On optimal dividends in the dual model

Abstract.

We revisit the dividend payment problem in the dual model of Avanzi et al. ([3], [2], and [4]). Using the fluctuation theory of spectrally positive Lévy processes, we give a short exposition in which we show the optimality of barrier strategies for all such Lévy processes. Moreover, we characterize the optimal barrier using the functional inverse of a scale function. We also consider the capital injection problem of [4] and show that its value function has a very similar form to the one in which the horizon is the time of ruin.

Key words: dual model; dividends; capital injections;

spectrally positive Lévy processes; scale functions.

JEL Classification: C44, C61, G24, G32, G35

AMS 2010 Subject Classifications: 60G51, 93E20

1. Introduction

In the so-called dual model, the surplus of a company is modeled by a Lévy process with positive jumps (spectrally positive Lévy processes); see [3], [7], [2], and [4]. This is an appropriate model for a company driven by inventions or discoveries. Our goal is to determine the optimal dividend strategy until the time of ruin for all spectrally positive Lévy processes.

In [2], Avanzi and Gerber consider the dividend payment problem when the Lévy process is assumed to be the sum of an independent Brownian motion and a compound Poisson process with i.i.d. positive hyper-exponential jumps; they determine the optimal strategy among the set of barrier strategies. (The special case in which the jumps are exponentially distributed was obtained by [7].) The optimality over all admissible strategies is later shown by [4] using the verification approach in [7].

In this paper, using the fluctuation theory, we give a short proof of the optimality of barrier strategies for all spectrally positive Lévy processes of bounded or unbounded variation. Moreover, the optimal barrier is characterized using a functional inverse of the scale functions. We also consider the cash injection problem considered in [4]: a variant of the dividend payment problem in which the shareholders are expected to give capital injection in order to avoid ruin. We observe that the form of the value function for this problem is very similar to the first problem we consider in which the horizon is the time of ruin.

Let us describe the dividend payment problems under consideration in more specific terms. We will denote the surplus of a company by a spectrally positive Lévy process whose Laplace exponent is given by

| (1.1) |

where is a Lévy measure with the support that satisfies the integrability condition . It has paths of bounded variation if and only if and ; in this case, we write (1.1) as

with . We exclude the trivial case in which is a subordinator (i.e., has monotone paths a.s.). This assumption implies that when is of bounded variation.

Let be the conditional probability under which (also let ), and let be the filtration generated by . Using this, the drift of is given by

| (1.2) |

We also assume that (and hence ) to ensure that the problem is nontrivial.

1.1. The dividend payment problem until the time of ruin

We first consider a control problem in which the goal is to maximize the expected net present value (NPV) of dividends until ruin. A (dividend) strategy is given by a nondecreasing, right-continuous and -adapted process starting at zero. Corresponding to every strategy , we associate a controlled surplus process , which is defined by

where is the initial surplus and . The time of ruin is defined to be

A lump-sum payment must be smaller than the available funds and hence it is required that

| (1.3) |

Let be the set of all admissible strategies satisfying (1.3). The problem is to compute, for , the expected NPV of dividends until ruin

and to obtain an admissible strategy that maximizes it, if such a strategy exists. Hence the problem is written as

| (1.4) |

1.2. Dividend payment problem with capital injections

In this variant of the dividend payment problem, the time horizon is infinity, and the shareholders are required to inject just enough cash to keep the company alive. A strategy is now a pair where is the cumulative amount of dividends as in the classical dividend problem and is again a nondecreasing, right-continuous and -adapted process starting at zero, representing the cumulative amount of injected capital satisfying

| (1.5) |

Assuming that is the cost per unit injected capital, we want to maximize

Hence the problem is

where is the set of all admissible strategies that satisfy (1.3) and (1.5).

1.3. Outline

In this note, we give a short proof showing that for a general spectrally positive Lévy process, barrier strategies are optimal for both problems, and we give a simple characterization of the optimal barriers in terms of the scale functions; see (2.15) and (3.4). It is interesting to note that the forms of the value functions (3.1) and (3.5) are the same, while the characterizations of barrier levels are in terms of different scale functions. Also, while, in the spectrally negative model, optimal strategies may not lie in the set of barrier strategies, our results show that the dual model can be solved in general by a barrier strategy regardless of the Lévy measure. Regarding the spectrally negative Lévy model, we refer the reader to [6] for examples where barrier strategies are suboptimal and to [15] for a sufficient condition for optimality.

The structure of the rest of the paper is as follows. In Section 2, we solve the optimal dividend problem in which the time horizon is the time of ruin. In this section, we first collect a few results about the scale functions for spectrally one-sided Lévy processes. We then construct a candidate optimal solution out of barrier strategies by (resp. ) conditions at the barrier when is of bounded (resp. unbounded) variation, and verify its optimality. In Section 3, we solve the dividend payment problem with capital injections, where we follow the same plan to the one described for Section 2. We conclude the paper with numerical examples in Section 4.

2. Solution of the dividend problem until the time of ruin

For the dividend problem we described in Section 1.1, a barrier strategy at level is denoted by where for all

and . The corresponding expected NPV of dividends becomes

| (2.1) |

Extending (2.1) to the whole ,

| (2.4) |

Our objective is to show that the optimal control lies in the class of barrier strategies and to identify such that .

2.1. Scale functions

Fix . For any spectrally positive Lévy process, there exists a function called the q-scale function

which is zero on , continuous and strictly increasing on , and is characterized by the Laplace transform:

| (2.5) |

where

Here, the Laplace exponent in (1.1) is known to be zero at the origin, convex on ; therefore is well-defined and is strictly positive as . We also define

and its anti-derivative

Notice that because is uniformly zero on the negative half line, we have

| (2.6) |

Remark 2.1.

-

(1)

If is of unbounded variation, it is known that is ; see, e.g., Chan et al. [9]. Hence, is and for the bounded variation case, while it is and for the unbounded variation case.

-

(2)

Regarding the asymptotic behavior near zero, we have that

(2.7) and

(2.8)

2.2. Constructing a candidate value function

The following is a direct application of the results given in Theorem 1 of [5] (see, in particular, page 167 of this reference).

Lemma 2.1.

For every ,

where

| (2.9) |

Remark 2.2.

Remark 2.3.

The function , , is uniformly bounded by , which follows from the stochastic representation of this function in [5]. As a result, using the duality and Wiener-Hopf factorization of spectrally positive Lévy processes (see, e.g., pages 73-74 and 212-213 of [13]),

where and is an exponential random variable with parameter that is independent of .

This asymptotic behavior is consistent with that of the expected NPV of dividends , when is a spectrally negative process, of a given barrier strategy starting at the barrier:

which is equation (3.15) in [5].

We note that , for any , is clearly continuous everywhere on with . Here, we shall examine the smoothness of at to obtain a candidate barrier level . In particular, we will choose so that is for the case is of bounded variation and for the case is of unbounded variation.

Fix . By differentiating (2.10), we obtain that

| (2.11) |

and when is of unbounded variation (see Remark 2.1 (1))

| (2.12) |

where

| (2.13) |

Substituting (2.9) into (2.13), we see that if and only if

| (2.14) |

On the other hand, since is strictly increasing, goes to as and to as , there exits a unique solution to (2.14). Because , the solution is strictly positive if and only if . We will denote our candidate barrier level by

| (2.15) |

The following proposition states that with this choice of barrier level, the corresponding expected NPV function (2.4) is smooth enough to apply the verification arguments addressed below. In view of Remark 2.1 (1), the smoothness at barrier level is the only point of concern.

Proposition 2.1.

Suppose .

-

(i)

If is of bounded variation, is continuously differentiable on if and only if .

-

(ii)

If is of unbounded variation, is continuously differentiable on for all . However, is twice continuously differentiable on if and only if .

Proof.

(i) Because and are continuous on and , respectively, it is clear in view of (2.11) that the differentiability holds anywhere on . In order to show for , letting in (2.11),

Since, when is of bounded variation (see (2.7)), only when , which happens only when .

(ii) When is of unbounded variation , therefore for all . The differentiability on is clear similarly to (i).

2.3. Verification

By Remark 2.1 (1) and Lemma 2.1, defined in (2.17) is (resp. ) when is of unbounded (resp. bounded) variation. Moreover, it is clear that in both cases. Therefore, we can use Proposition 4 of [5], which is a generic verification theorem for the dividend payment problems of any Lévy process. (Also see Lemma 3.1 of [7].) From this theorem it follows that to prove the optimality of it is sufficient to demonstrate the following variational inequality:

| (2.18) |

Here is the infinitesimal generator associated with the process applied to a sufficiently smooth function

We show that indeed satisfies (2.18) and its optimality over all admissible strategies .

Theorem 2.1.

We have as defined in (2.17) and is the optimal strategy over .

Proof.

We will verify that satisfies (2.18) in four steps:

Step 1. Suppose . By Lemma 2.1, it is clear that . Moreover, by (2.16), we have that

, for . Hence is decreasing on . This shows, for , we have .

Step 2. Again suppose . Because of our assumption that , Proposition 2 of [5] implies that, with and , the process for is a martingale. Now, thanks to the smoothness of as in Remark 2.1 (1), Itô’s lemma applies. In particular, following the same line of arguments presented in Section 4 of [8], this implies that , a.s. Hence we must have for . In view of (2.17), we have for all .

Step 3. For , by (2.4), we have .

Step 4. Suppose . Thanks to the smoothness of at , which we proved in Proposition 2.1, Step 2 implies that . Due to the form of on as in (2.4), is a constant. On the other hand, is increasing in . Hence is decreasing on and it follows that for .

Now suppose (thus ). Then and , which is bounded from above by because for any . ∎

3. Solution of the dividend problem with capital injection

For the capital injection problem as defined in Section 1.2, we consider the doubly reflected Lévy process with upper barrier and lower barrier of the form

As shown by [16], this is a Markov process taking values only on . By modifying Theorem 1 of [5], for any and , we obtain that

Hence the expected payoff corresponding to the strategy is

| (3.1) |

Similarly to our observations in Remark 2.2, using (2.6), (3.1) holds even when . Finally, we extend it to the negative line so that

| (3.2) |

Remark 3.1.

3.1. Ansatz and verification

Analogously to the previous section, we choose our candidate barrier level using the () condition at the barrier. For , by taking derivatives

| (3.3) | ||||

Hence it is clear that the (resp. ) condition at for the bounded (resp. unbounded) variation case holds if and only if . Since is strictly increasing on , and (see e.g. Lemma 3.3 in [12]), there exists a unique

| (3.4) |

The candidate value function simplifies to

| (3.5) |

Remark 3.2.

As , . This is consistent with the observation given in page 158 of [5]. On the other hand, as ; as increases, it gets more risky to pay dividends.

Thanks to Remark 2.1 (1) and the way is chosen to ensure the smoothness at , we can apply Proposition 4 (2) of [5], which tells us that it is sufficient to show that satisfies the following variational inequality:

| (3.6) | |||

| (3.7) | |||

| (3.8) |

The steps of proving the verification are similar to the ones in Theorem 2.1. Therefore we will only verify (3.7) and (3.8). For , by (3.3), the monotonicity of and (3.5) imply, . For , it is clear that . Also, (3.8) is satisfied by (3.2). In summary, we have the following.

Theorem 3.1.

We have as defined in (3.5) and is the optimal strategy over .

4. Numerical Examples

We have shown that the dividend payment and cash injection problems both admit solutions written in terms of the scale function. In order to put this in practice, the only task left to do is to compute the scale function. There are several examples of Lévy processes whose scale functions are known explicitly; see [13], [14], [11] and [12]. In general, the scale function can be computed efficiently by inverting the Laplace transform (2.5) (see [17] and [12]), or alternatively it can be approximated by those of phase-type Lévy processes (see [1] and [10]). Here, we shall use the latter and confirm via numerical examples the results obtained in the previous sections.

Consider a spectrally positive Lévy process of the form

for some and . Here is a standard Brownian motion, is a Poisson process with arrival rate , and is an i.i.d. sequence of phase-type-distributed random variables with representation ; see [1]. These processes are assumed mutually independent. Its Laplace exponent (1.1) is then

which is analytic for every except at the eigenvalues of . Suppose is the set of the (complex-valued) roots of the equality with negative real parts, and if these are assumed distinct, then the scale function can be written

for the case and , respectively for some ; see [10]. For the phase-type distribution, we use ,

This approximates (the absolute values of) the Gaussian distribution with mean zero and standard deviation , obtained using the EM-algorithm; see [10] for the approximation performance of the corresponding scale function. We also let and .

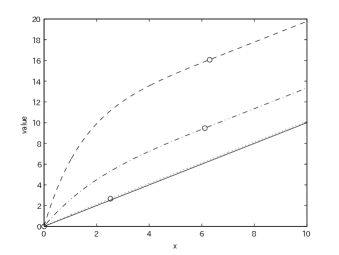

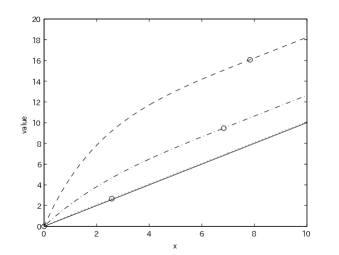

We shall first confirm the results obtained in Theorem 2.1. We consider both the bounded and unbounded variation cases with and , respectively. In Figure 1, we show the value function as well as the point for or equivalently . The value function as well as the value of decrease as increases (or decreases); in particular for the case (or ). It is also observed that the value function is smooth at for both bounded and unbounded variation cases.

|

|

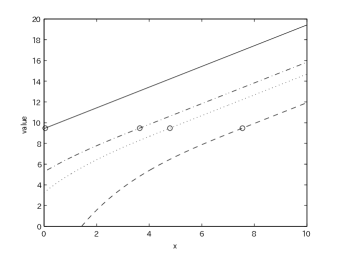

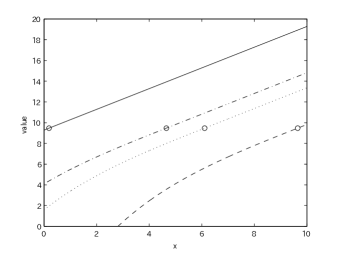

Next we give results on the capital injection problem and confirm the results in Theorem 3.1. In Figure 2, we plot the value function as well as the point for and . Here we use the common value of and hence is the same for each. The value function is indeed decreasing in the unit cost and the value of decreases to zero as decreases to . As in the case of dividend payment problem, we can again confirm the smoothness of the value function for all cases.

|

|

Acknowledgements

We would like to the thank the referees and the editors for their feedback. E. Bayraktar is supported in part by the National Science Foundation under a Career grant DMS-0955463 and in part by the Susan M. Smith Professorship. K. Yamazaki is in part supported by Grant-in-Aid for Young Scientists (B) No. 22710143, the Ministry of Education, Culture, Sports, Science and Technology, and by Grant-in-Aid for Scientific Research (B) No. 2271014, Japan Society for the Promotion of Science. A. Kyprianou would like to thank FIM (Forschungsinstitut für Mathematik) for supporting him during his sabbatical at ETH, Zurich.

References

- [1] S. Asmussen, F. Avram, and M. R. Pistorius. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl., 109(1):79–111, 2004.

- [2] B. Avanzi and H. U. Gerber. Optimal dividends in the dual model with diffusion. Astin Bull., 38(2):653–667, 2008.

- [3] B. Avanzi, H. U. Gerber, and E. S. W. Shiu. Optimal dividends in the dual model. Insurance Math. Econom., 41(1):111–123, 2007.

- [4] B. Avanzi, J. Shen, and B. Wong. Optimal dividends and capital injections in the dual model with diffusion. Astin Bull., 41(2):611–644, 2011.

- [5] F. Avram, Z. Palmowski, and M. R. Pistorius. On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl. Probab., 17(1):156–180, 2007.

- [6] P. Azcue and N. Muler. Optimal reinsurance and dividend distribution policies in the Cramér-Lundberg model. Math. Finance, 15(2):261–308, 2005.

- [7] E. Bayraktar and M. Egami. Optimizing venture capital investments in a jump diffusion model. Math. Methods Oper. Res., 67(1):21–42, 2008.

- [8] E. Biffis and A. E. Kyprianou. A note on scale functions and the time value of ruin for Lévy insurance risk processes. Insurance Math. Econom., 46(1):85–91, 2010.

- [9] T. Chan, A. Kyprianou, and M. Savov. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Fields, 150:691–708, 2011.

- [10] M. Egami and K. Yamazaki. Phase-type fitting of scale functions for spectrally negative Lévy processes. arXiv:1005.0064, 2012.

- [11] F. Hubalek and A. E. Kyprianou. Old and new examples of scale functions for spectrally negative Lévy processes. Sixth Seminar on Stochastic Analysis, Random Fields and Applications, eds R. Dalang, M. Dozzi, F. Russo. Progress in Probability, Birkhäuser, pages 119–146, 2010.

- [12] A. Kuznetsov, A. Kyprianou, and V. Rivero. The theory of scale functions for spectrally negative levy processes. Springer Lecture Notes in Mathematics, 2061:97–186, 2013.

- [13] A. E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin, 2006.

- [14] A. E. Kyprianou and V. Rivero. Special, conjugate and complete scale functions for spectrally negative Lévy processes. Electron. J. Probab., 13:no. 57, 1672–1701, 2008.

- [15] R. L. Loeffen. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Ann. Appl. Probab., 18(5):1669–1680, 2008.

- [16] M. R. Pistorius. On doubly reflected completely asymmetric Lévy processes. Stochastic Process. Appl., 107(1):131–143, 2003.

- [17] B. A. Surya. Evaluating scale functions of spectrally negative Lévy processes. J. Appl. Probab., 45(1):135–149, 2008.