Some New Asymptotic Theory for Least Squares Series: Pointwise and Uniform Results

JEL Classification: C01, C14.)

Abstract.

In econometric applications it is common that the exact form of a conditional expectation is unknown and having flexible functional forms can lead to improvements over a pre-specified functional form, especially if they nest some successful parametric economically-motivated forms. Series method offers exactly that by approximating the unknown function based on basis functions, where is allowed to grow with the sample size to balance the trade off between variance and bias. In this work we consider series estimators for the conditional mean in light of four new ingredients: (i) sharp LLNs for matrices derived from the non-commutative Khinchin inequalities, (ii) bounds on the Lebesgue factor that controls the ratio between the and -norms of approximation errors, (iii) maximal inequalities for processes whose entropy integrals diverge at some rate, and (iv) strong approximations to series-type processes.

These technical tools allow us to contribute to the series literature, specifically the seminal work of Newey (1997), as follows. First, we weaken considerably the condition on the number of approximating functions used in series estimation from the typical to , up to log factors, which was available only for spline series before. Second, under the same weak conditions we derive rates and pointwise central limit theorems results when the approximation error vanishes. Under an incorrectly specified model, i.e. when the approximation error does not vanish, analogous results are also shown. Third, under stronger conditions we derive uniform rates and functional central limit theorems that hold if the approximation error vanishes or not. That is, we derive the strong approximation for the entire estimate of the nonparametric function.

Finally and most importantly, from a point of view of practice, we derive uniform rates, Gaussian approximations, and uniform confidence bands for a wide collection of linear functionals of the conditional expectation function, for example, the function itself, the partial derivative function, the conditional average partial derivative function, and other similar quantities. All of these results are new.

Key words and phrases:

least squares series, strong approximations, uniform confidence bands1. Introduction

Series estimators have been playing a central role in various fields. In econometric applications it is common that the exact form of a conditional expectation is unknown and having a flexible functional form can lead to improvements over a pre-specified functional form, especially if it nests some successful parametric economic models. Series estimation offers exactly that by approximating the unknown function based on basis functions, where is allowed to grow with the sample size to balance the trade off between variance and bias. Moreover, the series modelling allows for convenient nesting of some theory-based models, by simply using corresponding terms as the first basis functions. For instance, our series could contain linear and quadratic functions to nest the canonical Mincer equations in the context of wage equation modelling or the canonical translog demand and production functions in the context of demand and supply modelling.

Several asymptotic properties of series estimators have been investigated in the literature. The focus has been on convergence rates and asymptotic normality results (see vandeGeer, 1990; Andrews, 1991; Eastwood and Gallant, 1991; Gallant and Souza, 1991; Newey, 1997; vandeGeer, 2002; Huang, 2003b; Chen, 2007; Cattaneo and Farrell, 2013, and the references therein).

This work revisits the topic by making use of new critical ingredients:

-

1.

The sharp LLNs for matrices derived from the non-commutative Khinchin inequalities.

-

2.

The sharp bounds on the Lebesgue factor that controls the ratio between the and -norms of the least squares approximation of functions (which is bounded or grows like a in many cases).

-

3.

Sharp maximal inequalities for processes whose entropy integrals diverge at some rate.

-

4.

Strong approximations to empirical processes of series types.

To the best of our knowledge, our results are the first applications of the first ingredient to statistical estimation problems. After the use in this work, some recent working papers are also using related matrix inequalities and extending some results in different directions, e.g. Chen and Christensen (2013) allows -mixing dependence, and Hansen (2014) handles unbounded regressors and also characterizes a trade-off between the number of finite moments and the allowable rate of expansion of the number of series terms. Regarding the second ingredient, it has already been used by Huang (2003a) but for splines only. All of these ingredients are critical for generating sharp results.

This approach allows us to contribute to the series literature in several directions. First, we weaken considerably the condition on the number of approximating functions used in series estimation from the typical (see Newey, 1997) to

for bounded or local bases which was previously available only for spline series (Huang, 2003a; Stone, 1994), and recently established for local polynomial partition series (Cattaneo and Farrell, 2013). An example of a bounded basis is Fourier series; examples of local bases are spline, wavelet, and local polynomial partition series. To be more specific, for such bases we require . Note that the last condition is similar to the condition on the bandwidth value required for local polynomial (kernel) regression estimators ( where is the bandwidth value). Second, under the same weak conditions we derive rates and pointwise central limit theorems results when the approximation error vanishes. Under a misspecified model, i.e. when the approximation error does not vanish, analogous results are also shown. Third, under stronger conditions we derive uniform rates that hold if the approximation error vanishes or not. An important contribution here is that we show that the series estimator achieves the optimal uniform rate of convergence under quite general conditions. Previously, the same result was shown only for local polynomial partition series estimator (Cattaneo and Farrell, 2013). In addition, we derive a functional central limit theorem. By the functional central limit theorem we mean here that the entire estimate of the nonparametric function is uniformly close to a Gaussian process that can change with . That is, we derive the strong approximation for the entire estimate of the nonparametric function.

Perhaps the most important contribution of the paper is a set of completely new results that provide estimation and inference methods for the entire linear functionals of the conditional mean function . Examples of linear functionals of interest include

-

1.

the partial derivative function: ;

-

2.

the average partial derivative: ;

-

3.

the conditional average partial derivative: .

where denotes the partial derivative of with respect to th component of , is a subvector of , and the measure entering the definitions above is taken as known; the result can be extended to include estimated measures. We derive uniform (in ) rates of convergence, large sample distributional approximations, and inference methods for the functions above based on the Gaussian approximation. To the best of our knowledge all these results are new, especially the distributional and inferential results. For example, using these results we can now perform inference on the entire partial derivative function. The only other reference that provides analogous results but for quantile series estimator is Belloni et al. (2011). Before doing uniform analysis, we also update the pointwise results of Newey (1997) to weaker, more general conditions.

Notation. In what follows, all parameter values are indexed by the sample size , but we omit the index whenever this does not cause confusion. We use the notation , and . The -norm of a vector is denoted by , while for a matrix the operator norm is denoted by . We also use standard notation in the empirical process literature,

and we use the notation to denote for some constant that does not depend on ; and to denote . Moreover, for two random variables we say that if they have the same probability distribution. Finally, denotes the space of vectors in with unit Euclidean norm: .

2. Set-Up

Throughout the paper, we consider a sequence of models, indexed by the sample size ,

| (2.1) |

where is a response variable, a vector of covariates (basic regressors), noise, and a regression (conditional mean) function; that is, we consider a triangular array of models with , , , and . We assume that where is some class of functions. Since we consider a sequence of models indexed by , we allow the function class , where the regression function belongs to, to depend on as well. In addition, we allow to depend on but we assume for the sake of simplicity that the diameter of is bounded from above uniformly over (dropping the uniform boundedness condition is possible at the expense of more technicalities; for example, without uniform boundedness condition, we would have an additional term in (4.20) and (4.22) of Lemma 4.2). We denote , , and . For notational convenience, we omit indexing by where it does not lead to confusion.

Condition A.1 (Sample) For each , random vectors , are i.i.d. and satisfy (2.1).

We approximate the function by linear forms , where

is a vector of approximating functions that can change with ; in particular, may increase with . We denote the regressors as

The next assumption imposes regularity conditions on the regressors.

Condition A.2 (Eigenvalues) Uniformly over all , eigenvalues of are bounded above and away from zero.

Condition A.2 imposes the restriction that are not too co-linear. Given this assumption, it is without loss of generality to impose the following normalization:

Normalization. To simplify notation, we normalize , but we shall treat as unknown, that is we deal with random design.

The following proposition establishes a simple sufficient condition for A.2 based on orthonormal bases with respect to some measure.

Proposition 2.1 (Stability of Bounds on Eigenvalues).

Assume that where is a probability measure on , and that the regressors are orthonormal on for some measure . Then A.2 is satisfied if

It is well known that the least squares parameter is defined by

which by (2.1) also implies that where is defined by

| (2.2) |

We call the target function and the surrogate function. In this setting, the surrogate function provides the best linear approximation to the target function.

For all , let

| (2.3) |

denote the approximation error at the point , and let

denote the approximation error for the observation . Using this notation, we obtain a many regressors model

The least squares estimator of is

| (2.4) |

where . The least squares estimator induces the estimator for the target function . Then it follows from (2.3) that we can decompose the error in estimating the target function as

where the first term on the right-hand side is the estimation error and the second term is the approximation error.

We are also interested in various linear functionals of the conditional mean function. As discussed in the introduction, examples include the partial derivative function, the average partial derivative function, and the conditional average partial derivative. Importantly, in each example above we could be interested in estimating simultaneously for many values . By the linearity of the series approximations, the above parameters can be seen as linear functions of the least squares coefficients up to an approximation error, that is

| (2.5) |

where is the series approximation, with denoting the -vector of loadings on the coefficients, and is the remainder term, which corresponds to the approximation error. Indeed, the decomposition (2.5) arises from the application of different linear operators to the decomposition and evaluating the resulting functions at :

| (2.6) |

Examples of the operator corresponding to the cases enumerated in the introduction are given by, respectively,

-

1.

a differential operator: , so that

-

2.

an integro-differential operator: , so that

-

3.

a partial integro-differential operator: , so that

where is a subvector of . For notational convenience, we use the formulation (2.5) in the analysis, instead of the motivational formulation (2.6).

We shall provide the inference tools that will be valid for inference on the series approximation

If the approximation error is small enough as compared to the estimation error, these tools will also be valid for inference on the functional of interest

In this case, the series approximation is an important intermediary target, whereas the functional is the ultimate target. The inference will be based on the plug-in estimator of the the series approximation and hence of the final target .

3. Approximation Properties of Least Squares

Next we consider approximation properties of the least squares estimator. Not surprisingly, approximation properties must rely on the particular choice of approximating functions. At this point it is instructive to consider particular examples of relevant bases used in the literature. For each example, we state a bound on the following quantity:

This quantity will play a key role in our analysis.111 Most results extend directly to the case that holds with probability . We refer to Hansen (2014) for recent results that explicit allows for unbounded regressors which required extending the concentration inequalities for matrices. Excellent reviews of approximating properties of different series can also be found in Huang (1998) and Chen (2007), where additional references are provided.

Example 3.1 (Polynomial series).

Let and consider a polynomial series given by

In order to reduce collinearity problems, it is useful to orthonormalize the polynomial series with respect to the Lebesgue measure on to get the Legendre polynomial series

The Legendre polynomial series satisfies

see, for example, Newey (1997). ∎

Example 3.2 (Fourier series).

Let and consider a Fourier series given by

for odd. Fourier series is orthonormal with respect to the Lebesgue measure on and satisfies

which follows trivially from the fact that every element of is bounded in absolute value by one.∎

Example 3.3 (Spline series).

Let and consider the linear regression spline series, or regression spline series of order 1, with a finite number of equally spaced knots in :

or consider the cubic regression spline series, or regression spline series of order 3, with a finite number of equally spaced knots :

Similarly, one can define the regression spline series of any order (here is a nonnegative integer). The function constructed using regression splines of order is times continuously differentiable in for any . Instead of regression splines, it is often helpful to consider B-splines , which are linear transformations of the regression splines with lower multicollinearity; see De Boor (2001) for the introduction to the theory of splines. B-splines are local in the sense that each B-spline is supported on the interval for some and satisfying and there is at most non-zero B-splines on each interval . From this property of B-splines, it is easy to see that B-spline series satisfies

see, for example, Newey (1997). ∎

Example 3.4 (Cohen-Deubechies-Vial wavelet series).

Let and consider Cohen-Deubechies-Vial (CDV) wavelet bases; see Section 4 in Cohen et al. (1993), Chapter 7.5 in Mallat (2009), and Chapter 7 and Appendix B in Johnstone (2011) for details on CDV wavelet bases. CDV wavelet bases is a class of orthonormal with respect to the Lebesgue measure on bases. Each such basis is built from a Daubechies scaling function (defined on ) and the wavelet of order starting from a fixed resolution level such that . The functions and are supported on and , respectively. Translate so that it has the support . Let

Then we can create the CDV wavelet basis from these functions as follows. Take all the functions , , that are supported in the interior of (these are functions with and with ). Denote these functions , . To this set of functions, add suitable boundary corrected functions , , , , , so that forms an orthonormal basis of . Suppose that for some . Then the CDV series takes the form:

This series satisfies

This bound can be derived by the same argument as that for B-splines (see, for example, Kato, 2013, Lemma 1 (i) for its proof). CDV wavelet bases is a flexible tool to approximate many different function classes. See, for example, Johnstone (2011), Appendix B. ∎

Example 3.5 (Local polynomial partition series).

Let and define a local polynomial partition series as follows. Let be a nonnegative integer. Partition as where where is the largest integer that is strictly smaller than . For , define by if and otherwise. For , define

for all . Finally, define the local polynomial partition series of order as an orthonormalization of with respect to the Lebesgue (or some other) measure on . The local polynomial partition series estimator was analyzed in detail in Cattaneo and Farrell (2013). Its properties are somewhat similar to those of local polynomial estimator of Stone (1982). When the partition satisfies , that is there exist constants independent of and such that for all , and the Lebesgue measure is used, the local polynomial partition series satisfies

This bound can be derived by the same argument as that for B-splines.∎

Example 3.6 (Tensor Products).

Generalizations to multiple covariates are straightforward using tensor products of unidimensional series. Suppose that the basic regressors are

Then we can create series for each basic regressor. Then we take all interactions of functions from these series, called tensor products, and collect them into a vector of regressors . If each series for a basic regressor has terms, then the final regressor has dimension

which explodes exponentially in the dimension . The bounds on in terms of remain the same as in one-dimensional case.∎

Each basis described in Examples 3.1-3.6 has different approximation properties which also depend on the particular class of functions . The following assumption captures the essence of this dependence into two quantities.

Condition A.3 (Approximation) For each and , there are finite constants and such that for each ,

Here is defined by (2.2) and (2.3) with replaced by . We call the Lebesgue factor because of its relation to the Lebesgue constant defined in Section 3.2 below. Together and characterize the approximation properties of the underlying class of functions under and uniform distances. Note that constants and are allowed to depend but we omit indexing by for simplicity of notation. Next we discuss primitive bounds on and .

3.1. Bounds on

In what follows, we call the case where as the correctly specified case. In particular, if the series are formed from bases that span , then as . However, if series are formed from bases that do not span , then as . We call any case where the incorrectly specified (misspecified) case.

To give an example of the misspecified case, suppose that , so that and . Further, suppose that the researcher mistakenly assumes that is additively separable in and : . Given this assumption, the researcher forms the vector of approximating functions such that each component of this vector depends either on or but not on both; see Newey (1997) and Newey et al. (1999) for the description of nonparametric series estimators of separately additive models. Then note that if the true function is not separately additive, linear combinations will not be able to accurately approximate for any , so that does not converge to zero as . Since analysis of misspecified models plays an important role in econometrics, we include results both for correctly and incorrectly specified models.

To provide a bound on , note that for any ,

so that it suffices to set such that . Next, the bounds for are readily available from the Approximation Theory; see DeVore and Lorentz (1993). A typical example is based on the concept of -smooth classes, namely Hölder classes of smoothness order , . For , the Hölder class of smoothness order , , is defined as the set of all functions such that for ,

for all and in . The smallest satisfying this inequality defines a norm of in , which we denote by . For , can be defined as follows. For a -tuple of nonnegative integers, let

Let denote the largest integer strictly smaller than . Then is defined as the set of all functions such that is times continuously differentiable and for some ,

for all and in and for all -tuples and of nonnegative integers satisfying and . Again, the smallest satisfying these inequalities defines a norm of in , which we denote .

If is a set of functions in such that is bounded from above uniformly over all (that is, is contained in a ball in of finite radius), then we can take

| (3.7) |

for the polynomial series and

for spline, CDV wavelet, and local polynomial partition series of order . If in addition we assume that each element of can be extended to a periodic function, then (3.7) also holds for the Fourier series. See, for example, Newey (1997) and Chen (2007) for references.

3.2. Bounds on

We say that a least squares approximation by a particular series for the function class is co-minimal if the Lebesgue factor is small in the sense of being a slowly varying function in . A simple bound on , which is independent of , is established in the following proposition:

Proposition 3.1.

If is chosen so that , then Condition A.3 holds with

The proof of this proposition is based on the ideas of Newey (1997) and is provided in the Appendix. The advantage of the bound established in this proposition is that it is universally applicable. It is, however, not sharp in many cases because satisfies

so that in all cases. Much sharper bounds follow from Approximation Theory for some important cases. To apply these bounds, define the Lebesgue constant:

where . The following proposition provides a bound on in terms of :

Proposition 3.2.

If is chosen so that , then Condition A.3 holds with

Note that in all examples above, we provided such that , and so the results of Propositions 3.1 and 3.2 apply in our examples. We now provide bounds on .

Example 3.7 (Fourier series, continued).

For Fourier series on , , and

where here and below and are some universal constants; see Zygmund (2002).∎

Example 3.8 (Spline series, continued).

For continuous B-spline series on , , and

under approximately uniform placement of knots; see Huang (2003b). In fact, the result of Huang states that whenever has the pdf on bounded from above by and below from zero by where is a constant that depends only on and .∎

Example 3.9 (Wavelet series, continued).

For continuous CDV wavelet series on , , and

The proof of this result was recently obtained by Chen and Christensen (2015) who extended the argument of Huang (2003b) for B-splines to cover wavelets. In fact, the result of Chen and Christensen also shows that whenever has the pdf on bounded from above by and below from zero by where is a constant that depends only on and .∎

Example 3.10 (Local polynomial partition series, continued).

For local polynomial partition series on , , and ,

To prove this bound, note that first order conditions imply that for any ,

Hence, for any ,

where the last inequality follows by noting that the sum contains at most nonzero terms, all nonzero terms in the sum are bounded by , and outside of a set with probability bounded from above by up to a constant. The bound follows. Moreover, the bound continues to hold whenever has the pdf on bounded from above by and below from zero by where is a constant that depends only on and . ∎

Example 3.11 (Polynomial series, continued).

Example 3.12 (Legendre Polynomials).

For Legendre polynomials that form an orthonormal basis on with respect to , and

for some constants . See, for example, DeVore and Lorentz (1993)). This means that even though some series schemes generate well-behaved uniform approximations, others – Legendre polynomials – do not in general. However, the following example specifies “tailored” function classes, for which Legendre and other series methods do automatically provide uniformly well-behaved approximations. ∎

Example 3.13 (Tailored Function Classes).

For each type of series approximations, it is possible to specify function classes for which the Lebesgue factors are constant or slowly varying with . Specifically, consider a collection

where or . This example captures the idea, that for each type of series functions there are function classes that are well-approximated by this type. For example, Legendre polynomials may have poor Lebesgue factors in general, but there are well-defined function classes, where Legendre polynomials have well-behaved Lebesgue factors. This explains why polynomial approximations, for example, using Legendre polynomials, are frequently employed in empirical work. We provide an empirically relevant example below, where polynomial approximation works just as well as a B-spline approximation. In economic examples, both polynomial approximations and B-spline approximations are well-motivated if we consider them as more flexible forms of well-known, well-motivated functional forms in economics (for example, as more flexible versions of the linear-quadratic Mincer equations, or the more flexible versions of translog demand and production functions). ∎

The following example illustrate the performance of the series estimator using different bases for a real data set.

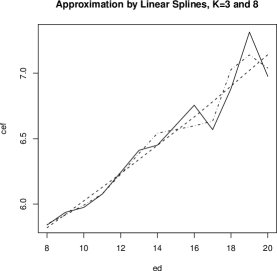

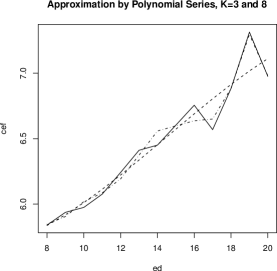

Example 3.14 (Approximations of Conditional Expected Wage Function).

Here is the mean of log wage () conditional on education

The function is computed using population data – the 1990 Census data for the U.S. men of prime age; see Angrist et al. (2006) for more details. So in this example, we know the true population function . We would like to know how well this function is approximated when common approximation methods are used to form the regressors. For simplicity we assume that is uniformly distributed (otherwise we can weigh by the frequency). In population, least squares estimator solves the approximation problem: for , where we form as (a) linear spline (Figure 1, left) and (b) polynomial series (Figure 1, right), such that dimension of is either or . It is clear from these graphs that spline and polynomial series yield similar approximations.

|

|

In the table below, we also present and norms of approximating errors:

| spline | spline | Poly | Poly | |

|---|---|---|---|---|

| Error | 0.12 | 0.08 | 0.12 | 0.05 |

| Error | 0.29 | 0.17 | 0.30 | 0.12 |

We see from the table that in this example, the Lebesgue factor, which is defined as the ratio of to errors, of the polynomial approximations is comparable to the Lebesgue factor of the spline approximations. ∎

4. Limit Theory

4.1. Limit Theory

After we have established the set-up, we proceed to derive our results. We start with a result on the rate of convergence. Recall that . In the theorem below, we assume that . This is a mild regularity condition.

Theorem 4.1 ( rate of convergence).

Assume that Conditions A.1-A.3 are satisfied. In addition, assume that and . Then under ,

| (4.8) |

and under ,

| (4.9) |

Comment 4.1.

(i) This is our first main result in this paper. The condition , which we impose, weakens (hence generalizes) the conditions imposed in Newey (1997) who required . For series satisfying , the condition amounts to

| (4.10) |

This condition is the same as that imposed in Stone (1994), Huang (2003a), and recently by Cattaneo and Farrell (2013) but the result (4.8) is obtained under the condition (4.10) in Stone (1994) and Huang (2003a) only for spline series and in Cattaneo and Farrell (2013) only for local polynomial partition series. Therefore, our result improves on those in the literature by weakening the rate requirements on the growth of (with respect to ) and/or by allowing for a wider set of series functions.

(ii) Under the correct specification (), the fastest rate of convergence is achieved by setting so that the approximation error and the sampling error are of the same order,

One consequence of this result is that for Hölder classes of smoothness order , , with , we obtain the optimal rate of convergence by setting , which is allowed under our conditions for all if (Fourier, spline, wavelet, and local polynomial partition series). On the other hand, if is growing faster than , then it is not possible to achieve optimal rate of convergence for some . For example, for polynomial series considered above, , and so the condition becomes . Hence, optimal rate of convergence is achieved by polynomial series only if or, equivalently, . Even though this condition is somewhat restrictive, it weakens the condition in Newey (1997) who required for polynomial series, so that optimal rate in his analysis could be achieved only if or, equivalently, . Therefore, our results allow to achieve optimal rate of convergence in a larger set of classes of functions for particular series.

(iii) The result (4.9) is concerned with the case when the model is misspecified (). It shows that when and , the estimator converges in to the surrogate function that provides the best linear approximation to the target function . In this case, the estimator does not generally converge in to the target function . ∎

4.2. Pointwise Limit Theory

Next we focus on pointwise limit theory (some authors refer to pointwise limit theory as local asymptotics; see Huang (2003b)). That is, we study asymptotic behavior of and for particular and . Here denotes the space of vectors in with unit Euclidean norm: . Note that both and implicitly depend on . As we will show, pointwise results can be achieved under weak conditions similar to those we required in Theorem 4.1. The following lemma plays a key role in our asymptotic pointwise normality result.

Lemma 4.1 (Pointwise Linearization).

Assume that Conditions A.1-A.3 are satisfied. In addition, assume that and . Then for any ,

| (4.11) |

where the term , summarizing the impact of unknown design, obeys

| (4.12) |

Moreover,

| (4.13) |

where the term , summarizing the impact of approximation error on the sampling error of the estimator, obeys

| (4.14) |

Comment 4.2.

(i) In summary, the only condition that generally matters for linearization (4.11)-(4.12) is that , which holds if and . In particular, linearization (4.11)-(4.12) allows for misspecification ( is not required). In principle, linearization (4.13)-(4.14) also allows for misspecification but the bounds are only useful if the model is correctly specified, so that . As in the theorem on rate of convergence, our main condition is that .

(ii) We conjecture that the bound on can be improved for splines to

| (4.15) |

since it is attained by local polynomials and splines are also similarly localized.∎

With the help of Lemma 4.1, we derive our asymptotic pointwise normality result. We will use the following additional notation:

In the theorem below, we will impose the condition that as uniformly over . This is a mild uniform integrability condition. Specifically, it holds if for some , . In addition, we will impose the condition that . This condition is used to properly normalize the estimator.

Theorem 4.2 (Pointwise Normality).

Assume that Conditions A.1-A.3 are satisfied. In addition, assume that (i) as uniformly over , (ii) , and (iii) . Then for any ,

| (4.16) |

where we set but if , then we can set . Moreover, for any and ,

| (4.17) |

and if the approximation error is negligible relative to the estimation error, namely , then

| (4.18) |

Comment 4.3.

(i) This is our second main result in this paper. The result delivers pointwise convergence in distribution for any sequences and with and . In fact, the proof of the theorem implies that the convergence is uniform over all sequences. Note that the normalization factor is the pointwise standard error, and it is of a typical order at most points. In this case the condition for negligibility of approximation error , which can be understood as an undersmoothing condition, can be replaced by

When , which is often the case if is contained in a ball in of finite radius (see our examples in the previous section), this condition substantially weakens an assumption in Newey (1997) who required in a similar set-up.

(ii) When applied to splines, our result is somewhat less sharp than that of Huang (2003b). Specifically, Huang required that and whereas we require in addition to Huang’s conditions (see condition (iii) of the theorem). The difference can likely be explained by the fact that we use linearization bound (4.12) whereas for splines it is likely that (4.15) holds as well.

4.3. Uniform Limit Theory

Finally, we turn to a uniform limit theory. Not surprising, stronger conditions are required for our results to hold when compared to the pointwise case. Let . We will need the following assumption on the tails of the regression errors.

Condition A.4 (Disturbances) Regression errors satisfy .

It will be convenient to denote in this subsection. Moreover, denote

We will also need the following assumption on the basis functions to hold with the same as that in Condition A.4.

Condition A.5 (Basis) Basis functions are such that (i) , (ii) , and (iii) .

The following lemma provides uniform linearization of the series estimator and plays a key role in our derivation of the uniform rate of convergence.

Lemma 4.2 (Uniform Linearization).

Assume that Conditions A.1-A.5 are satisfied. Then

| (4.19) |

where , summarizing the impact of unknown design, obeys

| (4.20) |

uniformly over . Moreover,

| (4.21) |

where , summarizing the impact of approximation error on the sampling error of the estimator, obeys

| (4.22) |

uniformly over .

Comment 4.4.

As in the case of pointwise linearization, our results on uniform linearization (4.19)-(4.20) allow for misspecification ( is not required). In principle, linearization (4.21)-(4.22) also allows for misspecification but the bounds are most useful if the model is correctly specified so that . We are not aware of any similar uniform linearization result in the literature. We believe that this result is useful in a variety of problems. Below we use this result to derive good uniform rate of convergence of the series estimator. Another application of this result would be in testing shape restrictions in the nonparametric model. ∎

The following theorem provides uniform rate of convergence of the series estimator.

Theorem 4.3 (Uniform Rate of Convergence).

Assume that Conditions A.1-A.5 are satisfied. Then

| (4.23) |

Moreover, for and given above we have

| (4.24) |

and

| (4.25) |

Comment 4.5.

This is our third main result in this paper. Assume that is a ball in of finite radius, , , and . Then the bound in (4.25) becomes

Therefore, setting , we obtain

which is the optimal uniform rate of convergence in the function class ; see Stone (1982). To the best of our knowledge, our paper is the first to show that the series estimator attains the optimal uniform rate of convergence under these rather general conditions; see the next comment. We also note here that it has been known for a long time that a local polynomial (kernel) estimator achieves the same optimal uniform rate of convergence; see, for example, Tsybakov (2009), and it was also shown recently by Cattaneo and Farrell (2013) that local polynomial partition series estimator also achieves the same rate. Recently, in an effort to relax the independence assumption, the working paper Chen and Christensen (2015), which appeared in ArXiv in 2013, approximately 1 year after our paper was posted to ArXiv and submitted for publication, 222Our paper was submitted for publication and to ArXiv on December 3, 2012. Our result as stated here did not change since the original submission. derived similar uniform rate of convergence result allowing for -mixing conditions, see their Theorem 4.1 for specific conditions.∎

Comment 4.6.

Primitive conditions leading to inequalities and are discussed in the previous section. Also, under the assumption that , inequality follows automatically from the definition of . Thus, one of the critical conditions to attain the optimal uniform rate of convergence is that we require . Under our other assumptions, this condition holds if and , and so we can set if and or, equivalently, and . ∎

After establishing the auxiliary results on the uniform rate of convergence, we present two results on inference based on the series estimator. The first result on inference is concerned with the strong approximation of a series process by a Gaussian process and is a (relatively) minor extension of the result obtained by Chernozhukov et al. (2013). The extension is undertaken to allow for a non-vanishing specification error to cover misspecified models. In particular, we make a distinction between and which are potentially asymptotically different if . To state the result, let be some sequence of positive numbers satisfying .

Theorem 4.4 (Strong Approximation by a Gaussian Process).

Assume that Conditions A.1-A.5 are satisfied with . In addition, assume that (i) , (ii) , and (iii) Then for some ,

| (4.26) |

so that for ,

| (4.27) |

and if , then

| (4.28) |

where we set but if , then we can set .

Comment 4.7.

One might hope to have a result of the form

| (4.29) |

where is some fixed zero-mean Gaussian process. However, one can show that the process on the left-hand side of (4.29) is not asymptotically equicontinuous, and so it does not have a limit distribution. Instead, Theorem 4.4 provides an approximation of the series process by a sequence of zero-mean Gaussian processes

with the stochastic error of size . Since , under our conditions the theorem implies that the series process is well approximated by a Gaussian process, and so the theorem can be interpreted as saying that in large samples, the distribution of the series process depends on the distribution of the data only via covariance matrix ; hence, it allows us to perform inference based on the whole series process. Note that the conditions of the theorem are quite strong in terms of growth requirements on , but the result of the theorem is also much stronger than the pointwise normality result: it asserts that the entire series process is uniformly close to a Gaussian process of the stated form. ∎

Our result on the strong approximation by a Gaussian process plays an important role in our second result on inference that is concerned with the weighted bootstrap. Consider a set of weights that are i.i.d. draws from the standard exponential distribution and are independent of the data. For each draw of such weights, define the weighted bootstrap draw of the least squares estimator as a solution to the least squares problem weighted by , namely

| (4.30) |

For all , denote . The following theorem establishes a new result that states that the weighted bootstrap distribution is valid for approximating the distribution of the series process.

Theorem 4.5 (Weighted Bootstrap Method).

(1) Assume that Conditions A.1-A.5 are satisfied. In addition, assume that . Then the weighted bootstrap process satisfies

where obeys

| (4.31) |

uniformly over .

(2) If, in addition, Conditions A.4 and A.5 are satisfied with and (i) , (ii) , and (iii) hold, then for and some ,

| (4.32) |

and so

| (4.33) |

where we set , but if , then we can set

Comment 4.8.

(i) This is our fourth main and new result in this paper. The theorem implies that the weighted bootstrap process can be approximated by a copy of the same Gaussian process as that used to approximate original series process.

(ii) We emphasize that the theorem does not require the correct specification, that is the case is allowed. Also, in this theorem, symbol refers to a joint probability measure with respect to the data and the set of bootstrap weights .∎

We close this section by establishing sufficient conditions for consistent estimation of . Recall that . In addition, denote , , and where , and let .

Theorem 4.6 (Matrices Estimation).

Assume that Conditions A.1-A.5 are satisfied. In addition, assume that . Then

Moreover, for and ,

Comment 4.9.

Theorem 4.6 allows for consistent estimation of the matrix under the mild condition and for consistent estimation of the matrices and under somewhat more restricted conditions. Not surprisingly, the estimation of and depends on the tail behavior of the error term via the value of . Note that under Condition A.4, we have that . ∎

5. Rates and Inference on Linear Functionals

In this section, we derive rates and inference results for linear functionals of the conditional expectation function such as its derivative, average derivative, or conditional average derivative. To a large extent, with the exception of Theorem 5.6, the results presented in this section can be considered as an extension of results presented in Section 4, and so similar comments can be applied as those given in Section 4. Theorem 5.6 deals with construction of uniform confidence bands for linear functionals under weak conditions and is a new result.

By the linearity of the series approximations, the linear functionals can be seen as linear functions of the least squares coefficients up to an approximation error, that is

where is the series approximation, with denoting the -vector of loadings on the coefficients, and is the remainder term, which corresponds to the approximation error. Throughout this section, we assume that is a subset of some Euclidean space equipped with its usual norm . We allow to depend on but for simplicity, we assume that the diameter of is bounded from above uniformly over . Results allowing for the case where is expanding as grows can be covered as well with slightly more technicalities.

In order to perform inference, we construct estimators of , the variance of the associated linear functionals, as

| (5.34) |

In what follows, it will be convenient to have the following result on consistency of :

Lemma 5.1 (Variance Estimation for Linear Functionals).

Assume that Conditions A.1-A.5 are satisfied. In addition, assume that (i) and (ii) . Then

uniformly over .

By Lemma 5.1, under our conditions, (5.34) is uniformly consistent for in the sense that uniformly over .

5.1. Pointwise Limit Theory for Linear Functionals

We now present a result on pointwise rate of convergence for linear functionals. The rate we derive is . Some examples with explicit bounds on are given below.

Theorem 5.1 (Pointwise Rate of Convergence for Linear Functionals).

Assume that Conditions A.1-A.3 are satisfied. In addition, assume that (i) , (ii) , (iii) , and (iv) . Then

Comment 5.1.

(i) This theorem shows in particular that is -consistent whenever . A simple example of this case is . In this example, , and so where the last inequality follows from the argument used in the proof of Proposition 3.1. Another simple example is . In this example, is a -vector whose first component is 1 and all other components are 0, and so . This example trivially implies -consistency of the series estimator of the linear part of the partially linear model. Yet another example, which is discussed in Newey (1997), is the average partial derivative.

(ii) Condition imposed in this theorem can be understood as undersmoothing condition. Unfortunately, to the best of our knowledge, there is no theoretically justified practical procedure in the literature that would lead to a desired level of undersmoothing. Some ad hoc suggestions include using cross validation or “plug-in” method to determine the number of series terms that would minimize the asymptotic integrated mean-square error of the series estimator (see Hardle, 1990) and then blow up the estimated number of series terms by some number that grows to infinity as the sample size increases.∎

To perform pointwise inference, we consider the t-statistic:

We can carry out standard inference based on this statistic because of the following theorem.

Theorem 5.2 (Pointwise Inference for Linear Functionals).

The same comments apply here as those given in Section 4.2 for pointwise results on estimating the function itself.

5.2. Uniform Limit Theory for Linear Functionals

In obtaining uniform rates of convergence and inference results for linear functionals, we will denote

The value of depends on the choice of the basis for the series estimator and on the linear functional. Newey (1997) and Chen (2007) provide several examples. In the case of splines with , it has been established that and ; see, for example, Newey (1997). With this basis we have for

-

1.

the function itself: , , and ;

-

2.

the derivatives: , , ;

-

3.

the average derivatives: , , and ,

where in the last example it is assumed that , is continuously distributed with the density bounded below from zero on , and is continuous on with uniformly in for all .

We will impose the following regularity condition on the loadings on the coefficients :

Condition A.6 (Loadings) Loadings on the coefficients satisfy (i) and (ii) .

The first part of this condition implies that the linear functional is normalized appropriately. The second part is a very mild restriction on the rate of the growth of the Lipschitz coefficient of the map .

Under Conditions A.1-A.6, results presented in Lemma 4.2 on uniform linearization can be extended to cover general linear functionals considered here:

Lemma 5.2 (Uniform Linearization for Linear Functionals).

Assume that Conditions A.1-A.6 are satisfied. Then for ,

where , summarizing the impact of unknown design, obeys

uniformly over . Moreover,

where , summarizing the impact of approximation error on the sampling error of the estimator, obeys

uniformly over .

From Lemma 5.2, we can derive the following theorem on uniform rate of convergence for linear functionals.

Theorem 5.3 (Uniform Rate of Convergence for Linear Functionals).

Assume that Conditions A.1-A.6 are satisfied. Then

| (5.35) |

If, in addition, we assume that (i) and (ii) , then

| (5.36) |

Theorem 5.3 establishes uniform rates that are up to factor agree with the pointwise rates. The requirement (ii) on the approximation error can be seen as an undersmoothing condition as discussed in Comment 5.1.

Next, we consider the problem of uniform inference for linear functionals based on the series estimator. We base our inference on the t-statistic process:

| (5.37) |

We present two results for inference on linear functionals. The first result is an extension of Theorem 4.4 on strong approximations to cover the case of linear functionals. As we discussed in Comment 4.7, in order to perform uniform in inference on , we would like to approximate the distribution of the whole process (5.37). However, one can show that this process typically does not have a limit distribution in . Yet, we can construct a Gaussian process that would be close to the process (5.37) for all simultaneously with a high probability. Specifically, we will approximate the -statistic process by the following Gaussian coupling:

| (5.38) |

where denotes a vector of i.i.d. random variables.

Theorem 5.4 (Strong Approximation by a Gaussian Process for Linear Functionals).

Assume that the conditions of Theorem 4.4 and Condition A.6 are satisfied. In addition, assume that (i) and (ii) . Then

As in the case of inference on the function , we could also consider the use of the weighted bootstrap method to obtain a result analogous to that in Theorem 4.5. For brevity of the paper, however, we do not consider weighted bootstrap method here.

The second result on inference for linear functionals is new and concerns with the problem of constructing uniform confidence bands for the linear functional . Specifically, we are interested in the confidence bands of the form

| (5.39) |

where is chosen so that for all with the prescribed probability where is a user-specified level. For this purpose, we would like to set as the -quantile of . However, this choice is infeasible because the exact distribution of is unknown. Instead, Theorem 5.4 suggests that we can set as the -quantile of or, if is unknown and has to be estimated, that we can set

| (5.40) |

where

and . Note that defined in (5.40) can be approximated numerically by simulation. Yet, conditions of Theorem 5.4 are rather strong. Fortunately, Chernozhukov et al. (2012a) noticed that when we are only interested in the supremum of the process and do not need the process itself, sufficient conditions for the strong approximation can be much weaker. Specifically, we have the following theorem, which is an application of a general result obtained in Chernozhukov et al. (2012a):

Theorem 5.5 (Strong Approximation of Suprema for Linear Functionals).

Assume that Conditions A.1-A.6 are satisfied with . In addition, assume that (i) , (ii) , (iii) , and (iv) . Then

Construction of uniform confidence bands also critically relies on the following anti-concentration lemma due to Chernozhukov et al. (2014) (Corollary 2.1):

Lemma 5.3 (Anti-concentration for Separable Gaussian Processes).

Let be a separable Gaussian process indexed by a semimetric space such that and for all . Assume that a.s. Then and

for all and some absolute constant .

From Theorem 5.5 and Lemma 5.3, we can now derive the following result on uniform validity of confidence bands in (5.39):

Theorem 5.6 (Uniform Inference for Linear Functionals).

Comment 5.2.

(i) This is our fifth (and last) main result in this paper. The theorem shows that the confidence bands constructed above maintain the required level asymptotically and establishes that the uniform width of the bands is of the same order as the uniform rate of convergence. Moreover, confidence intervals are asymptotically similar.

(ii) The proof strategy of Theorem 5.6 is similar to that proposed in Chernozhukov et al. (2013) for inference on the minimum of a function. Since the limit distribution may not exists, the insight was to use distributions provided by couplings. Because the limit distribution does not necessarily exist, it is not immediately clear that the confidence bands are asymptotically similar or at least maintain the right asymptotic level. Nonetheless, we show that the confidence bands are asymptotically similar with the help of anti-concentration lemma stated above.

(iii) Theorem 5.6 only considers two-sided confidence bands. However, both Theorem 5.5 and Lemma 5.3 continue to hold if we replace suprema of absolute values of the processes by suprema of the processes itself, namely if we replace and in Theorem 5.5 by and , respectively, and in Lemma 5.3 by . Therefore, we can show that Theorem 5.6 also applies for one-sided confidence bands, namely Theorem 5.6 holds with defined as the conditional -quantile of given the data and the confidence bands defined by for all .∎

6. Tools: Maximal Inequalities for Matrices and Empirical Processes

In this section we collect the main technical tools that our analysis rely upon, namely Khinchin Inequalities for Matrices and Data Dependent Maximal Inequalities.

6.1. Khinchin Inequalities for Matrices

For , consider the Schatten norm on symmetric matrices defined by

where is the system of eigenvalues of . The case recovers the operator norm and the Frobenius norm. It is obvious that for any

Therefore, setting and observing that for any , we get the relation:

| (6.44) |

Lemma 6.1 (Khinchin Inequality for Matrices).

For symmetric -matrices , , , and an i.i.d. sequence of Rademacher variables , we have

| (6.45) |

for some absolute constant . As a consequence, we have for

| (6.46) |

for some (possibly different) absolute constant .

This version of the Khinchin inequality is proven in Section 3 of Rudelson (1999). We also provide some details of the proof in the Appendix. The notable feature of this inequality is the factor instead of the factor expected from the conventional maximal inequalities based on entropy. This inequality due to Lust-Picard and Pisier (1991) generalizes the Khinchin inequality for vectors. A version of this inequality was derived by Guédon and Rudelson (2007) using generalized entropy (majorizing measure) arguments. This is a striking example where the use of generalized entropy yields drastic improvements over the use of entropy. Prior to this, Talagrand (1996a) provided ellipsoidal examples where the difference between the two approaches was even more extreme.

6.2. LLN for Matrices

The following lemma is a variant of a fundamental result obtained by Rudelson (1999).

Lemma 6.2 (Rudelson’s LLN for Matrices).

Let be a sequence of independent symmetric non-negative -matrix valued random variables with such that and a.s., then for

In particular, if , with a.s., then

For completeness, we provide the proof of this lemma in the Appendix; see also Tropp (2012) for a nice exposition of this result as well as many others concerning with maximal and deviation inequalities for matrices.

6.3. Maximal Inequalities

Consider a measurable space , and a suitably measurable class of functions mapping to , equipped with a measurable envelope function . (By “suitably measurable” we mean the condition given in Section 2.3.1 of van der Vaart and Wellner (1996); pointwise measurablity and Suslin measurability are sufficient.) The covering number is the minimal number of -balls of radius needed to cover . The covering number relative to the envelope function is given by

| (6.47) |

The entropy is the logarithm of the covering number.

We rely on the following result.

Proposition 6.1.

Let be i.i.d. random vectors, defined on an underlying -fold product probability space, in with and where denotes the support of . Let be a class of functions on such that (normalization) and for all . Let . Suppose that there exist constants and such that

for all for the envelope . If for some , then

where is a universal constant.

The proof is based on a truncation argument and maximal inequalities for uniformly bounded classes of functions developed in Giné and Koltchinskii (2006). We recall its version.

Theorem 6.1 (Giné and Koltchinskii (2006)).

Let be i.i.d. random variables taking values in a measurable space with common distribution , defined on the underlying -fold product probability space. Let be a suitably measurable class of functions mapping to with a measurable envelope . Let be a constant such that . Suppose that there exist constants and such that for all . Then,

where is a universal constant.

Acknowledgements.

This paper was presented and first circulated in a series of lectures given by Victor Chernozhukov at “Stats in the Château” Statistics Summer School on “Inverse Problems and High-Dimensional Statistics” in 2009 near Paris. Participants, especially Xiaohong Chen, and one of several referees made numerous helpful suggestions. We also thank Bruce Hansen for extremely useful comments.

Appendix A Proofs

A.1. Proofs of Sections 2 and 3

Proof of Proposition 2.1.

Recall that . Since is bounded above and away from zero on , and regressors are orthonormal under , we have

uniformly over all . The asserted claim follows. ∎

Proof of Proposition 3.1.

Fix . Let

Then

Further, first order conditions imply that , and so for any ,

This implies that

Moreover, since , is the coefficient on of the projection of onto , and so

Conclude that

and so Condition A.3 holds with . This completes the proof of the proposition. ∎

Proof of Proposition 3.2.

Fix . Define by

Note that for any functions , . Therefore,

and so we obtain

where on the third line we used the definition of . Hence,

Next,

implies that

and so Condition A.3 holds with . This completes the proof of the proposition. ∎

A.2. Proofs of Section 4.1

Proof of Theorem 4.1.

We have that

where under the normalization we have

Further,

By the Matrix LLN (Lemma 6.2), which is the critical step, we have that

Therefore, wp 1, all eigenvalues of are bounded away from zero. Indeed, if at least one eigenvalue of is strictly smaller than 1/2, then there exists a vector such that , and so

Hence, wp 1, all eigenvalues of are not smaller than 1/2. Therefore,

where the second inequality follows from

since is bounded. Moreover, since is a sample projection of on ,

| (A.48) |

by Markov’s inequality. Therefore, when ,

where the first inequality follows from all eigenvalues of being bounded away from zero wp 1 and the second from (A.48). This completes the proof of (4.8).

A.3. Proofs of Section 4.2

Proof of Lemma 4.1.

Decompose

We divide the proof in three steps. Steps 1 and 2 establish (4.12), the bound on . Step 3 proves (4.14), the bound on .

Step 1. Conditional on , the term

has mean zero and variance bounded by . Next, as in the proof of Theorem 4.1, wp 1, all eigenvalues of are bounded away from zero and from above, and so

where the second inequality follows from Matrix LLN (Lemma 6.2) and . We then conclude by Chebyshev’s inequality that

Step 2. By Matrix LLN (Lemma 6.2), , and so

where we used the bound obtained in the proof of Theorem 4.1. Steps 1 and 2 give the linearization result (4.12).

Step 3. Since , the term

has mean zero and variance

Thus, (4.14) follows from Chebyshev’s inequality. This completes the proof of the lemma. ∎

Proof of Theorem 4.2.

Note that (4.17) follows by applying (4.16) with , and (4.18) follows directly from (4.17). Therefore, it suffices to prove (4.16).

Observe that for any , because and

| (A.50) |

in the positive semidefinite sense. Further, by condition (iii) of the theorem and Lemma 4.1, (note that we can apply Lemma 4.1 because follows from condition (i) and follows from condition (iii) of the theorem). Therefore, we can write

where

Further, it follows from (A.50) that

| (A.51) |

Now we verify Lindberg’s condition for the CLT. First, by construction we have

Second, for each

since the left hand side is bounded by

and both terms go to zero. Indeed, the first term is bounded from above for some by

where we used (A.51), the uniform integrability in the condition (i) and , which follows from the condition (iii); the second term is bounded from above by

by Chebyshev’s inequality where we used (A.51), , and . ∎

A.4. Proofs of Section 4.3

Proof of Lemma 4.2.

Decompose

We divide the proof in three steps. Steps 1 and 2 establish (4.20), the bound on . Step 3 proves (4.22), the bound on .

Step 1. Here we show that

| (A.52) |

Conditional on the data, let . Define the norm on by . Recall that for , an -net of a normed space is a subset of such that for every there exists a point with . The covering number of is the infimum of the cardinality of -nets of .

Let be independent Rademacher random variables () that are independent of the data, and denote . Also, let denote the expectation with respect to the distribution of . Then by Dudley’s inequality Dudley (1967),

where

Since for any ,

we have for some ,

Thus we have

By A.4, we have where . In addition, note that for implies that . Therefore, we have and . Hence, it follows from that

where the first line is due to the symmetrization inequality. Thus, (A.52) follows.

Step 2. Observe that

where the second inequality was shown in the proof of Lemma 4.1. Now, Steps 1 and 2 give the linearizarion result (4.20).

Step 3. We wish to bound . We use Theorem 6.1. Consider the class of functions

Then, , , and for any ,

so that for some ,

Thus, using conditions (ii) and (iii) of A.5, we have by Theorem 6.1 that

where we have used the fact that

Therefore, we have by Markov’s inequality

| (A.53) |

So, the linearization result (4.22) follows. This completes the proof. ∎

Proof of Theorem 4.3.

Note that (4.24) and (4.25) follow from (4.23) and Lemma 4.2. Therefore, it suffices to prove (4.23), and so we wish to bound . To this end, we use Proposition 6.1. Consider the class of functions

Then, , and for any ,

Thus, taking , we have

Therefore, by Proposition 6.1, we have

| (A.54) |

where we have used the following inequality

This completes the proof. ∎

Proof of Theorem 4.4.

The proof follows similarly to that in Chernozhukov et al. (2013). We shall apply Yurinskii’s coupling (see Theorem 10 in Pollard (2002)):

Let be independent -vectors with for each , and finite. Let denote denote a copy of on a sufficiently rich probability space . For each there exists a random vector in this space with a distribution such that

for some universal constant .

In order to apply the coupling, consider a copy of the first order approximation to our estimator on a suitably rich probability space

When , a similar argument can be used with replaced by . As in the proof of Theorem 4.2, all eigenvalues of are bounded away from zero. Therefore,

where we used the assumption that . Therefore, by Yurinskii’s coupling, for each ,

because .

Hence, using (4.19) and (4.20), we obtain

uniformly over . Since is bounded from below uniformly over , we conclude that (4.26) holds, and (4.27) is a direct consequence of (4.26).

Further, under the assumption that ,

so that (4.28) follows. This completes the proof of the theorem. ∎

Proof of Theorem 4.5.

Note that solves the least squares problem for the rescaled data . The weight is independent of , , , , and . Thus, considering the model

allows us to extend all results from to replacing by and by and noting that . Also, since , condition assumed in A.5 implies that .

Now, we apply Lemma 4.2 to the original problem (2.4) and to the weighted problem (4.30). Then

where

uniformly over , and so (4.31) follows.

Further, (4.32) follows similarly to Theorem 4.4 by applying Yurinskii’s coupling for the weighted process with weights so that and . Thus there is a Gaussian random vector such that

| (A.55) |

Combining (A.55) with (4.31) yields (4.32) by the triangle inequality as in the proof of Theorem 4.4, and (4.33) follows from (4.32).

Note also that the results continue to hold in -probability if we replace by , since implies that . Indeed, the first relation means that for any , while the second means that for any . But the second clearly follows from the first by Markov inequality because . ∎

Proof of Theorem 4.6.

Note that it follows from that (see the definition of in (4.22)). Therefore, . In addition, it follows from Condition A.4 that , and so implies that

Further, the first result follows from the Markov inequality and Matrix LLN (Lemma 6.2), which shows that .

To establish the second result, we note that

| (A.56) |

The first term on the right hand side of (A.56) satisfies

since by Theorem 4.3, , and by Markov’s inequality. Therefore,

because , by the first result, , and is bounded away from zero.

To control the second term in (A.56), let be a sequence of independent Rademacher random variables () that are independent of the data. Then for ,

where the first inequality holds by Symmetrization Lemma (see Lemma 2.3.6 in van der Vaart and Wellner (1996)), the second by Khinchin’s inequality (Lemma 6.1), the third by , and the fourth by the Cauchy-Schwartz inequality.

Since for any positive numbers , , and , implies , the expression above using the triangle inequality yields

and so

because and . Now, the second result follows from Markov’s inequality.

Finally, we have

whenever and because eigenvalues of both and are bounded away from zero and from above. We can set . This gives the third result of the theorem and completes the proof. ∎

A.5. Proofs of Section 5

A.6. Proofs of Section 5.1

Proof of Theorem 5.1.

A.7. Proofs of Section 5.2

Proof of Lemma 5.2.

By the triangle inequality,

uniformly over where the last inequality follows from the definition of and the condition that uniformly over . Therefore, the proof follows from the same arguments as those given for Lemma 4.2. ∎

Proof of Theorem 5.3.

Proof of Theorem 5.4.

Since , we have

Further, as in the proof of Theorem 4.4 and using Lemma 5.2, we can find such that

uniformly over . Since is bounded away from zero uniformly over ,

or, equivalently,

uniformly over . Further,

uniformly over where the second line follows from being bounded away from zero uniformly over and the third line follows from Lemmas 5.1 and 5.2 and Theorem 5.3. Therefore,

| (A.63) |

uniformly over . In addition, uniformly over and Lemma 5.1 imply that , and so it follows from (A.63) that

uniformly over . This completes the proof of the theorem. ∎

Proof of Theorem 5.5.

We have

| (A.64) |

Under the condition ,

| (A.65) |

uniformly over by the argument used in the proof of Theorem 5.4 with . Further, by Lemma 5.2,

| (A.66) |

uniformly over since . In addition, as in the proof of Theorem 5.4 with ,

| (A.67) |

uniformly over . Combining (A.64), (A.65), (A.66), and (A.67) yields

| (A.68) |

Now, under the condition , the asserted claim follows from Proposition 3.3 in Chernozhukov et al. (2012a) applied to the first term on the right hand side of (A.68) (note that Proposition 3.3 in Chernozhukov et al. (2012a) only considers a special case where , , is replaced by , , but the same proof applies for a more general case studied here, with , ). ∎

Proof of Theorem 5.6.

The proof consists of two steps. The asserted claims are proven in Step 1, and Step 2 contains some intermediate calculations.

Step 1. Under our conditions, it follows from Step 2 that there exists a sequence such that and

| (A.69) |

Let denote the -quantile of . Then in view of (A.69), Lemma A.1 implies that there exists a sequence such that and

| (A.70) | |||

| (A.71) |

Further, it follows from Theorem 5.5 that there exists a sequence of constants and a sequence of random variables such that , equals in distribution to , and

| (A.72) |

Hence, for some universal constant ,

where the first inequality follows from (A.72), the second from (A.71), and the third from Lemma 5.3. This gives one side of the bound in (5.41). The other side of the bound can be proven by a similar argument. Therefore, (5.41) follows. Further, (5.42) is a direct consequence of (5.41).

Finally, we consider (5.43). The second inequality in (5.43) holds because since all eigenvalues of are bounded from above. To prove the first inequality, note that by Lemma 5.1, uniformly over . In addition, Step 2 shows that

| (A.73) |

Therefore, uniformly over , which is the first inequality in (5.43). To complete the proof, we provide auxilliary calculations in Step 2.

Step 2. We first prove (A.69). Note that

Denote . Then, conditional on the data, is a zero-mean Gaussian process. Further, we have for denoting the expectation with respect to the distribution of ,

uniformly over where the last line follows from Lemma A.2. In addition, uniformly over ,

Moreover, uniformly over ,

where the last inequality follows from Condition A.6. A similar argument shows that

uniformly over . Now, (A.69) follows from Dudley’s inequality (Dudley (1967)).

A.8. Proofs of Section 6

Proof of Lemma 6.1.

The first part of the lemma, inequality (6.45), is proven in Section 3 of Rudelson (1999). To prove the second part of the lemma, inequality (A.8), observe that for , the result is trivial. On the other hand, for , we have

where the first inequality follows from (6.44), the second from Jensen’s inequality, the third from the first part of the lemma, and the fourth from (6.44) again. Related derivation can be also found in Section 3 of Rudelson (1999). This completes the proof of the lemma. ∎

Proof of Lemma 6.2.

Using the Symmetrization Lemma 2.3.6 in van der Vaart and Wellner (1996) and the Khinchin inequality (Lemma 6.1), bound

Also, observe that for any ,

so that

Therefore,

where the last assertion follows from Jensen’s inequality. In addition, by the triangle inequality,

Hence,

Denoting and solving this inequality for gives

This completes the proof of the lemma. ∎

Proof of Proposition 6.1.

For a specified later, define and . Since , . Invoke the decomposition

We apply Theorem 6.1 to the first term. Noting that and , we have

On the other hand, applying Theorem 2.14.1 of van der Vaart and Wellner (1996) to the second term, we obtain

| (A.75) |

By assumption,

by which we have

Taking , we obtain the desired inequality. ∎

A.9. Additional technical results

Lemma A.1 (Closeness in Probability Implies Closeness of Conditional Quantiles).

Let and be random variables and be a random vector. Let and denote the conditional distribution functions, and and denote the corresponding conditional quantile functions. If , then for some with probability converging to one

Proof of Lemma A.1.

We have that for some , . This implies that , i.e. there is a set such that and for all . So, for all

which implies the inequality stated in the lemma, by definition of the conditional quantile function and equivariance of quantiles to location shifts. ∎

Lemma A.2.

Let and be symmetric positive semidefinite matrices. Assume that is positive definite. Then .

Proof of Lemma A.2.

This is exercise 7.2.18 in Horn and Johnson (1990). For completeness, we derive this result here. Let be an eigenvector of with eigenvalue . Then

where denotes the minimal eigenvalue of for or . Since is positive semidefinite, . Since is positive definite, . Combining these bounds gives the asserted claim. ∎

References

- Andrews (1991) Andrews, D.W.K., 1991, Asymptotic normality of series estimators for nonparametric and semiparametric models. Econometrica 59, 307-345.

- Angrist et al. (2006) Angrist, J., V. Chernozhukov, and I. Fernández-Val, 2006, Quantile regression under misspecification, with an application to the U.S. wage structure. Econometrica 74, 539-563.

- Belloni et al. (2011) Belloni, A., V. Chernozhukov and I. Fernández-Val, 2011, Conditional quantile processes based on series or many regressors. working paper, http://arxiv.org/abs/1105.6154.

- Burman and Chen (1989) Burman, P. and K.W. Chen, 1989, Nonparametric estimation of a regression function. Annals of Statistics 17, 1567-1596.

- Cattaneo and Farrell (2013) Cattaneo, M. and M. Farrell, 2013, Optimal convergence rates, Bahadur representation, and asymptotic normality of partitioning estimators. Journal of Econometrics 174, 127-143.

- Chen (2007) Chen, X., 2007, Large sample sieve estimation of semi-nonparametric models. In: Heckman, J.J., Leamer, E. (Eds.), Handbook of Econometrics, vol. 6B. Elsevier (Chapter 76).

- Chen (2009, private communication) Chen, X., 2009, Yale University, New Haven, CT, private communication.

- Chen and Christensen (2015) Chen, X. and T. Christensen, 2015, Optimal uniform convergence rates for sieve nonparametric instrumental variables regression, forthcoming in Journal of Econometrics.

- Chernozhukov et al. (2012a) Chernozhukov, V., D. Chetverikov and K. Kato, 2012a, Gaussian approximation of suprema of empirical processes. arXiv:1212.6906.

- Chernozhukov et al. (2014) Chernozhukov, V., D. Chetverikov and K. Kato, 2014, Anti-concentration and honest, adaptive confidence bands. Annals of Statistics, Volume 42, Number 5, 1787–1818.

- Chernozhukov et al. (2006) Chernozhukov, V., I. Fernández-Val and A. Galichon, 2010, Quantile and probability curves without crossing. Econometrica 78, 1093-1125.

- Chernozhukov et al. (2013) Chernozhukov, V., S. Lee, and A. Rosen, 2013, Intersection bounds: estimation and inference. Econometrica, Vol. 81, No. 2, 667–737.

- Cohen et al. (1993) Cohen, A., I. Daubechies and P. Vial, 1993, Wavelets on the interval and fast wavelet transforms. Applied and Computational Harmonic Analysis 1, 54-81.

- De Boor (2001) De Boor, C., 2001, A practical guide to splines (Revised Edition). Springer.

- DeVore and Lorentz (1993) DeVore, R.A. and G. G. Lorentz, 1993, Constructive Approximation. Springer.

- Dudley (1967) Dudley, R. M., 1967, The sizes of compact subsets of Hilbert space and continuity of Gaussian processes. Journal of Functional Analysis 1, 290–330.

- Eastwood and Gallant (1991) Eastwood, B.J. and A.R. Gallant, 1991, Adaptive rules for seminonparametric estimation that achieve asymptotic normality. Econometric Theory 7, 307-340.

- Gallant and Souza (1991) Gallant, A.R. and G. Souza, 1991, On the asymptotic normality of Fourier flexible functional form estimates. Journal of Econometrics 50, 329-353.

- Giné and Koltchinskii (2006) Giné, E. and V. Koltchinskii, 2006, Concentration inequalities and asymptotic results for ratio type empirical processes. Annals of Probability 34, 1143-1216.

- Guédon and Rudelson (2007) Guédon O. and M. Rudelson, 2007, -moments of random vectors via majorizing measures. Advances in Mathematics 208, 798-823.

- Hansen (2014) Hansen, B. E., 2014, A Unified Asymptotic Distribution Theory for Parametric and NonParametric Least Squares. Working paper.

- Hardle (1990) Hardle, W., 1990, Applied nonparametric regression. Cambridge University Press.

- Horn and Johnson (1990) Horn, R. and C. Johnson, 1990, Matrix Analysis. Cambridge University Press.

- Horowitz (2009) Horowitz, J.L., 2009, Semiparametric and Nonparametric Methods in Econometrics. Springer.

- Huang (1998) Huang, J., 1998, Projection estimation in multiple regression with application to functional ANOVA models Annals of Statistics 26, 242-272.

- Huang (2003a) Huang, J.Z., 2003a, Asymptotics for polynomial spline regression under weak conditions. Statistics & Probability Letters 65, 207-216.

- Huang (2003b) Huang, J.Z., 2003b, Local asymptotics for polynomial spline regression. Annals of Statistics 31, 1600-1635.

- Johnstone (2011) Johnstone, I.M., 2011, Gaussian Estimation: Sequence and Multiresolution Models. Unpublished draft.

- Kato (2013) Kato, K., 2013, Quasi-Bayesian analysis of nonparametric instrumental variables models. Annals of Statistics 41, 2359-2390.

- Lust-Picard and Pisier (1991) Lust-Picard, L. and G. Pisier, 1991, Non-commutative Khintchine and Paley inequalities. Arkiv för Matematik 29, 241-260.

- Mallat (2009) Mallat, S., 2009, A Wavelet Tour of Signal Processing. Third Edition. Academic Press.

- Massart (2000) Massart, P., 2000, About the constants in Talagrand’s concentration inequalities for empirical processes. Annals of Probability 28, 863-884.

- Newey (1997) Newey, W.K., 1997, Convergence rates and asymptotic normality for series estimators. Journal of Econometrics 79, 147-168.

- Newey et al. (1999) Newey, W., J. Powell and F. Vella, 1999, Nonparametric estimation of triangular simultaneous equations models. Econometrica 67, 565-603.

- Pollard (2002) Pollard, D., 2002, A User’s Guide to Measure Theoretic Probability. Cambridge Series in Statistics and Probabilistic Mathemathics.

- Rudelson (1999) Rudelson, M., 1999, Random vectors in the isotropic position. Journal of Functional Analysis 164, 1, 60-72.

- Stone (1982) Stone, C.J., 1982, Optimal global rates of convergence for nonparametric regression. Annals of Statistics 10, 1040-1053.

- Stone (1994) Stone, C.J., 1994, The use of polynomial splines and their tensor products in multivariate function estimation. With discussion by Andreas Buja and Trevor Hastie and a rejoinder by the author. Annals of Statistics 22, 118-184.

- Talagrand (1996a) Talagrand, M., 1996a, Majorizing measures: the generic chaining. Annals of Probability 24, 1049–1103.

- Talagrand (1996b) Talagrand, M., 1996b, New concentration inequalities in product spaces. Inventiones Mathematicae 126, 505–563.

- Tropp (2012) Tropp, J.A., 2012, User-friendly tools for random matrices: an introduction, forthcoming.

- Tsybakov (2009) Tsybakov, A.B., 2009, Introduction to Nonparametric Estimation. Springer.

- Wasserman (2006) Wasserman, L., 2006, All of nonparametric statistics. Springer.

- vandeGeer (1990) van de Geer, S. A., 1990, Estimating a regression function. Annals of Statistics, 18, 907–924.

- vandeGeer (2002) van de Geer, S., 2002, M-estimation using penalties or sieves. Journal of Statistical Planning and Inference 108, 55–-69.

- van der Vaart (1998) van der Vaart, A.W., 1998, Asymptotic Statistics. Cambridge University Press.

- van der Vaart and Wellner (1996) van der Vaart, A.W. and J.A. Wellner, 1996, Weak Convergence and Empirical Processes: With Applications to Statistics. Springer.