11institutetext: Radoslav Valkov 22institutetext: Faculty of Mathematics and Informatics, University of Sofia,

1000 Sofia, Bulgaria,

22email: rvalkov@fmi.uni-sofia.bg

Fitted Finite Volume Method for a Generalized Black-Scholes Equation Transformed on Finite Interval

Radoslav Valkov

(Received: date / Accepted: date)

Abstract

A generalized Black-Scholes equation is considered on the semi-axis. It is transformed on the interval in order to make the computational domain finite. The new parabolic operator degenerates at the both ends of the interval and we are forced to use the Gärding inequality rather than the classical coercivity. A fitted finite volume element space approximation is constructed. It is proved that the time -weighted full discretization is uniquely solvable and positivity-preserving. Numerical experiments, performed to illustrate the usefulness of the method, are presented.

The famous equation, proposed by F. Black, M. Scholes and R. Merton, see Duffy ; Sevc ; WHD , is

This is a typical example of a degenerate parabolic equation OR . It is well known Sevc ; WHD ; Zhu that it can be transformed to the heat equation that allows us to overcome the degeneracy at . Many numerical methods, based on classical finite difference schemes, applied to constant coefficients heat equations, are developed AP ; RS . However, when the problem has space-dependant coefficients and one can not transform the Black-Scholes equation to a standard heat equation. Finite difference and finite element methods have been applied in A ; CL1 ; CL2 ; CS ; CV ; Ehrhardt1 ; Ehrhardt2 ; Sulli ; Vasq ; Zhu in order to solve this type of generalized Black-Scholes equations. In Kadalbajoo cubic -splines are implemented. Often, the convergence of the full discretization is verified by numerical examples only.

An effective method, that resolves the degeneracy, is proposed by S. Wang SW for the Black-Scholes equation with Dirichlet boundary conditions. The method is based on a finite volume formulation of the problem, coupled with a fitted local approximation to the solution and an implicit time-stepping technique. The local approximation is determined by a set of two-point boundary value problems (BVPs), defined on the element edges. This fitted technique originates from one-dimensional computational fluid dynamics Morton .

A modification of the discretization, originally presented in SW , was proposed by L. Angermann A such that the method adequately treats the proper (natural) boundary condition at . Similar space discretization is derived in CV for a degenerate parabolic equation in the zero-coupon bond pricing.

The domain of is the half real line. For numerical computation it is desirable to have a finite computational domain. The transformation in the next section converts to , decreasing significantly the computational costs. Also, for a call option, the solution is not bounded and from the numerical methods’ point of view the problem transformation on a finite interval is better. The resulting equation has variable coefficients but this is not an essential difficulty for the numerical computation. However, the transformed equation degenerates at both ends of the finite interval.

The present paper deals with a degenerate parabolic equation, (5), derived after transformation of the generalized Black-Scholes equation (1) to a finite interval. The degeneration at the both ends of the interval does not allow the use of the Poincaré-Friedrichs inequality and we are forced to investigate the differential problem with the Gärding inequality rather than classical coercivity GV .

This paper is organized as follows. The model problem is presented in Section 2, where we discuss our basic assumptions and some properties of the solution. The space discretization method is developed in Section 3. Section 4 is devoted to the time discretization, where we show that the system matrix on each time-level is an -matrix so that the discretization is monotone. Numerical experiments are discussed in the last section.

Some results, concerning the case of the transformed Black-Scholes equation above, are reported in RV .

2 The transformed problem

We consider the generalized Black-Scholes equation Sevc ; WHD :

(1)

where denotes the volatility of the asset, is the risk-free interest rate, denotes the dividend of the dividend-paying asset. We also introduce such that , where the dividend rate is continuously differentiable with respect to .

There are various choices for the final (payoff) condition, depending on the models. In the case of vanilla European option

(2)

where is the strike price. Another example is the bullish vertical spread payoff, defined by

(3)

where and are two exercise prices, satisfying . This represents a portfolio of buying one call option with exercise price and issuing one call option with the same expiry date but a larger exercise price . For detailed discussion on this, we refer to WHD .

The constant is called mesh parameter. It controls the distribution of the mesh nodes w.r.t. on the interval . The higher the value of S, that we are interested in, the higher value of should be in order to obtain a reasonable accuracy. In the case of a call option, because of the nature of the terminal condition, should be equal to .

The inverse transformation is and after plugging it in the Black-Scholes equation, (1), we obtain:

(5)

We return to the original notation of the variable for the sake of simplicity. The initial data for a call option reads

(6)

Being different from the classical parabolic equations, in which the principle coefficient is assumed to be strictly positive, the parabolic equation (5) belongs to the second-order differential equations with non-negative characteristic form OR . The main difficulty of such kind of equations is the degeneracyWFV . It can be easily seen that at and (5) degenerates to

(7)

It is well known by the Fichera theory for degenerate parabolic equations OR that at the degenerate boundaries and the boundary conditions should not be given.

For theoretical analysis of our discrete problem as well as for the construction of a fitted finite volume mass-lumping discretization we need to consider weak solutions of (5). We shall use the standard notations for the function spaces and of which a function and it’s derivatives up to order are continuous on (respectively ). The space of square-integrable functions we denote by with the usual -norm and the inner product . We also use the function space with the norm . To handle the degeneracy in (5), we introduce the following weighted -norm

with corresponding inner product . Using and , we define the weighted Sobolev space

, where denotes the weak derivative of . Let be the functional on , defined by . Then it is easy to see that

is a norm on ; it is called weighted -norm on . Furthermore, using the inner products in

and , we define a weighted inner product on by

and, consequently, the pair is a Hilbert space. Also, contains the conventional Sobolev space as a proper subspace.

Here the notation is used and the function is the weighted flux density, associated with .

We are in position to state the variational formulation of problem (5),(6):

Find , such that for all

(9)

The following result provides the weak coercivity and continuity of the bilinear form .

Lemma 1

Let . Then:

1.

there exist constants and such that

for any ;

2.

(Gärding inequality) there exist constants and such that

In this section we describe the finite volume approximation of (8).

Let the interval be subdivided into intervals with . For each we set and . We also denote

for , , and for .

Finally, we define for .

Integrating (8) over the control volumes we obtain balance equations

Multiplying the i-th equation with an arbitrary number and summing up the results we get

(10)

For an arbitrary function we define the mass-lumping operator by

.

Therefore, using the operator , equation (10) can be written as follows:

The spatial discretization starts from this equation. Applying the mid-point quadrature rule to all terms except the second one we obtain for all

Clearly, we now need to derive approximations of the continuous weighted flux density , defined above, at the midpoints of the intervals for .

Case 1 Approximation of at for .

Let us consider the following two-point boundary value problem for

where .

Following considerations, similar to those in CV ; RV , we obtain

(11)

where and provides an approximation to at .

Case 2 Approximation of at .

Now we write the flux in the form

Note that the analysis in Case 1 can not be applied here because the flux degenerates at . To solve this difficulty, following A ; CV ; RV ; SW , we

will reconsider the flux ODE with an extra degree of freedom in the following form

where is an unknown constant to be determined. We obtain

(12)

Case 3 Approximation of at .

We write the flux in the form

The situation is symmetric to Case 2. We can not apply the arguments in Case 1 to the approximation of the weighted flux density on because equation (5) degenerates at . However the considerations, given in Case 2, should be modified in order to formulate an appropriate two-point BVP. Again, we consider the flux ODE with an extra degree of freedom in the following form (recall )

(13)

(14)

where is an unknown constant to be determined. Integration of (13) yields the first-order linear equation

(15)

where denotes an additive constant. Afterwards we multiply (15) by

Letting and making use of (14) we arrive at and finally

(17)

where is a free parameter. Therefore

Case 3.2 .

Now we solve the following ODE

Integrating over , we obtain

Letting one gets

Since we can conclude that this is the result of the limiting process , performed on (17). The flux in both cases 3.1 and 3.2 can be written in the form

and these are exactly the same results as in Case 3.3. Finally, a reasonable choice of the free parameter is 0 and

(18)

Let us introduce the finite element space by specifying it’s basis . Following CV ; RV we introduce the functions

On the intervals and we define the linear functions

Next we define the linear functions and on the intervals and

Then, for any , we have the representation , where . Associated with , we introduce the natural interpolation operator by

Furthermore, using the flux approximations (11),(12),(18), obtained in Cases 1, 2 and 3 respectively, we define by an approximation to

. Coming back to (9), this motivates the following semi-discretization of (8) in the space :

As usual, from (9) an equivalent ODEs system is obtained by setting successfully :

The complete set of equations forms an system of linear ODEs w.r.t. :

where

4 Full discretization

Let be a subdivision of the time interval with the step sizes . The fully discrete method with parameter for (8) reads as follows:

Find a sequence such that for

where and is an approximation to . By representing the elements in terms of the basis of and choosing we get the algebraic form

(23)

The initial condition is obtained from the representation of by means of the basis of .

We will show, Theorem 4.1, that the system matrix can be reduced to an -matrix by excluding the first two and the last two equations in (23). Therefore, the above problem (23) is uniquely solvable and our method preserves the positivity, Theorem 2.2 (maximum principle), of the numerical solution in time. Let us introduce the notations

and write down the elements of the system matrix:

for if then

and if then

for if then

and if then

for

for if

and if then

for if then

and if then

Theorem 4.1

For any given , if is sufficiently small, the system matrix of (23), , is an -matrix.

Let us first investigate the off-diagonal entries of the system matrix and . From the formulas for from the above we have , That is because

for each and each . We have used that has just the sign of

and this is also true for . Now it is clear that and are negative.

We should also note that is always positive since is small. The situation is different for , , , ,

and , , , , . From the first three equations we find

It is easily to see that when and then

for small . Therefore and .

In a similar way one can eliminate and . As a result we obtain a system of linear algebraic equations with unknowns

and coefficients matrix that is an -matrix.

While are non-negative, we have to prove that and are also non-negative. From the formula for it follows that when is small is non-negative since and are of the same order with respect to . is handled by the same way as and also considered non-negative.

Since the load vector is non-negative and the corresponding matrix is an M-matrix we can conclude that are non-negative. Finally, using the formulas for one can easily check that they are non-negative too if is small.

Remark 1

Theorem 4.1 shows that the fully-discretized system (23) satisfies the discrete maximum principle and therefore the above discretization is monotone. This guarantees the following: for a non-negative initial function the numerical solution , obtained via this method, is also non-negative as expected, because the price of the option is a non-negative number.

5 Numerical experiments

Numerical experiments, presented in this section, illustrate the properties of the constructed method. We solve numerically various European Test Problems (TP) with different final (initial) conditions and different choices of parameters.

1.

(). Call option with final condition (2). Parameters: , , , , and .

2.

(). Call option with cash-or-nothing payoff , where denotes the Heaviside function.

Parameters: , , , , and .

3.

(). Call option with final condition (2). Parameters: , , , , and .

4.

(). A portfolio of options. Combinations of different options have step final conditions such as the ’bullish vertical spread’ payoff, defined in (3). In this example, we assume that the final condition is a ’butterfly spread’ delta function, defined by

which arises from a portfolio of three types of options with different exercise prices WHD . Parameters: , , , , , , , and .

In the tables below are presented the computed and mesh norms of the error by the formulas

The rate of convergence (RC) is calculated using double mesh principle

where is the mesh -norm or -norm, and are respectively the exact solution and the numerical solution, computed at the mesh with subintervals. We choose the weight parameter with respect to the time variable .

In Table 1 we show the convergence and the accuracy of the constructed scheme, where we numerically solve the model problem with the known exact solution and initial data . We select this function because it’s feature is similar to that of the exact solution to the call option problem. The results, corresponding to problems and with , are listed in Table 1.

Table 1:

80

3.455e-3

-

2.801e-4

-

4.805e-3

-

3.914e-4

-

160

1.729e-3

0.998

9.914e-5

1.498

2.405e-3

0.998

1.385e-4

1.498

320

8.650e-4

0.999

3.507e-5

1.499

1.203e-3

0.999

4.900e-5

1.499

640

4.326e-4

0.999

1.240e-5

1.499

6.015e-4

0.999

1.733e-5

1.499

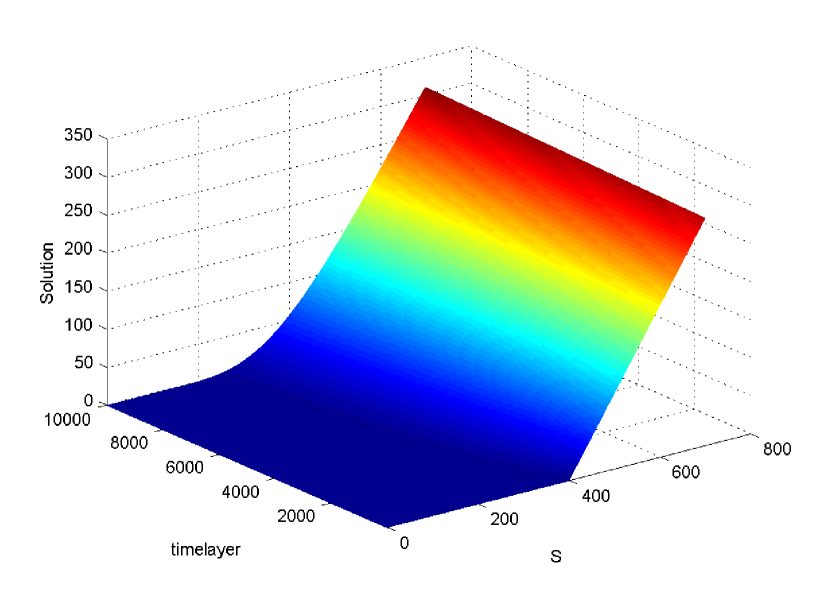

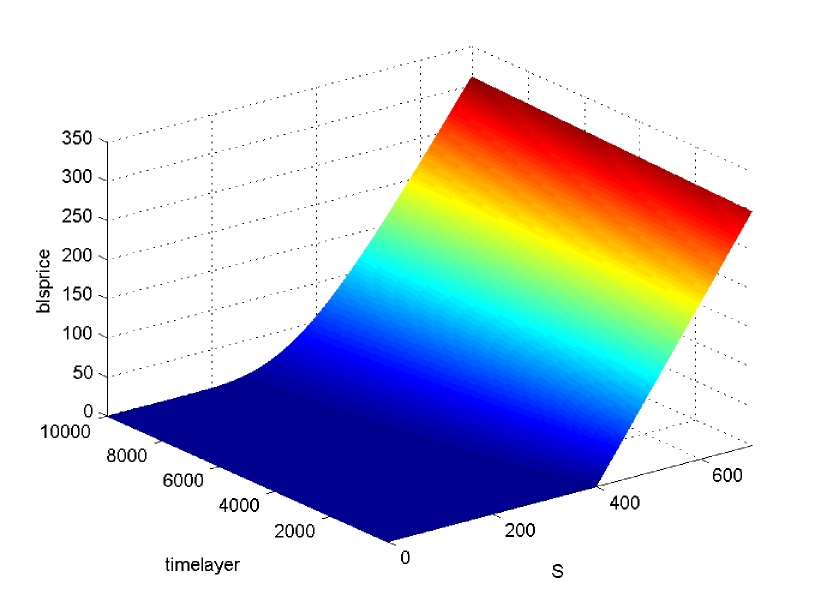

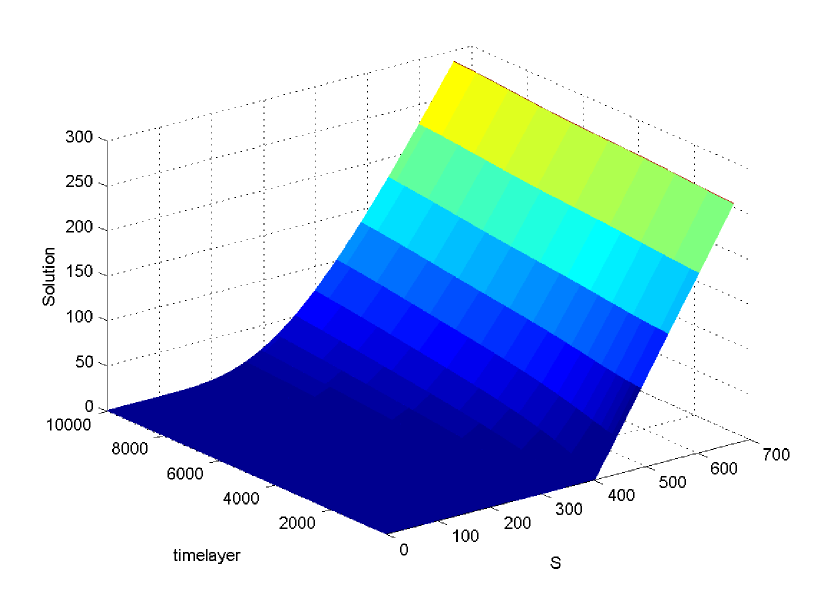

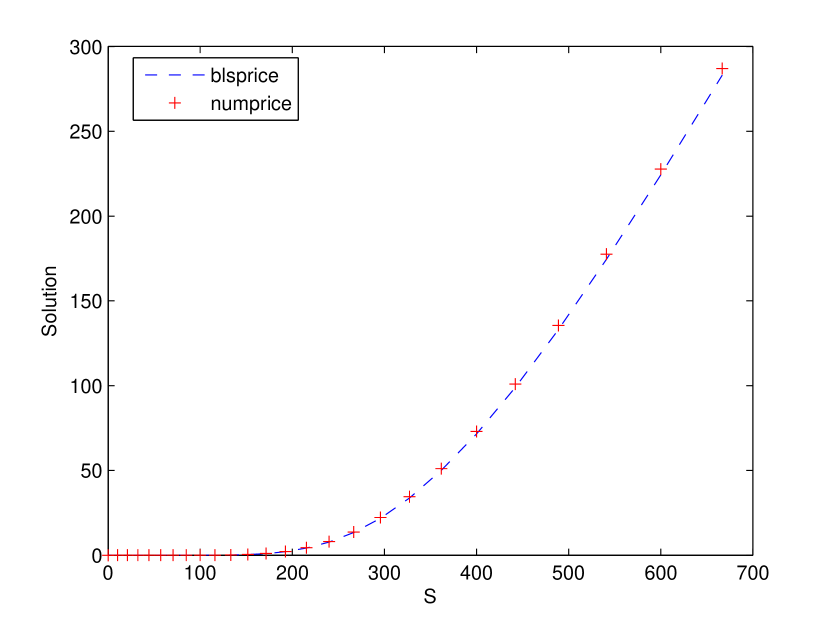

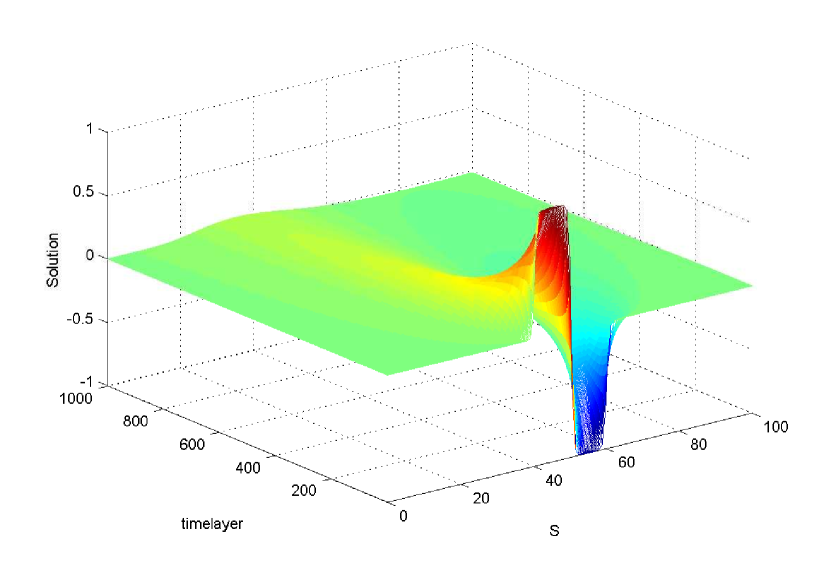

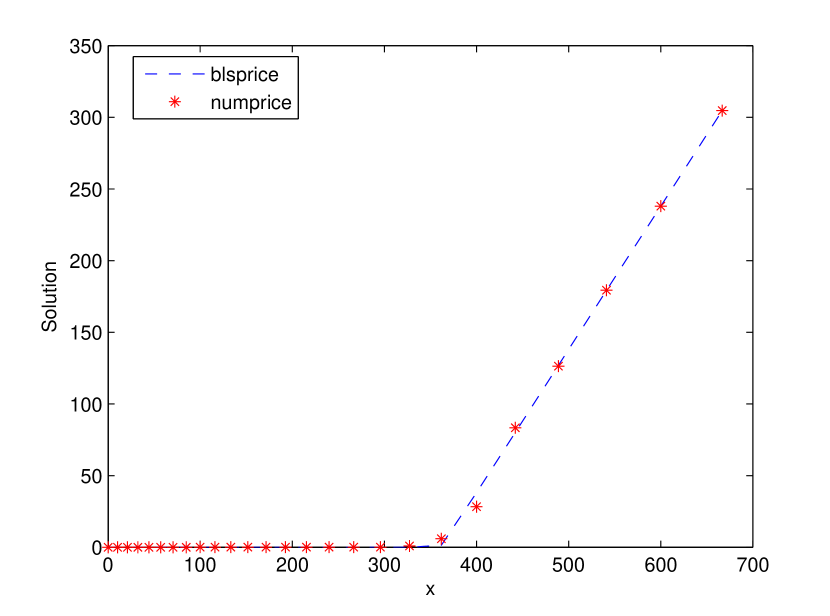

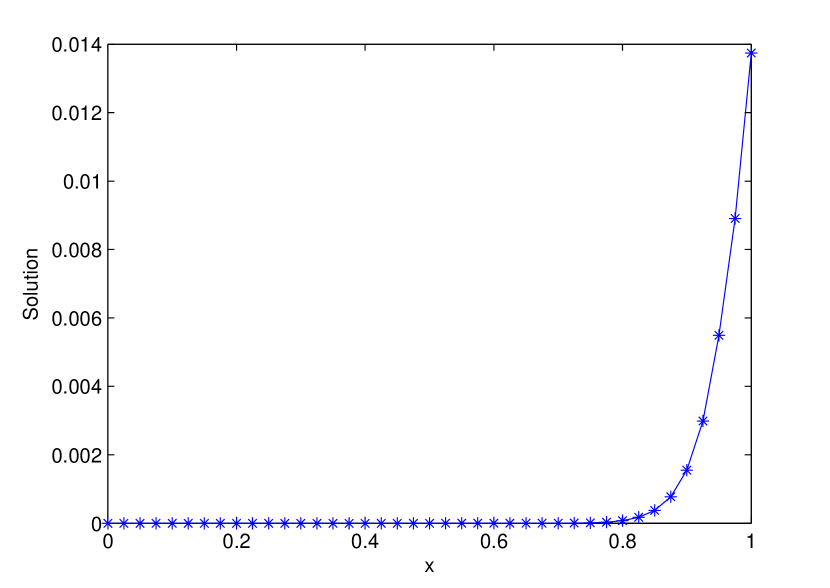

Figures 2-4 illustrate the numerical solution, computed with on an uniform mesh for and , and the well-known solution of the classical Black-Scholes equation, computed by the financial toolbox of MATLAB, blsprice(Price, Strike, Rate, Time, Volatility). Comparison results for , where and , are given in Figure 4, while the numerical solution is visualized in Figure 4.

Figure 1: Numerical Solution

Figure 2: Black-Scholes Solution

Figure 3: Numerical Solution

Figure 4: Comparison

In Table 2 the results are obtained by computations on a power-graded mesh for the same values of the parameters and exact solution. This mesh takes into account the degeneration at the both ends of the interval and is given by (in the current case )

The time step is chosen such that with .

Table 2:

20

7.154e-4

-

3.648e-4

-

6.263e-4

-

3.914e-4

-

40

1.880e-4

1.927

9.525e-5

1.947

1.650e-4

1.924

8.341e-5

2.230

80

4.818e-5

1.964

2.437e-5

1.966

4.226e-5

1.964

2.134e-5

1.966

160

1.220e-5

1.982

6.167e-6

1.982

1.970e-5

1.982

5.401e-6

1.982

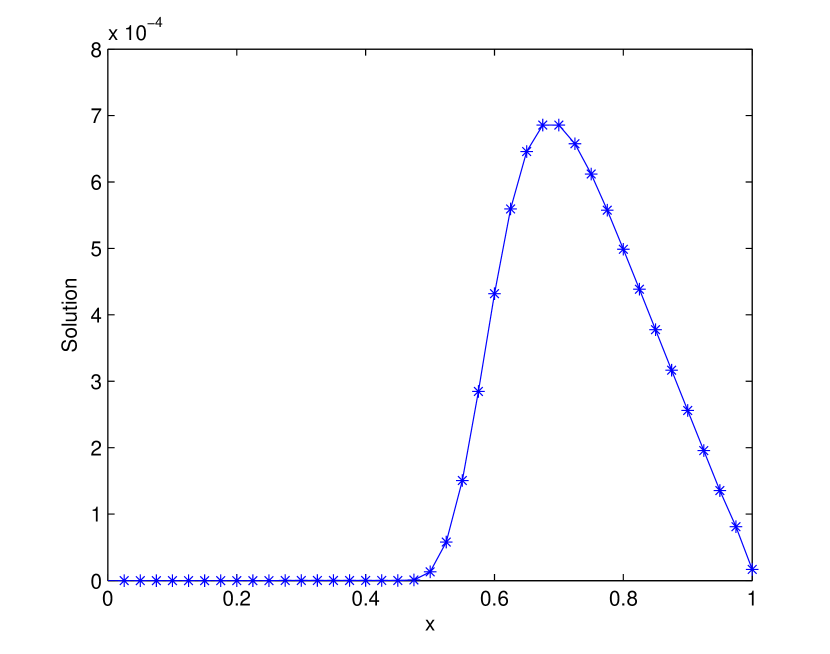

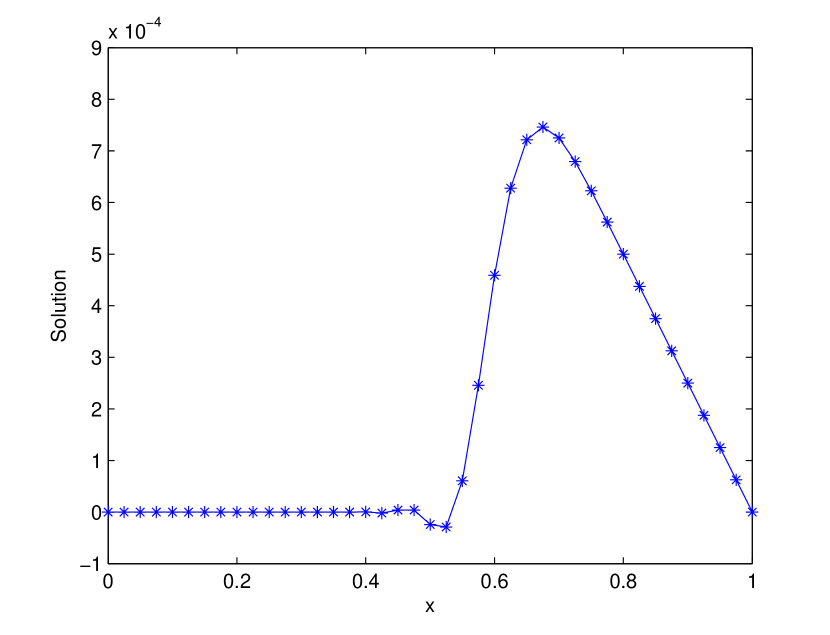

We now compute the solutions of the original models and . As exact solution we use the numerical solution on a very fine uniform grid, i.e. with . The results are given in Table 3. The numerical solutions of and for are plotted in Figures 6 and 6.

Table 3:

80

2.914e-7

-

1.112e-7

-

2.681e-3

-

2.171e-4

-

160

9.914e-8

1.555

2.841e-8

1.968

1.321e-3

1.021

7.476e-5

1.538

320

5.047e-8

0.974

7.386e-9

1.943

6.393e-4

1.046

2.544e-5

1.554

640

2.545e-8

0.987

1.973e-9

1.904

2.984e-4

1.099

8.374e-6

1.603

1280

1.269e-8

1.003

5.42e-10

1.864

1.279e-4

1.222

2.534e-6

1.724

Figure 5: Test Problem 2

Figure 6: Test Problem 4

The convergence of the numerical solution, obtained by the method to the solution of the classical Black-Scholes equation, transformed by (4), is given in Table 4. The node is omitted in the calculations since it corresponds to the case . We use the test parameters in with and . In the columns 2-5 of Table 4 we show the overall rate of convergence, while in the last column is given the rate of convergence in the strong norm of the numerical solution in a random node of the mesh, i.e. the one, corresponding to . The experiments are performed on an uniform mesh.

Table 4:

80

3.7473e-4

-

6.7765e-5

-

1.8848e-5

-

160

1.8939e-4

0.985

2.0388e-5

1.733

4.7877e-6

1.977

320

9.5196e-5

0.992

6.4913e-6

1.651

1.2016e-6

1.994

640

4.7722e-5

0.996

2.1574e-6

1.589

3.0070e-7

1.999

1280

2.3892e-5

0.998

7.3723e-7

1.549

7.5196e-8

1.999

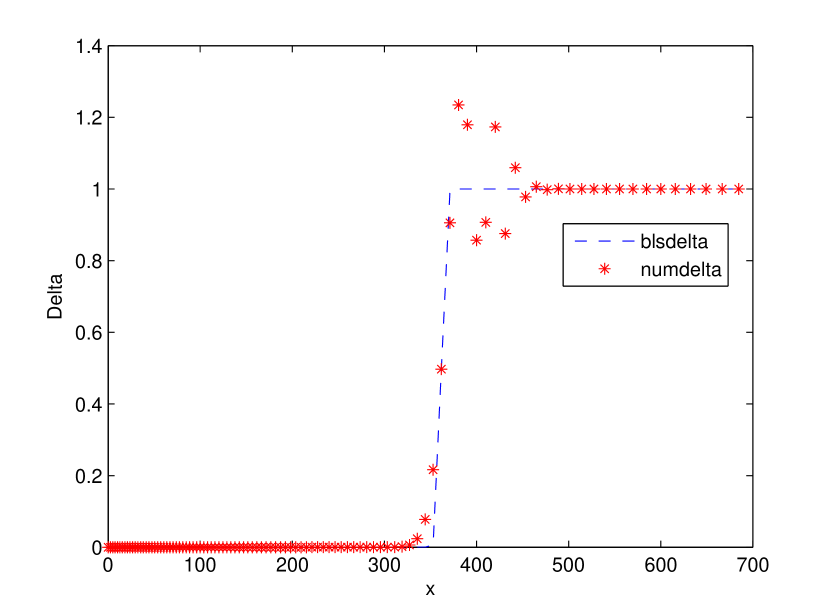

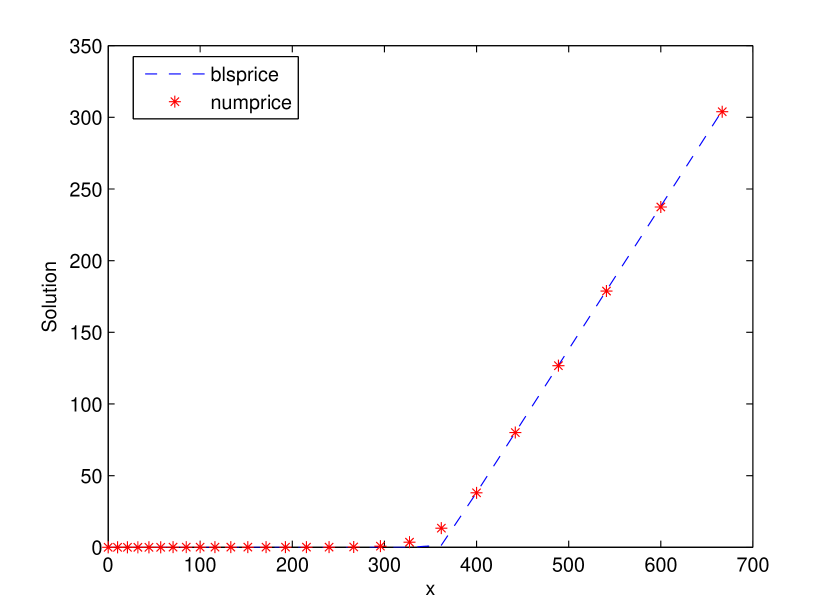

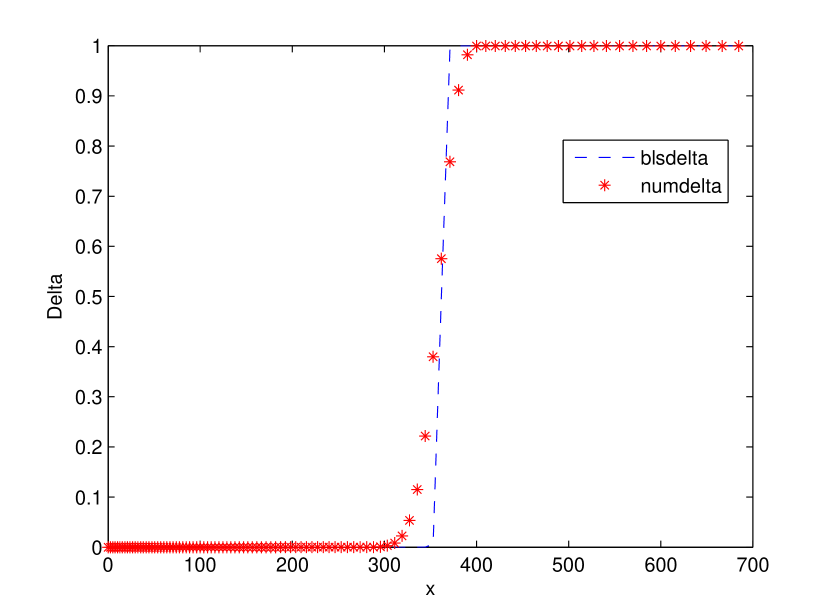

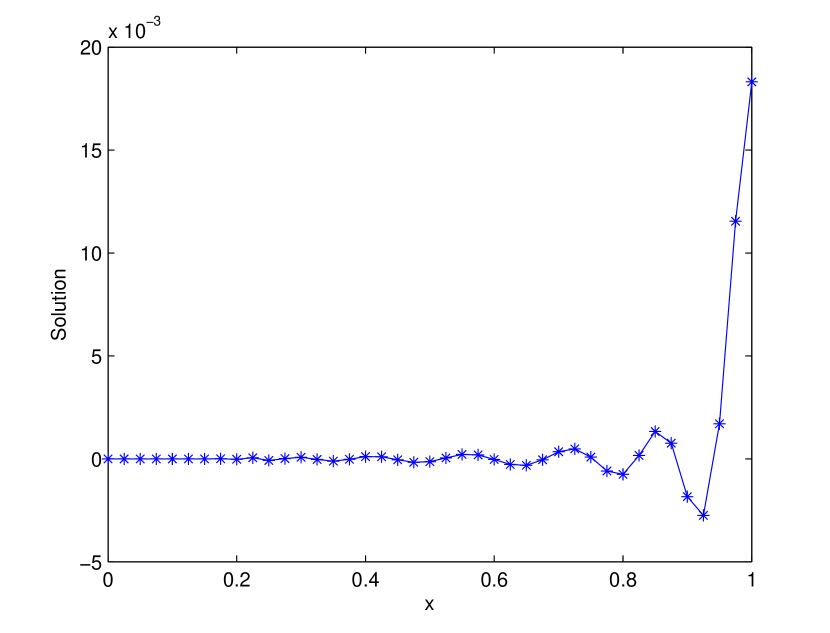

The benchmark of numerical methods in computational finance is the Crank-Nicolson second-order centered space difference scheme (CSDS). It is well known that it produces spurious oscillationsAP ; Duffy ; RS in the solution and it’s spatial derivatives, i.e. , that are financially unrealistic and are not tolerable. The Figures 8 and 8 illustrate the problem for the vanilla call option , computed on an uniform mesh for and parameters , , , , and . We compare the MATLAB function, blsdelta(Price, Strike, Rate, Time, Volatility), with the first derivative of the numerical solution. In the Figures 10 and 10, generated by the our difference scheme (ODS), no oscillations are observed.

Figure 7: Black-Scholes price CSDS

Figure 8: Black-Scholes CSDS

Figure 9: Black-Scholes price ODS

Figure 10: Black-Scholes ODS

A realistic situation in financial engineering occurs when the convection and diffusion terms have opposite signs. For example, situations, similar to , arise in the bond-pricing models, that are also of Black-Scholes type Duffy ; Sevc ; Zhu , where the parameters are interpreted in different context. In Figures 12 and 12 we show the numerical solutions, generated by our difference scheme and by the second-order centered space difference scheme respectively, applied to (5), for initial condition as in with parameters and . In Figures 14 and 14 are given the numerical solutions for initial condition as in with parameters and .

Figure 11: Black-Scholes price ODS

Figure 12: Black-Scholes price CSDS

Figure 13: Black-Scholes price ODS

Figure 14: Black-Scholes price CSDS

As seen in Figures 12-14, monotonicity and stability are not guaranteed for the centered space difference scheme if the convection and diffusion coefficients are of different signs. Simple calculations show that the discrete maximum principle is violated. We do not observe such problems in the numerical solution, generated by our numerical method.

6 Conclusion

In this article we present a fitted FVM for the generalized Black-Scholes equation (1). The method is applicable to more general Black-Scholes models, for example when and . We may also use any interval (here we took for simplicity) to solve the transformed problem. The main advantage of the developed numerical algorithm is reduction of the computational costs as well as positivity-preserving.

The conducted experiments show first order of convergence of the proposed scheme on a quasi-uniform mesh and second order of convergence on a particular graded mesh. Moreover, they also indicate better stability and unconditional (w.r.t. to the space step) monotonicity in comparison with other known schemes.

In a forthcoming paper we study the stability and the convergence of the proposed finite volume method.

Acknowledgement: The author is supported by the Bulgarian National Fund under Project DID 02/37/09 and by the European Social Fund through the Human Resource Development Operational Programme under contract BG051PO001-3.3.06-0052 (2012/2014).

References

(1) Achdou Y., Pironneau O., Computational Methods for Option Pricing, SIAM in the series Frontiers in Applied Mathematics (2005).

(2) Angermann L., Discretization of the Black-Sholes operator with a natural left-hand side boundary condition, Far East J. Appl. Math. 30(1), 1-41 (2008).

(3) Cen Z., Le A., A robust and accurate finite difference method for a generalized Black-Scholes equation, J. Comp. Appl. Mathematics 235, 3728-3733 (2011).

(4) Cen Z., Le A., A robust finite difference scheme for pricing American put options with singularity separating method, Numer. Algor. 52, 497-510 (2010).

(5) Chernogorova T., Stehlíková B., A comparison of asymptotic formulae with finite-difference approximations for pricing zero coupon bond, Numer. Algor. 59:571-588 (2012).

(6) Chernogorova T., Valkov R., Finite volume difference scheme for a degenerate parabolic equation in the zero-coupon bond pricing, Math. and

Comp. Modelling, 54, 2659-2671 (2011).

(7) Duffy D., Finite Difference Methods in Financial Engineering: A Partial Differential Approach, Wiley (2006).

(8) Ehrhardt M., Mickens R., A nonstandard finite difference scheme for Black-Scholes equation of option pricing, Preprint BUW-IMACM 12/08.

(9) Ramírez-Espinoza G.I., Ehrhardt M., Conservative and finite volume methods for the convection-dominated pricing problem, Preprint BUW-IMACM 12/07, Adv. Appl. Math. Mech. (accepted).

(10) Gyulov T., Valkov R., Classical and weak solutions for two models in mathematical finance, AIP Conf. Proc. v. 1410 , 195-202 (2011).

(11) Jackson N., Sülli E., Howison S., Computation of deterministic volatility surfaces, J. Comp. Finance 2, 5-32 (1999).

(12) Kadalbajoo M.K., Tripathi L.P., Kumar A., A cubic B-spline collocation method for a numerical solution of the generalized Black-Scholes equation, Math. and Comp. Modelling 55, 1483-1505 (2012).

(13) Morton K.W., Numerical Solution of Convection-Diffusion Problems, Chapman-Hall, London (1996).

(14) Mikula K., Ševčovič D., Stehlíková B., Analytical and Numerical Methods for Pricing Financial Derivatives, Nova Science Publishers Inc. Hauppauge (2011).

(15) Oleinik O.A., Radkevich E.V., Second Order Equations with Nonnegative Characteristic Form, Plenum Press, New York (1973).

(16) Seydel R., Tools for Computational Finance, Second ed., Springer, Berlin (2003).

(17) Vásquez C., An upwind numerical approach for an American and European option pricing model, Appl. Math. Comput., 97(2-3):273-286 (1998).

(18) Valkov R., Finite volume method for the Black-Scholes equation transformed on finite interval, AIP Conf. Proc. 1497, 76-83 (2012).

(19) Windcliff H., Forsyth P.A., Vetzal K.R., Analysis of the stability of the linear boundary condition for the Black-Scholes equation, J. Comput. Finance 8, 65-92 (2004).

(20) Wilmott P., Howison S., Dewynne J., The Mathematics of Financial Derivatives, Cambridge Univeristy Press, Cambridge (1995).

(21) Wang S., A novel fittied volume method for the Black-Scholes equation governing option pricing, IMA J. Numer. Anal., 24, 699-720 (2004).

(22) Zhu Y-I., Wu X., Chern I-L., Derivative Securities and Difference Methods, Springer, Berlin (2004).