Discussion: Latent variable graphical model selection via convex optimization

doi:

10.1214/12-AOS98410.1214/11-AOS949

and

Recently there has been an increasing interest in the problem of estimating a high-dimensional matrix that can be decomposed in a sum of a sparse matrix (i.e., a matrix having only a small number of nonzero entries) and a low rank matrix . This is motivated by applications in computer vision, video segmentation, computational biology, semantic indexing, etc. The main contribution and novelty of the Chandrasekaran, Parrilo and Willsky paper (CPW in what follows) is to propose and study a method of inference about such decomposable matrices for a particular setting where is the precision (concentration) matrix of a partially observed sparse Gaussian graphical model (GGM). In this case, is the inverse of the covariance matrix of a Gaussian vector extracted from a larger Gaussian vector with sparse inverse covariance matrix. Then it is easy to see that can be represented as a sum of a sparse precision matrix corresponding to the observed variables and a matrix with rank at most , where is the dimension of the latent variables . If is small, which is a typical situation in practice, then has low rank. The GGM with latent variables is of major interest for applications in biology or in social networks where one often does not observe all the variables relevant for depicting sparsely the conditional dependencies. Note that formally this is just one possible motivation and mathematically the problem is dealt with in more generality, namely, postulating that the precision matrix satisfies

| (1) |

with sparse and low-rank , both symmetric matrices. A small amendment to that inherited from the latent variables motivation is that is assumed negative definite (in our notation, corresponds to in the paper). We believe that this is not crucial and all the results remain valid without this assumption.

CPW propose to estimate the pair from a -sample of by the pair obtained by minimizing the negative log-likelihood with mixed and nuclear norm penalties; cf. (1.2) of the paper. The key issue in this context is identifiability. Under what conditions can we identify and separately? CPW provide geometric conditions of identifiability based on transversality of tangent spaces to the varieties of sparse and low-rank matrices. They show that, under these conditions, with probability close to 1, it is possible to recover the support of , the rank of and to get a bound of order on the estimation errors and . Here, is the dimension of and and stand for the componentwise -norm and the spectral norm of a matrix, respectively.

Overall, CPW pioneer a hard and important problem of high-dimensional statistics and provide an original solution both in the theory and in numerically implementable realization. While being the first work to shed light on the problem, the paper does not completely raise the curtain and several aspects still remain to be understood and elucidated.

The nature of the results

The most important problem for current applications appears to be the estimation of or the recovery of its support. Indeed, the main interest is in the conditional dependencies of the coordinates of in the complete model and this information is carried by the matrix . In this context, is essentially a nuisance, so that bounds on the estimation error of and the recovery of the rank of are of relatively moderate interest. However, mathematically, the most sacrifice comes from the desire to have precise estimates of . Indeed, if and denote the empirical and population covariance matrices, the slow rate comes from the bound on in Lemma 5.4, that is, from the stochastic error corresponding to . Since the sup-norm error is of order , can we get a better rate when solely focusing on ?

Extension to high dimensions

The results of the paper are valid and meaningful only when . However, for the applications of GGM, the case is the most common. A key question is whether the restriction is intrinsic, that is, whether it is possible to have results on in model (1) when . Since the traditional model with sparse component alone is still tractable when , a related question is whether introducing the model (1) with two components and estimating both and gives any improvement in the setting as compared to estimation in the model with a sparse component alone. A small simulation study that we provide below suggests that already for including the low-rank component in the estimator may yield no improvement as compared to traditional sparse estimation without the low-rank component, although this low-rank component is effectively present in the model.

Optimal rates

The paper obtains bounds of order on the estimation errors and with probability . Can we achieve a better rate than when solely focusing on the recovery of with the usual probability for some ? Is the rate optimal in a minimax sense on some class of matrices? Note that one should be careful in defining the class of matrices because in reality the rate is not but rather , where is the spectral norm of depending on . It can be large for large . Surprisingly, not much is known about the optimal rates even in the simpler case of purely sparse precision matrices, without the low-rank component. In this case, RavikumarEtal , cai_etal and sun_zhang provide some analysis of the upper bounds on the estimation error of different estimators and under different sets of assumptions on the precision matrix. All these bounds are of “order” , but again one should be very careful here because of the factors depending on that multiply this rate. In cai_etal , the factor is the squared norm of the precision matrix while in RavikumarEtal , it is the squared degree of the graphical model multiplied by some combinations of powers of matrix norms that are not easy to interpret. The most recent paper sun_zhang obtains the rate , where is the degree of the graph for -bounded precision matrices. An open problem is to find optimal rates of convergence on classes of precision matrices defined via sparsity and low rank characteristics. The same problem makes sense for covariance matrices. Here, some advances have been achieved very recently. In particular, some optimal rates of estimation of low-rank covariance matrices are provided by Lounici .

The assumptions of the paper are stated in terms of some inaccessible characteristics such as and and seem to be very strong. They are in the spirit of the irrepresentability condition for the vector case used to prove model selection consistency of the Lasso. For a given set of data, there is no means to check whether these assumptions are satisfied. What happens when they do not hold? Can we still have some convergence properties under no assumption at all or under weaker assumptions akin to the restricted eigenvalue condition in the vector case?

Choice of the tuning parameters

The choice of parameters ensuring algebraic consistency in Theorem 4.1 depends on various unknown quantities. Proposing a reasonable data-driven selector for (e.g., similarly to GHV12 for the pure sparse setting) would be very helpful for the practice.

Alternative methods of estimation

Constructively, the method of CPW is obtained from the GLasso of FHT by adding a penalization by the nuclear norm of the low-rank component. Similar low-rank extensions can be readily derived from other methods, such as the Dantzig type approach of cai_etal and the regression approach of MB06 , Gir08 . Consider a Gaussian random vector with mean 0 and nonsingular covariance matrix . Let be the precision matrix. We assume that is of the form (1) where is sparse and has low rank.

(a) Dantzig type approach. In the spirit of cai_etal , we may define our estimator as a solution of the following convex program:

| (2) |

where is the nuclear norm, and are tuning constants. Here, the nuclear norm is a convex relaxation of the rank of .

(b) Regression approach. The regression approach MB06 , Gir08 is an alternative point of view for estimating the structure of a GGM. In the pure sparse setting, some numerical experiments VillersEtal suggest that it may be more reliable than the -penalized log-likelihood approach. Let denote the diagonal of square matrix and its Frobenius norm. Defining

we have , where is the identity matrix and is the diagonal matrix with diagonal elements for . Thus, we have the decomposition

Note that and the nondiagonal elements of matrix are nonzero only if is nonzero. Therefore, recovering the support of and is equivalent to recovering the support of and .

Now, we estimate from an -sample of represented as an matrix . Noticing that the sample analog of is and using the decomposition , we arrive at the following estimator:

| (3) |

where are positive tuning constants and . Note that here the low-rank shrinkage is driven by the nuclear norm rather than by . The convex minimization in (3) can be performed efficiently by alternating block descents on the off-diagonal elements of , the matrix and the diagonal of . The off-diagonal support of is finally estimated by the off-diagonal support of .

Numerical experiment

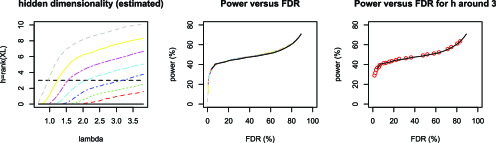

A sparse Gaussian graphical model in is generated randomly according to the procedure described in Section 4 of GHV12 . A sample of size is drawn from this distribution and is obtained by hiding the values of 3 variables. These 3 hidden variables are chosen randomly among the connected variables. The estimators defined in (3) are then computed for a grid of values of and . The results are summarized in Figure 1 (average over 100 simulations).

References

- (1) {barticle}[mr] \bauthor\bsnmCai, \bfnmTony\binitsT., \bauthor\bsnmLiu, \bfnmWeidong\binitsW. and \bauthor\bsnmLuo, \bfnmXi\binitsX. (\byear2011). \btitleA constrained minimization approach to sparse precision matrix estimation. \bjournalJ. Amer. Statist. Assoc. \bvolume106 \bpages594–607. \biddoi=10.1198/jasa.2011.tm10155, issn=0162-1459, mr=2847973 \bptokimsref \endbibitem

- (2) {barticle}[auto:STB—2012/06/01—15:11:24] \bauthor\bsnmFriedman, \bfnmJ.\binitsJ., \bauthor\bsnmHastie, \bfnmT.\binitsT. and \bauthor\bsnmTibshirani, \bfnmR.\binitsR. (\byear2007). \btitleSparse inverse covariance estimation with the graphical Lasso. \bjournalBiostatistics \bvolume9 \bpages432–441. \bptokimsref \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmGiraud, \bfnmChristophe\binitsC. (\byear2008). \btitleEstimation of Gaussian graphs by model selection. \bjournalElectron. J. Stat. \bvolume2 \bpages542–563. \biddoi=10.1214/08-EJS228, issn=1935-7524, mr=2417393 \bptokimsref \endbibitem

- (4) {barticle}[auto:STB—2012/06/01—15:11:24] \bauthor\bsnmGiraud, \bfnmC.\binitsC., \bauthor\bsnmHuet, \bfnmS.\binitsS. and \bauthor\bsnmVerzelen, \bfnmN.\binitsN. (\byear2012). \btitleGraph selection with GGMselect. \bjournalStat. Appl. Genet. Mol. Biol. \bvolume11 \bpages1–50. \bptokimsref \endbibitem

- (5) {bmisc}[auto:STB—2012/06/01—15:11:24] \bauthor\bsnmLounici, \bfnmK.\binitsK. (\byear2012). \bhowpublishedHigh-dimensional covariance matrix estimation with missing observations. Available at arXiv:\arxivurl1201.2577. \bptokimsref \endbibitem

- (6) {barticle}[mr] \bauthor\bsnmMeinshausen, \bfnmNicolai\binitsN. and \bauthor\bsnmBühlmann, \bfnmPeter\binitsP. (\byear2006). \btitleHigh-dimensional graphs and variable selection with the lasso. \bjournalAnn. Statist. \bvolume34 \bpages1436–1462. \biddoi=10.1214/009053606000000281, issn=0090-5364, mr=2278363 \bptokimsref \endbibitem

- (7) {barticle}[mr] \bauthor\bsnmRavikumar, \bfnmPradeep\binitsP., \bauthor\bsnmWainwright, \bfnmMartin J.\binitsM. J., \bauthor\bsnmRaskutti, \bfnmGarvesh\binitsG. and \bauthor\bsnmYu, \bfnmBin\binitsB. (\byear2011). \btitleHigh-dimensional covariance estimation by minimizing -penalized log-determinant divergence. \bjournalElectron. J. Stat. \bvolume5 \bpages935–980. \biddoi=10.1214/11-EJS631, issn=1935-7524, mr=2836766 \bptokimsref \endbibitem

- (8) {bmisc}[auto:STB—2012/06/01—15:11:24] \bauthor\bsnmSun, \bfnmT.\binitsT. and \bauthor\bsnmZhang, \bfnmC. H.\binitsC. H. (\byear2012). \bhowpublishedSparse matrix inversion with scaled lasso. Available at arXiv:\arxivurl1202.2723. \bptokimsref \endbibitem

- (9) {barticle}[mr] \bauthor\bsnmVillers, \bfnmFanny\binitsF., \bauthor\bsnmSchaeffer, \bfnmBrigitte\binitsB., \bauthor\bsnmBertin, \bfnmCaroline\binitsC. and \bauthor\bsnmHuet, \bfnmSylvie\binitsS. (\byear2008). \btitleAssessing the validity domains of graphical Gaussian models in order to infer relationships among components of complex biological systems. \bjournalStat. Appl. Genet. Mol. Biol. \bvolume7 \bpagesArt. 14, 36. \biddoi=10.2202/1544-6115.1371, issn=1544-6115, mr=2465331 \bptokimsref \endbibitem