Simulating the Continuation of a Time Series in R

Abstract

The simulation of the continuation of a given time series is useful for many practical applications. But no standard procedure for this task is suggested in the literature. It is therefore demonstrated how to use the seasonal ARIMA process to simulate the continuation of an observed time series. The R-code presented uses well-known modeling procedures for ARIMA models and conditional simulation of a SARIMA model with known parameters. A small example demonstrates the correctness and practical relevance of the new idea.

Halis Sak 111Corresponding author. Tel: +90.216.5780000-3363

Email addresses: halis.sak@gmail.com (Halis Sak), hormannw@boun.edu.tr (Wolfgang Hörmann)

Department of Industrial and Systems Engineering, Yeditepe University, Kayışdağı, 34755 İstanbul, Turkey

Wolfgang Hörmann

Department of Industrial Engineering,

Boğaziçi University,

34342 Bebek-İstanbul, Turkey

seasonal ARIMA, simulation, R

1 Introduction

In many application areas it is of practical interest to be able to simulate the possible continuation of a given time series. For example in finance the simulation of future stock prices is a well-known standard method used for risk assessment and for option pricing. In inventory management the simulation of future demands could be used to compare the performance of different inventory policies. Clearly many other examples of applications in different areas are possible. When we wanted to quantify the risk of a company due to the uncertainty of the demand in the next months we tried to find code that simulates random future observations of the demand subject to the SARIMA (Seasonal Autoregressive Integrated Moving Average) model we had fitted to the data. We were astonished when we realized that we were not able to find a single paper in the literature that tackles this problem. It is clear that such a simulation conditional on given data requires a modeling and a parameter estimation step. These two steps are also required for forecasting. Seasonal (and non-seasonal) ARIMA models have been considered as standard procedures for many years ([1]) and are described in many text books (see eg. [5]). After selecting an ARIMA model and the estimation of its parameters only the conditional simulation of future realizations given the observations is required. Many software packages (including R ([6])) contain functions to simulate realizations of ARIMA processes. But we were not able to find any description or implementation of a “simulation conditional on the observed values” for ARIMA models in the literature.

2 SARIMA processes

In R, the notation used for ARMA() processes is

| (1) |

where denotes the parameters of the autoregressive process, the parameters of the moving average process and the white noise error terms with standard deviation following the normal distribution. Using the well known backshift operator notation we can rewrite the above definition by

where denotes a backshift polynomial of order and a backshift polynomial of order . An ARIMA() process is a process whose -th difference

is an ARMA() process. An ARIMA() process is thus defined by the equation:

For seasonal ARIMA (SARIMA) processes with period , a seasonal AR polynomial of order , a seasonal MA polynomial of order and the seasonal difference operator of order

are required. The SARIMA()( is then defined by the equation:

| (2) |

For given observations the selection of the model orders for a SARIMA model is the topic of many books on time series analysis and without the scope of this note. The estimation of the parameters is easy using the arima() function of the R-base stats package. We now assume that the observed time series is a realization of the stochastic process defined by all model assumptions of the SARIMA model and its estimated parameters. We now consider the next observations of the time series that are not known yet. The distribution of that random vector conditional on the observed values is multi-normal and can be called conditional distribution of the future observation. The forecasts of the SARIMA model for the given time series are the expectations of the one- dimensional marginals of that conditional distribution and we write for example

The conditional standard deviations of the one-dimensional marginals are used to calculate the prediction error. Exactly these conditional expectations and variances are calculated by the predict() function.

3 Conditional simulation of a SARIMA process

The new idea of this note is now the suggestion to provide code that generates random realizations of the future observation vector conditional on the observed observations. We can write

for that future observation vector and we hope that the presentation above made clear, why we can call a realization of that random vector a random continuation of the time series data we have observed. As the distribution of the vector is multi-normal it would be possible to generate from that distribution calculating its mean vector and variance-covariance matrix. But it is much easier to use directly the recursion of the model equation of the ARMA model: To generate a random realization of conditional on the past we need the past observations, the estimated parameters and the residuals (ie. the estimates of the random shocks ). It is then no problem to simulate using the recursion given in formula (1). The new random shock is generated as a normal random variate with mean zero and standard deviation . The simulation of is done conditional on the past observations and on the generated values and .

For the case of SARIMA processes the model equation is again a linear combination of past observations and past random shocks together with the new random shock . Due to the seasonal model some of the AR-parameters () and MA-parameters () are equal to zero. So again we can use the recursive approach explained above.

In this code snippet we present the R routine we coded according to the above explanations. It generates future observations from seasonal and non-seasonal ARIMA processes conditional on an observed time series.

Algorithm 1 summarizes how future values are simulated from seasonal and non-seasonal ARIMA process. When we fit the ARIMA model using the arima() function of the R-base stats package, all the model parameters including the estimated variance of error terms ( are returned as demonstrated in Section 4. R codes for Algorithm 1 are given in Section 5.

4 Numerical experiments

In this section we first fit a seasonal model to monthly totals of international airline passengers between and using the arima(). (The data are available in the R package fma [2].)

R> library("fma")

R> set.seed(4321)

R> data <- airpass

R> Par <- c(1, 1, 1, 0, 1, 0)

R> fit <- arima(data, order = c(Par[1], Par[2], Par[3]),

+ seasonal = list(order = c(Par[4], Par[5], Par[6])))

R> fit

Series: data

ARIMA(1, 1, 1)(0, 1, 0)[12]

Coefficients:

ar1 ma1

-0.3009 -0.0073

s.e. 0.3835 0.4133

sigma^2 estimated as 137: log likelihood = -508.2

AIC = 1022.39 AICc = 1022.58 BIC = 1031.02

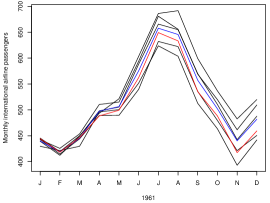

For demonstration purposes we generate five different independent continuations of the time series and show them, their average and the forecasted values in Figure 1.

R> sims <- arima.condsim(fit, data, n.ahead = 12, n = 5) R> ts1 <- ts(sims[, 1], f = frequency(data), s = tsp(data)[2] + + 1/tsp(data)[3]) R> ts2 <- ts(sims[, 2], f = frequency(data), s = tsp(data)[2] + + 1/tsp(data)[3]) R> ts3 <- ts(sims[, 3], f = frequency(data), s = tsp(data)[2] + + 1/tsp(data)[3]) R> ts4 <- ts(sims[, 4], f = frequency(data), s = tsp(data)[2] + + 1/tsp(data)[3]) R> ts5 <- ts(sims[, 5], f = frequency(data), s = tsp(data)[2] + + 1/tsp(data)[3]) R> tsA <- ts(sapply(seq_len(12), function(i) mean(sims[i,])), + f = frequency(data), s = tsp(data)[2]+1/tsp(data)[3]) R> ts.plot(ts1, ts2, ts3, ts4, ts5, gpars = list(xlab = "1961", + ylab = "Monthly international airline passengers", xaxt = "n")) R> lines(tsA, col="blue") R> lines(predict(fit, n.ahead=12)$pred, col="red") R> axis(1, time(ts1), rep(substr(month.abb, 1, 1), length = length(ts1)))

In the following experiment we simulate independent continuations and show that, as expected, the mean of the simulated values is very close to the forecasted values. It is also possible to use innovations equal to zero in our function arima.condsim() to produce the exact forecasts.

R> sims <- arima.condsim(fit, data, n.ahead = 12, n = 10000)

R> sims_mean <- sapply(seq_len(12), function(i) mean(sims[i, ]))

R> ts <- ts(sims_mean, f = frequency(data), s = tsp(data)[2] +

+ 1/tsp(data)[3])

R> ts

Jan Feb Mar Apr May Jun

1961 444.2828 418.1049 446.0237 487.9601 498.8899 562.0800

Jul Aug Sep Oct Nov Dec

1961 648.9706 633.0297 535.0563 487.9923 417.1746 459.2555

R> predict(fit, n.ahead = 12)

$pred

Jan Feb Mar Apr May Jun

1961 444.3670 418.2566 446.2898 488.2798 499.2828 562.2819

Jul Aug Sep Oct Nov Dec

1961 649.2822 633.2821 535.2821 488.2821 417.2821 459.2821

Finally, we fit a non-seasonal model to the same data to show that our function works both for seasonal and non-seasonal models.

R> Par <- c(1, 0, 1, 0, 0, 0)

R> fit <- arima(data, order = c(Par[1], Par[2], Par[3]),

+ seasonal = list(order = c(Par[4], Par[5], Par[6])))

R> fit

Series: data

ARIMA(1, 0, 1) with non-zero mean

Coefficients:

ar1 ma1 intercept

0.9373 0.4264 281.5426

s.e. 0.0302 0.0911 53.6135

sigma^2 estimated as 968.5: log likelihood = -700.87

AIC = 1409.75 AICc = 1410.04 BIC = 1421.63

R> sims <- arima.condsim(fit, data, n.ahead = 12, n = 10000)

R> sims_mean <- sapply(seq_len(12), function(i) mean(sims[i, ]))

R> ts <- ts(sims_mean, f = frequency(data), s = tsp(data)[2] +

+ 1/tsp(data)[3])

R> ts

Jan Feb Mar Apr May Jun

1961 453.9091 443.5161 432.8683 422.7560 414.1958 406.3113

Jul Aug Sep Oct Nov Dec

1961 398.7037 391.8506 384.9362 378.4532 372.7470 367.1855

R> predict(fit, n.ahead = 12)

$pred

Jan Feb Mar Apr May Jun

1961 453.9038 443.0989 432.9713 423.4785 414.5809 406.2410

Jul Aug Sep Oct Nov Dec

1961 398.4239 391.0969 384.2292 377.7920 371.7583 366.1029

5 Source code

arima.condsim <- function(object, x, n.ahead = 1, n = 1){

L <- length(x); coef <- object$coef;

arma <- object$arma; model <- object$model;

p <- length(model$phi); q <- length(model$theta)Ψ

d <- arma[6]; s.period <- arma[5];

s.diff <- arma[7]

ΨΨ

if(s.diff > 0 && d > 0){

diff.xi <- 0;

dx <- diff(data, lag = s.period, differences=s.diff)

diff.xi[1] <- dx[length(dx) - d + 1];

dx <- diff(dx, differences = d)

diff.xi <- c(diff.xi[1], data[(L - s.diff * s.period + 1):L])

}else if(s.diff > 0){

dx <- diff(data, lag = s.period, differences = s.diff)Ψ

diff.xi <- data[(L - s.diff * s.period + 1):L]Ψ

}else if(d > 0){

dx <- diff(data, differences = d);

diff.xi <- data[(L - d + 1):L]Ψ ΨΨΨ

}else{dx <- data}

use.constant <- is.element("intercept", names(coef))

mu <- 0Ψ

if(use.constant){

mu <- coef[sum(arma[1:4]) + 1][[1]] * (1 - sum(model$phi))Ψ

}

p.startIndex <- length(dx) - p

start.innov <- NULL

if(q > 0){

start.innov <- residuals(object)[(L - q + 1):(L)]

}Ψ

res <- array(0, c(n.ahead, n))

for(r in 1:n){

innov = rnorm(n.ahead, sd = sqrt(object$sigma2))

if(q > 0){

e <- c(start.innov, innov)

}else{e <- innov}

xc <- array(0, dim = p + n.ahead)

if(p != 0) for(i in 1:p) xc[i] <- dx[[p.startIndex + i]]

k <- 1

for(i in (p + 1):(p + n.ahead)){

xc[i] <- e[q + k]ΨΨΨ

if(q != 0)

xc[i] <- xc[i] + sum(model$theta * e[(q + k - 1):k]) ΨΨΨ

if(p != 0)

xc[i] <- xc[i] + sum(model$phi * xc[(i - 1):(i - p)])

if(use.constant)

xc[i] <- xc[i] + mu

k <- k + 1

}Ψ

xc <- as.vector(unlist(xc[(p + 1):(p + n.ahead)]))

if((d > 0) && (s.diff > 0)){

xc <- diffinv(xc, differences = d, xi = diff.xi[1])[-c(1:d)]

xc <- diffinv(xc, lag = s.period, differences = s.diff,

xi = diff.xi[2:(s.diff * s.period + 1)])

xc <- xc[-(1:(s.diff * s.period))]ΨΨ

}else if(s.diff > 0) {

xc <- diffinv(xc, lag = s.period, differences = s.diff,

xi = diff.xi[1:(s.diff * s.period)])

xc <- xc[-(1:(s.diff * s.period))]ΨΨΨΨ

}else if(d > 0){

xc <- diffinv(xc, differences = d, xi = diff.xi)[-c(1:d)]

}

res[, r] <- xc

}

res

}

6 Discussion

We have demonstrated that, using a SARIMA model, it is not difficult to simulate from the conditional distribution of future observations. Our code can thus be used to randomly generate possible future continuations of a time series. The identification of a suitable SARIMA model is an important step in the procedure we suggest; due to the nature of this short note we have to refer the reader to the vast literature on time series analysis for this task; an important point in the modeling procedure are also checks for the model assumption. Especially the normal assumption for the error term has an important impact on the simulated future observations.

Despite these important limitations, that are present in all parametric statistical models, we hope that our simple algorithm will be useful for many applications. This seems likely as we were not able to find any suggestions for a similar algorithm in the literature.

References

- Box and Jenkins [1976] Box G, Jenkins G (1976). Time Series Analysis: Forecasting and Control. San Francisco: Holden Day.

- Hyndman [2009] Hyndman RJ (2009). fma: Data Sets from Forecasting: Methods and Applications by Makridakis, Wheelwright & Hyndman (1998). R package version 2.00, http://www.robjhyndman.com/software/fma/.

- Hyndman [2011] Hyndman RJ (2011). forecast: Forecasting Functions for Time Series,. R package version 2.19, http://robjhyndman.com/software/forecast/.

- Hyndman and Khandakar [2008] Hyndman RJ, Khandakar Y (2008). “Automatic Time Series Forecasting: The forecast Package for R.” Journal of Statistical Software, 27, 1–22.

- Montgomery et al. [2008] Montgomery DC, Jennings CL, Kulahci M (2008). Introduction to Time Series Analysis and Forecasting. John Wiley and Sons, New Jersey.

- R Development Core Team [2011] R Development Core Team (2011). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, http://www.R-project.org.