Dynamic Scheduling for Markov Modulated Single-server Multiclass Queueing Systems in Heavy Traffic

Amarjit Budhiraja, Arka Ghosh and Xin Liu

This research is partially supported by the National Science Foundation

(DMS-1004418, DMS-1016441), the Army Research Office (W911NF-10-1-0158) and the US-Israel Binational Science Foundation (Grant 2008466).

Abstract:

This paper studies a scheduling control problem for a single-server multiclass queueing network in heavy traffic, operating in a changing environment. The changing environment is modeled as a finite state Markov process that modulates the arrival and service rates in the system. Various cases are considered: fast changing environment, fixed environment and slow changing environment. In each of the cases, using weak convergence analysis,

in particular functional limit theorems for renewal processes and ergodic Markov processes, it is shown that an appropriate “averaged” version of the classical -policy (the priority policy that favors classes with higher values of the product of holding cost and service rate ) is asymptotically optimal for an infinite horizon discounted cost criterion.

Keywords: Markov modulated queueing network, multiscale queueing systems, heavy traffic, diffusion approximations, scheduling control, scaling limits, asymptotic optimality, rule, Brownian control problem (BCP).

\@afterheading

1 Introduction

Heavy traffic modeling has a long history. For a small sample of some recent works on heavy traffic analysis, we refer the reader to [7, 14, 15, 11], a comprehensive list of references can be found in [9, 15].

The heavy traffic formulation provides tractable approximations for complex queueing systems that capture broad qualitative features of the networks. While most works in the literature deal with fixed (or internal network-state-dependent) rates, with the advent of modern wireless networks there is an explosion of research on models for networks where external factors such as meteorological variables (temperature, humidity, etc) can affect the transmission rates to and from the servers (see [3] and references therein).

The current paper deals with the simplest such setting of a multiclass network, namely a single server multiclass queueing system in heavy traffic, where the arrival and services fluctuate according to an environment process.

In the classical constant rate setting this model has been studied in [13] in the conventional heavy traffic regime.

The queueing system consists of a single server which can process different classes of jobs ().

The classes represent different types of jobs (voice traffic, data traffic etc.), and they have different arrival and service rate functions. We assume that these functions are modulated by a finite state Markov process that represents the background environment. The arrival and service rates satisfy a suitable heavy traffic assumption which, loosely speaking, says that the network capacity and service requirements are balanced in the long run. We consider a scheduling control problem, where the controller decides (dynamically, at each time point ) which class of jobs should the server process so as to minimize an infinite horizon discounted cost function, which involves a linear holding cost per job per unit time for each of the different classes. The jump rates of the modulating Markov process are modeled by a scaling parameter . The value of can vary from negative to positive – the larger the value of , the faster the environment changes – and we consider three distinct regimes for (see (3.5)). We show that

under different values of , with suitably scaling, queue length processes stabilize leading to different diffusion approximations.

Main result of the paper shows that, in each of these regimes, an asymptotically optimal scheduling policy is a variation of the classical and intuitively appealing -rule.

Classical -rule [12] is a simple priority policy, where the priority is always given to the class (of nonempty queue) with the highest -value where and represent the holding cost and the service rate of that class, respectively.

It is well known that -rule is optimal in many cases, see [10, 13] and references therein.

In our model, the arrival rates change randomly according to the background Markov process, and it is far from clear if the classical -rule would be optimal. In addition, in one of the regimes we consider, the service rates are allowed to be modulated by the random environment as well, which means that the order of the -values keeps changing according to the environment. In particular, in situations where the environment process is not directly observable and one only knows (or can estimate)

its statistical properties, the classical -rule cannot be implemented.

We propose a modified -rule, where represents the average service rate of each class and the average is taken with respect to the stationary distribution of the environment process. Under the -rule, the server always processes jobs from the nonempty queue with the highest -value. We show that, under an appropriate heavy traffic condition and a suitable scaling, the -rule is asymptotically optimal for the chosen cost functional for this environment-dependent queueing model, in each of the three regimes for .

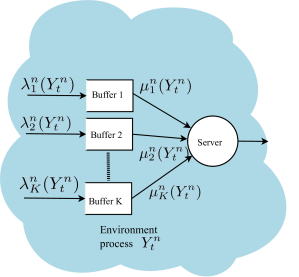

Fig 1: The Markov modulated single-server multiclass queueing system.

As is common practice in heavy traffic analysis, we consider a sequence of networks, indexed by , each of which is a single server multiclass network in a random environment (see Fig. 1). In our formulation, the environment process operates at a time-scale of , where the scaling parameter determines the rate of fluctuations of the environment process.

When (Case 1), the background environment is changing faster than typical arrivals and services (which are ), while the reverse is true when (Case 3). If (Case 2), the variation rates of the background process and the arrival and service processes are both .

The scaling that stabilizes the processes is different in each of the three cases: When , the space is scaling down by the usual factor of , and when , the scaling factor becomes (time is accelerated by a factor of in all cases). In each of the cases, we show, using functional central limit theorems for renewal processes and ergodic Markov processes, that the ‘driving process’ converges to a Brownian motion (the variance parameter of the Brownian motion is different in the three regimes, c.f. Lemma 5.3).

The application of the first limit theorem is quite common in heavy traffic theory, however the use of limit theorems for ergodic Markov processes in optimal

scheduling problems is less standard.

We then formulate a Brownian control problem (BCP), which is a formal approximation of the queueing network control problem, where the driving process is replaced by a Brownian motion.

This BCP is explicitly solvable and an optimal solution of the BCP is such that, the optimal state process (formal approximation of the scaled queue-length process) is zero for all the classes except for the one with the lowest value of the corresponding quantity. We use this insight gained from the solution of the BCP to propose a priority policy (see Definition 3.1), which prioritizes queues based on the value of the class. Our main result is Theorem 3.1, which shows that, under conditions, this priority policy is asymptotically optimal for the queueing control problem, in each of the three regimes.

As noted above, we consider three different regimes for : (1) ; (2) ; (3) .

Additionally, Case 1 is further subdivided into: (a) ; and (b) .

For cases 1(b), 2 and 3 we take the service rates to be constant (i.e. only the arrival rates are environment dependent).

For case 1(a), both the service and arrival rates are allowed to be environment dependent.

The key result that allows the treatment of environment dependent service rates is Lemma 5.2, where the condition is crucially used.

Although we leave the case when and service rates are environment dependent as an open problem, numerical experiments in Section 3

suggest that even in these settings priority policy may be suitable.

The paper is organized as follows. Section 2 describes the model, introduces the key assumptions and presents the main scheduling control problem. In Section 3, we introduce the cost criterion and state the main result of the paper, namely Theorem 3.1 (see also Theorem 4.1). Section 4 introduces the Brownian control problem associated with the scheduling control problem from

Section 3. Section 5 is devoted to the proofs of Theorems 3.1 and 4.1.

Finally, the appendix collects proofs of some auxiliary results and findings of our numerical experiments.

The following notation will be used. Denote the set of positive integers by . For , let be the -dimensional Euclidean space. Define . Vectors are understood to be column vectors. For a -dimensional vector , denote by the diagonal matrix whose diagonal entries are given by the components of . For , will denote the component of . The transpose of is denoted by , and the inner product of two -dimensional vectors and will be denoted by . Let be a norm on given by . For a matrix , denote by the entry of . Let

denote the space of functions that are right continuous with left limits (RCLL) defined from to with the usual Skorohod topology, and the class of continuous functions from to with the local uniform topology. Convergence of random variables to in distribution will be denoted as , and weak convergence of probability measures to will also be denoted as . A sequence of -valued random variables is said to be -tight if and only if the measures induced by on form a tight sequence and any weak limit of the sequence is supported on .

For a stochastic process , we will use the notation and interchangeably, and we let For semimartingales , we denote by and the quadratic covariation and predictable quadratic covariation of and , respectively. For a metric space , let be the collection of all probability measures on and the class of bounded measurable functions from to . For and , let

For , where , we write

A countable set will be endowed with the discrete topology. Finally, we denote generic positive constants by , the values of which may change from one proof to another.

2 Single-server multiclass queueing system

2.1 Network model

Consider a queueing system consisting of a single server which is shared by parallel classes of customers as depicted in Figure 1. Consider a sequence of such systems indexed by . Let be a filtered probability space satisfying the usual conditions. All the random variables and stochastic processes for the system are assumed to defined on this space. For the system, we define a -Markov process , where and is a Markov process with state space , a unique stationary distribution , and infinitesimal generator (rate matrix) which converges to the rate matrix

of an ergodic Markov process. Note that as , converges to the unique stationary distribution of this Markov process.

The expectation operator with respect to will be denoted by , but frequently we will suppress from the notation.

We will make the following uniform ergodicity assumption.

Assumption 2.1.

For some and

where .

As shown in Figure 1, there are classes of external arrivals. For , customers of Class arrive from outside to buffer and upon completion of service, they leave the system. For , denote by the number of customers of Class arriving from the outside by time and the number of customers of Class completing service by time if the server is continuously working on Class customers during . We assume and are Poisson processes with intensities modulated by Markov process . More precisely, for , let

. Then and can be described as follows: For ,

(2.1)

where and are independent unit rate Poisson processes. Here are the arrival and service rate functions, respectively.

The processes and are assumed to be mutually independent. Also, we assume that

is a martingale. An analogous assumption on will be introduced in Section 2.2 (see Condition 2.1 (iii)).

Let and .

We make the following convergence assumptions on . Define the “averaged” arrival and service rates as follows:

Assumption 2.2.

(i)

There exists a function such that as ,

, for all .

(ii)

There exists such that as ,

.

Let .

Assumption (i) in particular says that the arrival rates are and

Assumption on the service rates is somewhat weaker in that it only requires that the “averaged” service rates are convergent. Additional conditions on and (heavy traffic condition) are formulated in Assumption 2.3 at the end of Section 2.2.

2.2 Scheduling control and scaled processes

In the network, the scheduling policy is described by a service allocation process

where for , denotes the total time used to serve customers of Class during . The idle time process is defined as follows:

(2.2)

which gives the total idle time of the server during .

Denote by the -dimensional state process, i.e., the queue length process (including the job being served). Then the evolution of the queueing system can be described as follows: For ,

Here, for simplicity we assume that at time the system is empty.

The processes and are required to satisfy the following conditions: For ,

(2.3)

As a consequence of the conditions in (2.3), we have the following Lipschitz property of : For ,

(2.4)

Therefore, , is almost everywhere differentiable. Denoting its derivative by , we have

(2.5)

We make the following additional assumptions on . Define a sequence of nondecreasing random times . Let , and for , be the first time after when there is either an arrival or a service completion.

Condition 2.1.

For all for all

The process is -progressively measurable.

is a martingale.

Part (i) of the condition says does not change values between two successive changes

of the state of the system. Part (ii) is a natural nonanticipativity property of and the martingale condition in part (iii) is analogous to the one imposed on

in Section 2.1. We call satisfying (2.3) and Condition 2.1 an admissible control policy and denote the collection of all such by .

Using (2.5), we can write in the following way: For ,

(2.6)

Finally, we write and .

We now define the fluid and diffusion scaled processes. Roughly speaking, the fluid-scaled processes are defined by accelerating time by and scaling down space by the same factor, and the diffusion-scaled processes are defined by accelerating time by and scaling down space

(after an appropriate centering) by for some . Choice of is specified in (3.5).

Fluid scaling: For ,

(2.7)

Diffusion scaling: For ,

(2.8)

From the above scalings and (2.6) we see, for and ,

and furthermore, for each , there exists such that as ,

(2.12)

3 Objective and main results

For our optimization criterion we consider an expected infinite horizon discounted linear holding cost. More precisely, for the network, the cost function associated with the control policy is defined as follows:

(3.1)

where is the “discount factor” and is the vector of “holding costs” for the buffers.

The goal of this work is to find a sequence of admissible control policies such that it achieves asymptotic optimality in the sense that

(3.2)

where the infimum is taken over all admissible control policies .

For single server multiclass queueing systems (with constant rates), one attractive policy is the well-known rule, where and stand for holding cost and service rate, respectively. Under rule, the server always selects jobs from the nonempty queue with the largest values. In this work, we generalize the rule to the Markov modulated setting and show that, under conditions, an “averaged” rule is asymptotically optimal, where is the “averaged” service rate introduced in Assumption 2.2 (ii). Our precise result

is given in Theorem 3.1 below. We begin with the following definition. Let be a permutation of such that

(3.3)

Definition 3.1( rule).

For , let

(3.4)

Note that defines a priority policy in which the server always gives service priority to the nonempty queue with the largest value of .

Theorem 3.1 proves the asymptotic optimality of . Furthermore, in Theorem 4.1, we will characterize the limit of in terms of the solution of a Brownian control problem which is introduced in Section 4. Recall that the background environment Markov process modulating the network is Consider the following three regimes for and .

Case 1.

(3.5)

Case 2.

Case 3.

Case 1 considers a situation where the jump rates of are much higher than the interarrival and service rates. For Cases 1(b), 2 and 3, the service rate is independent of . In Case 2, has jump rates of the same order as the arrival and service rates, while in Case 3, is changing slowly in comparison with the arrival and service processes.

Throughout this work Assumptions 2.1, 2.2 and 2.3 will be taken to hold and will not be noted explicitly in statements of results.

Theorem 3.1.

Let be as in Definition 3.1. Then for each of the three cases in (3.5),

where the infimum is taken over all admissible control policies .

Remark 3.1.

Note that in Cases 1(b),2 and 3 the proposed control policy reduces to a standard -rule. Thus Theorem 3.1 shows that in these regimes, the classical rule to be optimal under conditions that in particular require

an ‘averaged’ form of heavy traffic condition (Assumption 2.3) to hold.

Remark 3.2.

One may conjecture that Theorem 3.1 is true even when the condition that is constant is dropped from Cases 1(b), 2 and 3. The key difficulty in treating these cases is in the proof of results analogous to Lemma 5.2. Although we are unable to treat these

cases, simulation results below suggest that the rule performs better than the dynamic rule in these settings.

Example 3.1.

Consider the special case of the model in Section 2.1 with, .

For the system, let for ,

Then

and

Clearly Assumption 2.3 is satisfied with and .

Note that for all ,

and so buffer 2 gets service priority under the rule.

However, for the dynamic rule, the priority changes according to the state of the modulating Markov process, since

for ,

(3.6)

More precisely, in the dynamic rule, when , customers of Class have priority to be served, while when , priority should be given to Class customers. The numerical study given below compares the performance of rule with the dynamic rule. The following table summarizes the simulation results for different scalings.

We consider the cost criterion (3.1) with . Let . We simulate sample paths of , which are denoted as , for each scaling case at discrete times . We then calculate the discounted cost as follows:

We find in our numerical results that the discounted cost is always smaller under the rule.

Cost ( rule)

Cost (dynamic rule)

Also note that only the first four rows of the table correspond to Case 1(a). The remaining rows, although consistently show that rule outperforms the dynamic rule, correspond to regimes not covered by our

results.

We also plot the cost at each discrete time for the average sample path (of the 10 sample paths) for a range of values of when . The figures can be found in Appendix C.

4 Brownian control problem

Our control policy is motivated by the solution of a Brownian control problem (BCP). In this section we introduce this BCP. Roughly speaking, the BCP is obtained by taking a formal limit, as , in the equation governing the queue length evolution for the system. Recall the evolution equations for from (2.10).

The last term on the right side of (2.10) can be rewritten as

Let

(4.1)

and

(4.2)

Then for and ,

(4.3)

We now formally take the limit as . Write .

In Lemma 5.3 it is shown that, under conditions, as ,

(4.4)

where is a -dimensional Brownian motion with drift and covariance matrix , where and are given explicitly in Lemma 5.3.

In particular the value of is different in the three cases considered in (3.5). Also, as , .

Although in general will not converge, formally taking limit in (4.3), as , we arrive at the following BCP.

Definition 4.1(Brownian control problem (BCP)).

Let be a -dimensional Brownian motion with drift and covariance matrix given on some filtered probability space

.

The BCP is to find an -valued RCLL adapted stochastic process which minimizes

subject to

(4.5)

Denote by the collection of all -valued RCLL adapted stochastic process that satisfy (4.5).

Brownian control problems of the above form were first formulated by Harrison in [6], and since then, many authors have used such control problems in the study of optimal scheduling for multiclass queuing networks in heavy traffic.

The BCP in Definition 4.1 has an explicit solution given in Lemma 4.1 which can be proved by standard methods (see [1] and references therein).

For completeness we provide the proof of Lemma 4.1 in Appendix A.

Lemma 4.1.

Define for ,

(4.6)

and

Then

is an optimal solution of the BCP.

Define for , by (4.5) with replaced by . Then we have

(4.7)

The optimal solution (4.7) suggests that the jobs should be always kept in the buffer with smallest value of . This motivates the control policy defined in Definition 3.1. Define

From Lemma 4.1 we have , where the infimum is taken

over all . In fact, we have the following result, which is proved in the next section.

Theorem 4.1.

Let be as in Definition 3.1. Then for each of the three cases in (3.5),

.

In this section we prove Theorems 3.1 and 4.1 . We begin with the following two lemmas, which play a crucial role in the proofs. The first lemma is a functional central limit theorem (FCLT) for the sequence of Markov processes . We first introduce some notation.

Denote by the infinitesimal generator of , namely defined as

(5.1)

As in Assumption 2.1, denote by the transition kernel of , namely, for .

For notational simplicity we denote this probability by and by the corresponding expectation operator. In

particular for . Define for and ,

(5.2)

Lemma 5.1.

For , exists.

Denote the limit by . Let be a nonnegative sequence such that as .

Define for and

Then converges weakly to a -dimensional Brownian motion with drift and covariance matrix , where for ,

Proof: From Assumption 2.1, there exists such that for ,

This shows that exists, and we denote this limit by .

Note that .

Next note that for ,

(5.3)

Noting that converges to , it follows that (cf. [4, Theorem 4.2.5]), if has limit distribution on , then there exists an -valued Markov process with initial distribution and rate matrix such that . Therefore, by

Assumption 2.2 (i), Assumption 2.1 and

dominated convergence theorem, as ,

This proves the first statement in the lemma, in fact

Following the proof of

(5.3) one can

check that for , where is defined as in (5.1) with replaced by . Next observe that for each ,

(5.4)

is a square integrable martingale. Furthermore

(5.5)

Thus it suffices to show

(5.6)

Proof of (5.6) follows from classical functional central limit theorems for martingales. For completeness, we provide the details in Appendix B.

Lemma 5.2.

Let , , be a sequence of functions such that . Define for and ,

where . Suppose that .

Then, there exists such that, for all

(5.7)

In particular, as ,

Proof:

Note that for ,

(5.8)

For the last expression in (5.8), note that there exists such that for all ,

(5.9)

In what follows, we set when . Then

Next note that, there exists such that for ,

(5.10)

where the last inequality is a consequence of the fact that

the arrival and service rates are , and by Condition 2.1 (i), does not change values between two successive arrivals and/or service completions.

Thus we can find such that for all ,

(5.11)

Define as

From Assumption 2.1 and calculations as in the proof of Lemma 5.1 it follows that

. Also,

is a martingale, where . For , let

Then

The last expression equals

(5.12)

The first term in the above display is a telescoping sum and since is uniformly bounded, we can find such that for all ,

(5.13)

Also, from (5.10), there exists such that for all ,

For , let . By Condition 2.1 (ii),

and so is a martingale difference. Furthermore, is uniformly bounded in and . Applying Doob’s inequality, there exists such that for ,

(5.15)

The result follows on combining (5.9), (5.11), and (5.13) – (5.15).

The following lemma gives a functional law of large numbers (FLLN) and a

FCLT.

For a sequence of admissible policies , and ,

let

(5.16)

Recall from equation (2.1).

Write and . Define the fluid scaled processes and .

Let be the identity map, and define for ,

Using the random change of time theorem (see [2, Lemma 3.14.1]), we have that

(5.23)

In cases 1(b), 2 and 3 (i.e. when ), by Assumption 2.2(ii), we have that for ,

(5.24)

Furthermore, in case 1(a) (i.e. when and is modulated by ), using Assumption 2.2(ii) and Lemma 5.2 (see (5.7)), we have the same convergence result as above. Combining (5.24) and (5.20), we have that

Let be a limit point, along a subsequence of . By Skorohod representation theorem, we can assume that this convergence holds almost surely, uniformly on compacts. From (5.19) and using Fatou’s lemma, we have

(5.30)

Since and has continuous sample paths, we have . By (5.23) and (5.27),

(5.31)

Also, from (5.20) and (5.24), we have that . Therefore,

(5.32)

Finally, (5.32) and heavy traffic condition (2.11) imply . This completes Part (i).

We now consider part (ii). From (4.1) we have that

(5.33)

We now treat the three cases separately.

Case 1. From functional central limit theorem for Poisson processes, we have that

(5.34)

where and , are -dimensional mutually independent standard Brownian motions. From (5.22), (5.24), and (5.32), we have

(5.35)

where , are -dimensional mutually independent Brownian motions with drift and variance .

In case 1(a) (i.e. when and is modulated by ), by Lemmas 5.1 and 5.2, we have . In case 1(b) (i.e. when and ), we have the same convergence by Lemma 5.1. Thus, using (2.12), converges weakly to , where , are mutually independent Brownian motions with drift and covariance .

Case 2. Here and . As in Case 1, we have the convergence in (5.35).

Also note that since . Furthermore, by Lemma 5.1, we have

(5.36)

where is a -dimensional Brownian motion with drift and covariance matrix .

The result now follows on recalling that, are mutually independent.

Case 3. Here and . From Lemma 5.1, the convergence in (5.36) continues to hold. Also,

since , we have

Finally, . The result follows.

We recall below the definition and basic properties of the -dimensional Skorohod map. Let .

Definition 5.1(-dimensional Skorohod Problem (SP)).

Let . A pair is a solution of the Skorohod problem for if the following hold.

(i)

For all .

(ii)

satisfies the following: (a) , (b) is nondecreasing, and (c) increases only when , that is,

We write and refer to the map as the Skorohod map.

The following proposition summarizes some well known properties of the -dimensional SP.

Proposition 5.1.

(i)

Let . Then there exists a unique solution of the SP for , which is given as follows:

(ii)

The Skorohod map is Lipschitz continuous in the following sense: There exists such that for all and ,

(iii)

Fix . Let be such that

(a)

,

(b)

is nondecreasing with .

Then .

We next present two lemmas that will be used in the proofs of Theorems 3.1 and 4.1. Recall the control policy introduced in Definition 3.1.

Lemma 5.4 says that the long run average of approaches and Lemma 5.5 shows that under , all the jobs are kept in buffer , i.e., the buffer with smallest value of , asymptotically.

Lemma 5.4.

As , .

Proof:

In the proof, all the quantities, e.g. queue lengths, idle times etc., are considered under the control policy .

Define, for ,

and let

(5.37)

Note that

(5.38)

Clearly , is nondecreasing and increases only when . Therefore we have (see Definition 5.1), for ,

(5.39)

Using the Lipschitz property in Proposition 5.1 (ii), for ,

Next from Lemma 5.2 (see (5.7)), we have in case 1(a), for some

(5.44)

We note that in cases 1(b), 2 and 3, and so the above estimate (5.44) holds for all cases.

Finally, we show that for some ,

(5.45)

For this, from (5.5) and the fact that , it suffices to show that there exists such that for all ,

Using Doob’s inequality and a standard martingale argument, we have that

where the last estimate uses the fact that is uniformly bounded in and . Combining (5.41) – (5.45), we have for some ,

(5.46)

Consequently, and so from (5.37)

. Following the proof of Lemma 5.3 (i) (see equations (5.27), (5.23), (5.31), and (5.32)), we have .

Lemma 5.5.

Under the control policy , as

Proof: Once again all the quantities in the proof are considered under the control policy .

Without loss of generality, we assume . For , let

It suffices to show that . Define for , ,

From Lemma 5.3(ii), we have that converges to a Brownian motion with drift and variance , where is given as follows:

Case 1.

Case 2.

Case 3.

Here is as defined in Lemma 5.1.

Next observe that

which is nondecreasing and increases only when .

Define for ,

Since , , a.s. By definition, . Also since for all , we have . Therefore, we have

(5.47)

and so

(5.48)

From the proof of Lemma 5.4 (see (5.41), (5.42), (5.44), and (5.45)), we have that

Also note that

Therefore, we have

(5.49)

Thus converges to in probability and uniformly on compact sets.

Using this observation in (5.48) we now have that

where is the identity map.

Finally, from (5.47), we have

The result follows.

Proof of Theorem 4.1: As in the proof of Lemma 5.5, we assume

without loss of generality, . Also, once again all the quantities in the proof are considered under control policy . From (5.46) it follows that (5.18) holds with . Thus from Lemma 5.3, we have , where is the Brownian motion introduced in Lemma 5.3.

Next recall that

as defined in (5.38) satisfies:

; is nondecreasing; and increases only when . Therefore, from Definition 5.1, we have for ,

(5.50)

Using the Lipschitz continuity property of (Proposition 5.1(ii)), and recalling defined in (4.6), we have that

Since in cases 1(b), 2 and 3, we have the result for these cases. Finally consider the case 1(a).

Using Lemma 5.2, we have for some ,

The result follows.

Proof of Theorem 3.1: Let be a sequence of admissible control policies.

The result holds trivially if .

Suppose now that

.

Let be a subsequence such that , as . Henceforth we relabel the subsequence

as .

Throughout the proof, all quantities are considered under the control sequence

. Recalling (5.37) and that

; is nondecreasing and starts from zero, we have from Proposition 5.1 (iii) that for ,

(5.57)

and with

we have for all ,

(5.58)

Also from Definition 5.1, we have

From Lemma 5.3(ii), and using the Lipschitz continuity of (Proposition 5.1 (ii)), we now have

We begin by introducing a -dimensional control problem referred to as the ‘workload control problem’

Definition A.1.

The workload control problem (WCP) is to find an -valued RCLL adapted stochastic process which minimizes

subject to

(A.1)

where and are as in Definition 4.1 and is defined in (5.61).

Proof of Lemma 4.1:

Recall , defined in (4.6).

From (4.7) we see that, for every , is a solution of the LP problem (5.60) associated with . Thus

(A.2)

Also note that the pair satisfies the two conditions in (A.1). Furthermore, if

is another pair satisfying (A.1), we have from Proposition 5.1(iii) that

and consequently,

, for all , where is as defined in (5.61).

Now let and define the corresponding , , and through (4.5).

Define

(A.3)

Clearly satisfy (A.1) and so from the

above discussion

(A.4)

Also, from the definition of and (A.3) we see that

, for all . Combining this inequality with (A.2) and (A.4)

we get that , for all . Since

is arbitrary, we have the result.

We only treat the case when . The general case can be proved similarly.

We first consider the special case when is stationary. Denote by the expectation operator when

has distribution .

Let . Noting that for all , we have that for any and ,

By martingale central limit theorem (see Corollary VIII.3.24 in [8]), it suffices to show that

in probability for all , where denotes the predictable quadratic variation

of the martingale . We note from (5.4) that

Noting that and , and using Assumption 2.1, we have that for

Thus we have that

This completes the proof for the case when is stationary.

Finally we consider the case when has an arbitrary distribution. It suffices to consider the setting where ,

for all . The argument below follows the proof of Theorem 4.3 in [5].

Define for ,

Clearly, for any ,

(B.1)

Let be a real valued bounded Lipschitz function on . Then from (B.1), we have, as ,

where denotes the expectation operator when a.s.

Using the Markov property, we have

(B.2)

Thus we have for some ,

Using (B.2) and Assumption (2.1) we see that the last expression converges to on sending first

and then .

This completes the proof of (5.6).

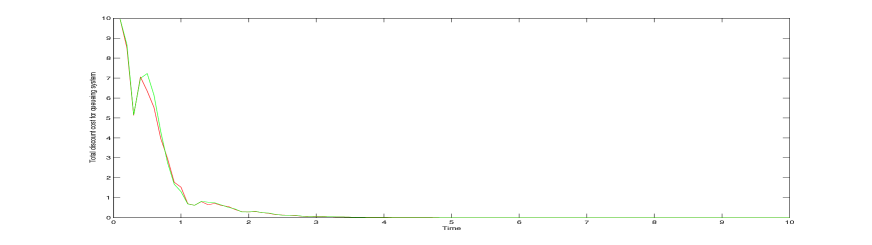

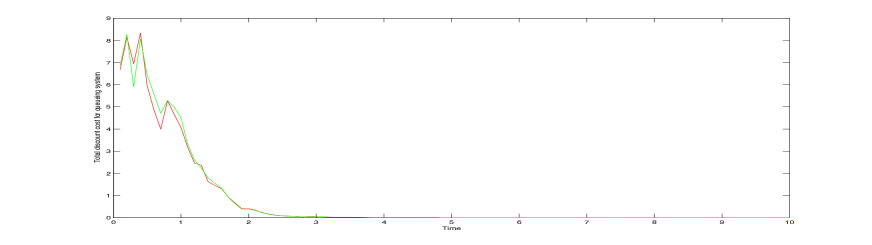

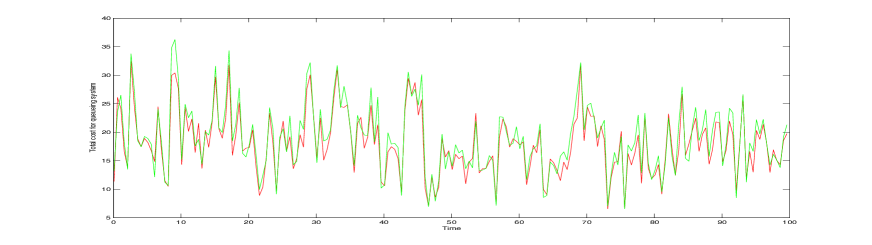

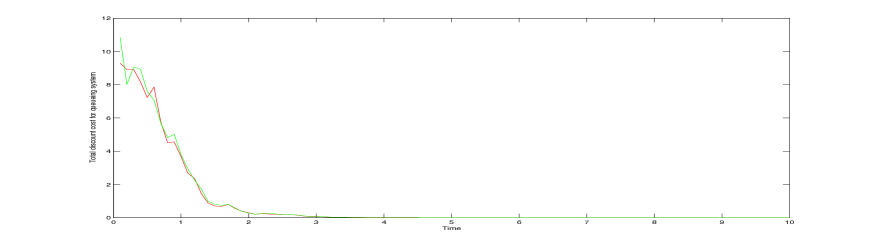

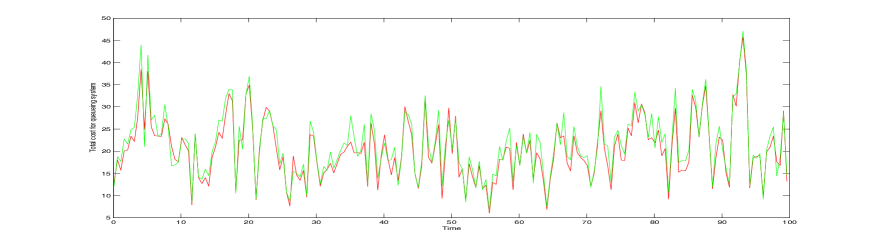

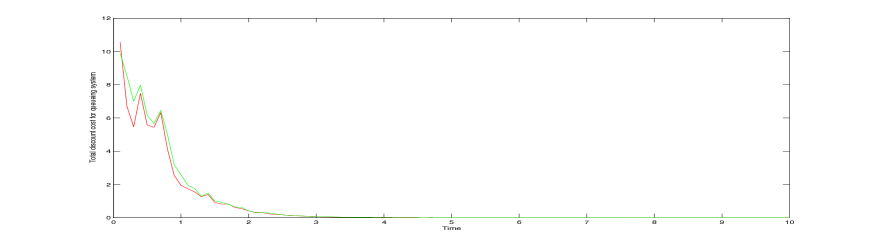

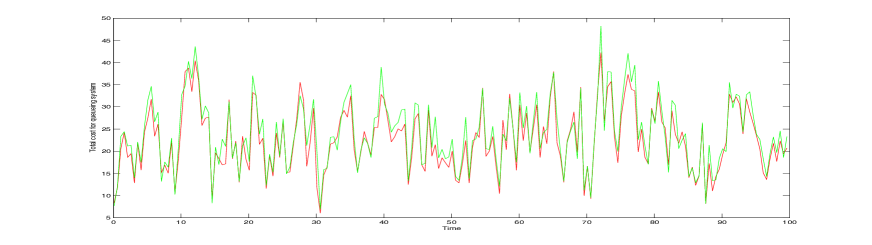

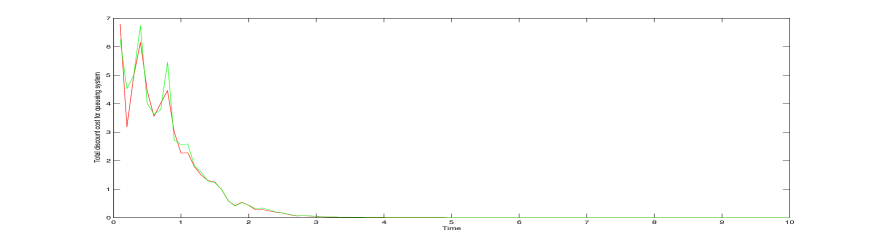

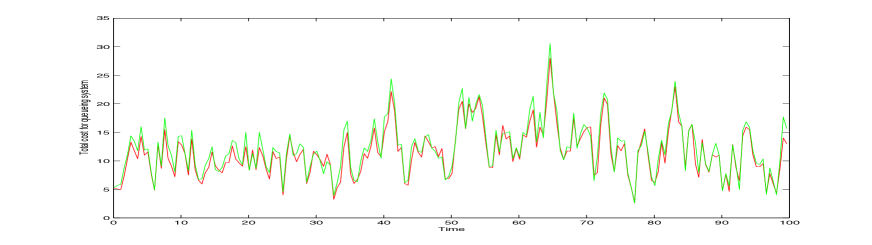

We continue with Example 3.1. We plot the total cost and total discounted cost at each discrete time. More precisely, recall that the holding cost and discount factor . For sample paths, define

and

Here measures the total cost for the queueing system at time , while gives the discount cost at time .

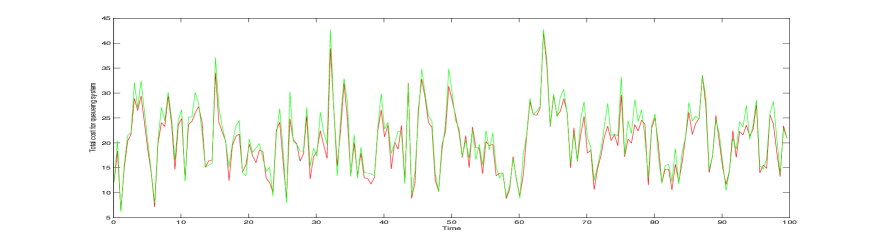

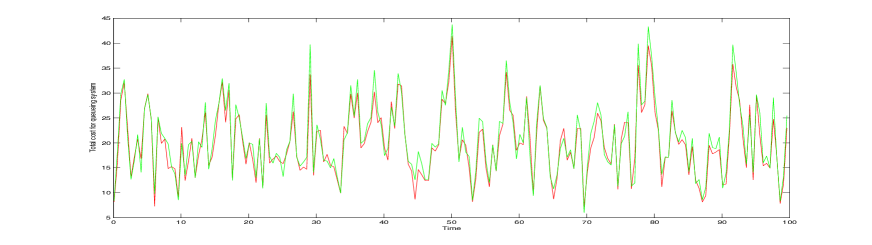

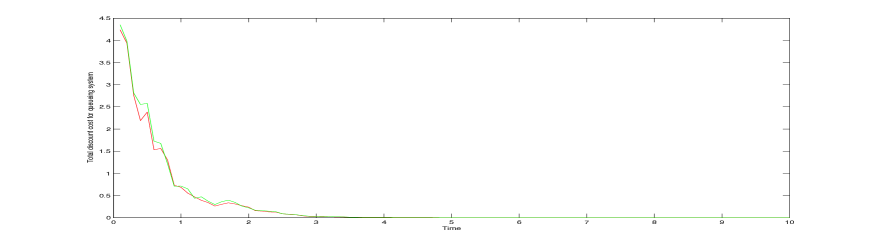

Let . We plot and for six different scalings. In all the following figures, the first plot gives and the second one is . We use red color to represent -rule and green color for dynamic -rule. We observe that in all the plots, the red line is located below the green one for most of time, which says that the cost under -rule is smaller.

Fig 2: Average sample path for the case when and .

Fig 3: Average sample path for the case when and .

Fig 4: Average sample path for the case when and .

Fig 5: Average sample path for the case when and

Fig 6: Average sample path for the case when and .

Fig 7: Average sample path for the case when and .

References

[1]

S. L. Bell and R. J. Williams.

Dynamic scheduling of a system with two parallel servers in heavy

traffic with resource pooling: Asymptotic optimality of a threshold policy.

Ann. Appl. Probab., 11(3):608 – 649, 2001.

[2]

P. Billingsley.

Convergence of Probability Measures.

Wiley, New York, 1999.

[3]

R. Buche and H. J. Kushner.

Control of mobile communications with time-varying channels in heavy

traffic.

IEEE Transactions on automatic control., 47(6):992 – 1003,

2002.

[4]

S. N. Ethier and T. G. Kurtz.

Markov Processes: Characterization and Convergence.

Wiley, New York, 1986.

[5]

P. W. Glynn and S. P. Meyn.

A Liapounov bound for solutions of the Poisson equation.

The Annals of Probability, 24(2):916–931, 1996.

[6]

J. M. Harrison.

Brownian models of queueing networks with heterogeneous customer

population.

In Stochastic Differential Systems, Stochastic Control Theory

and Applications (W. Fleming and F. L. Lion, eds), pages 147 – 186,

Springer, New York, 1988.

[7]

J. M. Harrison.

A broader view of Brownian networks.

Ann. Appl. Probab., 13(3):1119 – 1150, 2003.

[8]

J. Jacod and A. Shiryaev.

Limit Theorems for Stochastic Processes.

Springer-Verlag; 2nd Edition, 2002.

[9]

H. J. Kushner.

Heavy Traffic Analysis of Controlled Queueing and Communication

Networks.

Springer-Verlag, New York, 2003.

[10]

A. Mandelbaum and A. L. Stolyar.

Scheduling flexible servers with convex delay costs: Heavy-traffic

optimality of the generalized c-rule.

Operations Research, 52(6):836 – 855, 2004.

[11]

A. P. Ghosh R. T. Buche and V. Pipiras.

Heavy traffic approximations of a queue with varying service rates

and general arrivals.

Stochastic Models, 28(1):63 – 108, 2012.

[12]

W. E. Smith.

Various optimizers for single-stage production.

Naval Research Logistics Quarterly, 3:59 – 66, 1956.

[13]

J. A. van Mieghem.

Dynamic scheduling with convex delay costs: The generalized c-

rule.

Ann. Appl. Probab., 5(3):809 – 833, 1995.

[14]

N. H. Lee W. N. Kang, F. P. Kelly and R. J. Williams.

State space collapse and diffusion approximation for a network

operating under a fair bandwidth sharing policy.

Ann. Appl. Probab., 19(5):1719 – 1780, 2009.

[15]

W. Whitt.

Stochastic-Process Limits: an Introduction to Stochastic Process

Limits and their Application to Queues.New York: Springer-Verlag, 2002.