Split Sampling:

Expectations, Normalisation and Rare Events

This Draft: October 2013)

Abstract

In this paper we develop a methodology that we call split sampling methods to estimate high dimensional expectations and rare event probabilities. Split sampling uses an auxiliary variable MCMC simulation and expresses the expectation of interest as an integrated set of rare event probabilities. We derive our estimator from a Rao-Blackwellised estimate of a marginal auxiliary variable distribution. We illustrate our method with two applications. First, we compute a shortest network path rare event probability and compare our method to estimation to a cross entropy approach. Then, we compute a normalisation constant of a high dimensional mixture of Gaussians and compare our estimate to one based on nested sampling. We discuss the relationship between our method and other alternatives such as the product of conditional probability estimator and importance sampling. The methods developed here are available in the R package: SplitSampling.

Keywords: Rare Events, Cross Entropy, Product Estimator, Slice Sampling, MCMC, Importance Sampling, Serial Tempering, Annealing, Adaptive MCMC, Wang-Landau, Nested Sampling, Bridge and Path Sampling.

1 Introduction

In this paper we develop a methodology we refer to as split sampling methods to provide more precise estimates for high dimensional expectations and rare event probabilities. We show that more precise estimators can be achieved by splitting the expectation of interest into a number of easier-to-estimate normalisation constants and then integrating those estimates to produce an estimate of the full expectation. To do this, we employ an auxiliary variable MCMC approach with a family of splitting functions and a weighting function on the conditional distribution of the auxiliary random variable. We allow for an adaptive MCMC approach to specify our weighting function. We relate our method to the product estimator (Diaconis and Holmes, 1994, Fishman, 1994) which splits the rare event probability into a set of relatively larger conditional probabilities which are easier to estimate and to nested sampling (Skilling, 2006) for the estimation of expectations. Other variance reduction techniques, such as control variates will provide further efficiency gains (see Dellaportas and Kontoyiannis, 2012, Mira et al, 2012).

There are two related approaches in the literature. One approach is for estimating expectations is nested sampling (Skilling, 2006) which sequentially estimates the quantiles of the likelihood function under the prior. Other normalisation methods include bridge and path sampling (Meng and Wong, 1996, Gelman and Meng, 1998), generalized versions of the Wang-Landau algorithm (Wang and Landau, 2001), and the TPA algorithm of Huber and Schott (2010). Serial tempering (Geyer, 2010) and linked importance sampling (Neal, 2005) provide ratios of normalisation constants for a discrete set of unnormalised densities. The second approach is cross entropy (Rubinstein and Glynn, 2009, Asmussen et al, 2012) which sequentially constructs an optimal variance-reducing importance function for calculating rare event probabilities. We show that our adaptively chosen weighted MCMC algorithm can provide efficiency gains over cross entropy methods.

The problem of interest is to calculate an expectation of interest, , where is a likelihood and is a prior measure. For rare event probabilities, , and the splitting functions are specified by level sets in the likelihood, namely . This occurs naturally in the rare event simulation literature and in nested sampling. To develop an efficient estimator, we define a joint split sampling split distribution, , on and an auxiliary variable that tilts the conditional distribution with a weighting function, . We provide a default setting for the weight function to match the sampling properties of the product estimator and of nested sampling. We also allow for the possibility of adaptively learning a weight function from the MCMC output. As with other ergodic Monte Carlo methods, we assume that the researcher can construct a fast MCMC algorithm for sampling our joint distribution.

The rest of the paper is outlined as follows. Section 2 details our split sampling methodology. A key identity “splits” the expectation of interest into an integrated set of rare event normalisation constants. MCMC then provides an estimator of the marginal distribution of the auxiliary variable, which in turn provides our overall estimator. We provide a number of guidelines for specifying our weight function in both discrete and continuous settings. Section 3 describes the relationship with the product estimator and nested sampling methods. In both cases, we provide a theorem that provides a default choice of weight function to match the sampling behavior of the product estimator and nested sampling. Section 4 applies our methodology to a shortest path rare event probability and to the calculation of a normalisation constant for a spike-and-slab mixture of Gaussians. We illustrate the efficiency gains of split sampling over crude Monte Carlo, the product estimator and the cross entropy method. Finally, Section 5 concludes with directions for future research.

2 Split Sampling

We now introduce the notation to characterize the estimation problems and to develop our method. The central problem is to calculate an expectation of a non-negative functional of interest, which we denote as , under a -dimensional probability distribution . We write this expectation as:

The corresponding rare event probability is given by

We interpret as a “prior” distribution, as a likelihood, and as an auxiliary variable. Given a family of splitting functions, , their normalisation constants are, . For rare events, where is large. Here we assume that is continuous with respect to the prior and .

Split sampling works as follows. We define the set of “tilted” distributions and corresponding normalisation constants by

For rare events, and corresponds to conditioning on level sets of . The ’s correspond to “rare” event probabilities

For the functional , the expectation of interest, , is an integration of the rare event probabilities. Using Fubini and writing we have the key identity

We have “split” the computation of into a set of easier to compute normalisation constants . We will simultaneously provide an estimator and .

To do this, we further introduce a weight function on the auxiliary variable, , and the cumulative weight . The joint split sampling density, , is defined with as

where . The marginals on and are

| (1) |

where .

The key feature of our split sampling MCMC draws, , are that they provide an efficient Rao-Blackwellised estimate of the marginal without the knowledge of the ’s. We now show how to estimate and .

With , the joint splitting density is

The conditional posterior of the auxiliary index given is

The density is proportional to the weight function on the interval . Slice sampling corresponds to and uniform sampling on . This would lead to direct draws from the posterior distribution and the resultant estimator would be the Harmonic mean. Our approach will weight towards regions of smaller values to provide an efficient estimator of all the rare event probabilities and hence of .

The marginal density estimator of is

This is a re-weighted version of the initial weights . The function will be used to adaptively re-balance the initial weights in our adaptive version of the algorithm, see Section 4.

We now derive estimators for and by exploiting a Rao-Blackwellised estimator for the marginal density, . From (1), we have and so an estimate of is given by

With , this provides a new estimator , where , given by

To find , we use the summation-integral counterpart to Fubini and the fact that to yield

Therefore, we have our estimator

We now describe our split sampling algorithm.

Algorithm: Split Sampling

-

•

Draw samples by iterating and

-

•

Estimate the marginal distribution, , via

-

•

Estimate the individual normalisation constants, , via

(2) -

•

Compute a new estimate, , via

(3)

A practical use of the algorithm will involve a discrete grid . We write the rare event probabilities and the weights . The marginal probabilities are estimated by Rao-Blackwellization as

With , the estimator is for . In the next sections we provide a default choice of weights to match the sampling behaviour of the product estimator and nested sampling together with an adaptive MCMC scheme for estimating the weights. First, we turn to convergence issues.

2.1 Convergence and Monte Carlo standard errors

Roberts and Rosenthal (1997), Mira and Tierney (2002) and Hobert et al (2002) who provide general conditions for geometric ergodicity of slice sampling. Geometric ergodicity will imply a Monte Carlo CLT for calculating asymptotic distributions and standard errors. Our chain is geometrically ergodic if is bounded, and there exists an such that is nonincreasing on for some where

Then we can apply a central limit theorem to ergodic averages of the functional

which yields the condition

We have a central limit theorem for at any , where

This argument also works at as long as .

2.2 Importance Sampling

The standard Monte Carlo estimate of is where , with draws possibly obtained via MCMC. This is too inaccurate for rare event probabilities. Von Neumann’s original view of importance sampling was as a variance reduction to improve this estimator. By viewing the calculation of an expectation as a problem of normalising a posterior distribution, we can write

Importance sampling uses a blanket to compute

Picking to be the posterior distribution leads to the estimator with zero variance. While impractical, this suggests finding a class of importance blankets that are adaptive and depend on can exhibit good Monte Carlo properties.

Split sampling specifies a class of importance sampling blankets, indexed by , by

The estimator in (2) can be viewed as an importance sampling estimator where we average over the splitting set with . Similarly we can express as an importance sampling estimator as in (3) which uses a proposal distribution proportional to .

3 Comparison with the Product Estimator and Nested Sampling

3.1 Product Estimator

A standard approach to calculating the rare event probability is the product estimator. We set for some and introduce a discrete grid of -values starting at . The conditional probability estimator writes

or equivalently .

Variance reduction is achieved by splitting into pieces of larger magnitude which are relatively easier to estimate. With , we estimate

Given independent samples from the tilted distributions for each , we have

with mean and variance . The product estimator, as well as the cross-entropy estimator, relies on a set of independent samples drawn in a sequential fashion. Split sampling, on the other hand, uses a fast MCMC and ergodic averaging to provide an estimate . The Monte Carlo variation can be determined from the output of the chain. Controlling the Monte Carlo error of this estimator is straightforward due to independent samples with relative mean squared error, see Fishman (1994) and Garvels et al (2002),

3.1.1 Matching the Product Estimator Sampling Distribution

We can now compare the product estimator with split sampling. Suppose and let be the grid points of for where . By construction, are the tail -quantile of , and we have .

There are two versions of the product estimator. First, the standard product estimator has the long-run sampling distribution

The second product estimator includes samples from the previous level generation that were above the threshold. This has the long-run sampling distribution

We call this the product estimator with inclusion.

Theorem 1 (Product Estimator)

The two product estimators and the split sampling are related as follows. The standard product estimator corresponds to the (discrete) split sampling with . The product estimator with inclusion is equivalent to split sampling with cumulative weights

Split sampling with discrete knots , weights and has sampling distribution

Therefore, this is equivalent to the product estimator if and only if, for ,

As are the tail -quantile of , we have and

For the product estimator with inclusion, the equivalent split sampling weights are

3.2 Nested Sampling

We now provide a comparison with nested sampling. We provide a specification of so that the sampling distribution of matches that of nested sampling. We can adaptively determine the values from our MCMC output. Let be the -quantile of the likelihood function under the prior . Then, nested sampling expresses

where . This integral can be approximated by quadrature

The larger is, the more accurate the approximation, and so this suggests the following estimator

where are the simulated -quantiles of likelihoods with respect to the prior. Here, is the total number of samples. Nested Sampling is a sequential simulation procedure for finding the -quantiles, , by sampling .

Brewer et al (2011) propose a diffuse nested sampling approach to determine the levels . Both nested and diffuse nested sampling are product estimator approaches. The quantiles are chosen so that each level occupies times as much prior mass as the previous level . Diffuse nested sampling achieves this by sequentially sampling from a mixture importance sampler where the weights are exponential for some . MCMC methods are used to traverse this mixture distribution with a random walk step for the index that steps up or down a level with equal probability. A new level is added using the -quantile of the likelihood draws. Using diffuse nested sampling allows some chance of the samples’ escaping to lowered constrained levels and to explore the space more freely. One caveat is that a large contribution can come from values of near the origin and we have to find many levels to obtain an accurate approximation.

Murray et al (2006) provide single and multiple sample versions of nested sampling algorithms. If is known, we sample as follows:

-

1.

Set .

-

2.

Generate samples from and sort .

-

3.

Repeat while :

-

(a)

Set and .

-

(b)

Generate and set .

-

(c)

Sort ’s and set .

-

(a)

-

4.

Set and stop.

If is not known, replace step 3 with:

-

3(a).

Repeat while :

3.2.1 Matching the Nested Sampling Distribution

We now choose to match the sampling properties of nested sampling. The main difference between split and nested sampling is that in split sampling we specify a weight function for and sample from the full mixture distribution, rather than employing a sequential approach for grid selection which requires a termination rule. Another difference is that split sampling estimator does not need to know the ordered ’s.

We can now match the sampling distributions of split and nested sampling (see, Skilling, 2006). The expected number of samples less than is . Assume for a while. Since are independent standard uniforms and

the distribution of the number of samples less than is same as the number of arrivals before of a Poisson process with rate . For general , it only changes the arrival rate of the Poisson process into .

Theorem 2 (Nested Sampling)

If we pick the weights such that

Then the sampling distributions of split and nested sampling match.

The sampling distribution of the nested sampling for finite is hard to calculate, but we can observe limiting results. As , if , then we have

Split sampling has marginal density of given by

The tail distribution function is then

We now find the importance splitting density that matches the nested sampling distributional properties in the sense that . Since

where . We therefore set .

Since is unknown, we are not ready to begin sampling. As a remedy we propose approximating . We estimate ’s for certain grid points and interpolate by, for example, a piecewise exponentially increasing function. As we assume no information on a priori, we have to start with a single grid point and build more grid points as sampling goes. When we have collected enough samples higher than the current top grid point, we add a new grid point and adjust the approximated function. For that purpose, we introduce a condition that lets us monitor the number of visits, , to the current top level of the likelihood before we construct a new level. Specifically, we run

-

1.

Set , , , and .

-

2.

While , set

-

(a)

Draws , and set .

-

(b)

Obtain if or otherwise, where .

-

(c)

Repeat (a) and (b) until we have visits to level .

-

(d)

Choose the -quantile of likelihoods of level as .

-

(e)

Set and .

-

(a)

Under the condition , the chain will visit each level roughly uniformly. However, it may take a long time to reach the top level, and the uncertainty in may act like a hurdle for visiting upper levels. With these concerns, it is desirable to favor upper levels by replacing step (d) with

-

-

(d1)

Set .

-

(d1)

We call the boosting factor as increases the preference for the upper levels. This reduces the search time and ensures the time complexity to be . To further expedite this procedure, we may put more weight on the top level by substituting (d) with the step:

-

-

(d2)

Set and .

-

(d2)

For example, if , the chain spends half of the time on the top level and the other half backtracking the other levels.

Once we identify all levels, our split sampling algorithm runs:

-

1.

Set and for each .

-

2.

While , set .

-

(a)

Draw with and , and set .

-

(b)

For each with , update .

-

(c)

Update and set .

-

(a)

From a practical perspective, it is critical to have nonzero initial values on . If we start with , the early and are unstable, and the whole procedure can become abortive. Since, though not very accurate, is a reasonable initial estimate, we use them for the initial values of and . reflects the degree of dependence on those initial values.

Another point to make is even if the initial are not as accurate as needed to guarantee good mixing of our MCMC iterations, we dynamically refine as in step 2(c). The beauty of this algorithm is that this update makes the chain self-balanced. When is larger than it should be, or is smaller, the chain visits level more often. Thus increasing and decreases , which helps converge more quickly to the true value.

At first sight, the time complexity appears to be since steps 2(b) and 2(c) cost operations. However, if the values are chosen so that are exponentially decreasing, the work can be done in time. The updates needed at steps 2(b) and 2(c) are only for the last several ’s since the increment becomes negligible very quickly relative to as decreases.

4 Choice of cumulative weights: and

The previous subsection assumed that is fixed. The “correction factor” in the construction of needs to be estimated as accurately as possible. To do this we will use an adaptive choice of the weight function, and use convergence results from the adaptive MCMC literature.

A common initialisation is to set which leads to draws from the posterior. Then, . This leads to an estimate of the marginal, , given by the measure

The density estimate will be zero for by construction. We also have a set of estimates where which can be used to re-balance to weights .

Given an initial run of the algorithm, we can re-proportion the prior weight function to regions we have not visited frequently enough. To accomplish this, let be a desired target distribution for , for example a uniform measure. Then re-balance the weights inversely proportional to the visitation probabilities and set the new weights by

This will only adjust our weights in the region where . As the algorithm proceeds we will sample regions of higher likelihood values and further adaptive our weight function.

Other choices for weights are available. For example, in many normalisation problems will be exponential in due to a Laplace approximation argument. This suggests taking an exponential weighting for some . In this case, we have

The marginal distribution is

We can also specify to deal with the possibility that the chain might not have visited all states by setting a threshold which corresponds to the maximum allowable increase in the log-prior weights. This leads to a re-balancing rule

where we have also re-normalised the value of the largest state to one.

When is available, we set and for . To initialise , we use the harmonic mean for and an exponential interpolation for . Drawing , we have

The harmonic mean estimator (Raftery et al, 2007) is known to have poor Monte Carlo error variance properties (Polson, 2006, Wolpert and Schmidler, 2012) although we are estimating and not its inverse.

We can extend this insight to a fully adaptive update rule for , similar to stochastic approximation schemes. Define a sequence of decreasing positive step sizes with . A practical recommendation is where , see e.g. Sato and Ishii (2000). Another approach is to wait until a “flat histogram” (FH) condition holds:

for a pre-specified tolerance threshold, . The measure tracks our current estimate of the marginal auxiliary variable distribution. The Rao-Blackwellised estimate further reduces variance.

The empirical measure can be used to update as the chain progresses. Let denote the points at which will be decreased according to its schedule. Then an update rule which guarantees convergence is to set

Jacob and Ryder (2012) show that if is only updated on a sequence of values which correspond to times that a “flat-histogram” criterion is satisfied, then convergence ensues and the FH criteria is achieved in finite time. After updating , we re-set the counting measure and continue. Other adaptive MCMC convergence methods are available in Atchade and Liu (2010), Liang et al (2007), and Zhou and Wong (2008). Bornn et al (2012) provides a parallelisable algorithm for further efficiency gains. Peskun (1973) provides theoretical results on optimal MCMC chains to minimise the variance of MCMC functionals.

One desirable Monte Carlo property for an estimator is a bounded coefficient of variation. For simple functions, and , mixture importance functions achieve such a goal, see Iyengar (1991) and Adler et al (2008). Madras and Piccioni (1999, section 4) hint at the efficiency properties of dynamically selected mixture importance blankets. Gramacy et al (2010) propose the use of importance tempering. Johansen et al (2006) use logit annealing implemented via a sequential particle filtering algorithm.

4.1 Choosing a Discrete Cooling Schedule

We suggest a simple, sequential, empirical approach to selecting a “cooling schedule” in our approach. Specifically, set , then given we sample . We order the realisations of the criteria function and set equal to the -quantile of the samples. This provides a sequential approach to solving

A number of authors have proposed “optimal” choices of , which implicitly defines a cooling schedule, , for . L’Ecuyer et al (2006) and Amrein and Kunsch (2011) propose and , respectively. Huber and Schott (2010) define a well-balanced schedule as one that satisfies . They show that such a choice leads to fast algorithms. The difficulty is in finding the right order of magnitude of and the associated schedule that ensures that each slice is not exponentially small. For rare events, we sample until and then set . Our initial estimate and our weights are .

In hard cases, such as the multimodal mixture of Gaussians, the normalising constants are not exponential in . In such cases we initialize the weights by a piecewise exponential obtained by interpolating any point by where . For , we use . The final estimator is given by

Finally, our methodology can be viewed as an adaptive mixture importance sampler. As we rebalanced the weights we are adaptive changing the target distribution of our MCMC algorithm rather than the traditional adaptive proposal approaches with a fixed target. Other similar approaches include Umbrella sampling (Torrie and Valleau, 1997) which can be seen as a precursor to many of the current advanced MC strategies such as the Wang-Landau algorithm and its generalisations for sampling high dimensional multimodal distributions. These algorithms exploit an auxiliary variable and by their adaptive nature improve estimates continuously as the simulation advances. The main difference is how each algorithm traverses low and high energy states. The Wang-Landau algorithm aims to achieve a uniform distribution on the auxiliary variable, thus spending more time in low energy states than high states states as opposed to multicanonical sampling (Berg and Neuhaus, 1992), -ensemble sampling (Hesselbo and Stinchcombe, 1995) or simulated tempering (Geyer and Thompson, 1995).

5 Applications

5.1 Rare Event Shortest Path

Calculating rare event probabilities is a common goal of many problems. Rubinstein and Kroese (2004) consider the total length of the shortest path on a weighted graph with random weights . Suppose there are 4 vertices , , , and . The adjacent weight matrix is given by

Each weight follows an independent exponential distribution with scale parameter with joint distribution given by

The goal is to estimate the probability of the rare event corresponding to the length of the shortest path from to

We will consider three cases: and where the true rare event probabilities are

These can be estimated by the split sampler (SS) with and level breakpoints . is the estimator.

We implement three other competing estimators. First, the crude Monte Carlo (CMC) estimator simulates and estimates the rare event probabilities by

Second, the conditional probability product (CPP) estimator calculates the -quantile of samples of under for all with , , and . This estimator is defined as:

To find we need to sample . We use Gibbs sampling with complete conditionals given by truncated exponential distributions. By the lack of memory property, we have

The other conditionals follow in a similar manner.

Third, the cross-entropy (CE) estimator (de Boer et al, 2005) calculates an “optimal” importance blanket, , parameterised by . Then it draws samples of and estimates the shortest path probability

The sequential algorithm for finding is similar in spirit to the product estimator approach: set and . Choose ; typically . Then perform

| N | CMC | CE | CPP | SS | CE | CPP | SS | CE | CPP | SS | |||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.807 | 0.040 | 0.044 | 0.055 | 0.066 | 0.076 | 0.091 | 0.113 | 0.098 | 0.133 | ||||

| 0.275 | 0.011 | 0.015 | 0.015 | 0.017 | 0.025 | 0.026 | 0.028 | 0.033 | 0.036 | ||||

| 0.086 | 0.003 | 0.004 | 0.005 | 0.005 | 0.007 | 0.007 | 0.008 | 0.009 | 0.011 | ||||

-

1.

Draw samples of . Let be the quantile of .

If , set .

-

2.

Update via cross-entropy minimisation;

-

3.

If , set and exit. Otherwise, set and go to step 1.

Table 1 provides the simulation results. Each scenario was run times and relative RMS of each estimator was recorded. The CMC estimator was only recorded for as the other events are too rare to even have a single count. The total sample size, , was , , or . The tuning parameters for CE were , for and for , and . For CPP, we used and where is the number of required steps. For split sampling (SS), we set , and and . One can see the cross-entropy method outperforms the others. It is because it finds an efficient importance sampling function and uses independent samples. However, note that the split sampling estimator is almost as efficient as others despite of the fact that it is an MCMC estimator. Further gains from split sampling are expected in higher dimensional problems with multiple modes where finding at each stage in CE can be cumbersome in general.

5.2 Normalisation of a Mixture of Gaussians

As an illustration of the advantages of using split sampling we consider a centered and de-centered mixture of Gaussians. We follow the nested and diffuse nested sampling literature (Skilling, 2008, Brewer et al, 2011) and suppose that where . The centered likelihood is given by the classic Gaussian “spike-and-slab” of width and “plateau” of width , namely

The prior is uniform on . In the de-centered multimodal mixture we take

The goal is to calculate the so-called evidence, .

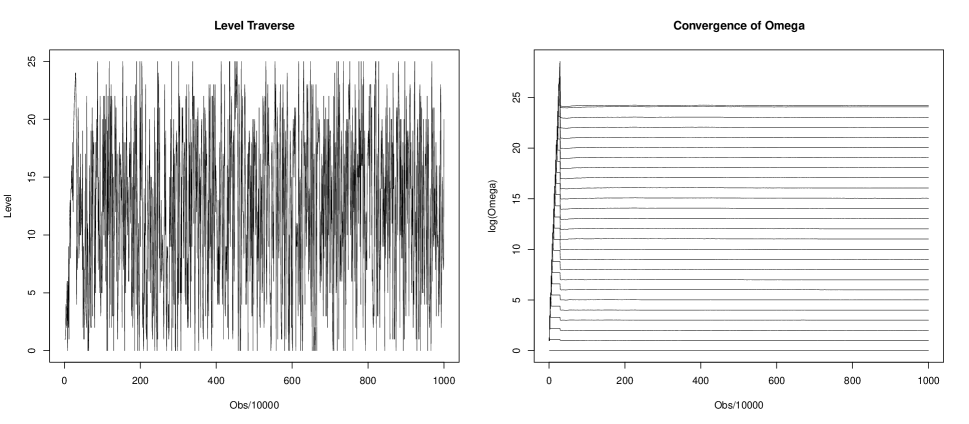

We implemented the split sampling algorithm as described in 3.2.1 and 4.1. The nested sampling is implemented via MCMC because drawing from the conditional distribution directly is not possible for this example. In both methods, we used a random walk MH proposal distribution given by where the density of the step size on for random chosen index .

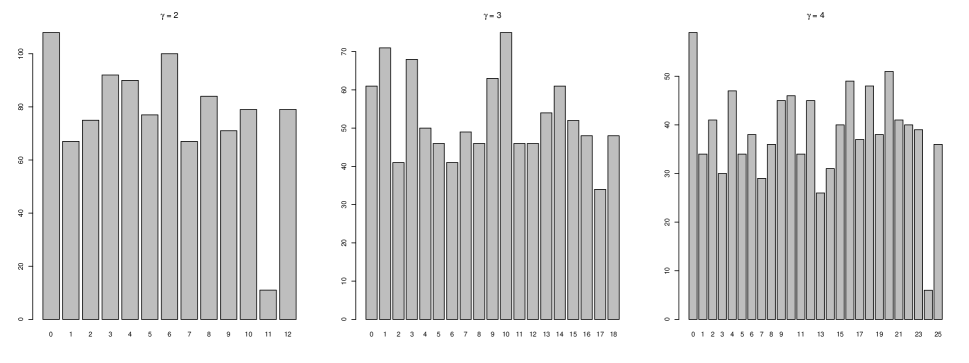

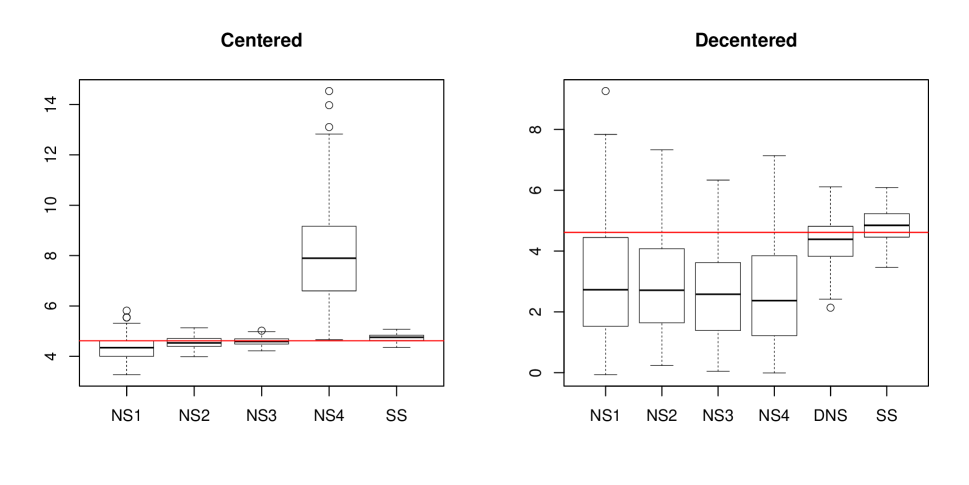

Table 2 and the boxplot in Figure 4 compare the performance of the nested sampling and the split sampling methods. For each run, were recorded and their root mean squares are reported in Table 2. The number of runs for each case is 500. Overall, the nested sampling works slightly better for the centered case. There is no advantage for split sampling in this case, but it is showing as good performance, too.

| Algorithm | Parameters | RMS |

|---|---|---|

| NS1 | 300 particles, 333 MCMC steps | |

| NS2 | 1000 particles, 100 MCMC steps | |

| NS3 | 3000 particles, 33 MCMC steps | |

| NS4 | 10000 particles, 10 MCMC steps | |

| SS | , , , |

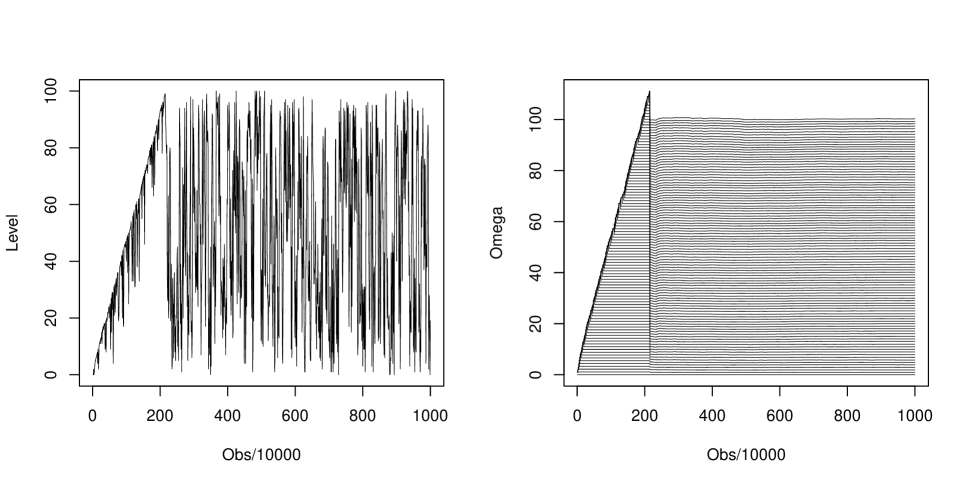

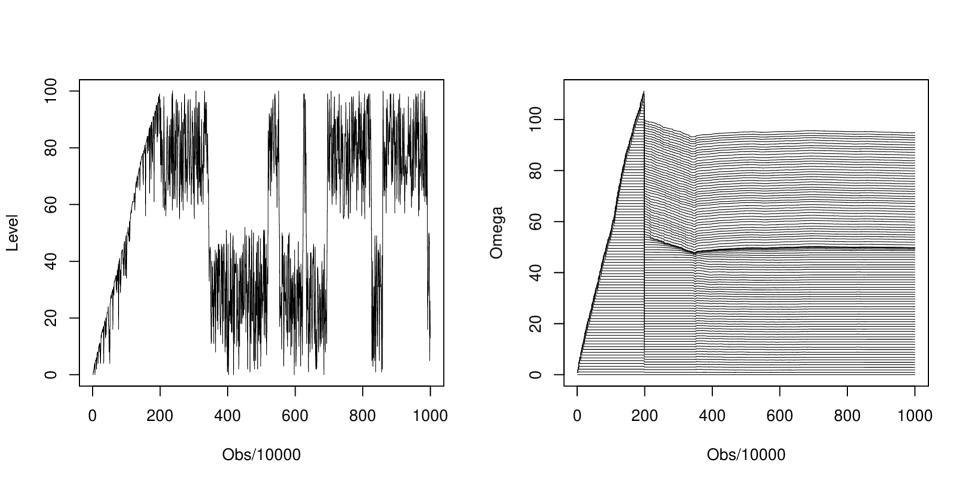

For the de-centered case, the diffuse nested sampling is preferable to the nested sampling, because when the likelihood is multimodal, one needs to be able to backtrack the lower levels of likelihood to traverse another mode. We implemented the diffuse nested sampling for comparison as stated in their paper (Brewer et al, 2011). As shown in Table 3 and the boxplot in Figure 4, the split sampling significantly outperforms others. It is largely due to the fact that the split sampling freely visits the two modes of likelihood function and fast convergence of ’s and ’s as one can see in the plots in Figure 5.

| Algorithm | Parameters | RMS |

|---|---|---|

| NS1 | 300 particles, 333 MCMC steps | |

| NS2 | 1000 particles, 100 MCMC steps | |

| NS3 | 3000 particles, 33 MCMC steps | |

| NS4 | 10000 particles, 10 MCMC steps | |

| DNS | Diffuse Nested Sampling | |

| SS | , , , |

6 Discussion

The advantage of the class of split sampling densities is that the resultant estimator of can be implemented via an auxiliary MCMC algorithm from a joint distribution indexed by a random auxiliary variable . Moreover, it allows an adaptive choice of to reduce the Monte Carlo error of the resultant estimator. Convergence results rely on adaptive MCMC literature. Roberts (2010) observes that MCMC methods are likely to achieve the largest efficiency gains in rare event probabilities (Glasserman et al, 1999, Glynn et al, 2010) and in counting problems where the resultant chains can be hard to sample exactly.

Split sampling illustrates the adaptive importance sampling nature of nested sampling and cross-entropy methods. There is also a clear relationship with slice sampling (Polson, 1996, Neal, 2003) as one can view the sampling of the posterior, , as the marginal from the augmented distribution . The main difference is that split sampling runs a Markov chain that traverses the whole space defined by to find regions where needs to be refined. Both CE and NS methods using a sequential sampling procedure as in the CPP estimator to split the quantity of interest into estimable pieces. Further research is required to tailor the specification of the weight function to the problem at hand.

We leave open the question of an optimal choice of . Here we have focused on , however, using logit-type functions might led to faster converging MCMC algorithms. The key to the efficiency of split sampling is being able to construct a rapidly mixing MCMC algorithm to sample the mixture distribution . We aim to report on direct applications in Bayesian inference in future work. For example, Murray et al (2006) shows that nested sampling performs well for Markov random fields models and split sampling should have similar properties.

7 References

Adler, R.J., J. Blanchet and J. Liu (2008). Efficient simulation for tail probabilities of Gaussian random fields. Proceedings of the Winter Simulation Conference, 328-336.

Amrein, M. and H. Künsch (2011). A variant of importance sampling for rare event estimation: fixed number of successes. ACM Transactions on Modeling and Computer Simulation, 21(2), Article 13.

Asmussen, S. and P. Dupuis, R. Rubenstein and H. Wang (2012). Importance Sampling for Rare Events. Encyclopedia of Operations Research (eds Gass, S. and M. Fu), Kluwer.

Atchadé,Y.F. and J.S. Liu (2010). The Wang-Landau algorithm in general state spaces: applications and convergence analysis. Statistica Sinica, 20, 209-233.

Berg, B.A. and T. Neuhaus (1992). Multicanonical ensemble: A new approach to simulate first-order phase transitions. Physical Review Letters, 68, 9-12.

Bornn, L., P.E. Jacob, P. Del Moral and A. Doucet (2012). An adaptive Wang-Landau algorithm for automatic density exploration. J. Computational and Graphical Statistics.

de Boer, P.T., D.P. Kroese and R.Y. Rubenstein (2005). A Tutorial on the cross-entropy method. Annals of Operations Research, 134, 19-67.

Brewer, B.J, L.B. Pártay and G. Csányi (2011). Diffusive Nested Sampling. Statistics and Computing, 21(4), 649-656.

Dellaportas, P. and I. Kontoyiannis (2012). Control variates for estimation based on reversible MCMC samplers. Journal of Royal Statistical Society, B, 74(1), 133-161.

Diaconis, P. and S. Holmes (1994). Three examples of the MCMC method. Discrete Probability and Algorithms, 43-56.

Fishman, G. (1994). Markov chain sampling and the Product Estimator. Operations Research, 42(6), 1137-1145.

Garvels, M.J.J., J.C.W. van Ommeren and D.P. Kroese (2002). On the importance function in splitting simulation. European Transactions on Telecommunications, 13(4), 363-371.

Gelman, A. and X. Meng (1998). Simulating normalizing constants: from importance sampling to bridge sampling to path sampling. Statistical Science, 13, 163-185.

Geyer, C.J. and E.A. Thompson (1995). Annealing Markov chain Monte Carlo with applications to ancestral inference. Journal of American Statistical Association, 90, 909-920.

Geyer, C.J (2012). Bayes factors via Serial Tempering. Technical Report, University of Washington.

Glasserman, P., P. Heidelberger, P. Shahabuddin and T.Zajic (1999). Multi-Level Splitting for rare event probabilities. Operations Research, 47(4), 585-600.

Glynn, P.W., A. Dolgin, R.Y. Rubinstein and R. Vaisman (2010). How to generate uniform samples on discrete sets using the splitting method. Prob. Eng. Info. Sci., 24(3), 405-422.

Gramacy, R., R. Samworth and R. King (2010). Importance Tempering. Statistics and Computing, 20(1), 1-7.

Hesselbo, B. and R.B. Stinchcombe (1995). Monte Carlo Simulation and global optimisation without parameters. Phys. Rev. Lett., 74, 2151-2155.

Huber, M. and S. Schott (2010). Using TPA for Bayesian Inference. Bayesian Statistics, 9, 257-282.

Iyengar, S. (1991). Importance Sampling for Tail Probabilities. Technical Report 440, Stanford University.

Jacob, P.E. and R.J. Ryder (2012). The Wang-Landau algorithm reaches the Flat Histogram criterion in finite time. Ann. Appl. Probab..

Johansen, A.M., P. Del Moral and A. Doucet (2006). Sequential Monte Carlo Samplers for Rare Events. Proceedings of the 6th International Workshop on Rare Event Simulation, 256-267.

L’Ecuyer, P., V. Demers and B. Tuffin (2006). Splitting for Rare event simulation. Proceedings of the 2006 Winter Simulation Conference, 137-148.

Liang, F. (2005). Generalized Wang-Landau algorithm for Monte Carlo computation. Journal of American Statistical Association, 100, 1311-1337.

Liang, F., C. Liu and R.J. Carroll (2007). Stochastic approximation in Monte Carlo computation. Journal of American Statistical Association, 102, 305-320.

Madras, N. and M. Piccioni (1999). Importance Sampling for Families of Distributions. Annals of Applied Probability, 9(4), 1202-1225.

Meng, X-L and W. Wong (1996). Simulating ratios of normalising constants via a simple identity: a theoretical exposition. Statistia Sinica, 6, 831-860.

Mira, A., R. Solgi, and D. Imparato (2012). Zero Variance MCMC for Bayesian Estimators. Statistics and Computing, 23(5), 653-662.

Murray, I., D.J.C. MacKay, Z. Ghahramani and J. Skilling (2006). Nested sampling for the Potts models. Advances in NIPS, 947-954.

Neal, R.M. (2003). Slice Sampling. Annals of Statistics, 31(3), 705-767.

Neal, R.M. (2005). Estimating ratios of normalising constants using linked importance sampling. Technical Report No. 0511, University of Toronto.

Peskun, P.H. (1973). Optimum Monte Carlo sampling using Markov Chains. Biometrika, 60(3), 607-612.

Polson, N.G. (1996). Convergence of Markov Chain Monte Carlo Algorithms. Bayesian Statistics, 5, 297-321.

Polson, N.G. (2006). Comment on: “Estimating the integrated likelihood in posterior simulation using the harmonic mean equality”. Bayesian Statistics, 8, 415-417.

Raftery, A.E., M.A. Newton, J.M. Satagopan and P.N. Krivitsky (2007). Estimating the integrated likelihood via posterior simulation using the Harmonic mean equality. Bayesian Statistics, 8, 371-417.

Roberts, G.O. (2010). Comment on: “Using TPA for Bayesian Inference”. Bayesian Statistics, 9, 280-282.

Rubinstein, R.Y. and P.W. Glynn (2009). How to deal with the curse of dimensionality of likelihood ratios in Monte Carlo simulation. Stochastic Models, 25, 547-568.

Rubenstein, R.Y. and D. Kroese (2004). The Cross Entropy Method. Springer.

Sato, M. and S. Ishii (2000). On-line EM algorithm for the normalized Gaussian network. Neural Computation, 12, 407-432.

Skilling, J. (2006). Nested Sampling for General Bayesian Computation. Bayesian Analysis, 1(4), 833-860.

Skilling, J. (2008). Nested Sampling for Bayesian computation. Bayesian Statistics, 8, 491-507.

Štefankovič, D., S. Vempola and E. Vigoda (2009). Adaptive simulated annealing: a near-optimal connection between sampling and counting. Journal of the ACM, 56(3), Article No. 18.

Torrie, G.M. and J.P. Valleau (1977). Nonphysical sampling distributions in Monte Carlo free-energy estimation: Umbrella Sampling. Journal of Computational Physics, 23(2), 187-199.

Wang, F. and D.P. Landau (2001). Efficient multiple-range random walk algorithm to calculate the density of states. Phys. Rev. Lett, 86, 2050-2053.

Wolpert, R.L. and S.C. Schmidler (2012). -Stable limit laws for Harmonic Mean estimators of marginal likelihoods. Statistica Sinica, 22, 1233-1251.

Zhou, Q. and W.H. Wong (2008). Reconstructing the energy landscape of a distribution from Monte Carlo samples. Annals of Applied Statistics, 2(4),1307-1331.