Calibrated Elastic Regularization in Matrix Completion

Tingni Sun

Statistics Department, The Wharton School

University of Pennsylvania

Philadelphia, Pennsylvania 19104

tingni@wharton.upenn.edu &Cun-Hui Zhang

Department of Statistics and Biostatistics

Rutgers University

Piscataway, New Jersey 08854

czhang@stat.rutgers.edu

Abstract

This paper concerns the problem of matrix completion, which is to estimate a matrix from observations in a small subset of indices. We propose a calibrated spectrum elastic net method with a sum of the nuclear and Frobenius penalties and develop an iterative algorithm to solve the convex minimization problem. The iterative algorithm alternates between imputing the missing entries in the incomplete matrix by the current guess and estimating the matrix by a scaled soft-thresholding singular value decomposition of the imputed matrix until the resulting matrix converges. A calibration step follows to correct the bias caused by the Frobenius penalty. Under proper coherence conditions and for suitable penalties levels,

we prove that the proposed estimator achieves an error bound of nearly optimal order and in proportion to the noise level.

This provides a unified analysis of the noisy and noiseless matrix completion problems.

Simulation results are presented to compare our proposal with previous ones.

1 Introduction

Let be a matrix of interest and .

Suppose we observe vectors ,

(1)

where and are random errors. We are interested in estimating when

is a small fraction of .

A well-known application of matrix completion is the Netflix problem where is the rating of movie by user for [1]. In such applications, the proportion of the observed entries is typically very small, so that the estimation or recovery of is impossible without a structure assumption on . In this paper, we assume that is of low rank.

A focus of recent studies of matrix completion has been on a simpler formulation, also known as exact recovery, where the observations are assumed to be uncorrupted, i.e. . A direct approach is to minimize subject to .

An iterative algorithm was proposed in [5] to project a trimmed SVD of the

incomplete data matrix to the space of matrices of a fixed rank .

The nuclear norm was proposed as a surrogate for the rank, leading to the following convex

minimization problem in a linear space [2]:

We denote the nuclear norm by here and throughout this paper.

This procedure, analyzed in [2, 3, 4, 11] among others,

is parallel to the replacement of the penalty by the penalty in solving

the sparse recovery problem in a linear space.

In this paper, we focus on the problem of matrix completion with noisy observations (1) and take

the exact recovery as a special case. Since the exact constraint is no longer appropriate in the

presence of noise, penalized squared error is considered.

By reformulating the problem in Lagrange form, [8] proposed the spectrum Lasso

(2)

along with an iterative convex minimization algorithm.

However, (2) is difficult to analyze when the sample fraction is small,

due to the ill-posedness of the quadratic term .

This has led to two alternatives in [7] and [9].

While [9] proposed to minimize (2) under an additional constraint on ,

[7] modified (2) by replacing the quadratic term with

.

Both [7, 9] provided nearly optimal error bounds when the noise level is of no smaller order

than the norm of the target matrix , but not of smaller order,

especially not for exact recovery.

In a different approach, [6] proposed a non-convex recursive algorithm and

provided error bounds in proportion to the noise level. However, the procedure requires the

knowledge of the rank of the unknown and the error bound is optimal only

when and are of the same order.

Our goal is to develop an algorithm for matrix completion that can be as easily computed as the spectrum Lasso

(2) and enjoys a nearly optimal error bound proportional to the noise level to continuously cover

both the noisy and noiseless cases.

We propose to use an elastic penalty, a linear combination of the nuclear and Frobenius norms, which leads to the estimator

(3)

where and are the nuclear and Frobenius norms, respectively.

We call (3) spectrum elastic net (E-net) since it is parallel to the E-net in linear regression,

the least squares estimator with a sum of the and penalties, introduced in [15].

Here the nuclear penalty provides the sparsity in the spectrum, while the Frobenius penalty regularizes

the inversion of the quadratic term.

Meanwhile, since the Frobenius penalty roughly shrinks the estimator by a factor ,

we correct this bias by a calibration step,

(4)

We call this estimator calibrated spectrum E-net.

Motivated by [8], we develop an EM algorithm to solve (3) for matrix completion.

The algorithm iteratively replaces the missing entries with those obtained from a scaled soft-thresholding singular value decomposition (SVD) until the resulting matrix converges. This EM algorithm is guaranteed to converge to

the solution of (3).

Under proper coherence conditions, we prove that for suitable penalty levels and ,

the calibrated spectrum E-net (4) achieves a desired error bound in the Frobenius norm.

Our error bound is of nearly optimal order and in proportion to the noise level.

This provides a sharper result than those of [7, 9] when the

noise level is of smaller order than the norm of , and than that of

[6] when is large. Our simulation results support the use of the calibrated spectrum E-net.

They illustrate that (4) performs comparably to (2) and outperforms

the modified method of [7].

Our analysis of the calibrated spectrum E-net uses an inequality similar to a duel certificate bound in [3].

The bound in [3] requires sample size ,

where . We use the method of moments to remove a factor in the first component of

their sample size requirement. This leads to a sample size requirement of , with an extra

in comparison to the ideal . Since the extra does not appear in our error bound,

its appearance in the sample size requirement seems to be a technicality.

The rest of the paper is organized as follows.

In Section 2, we describe an iterative algorithm for the computation of the spectrum E-net

and study its convergence.

In Section 3, we derive error bounds for the calibrated spectrum E-net. Some simulation results are presented in Section 4. Section 5 provides the proof of our main result.

We use the following notation throughout this paper.

For matrices , is the nuclear norm (the sum of all singular values of ), is the spectrum norm (the largest singular value), is the Frobenius norm

(the norm of vectorized ),

and . Linear mappings from to are denoted by the calligraphic letters. For a linear mapping , the operator norm is .

We equip with the inner product so that .

For projections , with being the identity.

We denote by the unit matrix with 1 at ,

and by the projection to : .

2 An algorithm for spectrum elastic regularization

We first present a lemma for the M-step of our iterative algorithm.

Lemma 1

Suppose the matrix has rank . The solution to the optimization problem

is given by with , where is the SVD of , and .

The minimization problem in Lemma 1 is solved by a scaled soft-thresholding SVD.

This is parallel to Lemma 1 in [8] and justified by Remark 1 there. We use Lemma 1

to solve the M-step of the EM algorithm for the spectrum E-net (3).

We still need an E-step to impute a complete matrix given the observed data .

Since are allowed to have ties, we need the following notation.

Let be the multiplicity of observations at

and be the maximum multiplicity. Suppose that the complete data is

composed of observations at each for a certain integer . Let

be the sample mean of the complete data at and be the matrix with

components . If the complete data are available, (3) is equivalent to

Let be the sample mean of

the observations at and .

In the white noise model, the conditional expectation of given is

for .

This leads to a generalized E-step:

(5)

where is the estimation of in the previous iteration. This is a genuine E-step when

but also allows a smaller to reduce the proportion of missing data.

We now present the EM-algorithm for the computation of the spectrum E-net in

(3).

The following theorem states the convergence of Algorithm 1.

Theorem 1

As , converges to a limit as a

function of the data and , and for .

Theorem 1 is a variation of a parallel result in [8] and follows from the same

proof there. As [8] pointed out, a main advantage of Algorithm 1 is the speed of each iteration.

When the maximum multiplicity is small, we simply use and ;

Otherwise, we may first run the EM-algorithm for an and use the output as the initialization

for a second run of the EM-algorithm with .

3 Analysis of estimation accuracy

In this section, we derive error bounds for the calibrated spectrum E-net.

We need the following notation. Let , be the SVD of , and

be the nonzero singular values of .

Let be the tangent space with respect to , the space of all matrices of the form

. The orthogonal projection to is given by

The proof of Theorem 2 is provided in Section 5.

When are random entries in , , so that

(8) and the first inequality of

(7) are expected to hold under proper conditions.

Since the rank of is no greater than ,

(9) essentially requires .

Our analysis allows to lie in a certain range , and

is large under proper conditions.

Still, the choice of is constrained by (7) and (8)

since is linear in .

When diverges to infinity, the calibrated spectrum E-net (4) becomes the modified

spectrum Lasso of [7].

Theorem 2 provides sufficient conditions on the target matrix and the noise for achieving a certain level

of estimation error. Intuitively, these conditions on the target matrix must imply a certain level of coherence

(or flatness) of the unknown matrix since it is impossible to distinguish the unknown from zero when the observations

are completely outside its support.

In [2, 3, 4, 11], coherence conditions are imposed on

(11)

where and are matrices of singular vectors of .

[9] considered a more general notation of spikiness of a matrix , defined as the ratio between

the and dimension-normalized norms,

(12)

Suppose in the rest of the section that are iid points uniformly distributed in

and are iid variables independent of .

The following theorem asserts that under certain coherence conditions on the matrices ,

, and , all conditions of Theorem 2 hold with large probability

when the sample size is of the order .

Theorem 3

Let . Consider and satisfying

(13)

Then, there exists a constant such that

(14)

implies

with probability at least , where and are the coherence constants in (11), is the spikiness of and .

We require the knowledge of noise level to determine the penalty level that is usually

considered as tuning parameter in practice.

The Frobenius norm in (13) can be replaced by

an estimate of the same magnitude in Theorem 3. In our simulation experiment, we use

with .

The Chebyshev inequality provides when and

.

A key element in our analysis is to find a probabilistic bound for the second inequality of (8),

or equivalently an upper bound for

(15)

This guarantees the existence of a primal dual certificate for the spectrum E-net penalty [14].

For , a similar inequality was proved in [3],

where the sample size requirement is

for a certain coherence factor .

We remove a log factor in the first bound, resulting in the sample size requirement in (14),

which is optimal when .

For exact recovery in the noiseless case, the sample size is sufficient if a golfing scheme is used to construct an approximate

dual certificate [4, 11].

We use the following lemma to bound (15).

Lemma 2

Let where are iid points uniformly distributed in .

Let and . Let be a deterministic matrix.

Then, there exists a numerical constant such that, for all and ,

(16)

We use a different graphical approach than those in [3] to bound

in the proof of Lemma 2.

The rest of the proof of Theorem 3 can be outlined as follows.

Assume that all coherence factors are .

Let and write

.

By (16) with for and an even simpler bound for and Rem,

(15) holds when , where .

Since , this is equivalent to .

Finally, we use matrix exponential inequalities [10, 12] to verify other conditions of

Theorem 2.

We omit technical details of the proof of Lemma 2 and

Theorem 3. We would like to point out that if the in (16) can be replaced by

, e.g. in view of [3], the rest of the proof of

Theorem 3 is intact with and a proper adjustment of

in (13).

Compared with [7] and [9], the main advantage of Theorem 3 is the

proportionality of its error bound to the noise level.

In [7], the quadratic term in (2) is replaced by its expectation and the resulting minimizer is proved to satisfy

(17)

with large probability, where is a numerical constant.

This error bound achieves the squared error rate as in Theorem 3

when the noise level is of no smaller order than , but not of smaller order.

In particular, (17) does not imply exact recovery when .

In Theorem 3, the error bound converges to zero as the noise level diminishes,

implying exact recovery in the noiseless case.

In [9], a constrained spectrum Lasso was proposed

that minimizes (2) subject to .

For and , [9] proved

(18)

with large probability. Scale change from the above error bound yields

Since and , the right-hand side

of (18) is of no smaller order than that of (17). We shall point out that (17) and (18) only

require sample size . In addition, [9] allows more practical weighted sampling models.

Compared with [6], the main advantage of Theorem 3 is the independence

of its sample size requirement on the aspect ratio , where is assumed without

loss of generality by symmetry. The error bound in [6] implies

(19)

for sample size ,

where are constants depending on the same set of coherence factors as in

(14) and are the singular values of .

Therefore, Theorem 3 effectively replaces the root aspect ratio in

the sample size requirement of (19) with a log factor, and removes the coherence factor

on the right-hand side of (19).

We note that is a larger coherence

factor than in the sample size requirement in Theorem 3.

The root aspect ratio can be removed from the sample size requirement for (19)

if can be divided into square blocks uniformly satisfying the coherence conditions.

4 Simulation study

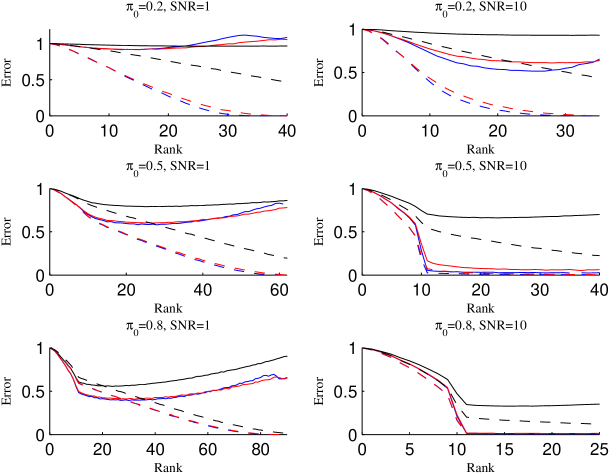

This experiment has the same setting as in Section 9 of [8].

We provide the description of the simulation settings in our notation as follows:

The target matrix is , where and are random matrices

with independent standard normal entries.

The sampling points have no tie and is a uniformly

distributed random subset of , where is fixed.

The errors are iid variables.

Thus, the observed matrix is with

being a projection.

The signal to noise ratio (SNR) is defined as .

Figure 1: Plots of training and testing errors against the estimated rank: testing error with solid lines; training

error with dashed lines; spectrum Lasso in blue, calibrated spectrum E-net in red; modified spectrum Lasso in black;

, .

We compare the calibrated spectrum E-net (4) with the spectrum Lasso (2)

and its modification of [7].

For all methods, we compute a series of estimators with 100 different penalty levels, where the smallest penalty level corresponds to a full-rank solution and the largest penalty level corresponds to a zero solution. For the calibrated spectrum E-net, we always use , where is an estimator for .

We plot the training errors and test errors as functions of estimated ranks, where the training and test errors are defined as

In Figure 1, we report the estimation performance of three methods. The rank of is 10 but

are regenerated in each replication.

Different noise levels and proportions of the observed entries are considered.

All the results are averaged over 50 replications.

In this experiment, the calibrated spectrum E-net and the spectrum Lasso estimator have very close testing

and training errors, and both of them significantly outperform the modified Lasso.

Figure 1 also illustrates that in most cases, the calibrated spectrum E-net and spectrum Lasso achieve

the optimal test error when the estimated rank is around the true rank.

We note that the constrained spectrum Lasso

estimator would have the same performance as the spectrum Lasso

when the constraint

is set with a sufficiently high . However, analytic properties of

the spectrum Lasso is unclear without constraint or modification.

The proof of Theorem 2 requires the following proposition that controls the approximation error

of the Taylor expansion of the nuclear norm with subdifferentiation.

The result, closely related to those in [13], is used to control the variation of the tangent space

of the spectrum E-net estimator. We omit its proof.

The last inequality above follows from the first inequalities in (7), (8) and (9).

It remains to bound . Let . We write the spectrum E-net

estimator (3) as

It follows that for a certain member in the sub-differential of at ,

Let .

Since , we have

(23)

(24)

(25)

(26)

The second inequality in (23) is due to and .

The last equality in (23) follows from the definition of , since it gives

.

By the definitions of , and ,

.

Since

and , we find

It follows from (30), (31) and the first inequalities of

(8) and (9) that

Thus, due to ,

(32)

Therefore, the error bound (10) follows from (20) and (32).

Acknowledgments

This research is partially supported by the NSF Grants DMS 0906420, DMS-11-06753

and DMS-12-09014,

and NSA Grant H98230-11-1-0205.

References

[1]

ACM SIGKDD and Netflix.

Proceedings of KDD Cup and workshop.

2007.

[2]

E. Candes and B. Recht.

Exact matrix completion via convex optimization.

Found. Comput. Math., 9:717–772, 2009.

[3]

E. J. Candès and T. Tao.

The power of convex relaxation: Near-optimal matrix completion.

IEEE Trans. Inform. Theory, 56(5):2053–2080, 2009.

[4]

D. Gross.

Recovering low-rank matrices from few coefficients in any basis.

CoRR, abs/0910.1879, 2009.

[5]

R. H. Keshavan, A. Montanari, and S. Oh.

Matrix completion from a few entries.

IEEE Transactions on Information Theory, 56(6):2980–2998,

2010.

[6]

R. H. Keshavan, A. Montanari, and S. Oh.

Matrix completion from noisy entries.

Journal of Machine Learning Research, 11:2057–2078, 2010.

[7]

V. Koltchinskii, K. Lounici, and A. B. Tsybakov.

Nuclear-norm penalization and optimal rates for noisy low-rank matrix

completion.

The Annals of Statistics, 39:2302–2329, 2011.

[8]

R. Mazumder, T. Hastie, and R. Tibshirani.

Spectral regularization algorithms for learning large incomplete

matrices.

Journal of Machine Learning Research, 11:2287–2322, 2010.

[9]

S. Negahban and M. J. Wainwright.

Restricted strong convexity and weighted matrix completion: Optimal

bounds with noise.

2010.

[10]

R. I. Oliveira.

Concentration of the adjacency matrix and of the laplacian in random

graphs with independent edges.

Technical Report arXiv:0911.0600, arXiv, 2010.

[11]

B. Recht.

A simpler approach to matrix completion.

Journal of Machine Learning Research, 12:3413–3430, 2011.

[12]

J. A. Tropp.

User-friendly tail bounds for sums of random matrices.

Found. Comput. Math. doi:10.1007/s10208-011-9099-z., 2011.

[13]

P.-A. Wedin.

Perturbation bounds in connection with singular value decomposition.

BIT, 12:99–111, 1972.

[14]

C.-H. Zhang and T. Zhang.

A general framework of dual certificate analysis for structured

sparse recovery problems.

Technical report, arXiv: 1201.3302v1, 2012.

[15]

H. Zou and T. Hastie.

Regularization and variable selection via the elastic net.

J. R. Statist. Soc. B, 67:301–320, 2005.