Optimal Liquidation in a Finite Time Regime Switching Model with Permanent and Temporary Pricing Impact

Baojun Bian and

Nan Wu and

Harry Zheng

Department of Mathematics, Tongji University,

Shanghai 200092, China. bianbj@tongji.edu.cn. This work was supported in part

by National Science Foundation of China(No.11371280,

No.71090404). Department of Mathematics, Imperial College, London SW7 2BZ, UK. nan.wu07@imperial.ac.ukDepartment of Mathematics, Imperial College, London SW7 2BZ, UK.

h.zheng@imperial.ac.uk.

Abstract.

In this paper we discuss the optimal liquidation over a finite time horizon until the exit time. The drift and diffusion terms of the asset price are general functions depending on all variables including control and

market regime. There is also a local nonlinear transaction cost associated to the liquidation. The model deals with both the permanent impact and the temporary impact in a regime switching framework. The problem can be solved with the dynamic programming principle. The optimal value function is the unique continuous viscosity solution to the HJB equation and can be computed with the finite difference method.

Optimal liquidation has attracted active research in recent years due to the liquidity risk. In a frictionless and competitive market an asset can be traded with any amount at any rate without affecting the market price of the asset. The optimal liquidation then becomes an optimal stopping problem which maximizes the expected liquidation value at the optimal stopping time.

In an incomplete market with trading constraints on the volume and the rate and with the liquidation impact on the underlying asset price, the optimal liquidation is difficult to model and to solve.

Despite the wide recognition of the importance of the liquidity risk,

there is no universal agreement on the definition of liquidity.

In the academic literature the liquidity is usually defined in terms of

the bid-ask spread and/or the transaction cost

whereas in the practitioner literature the illiquidity is often

viewed as the inability of buying and selling securities.

Black [2] classifies the following four major properties of

the liquidity:

the immediacy of the transaction, the tightness of the spread, the resiliency

of the market,

and the depth of the market. The concept of liquidity can be summarized as

the ability for traders to execute large trades rapidly at a price close

to current market price. The liquidity risk refers to the loss stemming

from the cost of liquidating a position.

Due to lack of universal agreement on the definition of liquidity, there are many different forms of mathematical characterizations. Apart from commonly used transaction cost and bid-ask spread and trading constraints (Cvitanic and Karatzas [5], Jouini [9], etc.), the other descriptions include, for example, that the order of a large investor adversely affects the stock price before being exercised (Bank and Baum [1]), that the market has a supply curve that depends on the order size of investors (Çetin et al. [3]), that trading can only happen at jump times of a Cox process (Gassiat et al. [8]), that the asset price is affected by the permanent and temporary impact of liquidation (Schied and Schöneborn [15]), etc.

Once the mathematical framework is chosen for the liquidity risk one can then study specific problems such as the arbitrage pricing theory, the optimal investment and consumption, etc., see [1, 3, 5, 8, 9, 15] and references therein.

This paper studies the optimal liquidation in the presence of liquidity risk. There are several variations in the problem formulation in the literature, including finite or infinite time horizon, continuous trading or optimal stopping, geometric Brownian motion (GBM) asset price process or Markov modulated process, etc.

Pemy et al. [13] study the optimal liquidation over an infinite time horizon. The stock

price follows a GBM process with an extra term that reflects the permanent impact of liquidation

on the asset price and there is no temporary impact. It is a constrained control problem which implicitly

assumes that the stock holdings will never be sold out for any admissible trading strategies.

The value function is

the unique continuous viscosity solution to the Hamilton-Jacobi-Bellman (HJB) equation (two state variables and no time variable).

In the continuous time finite state Markov chain framework

Pemy and Zhang [12] study an optimal stopping problem of liquidation in finite time horizon.

Pemy et al. [14] discuss the optimal liquidation over an infinite time, similar to that in [13]. The main difference is that the asset price follows a

GBM process in which the drift and diffusion coefficients are determined by market regimes and the temporary impact of liquidation is reflected in the payoff function and there is no permanent impact. The assumptions and the conclusions are basically the same as those in [13].

In this paper we discuss the optimal liquidation over a finite time horizon until the exit time. The drift and diffusion coefficients and of the asset price are general functions depending on all variables including control (see (2)), which implies the trading may cause the permanent impact on the asset price. There are also nonlinear transaction costs associated to the trading through the temporary pricing impact function and the block liquidation impact function (see (7)). The model deals with both the permanent impact and the temporary impact in a regime switching framework. We can apply the dynamic programing principle to derive the HJB equation that involves time variable as well as state variables, which makes the proofs more involved than those in [13, 14].

Our main contribution is that we show the optimal value function is the unique continuous viscosity solution to the HJB equation, which opens the way to solving the problem with the finite difference method.

The paper is organized as follows. Section 2 formulates the optimal liquidation problem and states the main results of the paper. Section 3 gives a numerical example. Section 4 proves that the optimal value function is continuous (Theorem 3). Section 5 proves that the value function is the viscosity solution to the HJB equation (Theorem 5). Section 6 proves the comparison theorem for the uniqueness of the viscosity solution (Theorem 6).

2 Model and Main Results

Let be a probability space and be the natural filtration generated by a standard Brownian motion process and

a continuous time Markov chain process , augmented by all -null sets. Assume and are independent to each other. Assume that the Markov chain has a

finite state space and is generated by the generator , where for , and

for each . The transitional

probability is given by

(1)

for small time interval . The continuous time Markov chain models

the economic environment which affects the growth rate and the volatility of the asset price.

Let be the time variable, where is the fixed terminal time and is the starting

time. Let denote the stock price and the number of shares of stock.

Let denote the rate of selling the stock, which is a control variable decided by the trader. We call is admissible if it is progressively measurable and for a compact set for all . The stock price follows a stochastic differential equation with regime switching

(2)

and the stock holding follows the dynamics

Since the drift and the diffusion terms of are affected by the trading strategy there is the permanent impact of liquidation on the asset price. Such an impact may be negligible for a small trader (when is small) but can be significant for a large trader (when is large). We implicitly assume that the asset price is positive for all . A sufficient condition that guarantees this is that follows a geometric Brownian motion process with drift and diffusion coefficients depending on time, control and Markov state. We denote by some generic positive constant which may take different values at different places.

Assumption 1.

Functions satisfy,

for all , , and ,

that

(3)

It can be shown, with

Assumption 1, that for any admissible control process and any initial values

, there exists a unique solution, denoted by , to equation (2), and that

the following inequalities hold:

(4)

(5)

(6)

The proofs of (4), (5) and (6) can be found in Mao and Yuan [10] with some minor changes to include control processes, see [10], Theorem3.23, Theorem 3.24 and Lemma 3.3.

Similarly,

denotes the stock holding and

the Markov chain process.

Suppose a trader starts from time , endowed with initial values .

Define a stopping time

This is the first time that exits from before or at time .

Since the model is to study

the liquidation strategy, the trader is only allowed to sell stock without buying back. When the number of shares reaches zero before

time the liquidation stops. Otherwise, it stops at time .

The expected discounted total payoff associated with a strategy

is defined by

(7)

where is a discount rate, a function measuring the temporary liquidation effect, a function measuring the block liquidation effect, and the conditional expectation given the information set which is equivalent to given , and since the model is Markov. The first term is the expected discounted accumulated cash value from the stock liquidation and the second term is the expected discounted cash value from the block liquidation at time for any remaining shares of the stock.

Assumption 2.

Functions are continuous

concave increasing on and satisfy and . Furthermore, function is continuously differentiable and satisfies,

for all , that

Note that in

a completely liquid market and , and that

and imply is approximately equal to when is close to 0, which means when the trading rate is small or the amount of stock is small then there is essentially no transaction cost and the liquidity impact can be ignored.

The objective of the trader is to maximize the expected discounted revenue from stock liquidation.

The value function is defined by

For define operators and of the value function

by

and

The HJB equation for the optimal control problem is, for ,

(8)

with the boundary condition

and the terminal condition

It is easy to check that the value function is an increasing function with respect to the asset price and the stock holding. It also

has the following continuity property.

Theorem 3.

Assume Assumptions 1 and 2. Then

the value function is continuous on

for .

Since we do not know if the value function is continuously differentiable and cannot discuss the solution to the HJB equation in the classical sense, we need to introduce the concept of the viscosity solution to the HJB equation.

Definition 4.

A system of continuous functions on is a viscosity

subsolution (resp. supersolution) of the HJB equation (8) if, for any fixed ,

and such that attains its maximum (resp. minimum) at , we have

(9)

The system of continuous functions is a viscosity solution if it is both a viscosity subsolution and a viscosity supersolution.

We have the following result for the value function.

Theorem 5.

Assume Assumptions 1 and 2.

Then the value function is a viscosity solution to the HJB equation (8).

One in general has to use some numerical scheme to find the value function. To ensure the numerical solution to the HJB equation is indeed the value function one has to show that the value function is the unique viscosity solution to the HJB equation, which can be achieved by the following comparison theorem.

Theorem 6.

Assume Assumptions 1 and 2.

Let be a viscosity subsolution and a viscosity supersolution to the HJB equation (8) and satisfy the polynomial growth condition and

for all . Then on

.

The proofs of Theorems 3, 5, and 6 are given in Sections 4, 5, and 6, respectively. The proofs are technical and lengthy as one would expect with the viscosity solution method. The further complication in the proofs over the standard diffusion model is that we need to deal with the Markov chain process and its relation with the diffusion process .

3 A Numerical Example

In this section we give a numerical example to find the approximation of the value function and the optimal selling strategy. The finite difference method is one of the most common approximation schemes for viscosity solutions due to its well-known consistency, stability, convergence analysis, in particular in the presence of the monotonicity property, see [7] for numerical solutions of HJB equation and [12] for a regime switching optimal stopping problem which results in a system of HJB variational inequalities. We may apply the numerical scheme of [12] to solve our optimal liquidation problem. The numerical example is to provide a snapshot of the optimal trading strategy at a given specific time.

Assume that there are only two regimes. Regime 1 represents the strong economy and regime 2 the weak economy and assume that the stock price

follows a GBM process with

and

.

Define variables and and a function

. The HJB equation (8) becomes

(10)

with the boundary condition and the terminal condition

.

To approximate the solution to (3) we discretize variables , and with stepsizes , respectively. The value of

at a grid point in the regime is denoted by . The derivatives of are approximated by

,

,

, and

.

Discretizing equation (3) and rearranging the terms,

we have

(11)

where and . Assume that the temporary liquidation impact function is given by

where , and the block liquidation impact function is given by

Functions and satisfy Assumption 2. In fact, is constructed as a smooth approximation to a function defined by

Function captures the block liquidation effect at time but is not differentiable at and 50 and does not satisfy Assumption 2.

Data used for numerical tests are , , , , , , ,

, , .

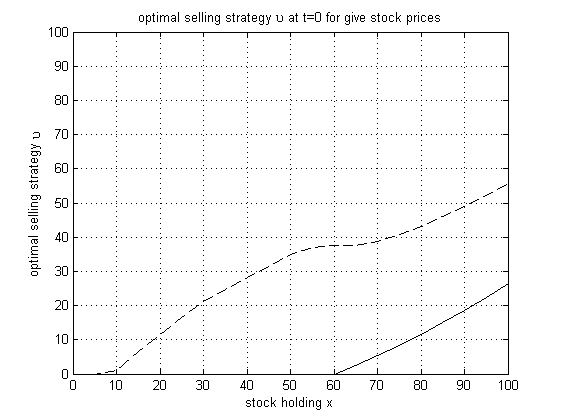

(a)Figure 1: The optimal control at time against stock holding . The solid line is for regime 1 and the dashed line for regime 2.

Figure 1 demonstrates the relationship between the optimal selling strategy and the stock holding. It is clear that the more shares

one holds, the sooner and the more one wants to sell to avoid the potential large transaction cost during the whole period. The market regime determines at what level of stock holding one should start to sell. In a rising market (regime 1) the trader is willing to keep the stock

for a longer period in the hope for a higher price, which results in a lower optimal selling rate, whereas in a falling market (regime 2) the trader wants to liquidate the stock quickly to avoid a lower price. This is consistent with the general market phenomenon. The optimal trading strategy is independent of initial asset price in the numerical test, which is not surprising as the asset price follows a GBM process and depends on the initial asset price linearly. In general, the optimal trading strategy should also depend on the asset price.

The particular shape of the curve

in Figure 1 is determined by the tradeoff between function that captures the liquidity effect from ’flow’ trading and function

that reflects the transaction cost for the block liquidation at the terminal time.

Note that if there is no temporary pricing impact on liquidation, i.e., , then the optimal liquidation strategy is a “bang-bang” control with either no trading or selling at maximum rate due to the linear dependence of control in the Hamiltonian function.

We first convert the original control problem into a problem without terminal bequest function. Since function is continuously

differentiable, we can apply Dynkin’s formula to

and rewrite the total payoff as

where

Define a new value function by

Since , we know

is continuous as long as is continuous. From now on in this section we work on the value function .

To prove the continuity of we need to define some perturbed problems and show their corresponding value functions are continuous and converge quasi-uniformly to , which establishes Theorem 3.

For define the stopping time

which is the

first time exits from .

A control process is admissible if it is progressively measurable and , where if and

, a compact subset of in , if .

The key here is to rule out zero from the

compact set after reaches zero. The admissible control set is the collection of all admissible controls, denoted by . Note that when we only look at the control process before , the two admissible control sets, and , are the same.

To simplify the notation denote by

Since is a compact set in , say , we know that for , which implies that and are bounded by some constant depending on due to continuity of and . Assumptions 1 and 2

imply that, for ,

(12)

and

(13)

for some constant depending on .

Remark 7.

In the proof we need to estimate several times for different . One case is that for . Then and constant can be replaced by a generic constant independent of . The other case is that is within a distance of another point . Then and constant can be written as depending on for all such .

For define a perturbed value function by

For define an auxiliary function

where . Clearly, we have

and,

by the definition of the stopping time ,

for .

The auxiliary value function is defined by

Step 1. Fix a point .

Since we have and for

the admissible control is in a compact set with , which implies that and

(15)

and

.

(15), (12) and (4) imply that, also noting Remark 7,

Similarly, we have

Combining the above two inequalities and taking the supremum, we have

Applying the dynamic programming principle (see [4]), for , we have

Similarly, we have

The above two inequalities imply that

converges to quasi-uniformly as , independent of .

Step 2. By the definition of the perturbed value function, the Cauchy-Schwartz inequality, (12) and (4), we have

for some constant depending on . Similarly, we have

As , converges to quasi-uniformly. Combining the results of

Steps 1 and 2, we conclude that converges to quasi-uniformly

as and .

∎

Lemma 9.

is continuous on

for and arbitrary constants and .

Proof.

Step 1. Let satisfying and and and . Consider the auxiliary value functions

and .

Since for any , we have

(16)

By the definition of and the relation we have

(17)

where is some constant depending on and . In the second last inequality we have used (13), (6), (4),

(12), (16) and Remark 7.

This shows that

the auxiliary value function is continuous in , uniformly in .

Step 2. We prove that the auxiliary value function is continuous in . Let

and . By the dynamic programming principle, for any , there exists an admissible control such that

for some constant depending on and . Noting that the term inside the expectation of is zero when , using Cauchy-Schwartz inequality and combining the above inequality, we have

for some constant depending on .

The above estimates for show that they all tend to 0 as tends to 0, independent of and control but dependent on and . Therefore,

The arbitrariness of confirms that is

continuous in .

Combining the results of Steps 1 and 2, we conclude that is continuous

in for each .

∎

By Lemmas 8 and 9, the auxiliary value function converges quasi-uniformly

to the value function as and and is continuous in , which shows that

is continuous on for each . We have proved Theorem 3.

Given Assumption 1, the value function is a viscosity supersolution

of the HJB equation (8).

Proof.

Let , . Let the test function

such that attains

its minimum at and, without loss of generality, . Choose a constant control for . Let the state variables and

start from time with initial values and .

Define as the first jump time of the regime . Without loss of generality, assume that is small enough such that

. Define by

For , define the stopping time . Note that . By dynamic programming principle,

(18)

Define

(19)

Applying Dynkin’s formula at point , also noting ,

we have

(20)

which implies, from the choice of and the definition of , that

(21)

Substitute (21) into (18) and divide both sides by we get

(22)

for some constant , due to continuity of the function on the left hand side of (9) and the boundedness

of state variable on the time interval .

By definition of , we have

So as , goes to zero.

By Chebyshev’s inequality, we have

(23)

Since each term on the numerator of (5) converges to zero as and

, we have

(24)

Let in (5). By the mean value theorem and the dominated convergence theorem, we have

Since is chosen arbitrarily, we take the supremum over and get

Therefore, V is a viscosity supersolution of the HJB equation (8).

∎

For , define the Hamiltonian function by

(25)

Lemma 11.

For all , the Hamiltonian is continuous in .

Proof.

Let the point and the ball with the center and the radius , a small constant.

By the definition of the Hamiltonian function, for an arbitrary given , there exists a such that

Letting in (38), we get , a contradiction. The inequality in (32) therefore holds, which completes the proof.

∎

Since the value function is both a viscosity subsolution and a viscosity supersolution,

we conclude that it is a viscosity solution of the HJB equation (8). We have proved Theorem 5.

In this section vectors and and their specific values such as appear many times. To simplify the expressions we denote by and . Their specific values are defined similarly, for example,

.

To prove the uniqueness, we need an alternative definition of viscosity solution in terms of superjets and subjets. The second-order superjet of an upper-semicontinuous function at a point , denoted by , is defined as a set of elements such that

(39)

where is a higher order error term.

The limiting superjet is the set of elements for which there exists

a sequence in and

such that

.

The second-order subjet of a lower-semicontinuous function at a point

, denoted by , is defined as in (39) with a greater than or equal () inequality. The set is defined similarly.

Note that since is a state variable superjets and subjects should normally also have second order terms with respect to . However, since the HJB equation (8) only involves the first order derivative of the value function with respect to , the second order expansion in is not needed.

Assume that is upper-semicontinuous and . Then is a maximum point of if and only if , where

. Similar conclusion holds for the minimum point and the subjet.

Lemma 13.

([6, Theorem 8.3])

An -tuple of continuous functions on is a viscosity

subsolution (resp. supersolution) of the HJB equation (8) if and only if for

such that

(resp. ) for any fixed , we have

where is the Hamiltonian define in (25). The -tuple is a viscosity solution if it is both a viscosity subsolution and a viscosity supersolution.

The uniform polynomial growth condition for and implies that there exists a constant such that, for each

Define functions and for .

Due to the linear growth condition (3) and the boundedness of set , there exists a

positive constant such that, for all ,

which is nonnegative as long as we choose the constant large enough such that . Therefore, for any , is a supersolution to the HJB equation (8).

To check this, let be the test function for . So

is the test function for the supersolution .

We have

By the polynomial growth condition of , and the definition of , we have

for all .

We can assume that the maximum of over and is

attained (up to a penalization) at and for some compact set

and . Let denote this maximum.

Suppose, for contradiction, that there exists

and such that . We have

(40)

For any , define a function by

where is defined by

(41)

For each , is continuous. Hence its maximum, denoted by , over the compact set

can be attained at

. Assume that the maximum is attained at and

. We have

(42)

As , the bounded sequence converges,

up to a subsequence, to a limit .

By assumption, is finite. For each , the sequence

converges, up to a subsequence, to its limit, respectively. Therefore, for small

enough, for .

Since and are continuous and is a finite set,

is bounded for all .

From (42), is also bounded, which implies that

(43)

By applying Ishii’s Lemma (see [11, Lemma 4.4.6, Remark 4.4.9]) to function at its maximum point with ,

we can find such that

and, for any ,

(44)

Denote by

Since is a viscosity subsolution and a supersolution, by the definition of viscosity solutions

in terms of superjets and subjets, we have

(45)

(46)

where the Hamiltonian is defined in (25).

By the definition of operator we have

(47)

The last line is from the fact that

is the maximum of

over and .

Subtracting (46) from (45) and rearranging, also noting (6), we have

(48)

By the definition of the Hamiltonian function, for any , there exists a such that

which contradicts (40). Therefore

on .

We have proved Theorem 6.

Acknowledgement. The authors thank two anonymous referees for their suggestions and comments that have helped to improve the paper.

References

[1]

Bank, P. and Baum, D., Hedging and portfolio optimization in

financial markets with a large trader, Mathematical Finance 14, 1-18, 2004.

[2]

Black, F.,

Towards a fully automated exchange: Part 1,

Financial Analyst Journal 27, 29-34, 1971.

[3]

Çetin, U., Jarrow, R.A. and Protter, P., Liquidity risk and arbitrage pricing theory, Finance and Stochastics 8, 311-341, 2004.

[4]

W.H. Fleming, and H.M. Soner Controlled Markov Processes and Viscosity Solutions,

Springer, 2006

[5]

Cvitanic, J. and Karatzas, I., Hedging and portfolio optimization under transaction costs: a martingale approach, Mathematical Finance 6, 370-398, 1996.

[6]

Crandall, M.G., Ishii, H. and Lions, P.L., User’s guide to viscosity

solutions of second order partial differential equations,

Bulletin American Mathematical Society 27, 1-67, 1992.

[7]

Crandall, M.G. and Lions, P.L., Two apprximations of solutions of Hamilton-Jacobi equations, Mathematics of Computation 43, 1-19, 1984.

[8]

Gassiat, P., Gozzi, F. and Pham, H., Investment/consumption problem in illiquid markets

with regimes switching, it SIAM J. Control Optimization, to appear, 2012.

[9]

Jouini, E., Price functionals with bid-ask spreads: an axiomatic approach, J. Mathematical Economics 34, 547-558, 2000.

[10]

Mao, X. and Yuan, C., Stochastic Differential Equations with Markovian Switching, Imperial College Press, 2006.

[11]

Pham, H., Continuous-time Stochastic Control and Optimization with Financial Applications,

Springer, 2010

[12]

Pemy, M. and Zhang, Q., Optimal stock liquidation in a regime switching model

with finite time horizon, J. Mathematical Analysis & Applications 321, 537-552, 2006.

[13]

Pemy, M., Zhang, Q. and Yin, G., Liquidation of a large block of stock,

J. Banking & Finance 31, 1295-1305, 2007.

[14]

Pemy, M., Zhang, Q. and Yin, G., Liquidation of a large block of stock

with regime switching, Mathematical Finance 18, 629-648, 2008.

[15]

Schied, A. and Schöneborn, T., Optimal portfolio liquidation for CARA investors, working paper, 2007.