Optimal stopping problems for a Brownian motion with a disorder on a finite interval

Abstract

We consider optimal stopping problems for a Brownian motion and a geometric Brownian motion with a “disorder”, assuming that the moment of a disorder is uniformly distributed on a finite interval. Optimal stopping rules are found as the first hitting times of some Markov process (the Shiryaev–Roberts statistic) to time-dependent boundaries, which are characterized by certain Volterra integral equations.

The problems considered are related to mathematical finance and can be applied in questions of choosing the optimal time to sell an asset with changing trend.

Keywords: optimal stopping problems; disorder detection problems; Shiryaev–Roberts statistic; Volterra equations.

1 Introduction

1.1.

In this paper we consider problems of stopping a Brownian motion or a geometric Brownian motion optimally on a finite time interval when it has a disorder, i. e. its drift coefficient changes at some unknown moment of time from a positive value to a negative one. We look for the stopping time that maximizes the expected value of the stopped process.

Let be a standard Brownian motion defined on a probability space . Suppose we sequentially observe the process ,

or, equivalently in stochastic differentials,

where , are known numbers and is an unknown time of a disorder – a moment when the drift coefficient of changes from value to value . The process is called a (linear) Brownian motion with a disorder.

Adopting the Bayesian approach, we let be a random variable defined on and independent of . In this paper, in view of applications (see below), we assume that is uniformly distributed on a finite interval , possibly, with mass at , i. e. the distribution function is given by

where is the probability that the disorder presents from the beginning, and is the density of . The probability may be strictly positive.

Let denote the class of all stopping times of the process . We consider the following two optimal stopping problems for and the exponent of (a geometric Brownian motion with a disorder):

| (1) |

The problems consist in finding the values , and finding the stopping times , at which the suprema are attained (if such stopping times exist). The superscript stands for the problem for a linear Brownian motion, while stands for a geometric Brownian motion.

Observe that, roughly speaking, the processes and increase on average “up to time ” and decrease on average “after time ”. But since is not a stopping time, we cannot simply take and need to stop by detecting the disorder based on sequential observation of .

We provide solutions to problems (1) using the results obtained in the recent paper [10]. The central idea is based on a reduction to a Markovian optimal stopping problem using a change of measure. This approach has already been applied in the literature, but we were able to generalize it to the case of a finite time interval.

1.2.

For economic applications, the problems considered are related to the question when to quit a financial “bubble”. By a bubble we mean growth of an asset price based mainly on the expectation of higher future price; eventually a bubble bursts and the price starts to decline.

Suppose that an asset price is modelled by a geometric Brownian motion with a disorder :

or, equivalently,

Thus the price initially has a positive trend, which changes to a negative one at an unknown time .

Let correspond to the “current” moment of time, when one is in a long position on an asset with positive trend. Usually, it is possible to predict that the trend will become negative by some (maybe, distant) time in the future. Then one is interested in the question when it is optimal to sell the asset maximizing the gain.

If nothing is known about the actual distribution of , it is natural to assume that is uniformly distributed on (since the uniform distribution has the maximum entropy on a finite interval). Interpreting the quantity as the average gain achieved by selling the asset at time , problem (1) for a geometric Brownian motion seeks for the optimal time to sell the asset. The problem for a linear Brownian motion can be thought of as a problem of finding the optimal time to sell the asset provided that a trader has the logarithmic utility function, i. e. maximizes , which is equivalent to maximizing with , .

An interesting result that follows from the solution of problems (1) is the qualitative difference between risk-neutral traders who maximize and risk-averse traders who maximize : if (i. e. the distribution of has no mass at ), then a risk-neutral trader will sell the asset strictly before time with probability one (), while a risk-averse trader will wait until the end of the time interval with positive probability (); see the Theorem and Remark 1 in Section 2.

1.3.

Problems (1) was considered in the papers [1, 7, 2], assuming that the moment of disorder is exponentially distributed. In [1], the problem for a geometric Brownian motion was solved. It was shown that if satisfy some relation, the optimal stopping time is the first hitting time of the posterior probability process , where , to some level. In [2] this result was extended to all values of and the optimal stopping level was found. In [7], the problem for a linear Brownian motion was considered on a finite interval, i. e. assuming that one should choose not exceeding some time horizon (but the disorder may happen after ). It turned out that the problem is equivalent to the original Bayesian setting of the disorder detection problem when one seeks for a stopping time minimizing the average detection delay and the probability of a false alarm (see e. g. [8, 9, 4]). The paper [7] also briefly discusses the optimal stopping problem for a geometric Brownian motion on a finite interval, but does not provide an explicit solution.

2 The main result

2.1.

Let denote the signal-to-noise ratio. For convenience of notation, introduce the process , , which is a Brownian motion with the unit diffusion coefficient and the drift coefficient changing at time from value to value .

Introduce the Shiryaev–Roberts statistic111In a general case, the Shiryaev–Roberts statistic is given by , where for the measures or , corresponding to that the disorder happens at time or does not happen at all (for details, see [10] and the proof of the Lemma in Section 3). :

| (2) |

with . Applying the Itô formula it is easy to see that satisfies the stochastic differential equation

| (3) |

On the measurable space , , define the probability measures and such that is a standard Brownian motion under and is a standard Brownian motion under . These measures will be used to solve the problems and respectively. It is well-known (see, e. g., [5, Ch. 7]) that and are equivalent on the space .

For any , by and we denote the mathematical expectations of functionals of the process defined by (2)–(3) with the initial condition , when is respectively a standard Brownian motion or a Brownian motion with drift . For brevity, instead of and we simply write and .

The main result of the paper is the following theorem.

Theorem.

The optimal stopping times in the problems and are given respectively by

where , are non-increasing functions on being the unique solutions of the integral equations ()

| (4) | |||

| (5) |

in the class of continuous bounded functions on satisfying the conditions

| (6) | ||||

| (7) |

The values and can be found by the formulas

| (8) | |||

| (9) |

Remarks.

1. Regarding the difference between a risk-averse trader and a risk-neutral trader mentioned in Section 1, observe that if , then because , while because (in the latter case the process stays below on the whole interval with positive probability).

2. In the above mentioned papers [1, 7, 2], solutions to problems (1) when is exponentially distributed were given in terms of the posterior probability process . Using the Bayes formula, one can check that the processes and are connected by the formula (see [10]). Consequently, it is easy to reformulate the Theorem in a such way that and are the first moments of time when the process crosses time-dependent levels. We prefer to work with the process because it has a somewhat simpler form than , when is uniformly distributed.

2.2.

Equations (4), (5) can be solved numerically by backward induction: we fix a partition of and sequentially find the values . The value can be found from condition (6) or (7) respectively. Having found the values and numerically computing integral (4) or (5) for through the values of the integrand at points , we obtain the equation, from which the value can be found. Repeating this procedure, we find the value of at every point of the partition.

To compute the mathematical expectations in (4), (5), (8), (9), one can use the Monte–Carlo method or use the explicit formula for the transitional density of (see e. g. [10], where it was obtained from the joint law of an exponent of a Brownian motion and its integral that can be found in [6]).

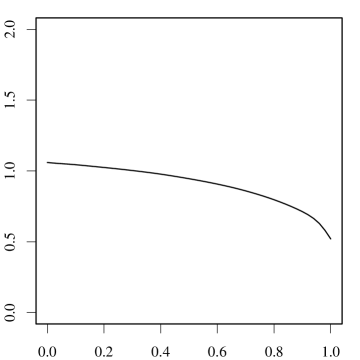

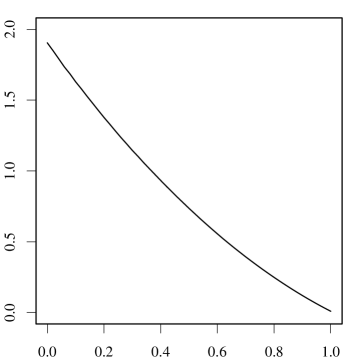

As an example of a numerical solution of equations (4), (5), on Figure 1 we present the optimal stopping boundaries for the case , , , , for .

3 Proof of the theorem

3.1.

To prove the theorem, we first reduce problems and to optimal stopping problems for the process , and then apply the Proposition from the Appendix, which was proved in [10]. The method we use is based on the ideas of [3, 1].

Lemma.

The following formulae hold:

The supremum in each formula is attained at the stopping time which is optimal in the corresponding problem (1).

Proof.

It is sufficient to show that for any stopping time

| (10) | |||

| (11) |

On the measurable space define the family of probability measures such that under the disorder occurs at the fixed time , i. e. for each the process can be represented as , where is a standard Brownian motion under . By we denote the mathematical expectation with respect to and by , , , we denote the restrictions of the corresponding measures to the -algebra , .

Let us prove (10). Since the Brownian motion is a zero-mean martingale, we have

| (12) |

Consider the second term in the sum:

| (13) |

Observe that for any the following relation is valid:

| (14) |

where we use that is an -measurable random variable and

(the explicit formula for the density of the measure generated by one Itô process with respect to the measure generated by another Itô process can be found in e. g. [5]). From (13)–(14), changing the order of integration we find

3.2.

Now the proof of the Theorem follows from the Proposition in the Appendix – for the problem we use that the process satisfies equation (3) with being a Brownian motion under the measure , and for the problem we use that satisfies the equation

| (15) |

where is a Brownian motion under .

4 Acknowledgements

The authors are grateful to Prof. H. R. Lerche and A. A. Levinskiy for valuable remarks. The work is supported by Laboratory for Structural Methods of Data Analysis in Predictive Modeling, MIPT, RF government grant, ag. 11.G34.31.0073. The work of M. V. Zhitlukhin is also supported by The Russian Foundation for Basic Research, grant 12-01-31449-mol_a.

Appendix

Let be a standard Brownian motion defined on a filtered probability space and be a stochastic process satisfying the stochastic differential equation (cf. (3), (15))

| (16) |

where and .

Consider the optimal stopping problem consisting in finding the quantity

| (17) |

where , and is a non-increasing bounded function which is continuous and strictly positive on . The supremum in (17) is taken over all stopping times of the filtration satisfying the condition a.s.

For arbitrary , let denote the mathematical expectation of functionals of the process , satisfying (16) with .

The following result was proved in [10].

Proposition.

The optimal stopping time in problem (17) is given by

where is a non-increasing function on being the unique solution of the equation ()

in the class of continuous bounded functions on satisfying the conditions

The quantity can be found by the formula

References

- [1] M. Beibel, H. R. Lerche. A new look at optimal stopping problems related to mathematical finance. Statistica Sinica, 7:93–108, 1997.

- [2] E. Ekström, C. Lindberg. Optimal closing of a momentum trade. To appear in Journal of Applied Probability, 2013.

- [3] E. A. Feinberg, A. N. Shiryaev. Quickest detection of drift change for Brownian motion in generalized bayesian and minimax settings. Statistics & Decisions, 24(4):445–470, 2006.

- [4] P. V. Gapeev, G. Peskir. The Wiener disorder problem with finite horizon. Stochastic processes and their applications, 116(12):1770–1791, 2006.

- [5] R. S. Liptser, A. N. Shiryaev. Statistics of Random Processes. Springer, 2nd edition, 2000.

- [6] H. Matsumoto, M. Yor. Exponential functionals of Brownian motion I: Probability laws at fixed time. Probability Surveys, 2:312–346, 2005.

- [7] A. Shiryaev, A. A. Novikov. On a stochastic version of the trading rule “Buy and Hold”. Statistics & Decisions, 26(4):289–302, 2009.

- [8] A. N. Shiryaev. On optimal methods in quickest detection problems. Theory of Probability and Its Applications, 8(1):22–46, 1963.

- [9] A. N. Shiryaev. Optimal Stopping Rules. Springer, 3rd edition, 2008.

- [10] M. V. Zhitlukhin, A. N. Shiryaev. Bayesian disorder detection problems on filtered probability spaces. Theory of Probability and Its Applications, 57(3):453–470, 2012.