Generalizations of Functionally Generated Portfolios with Applications to Statistical Arbitrage

Abstract

The theory of functionally generated portfolios (FGPs) is an aspect of the continuous-time, continuous-path Stochastic Portfolio Theory of Robert Fernholz. FGPs have been formulated to yield a master equation - a description of their return relative to a passive (buy-and-hold) benchmark portfolio serving as the numéraire. This description has proven to be analytically very useful, as it is both pathwise and free of stochastic integrals. Here we generalize the class of FGPs in several ways: (1) the numéraire may be any strictly positive wealth process, not necessarily the market portfolio or even a passive portfolio; (2) generating functions may be stochastically dynamic, adjusting to changing market conditions through an auxiliary continuous-path stochastic argument of finite variation. These generalizations do not forfeit the important tractability properties of the associated master equation. We show how these generalizations can be usefully applied to scenario analysis, statistical arbitrage, portfolio risk immunization, and the theory of mirror portfolios.

ETH Zürich, Department of Mathematics

CH-8092 Zürich, Switzerland

winslow.strong@math.ethz.ch

Keywords: Stochastic Portfolio Theory, functionally generated portfolio, statistical arbitrage, portfolio theory, portfolio immunization, mirror portfolio, master equation

Mathematics Subject Classification: 91G10 60H30

JEL Classification: G11 C60

1 Introduction and background

Functionally generated portfolios (FGPs) were introduced by Robert Fernholz in [5, 7], see also [8, 10]. They have historically been constructed by selecting a deterministic generating function that takes the market portfolio as its argument. They are notable for admitting a description of their performance, relative to a passive (buy-and-hold) numéraire, that is both pathwise and free of stochastic integrals. This description is known as the master equation, and is a useful tool for portfolio analysis and optimization.

In markets that are uniformly elliptic and diverse [11], and more generally those markets with sufficient intrinsic volatility [9], FGPs yield explicit portfolios that are arbitrages relative to the market portfolio (although see [18] for an alternative diverse market model that is compatible with no-arbitrage). In more general equity market models, FGPs are useful for exploiting certain statistical regularities, such as the stability of the distribution of capital over time [8, 10], and the non-constancy of the rate of variance of log-prices as a function of sampling interval [12]. These FGP-derived portfolios are best described as statistical arbitrages [12], since they exploit the aforementioned statistical regularities in the data to achieve favorable risk-return profiles. One of the main attractions of the techniques presented in this paper will undoubtedly be towards characterizing and optimizing such statistical arbitrage portfolios.

This paper is organized as follows: Section 2 defines a market model typical of those used in Stochastic Portfolio Theory. Section 3 extends the class of FGPs from its historical definition by allowing an arbitrary wealth process to serve as numéraire, rather than restricting it to be the market portfolio or a more general passive portfolio. Generating functions are also extended to accommodate continuous-path auxiliary stochastic arguments of finite variation. Section 3.2 highlights the usefulness of FGPs for scenario analysis. Sections 3.3 and 3.4 provide some characterization of equivalence classes of FGPs in general, and in the case of passive numéraires, respectively. Section 4 explores two approaches of applying FGPs to statistical arbitrage: extending the original idea from [12] and using a new construction based on quadratic generating functions. Section 5 presents a method of immunizing a given FGP from certain market risks, while keeping it in the family of FGPs. Section 6 extends the notion of mirror portfolios introduced in [11] and analyzes their asymptotic behavior. Section 7 summarizes the results, and poses some remaining challenges to tackle for the theory of FGPs.

2 Setting and definitions

The market consists of processes with prices , one of which may be a money market account. lives on a filtered probability space , which supports a -dimensional Brownian motion , where . All processes introduced are assumed to be progressive with respect to , which may be strictly bigger than the Brownian filtration.

Most of the analysis herein will take place on log prices . The dynamics of are given by

where and are -progressive and satisfy

and takes values in , , . Throughout, all equalities hold merely almost surely. The notation is used, where the dimensionality should be clear from the context.

Definition 2.1.

A portfolio on is an -progressively measurable -valued process satisfying

| (2.1) | ||||

The wealth process arising from investment according to is given by

The process is called the excess growth rate, and plays an important role in Stochastic Portfolio Theory [8, 10]. To ease notation, we will use and often omit the subscript “” when referring to processes.

Remark 2.2.

There is no need for to be restricted to be the directly tradeable assets of a market. Some components may also be wealth processes of portfolios on the tradeable assets, e.g. , where is a portfolio on the tradeable assets. A weighting of in is equivalent to (additional) weights of in the tradeable assets (beyond what already explicitly specifies for those assets). This flexibility may seem needlessly confusing, but it is useful when portfolios are constructed with consideration to certain market segments - e.g. value, growth, large/small cap, sectors, countries, etc. It’s also used in Section 4 below. Distinguishing between the directly tradeable assets and portfolios assembled on them can be important if and when transaction costs and liquidity constraints are taken into consideration, as turnover and leverage may be vastly different. Those issues are beyond the scope of this paper.

The following notation will prove useful:

| (2.2) | ||||

The numéraire invariance property of holds for arbitrary portfolios and :

| (2.3) |

3 Generalizations of functionally generated portfolios

Functionally generated portfolios were first introduced in [5, 7], see also [8, 10], and the recent extension [15]. There are two generalizations presented here:

-

(i)

The numéraire in the master equation may be arbitrary. Previously, it had been taken to be the market portfolio or some other passive (buy-and-hold) portfolio.

-

(ii)

Generating functions may take stochastic arguments, which here we limit to finite-variation processes.

3.1 Stochastic generating functions and arbitrary numéraires

It is natural to adjust a portfolio based on changing market conditions. However, FGPs adjust their weights only as a deterministic function of the underlying discounted price process , which doesn’t allow for much flexibility. Ideally, one would like to be able to modify the generating function stochastically while preserving a useful pathwise description of relative return that is free from stochastic integrals. As a step in this direction, time-dependent generating functions have already been introduced in [8]. In this section we extend that idea to allow a dependence on auxiliary stochastic processes of finite variation.

With respect to the historical work on portfolio generating functions, we formulate them here in the log sense with logarithmic argument. Specifically, our generating function is related to the previous notion of generating function by . This makes the analysis cleaner for our purposes.

For , let be the gradient with respect to the first (-dim) argument of , be the gradient with respect to the second (-dim) argument, and , be the second-order differential operator with respect to components and of the first argument of , and generally, respectively.

Theorem 3.1.

Let and let be an -valued, -progressive, continuous-path process of finite variation. Then the portfolio

| (3.1) |

satisfies the following master equation:

| (3.2) | ||||

When the argument is not present (or constant), then it may be suppressed. Hence

| (3.3) |

satisfies the following master equation:

| (3.4) | ||||

| (3.5) |

Remark 3.2.

Except for the change to the log representation, the derivation proceeds analogously to the original master equation [5, Theorem 3.1], which can also be found in [7, 10]. The intermediate equations in the earlier derivations are each generalizable to our setting, shown here as Lemmas 3.3 and 3.4. In the special (original) case where is the total capitalization (shares price per share), then normalizing by the initial values so that the #shares of each asset is and choosing to be the market portfolio results in

| (3.6) |

Inserting and this into (3.4) recovers the original master equation. However, in the general setting of this paper, is arbitrary, making and distinct.

The following two lemmas will be used in the proof of Theorem 3.1.

Lemma 3.3.

For any two portfolios and , the following hold

| (3.7) | ||||

| (3.8) |

Proof.

Lemma 3.4.

For any portfolio on ,

Now we prove Theorem 3.1.

Proof of Theorem 3.1.

Initially, consider the case where , and hence the second argument to may be suppressed. First plug in (3.3) for into (3.7), and then get (3.9) by applying Lemma 3.4:

| (3.9) |

where is the first derivative operator with respect to the th component. Expanding gives

Plugging this into (3.9) yields

| (3.10) |

proving the case when . For a finite variation with continuous paths, the Itô-Doeblin formula yields

which when combined with (3.10) proves the theorem. ∎

While adding an auxiliary stochastic process causes FGPs to lose some elegance and tractability (comparing (3.4) to (3.2)), the extra flexibility gained can be useful in practice. For example, may be factors that inform portfolio construction, such as those of Fama and French [3, 4], fundamental economic data such as bond yields or stock market diversity [6, 8, 11, 10], or information extracted from Twitter feeds [2].

Remark 3.5 (Generalizations).

It’s possible to remove the restrictions on - that it’s finite variation and has continuous paths - to derive a more general master equation, but this would make the correction term of (3.2) more complex. A continuous of finite variation is sufficient for the applications that follow, so we do not pursue these extensions here.

If a portfolio satisfies (3.4) in place of , then must be indistinguishable from . Hence, any differences between and are not meaningful in the context of wealth-creation. However, there are portfolios obeying generalizations of the master equation for which , such as the class presented in Theorem 4.1 of [16].

The following example looks at the strategy of switching from an initial FGP to a subsequent one at a stopping time. The overall portfolio is an example of a stochastic FGP.

Example 3.6 (Stochastic switching between FGPs111The author wishes to thank Radka Pickova for suggesting this idea.).

Let and be arbitrary generating functions and let be

For an arbitrary stopping time is a stochastic generating function (i.e. a function meeting the requirements of Theorem 3.1 with auxiliary ) which will generate an FGP that switches at from generated by to generated by . This type of portfolio was used by Banner and D. Fernholz in [1] for constructing arbitrages relative to the market portfolio at arbitrarily short deterministic horizons in a class of market models including volatility-stabilized markets [9]. Those models have also been shown to admit functionally generated relative arbitrage over sufficiently long time horizons [9]. However, there is a horizon before which functionally generated relative arbitrage is not possible, regardless of the choice of generating function [19]. This example shows that relative arbitrages exist on arbitrarily short horizons within the class of FGPs that have stochastic generating functions.

3.2 Pathwise returns for scenario analysis

One of the main analytical benefits of the master equation is that it is free of stochastic integrals. When formulas for portfolio returns contain stochastic integrals, then correct analysis may be counterintuitive, and incorrect analysis may be intuitively appealing, as the following example demonstrates.

Example 3.7.

Consider two portfolios on horizons : Let be a long-only constant-weight portfolio so that , , and let be a passive (buy-and-hold) portfolio starting from the same initial allocation . Consider the set . In some models for , (e.g. geometric Brownian motion), , . Recalling that the usual description of the wealth process of an arbitrary portfolio is

| (3.11) |

then we may write

If and are bounded, then it is tempting to make the erroneous conclusion that

| (3.12) |

The erroneous conclusion might be stated in words as:

If two portfolios remain sufficiently close to each other, then their returns must be close.

The erroneous conclusion can be avoided by noting that and are functionally generated by generating functions , and , respectively, where . Comparing their wealth processes via their master equations gives the pathwise equation

| (3.13) |

If the covariance is uniformly elliptic (there exists such that for all , ), and if , , then , [10, Lemma 3.4]. For all there exists such that on . Hence, (3.13) and the continuity of and imply that

contradicting (3.12). This correct conclusion is simply obtainable from the pathwise representation of return given by the master equation, but is difficult to arrive at from the traditional representation of return given in (3.11). The upshot is that

Just because two portfolios remain arbitrarily close does not imply that their returns are close.

More generally, the master-equation description of relative return (3.4) has advantages over the usual description (3.11) for scenario analysis, a technique currently popular in investment management (e.g. see [14]). In the short term, an FGP’s performance (particularly its potential for loss) is largely attributable to the first term of (3.4), which is entirely determined by the terminal values of the underlying assets, which themselves are outputs of scenario analysis. Whereas the last term involves the quadratic variation of the path, and is usually easier to estimate with high precision. In contrast, knowledge of the terminal values of the assets is difficult to use in the Itô-integral formulation (3.11).

3.3 Translation equivariance and numéraire invariance

Generating functions are overspecified in the following sense. Given a generating function , each member of the equivalence class of generating functions

| (3.14) |

yields the same function . Hence, given an arbitrary market and numéraire , any member of yields the same functionally generated portfolio (3.3).

Definition 3.8.

is translation equivariant if

When is translation equivariant, then and hence its corresponding FGP depend only on the relative rather than absolute price level. An example of a class of translation-equivariant generating functions is the diversity- family (see [8, 10]):

The following is an invariance property of the master equation when is translation equivariant.

Proposition 3.9.

Proof.

Starting with (3.4), we show that when is translation equivariant, then of (3.3) is identically :

Next, we show that may be formally replaced with in (3.5). We note that

Using this and the form (2.2) for yields

Reversing the steps shows that may be replaced with for arbitrary .

It remains to show that may be replaced with as the argument to :

Since , this implies that

| ∎ |

Remark 3.10.

An FGP can be thought of as a -hedge for its generating function, as it eliminates stochastic integrals from . Under this interpretation, is the position taken in the numéraire with the leftover money in the portfolio. The numéraire sets a stochastic relative price level for and in the master equation. When is translation equivariant, then the corresponding FGP and wealth process have no sensitivity to the price level, as can be seen by Proposition 3.9 and

which simplifies (3.15) to

| (3.17) |

Generally, each choice of numéraire results in a unique master equation. But when is translation equivariant, then there’s no excess exposure to the numéraire (beyond what’s needed to -hedge ), making the master equations arising from different numéraire choices trivial translations of the same one equation (3.17).

3.4 Passive numéraires and gauge freedom

The historical work on FGPs [5, 7, 8, 10] takes as the total capitalizations and the numéraire as the market portfolio, leading to (see 3.6), as in Remark 3.2. The important property of the market portfolio that was exploited in those works was its passivity on (see Definition 3.11). In the traditional case, the equality of and means that , hence the generating function need not be defined on all of . In this section we explore more generally to what extent a passive numéraire allows a reduction of the domain of the generating function.

Definition 3.11.

A portfolio is passive if there exists a constant , called the shares, such that

Passive portfolios are untraded after the initial allocation, so are unaffected by transaction costs and other liquidity concerns. Generally, the are unbounded from above, so in order that is guaranteed, we assume henceforth that any passive portfolio is long-only. That is, that .

When the numéraire is passive, then a generating function need not be defined on all of , as will be confined to a hyperplane. Let be the constant vector of shares such that . Then,

Thus, is confined to a hyperplane of codimension , and it should be sufficient to define on

However, Theorem 3.1 uses the Cartesian coordinate system, which is quite convenient, so we sacrifice some generality and require generating functions to be defined on a neighborhood in containing .

Definition 3.12.

Let and let the passive portfolio be given by , . A -generating function is a function , where is a neighborhood in containing .

When is the market portfolio and is the total capitalization, then . In [8, Proposition 3.1.14], where generating functions are specified as , the following equivalence is demonstrated: Generating functions and generate the same portfolio if and only if is constant on . This generalizes to general passive portfolios as follows.

Proposition 3.13.

Let be passive with corresponding shares . Let and be two -generating functions defined on a neighborhood containing . Then and generate the same portfolio for any realization of if and only if is constant on .

Proof.

Let be the portfolio generated by , . The condition , for all realizations of is equivalent by (3.3) to the following holding :

| (3.18) |

Differentiating the equation determining the surface shows that (3.18) is equivalent to being orthogonal to , hence equivalent to being constant on . Conversely, if is constant on , then (3.18) holds. Since by definition , then from (3.3) . But is long-only, and . Thus . ∎

The gauge freedom implied by Proposition 3.13, specifically by (3.18), is that if generates , then

also generates , for any . This gauge freedom allows one to make any convenient choice for in order to simplify calculations. The -generating functions and general generating functions have their associated respective equivalence classes:

Each member of a given or is equivalent for the purposes of -FGPs, or generally FGPs, respectively.

4 Statistical arbitrage

4.1 Long-short statistical arbitrage with FGPs

The paper [12] of R. Fernholz and C. Maguire introduces an idea for a statistical arbitrage strategy in markets where the realized rate of variance of log market prices depends on the sampling interval. The general idea is to take a long position in an FGP that is rebalanced over a time interval corresponding to a high variance rate, hedged with a short position in an FGP generated from the same generating function, but rebalanced over a different time interval corresponding to a low variance rate. Statistical arbitrage profits accrue from the different rates of variance-capture (the of (3.5)) - named so because these terms are directly proportional to the variance rate. Because the long and short FGPs have the same generating function, their corresponding terms of (3.4) are identical, providing an effective hedge for each other.

The data presented in [12] indicate that for , the variance rate was significantly higher at higher sampling frequencies intradaily for large-cap US equities. The authors looked at rebalancing the long component at -second intervals and rebalancing the short component once a day. These choices of rebalancing intervals were ad hoc, not the output of an optimization problem. In this section we develop general performance formulas for such long-short statistical arbitrages, creating a framework for optimizing the selection of generating function and rebalancing intervals.

We will show that the growth rate of the statistical arbitrage portfolio always has the quadratic form

| (4.1) |

where is the leverage factor, that is, the weight invested in the long portfolio. Hence, there is a level of leverage above which the portfolio tends to shrink in value rather than grow. The leverage gives the maximal growth rate of .

To estimate the performance of the strategy described in [12], we use , where is the money market, and are the risky assets that are directly tradeable on the market (e.g. the equities). and are the values of long-only portfolios on . The statistical arbitrage portfolio is an FGP specified on the submarket (for more detail, see Remark 2.2). In [12] constant-weight FGPs are considered, where the overall portfolio has , and . This portfolio is functionally generated by the generating function , so (3.4) yields

The statistical arbitrage construction uses and as discretely-traded approximations to the same (continuously traded) FGP, starting from . The portfolios differ only in their rebalancing interval. Their values are approximated with the master equation, as if they were continuously-traded. This approximation has been shown empirically to be accurate for diversity- and entropy-weighted FGP approximations that are rebalanced merely once a month [8, Chapter 6]. and have the same generating functions, , so under this approximation their values differ only through their variance-capture terms, and , which differ only because rebalancing occurs at different intervals, and hence different effective variance-rates may (and do in practice) apply. The resulting approximation is

| (4.2) |

The overall portfolio is a constant-weight FGP, hence has from (3.4). Therefore,

This has the quadratic form of (4.1). To estimate the parameters, we approximate the stochastic quantities as constants, and plug in the values of their sample estimators. We can identify

In [12] the FGP chosen to give the value processes and was the equal-weight portfolio on large cap US equities, specifically those in the S&P500 and/or Russell 1000 in 2005. The annualized sample averages for that year were , , , , .222These are the numbers from [12], after transforming standard deviations to variances and annualizing all numbers: , , , , . These result in , , , and (base ).

While is not of the order of magnitude usually seen in portfolio construction, it must be remembered that it is not a weight for investment into equities, but rather into a long-short combination of two very diverse portfolios that are very similar nearly always. At the beginning of each day, the long and short portfolios are equal, so the net position in each equity starts at 0. Each FGP is an equal-weight portfolio in about 1000 equities. If we approximate each initial weight as and use a leverage factor of , then an isolated intraday price movement of a particular equity induces a change in net weight of in that equity. While this is still an unrealistically leveraged portfolio, it is much closer to a reasonable order of magnitude considering that it would be offset by similarly sized positions of opposite sign.

Despite the above remark, the amount of leverage involved in the portfolio is prohibitive due to the realities of equity markets that lie outside of the framework of this paper, such as price jumps, margin requirements, transaction costs, short-selling fees, liquidity constraints, etc. It is these factors then that become the limiting ones for the level of leverage to use in seeking profitability from a statistical arbitrage portfolio of this type. A more plausible level of leverage of results in , still orders of magnitude outside the realm of documented performance.

4.2 Quadratic generating functions

This section again considers a market whose log asset prices have a variance rate varying with the sampling interval (e.g. Figure 1). Taylor expanding the generating function term in the master equation (3.4) yields

| (4.3) | ||||

and is the remainder term. For a given path , there is a sufficiently short time horizon such that an FGP generated by an analytic behaves nearly as if it were generated by a quadratic :

| (4.4) | ||||

Since statistical arbitrage portfolios are generally rebalanced quite frequently (intradaily), the above motivates consideration of FGPs having quadratic for application in statistical arbitrage. We assume that the investor has no information, or at least does not wish to speculate, on the drifts of . If this is the case, then it makes no sense for him to take on unnecessary exposure to the term in (4.3). This term can be eliminated by selecting an satisfying .

To accomplish this initial hedge, take and in (4.4). Then

For simplicity in illustrating the idea, we restrict the investment to one risky asset (possibly a wealth process of a more general portfolio, as in the previous section) and one locally risk-free asset, i.e. a money market account, which will be the numéraire. The procedure is readily generalizable to a bigger market, with the cost being solving and optimizing vector instead of scalar equations. In this setting , , and . Since the money market discounted with itself has value one for all time, then only need be prescribed on the risky discounted asset’s log price, , and hence is a scalar. The log wealth is

| (4.5) |

To proceed, we take an expectation, assume Brownian integrals are martingales, and approximate some time-dependent parameters as constants. This simplifies the model, allowing for easy fitting to data:

Note: is best interpreted as at the at which trading actually occurs. Using the above in (4.5) yields

| (4.6) | ||||

By assumption, is not identically . If its deviation from is not substantially greater than for some , then our exposure to results in large risk for little gain. In any case, we are ignorant of the drift, so we drop it and are left with

All that is needed is the variogram for , from which the other quantities are easily derived. The that maximizes the expected log growth by horizon is

This yields a maximal expected log-growth rate of

| (4.7) |

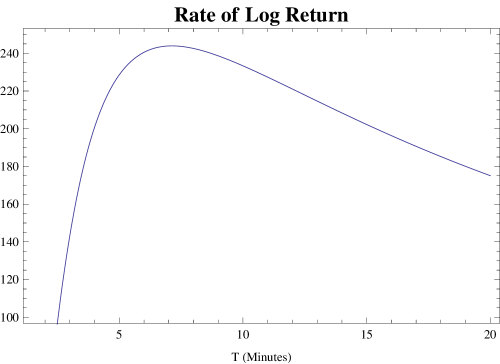

Empirically, the quantity tends to a constant for large , thus for . This means that the growth rate tends to as . The question then arises of what the optimal period is for restarting this strategy. This can be obtained by maximizing (4.7) as a function of .

Conjecture 4.1.

Rather than restarting the portfolio after a given time period, it may be better to solve an optimal control problem, restarting when the price of the risky asset wanders sufficiently far from its origin.

A positive feature of both the methodologies of Section 4 is that they are entirely data-driven, and depend only on variance measurements, which can be estimated in practice with high precision. Of course if the data suggests a parametric model, then the added structure could be additionally exploited.

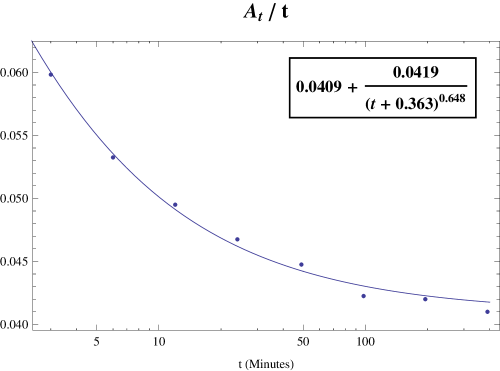

Example 4.2.

We apply a quadratic generating function to the data from [12], i.e. of an equal-weight portfolio on large cap US equities in 2005. The variogram (Figure 1) is fitted to

The form was chosen for fitting fairly well and also because has a closed-form antiderivative, yielding

Assuming, as in Section 4.1, that our (fastest) rebalancing frequency is minutes, then effectively (annualized). From (4.7) we numerically obtain minutes, leading to , and a maximal rate of log return of (base , per year). This is an order of magnitude lower than obtained from the same data via the methodology in Section 4.1. This may be explained by the approximation made in (4.2) breaking down under substantial leverage. Another factor may be that our dropping the drift term of (4.6) underestimates the return of the quadratic FGP: Since , then conditioned on a price movement, a large drift in the opposite direction is typical, which the portfolio implicitly bets on.

5 Portfolio immunization

Suppose that we have selected a generating function that is appealing, except that it produces a generated portfolio that is exposed, relative to the numéraire, to risk factors that we would rather remain unexposed to. For example, we may wish to avoid taking on numéraire risk by maintaining zero excess exposure to it.

One way to remove unwanted risk exposure is to modify the initial generating function, only in so far as to make it invariant to changes in the argument along the direction of given risk factors. To be more concrete, suppose that is the initial generating function, and that are each continuous-path finite variation processes in satisfying

The orthonormal set of random vectors spans the subspace in that we would like to immunize the generated portfolio’s performance to at time . That is, we would like to find a generating function , similar to , except also obeying

For this to hold, will need to be stochastic, via taking as a second argument. Perhaps the most natural way to modify in order to achieve this is to project onto the complement of the span of and allow that to determine the new function . To that end, let be the projection operator that projects onto the orthogonal complement of the span of vectors . It is simplest to specify in the case where are orthonormal:

Proposition 5.1.

Let be finite variation processes in that are mutually orthonormal at all times. The generating function and generated portfolio

satisfy the following master equation:

where

Proof.

Define

The result is then obtained from a direct application of Theorem 3.1 to . The relevant derivatives are

| ∎ |

The characterization of the performance of the immunized FGP given by Proposition 5.1 is not so pretty, but the idea of what has changed from the non-immunized FGP is straightforward. The relative wealth process of the generated portfolio of Proposition 5.1 is locally not exposed to changes in along the linear span of . This can be seen from

Example 5.2 (Numéraire exposure).

Consider the case where immunization is desired with respect to relative exposure to the numéraire. The appropriate to use to hedge against excess numéraire exposure is less than the “CAPM ” (see e.g. [17]). The instantaneous version of this parameter is

Although theoretically this instantaneous may not be a continuous-path finite variation process, in practice the instantaneous is not observable, and is typically estimated by time-averaging over some historical time window. The practical and theoretical result of such a time-averaging procedure is a continuous-path finite variation process. For example, the estimator might have the theoretical form

for some . In practice the integrals are approximated by sums of discretely sampled values.

Example 5.3 (Price level).

Another possibly desirable immunization is to hedge out any exposure to a rise or fall in the overall price level. This can be done by choosing the constant vector .

6 Mirror portfolios

In this section we use generating functions to elaborate some of the properties of mirror portfolios, introduced in [11]. In that paper, mirror portfolios were used to construct arbitrages over arbitrarily short time horizons in markets that are both diverse and uniformly elliptic. A passive portfolio that is short any asset is typically inadmissible, due to each asset’s price usually being unbounded from above. Hence, flipping the sign of the shares invested in assets (while adjusting the weight in the numéraire so that weights sum to one) does not in general produce a suitable notion of a reflected portfolio. Mirror portfolios accomplish that task.

Definition 6.1.

If and are portfolios, then the portfolio

is called the -mirror of with respect to . When is fully invested in the money market, then , abbreviated the -mirror of . For , , called simply the mirror of with respect to .

For portfolios and , the -mirror of with respect to satisfies (2.1), so is also a portfolio. As an example, if is the money market, then the portfolio has the mirror .

Proposition 6.2.

The -mirror of with respect to is functionally generated from the market by the generating function , and thus satisfies

If, additionally, is the money market, then

If, additionally, , then

| (6.1) |

Proof.

is translation equivariant and , so we may apply Proposition 3.9 to obtain the first result. The others are easy consequences of plugging in when is the money market. ∎

The following corollary shows that under typical market conditions a given portfolio or its mirror or both will lose all wealth, asymptotically.

Corollary 6.3.

Suppose that both of the following hold:

-

(i)

(6.2) -

(ii)

(6.3)

Then

Proof.

Equation (6.1) shows that at least one and possibly both of and have negative drift at any time when is increasing. The preceding corollary shows that a portfolio, its mirror, or possibly both, lose all wealth relative to the money market asymptotically, assuming that the asymptotic local variance rate does not approach 0. A portfolio whose wealth tends to asymptotically would typically be considered a poor long-term investment. In this sense, “mirroring” a poor investment may still be a poor investment. A concrete example is a market with a risk-free rate of , and one risky asset whose price is a geometric Brownian motion with . Then full investment in the risky asset loses all wealth asymptotically, as does its mirror, which also has drift by (6.1).

7 Concluding remarks

The key analytical benefit of portfolios that are functionally generated is the representation of their return relative to a numéraire via a pathwise master equation free of stochastic integrals. The generalizations of FGPs presented here expand the class of portfolio-numéraire pairs that may be analyzed in this way. The dynamism of FGPs is enhanced by the freedom to incorporate processes having continuous, finite-variation paths as auxiliary arguments to generating functions. This allows FGPs to be sensitive to changing market conditions beyond the price changes of the assets. The main applications that we have shown are (1) direct, intuitive comparison of the performance of FGPs, useful for scenario analysis (Section 3.2), (2) statistical arbitrage based purely on variance data, (3) portfolio immunization, and (4) mirror portfolios analysis.

It is a shortcoming of this work that transaction costs are ignored throughout. They are especially important to the performance of the statistical arbitrage portfolios examined in Section 4. The inclusion of transaction costs in a tractable way for FGPs in -asset markets is a topic of ongoing research. Due to its complexity, it warrants a separate paper that the author hopes will be forthcoming in the future.

References

- [1] Adrian Banner and D. Fernholz. Short-term relative arbitrage in volatility-stabilized markets. Annals of Finance, 4:445–454, 2008.

- [2] J. Bollen, H. Mao, and X. Zeng. Twitter mood predicts the stock market. Journal of Computational Science, 2(1):1–8, 2011.

- [3] F. Eugene and K. French. The cross-section of expected stock returns. Journal of Finance, 47(2):427–465, 1992.

- [4] E.F. Fama and K.R. French. Common risk factors in the returns on stocks and bonds. Journal of financial economics, 33(1):3–56, 1993.

- [5] E. Robert Fernholz. Portfolio generating functions. Technical report, INTECH, 1995. https://ww3.intechjanus.com/Janus/Intech/intech?command=researchListing.

- [6] E. Robert Fernholz. On the diversity of equity markets. Journal of Mathematical Economics, 31:393–417, 1999.

- [7] E. Robert Fernholz. Portfolio generating functions. In Marco Avellaneda, editor, Quantitative Analysis in Financial Markets, pages 344–364. World Scientific, Singapore, 1999.

- [8] E. Robert Fernholz. Stochastic Portfolio Theory. Springer, Berlin, first edition, 2002.

- [9] E. Robert Fernholz and Ioannis Karatzas. Relative arbitrage in volatility-stabilized markets. Annals of Finance, 1:149–177, 2005.

- [10] E. Robert Fernholz and Ioannis Karatzas. Stochastic Portfolio Theory: an overview. In A. Bensoussan and Q. Zhang, editors, Handbook of Numerical Analysis: Volume XV: Mathematical Modeling and Numerical Methods in Finance, pages 89–167. North Holland, Oxford, 2009.

- [11] E. Robert Fernholz, Ioannis Karatzas, and Constantinos Kardaras. Diversity and relative arbitrage in equity markets. Finance and Stochastics, 9:1–27, 2005.

- [12] E.R. Fernholz and C Maguire. The statistics of statistical arbitrage. Financial Analysts Journal, 63:46–52, 2007.

- [13] Ioannis Karatzas and Steven E. Shreve. Brownian Motion and Stochastic Calculus. Springer, Berlin, second edition, 1991.

- [14] J. Mina, J.Y. Xiao, et al. Return to riskmetrics: the evolution of a standard, 2001. New York: RiskMetrics Group.

- [15] Soumik Pal and Ting-Kam Leonard Wong. Energy, entropy, and arbitrage. arXiv preprint arXiv:1308.5376, 2013.

- [16] Olivier Menoukeu Pamen. A general theorem for portfolio generating functions. Communication on Stochastic Analysis, 5(2):271–283, 2011.

- [17] William Sharpe. Portfolio Theory and Capital Markets. McGraw-Hill, 1970.

- [18] Winslow Strong and Jean-Pierre Fouque. Diversity and arbitrage in a regulatory breakup model. Annals of Finance, 7:349–374, 2011.

- [19] Phillip Whitman. Personal Communication.