Approximate Bayesian Computation via Regression Density Estimation

Y. Fan, 111School of Mathematics and Statistics, University of New South Wales, Sydney, 2052, AUSTRALIA D. J. Nott 222Dept. of Statistics and Applied Probability, National University of Singapore, SINGAPORE, 117546 and S. A. Sisson1

Abstract

Approximate Bayesian computation (ABC) methods, which are applicable when the likelihood

is difficult or impossible to calculate, are an active topic of current research. Most current

ABC algorithms directly approximate the posterior distribution, but an alternative, less common strategy

is to approximate the likelihood function. This has several advantages.

First, in some problems, it is easier to approximate the likelihood than to approximate the

posterior. Second, an approximation to the likelihood allows reference analyses to be constructed

based solely on the likelihood. Third, it is straightforward to perform sensitivity analyses for

several different choices of prior once an approximation to the likelihood is constructed, which needs

to be done only once. The contribution of the present paper is to consider regression density estimation techniques

to approximate the likelihood in the ABC setting. Our likelihood approximations

build on recently developed marginal adaptation density estimators by extending them for

conditional density estimation. Our approach facilitates reference Bayesian inference, as well as

frequentist inference. The method is demonstrated via a challenging problem of inference

for stereological extremes, where we perform both frequentist and Bayesian inference.

Keywords: Approximate Bayesian computation; Copulas; Likelihood-free inference; Mutivariate density estimation; Regression density estimation.

1 Introduction

Approximate Bayesian computation (ABC) methods (commonly described as “likelihood-free” methods)

have been attracting increasing research interest as a viable procedure for performing

Bayesian inference in the presence of computationally intractable likelihood functions. Initially popular

in the biological sciences \shortcitebeaumont+zb02,luciani+sjft09,ratmann+jhsrw07,ratmann+ahwr09,

ABC has now found application in a wide range

of areas – see the reviews by \shortciteNbeaumont10, \shortciteNcsillery+bgf10 and \shortciteNsisson+f11

ABC methods require the ability to simulate data from the intractable likelihood,

, for a given parameter vector . An integral part of all

existing algorithms involves

sampling from some distribution (typically the prior, ) and comparing

simulated data with the observed data .

Posterior samples approximately from are then obtained by weighting

according to some weighting function or kernel with scale parameter . Accordingly, samples for which receive larger weights than those where is very different to .

More formally, ABC algorithms produce samples from an augmented posterior distribution

| (1) |

It is easy to see that as , only is given non-trivial weight by , and the ABC posterior converges

to the true posterior distribution, . However, practically

equates to repeated simulation until is matched exactly for each ,

which is computationally impractical in general.

As such, for some , a necessarily approximate posterior is obtained.

Regression-adjustment strategies have been proposed to post-process the approximate posterior samples to

correct the error in the ABC posterior (e.g. \shortciteNPbeaumont+zb02,blum+f09,nott+fms11).

Dimension reduction techniques are also typically used to reduce the overall computational overhead. Here, the vectors, , are replaced by lower-dimensional sufficient or summary statistics, .

Readers should refer to \shortciteNblum12, \shortciteNprangle12 and

\shortciteNrobert11 for further discussion of the use and elicitation of summary statistics in ABC.

In this paper, we present an alternative ABC approach based on constructing a direct approximation to the likelihood.

The approximation is based on samples (not necessarily from the prior), and the corresponding

summaries , simulated from the intractable likelihood.

Such an approach is attractive in several ways. Firstly, it is sometimes easier to approximate the likelihood

than to approximate the posterior directly. Secondly, separate estimation of the likelihood is

useful for performing purely likelihood based analyses, such as maximum likelihood estimation. This may be more attractive to researchers more familiar with frequentist inference.

Thirdly, direct approximation of the likelihood is useful for diagnosing prior-likelihood conflict,

or for running many analyses with different priors in a sensitivity

analysis, as the likelihood approximation only needs to be constructed once.

A further example of a Bayesian use for a separate estimate of the likelihood is the construction

of credible regions based on contours of the likelihood – these have a robust Bayes interpretation in terms of

posterior probability content being minimally sensitive to perturbations of the

prior \shortcitewasserman89. The method we propose here provides an

explicit analytical expression for the likelihood function. It also does not require simulation from the prior, which is typically required by many ABC algorithms (see e.g. \shortciteNPpritchard+spf99,tavare+bgd97,sisson+ft07). This is useful where there is interest in using reference priors.

An early discussion of the concept of directly approximating an intractable

likelihood function using simulated data sets was given by \shortciteNdiggle84, predating

the current wave of activity in ABC research. More recently, several researchers have considered direct likelihood approximations within ABC.

\shortciteNleuenberger+we10

developed an approach that involves embedding the regression adjustment

of \shortciteNbeaumont+zb02 into a likelihood approximation based on a generalised linear model.

\shortciteNwood10 considers a “synthetic likelihood” which involves estimating a normal

distribution for the summary statistics, , with mean and covariance depending on . The approximation of the mean and covariance is performed within

a Markov chain Monte Carlo (MCMC) scheme, and through clever choice of summary statistics and

quantile transformations it may be possible to improve the approximation to normality.

The approach we propose is also related to that introduced by

\shortciteNbonassi11, although this method does not directly approximate the likelihood.

They propose to use mixtures of multivariate normals to estimate a joint distribution for where the summary statistics are simulated from an informative prior, and then condition on the observed summary statistic

in the estimated mixture model. Appropriate localization and choice of summary statistics can

help to improve the efficiency of the approach.

We note that a direct approximation of the likelihood function is available by Monte Carlo integration (e.g. \shortciteNPsisson+pfb08,sisson+f11). If we consider marginalising the distribution of the augmented posterior (1) with respect to the auxiliary data , we then have the marginal posterior

| (2) |

where , are samples from .

The summation term is a simple Monte Carlo estimate of the likelihood of at the point .

Clearly, this estimate is a function of , and so posterior inferences will still require regression-adjustment post-processing. It is also a pointwise estimate, and so it must be effectively re-estimated for each likelihood evaluation in an analysis.

Our approach results in a stand-alone functional expression for the likelihood function at .

However, in the context of this paper, the estimator (2) could usefully serve as a

goodness-of-fit diagnostic.

Our proposed approach to conditional density estimation for ABC (that is, estimating the distribution of given the joint samples )

builds on recent work on flexible multivariate

density estimation – in particular the marginal adaptation method of \shortciteNgiordani+mk09.

The basis of their approach argues that estimation of univariate marginal distributions is easier

than estimating a full multivariate density estimation directly. Hence, a fruitful strategy is to adapt a multivariate

density estimate to have given marginals, which are more precisely estimated individually. In this paper, we develop a strategy for implementing this

approach for the related problem of conditional density estimation, in the context of likelihood estimation in ABC.

2 ABC via multivariate regression density estimation

Our goal is to obtain an estimate of the likelihood , denoted by , and then approximate the intractable posterior distribution by

where denotes the summary statistics from the observed data. Once is obtained, drawing samples from can be achieved by any standard posterior simulation algorithm e.g. Markov chain Monte Carlo.

We assume that the vector of summary statistics, , are given, with and that .

The likelihood estimate is constructed from samples for , where and with . The distribution function determines the region of parameter space in which we require to be a good approximation of .

This must necessarily include the region of high posterior density.

One option, where this is convenient, is to perform an initial pilot ABC analysis with a large value of to broadly identify the high posterior density region, and then define to be proportional to the prior in this region [\citeauthoryearFearnhead and PrangleFearnhead and

Prangle2012].

We first consider flexible estimation of the individual marginal distributions for each . Estimation of marginals is typically easier than estimation of the joint distribution due to the lower dimensionality, and there are many different methods available for this purpose. Here we adopt a mixture of experts approach \shortcitejacobs+jnh91,jordan+ja94. Mixtures of experts models are mixtures of regression models where both parameters in the component response distributions and mixing weights are allowed to vary with covariates. In our case, for each , we express the marginal distribution of as a mixture of normal distributions

| (3) |

where

Here and , for , with for identifiability, and

with and .

For a sufficiently large sample size () and number of components (), the model (3) can approximate the

marginal distribution of arbitrarily well.

Methods for fast and parsimonious fitting of (3) can be found in

\shortciteNnotttvk11 and \shortciteNtrannk12.

For the estimation of the joint dependencies, we propose a mixture of Gaussian copulas approach similar to that proposed by \shortciteNgiordani+mk09 for density estimation. More precisely, for joint samples of we firstly transform the fitted margins of to be standard normal, so that

| (4) |

where , denotes the cumulative distribution function for the fitted density in (3) and denotes the standard normal cumulative distribution function. We then fit a mixture of multivariate normals to the joint samples , and obtain the conditional distribution of in this mixture (see e.g. \shortciteNPnoretsp11). In more detail, the joint density of is modelled via a mixture of multivariate normal distributions

| (5) |

where and denote the mean and covariance matrices of the normal mixture components. The conditional density is then given by

| (6) |

where and are the mean and covariance matrix of the conditional distribution given in the the -th mixture component, . The mixing weights for the conditional distribution, , are

where denotes the marginal density for

in the normal component .

Our density estimator for the likelihood is then given as

| (7) |

where denotes a standard normal density evaluated at .

Note that does not have exactly as it’s marginal distribution, since the marginal distribution for under is not exactly

standard normal, unless .

For this reason, \shortciteNgiordani+mk09 suggest recomputing the distribution of using another normal

mixture, which would lead to replacing with this distribution in (7). This will improve the quality of the likelihood approximation, albeit at additional computational cost. However in our experience we have found that an acceptable approximation is obtained even without enforcing the marginals exactly.

A key component of the above approach is the transformation . If the summary statistics are too highly correlated, or if the dependence between the statistics and the parameters is too complex, it will be difficult to capture the joint distribution of well in a simple mixture model. The primary role of the flexible mixture of experts approach (3) is to construct the transformation to simplify this complexity. However, such modelling can be greatly aided by careful initial selection of summary statistics to achieve near orthogonality and low dependence (e.g. \shortciteNPblum12, \shortciteNPprangle12).

A step by step description of how to of construct is:

The estimate, , can then be used as part of any standard Bayesian or frequentist analysis.

3 Connections with other methods

bonassi11 provide a method to directly estimate the posterior density. A mixture of multivariate normals is used to approximate the joint distribution of based on samples , where the prior must be informative. Conditioning this mixture on then provides an estimate of the posterior. To the best of our knowledge, this is the only approach that directly uses non-parametric conditional density estimation techniques in ABC. Note that alternatively conditioning the mixture approximation of on would result in a mixture of normals conditional density estimate for the likelihood. Similarly, we may derive a direct estimate of the posterior similar to (7) by conditioning on rather than , although the sampling distribution must then equal the prior . Arguments for estimating likelihoods, rather than posterior distributions are provided in the Introduction.

giordani+mk09 discuss the performance of the mixture of multivariate

normals density estimator, and observe that it can be difficult to estimate the

marginals well using this approach.

Our conditional estimator (7) uses a mixture of normals to estimate

the joint distribution of transformed data. The benefit of the transformation is that it is simpler to estimate the joint distribution of than that of . The mixture of normals model also provides greater flexibility over Gaussian copula models which would simply fit a normal distribution to the transformed data.

There are clear benefits in using more flexible density estimation methods. For example, the flexibility in the mixture of experts model (3) to describe the relationship between and , means that good transformations can be constructed for a wide range of vectors drawn from . As such, we can obtain good approximations to for a wide range of as long as the regression models in (3) are adequate and enough samples are available. Clearly, well-chosen summary statistics can also make the modelling easier, especially when they behave nearly linearly with the parameters. See \shortciteNblum12 for a review of dimension reduction methods for ABC.

Finally, we note that if the initial sample is obtained via a pilot ABC analysis with a moderately large kernel scale parameter , then our approach can be viewed as another form of ABC posterior adjustment method. This is in the sense that the initial samples are used to estimate the likelihood at the point , from which (new) samples are subsequently obtained. See e.g. \shortciteNleuenberger+we10 and other regression adjustment postprocessing methods \shortcitebeaumont+zb02,blum+f09,nott+fms11 for further information.

4 Example: Inference for stereological extremes

We now present a reanalysis of a stereological problem studied by \shortciteNbortot+cs07 focusing on the production of clean steels. Here inference is required on the size and intensity of the largest microscopic particle inclusions in a 3-dimensional block of steel, based on inclusion cross sections observed in a 2-dimensional planar slice.

The observed data consist of 112 inclusions intersecting the planar slice, with cross sectional diameters above a measurement threshold of .

We follow \shortciteNbortot+cs07 and consider two models. The first assumes a Poisson process with rate for inclusion centres, and a size distribution for the inclusions, which are assumed to be spherical, based on univariate extreme value theory. Here, conditional on exceeding the threshold, , inclusion sizes are assumed to follow a generalised Pareto distribution with scale and shape parameters and . In this setting it is possible to perform standard Bayesian inference, and so the correct posterior distribution is available. The second model is the same as the first,

but assumes that the inclusions are ellipsoidal. For each model we have .

The analysis of \shortciteNbortot+cs07 took the number of inclusions, and 112 equally spaced quantiles, , as summary statistics. Here, as the quantiles will be highly correlated, we instead use for , where is the log number of inclusions. In order to determine the distribution in regions of non-negligible posterior density, we found it convenient to first draw samples from , where denotes squared Euclidean distance, for a large value of , where is uniform over a moderately large region of parameter space expected to contain the posterior. We then defined

as a truncated normal distribution, where and denote the mean and covariance of the -component of these samples. In this manner, we obtained a final sample of size 5,000 for each model.

In the following, we demonstrate the performance of the regression density estimation methodology using the above summary statistics (corresponding to conditional density estimation in 115 dimensions), as well as the “semi-automatic” summary statistics of \shortciteNprangle12, which provide one summary statistic per parameter (i.e. 6-dimensional density estimation). In addition to standard ABC posterior inference we also perform a prior sensitivity analysis and a maximum-likelihood based inference.

4.1 Results

To fit the mixture of experts marginal distributions (3), we adopted the variational Bayes

approach of \shortciteNnotttvk11 and used the variational lower bound to select the number of mixture components.

For both spherical and ellipsoidal models we found mixture components worked well for each of the 112 summaries, although components were required for the 3 semi-automatic statistics.

Note that the fitting of the marginal models, , is highly parallelizable, and is accordingly suitable for applications in high dimensions.

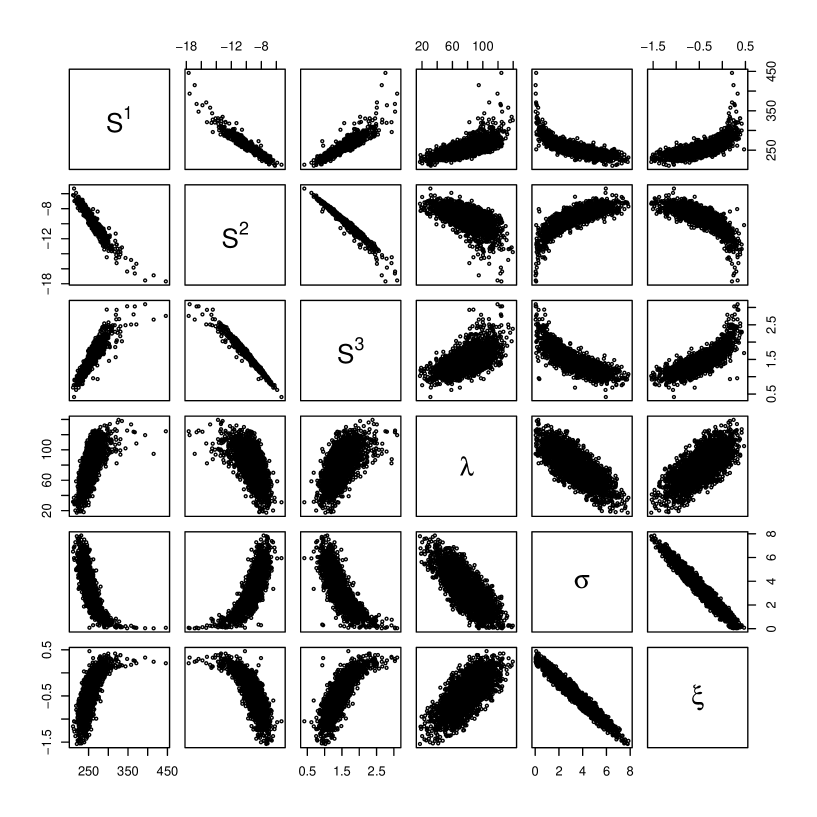

Figure 1

shows the relationship between the parameters and the three semi-automatic summary statistics, as observed in the sample for the ellipsoidal model.

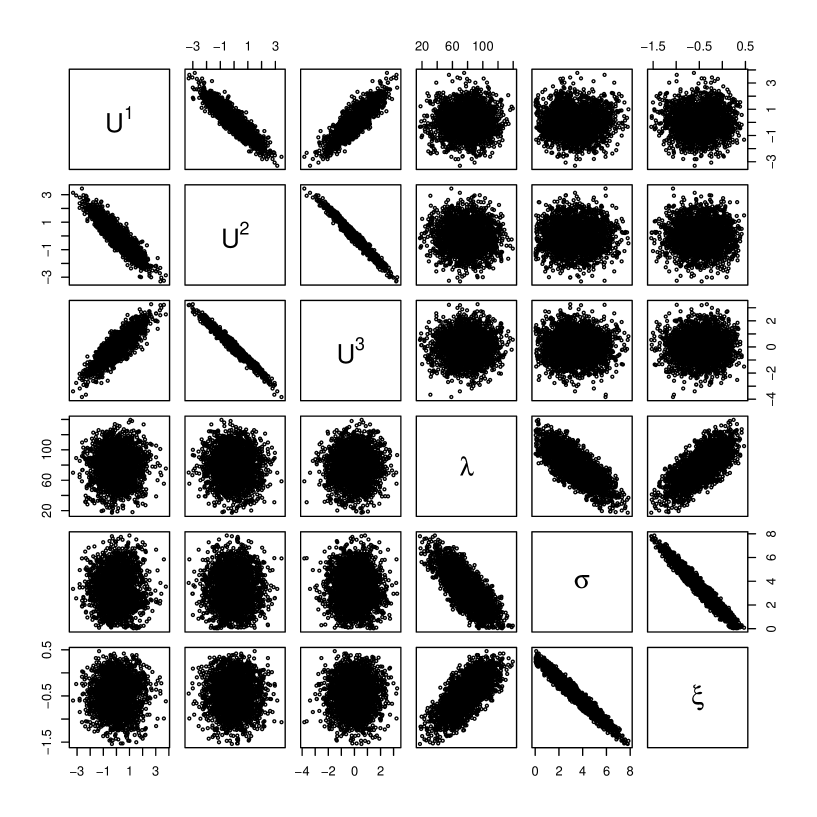

There are visibly strong relationships both within the summary statistic and parameter vectors, and between them. Figure 2 displays the same information following the transformation . Clearly, the transformation has greatly simplified the underlying dependence structure. As a result, while the joint distribution of could be reasonably well modelled by a mixture of multivariate normal distributions (e.g. \shortciteNPbonassi11), a better fit is likely to be obtained by alternatively fitting to .

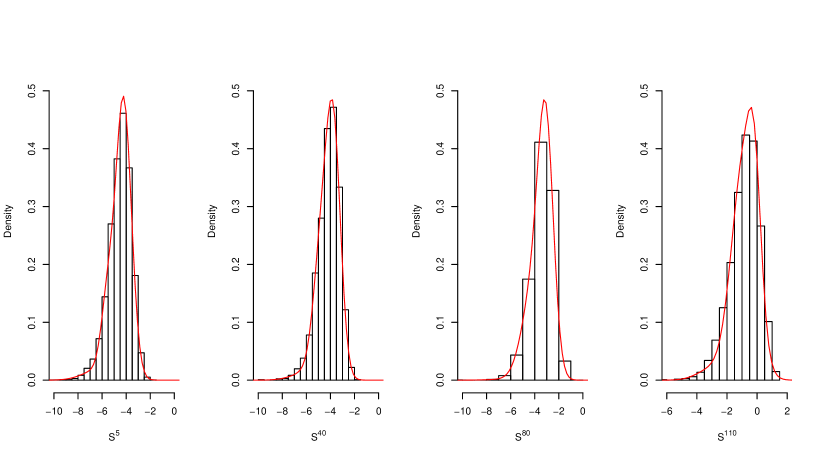

Figure 3 shows the fitted marginal density estimate, , for under the spherical model, evaluated at . The histogram corresponds to the true density, obtained from data generated under the model at the point , and the solid line denotes the fitted density.

The plots indicate a very good fit, and this was typical of all other summary statistics, , and conditioned parameters, , examined.

These results indicate that marginal densities can be very well estimated. Indeed, marginal densities are much easier to estimate in general than joint densities.

We used the R package Mclust to fit the joint distribution (5) to the transformed samples, using mixture components for both spherical and ellipsoidal models.

Model selection for the number of mixture components is typically performed using the BIC. However care should be taken in high dimensions,

as the dimension of can grow quickly, and the BIC tends to overpenalise the number of parameters.

\shortciteNgiordani+mk09 use the variational Bayes approximation method to fit the mixture model,

and advocate the use of the variational lower bound for model selection.

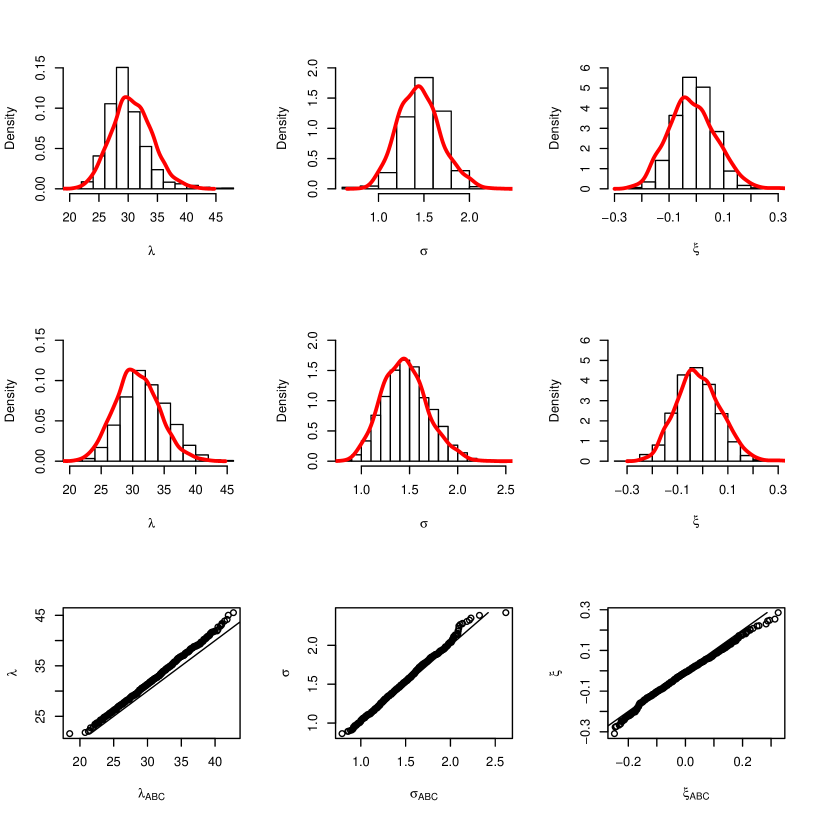

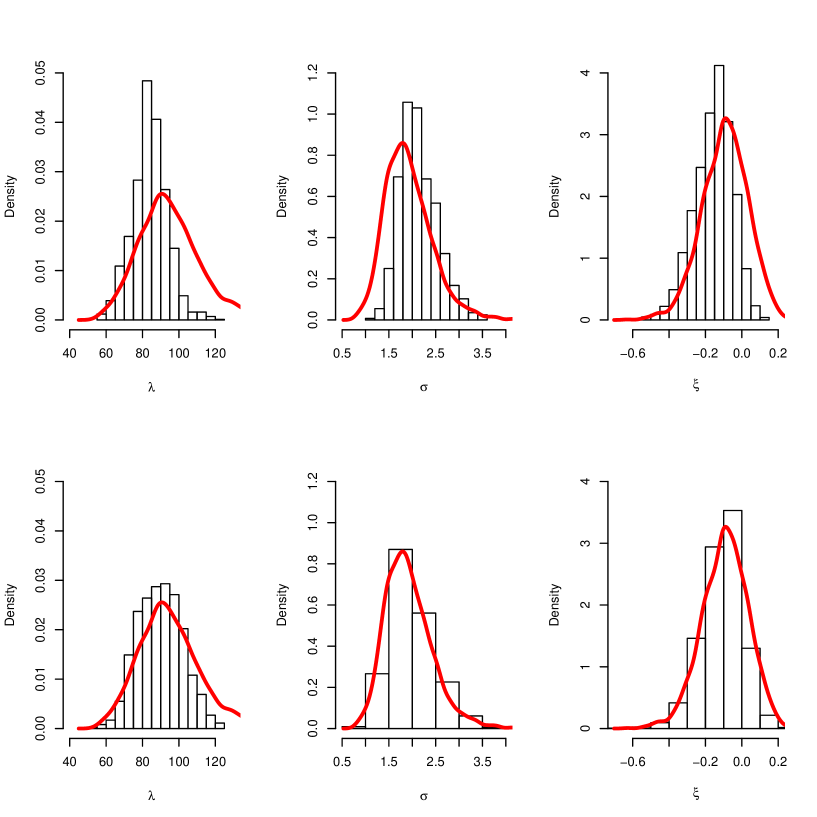

The histograms in Figure 4 shows the regression density estimates of the marginal posteriors for the spherical inclusion model, based on 500,000 MCMC samples, obtained under the prior specification

, and . The top panels are based on using 112 summary statistics, with the middle panels using the 3 semi-automatic summary statistics.

The solid line indicates a density estimate of the true posterior marginal distribution derived from MCMC output using the known likelihood for the spherical inclusions model. The quantile-quantile plots compare the posterior estimated with the semi-automatic statistics with the true marginals.

Even when constructing regression density estimates of the likelihood in 115 dimensions, reasonably good marginal parameter estimates are obtained, although they are clearly not perfect. The estimates improve considerably when only using 3 summary statistics, as the regression density estimation is then performed in only 6 dimensions. Clearly, the regression density approach has worked well, even in high dimensions.

Recall that these approximations are obtained based on flexible modelling with only 5,000 well placed samples (though there are some computational overheads to identify where to place these). This compares favourably with earlier analyses of these data \shortcitebortot+cs07 with the number of simulations in the tens of millions.

The histograms in Figure 5 display the marginal posterior regression density estimates for the ellipsoidal model. Again, the top panels are based on using 112 summary statistics, with the bottom panels using the 3 semi-automatic summary statistics.

The solid lines represent the estimate of the posterior distribution obtained using the MCMC-based ABC method of \shortciteNbortot+cs07 with kernel scale parameter . Under the spherical model, this method is able to correctly reproduce the true posterior for (or lower). \shortciteNbortot+cs07 then assumed that this approach could correctly reproduce the true posterior for the ellipsoidal model, although they were unable to verify their results by reducing further.

From Figure 5, as with the spherical inclusions model, while the marginal posterior distributions under the regression density approach using the 112 summary statistics appear less accurate than when using the semi-automatic statistics, they still have broadly the right shape and location. Of course, because of the lower-dimensional regression density modelling, when using the 3-dimensional semi-automatic statistics, the resulting density estimates are closer to the MCMC-based estimate of \shortciteNbortot+cs07, albeit obtained with a far smaller computational overhead.

In summary, these results appear to broadly support the previous study of the ellipsoidal model by \shortciteNbortot+cs07, although there is some indication that the posterior marginals obtained by \shortciteNbortot+cs07 may be too wide, especially for . This would be consistent with the regression density estimate’s construction at compared with that of for \shortciteNbortot+cs07.

As previously discussed, once the estimate of is obtained, it is then a simple matter to perform a range of likelihood-based inferences that are not immediately available with standard ABC methods.

Table 1 provides numerical estimates of the mean and the 0.025 and 0.975 quantiles of the

marginal posterior for each parameter under various models and analyses, based on the semi-automatic summary statistics.

The estimates denote the maximum likelihood estimates based on , obtained by maximising the analytical expression for the approximate likelihood using the optim function in R.

These frequentist estimates are consistent with their Bayesian counterparts in Table 1 due to the uninformative prior implementation.

The estimates indicate those obtained using the MCMC-based ABC method of \shortciteNbortot+cs07 with kernel scale parameter . These analyses use the 112-dimensional summary statistics. For the spherical model, this ABC posterior is known to coincide with the true posterior, and this is in evidence in the results, although the upper tail for is estimated slightly shorter. As with Figure 5, the marginal posteriors for the \shortciteNbortot+cs07 analysis are wider than those obtained from .

Finally, the estimates correspond to those obtained under the regression density approach for different choices of the prior for , for and . The original analysis of \shortciteNbortot+cs07 with did not incorporate any information about the upper-tail heaviness of inclusion sizes: is physically unlikely, as this would result in extremely heavy tails; is also unlikely as this would result in a very clear maximum inclusion size truncation. It is computationally trivial to implement this prior sensitivity analysis once the estimate has been obtained, in contrast with standard ABC approaches. The sensitivity analysis in Table 1 indicates that the vague prior () does not affect the conclusions, with differences in the posterior only emerging for very strong prior beliefs ().

For both spherical and ellipsoidal inclusion models we additionally constructed a likelihood estimate by simply fitting a mixture of multivariate normals to the samples and then conditioning on . This is equivalent to our regression density approach without the transformation , or the method of \shortciteNbonassi11 but conditioning on to obtain a likelihood, rather than on to produce a posterior. For both models this approach performed reasonably well when the 3 semi-automatic statistics were used (results not shown). However, it became numerically unstable in the 115 dimensional setting. That the regression density approach is numerically stable even in high dimensions indicates the importance of the flexible mixture of experts transformation, , in this setting.

5 Discussion

Approximate Bayesian computation using an estimated likelihood function has many advantages over direct estimation of the posterior. As such, we argue that methods that focus on likelihood construction should be considered an important part of the ABC toolbox. While conditional density estimation in high dimensions is challenging, it is an active area of current research. As the reliability and flexibility of these techniques improve, this will only enhance the value of the likelihood-focused approach to ABC.

References

- [\citeauthoryearBeaumontBeaumont2010] Beaumont, M. A. (2010). Approximate Bayesian computation in evolution and ecology. Annu. Rev. Ecol. Evol. Syst. 41, 379–406.

- [\citeauthoryearBeaumont, Zhang, and BaldingBeaumont et al.2002] Beaumont, M. A., W. Zhang, and D. J. Balding (2002). Approximate Bayesian computation in population genetics. Genetics 162, 2025 – 2035.

- [\citeauthoryearBlum and FrancoisBlum and Francois2010] Blum, M. G. B. and O. Francois (2010). Non-linear regression models for approximate Bayesian computation. Statistics and Computing 1(20), 63 – 73.

- [\citeauthoryearBlum, Numes, Prangle, and SissonBlum et al.2012] Blum, M. G. B., M. A. Numes, D. Prangle, and S. A. Sisson (2012). A comparative review of dimension reduction methods in approximate Bayesian computation. Statistical Science, in press.

- [\citeauthoryearBonassi, You, and WestBonassi et al.2011] Bonassi, F. V., L. You, and M. West (2011). Bayesian learning from marginal data in bionetwork models. Statistical Applications in Genetics and Molecular Biology 10(1).

- [\citeauthoryearBortot, Coles, and SissonBortot et al.2007] Bortot, P., S. G. Coles, and S. A. Sisson (2007). Inference for stereological extremes. Journal of the American Statistical Association 102, 84–92.

- [\citeauthoryearCsilléry, Blum, Gaggiotti, and FrançoisCsilléry et al.2010] Csilléry, K., M. G. B. Blum, F. Gaggiotti, and O. François (2010). Approximate Bayesian computation (ABC) in practice. Trends in Ecology and Evolution (25), 410–418.

- [\citeauthoryearDiggle and GrattonDiggle and Gratton1984] Diggle, P. J. and R. J. Gratton (1984). Monte Carlo methods of inference for implicit statistical models. Journal of the Royal Statistical Society, Series B 46(2), 193 – 227.

- [\citeauthoryearFearnhead and PrangleFearnhead and Prangle2012] Fearnhead, P. and D. Prangle (2012). Constructing summary statistics for approximate Bayesian computation: Semi-automatic approximate Bayesian computation (with discussion). Journal of the Royal Statistical Society, Series B 74(3), 419–474.

- [\citeauthoryearGiordani, Mun, Tran, and KohnGiordani et al.2012] Giordani, P., X. Mun, M.-N. Tran, and R. Kohn (2012). Flexible multivariate density estimation with marginal adaptation. Journal of Computational and Graphical Statistics, in press.

- [\citeauthoryearJacobs, Jordan, Nowlan, and HintonJacobs et al.1991] Jacobs, R., M. Jordan, S. Nowlan, and G. Hinton (1991). Adaptive mixtures of local experts. Neural Computation 3, 79 – 87.

- [\citeauthoryearJordan and JacobsJordan and Jacobs1994] Jordan, M. and R. Jacobs (1994). Adaptive mixtures of local experts. Neural Computation 6, 181 – 214.

- [\citeauthoryearLeuenberger and WegmannLeuenberger and Wegmann2010] Leuenberger, C. and D. Wegmann (2010). Bayesian computation and model selection without likelihoods. Genetics 184, 243 – 252.

- [\citeauthoryearLuciani, Sisson, Jiang, Francis, and TanakaLuciani et al.2009] Luciani, F., S. A. Sisson, H. Jiang, A. Francis, and M. M. Tanaka (2009). The high fitness cost of drug resistance in mycobacterium tuberculosis. Proc. Natl. Acad. Sci. USA 106, 14711–14715.

- [\citeauthoryearNorets and PelenisNorets and Pelenis2012] Norets, A. and J. Pelenis (2012). Bayesian modeling of joint and conditional distributions. Journal of Econometrics 168, 332–346.

- [\citeauthoryearNott, Fan, Marshall, and SissonNott et al.2012] Nott, D. J., Y. Fan, L. Marshall, and S. A. Sisson (2012). Approximate Bayesian computation and Bayes linear analysis: towards high-dimensional ABC. Journal of Computational and Graphical Statistics, in press.

- [\citeauthoryearNott, Tan, Villani, and KohnNott et al.2012] Nott, D. J., S. L. Tan, M. Villani, and R. Kohn (2012). Regression density estimation with variational methods and stochastic approximation. Journal of Computational and Graphical Statistics 21, 797–820.

- [\citeauthoryearPritchard, Seielstad, Perez-Lezaun, and FeldmanPritchard et al.1999] Pritchard, J. K., M. T. Seielstad, A. Perez-Lezaun, and M. W. Feldman (1999). Population growth of human Y chromosomes: A study of Y chromosome microsatellites. Molecular Biology and Evolution 16, 1791–1798.

- [\citeauthoryearRatmann, Andrieu, Hinkley, Wiuf, and RichardsonRatmann et al.2009] Ratmann, O., C. Andrieu, T. Hinkley, C. Wiuf, and S. Richardson (2009). Model criticism based on likelihood-free inference, with an application to protein network evolution. Proc. Natl. Acad. Sci. USA 106, 10576–10581.

- [\citeauthoryearRatmann, Jorgensen, Hinkley, Stumpf, Richardson, and WiufRatmann et al.2007] Ratmann, O., O. Jorgensen, T. Hinkley, M. Stumpf, S. Richardson, and C. Wiuf (2007). Using likelihood-free inference to compare evolutionary dynamics of the protein networks of H. Pylori and P. falciparum. PLoS Comp. Biol. 3, e230.

- [\citeauthoryearRobert, Cornuet, Marin, and PillaiRobert et al.2011] Robert, C. P., J.-M. Cornuet, J.-M. Marin, and N. Pillai (2011). Lack of confidence in approximate Bayesian computation model choice. Proc. Natl. Acad. Sci. 108(37), 15112–15117.

- [\citeauthoryearSisson and FanSisson and Fan2011] Sisson, S. A. and Y. Fan (2011). Likelihood-free Markov chain Monte Carlo. In S. P. Brooks, A. Gelman, G. Jones, and X.-L. Meng (Eds.), Handbook of Markov Chain Monte Carlo, pp. 319–341. Chapman and Hall/CRC Press.

- [\citeauthoryearSisson, Fan, and TanakaSisson et al.2007] Sisson, S. A., Y. Fan, and M. M. Tanaka (2007). Sequential Monte Carlo without likelihoods. Proc. Natl. Acad. Sci. 104, 1760–1765. Errata (2009), 106:16889.

- [\citeauthoryearSisson, Peters, Fan, and BriersSisson et al.2008] Sisson, S. A., G. W. Peters, Y. Fan, and M. Briers (2008). Likelihood-free samplers. Technical report, University of New South Wales.

- [\citeauthoryearTavaré, Balding, Griffiths, and DonnellyTavaré et al.1997] Tavaré, S., D. J. Balding, R. C. Griffiths, and P. Donnelly (1997). Inferring coalescence times from DNA sequence data. Genetics 145(505-518).

- [\citeauthoryearTran, Nott, and KohnTran et al.2012] Tran, M.-N., D. J. Nott, and R. Kohn (2012). Simultaneous variable selection and component selection for regression density estimation with mixtures of heteroscedastic experts. Electronic Journal of Statistics 6, 1170–1199.

- [\citeauthoryearWassermanWasserman1989] Wasserman, L. A. (1989). A robust Bayesian interpretation of likelihood regions. The Annals of Statistics 17(3), 1387 – 1393.

- [\citeauthoryearWoodWood2010] Wood, S. N. (2010). Statistical inference for noisy nonlinear ecological dynamic systems. Nature 466, 1102 – 1104.

| Spherical | Ellipsoidal | |||||

| 0.025 | mean | 0.975 | 0.025 | mean | 0.975 | |

| 24.25 | 31.67 | 39.08 | 69.53 | 96.77 | 124.01 | |

| 24.26 | 30.61 | 37.93 | 65.01 | 95.18 | 135.11 | |

| 25.00 | 31.59 | 39.29 | 68.82 | 93.40 | 119.38 | |

| 25.09 | 31.65 | 39.34 | 69.41 | 93.66 | 118.28 | |

| 25.05 | 31.63 | 39.32 | 70.42 | 93.97 | 116.76 | |

| 25.18 | 31.77 | 39.44 | 72.04 | 94.98 | 117.84 | |

| 1.01 | 1.48 | 1.94 | 1.08 | 1.84 | 2.60 | |

| 1.02 | 1.45 | 1.95 | 1.12 | 1.92 | 3.06 | |

| 1.03 | 1.46 | 1.95 | 1.08 | 1.88 | 2.96 | |

| 1.03 | 1.46 | 1.96 | 1.07 | 1.87 | 2.95 | |

| 1.03 | 1.46 | 1.95 | 1.09 | 1.85 | 2.86 | |

| 1.07 | 1.44 | 1.86 | 1.11 | 1.68 | 2.34 | |

| -0.21 | -0.03 | 0.15 | -0.29 | -0.08 | 0.14 | |

| -0.18 | -0.02 | 0.17 | -0.35 | -0.09 | 0.14 | |

| -0.18 | -0.02 | 0.15 | -0.33 | -0.09 | 0.12 | |

| -0.18 | -0.02 | 0.15 | -0.33 | -0.08 | 0.12 | |

| -0.17 | -0.02 | 0.15 | -0.31 | -0.08 | 0.12 | |

| -0.13 | -0.01 | 0.12 | -0.18 | -0.04 | 0.10 | |