) Sparse principal component analysis via regularized low rank matrix approximation. Journal of Multivariate Analysis 99(6):1015–1034

- Trendafilov (2016) Trendafilov NT (2016) From simple structure to sparse components: a review. Computational Statistics 29:431–454

- Trendafilov and Jolliffe (2006) Trendafilov NT, Jolliffe IT (2006) Projected gradient approach to the numerical solution of the scotlass. Journal of Computational Statistics and Data Analysis 50:242–253

- Vu and Lei (2013) Vu VQ, Lei J (2013) Minimax sparse principal subspace estimation in high dimensions. Annals of Statistics 41:2905–2947

- Vu et al. (2013) Vu VQ, Cho J, Lei J, Rohe K (2013) Fantope projection and selection: A near-optimal convex relaxation of sparse PCA. In: Burges CJC, Bottou L, Welling M, Ghahramani Z, Weinberger KQ (eds) Advances in Neural Information Processing Systems, Curran Associates, Red Hook, NY, vol 26, pp 2670–2678

- Witten et al. (2009) Witten DM, Tibshirani R, Hastie T (2009) A penalized matrix decomposition, with applicaitons to sparse principal components and canonical correlation analysis. Biostatistics 10:515–534

- Zhang and El Ghaoui (2011) Zhang Y, El Ghaoui L (2011) Large-scale sparse principal component analysis with application to text data. In: Advances in Neural Information Processing Systems (NIPS), vol 24, pp 532–539

- Zou et al. (2006) Zou H, Hastie T, Tibshirani R (2006) Sparse principal component analysis. Journal of Computational and Graphical Statistics 15(2):265–286