Testing for a change of the innovation distribution in nonparametric autoregression – the sequential empirical process approach

Abstract

We consider a nonparametric autoregression model under conditional heteroscedasticity with the aim to test whether the innovation distribution changes in time. To this end we develop an asymptotic expansion for the sequential empirical process of nonparametrically estimated innovations (residuals). We suggest a Kolmogorov-Smirnov statistic based on the difference of the estimated innovation distributions built from the first and the last residuals, respectively (). Weak convergence of the underlying stochastic process to a Gaussian process is proved under the null hypothesis of no change point. The result implies that the test is asymptotically distribution-free. Consistency against fixed alternatives is shown. The small sample performances of the proposed test is investigated in a simulation study and the test is applied to data examples.

Running title: Testing for changes in nonparametric autoregression

AMS 2010 Classification: Primary 62M10, Secondary 62G30, 62G05, 62G10

Keywords and Phrases: conditional heteroscedasticity, empirical distribution function, hypothesis testing, kernel estimation, nonparametric AR-ARCH model, nonparametric CHARN model, partial sum process, time series

1 Introduction

Assume we have observed a time series that can be modelled via an autoregression model, possibly with conditional heteroscedasticity. We aim at testing for a change point in the innovation distribution. Tests for change points in the distribution of time series data have received a lot of attention in mathematical statistics; see Picard (1985), Giraitis, Leipus & Surgailis (1996), Horváth, Kokoszka & Teyssière (2001), Inoue (2001), Boldin (2002), Lee & Na (2004), Hušková, Prášková & Steinebach (2007), Hušková, Kirch, Prášková & Steinebach (2008), among others. Recently, an online-monitoring procedure to detect changes in the innovation distribution of linear autoregressive models was developed by Hlávka, Hušková, Kirch & Meintanis (2012). Those tests have applications in different areas, e. g. finance, climate science and medicine. For instance financial time series are tested for changes in the volatility or return (see e. g. Andreou & Ghysels (2009)) or, for climate control reasons, the annual water flow of rivers are tested for changes (see Hušková & Antoch (2003)).

Classical tests for change points in the distribution of independent data are often based on the difference of empirical distributions of the first and the last observations, respectively (). To derive asymptotic properties of the test sequential empirical processes are considered; see Shorack & Wellner (1986, p. 131) and also Csörgö, Horváth & Szyszkowicz (1997). Those methods for independent data have been transferred to test for change points in the innovation distribution of parametric time series models. Sequential empirical processes based on estimated residuals and corresponding change point tests were suggested by Bai (1994) for ARMA-models, by Koul (1996) in the context of nonlinear time series and by Ling (1998) for nonstationary autoregressive models. Those articles are the ones most similar in spirit to the paper at hand. However, we do not assume any parametric model for either the autoregression function, nor for the conditonal variance function, but use nonparametric kernel estimation methods. The (non-sequential) empirical process of residuals in a nonparametric homoscedastic autoregressive time series model was considered by Müller, Schick & Wefelmeyer (2009) who prove an asymptotic expansion. Moreover, residual empirical processes play an important role in the test for multiplicative structure in a nonparametric heteroscedastic time series regression model by Dette, Pardo-Fernández & Van Keilegom (2009). On the other hand our approach is similar in spirit to Neumeyer & Van Keilegom (2009) who consider change point tests for the error distribution in nonparametric regression models with independent observations. However, in comparison to the latter three articles the methods of proof in the paper at hand require considerably more technical effort because both the time series structure of the data and the additional index in the stochastic process have to be taken into account.

We prove an asymptotic expansion for the sequential empirical process of residuals and prove weak convergence of the scaled and centered process to a Gaussian process. It can be seen from those results that the nonparametric estimation of the autoregression and variance function decisively changes the asymptotic behaviour in comparison to the case where innovations would be known. The asymptotic expansion of the sequential process is then used to show that nevertheless the Kolmogorov-Smirnov test for a change point as described above is asymptotically distribution-free. As a by-product of our proofs we obtain results on uniform rates of convergence of kernel estimators (see Lemma B.1 in the appendix). Those are similar in spirit to results derived by Hansen (2008), but in contrast we avoid the stationarity assumption. Only some stabilization of the mean of innovation densities is needed (see assumption (F’)), which allows us to apply the results to prove consistency of the test under the existence of a change point. We moreover present a simulation study which shows good approximations of the asymptotic level as well as good power properties of the test under the example models considered. As data applications we consider two financial time series, namely the quarterly GNP of the USA and the S&P 500 index.

The paper is organized as follows. In section 2 we present the model, the nonparametric curve estimators and the stochastic process used for the change point test. In section 3 we list technical assumptions and present the asymptotic results for the sequential empirical process as well as for the process used for the change point test under the null hypothesis of no change point. Asymptotic results under fixed alternatives are presented in section 4. Section 5 is concerned with a homoscedastic modification of the model. In section 6 we present simulation results and consider the data examples. Section 7 concludes the paper, whereas all proofs are given in the appendix.

2 Model, hypotheses and test statistic

Let be a real valued stochastic process following the heteroscedastic autoregressive model of order one,

- (AR)

-

,

where the innovations , , are independent with and and is independent of the past , , .

Assume we have observed and our aim is to test for a change point in the innovation distribution. Thus we formulate the null hypothesis as

(with unknown) while the fixed alternative has the form

( unknown). Let denote an estimator for the innovation , , to be defined below. We consider a Kolmogorov-Smirnov type test statistic based on the stochastic process

| (2.1) |

where the sequential empirical processes are defined as

The weights are chosen as with continuous weight function such that for some sequences , ,

| (2.2) |

for some fixed independent of . The weights are included in the definition of the sequential empirical processes to avoid problems of kernel estimation in areas where only few data are available, compare to Müller, Schick & Wefelmeyer (2009) and Dette, Pardo-Fernández & Van Keilegom (2009). Further let the residuals be defined as

for kernel regression and variance estimators

| (2.3) | |||||

| (2.4) |

and . Here denotes a kernel function and a positive sequence of bandwidths. For the ease of representation we use the same bandwidth to estimate and , though in practice it may be advisable to choose different bandwidths. The asymptotic results presented in the paper remain valid when two different bandwidths according to the assumptions (C) and (C’), respectively, in the next sections are chosen.

We list model assumptions as well as assumptions on the estimators in the next two sections.

3 Asymptotic results under the null hypothesis

Throughout this section we make use of the following assumptions.

- (K)

-

The kernel is a three times differentiable density with compact support and , . Moreover and .

- (C)

-

The sequence of bandwidths fulfills

Remark: As can be seen from the proof the first bandwidth condition can be replaced by , where are defined in assumptions (X) and (M) below. The second bandwidth condition is equivalent to the existence of some such that

(3.1) for all . The first condition in (3.1) is typical in the context of empirical processes of nonparametrically estimated residuals, compare Dette, Pardo-Fernández & Van Keilegom (2009) or Neumeyer & Van Keilegom (2009), while the -factor stems from the boundary truncation via the weight function. The second condition in (3.1) arises at the very end of the proof of Lemma B.4 in appendix B due to a -dependent covering number. The constant is also used in Lemma B.2 in appendix B.

- (I)

-

For the interval there exists some such that . Moreover .

- (W)

-

The weight function fulfills (2.2) and is three times differentiable such that for .

- (F)

-

The innovations , , are identically distributed with distribution function . Their density is continuously differentiable and as well as .

Remark: Due to the continuity of the density and the derivative it follows that also , and .

- (E)

-

There exists some such that and .

- (X)

-

The observations , , are identically distributed and the process is -mixing with exponentially fast decaying mixing-coefficient .

Their density is bounded and four times differentiable with bounded derivatives. The density is also bounded away from zero on compact intervals and there exists some such that .Remark: Assumptions (F) and (X) imply strong stationarity of the process .

- (Z)

-

It holds that

and there exists some such that

is valid for all , for , with .

- (M)

-

The regression function and the scale function are four times differentiable and there exist some and , with , , , such that , , and .

An example for which the assumptions are fulfilled is the AR(1) model with standard normally distributed innovations , . Then the observations , , are identically distributed and with , a weight function that fulfills (W), a kernel function that fulfills (K) and a bandwidth that fulfills (C) all assumptions are fulfilled. To this end note that exponential -mixing holds for stationary models with for some with ; see Doukhan (1994).

In the first theorem we state a stochastic expansion of the residual based sequential empirical process. The proof is given in appendix A.

Theorem 3.1

Under model (AR) with assumptions (K), (C), (I), (W), (F), (E), (X), (Z), and (M) we have that under the null hypothesis of no change point

uniformly with respect to and .

Remark 3.2

The theorem complements results by Müller, Schick & Wefelmeyer (2009) and Dette, Pardo-Fernández & Van Keilegom (2009). In both articles only non-sequential processes are considered (i. e. the case ). While Müller, Schick & Wefelmeyer (2009) consider a homoscedastic version of model (AR) (, see also section 5), Dette, Pardo-Fernández & Van Keilegom (2009) consider a heteroscedastic autoregression/regression model and a result similar to Theorem 3.1 (for ) can be derived from their proofs. The sequential process () though requires much more involved methods of proof that also result in slightly more complicated assumptions.

From the stochastic expansion weak convergence of the sequential residual process can be derived. The proof of Corollary 3.3 is given in appendix A.

Corollary 3.3

Under the assumptions of Theorem 3.1 under the null hypothesis of no change point the process

converges weakly to a centered Gaussian process with

Remark 3.4

From Theorem 3.1 and Corollary 3.3 it can be seen that the nonparametric estimation of the autoregression and conditional variance function vastly influences the asymptotic behaviour of the process. The asymptotic distribution of the partial sum processes decicively changes when based on residuals compared to the corresponding processes built from iid innovations. This is different from simpler situations in specific parametric time series models, see Bai (1994) and Kreiß (1991), among others, but corresponds to situations in parametric as well as nonparametric regression models, see e. g. Koul (2002) and Neumeyer & Van Keilegom (2009). Note however that neither the chosen kernel function nor the bandwidth have any influence on the asymptotic distribution.

The stochastic expansion given in Theorem 3.1 can be used to derive the asymptotic distribution of the change point test. First we state weak convergence of the process defined in (2.1). To this end in the following let denote a completely tucked Brownian sheet, i. e. a centered Gaussian process with covariance structure

Theorem 3.5

Under model (AR) with the assumptions (K), (C), (I), (W), (F), (E), (X), (Z), and (M) under the null hypothesis of no change point there exist Gaussian processes , , with the same distribution as such that

The proof is again given in appendix A as well as the proof of the next corollary in which we state the asymptotic distribution of the change point test.

Corollary 3.6

Under the assumptions of Theorem 3.5 under the null hypothesis of no change point the Kolmogorov-Smirnov type test statistic converges in distribution to .

Remark 3.7

From Corollary 3.6 it follows that the test is asymptotically distribution-free although the stochastic expansion given in Theorem 3.1 still depends on the innovation distribution in a complicated way. This remarkable feature in the context of procedures based on nonparametric residual empirical processes was already observed by Neumeyer & Van Keilegom (2009) in the context of independent observations. The critical values for the test are tabled in Picard (1985).

4 Asymptotic results under fixed alternatives

The assumptions (K) and (M) as well as the following assumptions are used to proof consistency of the test under fixed alternatives.

- (C’)

-

The sequence of bandwidths fulfills

- (I’)

-

For the interval there exists some such that .

- (W’)

-

The weight function is continuous and fulfills (2.2).

- (F’)

-

Let have distribution function and density , . Let as well as for .

Remark: Under the alternative the assumption is fulfilled when , , , and , where and are densities corresponding to and , respectively.

- (E’)

-

It holds that for some , .

- (X’)

-

The observation process is -mixing with mixing-coefficient for some

The observation densities are four times differentiable and fulfill , . Moreover there exists some such that .

- (Z’)

-

For all with it holds that

,

,

and there exists some such thatand

for , with .

Remark: It suffices when the assumption is valid for defined in (B.6) in the proof.

Under the alternative the arithmetic mean of all converges to the weighted sum of the observation density before the change point and the long range observation density after the change point with weights and , so (Z’) is fulfilled if (Z) and (Z) with the long range observation density instead of are fulfilled and the last part of (Z’) holds.

Remark 4.1

If the observations and the innovations are identically distributed it holds that the second and third part of (X’) are equivalent to the second and third part of (X) and (Z’) is equivalent to (Z). The other assumptions are not equivalent, even if the the innovations are identically distributed. In detail it holds that assumption (I’) is weaker than (I), (F’) is weaker than (F), (E’) is weaker than (E), the first part of (X’) is weaker than the first part of (X), as well as (C’) is weaker than (C).

Remark 4.2

Note that under the alternative the process is not stationary. Thus to obtain consistency most auxiliary results in appendix B are proved without assuming stationarity. A stabilisation of the density averages as in assumptions (F’), (X’) is sufficient for our results to hold. In particular we generalize some of Hansen’s (2008) results in Lemma B.2.

Theorem 4.3

Under the assumptions (K), (C’), (I’), (W’), (F’), (E’), (X’), (Z’), and (M) under the fixed alternative with a change point in , we have

Corollary 4.4

Under the assumptions of Theorem 4.3 the Kolmogorov-Smirnov type test based on the process is consistent against fixed alternatives .

5 The homoscedastic AR-model

In this section we consider a homoscedastic AR-model

- (AR1)

-

,

where the innovations , , are independent with and and is independent of the past , , .

Our aim is to test the change point hypotheses vs. from section 2. Note that here under the change in the innovation distribution can result from a change in the variance. The residuals are now defined as and the test statistic is built with these in the same way as described for the heteroscedastic case; see (2.1). Let assumptions (), () under the null hypothesis and assumption (Z”) under the alternative be formulated as (Z), (M) in section 3 and (Z’) in section 4, respectively, but replacing the variance function by a constant. Let () be formulated as (F), but replacing conditions , by , . Let (F”) be formulated as (F’), but deleting the last condition. Let () and (E”) be formulated as (E) and (E’) respectively, but replacing by . Then the following asymptotic results are valid.

Theorem 5.1

Under model (AR1) with assumptions (K), (C), (I), (W), (), (), (X), (), and () we have that under the null hypothesis of no change point

uniformly with respect to and .

Corollary 5.2

Under the assumptions of Theorem 3.1 under the null hypothesis of no change point the process

converges weakly to a centered Gaussian process with

Theorem 5.3

Under model (AR1) with assumptions (K), (C’), (I’), (W’), (F”), (E”), (X’), (Z”), and () the Kolmogorov-Smirnov type test based on the process is consistent against fixed alternatives .

6 Small sample performance

6.1 Simulations

The heteroscedastic model.

To examine the performance of the test on small samples we considered AR(1) models and ARCH(1) models.

For the AR(1) case we considered the models

where is the distribution function of a random variable that is distributed with probability and distributed with probability and is the distribution function of a random variable that is distributed with probability and distributed with probability , for different values of . Though the data are generated by a homoscedastic model we assume for the data analysis validity of the heteroscedastic model (AR).

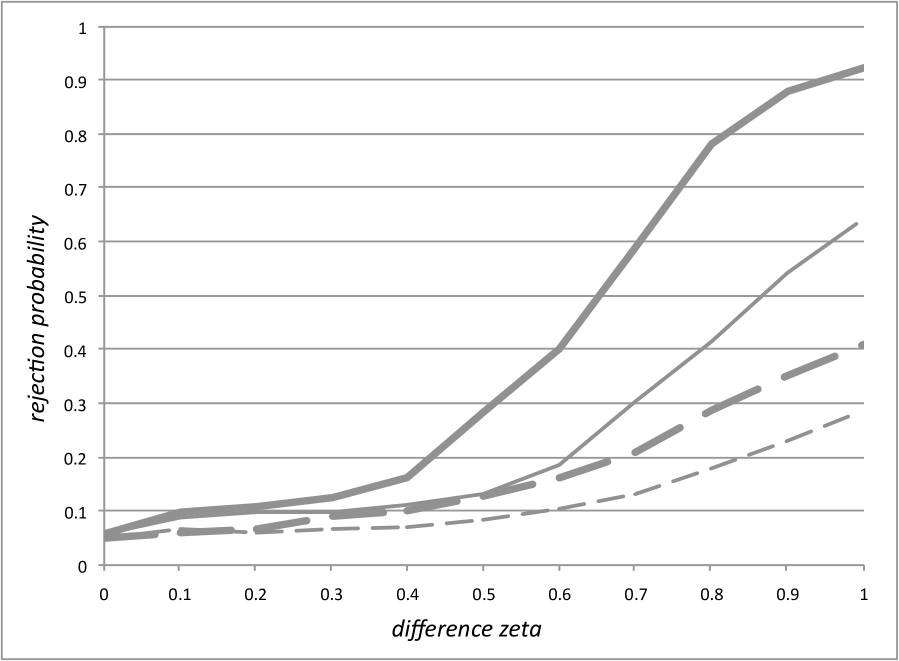

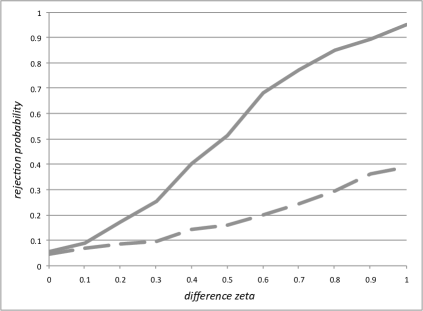

In Table 1 the rejection probabilities for 500 repetitions, level 5% and sample sizes are shown. They are also shown in the left panel of Figure 1. It can be seen that the level is approximated well and the power increases for increasing parameter as well as for increasing sample size .

| , | ||||||||

|---|---|---|---|---|---|---|---|---|

| , | ||||||||

| , | ||||||||

| , |

The same kind of change points was examined for ARCH(1) models

with rejection probabilities for 500 repetitions and level 5% as displayed in Table 2 and in the right panel of Figure 1.

| , | ||||||||

|---|---|---|---|---|---|---|---|---|

| , | ||||||||

| , | ||||||||

| , |

We also considered innovations with Student-t distribution with three degrees of freedom. The Student-t distribution has heavier tails than the normal distribution and is therefore more appropriate for modeling financial data. Due to the fact that Var has to be one for all , the Student-t distribution was standardized. We considered the ARCH(1) models

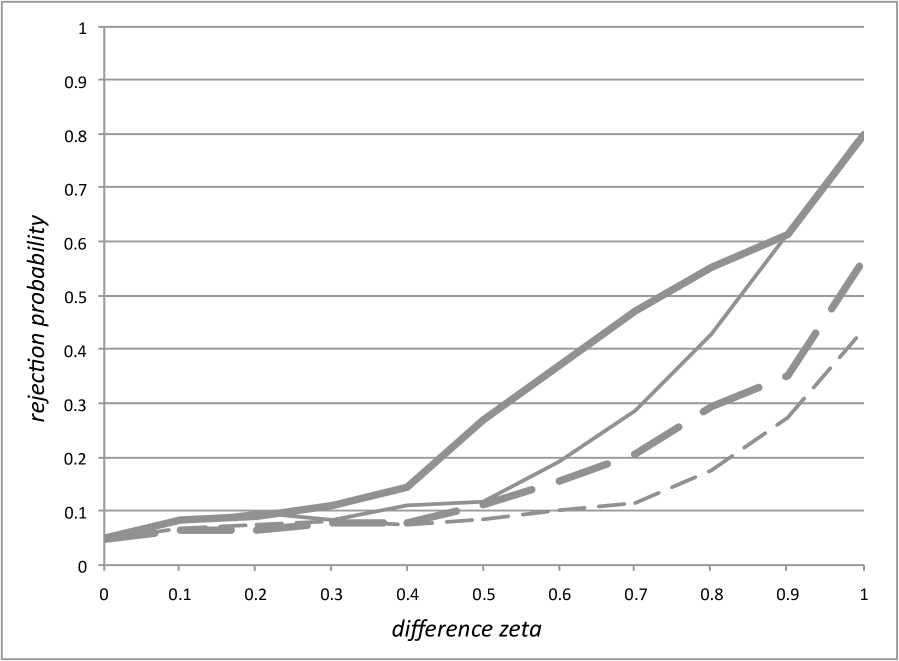

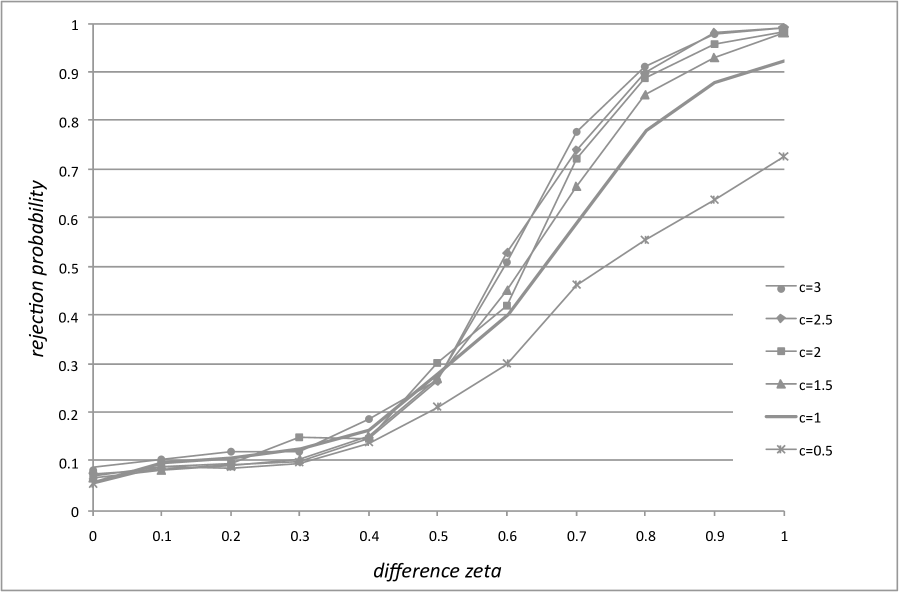

for different values of . The rejection probabilities for 500 repetitions, level 5% and sample sizes are shown in Table 3 and in Figure 3.

The asymptotic level is approximated reasonably well and the power increases with increasing as well as with increasing .

Here the increase with for small is not as pronounced as for the models considered before, because the difference between the distribution before and after the change point is for just slightly different to that for because the Student-t distribution converges to the standard normal distribution.

We also examined the following ARCH(1) models:

where is the distribution function of a random variable that is distributed with probability and distributed with probability and is the distribution function of a random variable that is distributed with probability and distributed with probability , for different values of .

The rejection probabilities for 500 repetitions and level 5% are shown in Table 4 and Figure 3.

| , | ||||||||

|---|---|---|---|---|---|---|---|---|

| , | ||||||||

| , | ||||||||

| , |

The models with Student-t distributed innovations with three degrees of freedom do not fulfill the moment assumptions, because moments greater than or equal to do not exist, but the simulations show that the test works on them just the same.

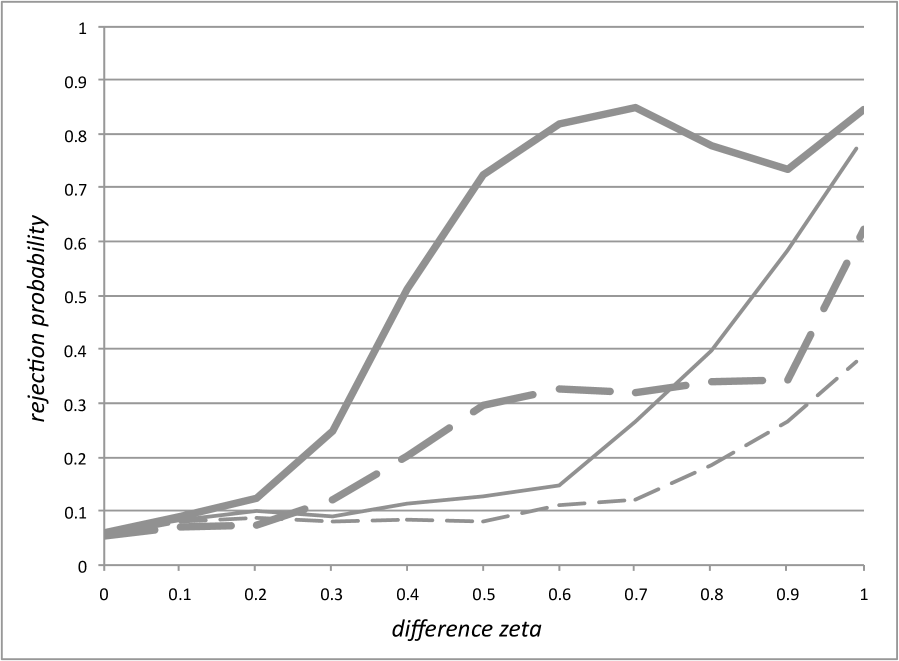

Finally, we considered the skew-normal distribution as innovation distribution. Let denote the skew-normal distribution with location parameter

scale parameter and shape parameter . We considered the AR(1) and ARCH(1) models

and

for different values of . The parameters in the skew-normal distribution were chosen like this to guarantee and Var for all . The rejection probabilities for 500 repetitions and level 5% are shown in Table 5 and Figure 4.

| AR(1), | ||||||||

|---|---|---|---|---|---|---|---|---|

| AR(1), | ||||||||

| AR(1), | ||||||||

| ARCH(1), | ||||||||

| ARCH(1), | ||||||||

| ARCH(1), |

The homoscedastic model. For the homoscedastic model as considered in section 5 only Var is assumed so that we can simulate a change in the variance. To this end we generated data from the AR(1) model

for different values of .

The rejection probabilities for 500 repetitions and level 5% are shown in Table 6 and in Figure 5.

It can be seen that the theoretical results are supported by the simulations.

Simulation setting.

For each simulation observations were generated, with distribution before and with distribution after the change point. For the test the last observations were used. This was done to ensure that the process is in balance.

The empirical processes were built without the weight function , which means that was chosen as the real line. This is contrary to the assumptions. Nevertheless the simulations support our theoretical results very well, so it can be assumed that the weight function is necessary for the theory but the test can be used regardless.

The Nadaraya-Watson estimators and were calculated with Gaussian kernel and bandwidth . This is also not compatible with all assumptions, e. g. the support of the kernel is not compact. However this has negligible effect on the simulations because the Gaussian kernel decreases exponentially fast at the tails. The choice of bandwidth is not compatible to the assumption as well because it does not converge faster than . A compatible choice would be for some adequate , but for the small sample sizes that were used the logarithm would be too strong in comparison to , so we omitted it.

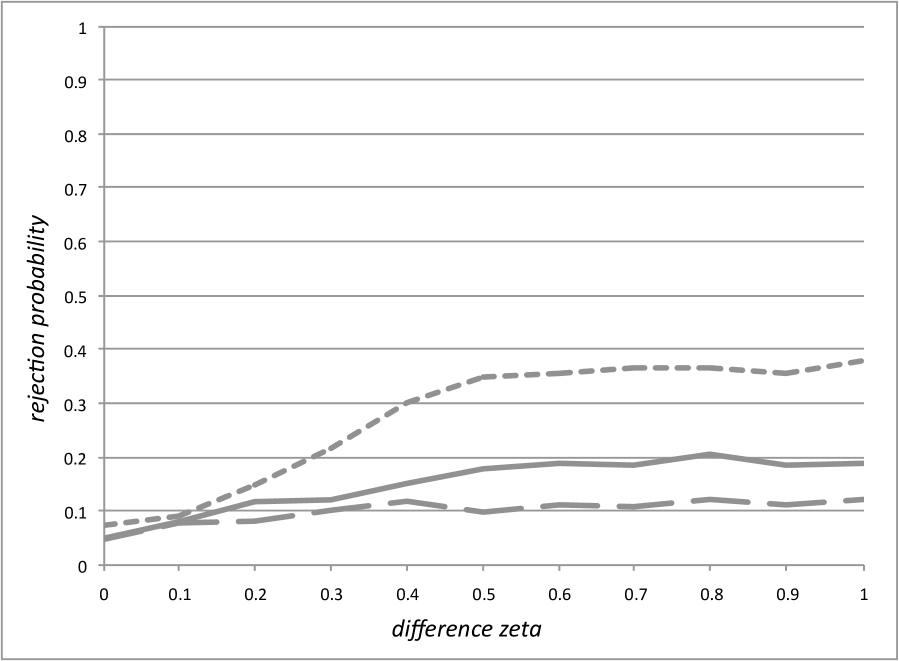

To study the influence of the size of bandwidth we simulated the first AR(1) model (with ) with for different values of . The results are shown in Figure 6. It can be seen that the rejection probability increases with , especially for , but also the rejection probability under the null hypothesis increases with .

6.2 Real data applications

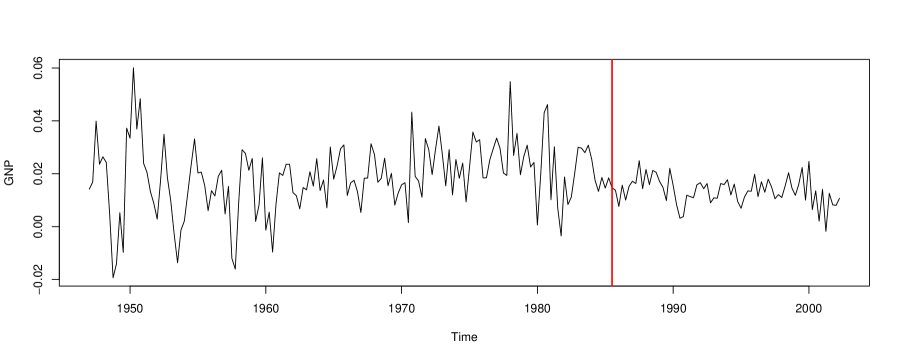

We also applied our new test to real datasets. Firstly we examined the quarterly GNP (Gross National Product) of the USA in billions of dollars from 1947(1) to 2002(3). The data have been seasonally adjusted. We looked at the difference of the logarithm of the GNP, which is naturally interpreted as the growth rate of GNP. Figure 8 shows that there might be a structural break in the data and indeed our testing procedure rejects the null hypothesis of no change point with p-value smaller than 0.001. The vertical line marks the point at which the test process is maximal. We used the test statistic for homoscedastic cases, next to the one for heteroscedastic cases, for these data, because the plot suggests that there might be some change in the variance. Both tests delivered the same value of the test statistic which is 1.392 (approximately).

The same data were examined in Shao & Zhang (2010) with some kind of CUSUM test that is based on an self-normalization method. They tested for a possible change in the marginal variance, 75% quantile and 25% quantile of the observations, and the test for a change in the 75% quantile rejected the null hypothesis of no change point with p-value smaller than 0.001. The tests for a change in the marginal variance and 25% quantile did not reject the null hypothesis of no change point. The p-values for these were greater than 0.1.

Shumway & Stoffer (2006) also examined these data and used stationary time series models, such as AR(1) and MA(2), to fit them. Both model fits pass their diagnostic checking tests, but our results, as well as the results of Shao & Zhang (2010), indicate that the data might not be a stable process but contain a change point.

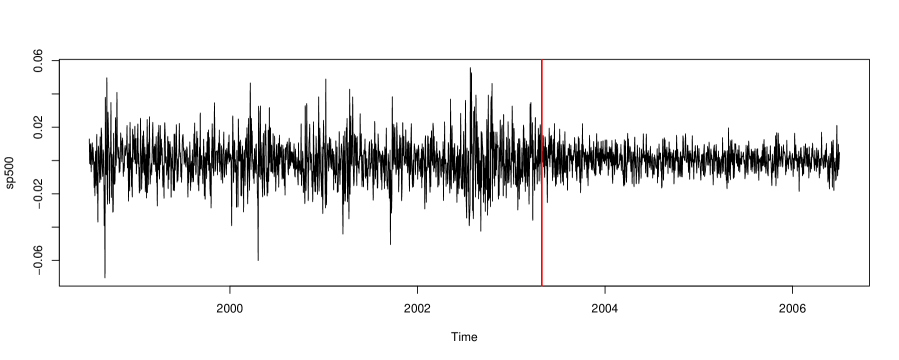

Another dataset that we examined is the daily log-return of the S&P 500 index, a world known stock index that is quoted at the New York stock exchange, from July 1st 1998 to June 30th 2006. Figure 8 shows that there might be a structural break in these data as well, which is confirmed by our testing procedure with p-value smaller than 0.001. Again the vertical line marks the point at which the test process is maximal. Like in the GNP example we used the test statistics for both cases (hetero- and homoscedastic) and both delivered nearly the same value of the test statistic which is 1.578 for the heteroscedastic and 1.575 for the homoscedastic case (approximately).

We examined these data although it is known that for financial data often higher moments do not exist, because our simulation study with Student-t distributed innovations shows that the testing procedure works even if the moment assumption is not fulfilled.

The S&P 500 data were also examined by Kirch & Tadjuidje Kamgaing (2012). They used a testing procedure based on cumulative sums of parametrically estimated residuals for nonlinear autoregressive models. Instead of log-returns they used transformed squared log-returns and they also reject the null hypothesis of no change point. They do not give a p-value but reject clearly at level 5%.

7 Concluding remarks and outlook

In this paper we transferred classical ideas of testing for change points in samples of independent observations to testing for change points in the innovation distribution in nonparametric autoregressive models with conditional heteroscedasticity. To this end we considered the sequential empirical process of estimated innovations, proved an asymptotic expansion and weak convergence. We showed that the classical Kolmogorov-Smirnov test for a change point is asymptotically distribution-free in the new context and is not influenced asymptotically by the nonparametric estimation of the innovations. We proved consistency of the test under fixed alternatives and demonstrated the good performance in a simulation study. The proofs are based on empirical process theory for time series data and require the development of several technical auxiliary results. In particular we prove uniform rates for kernel estimators and their derivatives under nonstationarity assumptions.

It is the topic of a future project to apply the theory developed here to test for serial independence of innovations or independence of the current innovation and past observations resp. covariates in nonparametric time series regression models. Moreover our aim is to model -dimensional joint innovation distributions in multivariate time series models.

Appendix A Proofs: main results

In this section we give the proofs for Theorems 3.1, 3.5, 4.3 and Corollaries 3.3, 3.6, 4.4, whereas some auxiliary results (Lemmata B.1–B.6) are stated and proved in section B. In some proofs standard arguments are given in condensed form for the sake of brevity. All details can be found in Selk (2011).

A.1 Proofs for results under the null hypothesis

Proof of Theorem 3.1. From Lemma B.4 and Lemma B.5 it follows that under uniformly with respect to and

| (A.1) | |||||

where for

| (A.2) |

it is straightforward to show by a first order Taylor expansion applying assumption (F) as well as Lemma B.2 that

| (A.3) |

uniformly with respect to and . Now inserting the definition of from (2.3) we have

uniformly with respect to and , which follows from Lemma B.3 (i)–(iii). Now

| (A.4) |

can be shown by Chebyshev’s inequality and we obtain

| (A.5) |

By an application of

and Lemma B.2, for the second term arising from (A.3) we have

Now noting that

| (A.6) |

similarly to the derivation of (A.5) with results similar to those in Lemma B.3 one obtains

| (A.7) |

Finally from (A.3), (A.5) and (A.7) one has

and the assertion follows from this equality and (A.1).

Proof of Corollary 3.3. By an application of Theorem 3.1 it remains to show that

| (A.8) | |||||

converges weakly to the process . Here we use the notations

where

is equipped with the semi-metric

and is totally bounded. By an application of Theorem 2.11.9 in van der Vaart & Wellner (1996) one can show weak convergence of the process

to a centered Gaussian process. Details are omitted for the sake of brevity, but the arguments are similar to (but simpler than) those in the proofs in Neumeyer & Van Keilegom (2009) (see their proof of theorem 3 and the online supporting information).

The assertion now follows by the continuous mapping theorem applied to the projections and and by a straightforward calculation of the asymptotic covariance.

Proof of Theorem 3.5. For the process defined in (2.1) we have by a straightforward calculation

uniformly with respect to and . Here the last equality follows from (A.4). Now inserting the expansion given in Theorem 3.1 we directly obtain

uniformly with respect to and . The assertion follows from Remark 2 in Neumeyer & Van Keilegom (2009), which goes back to Theorem 3.1 by Csörgö, Horváth & Szyszkowicz (1997).

A.2 Proofs for results under fixed alternatives

Proof of Theorem 4.3. Assume that is valid with a change point in . Analogously to the proof of Theorem 3.1 we have from Lemma B.4 that uniformly with respect to

where the last equality follows from Lemma B.6. Here, for as defined in (A.2) one has by the mean value theorem applying assumption (F’) and Lemma B.2 that

Thus the first assertion of the Theorem follows. The second assertion is shown analogously.

Appendix B Proofs: auxiliary results

B.1 Results

For easy overview we first state the auxiliary results and then collect the proofs in the next subsection.

Lemma B.2

Lemma B.3

Under the assumptions of Theorem 3.1 we have

-

(i)

-

(ii)

-

(iii)

.

Lemma B.4

Lemma B.5

Lemma B.6

B.2 Proofs

Proof of Lemma B.1. Let . Throughout the proof we assume that for all with from assumptions (E), (E’). This is possible, because

by assumption (E) resp. (E’).

Choose points , (for from assumption (I) resp. (I’)) such that is covered by intervals . Now let , where is bounded by on the support of for (assumption (K)). Then by the mean value theorem we have

for all such that . From this we obtain

The last term on the right hand side can be bounded by

by a change of variable and by assumption (K) and (Z) or (Z’), respectively, and model assumption (AR). In what follows we show that term (B.2) is of order ; it can be shown analogously that (B.2) is of the same order. Define (for fixed)

then the sequence inherits the mixing conditions from due to 2.6.1 (ii) in Fan & Yao (2005). Further the variables are centered and bounded by . We apply Liebscher’s (1996) Theorem 2.1 to to obtain

| (B.3) | |||||

for some independent of and for

| (B.6) |

Further,

with as in assumption (Z) resp. (Z’). In order to obtain B.3 from Liebscher’s Theorem one has to show that

This can be done by some tedious calculations, which are omitted for the sake of brevity.

By assumption (Z) resp. (Z’) we have . To see this consider for example for the term

(note that ), and

The other terms in the definition of are treated similarly.

Inserting the definitions of , , and one obtains with a simply calculation that (B.3) is of order by the assumptions on the bandwidth and the mixing coefficient. This concludes the proof.

Proof of Lemma B.2. We only present the proofs for the assertions on , those on follow by similar arguments using (A.6).

Let for . Then from Lemma B.1 it directly follows that

| (B.7) |

Let further for . Then

Noting that by assumption (K),

for , from a Taylor expansion it further follows that

| (B.8) | |||||

where the last equality follows from assumption (X) resp. (X’) and (M) (note that , , ). Note further that

| (B.9) | |||||

Now for from (2.3) we obtain

by (B.7), (B.8), (B.9) and assumption (X) resp. (X’). The first assertion in (i) now directly follows from (assumption (M)).

Differentiating it is easy to see that from (B.7) and (B.8) it follows that

where the last equality only holds for by our bandwidth conditions. The first assertion of (ii) follows.

Finally, note that by considering the cases and we have

and the first assertion of (iii) follows.

Proof of Lemma B.3. (i). For

we have

where last equality follows by a calculation of the variance and Chebyshev’s inequality. The first equality can be derived by using

| (B.10) |

which follows from the proof of Lemma B.2 (note that with the notations used there, , ) and results from Lemma B.2 (i) for the AR-model with , .

Now assertion (i) is equivalent to

with centered functions . By arguments similar to those in the proof of Lemma B.2 and by results from Lemma B.2 for , we have for for the function classes

with . Thus it remains to show that

| (B.11) |

To this end let . It follows from Theorem 2.7.1 in van der Vaart & Wellner (1996) that balls of radius with respect to the supremum norm on the interval are needed to cover . Here the constant only depends on . Let denote centers of those balls. We may assume that those functions are elements of , too (see Pollard (1990), p. 10). Further let segment in intervals of length such that . Then it can be shown that

By an application of Liebscher’s (1996) Theorem 2.1 to random variables (for fixed) one can show the existence of some constant such that

Details are omitted for the sake of brevity. From this the rate follows for (B.11).

(ii). We only describe the main steps of this proof. The random denominator can be replaced by the true density due to (B.10). Now define

Then, can be shown by Chebyshev’s inequality and for the assertion

is shown analogously to the proof of (i).

(iii). The assertion can be proved by the same methods.

Proof of Lemma B.4. Let and . Now the assumption of the lemma is equivalent to

with

For the proof we may assume that , and for all because , by Lemma B.2, and further

by the model assumption for all .

Note that for all such that , for all . Thus, by some simple estimations,

where in the last line we have applied that for

| (B.12) |

by the model assumption and analogously for , .

For the remainder of the proof we therefore only need to consider . Define sequences of function classes by

Then by Lemma B.2, , and it remains to show that

To this end we apply covering arguments. Let . The -covering numbers of both function classes with respect to the supremum norm on can be bounded by , see Theorem 2.7.1 by van der Vaart & Wellner (1996). Let and , respectively, denote the corresponding centers of covering balls. Note that then and for all . Let further the intervals and be segmented by points and , respectively, in segments of length such that the number of points are bounded by and . Let denote the supremum norm on . Then

| (B.13) | |||||

| (B.14) | |||||

| (B.15) | |||||

| (B.16) |

where the maximum is always with respect to , , .

To further bound the term (B.14) first consider fixed , , such that (the other case is treated analogously). Then

where the last step follows from the mean value theorem, assumption (F) resp. (F’) and . Similarly for (B.16) we obtain

| (B.17) | |||||

For (B.13) we have

and analogously for (B.15) the same rate . Altogether we have shown that

To conclude the proof we exemplarily consider term (B.2); the other terms are treated analogously. For all we have

| (B.19) | |||||

by an application of Theorem 1.6 by Freedman (1975). To see this define (for fixed)

and note that , as well as

by an application of the mean value theorem, the definition of , and assumption (F) resp. (F’), for some constant independent of . Hence, inserting the bounds on , and , can be bounded by

which follows from bandwidth condition (3.1).

Proof of Lemma B.5. Analogous to the proof of Lemma B.4 we may assume that for all . Then

where the second last equality follows from (B.12).

Now let and let be such that for all and . Further let be such that for all and . Then we have

| (B.21) | |||||

| (B.25) | |||||

To obtain the last inequality it can be shown analogously to the treatment of (B.13) in the proof of Lemma B.4 that (B.21) is of order . Further the bounding of (B.21) by the sum of (B.25), (B.25) and (B.25) is straightforward by using monotonicity of indicator and distribution functions.

Now by the mean value theorem and assumption (F) it follows that (B.25) is of order . The remaining terms (B.25), (B.25), (B.25) are treated in the same way and we will only consider (B.25) in what follows. For this term we have for each that

(where denotes the -mixing coefficient) by an application of Theorem 2.1 by Liebscher (1996) and the bandwidth conditions. Details are omitted for the sake of brevity, but note that

by assumption (I).

References

-

Andreou, E. & Ghysels, E. (2009) Structural Breaks in Financial Time Series. T. G. Andersen (ed) et al, Handbook of Financial Time Series. Springer, Berlin, 839-870.

-

Bai, J. (1994). Weak convergence of the sequential empirical processes of residuals in ARMA models. Ann. Statist. 22, 2051-2061.

-

Boldin, M. V. (2002). On sequential residual empirical processes in heteroscedastic time series. Math. Methods Statist. 11, 453-464.

-

Csörgö, M., Horváth, L. & Szyszkowicz (1997). Integral tests for suprema of Kiefer processes with application. Statist. Decisions 15, 365-377.

-

Dette, H., Pardo-Fernández, J. C. & Van Keilegom, I. (2009). Goodness-of-Fit Tests for Multiplicative Models with Dependent Data. Scand. J. Statist. 36, 782-799.

-

Doukhan, P. (1994). Mixing, Properties and Examples. Springer, New York.

-

Fan, J. & Yao, Q. (2005). Nonlinear Time Series. Springer, New York.

-

Freedman, D. A. (1975). On tail probabilities for martingals. Ann. Probab. 3, 100-118.

-

Giraitis, L., Leipus, R. & Surgailis, D. (1996) The change-point problem for dependent observations. J. Statist. Plann. Inf. 53, 297-310.

-

Hansen, B. E. (2008). Uniform Convergence Rates for Kernel Estimation with Dependent Data. Econom. Theory 24, 726-748.

-

Hlávka, Z., Hušková, M., Kirch, C. & Meintanis, S. (2012). Monitoring changes in the error distribution of autoregressive models based on Fourier methods. to appear in Test.

-

Horváth, L., Kokoszka, P. & Teyssière, G. (2001). Empirical process of the squared residuals of an ARCH sequence. Ann. Statist. 29, 445-469.

-

Hušková, M. & Antoch, J. (2003). Detection of structural changes in regression. Tatra Mt. Math. Publ. 26, 201-215.

-

Hušková, M., Prášková, Z. & Steinebach, J. (2007). On the detection of changes in autoregressive time series. I. Asymptotics. J. Statist. Plann. Inference 137, 1243-1259.

-

Hušková, M., Kirch, C., Prášková, Z. & Steinebach, J. (2008). On the detection of changes in autoregressive time series. II. Resampling. J. Statist. Plann. Inference 138, 1697-1721.

-

Inoue, A. (2001). Testing for distributional change in time series. Economet. Theory 17, 156-187.

-

Kirch, C. & Tadjuidje Kamgaing, J. (2012). Testing for parameter stability in nonlinear autoregressive models. J. Time Ser. Anal., to appear.

-

Koul, H. L. (1996). Asymptotics of some estimators and sequential residual empiricals in nonlinear time series. Ann. Statist. 24, 380-404.

-

Koul, H. L. (2002). Weighted Empirical Processes in Dynamic Nonlinear Models (Second Edition). Springer, New York.

-

Kreiß, J.-P. (1991). Estimation of the distribution function of noise in stationary processes. Metrika 38, 285-297.

-

Lee, S. & Na, S. (2004). A nonparametric test for the change in the density function in strong mixing processes. Statist. Prob. Letters 66, 1-25.

-

Liebscher, E. (1996). Strong convergence of sums of -mixing random variables with applications to density estimation. Stochastic Processes and their Applications 65, 69-80.

-

Müller, U. U., Schick, A. & Wefelmeyer, W. (2009). Estimating the innovation distribution in nonparametric autoregression. Probab. Theory Relat. Fields 144, 53-77.

-

Neumeyer, N. & Van Keilegom, I. (2009). Change-Point Tests for the Error Distribution in Nonparametric Regression. Scand. J. Statist. 36, 518-541.

-

Picard, D. (1985). Testing and estimating change-points in time series. Adv. Appl. Probab. 17, 841-867.

-

Pollard, D. (1990). Empirical Processes: Theory and Applications. NSF-CBMS Regional Conference Series in Probability and Statistics 2, Institute of Mathematical Statistics.

-

Selk, L. (2011). Change-Point-Tests für die Innovationenverteilung in nichtparametrischen Autoregressionsmodellen auf Basis sequentieller empirischer Prozesse. PhD thesis (in German), Universität Hamburg. http://ediss.sub.uni-hamburg.de/volltexte/2011/5338/

-

Shao, X. & Zhang, X. (2010). Testing for Change Points in Time Series. J. Amer. Statist. Assoc. 105, 1228-1240.

-

Shorack, G. R. & Wellner, J. A. (1986). Empirical Processes with Applications ot Statistics. Wiley, New York.

-

Shumway, R. H. & Stoffer, D.S. (2006). Time Series Analysis and Its Applications: With R Examples. Springer, New York.

-

van der Vaart, A. W. & Wellner, J. A. (1996). Weak Convergence and Empirical Processes. Springer, New York.