Approximation Multivariate Distribution with pair copula Using the Orthonormal Polynomial and Legendre Multiwavelets basis functions

Abstract

In this paper, we concentrate on new methodologies for copulas introduced and developed by Joe, Cooke, Bedford, Kurowica, Daneshkhah and others on the new class of graphical models called vines as a way of constructing higher dimensional distributions. We develop the approximation method presented by Bedford et al (2012) at which they show that any -dimensional copula density can be approximated arbitrarily well pointwise using a finite parameter set of 2-dimensional copulas in a vine or pair-copula construction. Our constructive approach involves the use of minimum information copulas that can be specified to any required degree of precision based on the available data or experts’ judgements. By using this method, we are able to use a fixed finite dimensional family of copulas to be employed in a vine construction, with the promise of a uniform level of approximation.

The basic idea behind this method is to use a two-dimensional ordinary polynomial series to approximate any log-density of a

bivariate copula function by truncating the series at an appropriate point. We present an alternative approximation of the multivariate distribution of interest by considering orthonormal polynomial and Legendre multiwavelets as the basis functions. We show the derived approximations are more precise and computationally faster with better properties than the one proposed by Bedford et al. (2012). We then apply our method to modelling a dataset of Norwegian financial data that was previously analysed in the series of papers, and finally compare our results by them.

Keyword: copula, entropy, expert judgement, information, Legendre multiwavelets, orthonormal polynomial series, pair-copula construction, uncertainty modelling, vine

1 Introduction

Bedford and Cooke (2001, 2002) introduce a probabilistic construction of multivariate distributions based on the simple graphical model called vine. This model represents an entirely new approach of building complicated multivariate and highly dependent models which can be seen as the classical hierarchical modelling. The principle behind the vine construction is to model dependency using simple local building blocs based on conditional independence (e.g. cliques in random fields). Aas et al (2009) called these building blocs, pair-copulae. They use the pair-copula decomposition of a general multivariate distribution and propose a method to perform inference.

They investigate modelling complicated high-dimensional data by fitting different parametric bivariate copulas to construct the corresponding pair-copula model. However, there is a huge number of parametric bivariate copulas, but it is well known that building higher-dimensional copulae is generally a difficult problem, and choosing a parametric family for the given higher-dimensional copula is rather more difficult and limited (see Embrechts et al., 2003). As a result, the problem of choosing a parametric copula for a higher-dimensional copula is reduced to fitting a parametric bivariate copulas to data. Bedford et al. (2012) stated that the use of a copula to model dependency is simply a translation of one difficult problem into another: instead of the difficulty of specifying the full joint distribution we have the difficulty of specifying the copula. The main advantage is the technical one that copulas are normalized to have support on the unit square and uniform marginal distributions. Therefore, the potential flexibility of the copula, by restricting them to a particular parametric class (e.g., Gaussian, multivariate -student, etc) is not realized in practice.

To overcome this difficulty, Bedford et al (2012) proposed an alternative approach at which a vine structure can be used to approximate any given multivariate copula to any required degree of approximation. This method can be easily implemented in practice. It is only required to assume that the multivariate copula density of interest must be continuous and non-zero.

This method is constructive and involves the use of minimum information copulas that can be determined to any required degree of precision based on the available data or expert judgements. It can be shown that good approximation ‘locally’ guarantees good approximation globally. It can be shown hat a vine structure imposes no restrictions on the underlying joint probability distribution it represents (Bedford et al., 2012). Furthermore, Kurowicka and Joe (2011) reported that this is essential to address this question that which vine structure is most appropriate where some structures allow the use of less complex conditional copulas than others. Conversely, if we only allow certain families of copulas then one vine structure might fit better than another. This question is still open and under study, and is beyond the scope of this paper.

Thus, it is trivial to show that if there is any difficulty to fit a multivariate distribution by a pair-copulae model, then the problem is not related to the vine structure but the copulae/conditional copulae. As a result, the question “does a vine structure fit” only makes sense in the context of a given family of copulae. Therefore, we need to have a class of copulae with which we can approximate any given copula to an arbitrary degree.

A natural way to build a minimum information copula or specifying dependency constraints is through the use of moments (Bedford, 2006). These can be specified either on the copula or on the underlying bivariate density. We follow Bedford et al. (2012) to consider the moment constraints in which real-valued functions are required to take expected values , respectively. We then fit a minimum information copula that satisfies a set of constraints as above and which has minimum information (with respect to the uniform copula ) amongst the class of all copulas satisfying those constraints. It is trivial to show that this copula is the “most independent” bivariate density that satisfies these constraints. In addition, a specification of minimum information bivariate copulas naturally leads us to the minimum information vine distributions. Particularly, it can be shown that if a minimal information copula satisfied each of the (local) constraints (on moments, rank correlation, etc.), then the resulting joint distribution would also be minimally informative given those constraints (see Kurowicka and Cooke, 2006).

In order to calculate the minimum information copula associated with the constraints mentioned above, an iterative numerical method called algorithm is used by Bedford and Meeuwissen (1997). The number and type of the real-valued functions can control the accuracy of the approximation approach and the cost of computation. Bedford et al (2012) develop this method by using the ordinary polynomial bases to approximate a multivariate distribution of interest.

The main objective of this paper is to improve the density approximation proposed by Bedford et al (2012) by considering several other bases including orthonormal polynomial series and Legendre multiwavelets, and examine their properties and possible applications. By using orthonormal polynomial basis functions the accuracy of approximation will be increased and the computation cost will be considerably decreased. We will show that orthonormal polynomial bases are more convenient than the other natural bases (e.g. polynomial series) for the purpose of calculation.

In addition to the orthonormal polynomial bases which exhibits very nice properties and efficient to implement in practice, we can improve the approximation of a multivariate density even further using the wavelets which have been recently used for density estimation. The wavelets have become popular due to their ability to approximate a large class of functions, including those with localized, abrupt variations. However, a well-known attribute of wavelet bases is that they can not be simultaneously symmetric, orthogonal, and compactly supported. Multiwavelets–a more general, vector–valued, construction of wavelets -overcome this disadvantage, making them natural choices for estimating density functions, many of which exhibit local symmetries around features such as a mode. In particular, using Legender multiwavelets as basis functions will improve accuracy of approximation incredibly and the computation cost will be considerably decreased even in comparison of the orthonormal polynomial bases. We show the efficiency of our method using the mentioned bases as above by comparing them with the model developed by Bedford et al. (2012) and the one proposed by Aas et al (2009) for modeling the Norwegian financial data which has been also studied by these authors.

The paper is organised as follows. In Section 2, we introduce the pair-copula decomposition associated with a multivariate distribution of interest. As an example for better understanding, we also present a vine structure regarding the Norwegian financial data in this section. We briefly study the minimum information copula and the approximation approach presented by Bedford et al (2012) in Section 3. In section 4, we develop the minimum information copula based approximation method to estimate corresponding multivariate distribution. We develop this method using orthonormal polynomial series (obtained based on Graham-Schmidt method) and Legender multiwavelets as the basis functions in Section 5. In section 5, we also illustrate how to construct Legender multiwavelets basis. In Section 6, we apply our method based on these new bases to modelling Norwegian Financial returns data. We also exhibit the potential flexibility of our approach by comparing it with the other methods. The future directions of this work and some other conclusions will be given in Section 7.

2 Vine Constructions of multiple dependence

Kurowicka and Cooke (2006) highlighted the point that however, the copula families, such as the exchangeable multivariate Archimedean copula or the nested Archimedean constructions, constitute a huge improvement, but they are still not rich enough to model all possible mutual dependencies amongst the variables. This is also illustrated by Aas et al (2009) and Bedford et al (2012). Therefore, a more flexible structure called pair-copula construction or vine proposed by them which allows for the free specification of copulae and is hierarchical in nature. This modelling structure is based on a decomposition of a multivariate density into a cascade of bivariate copulae.

In other words, a vine associated with variables is a nested set of trees, where the edges of the tree are the nodes of the tree , and each tree has the maximum number of edges. A regular vine on variables is a vine in which two edges in tree are joined by an edge in tree only if these edges share a common node, . There are edges in a regular vine on variables. The formal definition of vine and regular vine can be found in Kurowicka and Cooke (2006). The following theorem expresses a regular vine distribution in terms of its density.

Theorem 1

Let be a regular vine on elements, where is a connected tree with nodes and edges ; for , is a connected tree with nodes . For each edge with conditioned set and conditioning set , let the conditional copula and copula density be and respectively. Let the marginal distributions with densities be given. Then, the vine-dependent distribution is uniquely determined and has a density given by

| (1) |

Proof. See Bedford and Cooke (2001).

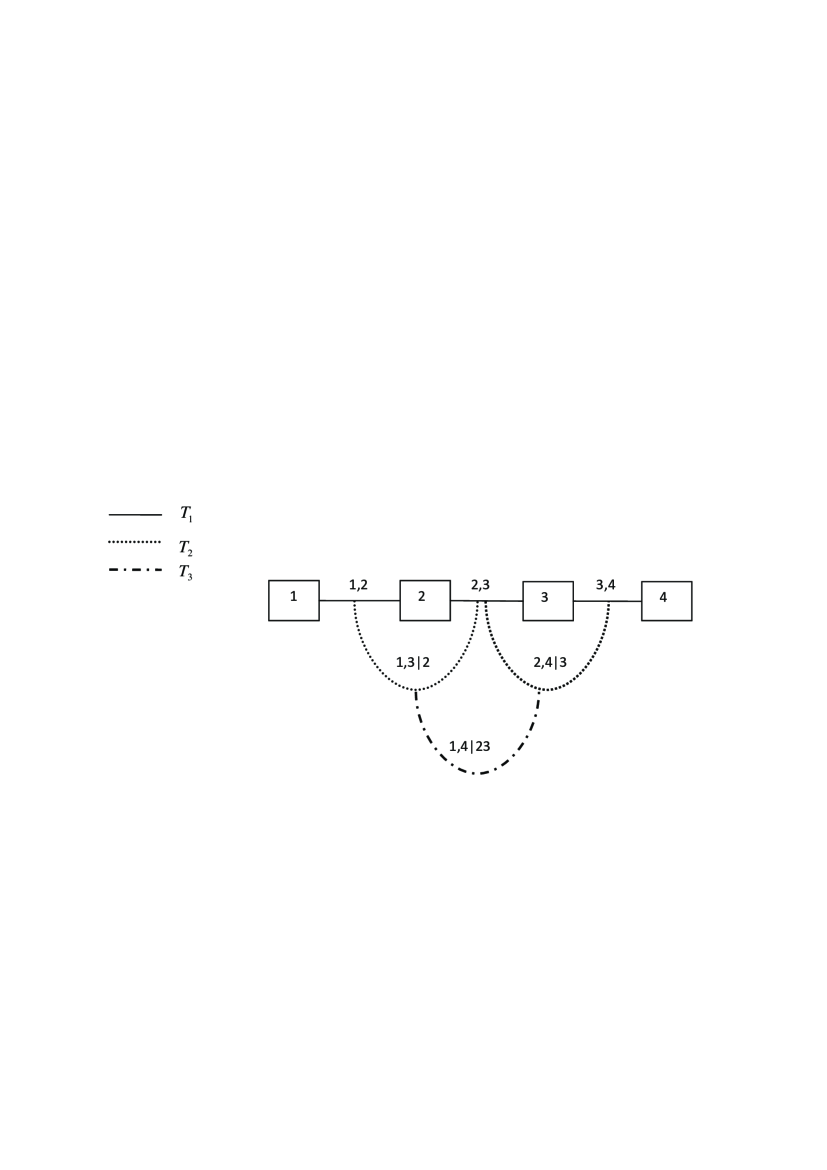

The density decomposition associated with random variables with a joint density function satisfying a copula-vine structure (this structure is called D-vine, see Kurowicka and Cooke, 2006, pp. 93) shown in Figure 1 with the marginal densities is illustrated as follows

| (2) |

It is trivial to show that if is absolutely continuous to product , it then can be represented by any vine-dependent distribution. The existence of regular vine distributions in details is discussed in Bedford and Cooke (2002). We illustrate briefly how such a distribution is determined using the regular vine in Figure 1 as an example. We make use of the expression

The marginal distribution of is known, so we have . The marginals of and are known, and the copula of , is also known, so we can get , and hence . In order to get we can determine in the similar way as . Next we calculate from . With , , and the conditional copula of given we can determine the conditional joint distribution , and hence the conditional marginal . Progressing in this way we obtain . As a result, we can state the following theorem.

Theorem 2

Given a distribution with density function and a vine on elements, there are copulae such that (1) is satisfied, that means

Proof: It is trivial, one should follow the explanation given above to build a 4-dimensional multivariate distribution to prove this theorem. See also Bedford et al. (2012) and references therein.

The above theorem gives us a constructive approach to build a multivariate distribution given a vine structure: If we make choices of marginal densities and copulae then the above formula will give us a multivariate density. Hence vines can be used to model general multivariate densities. However, in practice we have to use copulae from a convenient class, and this class should ideally be one that allows us to approximate any given copula to an arbitrary degree. In the following sections, we address this issue in more detail. By having this class of copulae, we then can approximate any multivariate distribution using any vine structure.

Unlike the situation with Bayesian networks, where not all structures can be used to model a given distribution, the theorem shows that - in principle - any vine structure may be used to model a given distribution. However, in practice it seems that some vine structures do work better than others, and so this must be a result of restricting to a particular family of copulas. That is, given a family of copulae, some vine structures may give a better degree of approximation than others. In fact, we could say that the question “does a vine structure fit” only makes sense in the context of a given family of copulae.

3 Building bivariate minimum information copulae

This section sets out to show that we can use the minimum information techniques originated from Bedford and Meeuwissen (1997) in conjunction with the observed data or expert elicitation of observables, to define a copula that can be used to build the joint distribution of two random variables. The method that will be described below is based on using the algorithm to determine the copula in terms of potentially asymmetric information about two variables of interests.

3.1 The algorithm and minimum information copula

Bedford and Meeuwissen (1997) applied a so-called algorithm to produce discretized minimally informative copula between two variables with given rank correlation. This approach relies on the fact that the correlation is determined by the mean of the symmetric function . The same approach can be used whenever we wish to specify the expectation of any symmetric function of and (see Bedford, 2006; Lewandowski, 2008).

This method can be developed further using the idea stated in Borwein et al. (1994) which enables us to have asymmetric specifications. In the revised method, we first determine a positive square matrix , also called a kernel, and two diagonal matrices and should be then found in such a way that the following product, is doubly stochastic. The theory can be easily generalised for continuous functions (see Bedford et al, 2012).

Now, suppose there are two random variables and , with cumulative distribution functions and , respectively. These are the variables of interest that we would like to correlate by introducing constraints based on some knowledge about functions of these variables. Suppose there are of these functions, namely , and that we wish either to calculate their mean values in terms of the observed data, or the expert wishes to specify mean values for all these functions, respectively. We can simply specify corresponding functions of the copula variables and , defined by , where , at which we can specify the mean values that these functions should simultaneously take. Further suppose that are linearly independent for . We seek a copula that has these mean values, a problem which is usually either infeasible or under determined. Hence, assuming feasibility for the moment, we also ask that the copula be minimally informative (with respect to the uniform distribution), which guarantees a unique and reasonable solution. We form the kernel

| (3) |

where denote the realization of and the realization of .

For practical implementations, we use the same method as proposed by Bedford et al (2012) to discretize the set of values such that the whole domain of the copula is covered. Thus, the aforementioned kernel becomes a 2-dimensional matrix, and two matrices and should be then determined. As a result, the following product denoted by over becomes a doubly stochastic matrix which represents a discretized copula density.

| (4) |

The algorithm can be used to generate a unique joint density with uniform marginals for each vector . The set of all possible expectation vectors that could be taken by under some probability distribution is convex, and that for every in the interior of that convex set there is a density with parameters for which take these values (see Borwein et al., 1994; and Bedford et al., 2012).

We now explain the iterative algorithm required to approximate the mentioned copula density by this algorithm. Suppose that both are discretized into points, respectively as , and . Then, we write , where , , . We define the doubly stochastic matrix, with the uniform marginals as follows

The idea behind of algorithm is very simple which starts with arbitrary positive initial matrices for and , and the new vectors will then be successively defined by iterating the following maps

It can be shown that this iteration scheme converges geometrically to the requested vectors (see Borwein et al., 1994).

Note that to compare different discretizations (for different ) we should multiply each cell weight by as this quantity approximates the continuous copula density with respect to the uniform distributions.

The mapping from the set of vectors of ’s onto the set of vectors of resulting expectations of functions has to be found numerically. Bedford and Daneshkhah (2010) and Bedford et al (2012) proposed the optimization techniques to determine the ’s and corresponding copula. The expectations of functions of variables and are given by

We now wish to determine the appropriate set of ’s for given expectations , where the expectations have been calculated using the discrete copula density given in (4). Hence, to determine ’s satisfying the constraints, the following set of equations has to be solved

| (5) |

The left hand sides of the above equations are just functions of ’s and with optimization algorithms their roots can be found. One of the possible solvers for this task would be FSOLVE - MATLAB’s optimization routine. An alternative method is to use another MATLAB’s optimization procedure called FMINSEARCH, which implements the Nelder-Mead simplex method (see Lagarias et al., 1998). The minimized function is then

We refer the interested reader to Lewandowski (2008) and Bedford et al (2012) to show how an expert could specify a copula though defining expected values.

4 Approximating Multivariate Density by Vine

In this section, we use techniques from approximation theory to show that any -dimensional multivariate density which is (that is, twice differentiable, with continuous second derivatives) can be approximated arbitrarily well pointwise using a finite parameter set of 2-dimensional copulas in a vine construction. The basic idea is that we can use a series expansion, like a two-dimensional Polynomial series, orthonormal Polynomial series or Legender multiwavelets, to approximate any log-density function by truncating the series at an appropriate point. What is non-trivial, however, about this method, is that the same truncation can be used everywhere in a vine construction and gives overall uniform pointwise approximation. Hence our method allows the use of a fixed finite dimensional family of copulas to be used in a vine construction, with the promise of a uniform level of approximation. Since the approximations we make of copula densities might not be quite copula densities themselves, we need to transform them to make them copulas.

To demonstrate this, we first should show that the family of bivariate (conditional) copula densities contained in a given multivariate distribution forms a compact set in the space of continuous functions on . Then, it can be shown that the same finite parameter family of copulae can be used to derive a given level of approximation to all conditional copulae simultaneously.

Here, we develop the approximation method used by Bedford et al. (2012) to approximate any log-density function at the desired level of approximation which is more accurate and exhibits better properties. We first introduce some notations. The basic assumption is that all densities are continuous. We denote as the space of continuous real valued functions on a space , where for some , and the corresponding norm on is given by

The set of all possible 2-dimensional (conditional) copulae is denoted by

where is the copula of the conditional density of given .

The famous Arzela-Ascoli theorem can be used to check the compactness of the following function space, . This space is relatively compact if the functions in are equicontinuous and pointwise bounded.

It can be shown that the following two spaces are relatively compact (Bedford et al. (2012), Theorem 3).

and

where is the conditional density of given , and is the conditional density of given .

It is then straightforward to show that the set is relatively compact. In addition, since all the functions in are positive and uniformly bounded away from 0, the set is also relatively compact (see Bedford et al. (2012) for details and proofs).

As a result, the set can be considered as a vector space, and in this context a base is simply a sequence of functions such that any function can be written as . In other words, it can be shown that given , there is a such that any member of (or can be approximated to within error by a linear combination of . There are lots of possible bases, for example, the following polynomial series

which was mainly used in Bedford et al. (2012).

In the next section, we will improve this density approximation based on the minimum information techniques considerably using the orthonormal polynomial series and Legender multiwavelets instead the ordinary polynomial series as the basis functions. We also exhibit other nice properties of these approximations.

It should be noticed that the approximated copula density by the method described above might not be a copula density itself. Therefore,

the resulting approximation needs to be transformed in such a way to obtain a copula. This can be done by

weighting the approximated density. One of the most effective weighting

schemes is the algorithm mentioned in the previous section. If we have a continuous positive

real valued function on then there are continuous positive functions and ,

such that is a copula density, that is, it has uniform marginal distributions. This density is called

-Projection of and denoted by . Bedford et al (2012) present the following

lemma at which it allows us to control the error made when approximating a copula by another function.

Lemma 1

Let be a non-negative continuous copula density. Given there is a such that if then .

Note that these reweighting functions have the same differentiability properties as the function being reweighted. This can be seen from the integral equation that they satisfy:

Eventually, the term given in (1) can be used to see that good approximation of each conditional copula would result in a good approximation of the multivariate density of interest.

5 Building approximations using minimally informative distributions

In this section, we give practical guide to build a minimally - informative vine structure to approximate any multivariate distribution. In the previous section, we present a method proposed by Bedford et al. (2012) that all conditional copulae can be approximated using linear combinations of basis functions. In this section, we are going to address the issue of how the appropriate parameter values can be chosen. We also introduce a practical and efficient alternative based on using the minimum information criterion that lies very close to the approach described above. In other words, given the basis functions , we seek values so that is close to the approximated copula density. This can be done by fitting the moments of in the minimum information framework. Therefore, if , we seek for the minimum information copula density that also has these moments. This copula density can uniquely be determined, using the algorithm, as follows

As mentioned above, a multivariate distribution can be modelled by a vine structure where it can be defined as a decomposition of the given multivariate distribution into certain conditional copulae, associated with the conditioned and conditioning sets of the vine. The following algorithm is summarised the steps to approximate the given multivariate distribution associated with a vine structure:

-

1.

Specify a basis family, denoted by

-

2.

Specify a vine structure

-

3.

For each part of vine, the bivariate copulae, specify either

-

•

mean for on each pairwise copula;

-

•

functions for the mean values as functions of the conditioning variables, for .

-

•

One of the main aspect that would effect the aforementioned approximation is the basis family. Here, we examine the impact of two basis families, the orthonormal polynomial series and Legender multiwavelets on approximating the minimum information copulae and the multivariate distribution associated with the chosen vine structure. We first briefly introduce these two basis functions.

5.1 Constructing Orthonormal Polynomial base

In mathematics, particularly numerical analysis, a basis function is an element of the basis for a function space. The term is a degeneration of the term basis vector for a more general vector space; that is, each function in the function space can be represented as a linear combination of the basis functions. We say two polynomial functions and are orthonormal polynomial in the interval , if

| (6) |

Orthonormal polynomial base can be more convenient than some natural basis for the purpose of calculation. In fact, if the basis is an orthonormal polynomial basis, adding a new item to the expansion does not change coefficient of the already found shorter expansion (Gui, 2009). But if the basis is not orthonormal, any new item has in general nonzero projection on previous items. It means that the already found coefficients of the expansion would have to be changed. That is one of the reason we use orthonormal polynomial basis functions as the basis family, . It is reasonable to consider Gram-Schmidt orthonormal polynomial basis which is one of the famous orthonormal polynomial basis functions on .

To construct this orthonormal polynomial basis over the interval , we use the Gram-Schmidt process as follows.

The first few functions are

5.2 Constructing Legender Multiwavelets base

The use of wavelets for density estimation has recently gained in popularity due to their ability to approximate a large class of functions, including those with localized, abrupt variations. However, a well-known attribute of wavelet bases is that they can not be simultaneously symmetric, orthogonal, and compactly supported. Therefore, a more general, vector-valued, construction of wavelets is proposed by Locke and Peter (2012) to overcome this disadvantage, and making them natural choices for estimating density functions, many of which exhibit local symmetries around features such as a mode. Locke and Peter (2012) introduce the methodology of wavelet density estimation using multiwavelet bases and illustrate several empirical results where multiwavelet estimators outperform their wavelet counterparts at coarser resolution levels.

In this section, we use the multiwavelet bases to approximate the minimum information copula. The main advantage of using these bases over the polynomial bases introduced in the previous subsection is that the wavelets (and in particular, multiwavelets) are are better choices where the functions of interest contain discontinuities and sharp spikes. In addition, in order to preserve the orthonormality property among the multiwavelet bases, we use Legender multiwavelet bases.

In order to construct these bases, we need to introduce some notions and definitions which are briefly described in the following subsections.

5.2.1 Multiresolution analysis

Wavelet theory is based on the idea of multiresolution analysis (MRA). Usually it is assumed that an MRA is generated by one scaling function, and dilates and translates of only one wavelet form a stable basis of .

We can generate a reference subspace or sample space as -closure of the linear span of the integer translation of the following functions , namely

and consider subspace

where

Now, we are able to present a proper definition of multiresolution analysis as follows.

Definition 1: Functions , are said to generate a multiresolution analysis (MRA) if they generate a nested sequence of closed subspaces that satisfies

| (7) |

If generates an MRA, then are called scaling functions. In case that the different integer translate of are orthogonal (with respect to the standard linear product ) for two functions in , denoted by for the scaling functions are called an orthogonal scaling functions.

As the subspaces are nested, there exist complementary orthogonal subspaces such that

here and in the following denotes orthogonal sums.

This yields an orthogonal decomposition of , namely;

Definition 2: Functions are called wavelets, if they generate the complementary orthogonal subspaces of a MRA, i.e.,

where

Obviously, for , and , if

,

then are called orthogonal wavelets, where

Now, we are able to define Legender scaling functions and its corresponding multiwavelets according to MRA definition give above.

5.2.2 Construction of Scaling Functions

Legendre multiwavelets system with multiplicity consists of scaling functions and wavelets. The -th order Legendre scaling functions are the set of functions where is a polynomial of -th order and all ’s form orthogonal basis (Shamsi and Razzaghi, 2005), that is, for

| (8) |

The coefficient are chosen so that , and

| (9) |

The scaling functions have symmetry, anti-symmetry properties for odd or even , respectively. The two-scale relations for Legendre scaling functions of order , are in the form (Albert et al., 2002);

| (10) |

The coefficients determined uniquely by substituting equation (8) to (10). Now we would like to mention two remarks on the two scale relations.

-

1.

Since is a -th order polynomial, the right hand side of (10) has at most -th order scaling functions. Therefore, for .

-

2.

The two scale relations for the Legendre scaling function of order which is lower than r is a subset of first two-scale relations for for form -th order two scale relations.

5.2.3 Construction of Wavelets

The two-scale relation for the -th order Legendre multiwavelets is given in the following form (Albert et al., 2002):

| (11) |

The unknown coefficients in (11) can be determined in terms of the following vanishing moment conditions (12) and orthongonal conditions (13).

- Vanishing moments

-

(12) - Orthogonality

-

(13)

For example, the Legendre scaling functions of order 5 consist of 6 functions as follows:

| (14) |

6 Application: Norwegian Financial returns

In this section, we apply the approximation method presented in this paper using the basis functions introduced in the previous section as the basis families, (as mentioned in the first step in the algorithm above) to approximate the multivariate

distribution associated with the selected vine structure corresponding to the Norwegian financial returns. We then exhibit the potential flexibility of our approach by comparing it with the other methods cited in Bedford et al. (2012) and Aas et al. (2009).

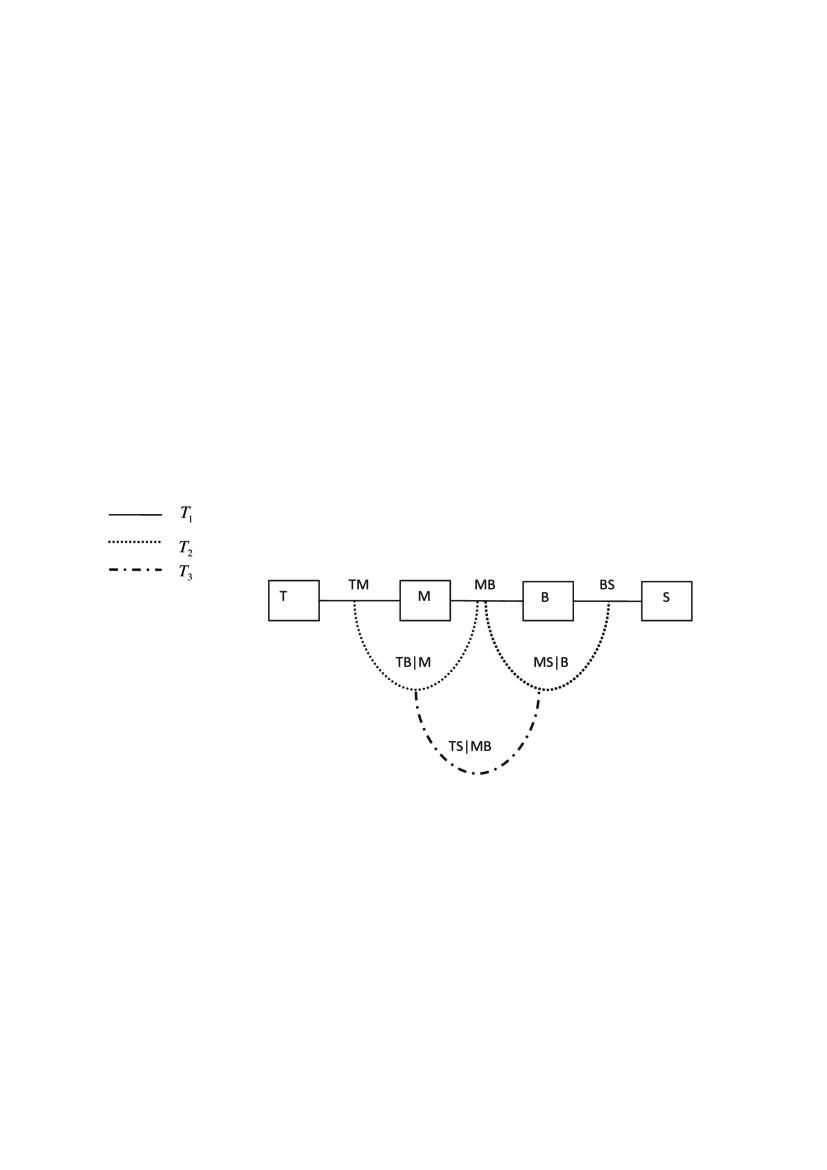

Example: In this example we use the same data set as considered by Aas et al. (2009) and Bedford et al. (2012) to illustrate the approximation method introduced in this paper. The data consists of four time series of daily data: the Norwegian stock index (TOTX), the MSCI world stock index, the Norwegian bond index (BRIX) and the SSBWG hedged bond index. They are recorded over the period 04.01.1999 to 08.07.2003 at which 1094 data are collected. We denote these four variables and , respectively.

We first shall remove serial correlation in these four time series, that is, the observation of each variable must be independent over time. Hence, the serial correlation in the conditional mean and the conditional variance are modeled by an AR(1) and a GARCH(1,1) model (Bollerslev, 1986), respectively. Thus, the following model for log-return is considered for the time series

where (see Aas et al., 2009).

The further analysis is performed on the standardized residuals

. If the AR(1)-GARCH(1,1) models are successful at modeling

the serial correlation in the conditional mean and the conditional

variance, there should be no autocorrelation left in the

standardized residuals and squared standardized residuals. We can use the modified Q-statistic

and the Lagrange multiplier test, respectively, to check this (Aas et al, 2009).

For all series, the null hypothesis that there is no autocorrelation

left for the both tests cannot be rejected at the %5 level. Since, we are mainly interested in estimating the dependence structure of

the risk factor, the standardized residual vectors are converted to

the uniform variables using the kernel method before further

modeling. We denote the converted time series of and by

and , respectively.

Here, we are going to derive the vine approximation fitted to this data set to any given multivariate density using minimum information distribution. We adopt a vine structure to these data, as presented in Figure 2. Note that, the corresponding functions of the copula variables , , and associated with can be derived. For instance, these are defined by and should also have the same specified expectation, that is, . We derive the minimum information copulae calculated in this example based on them the copula variables, . We initially construct minimally informative copulas between each set of two adjacent variables in the first tree, . Therefore, it is essential to decide which bases should be taken and how many discretization points should be used in each case. We start illustrate our procedure for the first copula in the first tree between .

We could simply choose basis functions, starting with simple orthonormal polynomials or Legendre multiwavelets basis, and moving to more complex ones, and include them until we are satisfied with our approximation. We included the following orthonormal polynomial basis functions, constructed using Gram-Schmidt process, in order

and the following Legendre multiwavelets basis functions which is constructed based on the method presented in subsection 5.2

Bedford et al. (2012) show that adding the basis functions in this way is not optimal, and propose a method which is similar to a stepwise regression. In this method, at each stage, we propose to assess the log-likelihood of adding each additional basis function. We then include the function which produces the largest increase in the log-likelihood. At moment, we are investigating some other methods, such as, Genetic, PSO algorithm, Lasso and ant-colony algorithms, to find the most optimal basis functions in a sense that with smaller number of these bases, we would get the largest log-likelihood.

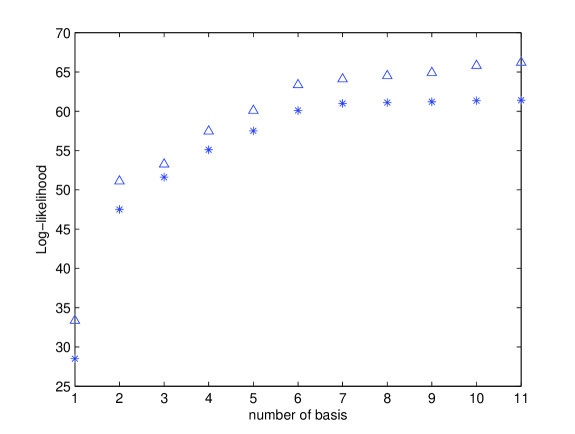

Figure 3 shows the changes of log-likelihood in terms of adding basis functions for orthonormal polynomial () and Legendre multiwavelets (). In order to compare our results with the approximations made in Bedford et al. (2012) using the ordinary polynomial series, we choose six orthonormal basis functions using the stepwise method as follows

and also we choose six Legendre multiwavelet basis functions as follows

The corresponding log-likelihood based on orthonormal plynomial functions reaches to 60.66 and based on Legendre multiwaveletswhich reaches to 63.36 which both are more than the log-likelihood, 58.1256, based on six basis functions calculated in Bedford et al. (2012). The corresponding expectations of the selected orthonormal plynomial basis functions using the Norwegian financial returns data are calculated as

and also for the selected Legendre multiwavelet bases are given by

We now able to construct the minimum information copula with respect to the uniform distributions given the constraints as the selected basis functions reported above by the method described in this paper. We first need to determine the number of discretization points (grid size). It is trivial to conclude that a larger grid size will provide a better approximation to the continuous copula but at the cost of more computation time. Similarly, the approximation will become more precise if we run the algorithm in more iterations. Indeed, this would cost us more computation time. Bedford et al. (2012) show that the number of iterations needed will also depend on the grid size. The considered errors are reported to be in the range to . Thus, the larger the number of grid points used, the larger the number of iterations that are needed for convergence which is true over all error levels. The grid sizes all follow the same pattern with large increases in the number of iterations needed for improved accuracy initially and smaller increases when the error is smaller. We choose a grid size of throughout of this example.

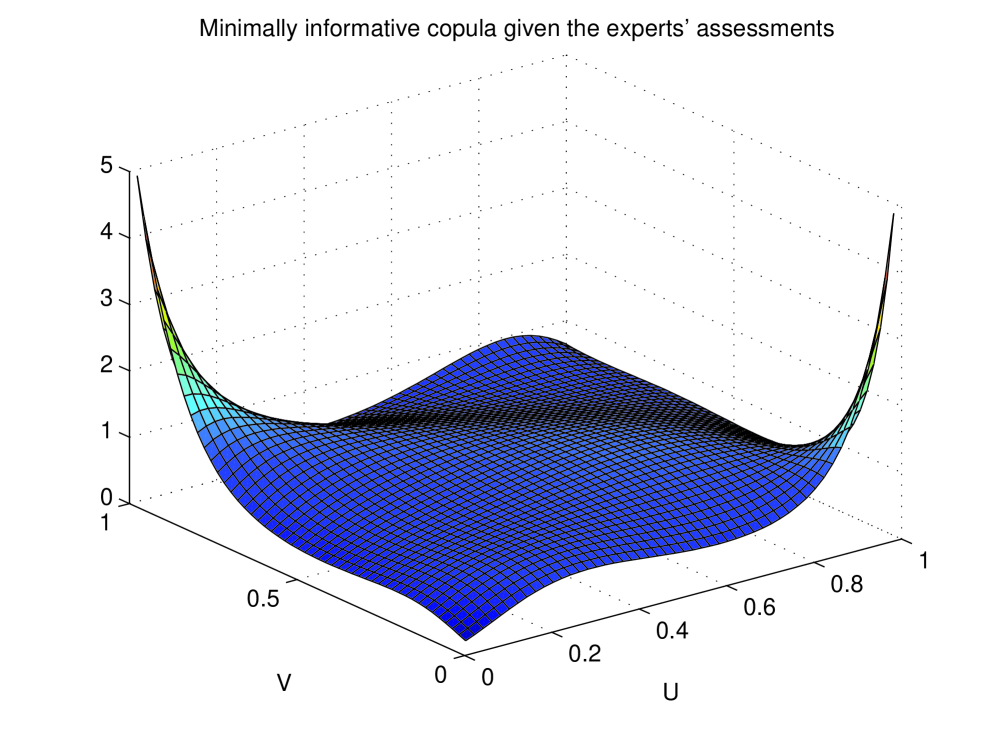

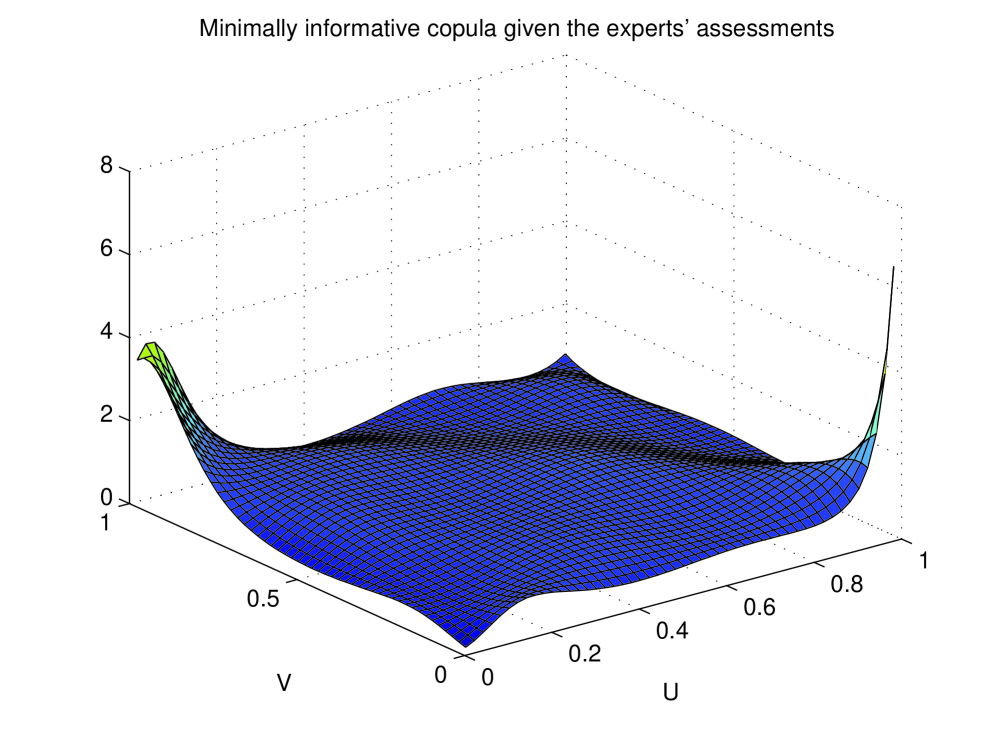

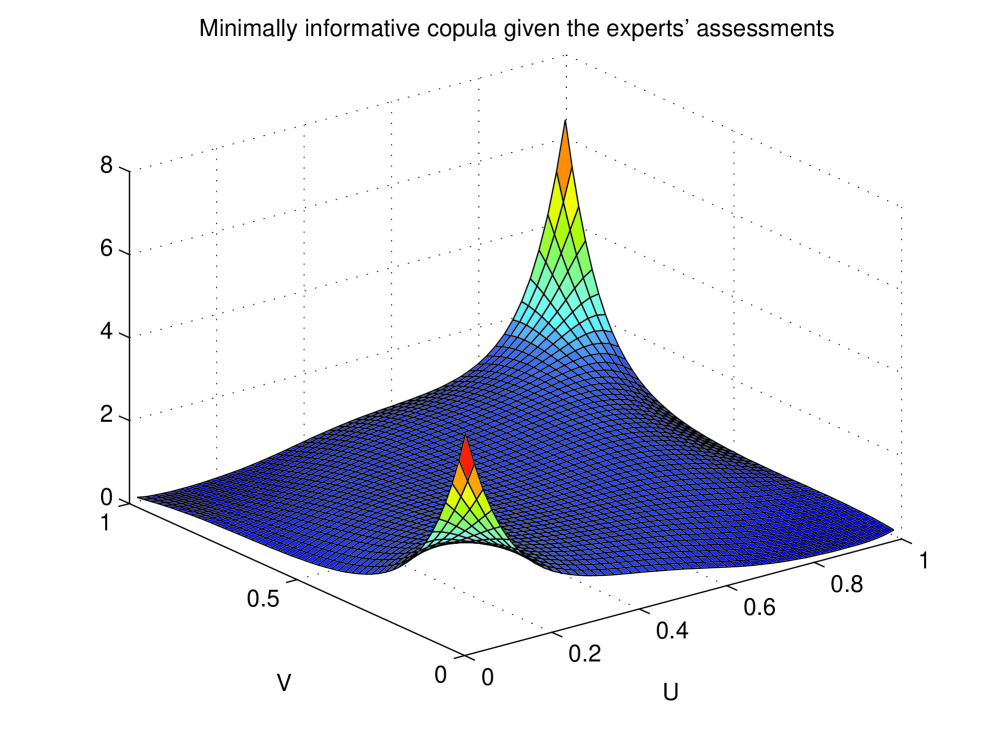

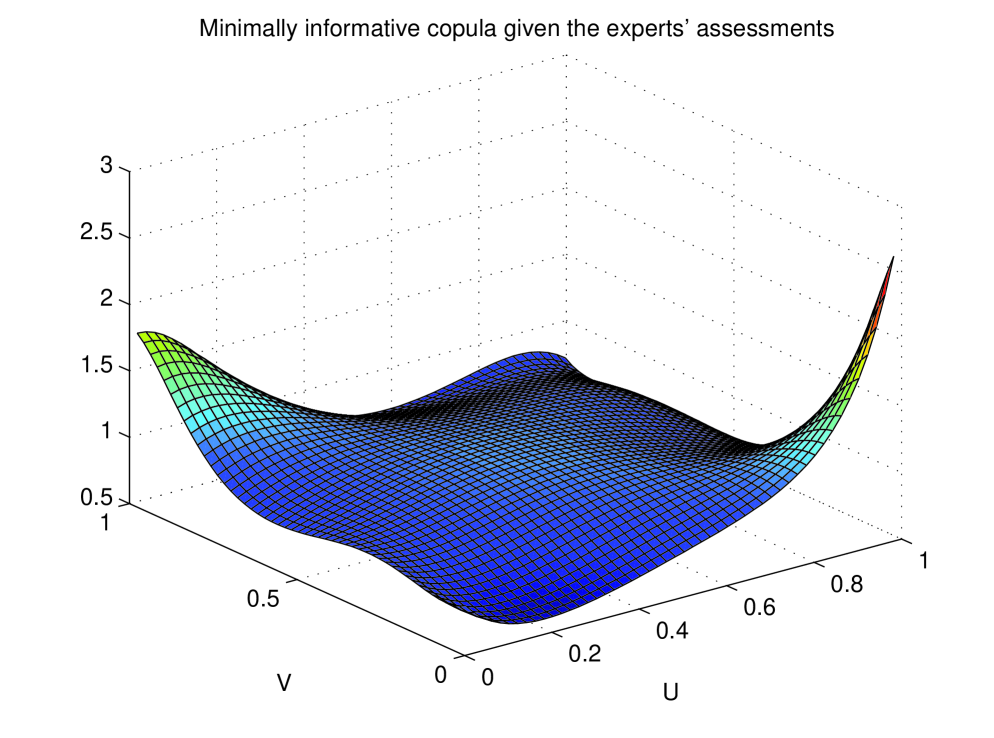

Based on the information given above regarding the grid size, number of iterations and error size, we can derive the minimum information copula associated with the chosen constraints. This copula based on the orthonormal polynomial bases is plotted in Figure 5, and the copula based on the Legendre multiwavelet basis functions is plotted in Figure 5. We present Lagrange multiplies values (or parameter values) for this approximated copula density as follows

and in the similar way these parameter values for the minimum information copula based on the Legendre multiwavelets bases are given by

One of the main advantages of using the orthonormal polynomial and Legendre multiwavelets basis functions over the ordinary polynomial series considered in Bedford et al. (2012) is that the algorithm converges faster using these bases. This is because of the nice property of these two bases that adding a new basis to the kernel defined in (3) and used to construct the minimum information copula, does not change the Lagrange multipliers of the already used in the kernel. This is shown in Table 1 for the orthonorma polynomial basis functions. But, this is not the case when one is applying the ordinary polynomial bases (as proposed by Bedford et al, 2012) to calculate the minimum information copula. In this situation, we need to run the algorithm each time a new base is added to the already chosen bases, and the parameter values are changing accordingly. Therefore, more iterations are required for the algorithm to converge. The optimisation time required for the algorithm using the the orthonormal polynomial bases is only 35.8646 seconds, for Legendre multiwavelets is 29.359 while this time for the ordinary polynomial bases is 72.93 seconds which is almost twofold of the former one and almost two and half times more than the latter one.

| Base | Parameter values | Log-Likelihood |

|---|---|---|

| -0.1995 | 29.36 | |

| Previous one, | -0.1995, 0.1651 | 49.2 |

| Previous one, | -0.1995, 0.1651, 0.0912 | 52.8 |

| Previous basis, | -0.1995, 0.1651, 0.0912, -0.0774 | 56.16 |

| Previous basis, | -0.1995, 0.1651, 0.0912, -0.0774, -0.0772 | 59.04 |

| Previous basis, | -0.1995, 0.1651, 0.0912, -0.0774, -0.0772, 0.0527 | 60.66 |

Furthermore, by comparing the log-likelihoods of the minimum information copulas based on the ordinary polynomial, orthonormal polynomial and Legangre multiwavelets, we can conclude that the latter one produce more reliable copula density approximation in the sense that the corresponding log-likelihood is much larger. We present the log-likelihood of these approximated copulae using the aforementioned bases in Table 2.

| Type of Bases | Number of bases | Log-Likelihood |

|---|---|---|

| Ordinary Polynomial (Bedford et al. 2012) | 6 | 58.1256 |

| Orthonormal polynomial (Subsection 5.1) | 6 | 60.66 |

| Legangre multiwavelets (Subsection 5.2) | 6 | 63.36 |

It should be noticed that the log-likelihood of the approximated copula using only 5 bases of orthonormal polynomial or Legangre multiwavelets is still larger than the fitted copula based on the six ordinary polynomial bases. In addition, we realize that the derived approximated copula in term of the bases proposed in this paper are more flexible than ordinary polynomial bases, since they aren’t sensitive to the initial values chosen for the parameter values (Lagrange multipliers) in the algorithm.

The second copula in the first tree () is . Using the stepwise method, we choose the following orthonormal polynomial bases

and we also select the following Legendre multiwavelets basis functions

We similarly construct the minimally informative copulae associated with the orthonormal polynomial bases which is shown in Figure 7. Note that the minimum information copulas for the orthonormal polynomial and Legendre multiwavelets bases are quite similar, but the figure of later one to some extent is smoother than the former one. The constraints as the mean of the chosen orthonormal polynomial bases for the Norwegian Financial returns data are presented as

The parameter values associated with the fitted minimum information copula to the data with these constraints are given by

The constraints for the Legendre multiwavelets bases are

and the corresponding parameter values are as follows

The log-likelihoods corresponding to the orthonormal polynomial and Legendre multiwavelets bases are 158.0013 and 159.72, respectively, which are again more than the log-likelihood calculated based on the ordinary polynomial bases.

The third marginal copula is between and . Similarly, the six bases are selected using the stepwise procedure, and the corresponding constraints and resulting Lagrange multipliers are given in Table 4 and Table 4 for orthonormal and Legendre multiwavelets, respectively. The approximated minimally informative copula in terms of the orthonormal polynomial bases is shown in Figure 7. Note that the minimum information copula associated with the Legendre multiwavelets bases is very similar to the one given Figure 7, but to some extent is slightly smoother.

| Base | Log- | ||

|---|---|---|---|

| Likelihood | |||

| -0.1557 | -0.1467 | ||

| 0.1010 | 0.0836 | ||

| -0.0510 | -0.0426 | 20.13 | |

| -0.0378 | -0.0365 | ||

| 0.0253 | 0.0257 | ||

| 0.0222 | 0.0240 |

| Base | Log- | ||

|---|---|---|---|

| Likelihood | |||

| 0.4803 | -70.35 | ||

| 0.2298 | 91.72 | ||

| 0.0539 | 16.61 | 25.07 | |

| 0.0531 | -22.29 | ||

| 0.0011 | 2.39 | ||

| -0.0098 | -3.49 |

The conditional copulas in the second tree, can similarly be approximated using the minimum information approach. We only illustrate construction of the conditional minimum informative copula between and , and the other conditional copulas in this tree can be similarly approximated. In order to calculate this copula, we divide the support of into some arbitrary sub-intervals or bins and then construct the conditional copula within each bin. To do so we select bases in the same way as for the marginal copulas and fit the copulae to the calculated mean values or constraints. Here, we use four bins so that the first copula is for . The bases for this copula based on the orthonormal polynomial basis are

and the Legendre multiwavelets bases are also given by

The mean values for orthonormal polynomial basis functions which will constrain the minimum information copula are

and these expectations for Legendre multiwavelets bases are as follows

We can follow this process again for the remaining bins. Tables 5 and 6 show the mean values or constraints (denoted by ) and corresponding Lagrange multipliers () required to build the conditional minimum information copula between and for orthonormal polynomial and Legendre multiwavelets bases, respectively. The log-likelihood of the approximated copula in each bin is also reported in these tables.

| Interval | Bases | Log-Likelihood | ||

|---|---|---|---|---|

| -0.2995 | -0.3511 | |||

| -0.1240 | -0.135 | |||

| -0.1634 | -0.057 | 18.22 | ||

| -0.0317 | 0.0776 | |||

| -0.0585 | -0.0705 | |||

| -0.0630 | 0.001 | |||

| 0.1504 | 0.1902 | |||

| 0.0562 | 0.1051 | |||

| 0.1030 | 0.1363 | 9.05 | ||

| 0.0836 | 0.0944 | |||

| 0.0823 | 0.0804 | |||

| -0.0621 | -0.0094 | |||

| 0.1184 | 0.1679 | |||

| -0.1080 | -0.2311 | |||

| 0.0956 | 0.1459 | 9.74 | ||

| -0.0815 | -0.2047 | |||

| -0.0627 | -0.1869 | |||

| 0.0245 | 0.1253 | |||

| -0.2659 | -0.3177 | |||

| 0.1568 | 0.1135 | |||

| 0.1025 | 0.1290 | 10.53 | ||

| -0.0079 | 0.0526 | |||

| -0.1737 | -0.1007 | |||

| -0.0376 | 0.0456 |

| Interval | Bases | Log-Likelihood | ||

|---|---|---|---|---|

| -0.020 | -2.53 | |||

| -0.021 | 2.17 | |||

| -0.018 | -0.64 | 22.17 | ||

| -0.002 | -3.00 | |||

| -0.004 | 2.35 | |||

| 0.001 | 5.23 | |||

| 0.1504 | 0.226 | |||

| 0.109 | -7.30 | |||

| 0.102 | 9.97 | 12.08 | ||

| 0.056 | -3.31 | |||

| 0.103 | -0.25 | |||

| 0.106 | 10.46 | |||

| 0.118 | -269.93 | |||

| -0.1080 | -439.13 | |||

| -0.102 | 104.95 | 11.30 | ||

| 0.096 | -29.99 | |||

| 0.093 | 373.59 | |||

| 0.059 | -14.53 | |||

| -0.2659 | 247.49 | |||

| 0.1568 | -110.67 | |||

| 0.1025 | -108.01 | 12.86 | ||

| 0.069 | -222.75 | |||

| 0.021 | -175.39 | |||

| 0.063 | -15.69 |

Note that the resulting minimum information copula over all bins for orthonormal polynomial bases is 47.54 and for Legendre multiwavelets is 58.41 while this amount for the ordinary polynomial bases is only 29.242 which indicates superiority of the former bases.

We can obtain the conditional minimum informative copula in the third tree, , similarly by dividing each of the conditioning variables’ supports into four bins. Then the minimum information copulas for and are calculated on each combination of bins for and which makes 16 bins altogether for this tree. The bins, bases and log-likelihoods associated with each copula based on the orthonormal polynomial and Legendre multiwavelets basis are given in Tables 7 and 8, respectively.

| Interval | Bases | Log-Likelihood |

|---|---|---|

| , | 8.93 | |

| , | 7.31 | |

| , | 6.81 | |

| , | 9.65 | |

| , | 8.63 | |

| , | 7.67 | |

| , | 9.5 | |

| , | 5.62 | |

| , | 4.93 | |

| , | 10.49 | |

| , | 8.97 | |

| , | 10.08 | |

| , | 3.7 | |

| , | 8.7 | |

| , | 5.61 | |

| , | 20.24 |

| Interval | Bases | Log-Likelihood |

|---|---|---|

| , | 10.64 | |

| , | 9.42 | |

| , | 13.67 | |

| , | 10.42 | |

| , | 12.99 | |

| , | 15.67 | |

| , | 10.56 | |

| , | 10.77 | |

| , | 9.89 | |

| , | 10.26 | |

| , | 14.01 | |

| , | 17.97 | |

| , | 11.17 | |

| , | 14.31 | |

| , | 10.61 | |

| , | 24.39 |

Thus the log-likelihood of the overall vine, obtained by summing the log-likelihoods of each of the component copulas above, is 388.859.

The log-likelihood of the overall pair-copula model using the orthonormal polynomial (and Legendre multiwavelets) bases, derived by adding the log-likelihoods of the copulas constructed above, is then 434.135 (and this amount for Legendre multiwavelets is 552.25). These values are considerably greater than the log-likelihoods of the fitted pair-copula models to the data using the Gaussian copula, -copula and the approximated pair-copula model using the ordinary polynomial bases.

6.1 Comparison To Other Approaches

In this subsection, we compare our method with the other methods used to approximate the multivariate distribution fitted to the Norwegian financial returns data. In order to make a comparison we compute the log-likelihood of the approximated density function by the method presented in this paper and other approaches reported in Aas et. (2009) and Bedford et. (2012). The log-likelihood of the overall pair-copula model using the orthonormal polynomial and Legendre multiwavelets bases, obtained by adding the log-likelihoods of each of the component copulas presented above, are 434.135 and 552.25, respectively. These values are much greater than that obtained using the -copula examined by Aas et al (2009) of 291.801 and the minimum information copula based on the ordinary polynomial bases of Bedford et al (2012) of 388.859. Note that, if we only use five bases to approximate the multivariate density of interest, the log-likelihoods associated with orthonormal polynomial and Legendre multiwavelets bases will be 429.3982 and 446.235, respectively, which are still clearly better than the model proposed by Bedford et al (2012) based on the six ordinary polynomial bases. We have computed the log-likelihood of the data sample for five different copula models used on the same vine structure: The Gaussian copula, the -copula used by Aas et al. (2009), the minimum information copula using the ordinary polynomial bases presented by Bedford et al. (2012) and our approximated copulas. We illustrate the corresponding results in Table 9.

| Type of copula | Log-Likelihood |

|---|---|

| Gaussian copula (Aas et al. 2009) | 263.5052 |

| copula (Aas et al. 2009) | 291.8014 |

| Minimum information copula based | 388.859 |

| on polynomial basis (Bedford et al., 2012) | |

| Minimum information copula | 434.135 |

| based on orthonormal polynomial | |

| Minimum information copula | 552.25 |

| based on Legendre multiwavelets |

7 Conclusion

In this paper, we extend the novel method originally presented by Bedford et al (2012) to approximate a multivariate distribution by any vine structure to any degree of approximation. The main idea to implement this approximation method is to use the minimum information copulae that can be determined to any required degree of precision based on the data available. To approximate a multivariate distribution by this method, we need to specify: 1) a vine structure; 2) a basis family; 3) for each part of vine, expected values for the certain functions associated with some constraints on each pairwise copula.

Bedford et al (2012) approximate all conditional copulas using linear combinations of the ordinary polynomial basis functions. We make this approximation more precise by choosing more appropriate basis family. We concentrate on the orthonormal polynomial basis functions and Legendre multiwavelets in this paper. The Legendre multiwavelets and orthonormal polynomial basis functions are shown that to be more convenient than some other natural basis for the purpose of calculation. A very nice property of the orthonormal polynomial basis is that adding a new item to the expansion does not change coefficient of the already found shorter expansion which is not the case for the non-orthonormal basis where any new item has in general nonzero projection on previous items. It means that the already found coefficients of the expansion would have to be changed. The Legendre multiwavelets basis, not only has this property, but the computation of the minimum information copula using this basis becomes even faster and the approximation would considerably improve. In other words, applying these basis is so important from three main aspects: firstly, less computation time is required to approximate the minimum information copula of interest; secondly, the fitted models to the data using the minimum information copulas based on the orthonormal polynomial and Legendre multiwavelets bases are better in the sense that their log-likelihoods are much larger than than log-likelihood of the alternative models; thirdly, the approximations made in this paper are robust in the sense that they are not sensitive to the initial values chosen for the parameter values.

In addition to these properties, our method has this property that it can be used to build arbitrarily good approximations to the original distribution. One of the most clear sources of potential error in our approximation is the choice of base where it is convenient to take a low number of functions . The terms chosen in both orthonormal polynomial and Legendre multiwavelets would generate asymmetric copulas which seems to have great impact in modelling general data sets. The use of large numbers of functions does give more accuracy, at the cost of considerable extra computation at the construction stage but at no extra cost at the sampling stage. Indeed, we can approximate the requested model more precisely using less numbers of basis functions proposed in this paper and with smaller computation time than the alternative methods. In fact, the generalization made in this paper gives natural ways to generate asymmetric copulas, and simple ways to specify non-constant conditional correlations (or other moments). At moment, we are investigating some alternative methods to the stepwise method used in this paper to find the most optimal basis functions in a sense that with smaller number of these bases, we would get the largest log-likelihood.

The method used in this paper is very flexible and any functions can be used to construct the minimum information copulas used here. This method can be use for modeling more complex applications at which basis functions should be computed in computer codes. Due to numerous evaluation of these function to construct the minimum information distribution, the computation and then approximation will be infeasible. One suggestion to ease the computation and reduce the complexity of model is to use the Gaussian process emulators.

Acknowledgement: The authors are grateful to Professor Tim Bedford for his helpful comments for some parts of the paper.

References

- [1] Aas, K., Czado, K. C., Frigessi, A., and Bakken, H. (2009). Pair-copula constructions of multiple dependence. Insurance, Mathematics and Economics, 44, 182–198.

- [2] Alpert, B., Beylkin, G., Gines, D., Vozovoi, L. (2002). Adaptive solution of partial differential equations in multiwavelet bases. J. Comput. Phys., 182: 149-190.

- [3] Bedford, T. (2006). Interactive expert assignment of minimally-informative copulae, Management Science Working Paper No. 5.

- [4] Bedford, T. and Cooke. R. M. (2001). Probability density decomposition for conditionally dependent random variables modeled by vines. Annals of Mathematics and Artificial Intelligence 32, 245–268.

- [5] Bedford, T., and Cooke. R. M. (2002). Vines - a new graphical model for dependent random variables. Annals of Statistics, 30(4): 1031–1068. random variables modeled by vines. Annals of Mathematics and Artificial Intelligence 32, 245–268.

- [6] Bedford, T. and Daneshkhah, A. (2010). Approximating Multivariate Distributions with Vines. Submitted to Operation Research.

- [7] Bedford, T. and Daneshkhah, A., Wilson, K. (2012). Approximate Uncertainty Modeling with Vine copulas. Submitted to European Journal of Operation Research.

- [8] Bedford, T., and Meeuwissen, A. (1997). Minimally informative distributions with given rank correlation for use in uncertainty analysis. Journal of Statistical Computation and Simulation, 57(1 - 4): 143 - 174.

- [9] Bollerslev, T. (1986). Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics , 31, 307–327.

- [10] Borwein, J., Lewis, A., and Nussbaum, R. (1994). Entropy minimization, DAD problems, and doubly stochastic kernels. Journal of Functional Analysis, 123, 264-307.

- [11] Embrechts, P., F. Lindskog, and A. J. McNeil. (2003). Modelling Dependence with Copulas and Applications to Risk Management. In Handbook of Heavy Tailed Distributions in Finance. Amsterdam: Elsevier/North-Holland, 31, 307–327.

- [12] Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom. Econometrica, 50(4), 987–1007.

- [13] Gui, W. (2009). Adaptive Series Estimators for Copula Densities. PhD thesis, Florida State University College of Arte and Sciences.

- [14] Joe, H. (1997). Multivariate Models and Dependence Concepts. Chapman & Hall, London.

- [15] Kurowicka, D., and Cooke. R. (2006). Uncertainty Analysis with High Dimensional Dependence Modelling. John Wiley.

- [16] Kurowicka, D. and Joe, H. (2011). Dependence Modeling: Vine Copula Handbook. World Scientific, Singapore.

- [17] Lagarias, J. C., Reeds, J. A., Wright, M. H., and Wright. P. E. (1998). Convergence properties of the Nelder-Mead simplex method in low dimensions. SIAM Journal of Optimization, 9(1): 112–147.

- [18] Lewandowski, D. (2008).High Dimensional Dependence: Copulae, Sensitivity, Sampling. PhD thesis, Delft University.

- [19] Ljung, G. M., and Box, G. E. P. (1978). On a Measure of lack of Fit in Time Series Models. Biometrika, 65(2), 297–303.

- [20] Locke, B., and Peter, A. (2012). Multiwavelet Density Estimation, submitted to Computational Statistics and Data Analysis.

- [21] Shamsi, M., Razzaghi, M. (2005). Solution of Hallen’s Integral Equation Using Multiwavelets,. Computer Physics Communications, 168: 187-197.