The Algebraic Combinatorial Approach for Low-Rank Matrix Completion

Abstract

We present a novel algebraic combinatorial view on low-rank matrix completion based on studying relations between a few entries with tools from algebraic geometry and matroid theory. The intrinsic locality of the approach allows for the treatment of single entries in a closed theoretical and practical framework. More specifically, apart from introducing an algebraic combinatorial theory of low-rank matrix completion, we present probability-one algorithms to decide whether a particular entry of the matrix can be completed. We also describe methods to complete that entry from a few others, and to estimate the error which is incurred by any method completing that entry. Furthermore, we show how known results on matrix completion and their sampling assumptions can be related to our new perspective and interpreted in terms of a completability phase transition.

On this revision

This revision - version 4 - is both abridged and extended in terms of exposition and results, as compared to version 3 Király et al. (2013). The theoretical foundations are developed in a more ad-hoc way which allow to reach the main statements and algorithmic implications more quickly. Version 3 contains a more principled derivation of the theory, more related results (e.g., estimation of missing entries and its consistency, representations for the determinantal matroid, detailed examples), but a focus which is further away from applications. A reader who is interested in both is invited to read the main parts of version 4 first, then go through version 3 for a more detailed view on the theory.

1. Introduction

Matrix completion is the task to reconstruct (to “complete”) matrices, given a subset of entries at known positions. It occurs naturally in many practically relevant problems, such as missing feature imputation, multi-task learning (Argyriou et al., 2008), transductive learning (Goldberg et al., 2010), or collaborative filtering and link prediction (Srebro et al., 2005; Acar et al., 2009; Menon and Elkan, 2011).

For example, in the “NetFlix problem”, the rows of the matrix correspond to users, the columns correspond to movies, and the entries correspond to the rating of a movie by a user. Predicting how one specific user will rate one specific movie then reduces to completing a single unobserved entry from the observed ratings.

For arbitrarily chosen position , the primary questions are:

-

•

Is it possible to reconstruct the entry ?

-

•

How many possible completions are there for the entry ?

-

•

What is the value of the entry ?

-

•

How accurately can one estimate the entry ?

In this paper, we answer these questions algorithmically under the common low-rank assumption - that is, under the model assumption (or approximation) that there is an underlying complete matrix of some low rank from which the partial observations arise. Our algorithms are the first in the low-rank regime that provide information about single entries. They adapt to the combinatorial structure of the observations in that, if it is possible, the reconstruction process can be carried out using much less than the full set of observations. We validate our algorithms on real data. We also identify combinatorial features of the low-rank completion problem. This then allows us to study low-rank matrix completion via tools from, e.g., graph theory.

1.1. Results

Here is a preview of the results and themes of this paper, including the answers to the main questions.

Is it possible to reconstruct the entry ?

We show that whether the entry is completable depends, with probability one for any continuous sampling regime, only on the positions of the observations and the position that we would like to reconstruct (Theorem 10). The proof is explicit and easily converted into an exact (probability one) algorithm for computing the set of completable positions (Algorithm 1).

How many possible completions are there for the entry ?

Whether the entry at position is uniquely completable from the observations, or, more generally, how many completions there are also depends, with probability one, only on the positions of the observed entries and (Theorem 17). We also give an efficient (randomized probability one) algorithm (Algorithm 1) that verifies a sufficient condition for every unobserved entry to be uniquely completable.

What is the value of the entry ?

To reconstruct the missing entries, we introduce a general scheme based on finding polynomial relations between the observations and one unobserved one at position (Algorithm 5). For rank one matrices (Algorithm 6), and, in any rank, observation patterns with a special structure (Algorithm 4) that allows “solving minor by minor”, we instantiate the scheme completely and efficiently.

Since, for a specific , the polynomials needed can be very sparse, our approach has the property that it adapts to the combinatorial structure of the observed positions. To our knowledge, other algorithms for low-rank matrix completion do not have this property.

How accurately can one estimate entry ?

Our completion algorithms separate out finding the relevant polynomial relations from solving them. When there is more than one relation, we can use them as different estimates for the missing entry, allowing for estimation in the noisy setting (Algorithm 5). Because the polynomials are independent of specific observations, the same techniques yield a priori estimates of the variance of our estimators.

Combinatorics of matrix completion

Section 6 contains a detailed analysis of whether an entry is completable in terms of a bipartite graph encoding the combinatorics of the observed positions. We obtain necessary (Theorem 38) and sufficient (Proposition 42) conditions for local completability, which are sharp in the sense that our local algorithms apply when they are met. We then relate the properties we find to standard graph-theoretic concepts such as edge-connectivity and cores. As an application, we determine a binomial sampling density that is sufficient for solving minor-by-minor nearly exactly via a random graph argument.

Experiments

Section 7 validates our algorithms on the Movie Lens data set and shows that the structural features identified by our theories predict completability and completability phase transitions in practice.

1.2. Tools and themes

Underlying our results are a new view of low-rank matrix completion based on algebraic geometry. Here are some of the key ideas.

Using the local-to-global principle

Our starting point is that the set of rank , -matrices carries the additional structure of an irreducible algebraic variety (see Section 2.1). Additionally, the observation process is a polynomial map. The key feature of this setup is that it gives us access to fundamental algebraic-geometric “local-to-global” results (see Appendix A) that assert the observation process will exhibit a prototypical behavior: the answers to the main questions will be the same for almost all low-rank matrices, so they are essentially properties of the rank and observation map. This lets us study the main questions in terms of observed and unobserved positions rather than specific partial matrices.

On the other hand, the same structural results show we can certify that properties like completability hold via single examples. We exploit this to replace very complex basis eliminations with fast algorithms based on numerical linear algebra.

Finding relations among entries using an ideal

Another fundamental aspect of algebraic sets are characterized exactly by the vanishing ideal of polynomials that evaluate to zero on them. For matrix completion, the meaning is: every polynomial relation between the observations and a specific position is generated by a finite set of polynomials we can in principle identify (See Section 5).

Connecting geometry to combinatorics using matroids

Our last major ingredient is the use of the Jacobian of the observation map, evaluated at a “generic point”. The independence/dependence relation among its rows is invariant (with matrix-sampling probability one) over the set of rank matrices that characterizes whether a position is completable. Considering the subsets of independent rows as simply subsets of a finite set, we obtain a linear matroid characterizing completability. This perspective allows access to combinatorial tools of matroid theory, enabling the analysis in Section 6.

1.3. Context and novelty

Low-rank Matrix Completion has received a great deal of attention from the community. Broadly speaking, two main approaches have been developed: convex relaxations of the rank constraints (e.g., Candès and Recht, 2009; Candès and Tao, 2010; Negahban and Wainwright, 2011; Salakhutdinov and Srebro, 2010; Negahban and Wainwright, 2012; Foygel and Srebro, 2011; Srebro and Shraibman, 2005); and spectral methods (e.g., Keshavan et al., 2010b; Meka et al., 2009; Chaterjee, 2012). Both of these (see Candès and Tao, 2010; Keshavan et al., 2010b) yield, in the noiseless case, optimal sample complexity bounds (in terms of the number of positions uniformly sampled) for exact reconstruction of an underlying matrix meeting certain analytic assumptions. All the prior work of which we are aware concentrates on: (i) completing all the unobserved entries; (ii) sets of observed positions sampled from some known distribution. The results here, by contrast, apply specifically to fixed sets of observations and provide information about any unobserved position .

Analogously, all the prior work on Low-rank Matrix Completion from noisy observations concentrates on: (i) estimating every missing entry; (ii) denoising every observed entry; and (iii) minimizing the MSE over the whole matrix. Our approach allows, for the first time, to construct single-entry estimators that minimize the variance of the entry under consideration; Király and Theran (2013b) showed how to do this efficiently in rank .

1.4. Organization

The sequel is structured as follows: Section 2 introduces the background material we need; Sections 3 and 4 develop our algebraic-combinatorial theory and derive algorithms for determining when an entry is completable; Section 5 formulates the reconstruction process itself algebraically; Section 6 contains a combinatorial analysis of the problem; finally Section 7 validates our approach on real data. The Appendix collects some technical results required in the proofs of the main theorems.

2. Background and setup

In this section, we introduce two essential objects, the set of low-rank matrices and the set of observed positions . We also define the concept of genericity.

2.1. The determinantal variety

First, we set up basic notation. A matrix is denoted by upper-case bold character like . We denote by the set of integers . denotes the submatrix of an matrix specified by the sets of indices and . The element of a matrix is denoted by . The cardinality of a set is denoted by .

Now we define the set of matrices of rank at most .

Definition 1.

The set of all complex -matrices of rank or less will be denoted by We will always assume that by transposing the matrices, this is no loss of generality.

Some basic properties of are summarized in the following proposition.

Proposition 2 (Properties of the determinantal variety).

The following hold for :

-

(i)

is the image of the map , where and , and is therefore irreducible.

-

(ii)

has dimension

-

(iii)

Every minor of a matrix in is zero, namely,

where , , and .

-

(iv)

The vanishing ideal of is generated by the vanishing of the minors from part 3.

Proof.

(i) The existence of the singular-value decomposition imply that is the surjective image of under the algebraic map .

(ii) This follows from (i) and the uniqueness of the SVD, or (Bruns and Vetter, 1988, section 1.C, Proposition 1.1).

(iii) The rank of a matrix equals the order of the largest non-vanishing minor.

(iv) By (Bruns and Vetter, 1988, Theorem 2.10, Remark 2.12, and Corollary 5.17f), the ideal generated by the minors is prime. Since it vanishes on the irreducible , it is the vanishing ideal. ∎

The set of observed positions is denoted by and can be viewed as a bipartite graph as follows.

Definition 3.

Let . The set containing the positions of observed entries is denoted by . We define the bipartite graph with vertices corresponding to rows and vertices corresponding to columns. We call the adjacency matrix of the bipartite graph a mask. The map

where , is called a masking (in rank ).

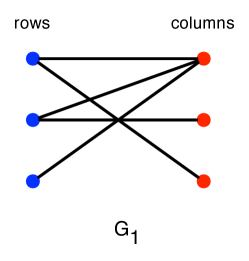

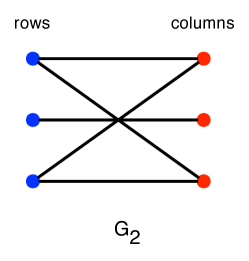

Note that the set of observed positions , the adjacency matrix , and the map can be used interchangeably. For example, we denote by the adjacency matrix corresponding to the map , and by the set of positions specified by , and so on. Figure 1 shows two bipartite graphs and corresponding to the following two masks:

2.2. The Jacobian of the masking operator

Informally, the question we are going to address is:

Which entries of are (uniquely) reconstructable, given the masking ?

The answer will depend on the interaction between the algebraic structure of and the combinatorial structure of . The main tool we use to study this is the Jacobian of the map , since at smooth points, we can obtain information about the dimension of the pre-image from its rank.

Definition 4.

We denote by the Jacobian of the map . More specifically, the Jacobian of the map from and to can be written as follows:

| (6) |

where is the th row vector of and is the th row vector of . Stacking the above row vectors for , we can write the Jacobian as an matrix as follows:

| (7) |

where denotes the Kronecker product. Here the rows of correspond to the entries of in the column major order.

Lemma 5.

Every matrix whose vectorization lies in the left null space of satisfies

and any satisfying the above lies in the left null space of . In addition, the dimension of the null space is if and have full column rank .

Proof.

Let be the permutation matrix defined by

Note that , and

Thus we have

which is what we wanted. To show the last part of the lemma, let and be any basis of the orthogonal complement space of and , respectively. Since the null space can be parametrized as by , and this parametrization is one-to-one, we see that the dimension of the null space is . ∎

Now we define the Jacobian corresponding to the set of observed positions .

Definition 6.

For a position , we define to be the single row of corresponding to the position . Similarly, we define to be the submatrix of consisting of rows corresponding to the set of observed positions . Due to the chain rule, is the Jacobian of the map .

2.3. Genericity

The pattern of zero and non-zero entries in (6) hints at a connection to purely combinatorial structure. To make the connection precise, we introduce genericity.

Definition 7.

We say a boolean statement holds for a generic in irreducible algebraic variety , if for any Hausdorff continuous measure on , holds with probability .

These kinds of statements are sometimes called “generic properties,” and they are properties of , rather than any specific . The prototypical example of a generic property is where , is a polynomial, and the statement is “.”

Here, we are usually concerned with the case . Proposition 2 tells us that , and define completely. Assertions of the form “For generic , depends only on ” mean is a generic statement for all with the parameters fixed.

Although showing whether some statement holds generically might seem hard, we are interested in defined by polynomials. In this case, results in Appendix A imply that it is enough to show that either holds: (a) on an open subset of in the metric topology; or (b) almost surely, with respect to a Hausdorff continuous measure.

As a first step, and to illustrate the “generic philosophy” we show that the generic behavior of the Jacobian is a property of . We first start by justifying the definition via (as opposed to ).

Lemma 8.

For all and generic, with , and and generic, the rank of is independent of , , and .

Proof.

We first consider the composed map . This is a polynomial map in the entries of and , so its critical points (at which the differential attains less than its maximum rank) is an algebraic subset of . The “Semialgebraic Sard Theorem” (Kurdyka et al., 2000, Theorems 3.1, 4.1) then implies that the set of critical points is, in fact, a proper algebraic subset of .

So far, we have proved that the rank of is independent of and . However, and are not uniquely determined by . To reach the stronger conclusion, we first observe that a generic is a regular value of , again by Semialgebraic Sard. Thus, the set of such that and are both regular values is the intersection of two dense sets in . ∎

3. Finite completability

This section is devoted to the question “Is it possible to reconstruct the entry ?”. We will show that under mild assumptions, the answer depends only on the position , the observed positions, and the rank, but not the observed entries. The main idea behind this result is relating reconstructability to the rows of the Jacobian , and their rank, which can be shown to be independent of the actual entries for almost all low-rank matrices. Therefore, we can later separate the question of reconstructibility from the actual reconstrution process.

3.1. Finite completability as a property of the positions

We show how to predict whether the entry at a specific position will be reconstructible from a specific set of positions . For the rest of this section, we fix the parameters , and , and denote by a set of observed positions. The symbol will denote either of the real numbers or the complex numbers .

We start by precisely defining what it means for one set of entries to imply the imputability of another entry.

Definition 9.

Let be a set of observed positions and be a rank true matrix. The entry is finitely completable in rank from the observed set of entries if the entry can take only finitely many values when fixing .

There are two subtleties here: the first is that, even if there is an infinity of possible completions for the whole matrix , it is possible that some specific takes on only finitely many values; the question of whether the entry at position is finitely completable may have different answers for different . The theoretical results in this section take care of both issues.

Theorem 10.

Let be a set of positions, be arbitrary, and let be a generic, -matrix of rank . Whether the entry at position is finitely completable depends only on the position , the true rank , and the observed positions (and not on , , , or ).

This lets us talk about the finite completability of positions instead of entries.

Definition 11.

Let be a set of observed positions, and . We say that the position is finitely completable from in rank if, for generic , the entry is finitely completable from . The rank finitely completable closure is the set of positions generically finitely completable from .

The main tool we use to prove Theorem 10 is the Jacobian matrix . For it, we obtain

Theorem 12.

Let and let be a generic, rank matrix. Then

One implication of Theorem 12 is that linear independence of subsets of rows of is also a generic property. (In fact, the proof in Section 3.3 goes in the other direction.) The combinatorial object that captures this independence is a matroid.

Definition 13.

Let be a generic rank matrix. The rank determinantal matroid is the linear matroid , with rank function .

In the language of matroids, Theorem 12 says that, generically, the finitely completable closure is equal to the matroid closure in the rank determinantal matroid. This perspective will prove profitable when we consider entry-by-entry algorithms for completion in Section 5 and combinatorial conditions related to finite completability in Section 6.

3.2. Computing the finite closure

We describe, in pseudo-code, Algorithm 1 which computes the finite closure of . An algorithm for testing whether a single entry is finitely completable is easily obtained by only testing the entry in step 4. The correctness of Algorithm 1 follows from Theorem 12 and the fact that, if we sample and from any continuous density, with probability one, we obtain generic and .

Input: A set of observed positions.

Output: The rank completable closure .

Remark 14.

We have presented Algorithm 1 as a numerical routine based on SVD. It is also strongly polynomial time in the RAM model. The key observation is that all of our computations estimate only the rank of a matrix, which is a polynomial identity testing problem. By Proposition 2, the rank of is never higher than . If , then , so the the rank of is detected by a minor of degree . The main result of Schwartz (1980) then implies that, if we sample the entries of and uniformly from a field of prime order , with probability we obtain the generic rank of and each , using, e.g., Gaussian elimination.

3.3. Proofs

3.3.1. Proof of Theorem 12

Let . Factor the map into

so that is the projection of onto the set of entries at positions and then projects out the coordinate corresponding to . Lemma 8 implies that, since is generic, all the intermediate image points are smooth. The constant rank theorem then implies that we can find open neighborhoods and such that the restriction of to is smooth and . The constant rank theorem then implies that we have

Since, again using smoothness,

and

the position is finitely completable from and , if and only if

| (8) |

Equation (8) is just the assertion that .

By Lemma 8, Equation (8) is a generic statement, independent of , and . Because the rows of and have non-zero columns only at positions depending on and , whether (8) holds does not depend on and (which are, by hypothesis, large enough).

Finally, statement that finite completability is the same for and follows from Theorem 65 in the appendix. ∎

3.3.2. Proof of Theorem 10

The theorem follows directly from Theorem 12 and the definition of closure. ∎

3.4. Discussion

The kernel of spans the space of infinitesimal deformations of that preserve . Because generic points are smooth, (Milnor, 1968, Curve Selection Lemma) implies that every infinitesimal deformation can be integrated to a finite deformation. Conversely (this is the harder direction) every curve in through has, as its tangent vector a non-zero infinitesimal deformation. At non-generic points, this equivalence does not hold, so the arguments here require genericity and smoothness in an essential way.

The finite identifiability statements in this section are instances of a more general phenomenon, which is explored in Király et al. (2013). The results there imply similar identifiability results, such as Hsu et al. (2012); Allman et al. (2009); Bamber (1985), that use criteria based on a Jacobian, and also show that our use of the “” parameterization of is not essential.

Another connection is that, since permuting the rows and columns of a matrix preserves its rank, we get:

Corollary 15.

The rank function of the determinantal matroid depends only on the graph isomorphism type of the graph associated with .

4. Unique completability

In this section, we will address the question “How many possible completions are there for the entry ?”. In section 3.1, it was shown that whether the entry is completable depends (under mild assumptions) only on the position , the observed entries, and the rank. In this section, we show an analogue result that the same holds for the number of possible completions as well. Whether there is exactly one solution is of the most practical relevance, and we give a sufficient condition for unique completability.

4.1. Unique completability as a property of the positions

We start by defining what it means for one entry to be uniquely completable:

Definition 16.

Let be a set of observed positions and be a rank true matrix. The entry at position is called uniquely completable from the entries , if is uniquely determined by the .

The main theoretical statement for unique completability is an analogue to the main theorem for finite completability; again, whether an entry is uniquely completable, depends only on the positions of the observations, assuming the true matrix is generic.

Theorem 17.

Let be a generic -matrix of rank , and consider a masking where the entries with are observed. Let be arbitrary. Then, whether is uniquely completable from the depends only on the position , the true rank and the observed positions (and not on , or ).

The proof of Theorem 17 is a bit more technical than its finite completability analogue, Theorem 10. The main problem is that the constant rank theorem cannot be applied since the latter is a local statement only and does not make say anything about the global number of solutions. The proper tools to overcome that are found in algebraic geometry; a complete proof is deferred to section 4.4. The proof we give also shows that there is an analoge statement for the total number of possible completions, even if there is more than one. Since the number of completions over the reals can potentially change even with generic , the result is stated only over the complex numbers.

Theorem 17 shows that it makes sense to talk about positions instead of entries that are uniquely completable, in analogy to the finite case; moreover, it shows that there is a biggest such set:

Definition 18.

Let be the set of observed positions, and let be a position. We will call uniquely completable if is uniquely completable from for a generic matrix of rank .

Furthermore, we will denote by the inclusion-wise maximal set of positions such that every index is uniquely completable from . We will call the unique closure of in rank .

As for finite completability, we can check generic unique completability of a position by testing a random . However, we don’t have an analogue for the Jacobian that exactly characterizes unique completability. One could, of course, use general Gröbner basis methods, but these are computationally impractical. In the next section, we describe an easy-to-check sufficient condition for unique completability in terms of the Jacobian.

4.2. Characterization by Jacobian stresses

As for the case of finite completability, the Jacobian of the masking can be used to provide algorithmic criteria to determine whether an entry is uniquely completable. The characterizing objects will be the so-called stresses, dual objects to the column space of the Jacobian. Intuitively, they correspond to infinitesimal dual deformations. Singer and Cucuringu (2010, Equation 3.7) have conjecturally defined a similar concept.

Mathematically, stresses are left kernels of the Jacobian:

Definition 19.

A rank- stress of the matrix is a matrix whose vectorization is in the left kernel of the Jacobian ; that is,

Let be a set of observed entries. A stress such that for all is called -stress of .

The -vector space of -stresses of will be denoted by noting that it does not depend on the choice of .

Note that -stresses are, after vectorization and removing zeroes, in the left kernel of the partial Jacobian .

The central property of the stress which allows to test for unique completability is its rank as a matrix:

Definition 20.

Let be as set of observed entries. We define the maximal -stress rank of in rank to be

As for the rank of the Jacobian, the dependence on can be removed for generic matrices:

Proposition 21.

Let be a generic -matrix of rank . The maximal stress rank depends only on and . In particular, does not depend on the entries of .

Proof.

Let . By Cramer’s rule, if , the entries of are rational functions of the entries of and . After clearing denominators, the proof is similar to that of Lemma 8. ∎

We can therefore just talk about the generic -stress rank, omitting again the dependence on the entries :

Definition 22.

Let be as set of observed entries. We define the generic -stress rank to be equal to for generic or rank .

Our main theorem states that if the generic -stress rank is maximal for finitely completable , then is also uniquely completable:

Theorem 23.

Let . If the generic -stress rank in rank is , then .

We defer the somewhat technical proof to section 4.4.

4.3. Computing the generic stress rank

Theorem 23 implies that the generic stress rank can be used to certify unique completability of an observation pattern . We explicitly describe the necessary computational steps in Algorithm 2.

Input: Observed positions . Output: The generic stress rank of in rank .

As the algorithm for finite completion, it uses a randomized strategy which allows to compute over the real numbers instead of a field of rational functions by substituting a generic entry. Steps 1 and the beginning of step 2 are thus analogous as in Algorithm 1. In step 2, the completion matrix is computed, evaluated at the matrices . In 3, an evaluated stress is obtained in the left kernel of . Its rank, which is computed in step 5, will be the generic stress rank. Correctness (with probability one) is implied by Proposition 21. Also, similar to Algorithm 1, Algorithm 2 is a randomized algorithm for which considerations analogue to those in Remark 14 hold.

4.4. Proofs

4.4.1. Proof of Theorem 17

4.4.2. Proof of Theorem 23

This sections contains the proof for Theorem 23 and some related results.

Lemma 24.

Let be a stress w.r.t. . Then,

(where denotes the zero matrix of the correct size).

Proof.

Since is an stress, it holds by definition that The statement then follows from Lemma 5. ∎

Lemma 24 immediately implies a rank inequality:

Corollary 25.

Let , assume the true matrix has full rank . Then, it holds that

Proof.

In keeping with our development of finite completability in terms of , we have defined stresses in a way that might depend on the coordinates . In the proof of Theorem 23, we will check that this can be removed when necessary. An alternative but probably less concise approach would be to express the matrix directly in terms of the entries .

Proof of Theorem 23

We start with a general statement that stresses are invariant over the pre-image .

Lemma 26.

Let be generic, with , , and an -stress. Then is also an -stress for any with

Proof.

Let be a point different from . Because is a regular value of the composed map , the Inverse Function Theorem provides diffeomorphic neighborhoods and ; let be the diffeomorphism.

By construction, is non-singular. The chain rule then implies that , so the left kernels of both Jacobians are the same. The definition of stress as a vector in the left kernel then proves the lemma. ∎

Proof of Theorem 23.

It is clear that . Thus we show that . By Lemma 26, is a stress for any that agrees with the observed entries on the observed positions . Then by Lemma 24, any such pair must satisfy and . Since generically the stress has rank , these equations determine the row and column spans of . Once the row and column spans are fixed, any row or column with at least observed positions can be uniquely determined. On the other hand, any row or column with fewer than observed positions cannot be recovered (even if the row or column span is known). Therefore we have . ∎

5. Local completion

In this section, we connect our theoretical results to the process of reconstructing the missing entries. In a nutshell, the idea is that a completable missing entry is covered by at least one so-called circuit in , to which we can associate circuit polynomials which can be used to solve for in terms of the observations, addressing the question “What is the value of the entry ?”. Just as in theory where we could separate the reconstructability from the reconstruction, we can obtain a quantitative version of this separation by estimating the entry-wise reconstruction error without actually performing the reconstruction, allowing to give an answer to “How accurately can one estimate the entry ?”. We give general algorithms for arbitrary rank, and a closed-form solution for rank one.

5.1. Circuits as rank certificates

We start with some concepts from matroid theory.

Definition 27.

A set of observed positions is called a circuit of rank if and for all proper subsets . The graph is called circuit graph of rank .

A reformulation of Theorem 10, in terms of circuits is the following.

Theorem 28.

The position is finitely completable if and only if there is a circuit with .

Proof.

See (Oxley, 2011, Lemma 1.4.3) ∎

The connection to reconstructing missing entries is that every circuit comes with a unique polynomial:

Theorem 29.

Let be a circuit in rank , be the mask corresponding to , and . There is a unique, up to scalar multiplication, square-free polynomial such that: if and only if there is and .

Proof.

In other words, circuit polynomials minimally certify for the rank condition being fulfilled on the entries in . The simplest example of a circuit is an rectangle in . The associated polynomial is the determinant of an minor of . Thus, Theorem 29 is a generalization of the linear algebra fact that a matrix is rank if and only if all -minors vanish.

Definition 30.

We will call the polynomial from Theorem 29 a circuit polynomial associated to the circuit . Understanding that there are an infinity up to multiplication with a scalar multiple, we will also talk about the circuit polynomial when that does not make a difference.

Remark 31.

The circuit polynomial can be interpreted algorithmically as follows: let be a circuit, assume all entries but one in are observed, e.g., is not observed and is observed. Then, can be interpreted as a polynomial in the one unknown . That is, the circuit polynomial allows to solve entry-wise for single missing entries.

Definition 32.

Fix some set of observed entries . A circuit is called completing for the observations in , or with respect to , if .

5.2. Completion with circuit polynomials

The circuit properties inspire a general solution strategy.

Input: A set of observed positions.

Output: Estimates for the entries

In general, Algorithm 3 is ineffective, in the sense that Step 4 is unlikely to have a sub-exponential time algorithm in the general case. However, there is a specific instance in which it is effective: when the circuit is always an rectangle. In this case, the circuit polynomial is the corresponding minor. This means that enumerating all the circuits through is not necessary, because a minor is linear in the unknown entry .

A practical algorithm for computing the closure of a mask and recovering the corresponding entries based on minors is given in Algorithm 4. In Step 5, and denote the set of neighbors of vertices and , respectively. In Step 10, denotes the Moore-Penrose pseudoinverse of . Intuitively, the algorithm iterates over missing edges and look if there is a biclique in the union of current set of edges and . If such a biclique exists, then the edge is added to so that the edge is used in the next round. The iteration terminates when there is no more edge to add.

Inputs: bipartite graph , rank .

Outputs: completed matrix and minor closure of .

Note that is uniquely determined from and the process is monotone and bounded, i.e., . The first statement is true because the order of the iteration over missing edges in line 4 is irrelevant as we look if there is a biclique in for each missing edge . Therefore, Algorithm 4 terminates with either or and the following definition is valid.

Definition 33.

Since each entry is uniquely determined when it is reconstructed, any minor closable set is uniquely completable.

A crucial step in Algorithm 4 is FindAClique in line 7. The function should return the indices of rows and columns, if an biclique exists in subgraph . This can be achieved in various ways. Although the worst case complexity is , it can be much more efficient in practice, because many vertices can be safely pruned due to the fact that any biclique may not contain vertices with degree less than . An efficient implementation that employs a row-wise recursion of this step, proposed by Takeaki Uno, is presented in Appendix B.

5.3. Local completion

The circuit property can also be interpreted differently: instead of using multiple ciruits to complete many different entries, one can also think of concentrating on one single entry and trying to reconstruct that as accurately as possible. Algorithm 5 describes a general strategy on how to obtain estimates of single finitely or uniquely completable entries, from noisy observations via local circuit completion.

Input: A set of observed positions, the entry.

Output: Estimate for

The idea in Algorithm 5 is to obtain many candidate solutions in step 3 and then trade them off appropriately in step 4. If all circuit polynomials have degree one, there is only one solution per polynomial, and can be taken as the mean, or a weighted average that minimizes some loss or a variance. If there are some circuit polynomial with higher degree, then one can try to decide which solution is the right one - e.g., by clustering the and rejecting all candidate solutions except the one which contains some for the highest number of , and then proceeding as in the degree one case. Also, one can imagine being adaptive, e.g. including Bayesian learning methods.

For rank one, an closed explicit form is possible for the variance minimizing estimate, as it was shown in Király and Theran (2013b). For arbitrary rank, a first-order approximation to variance minimization can be employed to yield fast and competitive single-entry estimates, by results from Blythe et al. (2014).

For illustration, we give a short overview of the crucial statements in the rank one case. The proofs can be found in Király and Theran (2013b).

Theorem 34.

The rank one circuit graphs are exactly the simple cycles (bipartite and thus of even length). The corresponding circuit polynomials are all binomials of the form

where is an arbitrary number, are arbitrary disjoint numbers, and are arbitrary disjoint numbers, with the convention that . The and do not need to be disjoint from each other.

In particular, Theorem 34 implies that the circuit polynomials are all linear in every occurring variable. Moreover, the specific structure of the problem allows a further simplification:

Remark 35.

With the elementary computation in Remark 35, matrix completion becomes estimation with linear boundary constraints. That is, the function in step 4 of Algorithm 5 could be taken as the least squares regressor of all obtained from completing circuits for . The algorithm in Király and Theran (2013b) gives a version which takes different observation variances into account, and efficient graph theoretical observations making the computation polynomial.

We paraphrase this as Algorithm 6; more details, e.g. on how to efficiently find a basis for the set of completing circuits111This is equivalent to finding a basis for first -homology of the graph , taken as a -complex. is efficiently found, or how the kernel matrix is constructed, can be found in Király and Theran (2013b).

Input: A set of observed positions, observation variances , the position .

Output: Estimate for

5.4. Variance and error estimation

The locality of circuits also allows to obtain estimates for the reconstruction error of single missing entries obtained by the strategy in section 5.3, independent of the method which does the actual reconstruction. The simplest estimate of this kind is obtained from a variational approach: say is a completing circuit (w.r.t ) for the missing entry . In the simplest case, where is linear in the missing entry , we can obtain a solving equation

by solving for as an unknown. A first order approximation for the standard error can be obtained by the variational approach

The right hand side can be obtained from a suitable noise model and the observations , or, if the error should be estimated independently from the , from a noise model plus a sampling model for the . A general strategy for entry-wise error estimation is analogous to Algorithm 5 for local completion. For rank one, it has been shown in Király and Theran (2013b) that the variance estimate depends only on the noise model and not on the actual observation, and takes a closed logarithmic-linear form, as it is sketched in Algorithm 7.

Input: A set of observed positions, observation variances , the position .

Output: Estimate for the (log-)variance error of the estimate

Note that the log-variance error is independent of the actual estimate , therefore the variance patterns can be estimated without actually reconstructing the entries.

6. Combinatorial completability conditions

Through Sections 3 and 4, we have shown that for a given , both finitely completable closure (Theorem 12) and uniquely completable closure (Theorem 17) are properties of the (isomorphism type of) the associated bipartite graph ; see also Corollary 15.

In this Section, using tools from graph and matroid theories, we relate the structural properties of the bipartite graph to the finite completability.

For a set of observed positions, , let be a bipartite graph, where the sets of vertices and correspond to row and column of the observed positions; we call and row vertices and column vertices, respectively. We assume that has no isolated vertices (those corresponding to rows or columns with no observed positions.)

As usual, we will take , , and to be the rank and parameters of the ground set , respectively. However, since our convention for graphs is that they do not have isolated vertices, we will take care to indicate the ambient ground set.

6.1. Sparsity and independence

Suppose we want to maximize the size of the completable closure , with the number of positions to observe fixed. To do this, consider the process of constructing one position at a time. What we need is to pick each successive entry in a way that causes to grow. Theorem 12 implies that a position is finitely completable from , if and only if lies in the span of . In particular, this tells us that adding such a to will not affect the finite completability of other unobserved positions; in matroid terminology, we say is dependent on . We see, then, that it is wasteful to choose positions that are dependent on the already chosen positions. Therefore intuitively we need to choose the positions so that they are well spread out, which we call rank- sparse; see Section 6.1.1. Rank- sparsity implies a more classical combinatorial property, namely -connectivity; see Section 6.1.2. Finally, in Section 6.1.3, we show by a counterexample that rank- sparsity, though necessary, is not a sufficient condition for finite completability.

We recall some basic terminologies from matroid theory. The rank function of the rank determinantal matroid is defined in Definition 13. Note that , where if and , , otherwise. A set of positions is called independent if . On the other hand, it is called dependent if . A basis of is a maximally independent subset of . In addition, a basis of is called a basis of the rank determinantal matroid. A basis of consists of edges. In particular, a basis of the rank determinantal matroid consists of edges. A basis of is not unique unless is independent. A circuit of of the rank determinantal matroid is a minimally dependent set in the sense that for any , is an independent set; see also Definition 27.

We have the following two properties from matroid theory.

Proposition 36.

-

1.

Let be a set of observed positions and be any basis of . Then, .

-

2.

Let be an independent set in the rank determinantal matroid. Then, any is independent.

In other words, (i) the finitely completable closures of and any basis of are the same (ii) and an independent graph cannot contain a dependent subgraph . Both statements arise from the fact that the rank- determinantal matroid is a linear matroid defined by the linear independence of the rows of the Jacobian and that the matroid closure coincides with the finitely completable closure.

6.1.1. Rank--sparsity

Let be a subgraph of . Since being independent implies a bound on the cardinality , we consider the notion of rank--sparsity defined as follows.

Definition 37.

A graph is rank--sparse if, for all subgraphs of , .

Theorem 38.

Let be an independent set in the rank determinantal matroid on . Then is rank--sparse.

Proof.

Suppose that there is a subgraph with , then this subgraph must be dependent, which contradicts Proposition 36, part 2. ∎

6.1.2. Connectivity and vertex degrees

Rank sparsity implies some other, more classical, graph theoretic properties in a straightforward way, since rank--sparsity is hereditary.

Corollary 39.

Let , and be the set of observed positions. If contains a rank- sparse subgraph with edges, then:

-

1.

has minimum vertex degree at least .

-

2.

is -edge-connected.

In particular, if is finitely completable, it contains a basis (Proposition 36, part 1) with edges and is rank- sparse. Thus, is -edge connected.

The proof of the above corollary relies on the following lemma:

Lemma 40.

Let be rank- sparse with edges, and be an edge disjoint partition of . For any set of edges incident to row and column vertices, we define . Then we have

Proof.

By the assumption,

where the first equality holds because is independent and the last inequality follows from Theorem 38. ∎

Proof of Corollary 39.

Since Statement 2 implies statement 1, we prove Statement 2. First, we can assume without loss of generality that is rank- sparse and without loss of generality, because if is -edge-connected, so is .

Consider any partition and . or can be empty (but not at the same time). This induces an edge disjoint partition , where and are sets of edges induced by and , respectively. Treating each edge in as a subgraph, we have . By applying Lemma 40, we have

| (9) |

Let , , , and . Due to symmetry, there are three situations that we need to consider. First, if , . Next, if and , , which is true considering maximizing the inner product between and subject to and . Finally, if , . The minimum is obtained for and , or vice versa. Therefore is -edge connected. ∎

6.1.3. Sparsity is not sufficient

On the other hand, rank sparsity is not a sufficient condition for independence in determinantal matroids. The bipartite graph defined by the following mask in rank have edges and rank- sparse but not independent:

This example amounts, graph theoretically, to gluing the graphs of two bases of the determinantal matroid together along vertices in a way that preserves rank--sparsity but not independence. One can make the construction rigorous to show that, for any , there are infinitely many rank--sparse dependent sets in the determinantal matroid.

6.2. Circuit and stress supports

We have discussed stresses in Section 4 and circuits in Section 5. Here we show that for each circuit , there is a corresponding stress that is supported on every position of . Here the support of stress is defined as . Moreover, using the structure of the Jacobian matrix (see Definition 4), we show that every vertex of circuit has degree at least . These results further imply that any finitely completable position spans vertices in the -core (see Section 6.2.1). Furthermore, combining the above degree lower bound with the rank- sparsity shown in the previous subsection, we show a bound on the number of circuits in the rank determinantal matroid in Section 6.2.2. The proof of the key Theorem 41 is presented in Section 6.2.3.

Theorem 41.

For a generic , and a circuit , the stress space is one dimensional; thus a stress of a circuit is unique up to scalar multiplication. Moreover, the support of is all of .

The power of Theorem 41 can be seen in the following proposition, which lower bounds the degree of a vertex in a circuit.

Proposition 42.

Let be a circuit in the rank determinantal matroid. Then every vertex in the graph has degree at least edges.

Proof.

By Theorem 41, for generic , the rows of are dependent, with the associated stress supported on all the rows.

From (7), we see that any vertex is associated with exactly columns in . Let be the indices of these columns. The number of non-zero rows in is exactly the degree of . If we suppose , the stress cannot generically cancel these columns. Therefore, it holds that . ∎

6.2.1. Where are the completable positions?

The concept of -core is useful for narrowing down where the completable positions can be and where the circuits can lie.

We recall a concept from graph theory:

Definition 43.

Let be a graph, and let . The -core of , denoted , is the maximal subgraph of with minimum vertex degree .

In rank , the non-trivial aspects of matrix completion occur inside the -core.

Theorem 44.

Let ,

-

(i)

If and , then the vertices and are in .

-

(ii)

Any circuit is contained in .

Proof.

(i) We have if and only if there is a circuit

with . Then will follow from because for

, we need

and .

(ii) This follows from the fact that the -core is the union of all

induced subgraphs with minimum degree at least and by Proposition

42, every lies inside such an induced subgraph.

∎

Note here that , so the same things are true for the uniquely completable closure.

6.2.2. Circuit size and counting

Combining the results in this section, we obtain bounds on the number of circuits in the rank determinantal matroid.

Theorem 45.

Let be a circuit in the rank determinantal matroid with graph . Then

Proof.

Corollary 46.

The number of circuits in the rank determinantal matroid on is at most .

6.2.3. Proof of Theorem 41

First, by Definition 19, . Thus the left null space of is one dimensional.

Next, we explicitly construct a stress . By Theorem 29, there is a unique polynomial for each circuit . Then taking the derivative of , we have

for any tangent vector of at . The vector is, then, a stress for . In addition, the coefficient of the stress is uniquely determined by the entries . If any of the coefficients of were identically zero, we could remove the associated row of and the left-kernel of would still be one-dimensional. Since this is a contradiction to being a circuit, we conclude that none of the coefficients are identically zero. Since the coefficients are, in addition, polynomials in , each of them is non-vanishing on a Zariski open subset of . The (finite) intersection of these sets is again open, proving that the generic support of the stress is all of .

6.3. Completability of random masks

Up to this point we have considered the completability of a fixed mask, which we have shown to be equivalent to questions about the associated bipartite graph. We now turn to the case where the masking is sampled at random, which, by Corollary 15, implies that, generically, this is a question about random bipartite graphs.

6.3.1. Random graph models

A random graph is a graph valued random variable. We are specifically interested in two such models for bipartite random graphs:

Definition 47.

The Erdős-Rényi random bipartite graph is a bipartite graph on row and column vertices vertices with each edge present with probability , independently.

Definition 48.

The -biregular random bipartite graph is the uniform distribution on graphs with row vertices, column ones, and each row vertex with degree and each column vertex with degree .

Clearly, we need , and if , the -regular random bipartite graph is, in fact -regular.

We will call a mask corresponding to a random graph a random mask. We now quote some standard properties of random graphs we need.

Proposition 49.

- (Connectivity threshold)

-

The threshold for to become connected, w.h.p., is (Bollobás, 2001, Theorem 7.1).

- (Minimum degree threshold)

-

The threshold for the minimum degree in to reach is . When , w.h.p., there are isolated vertices (Bollobás, 2001, Exercise 3.2).

- (-regular connectivity)

-

With high probability, is -connected (Bollobás, 2001, Theorem 7.3.2). (Recall that we assume ) .

- (Density principle)

-

Suppose that the expected number of edges in either of our random graph models is at most , for constant . Then for every , there is a constant , depending on only and such that, w.h.p., every subgraph of vertices spanning at least edges has (Janson and Luczak, 2007, Lemma 5.1).

- (Emergence of the -core)

-

Define the -core of a graph to be the maximal induced subgraph with minimum . For each , there is a constant such that is the first-order threshold for the -core to emerge. When the -core emerges, it is giant and afterwards its size and number of edges spanned grows smoothly with Pittel et al. (1996).

6.3.2. Sparser sampling and the completable closure

The lower bounds on sample size for completion of rank incoherent matrices do not carry over verbatim to the generic setting of this paper. This is because genericity and incoherence are related, but incomparable concepts: there are generic matrices that are not incoherent (consider a very small perturbation of the identity matrix); and, importantly, the block diagonal examples showing the lower bound for incoherent completability are not generic, since many of the entries are zero.

Thus, in the generic setting, we expect sparse sampling to be more powerful. This is demonstrated experimentally in Section 7.2. In the rest of this section, we derive some heuristics for the expected generic completability behavior of sparse random masks. We are particularly interested in the question of: when are of the entries completable from a sparse random mask? We call this the completability transition. We will conjecture that there is a sharp threshold for the completability transition, and that the threshold occurs well below the threshold for to be completable.

Let be a constant. We first consider the emergence of a circuit in . Theorem 44 implies that any circuit is a subgraph of the -core. By Theorem 12 and Proposition 36, having a circuit is a monotone property, which occurs with probability one for graphs with more than edges, and thus the value

is a constant. If we define as

smoothness of the growth of the -core implies that we have

where we recall that is the threshold degree for the -core to emerge. Putting things together we get:

Proposition 50.

There is a constant such that, if then w.h.p., is -independent, and, if then w.h.p. contains a giant -circuit inside the -core. Moreover, is at most the threshold for the -core to reach average degree .

Proposition 50 gives us some structural information about where to look for rank circuits in : they emerge suddenly inside of the -core and are all giant when they do. If rank circuits were themselves completable, this would then yield a threshold for the completability transition. Unfortunately, the discussion in Section 6.1.3 tell us that this is not always true. Nonetheless, we conjecture:

Conjecture 50.

The constant is the threshold for the completability transition in . Moreover, we conjecture that almost all of the -core is completable above the threshold.

We want to stress that the conjecture includes a conjecture about the existence of the threshold for the completabilty transition, which hasn’t been established here, unlike the existence for the emergence of a circuit. The subtlety is that we haven’t ruled out examples of -independent graphs with no rank--spanning subgraph for which, nonetheless, the closure in the rank completion matroid is giant. Conjecture 6.3.2 is explored experimentally in Sections 7.1 and 7.2. The conjectured behavior is analogous to what has been proved for distance matrices (also known as bar-joint frameworks) in dimension in (Kasiviswanathan et al., 2011).

Our second conjecture is about -regular masks.

Conjecture 50.

With high probability is completable. Moreover, we conjecture that it remains so, w.h.p., after removing edges uniformly at random.

6.3.3. Denser sampling and the -closure

The conjectures above, even if true, provide only information about matrix completability and not matrix completion. In fact, the convex relaxation of Candès and Recht (2009) does not seem to do very well on -regular masks in our experiments, and the density principle for sparse random graphs implies that, w.h.p., a -regular mask has no dense enough subgraphs for our closability algorithm in section B.1 to even get started. Thus it seems possible that these instances are quite “hard” to complete even if they are known to be completable.

If we consider denser random masks, then the closability algorithm becomes more practical. A particularly favorable case for it is when every missing entry is part of some . In this case, the error propagation will be minimal and, heuristically, finding a is not too hard, even though the problem is NP-complete in general.

Define the -step -closure of a bipartite graph as the graph obtained by adding the missing edge to each in . If the -step closure of is , we define to be -step -closable. We conjecture an upper bound on the threshold for -step -closability.

Conjecture 50.

There is a constant such that, if then, w.h.p., is -step -closable.

7. Experiments

In this section we will investigate the set of entries that are finitely completable from a set of given entries. In section 3 we have seen that the finitely completable closure does not depend on the values of the observed entries but only on their positions . First, we check the set of completable entries for synthetic random positions and empirically investigate the completability phase transitions in terms of the number of known entries, as described in Section 6.3. We also check the number of completable entries for MovieLens data set in terms of the putative rank. Then, we present experiments on actual reconstruction and algorithm-independent error estimation in the case of rank one matrices.

7.1. Randomized algorithms for completability

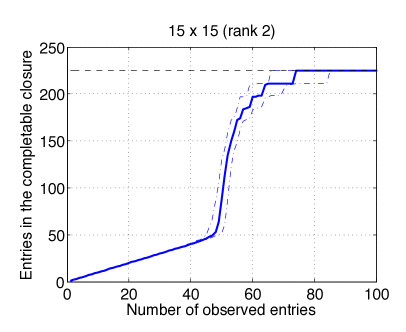

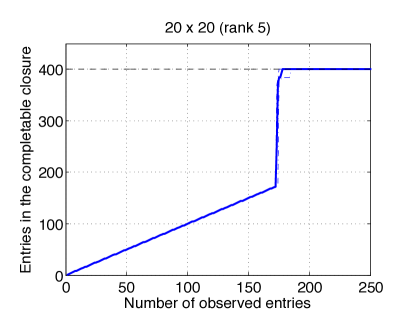

For a quantitative analysis, we perform experiments to investigate how the expected number of completable entries is influenced by the number of known entries. In particular, section 6.3 suggests that a phase transition between the state where only very few additional entries can be completed and the state where a large set of entries can be completed should take place at some point. Figure 2 shows that this is indeed the case when slowly increasing the number of known entries: first, the set of completable entries is roughly equal to the set of known entries, but then, a sudden phase transition occurs and the set of completable entries quickly reaches the set of all entries.

7.2. Phase transitions

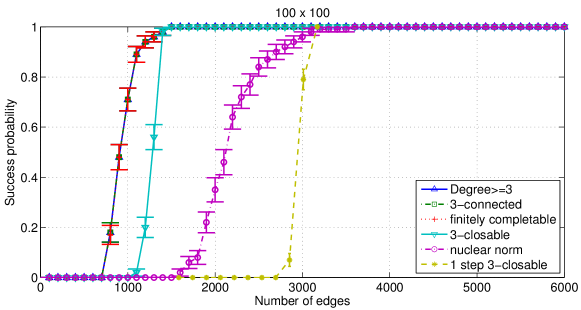

Figure 3 shows phase transition curves of various conditions for matrices at rank 3. We consider uniform sampling model here. More specifically, we generated random masks with various number of edges by first randomly sampling the order of edges (using MATLAB randperm function) and adding 100 entries at a time from 100 to 6000 sequentially. In this way, we made sure to preserve the monotonicity of the properties considered here. This experiment was repeated 100 times and averaged to obtain estimates of success probabilities. The conditions plotted are (a) minimum degree at least , (b) -connected, (c) completable at rank , (d) minor closable in rank (e) nuclear norm successful, and (f) one-step minor closable. For nuclear norm minimization (e), we used the implementation of the algorithm in (Tomioka et al., 2010) which solves the minimization problem

where is the nuclear norm of . The success of nuclear norm minimization is defined as the relative error less than 0.01.

The success probabilities of the (a) minimum degree, (b) -connected, and (c) completable are almost on top of each other, and exceeds chance (probability 0.5) around . The success probability of the (d) minor closable curve passes through 0.5 around . Therefore the -closure method is nearly optimal. On the other hand, the nuclear norm minimization required about entries to succeed with probability larger than 0.5.

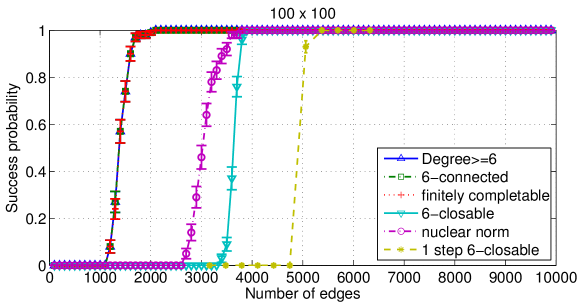

Figure 4 shows the same plot as above for matrices at rank 6. The success probabilities of the (a) minimum degree, (b) -connected, (c) completable are again almost the same, and exceeds chance probability 0.5 around . On the other hand, the number of entries required for minor closability is at least . This is because the masks that we need to handle around the optimal sampling density is so large and sparse that we cannot hope to find a biclique required by the minor clusre algorithm to even get started. The nuclear norm minimization required about samples.

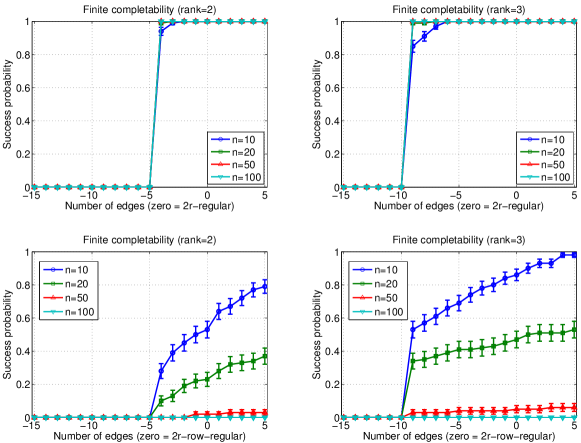

Figure 5 shows the phase transition from a non-completable mask to a completable mask for almost -regular random masks. Here we first randomly sampled -regular masks using Steger & Wormald algorithm (Steger and Wormald, 1999). Next we randomly permuted the edges included in the mask and the edges not included in the mask independently and concatenated them into a single list of edges. In this way, we obtained a length ordered list of edges that become -regular exactly at the th edge. For each ordered list sampled this way, we took the first edges and checked whether the mask corresponding to these edges was completable for . This procedure was repeated 100 times and averaged to obtain a probability estimate. In order to make sure that the phase transition is indeed caused by the regularity of the mask, we conducted the same experiment with row-wise -regular masks, i.e., each row of the mask contained exactly entries while the number of non-zero entries varied from a column to another.

In Figure 5, the phase transition curves for different at rank 2 and 3 are shown. The two plots in the top part show the results for the -regular masks, and the two plots in the bottom show the same results for the -row-wise regular masks. For the -regular masks, the success probability of completability sharply rises when the number of edges exceeds ( for and for ); the phase transition is already rather sharp for and for it becomes almost zero or one. On the other hand, the success probabilities for the -row-wise regular masks grow rather slowly and approach zero for large . This is natural, since it is likely for large that there is some column with non-zero entries less than , which violates the necessary conditions in Corollary 39.

7.3. Completability of the MovieLens data set

This section is devoted to studying a well-known data set - the MovieLens data published by GroupLens - with the methods developed in this paper. We demonstrated how the algorithms given above can be used to make statements about the sets of entries which are (a) completable, (b) uniquely completable, and (c) not completable with any algorithm.

The underlying data set for the following analyses is the MovieLens 100k data set. By convention, columns will correspond to the movies, while the rows will correspond to the users in the data set.

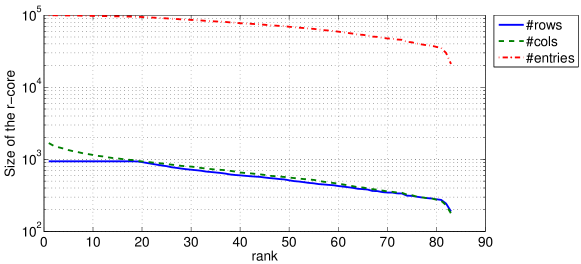

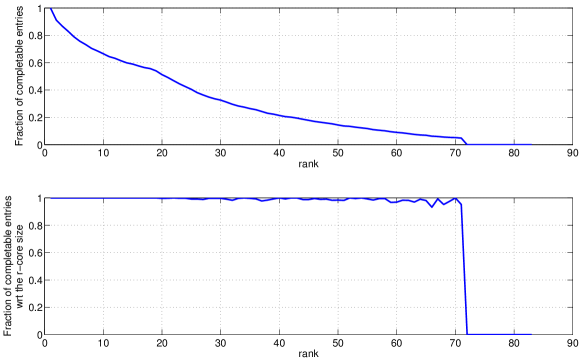

For growing rank , the -core of the MovieLens data set was computed by the algorithm which is standard in graph theory - by Theorem 44 only the missing entries in the -core can be completed, and any entry not contained in the -core is not completable by any algorithm. Figure 6 shows the size (columns, rows, entries) of the -core of the MovieLens data for growing .

Under rank , the vast majority of the entries are in -core, and so is the majority of the rows, while some columns with very few entries are removed with increasing . At rank , the number of columns in the -core attains the number of rows in the -core; above rank , the number of rows and columns in the -core diminish exponentially with the same speed. Above rank , the -core rapidly starts to shrink, with being the biggest rank with non-empty -core.

For growing rank , finitely completable closure in the MovieLens data set were identified in the following way: First, it was checked with Algorithm 1 whether the -core was -completable. If not, the completable entries in the -core were computed by an implementation of Algorithm 1. Then, the minor closure of the completed -cores was computed by Algorithm 4; by Theorem 44, it was sufficient to check for completable entries in the -core. Note that the positions of the completable entries were also computed in the process.

Figure 7 shows the number of completable entries in the MovieLens data set for growing determined in this way.

An interesting thing to note is the inflection point at rank . It corresponds to the phase transition in Figure 6 where the -core starts to shrink exponentially and simultaneously in rows and columns. At rank and above, no missing entry in the -core can be completed.

7.4. Entry-wise completion and error prediction

In the rest of the experiments, we recapitulate some results from Király and Theran (2013b) on entry-wise reconstruction and error prediction for rank one matrices.

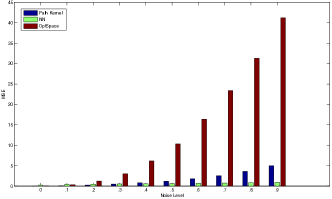

To test reconstruction, we generated random masks of size with entries sampled uniformly and a random matrix of rank one. The multiplicative noise was chosen entry-wise independent, with variance for each entry. Figure 9(a) compares the Mean Squared Error (MSE) for three algorithms: Nuclear Norm (using the implementation Tomioka et al. (2010)), OptSpace (Keshavan et al., 2010a), and Algorithm 6. It can be seen that on these masks, Algorithm 6 is competitive with the other methods and even outperforms them for low noise.

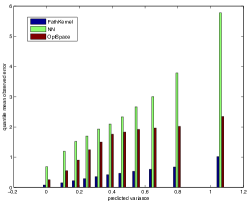

Figure 9(b) compares the error of each of the methods with the variance predicted by Algorithm 7 each time the noise level changed. The figure shows that for any of the algorithms, the mean of the actual error increases with the predicted error, showing that the error estimate is useful for a-priori prediction of the actual error - independently of the particular algorithm. Note that by construction of the data this statement holds in particular for entry-wise predictions. Furthermore, in quantitative comparison Algorithm 7 also outperforms the other two in each of the bins. The qualitative reversal between the algorithms in Figures 9(b) (a) and (b) comes from the different error measure and the conditioning on the bins.

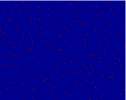

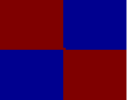

7.5. Universal error estimates

For three different masks, we calculated the predicted minimum variance for each entry of the mask. The mask sizes are all . The noise was assumed to be i.i.d. Gaussian multiplicative with for each entry. Figure 8 shows the predicted a-priori minimum variances for each of the masks. The structure of the mask affects the expected error. Known entries generally have least variance, and it is less than the initial variance of , which implies that the (independent) estimates coming from other paths can be used to successfully denoise observed data. For unknown entries, the structure of the mask is mirrored in the pattern of the predicted errors; a diffuse mask gives a similar error on each missing entry, while the more structured masks have structured error which is determined by combinatorial properties of the completion graph.

8. Discussion and outlook

In this paper we have demonstrated the usefulness and practicability of the algebraic combinatorial approach for matrix completion, by deriving reconstructability statments, and actual reconstruction algorithms for single missing entries. Our theory allows to treat the positions of the observations separately from the entries themselves. As a prominent model feature, we are able to separate the sampling scheme from algebraic and combinatorial conditions for reconstruction and explain existing reconstruction bounds by the combinatorial phase transition for the uniform random sampling scheme.

In our new setting, we are left with a number of major open questions:

-

•

Characterize all circuits and circuit polynomials in rank 2 or higher (a more extensive account on this problem can be found in Király et al. (2013)).

-

•

Give a sufficient and necessary combinatorial criterion for unique completability.

-

•

Give an efficient algorithm certifying for unique completability when given the positions of the observed entries (or, more generally, one which computes the number of solutions).

-

•

Prove the phase transition bound for the completable core (the phase transition bound for completability has been shown in Király and Theran (2013a)).

-

•

Explain the existing guarantees for whole matrix reconstruction MSE in terms of single entry expected error, for the various sampling models in literature. An explanation for rank one can be inferred from Király and Theran (2013b).

The presented results also suggest a number of future directions:

-

•

Problems such as matrix completion under further constraints such as for symmetric matrices, distance matrices or kernel matrices, are closely related to the ones we consider here, and can be treated by similar techniques. (under a phase transition aspect, these models were studied in Király and Theran (2013a); under a matroidal aspect, the theory in Király et al. (2013) yields a starting point)

- •

-

•

We have essentially shown matrix completion to be an algebraic manifold learning problem. This makes it accessible to the kernel/ideal learning techniques presented in Király et al. (2014).

-

•

The algebraic theory used to infer genericity and identifiability is largely independent of the matrix completion setting and can be applied to inverse problems and compressed sensing problems that are algebraic. In Király and Ehler (2014), this was demonstrated for phase retrieval.

Sumamrizing, we argue that recognizing and exploiting algebra and combinatorics in machine learning problems is beneficial from the practical and theoretical perspectives. When it is present, methods using underlying algebraic and combinatorial structures yield sounder statements and more practical algorithms than can be obtained when ignoring it, conversely algebra and combinatorics can profit from the various interesting structure surfacing in machine learning problems. Therefore all involved fields can only profit from a more widespread interdiscplinary collaboration with and between each other.

Acknowledgements

We thank Andriy Bondarenko, Winfried Bruns, Eyke Hüllermeyer, Mihyun Kang, Yusuke Kobayashi, Martin Kreuzer, Cris Moore, Klaus-Robert Müller, Kazuo Murota, Kiyohito Nagano, Zvi Rosen, Raman Sanyal, Bernd Sturmfels, Sumio Watanabe, Volkmar Welker, and Günter Ziegler for valuable discussions. RT is partially supported by MEXT KAKENHI 22700138, the Global COE program “The Research and Training Center for New Development in Mathematics”, FK by Mathematisches Forschungsinstitut Oberwolfach (MFO), and LT by the European Research Council under the European Union’s Seventh Framework Programme (FP7/2007-2013) / ERC grant agreement no 247029-SDModels. This research was partially carried out at MFO, supported by FK’s Oberwolfach Leibniz Fellowship.

References

- Acar et al. [2009] Evrim Acar, Daniel M. Dunlavy, and Tamara G. Kolda. Link prediction on evolving data using matrix and tensor factorizations. In Data Mining Workshops, 2009. ICDMW’09. IEEE International Conference on, pages 262–269. IEEE, 2009.

- Allman et al. [2009] Elizabeth S. Allman, Catherine Matias, and John A. Rhodes. Identifiability of parameters in latent structure models with many observed variables. Ann. Statist., 37(6A):3099–3132, 2009.

- Argyriou et al. [2008] Andreas Argyriou, Craig A. Micchelli, Massimiliano Pontil, and Yi Ying. A spectral regularization framework for multi-task structure learning. In J.C. Platt, D. Koller, Y. Singer, and S. Roweis, editors, Advances in NIPS 20, pages 25–32. MIT Press, Cambridge, MA, 2008.

- Bamber [1985] Donald Bamber. How many parameters can a model have and still be testable? Journal of Mathematical Psychology, 29(4):443 – 473, 1985.

- Blythe et al. [2014] Duncan Blythe, Franz J. Király, and Louis Theran. Algebraic combinatorial methods for low-rank matrix completion with application to athletic performance prediction. arXiv Preprint, 2014. arXiv 1406.2864.

- Bollobás [2001] Béla Bollobás. Random graphs, volume 73 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, second edition, 2001. ISBN 0-521-80920-7; 0-521-79722-5. doi: 10.1017/CBO9780511814068. URL http://dx.doi.org/10.1017/CBO9780511814068.

- Bruns and Vetter [1988] Winfried Bruns and Udo Vetter. Determinantal Rings. Springer-Verlag New York, Inc., 1988.

- Candès and Recht [2009] Emmanuel J. Candès and Benjamin Recht. Exact matrix completion via convex optimization. Found. Comput. Math., 9(6):717–772, 2009. ISSN 1615-3375.

- Candès and Tao [2010] Emmanuel J. Candès and Terence Tao. The power of convex relaxation: near-optimal matrix completion. IEEE Trans. Inform. Theory, 56(5):2053–2080, 2010. ISSN 0018-9448. doi: 10.1109/TIT.2010.2044061. URL http://dx.doi.org/10.1109/TIT.2010.2044061.

- Chaterjee [2012] Sourav Chaterjee. Matrix estimation by Universal Singular Value Thresholding. Preprint, arXiv:1212.1247, 2012. URL http://arxiv.org/abs/1212.1247.

- Dress and Lovász [1987] A. Dress and L. Lovász. On some combinatorial properties of algebraic matroids. Combinatorica, 7(1):39–48, 1987.

- Foygel and Srebro [2011] Rina Foygel and Nathan Srebro. Concentration-based guarantees for low-rank matrix reconstruction. Arxiv preprint arXiv:1102.3923, 2011.

- Goldberg et al. [2010] Andrew Goldberg, Xiaojin Zhu, Benjamin Recht, Jun-Ming Xu, and Robert Nowak. Transduction with matrix completion: Three birds with one stone. In J. Lafferty, C. K. I. Williams, J. Shawe-Taylor, R.S. Zemel, and A. Culotta, editors, Advances in Neural Information Processing Systems 23, pages 757–765. 2010.

- Grothendieck and Dieudonné [1965] Alexander Grothendieck and Jean Dieudonné. Éléments de géométrie algébrique iv, deuxième partie. Publ. Math. IHES, 24, 1965.

- Grothendieck and Dieudonné [1966] Alexander Grothendieck and Jean Dieudonné. Éléments de géométrie algébrique iv, troisième partie. Publ. Math. IHES, 28, 1966.

- [16] GroupLens. Movielens 100k data set. Available online at http://grouplens.org/datasets/movielens/; as downloaded on November 27th 2012.

- Hsu et al. [2012] Daniel Hsu, Sham Kakade, and Percy Liang. Identifiability and unmixing of latent parse trees. In P. Bartlett, F.C.N. Pereira, C.J.C. Burges, L. Bottou, and K.Q. Weinberger, editors, Advances in Neural Information Processing Systems 25, pages 1520–1528. 2012.

- Jackson et al. [2007] Bill Jackson, Brigitte Servatius, and Herman Servatius. The 2-dimensional rigidity of certain families of graphs. J. Graph Theory, 54(2):154–166, 2007. ISSN 0364-9024.

- Janson and Luczak [2007] Svante Janson and Malwina J. Luczak. A simple solution to the -core problem. Random Structures Algorithms, 30(1-2):50–62, 2007. ISSN 1042-9832. doi: 10.1002/rsa.20147. URL http://dx.doi.org/10.1002/rsa.20147.

- Kasiviswanathan et al. [2011] Shiva Prasad Kasiviswanathan, Cristopher Moore, and Louis Theran. The rigidity transition in random graphs. In Proceedings of the Twenty-Second Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1237–1252, Philadelphia, PA, 2011. SIAM.

- Keshavan et al. [2010a] Raghunandan H. Keshavan, Andrea Montanari, and Sewoong Oh. Matrix completion from a few entries. IEEE Trans. Inform. Theory, 56(6):2980–2998, 2010a. ISSN 0018-9448. doi: 10.1109/TIT.2010.2046205. URL http://dx.doi.org/10.1109/TIT.2010.2046205.

- Keshavan et al. [2010b] R.H. Keshavan, A. Montanari, and S. Oh. Matrix completion from a few entries. Information Theory, IEEE Transactions on, 56(6):2980–2998, 2010b.

- Király and Ehler [2014] Franz J. Király and Martin Ehler. The algebraic approach to phase retrieval and explicit inversion at the identifiability threshold. arXiv e-prints, February 2014. arXiv:1402.4053.

- Király and Theran [2013a] Franz J. Király and Louis Theran. Coherence and sufficient sampling densities for reconstruction in compressed sensing. arXiv Preprint, 2013a. arXiv 1302.2767.

- Király and Theran [2013b] Franz J. Király and Louis Theran. Obtaining error-minimizing estimates and universal entry-wise error bounds for low-rank matrix completion. arXiv Preprint, 2013b. arXiv 1302.5337.

- Király et al. [2013] Franz J. Király, Louis Theran, Ryota Tomioka, and Takeaki UNo. The algebraic combinatorial approach for low-rank matrix completion. arXiv Preprint, 2013. arXiv 1211.4116v3.

- Király et al. [2014] Franz J. Király, Martin Kreuzer, and Louis Theran. Dual-to-kernel learning with ideals. arXiv e-prints, February 2014. arXiv:1402.0099.

- Király et al. [2013] Franz J. Király, Zvi Rosen, and Louis Theran. Algebraic matroids with graph symmetry. arXiv Preprint, 2013. arXiv 1312.3777.

- Kurdyka et al. [2000] K. Kurdyka, P. Orro, and S. Simon. Semialgebraic Sard theorem for generalized critical values. J. Differential Geom., 56(1):67–92, 2000.

- Meka et al. [2009] Raghu Meka, Prateek Jain, and Inderjit S. Dhillon. Guaranteed rank minimization via singular value projection, 2009. Eprint arXiv:0909.5457.

- Menon and Elkan [2011] Aditya K. Menon and Charles Elkan. Link prediction via matrix factorization. Machine Learning and Knowledge Discovery in Databases, pages 437–452, 2011.

- Milnor [1968] John Milnor. Singular points of complex hypersurfaces. Annals of Mathematics Studies, No. 61. Princeton University Press, Princeton, N.J., 1968.