Stochastic Stefan Problems Driven By Standard Brownian Sheets

Abstract

In this paper we study the effect of stochastic perturbations on a common type of moving boundary value PDE’s which endorse Stefan boundary conditions, or Stefan problems, and show the existence and uniqueness of the solutions to a number of stochastic equations of this kind. Moreover we also derive the space and time regularities of the solutions and the associated boundaries via Kolmogorov’s Continuity Theorem in an appropriately defined normed space.

The paper first conveys our previous results where randomness is smoothly correlated in space and Brownian in time, then introduces a new methodology that enables us to prove the existence and uniqueness of the solution to the standard heat equation driven by a space-time Brownian sheet as well as its boundary regularity, and finally extends it to the stochastic moving boundary partial PDE’s driven by the same type of randomness.

1 Introduction

An important type of problems in the theory of partial differential equations (PDE’s) is the moving boundary value problems. In this paper we study the effect of stochastic perturbations on such type of problems with Stefan boundary conditions, or Stefan problems, which have various applications in physics, engineering, and finance, and show the existence and uniqueness of the solutions to a number of stochastic equations of such kind. We also obtain the space and time regularities of the solutions and their associated boundaries via Kolmogorov’s Continuity Theorem in a defined normed space.

The paper first conveys our previous results where randomness is smoothly correlated in space and Brownian in time, which has the convenience that the boundary regularity is naturally satisfied, then introduces a new methodology that enables us to prove the existence and uniqueness of the solution to the standard heat equation driven by a space-time Brownian sheet as well as its boundary regularity by defining an appropriate normed space whose norm correctly curvatures both the decay of the solution and its regularity at the boundary, and finally extends it to the stochastic moving boundary partial PDE’s driven by the same type of randomness, where the new normed space is defined essentially in the same manner as enlightened by the previous result.

1.1 Background

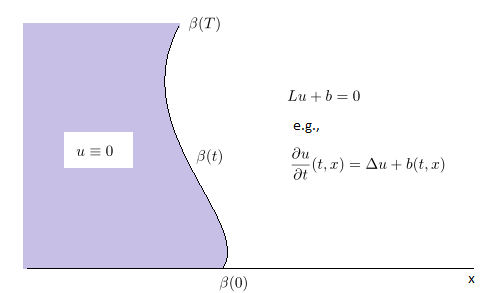

A moving boundary PDE of describes the behavior of a system that consists of two phases, as illustrated in Figure 1, where is a moving boundary which is part of the solution and must be solved simultaneously with . As can be seen in Figure 1, in the region to the left of the moving boundary (namely, the set ) is constantly set to ; on the right side of the boundary (the set ) is described by a PDE of the general form where is a predefined second-order differential operator.

For a moving boundary PDE problem, in addition to the regular boundary condition such as the Dirichlet condition , there is always an extra boundary condition that describes the dynamics at the moving boundary, for instance, the Stefan boundary condition

| (1) |

The type of moving boundary PDE’s we consider throughout the thesis is the Stefan problems, where is a heat or parabolic operator (for instance, ) with the Stefan boundary condition. Such type of problems has a variety of applications. For instance, in physics, they model the phenomena such as ice melting with the Stefan condition describing the heat balance at the interface (the moving boundary, see [2]); in finance they model the valuation of American options with the PDE derived from the Black-Scholes formula and the moving boundary describing the early exercise price boundary (see Lemma 7.8, Chapter 2, [4]).

1.2 Motivation and Results

In the mathematics of this thesis we are interested in the stochastic versions of the Stefan problems, namely, is a formal notation about the stochastic addition (noise). In general is a 2-dimensional distribution and therefore we work within the framework of the stochastic PDE theory by Walsh in [7], and based on the weak formulations of the equations and their equivalent evolution equations.

When is multiplicative, namely, where is the noise (formal), [5] proves the existence and uniqueness of the solution when is a distribution (Brownian) only in time and is constant in space. Also, in [6] we proved the existence and uniqueness of the solution when is a distribution (Brownian) only in time and is smoothly correlated (“colored”) in space, which is quickly reviewed in Section 2.

However, when is a distribution (Brownian) in both space and time, we face a number of novel challenges that are beyond the scope of current literature:

-

(1)

The spatial derivatives of the solution may not exist (see [7]), which means the techniques we used in [6] based on -norms may not be available; more importantly, the Stefan condition (1) involves the spatial derivative of the solution at the boundary, and therefore we shall show the existence of such a derivative simultaneously with the existence and uniqueness of the solution.

-

(2)

The stochastic perturbation given by is no longer spatially Lipschitz as in [5] and [6], which means in order to control the boundary shift effect in the Itô integrals and the nonlinear drift term we may need additional spatial regularities on in addition to just being multiplicative as in [5] and [6]; in other words, although the perturbation vanishes when , itself may not provide sufficient spatial smoothness to control the Itô integrals when the boundary shifts.

To tackle (1) alone, in Section 3 we first study the stochastic heat equation driven by a multiplicative space-time Brownian noise, namely, with a standard 2-dimensional Brownian sheet defined in [7],

From such study we obtain the conditions and form of norms under which a boundary derivative exists, and more importantly, develop the essential techniques to calculate the sample-wise space and time modulus of continuity of the solution by means of Kolmogorov’s Continuity Theorem (see [3]), which is critical to evaluate the regularity needed to control the boundary shift effect.

Next, in Section 4, first with the same multiplicative space-time Brownian noise (that is, ,) we preliminarily calculate the effect of a boundary shift on the Itô integral using the techniques and results obtained in the previous section, and find that it may be difficult to obtain the wanted control on iteration. Therefore we make the change in the stochastic perturbation such that it is even smoother in space and in turn study the following stochastic Stefan problem driven by a scaled space-time Brownian noise:

where and is a function that satisfies certain regularity conditions which are sufficient to tackle (2). We show the existence and uniqueness of the solution to the above equation and additionally the regularity of the boundary using results from this and previous sections. This result also serves as the mathematical foundation for the modeling of the dynamics of limit orders.

2 A Stochastic Stefan Problem with Spatially Colored Noise

In this section we quickly review our work in [6] by giving the main theorems and lemmas without proofs. We studied a stochastic Stefan problem of driven by a multiplicative noise , where is a noise that is Brownian in time and smoothly correlated (or “colored”) in space. Specifically, fix a probability space , and suppose is the standard 2-dimensional Brownian sheet. Suppose also that is and . Then for , define

Then we have the following problem and results.

2.1 Problem and Main Theorem

We showed the existence and uniqueness of the solution to the following formal equation:

| (2) |

for where is some well defined stopping time.

2.2 A Transformation

We make the natural transformation , which transforms the original weak definition and its equivalent evolution equation to a nonlinear PDE in the fixed domain . Then we have

Lemma 2.2

The weak solution is obtained by getting it from of (3) by the transformation , where

This technique is also used in Section 4.

2.3 Existence and Uniqueness of the Truncated Solution

First, in order to control the nonlinear drift term we shall truncate the -norm of the solution (which is shown as equivalent to truncating the nonlinear term, or ), and work with the truncated solution , namely, the solution to

| (4) |

where is as a smooth monotone decreasing function that satisfies .

The existence and uniqueness of the truncated solution is proved by a Picard-type iteration on -spaced combined with similar calculations in Lemma 3.3 of [7]. Unlike in Section 3 and Section 4, in this problem we need not worry about the existence of the spatial derivatives, or in particular,

which is the right hand side in the Stefan boundary condition, because the stochastic perturbation is smooth in space. By calculations of such an iteration and the structural results about -space (see Section 5.1 of [6]), combined with Lemma 3.3 of [7], we have

Lemma 2.3

Fix . Then the solution to (4) exists and is unique.

2.4 Relaxation of the Truncation

Define the stopping time

Also, define

and

We then have

Lemma 2.4

and

Finally, we have

Lemma 2.5

The solution to (3) exists and is unique.

Combining all the lemmas, we showed the main theorem. Note that the idea of first stopping from growing too large (that is, exceeding a fixed ), then using this to control the nonlinear drift term, and finally relaxing this truncation and obtaining a global stopping time is important, and is also used in Section 4 when we study a stochastic Stefan problem driven by a scaled space-time Brownian noise.

3 Boundary Regularity of the Stochastic Heat Equation

In the previous section we have shown the existence and uniqueness of a stochastic Stefan problem with a spatially-colored and Brownian-in-time noise. Since we would further study a stochastic Stefan problem with space-time Brownian noise under certain regularity conditions, it is necessary that we first understand the effect of such noise on the regularity of the boundary, namely, the differentiability of the solution at the moving boundary, in addition to the existence and uniqueness of the solution itself. This task is critical because the Stefan boundary condition of such a problem involves the spatial derivative of the solution at the boundary, and since the noise is Brownian in space (as well as in time), the solution in general may not have a spatial derivative everywhere except at the boundary.

Therefore, to simplify the problem, we first in this section consider a stochastic heat equation of driven by a multiplicative space-time Brownian noise, so that the noise vanishes at the boundary (where ), and we would expect that is differentiable just at the boundary. Specifically, by removing the shift effect of the moving boundary and studying a stochastic heat equation of this kind, we look to understand

-

(1)

under what sense (or, in what normed space) the solution exists, and the connection between such a norm or space and the differentiability of the solution at the moving boundary;

-

(2)

in what sense (-a.s.? in ? etc.) the Stefan boundary condition holds;

-

(3)

the spatial regularity of the solution (Hölder continuity? with what parameters?) which may guide us on the study of a Stefan problem with a space-time Brownian noise in the next section, in particular, the effect of a boundary shift on the iteration of the Itô integral.

3.1 Problem and Main Theorem

Fix a probability space , and suppose is a standard 2-dimensional Brownian sheet. Consider the (formal) stochastic heat equation of with a multiplicative space-time Brownian noise on , under a Dirichlet boundary condition:

| (5) |

From the classic work of [7] by Walsh, the weak solution to the formal equation (5) is equivalent to the evolution equation

where and is the corresponding kernel as defined in the previous section. Then we have the following theorem as the main conclusion of this section:

Theorem 3.1

-

(1)

The solution to (5) exists and is unique with respect to a normed space;

-

(2)

-a.s., for all , is differentiable at , and

-

(3)

For , define for and , then -a.s., is -Hölder continuous on for .

3.2 Integral Regularities of Kernel

The existence, uniqueness, and regularity of the solution described in Theorem 3.1 are based on a number of integral regularities of a newly defined kernel . We present and prove them in this section.

Define a new kernel as

and

then we have

Lemma 3.2

-

(1)

,

-

(2)

,

-

(3)

,

-

Proof

We only need to prove the above facts for , since by Fatou’s Lemma they can be extended to the cases for .

Throughout the calculations we repeatedly use the following facts:

-

(a)

-

(b)

if and are even, then

-

(c)

using the fact that , we have for ,

Then

-

(1)

-

(2)

Suppose , and define . Then from above,

where

Note that from (c) above, we get

Then we need to consider

Now we use two methods to bound .

-

(I)

Using the fact that , we get

-

(II)

Define a function

Then

Then we have

Combining (I) and (II), we have that for some , when , using (I) and we get ; when , using (II) and we get .

-

(I)

-

(3)

Suppose , and define . The first integral on the left hand side is bounded by using (1). Now, from (1),

where (defining )

Therefore we have for some

-

(a)

3.3 Proof of the Main Theorem

Theorem 3.1 is proved in two steps. First we show that the solution to (5) exists and is unique in a normed space, where the norm is defined so that in the second step the regularity results of the solution can be derived by using the defined norm and the integral regularities of the kernel in Lemma 3.2. In other words, the norm we defined in the next part characterizes the essential component from which we derive the desired Hölder continuity of the solution and its differentiability at the boundary, which are shown by using Kolmogorov’s Continuity Theorem in the second step.

3.3.1 Existence and Uniqueness of the Solution

Existence and uniqueness of the solution is shown by a Picard-type iteration. Consider the iteration

| (6) |

Or, if we define

then

| (7) |

Fix . Suppose is a stochastic process. Define a norm

Then we have

Lemma 3.3

For all , the solution to (7) exists and is unique in the space defined by the norm .

-

Proof

We have

or equivalently,

Define . Then we have from Lemma 3.2 (1) that

where the first inequality comes from Burkholder inequality, the second inequality comes from Jensen’s inequality that for ,

and the third inequality comes from Lemma 3.2 (1). By Lemma 3.3 of [7],

and the convergence is uniform on compacts. That is, if , then where is a constant dependent only on . This gives immediately by Picard-type iteration that the solution exists and is unique with respect to . Moreover,

Define , then is the unique solution to (6).

3.3.2 Regularity of the Solution and Differentiability at the Boundary

In this part we shall prove the differentiability of the solution at the boundary by giving a -a.s. limit or the spatial derivative at the boundary. This is shown by using Kolmogorov’s Continuity Theorem combined with the integral regularities shown in the previous parts and the existence of the solution under the norm. In fact, a stronger result is shown, namely, the solution is -a.s. Hölder continuous with parameters on for , which can also be used to evaluate the impact of its spatial regularity on the boundary shift effect required in the stochastic Stefan problems drive by space-time Brownian noise.

Lemma 3.4

-a.s., for all the solution to (7) is continuous at and

Moreover, for define , then -a.s., is -Hölder continuous on for .

-

Proof

We only need to consider the Brownian term. Fix . For , define

and

Then for , we have

where the first inequality comes from Burkholder inequality, the second comes from Jensen’s inequality, the third comes from the previous part about uniform boundedness of on , and the last one comes from Lemma 3.2 (2).

Similarly, We also have for ,

where

by Jensen’s inequality . Now,

using Burkholder’s inequality, Jensen’s inequality, and Lemma 3.2 (3). Similarly, using Burkholder’s inequality, Jensen’s inequality, and Lemma 3.2 (1), we have

Summing things up, for all , we have for ,

By Kolmogorov Continuity Theorem, the above calculations imply that almost surely, is -Hölder continuous on for all . This implies that , and that is -Holder continuous on for all .

4 A Stochastic Stefan Problem with Space-Time Brownian Noise

In the previous section we considered the stochastic heat equation of driven by a multiplicative space-time Brownian noise and showed the existence and uniqueness of the solution under normed space defined by for all and the -a.s. differentiability at the boundary and as a by-product, the Hölder continuity of . The proof provides us with important hints on how to prove the existence and uniqueness of a stochastic Stefan problem driven by space-time Brownian noise, since we shall also prove that the Stefan boundary condition holds simultaneously at the moving boundary.

Fix a probability space , and suppose is the standard 2-dimensional Brownian sheet. Then the stochastic Stefan problem of has the general (formal) form

for where is some well defined stopping time.

The introduction of a moving boundary brings about a number of challenges that do not exist in the stochastic heat equation problem, and one of them is to control the boundary shift effect, namely, if we iterate on the boundary , then is the shift of the boundary between iterations. We look to control

whose variance is

For multiplicative noise where , the variance above in terms of is completely determined by the spatial regularity of or . From the previous section we know that spatially is continuous only at the boundary and has -Hölder continuity for on . To evaluate the impact of the spatial regularity on the above variance in terms of , we let , and a calculation with two methods similar to Lemma 3.2 (2) shows that

Although the tightness of the inequality is not justified, it still gives strong evidence that it would be difficult to have an iteration on , even if is as smooth as . Therefore, instead of working with a multiplicative noise, we in this section consider a stochastic Stefan problem drive by scaled space-time Brownian noise where satisfies certain regularity conditions:

-

Definition

A function is a regular scaling function if is Lipschitz in and at with . Equivalently, for some .

Note that provides enough smoothness to control the boundary shift effect as iterating on below and provides enough control as for other parts so that the noise does not grow too large at infinity.

4.1 Problem and Main Theorem

Suppose is a regular scaling function. Then we consider the stochastic Stefan problem of

| (8) |

for for some well defined stopping time .

As before we work on a weak formulation of (8) and its transformed equivalent evolution equation. Unlike in the colored noise case, we do not directly have the differentiability of the solution at the boundary, so in the iteration of the boundary we cannot simply let it be the spatial derivative of the solution at the boundary, but the one similar to what was obtained in the stochastic heat equation, and finally we have an extra step to show that the two coincide -a.s., or equivalently, the Stefan boundary condition in (8) holds.

Theorem 4.1

The solution to (8) exists and is unique for where . Moreover, -a.s., and is -Hölder continuous for .

4.2 Integral Regularities of Kernels

As in the previous section, the proof to the main theorem is based on the integral regularities of newly defined kernels. Define two new kernels (where is the same as in the previous section)

Then we have the following integral regularity results about , similar to those for as in Lemma 3.2:

Lemma 4.2

There exists such that

-

(1)

-

(2)

for ,

-

(3)

for ,

-

Proof

First we observe that

where

Therefore the calculations to prove the above facts are fairly similar to those in Lemma 3.2, hence we only provide sketch here.

-

(1)

this can be shown by using facts (a) and (b) in Lemma 3.2, where

followed by a direct calculation of the integral after applying (b) with .

- (2)

- (3)

-

(1)

4.3 Proof of the Main Theorem

As in the previous sections, we work with the weak formulation of the solution and its equivalent evolution equation. Define , Then the equivalent evolution equation gives

| (9) |

where is the Brownian sheet obtained by shifting spatially by . The main theorem is proved by adopting the following strategy:

-

(1)

prove the existence and uniqueness of the truncated solution and its corresponding in for for a fixed by an argument based on Picard-type iterations;

-

(2)

based on (1), show that -a.s., the Stefan boundary condition

holds by using Kolmogorov’s Continuity Theorem on the drift term and the Brownian term;

-

(3)

let and obtain the solution ; transform back to and obtain a weak solution of (8).

4.3.1 Existence and Uniqueness of the Truncated Solution

In this section we first show the existence and uniqueness of that satisfies (10), and then truncate by a fixed so that the drift term of the solution is controlled from growing too large. Then we show the existence and uniqueness of the solution under the truncation.

Defining as before, then we have

| (10) |

Lemma 4.3

There exists a unique that satisfies (10).

-

Proof

Consider the following iteration on :

Fix and define

Also define

Then letting , we have

Note that for the above argument to work we must have , otherwise the first integral with respect to is . Since , we get that

Therefore, by Walsh’s Lemma 3.3 in [7], we obtain that as the limit of exists and is unique, and we also have

and its bound is uniform (that is, not dependent of ).

Let be the solution to (10). Fix , and define as a smooth monotone decreasing function that satisfies . Now consider the following iteration of :

| (11) |

where the initial value

Then we have

Lemma 4.4

The solution to (11) exists and is unique.

-

Proof

By adopting a similar approach to the proof of Theorem 3.1, we first compute

Also, from Lemma 3.2 (1) and , by following the same calculations as in the previous sections we get

Therefore, by Walsh’s Lemma 3.3 in [7], we obtain that as the limit of exists and is unique, and we also have

and its bound is uniform (that is, not dependent of ).

4.3.2 The Stefan Boundary Condition Holds

Lemma 4.5

-

Proof

This lemma is shown by using Kolmogorov Continuity Theorem and adopting the similar calculations as in the previous section. In fact, define for and , then we claim that -a.s., is -Hölder continuous for fixed on with .

Indeed, by Burkholder’s inequality,

By Lemma 3.2 (2) and Lemma 4.2 (2) about and , we have that by using Jensen’s inequality as in the previous section, for ,

where does not depend on . Also, by Lemma 3.2 (3) and Lemma 4.2 (3), we have that still by using Jensen’s inequality, for ,

By Kolmogorov’s Continuity Theorem, we have that for all , is -a.s. uniformly -Hölder continuous, which implies that -a.s.,

and is -Hölder continuous.

Now, when , we simply let . When , we choose for all , and since the above statement holds for for all we have that it holds for .

4.3.3 Relaxation of the Truncation

Lemma 4.6

Define and . Then is the unique solution to (8).

-

Proof

Fix and define . Then we have . Therefore for we have that also satisfies the equation of . By the uniqueness of and , this implies that for ,

Therefore, for , satisfies (8) and also

4.4 Numerical Simulation

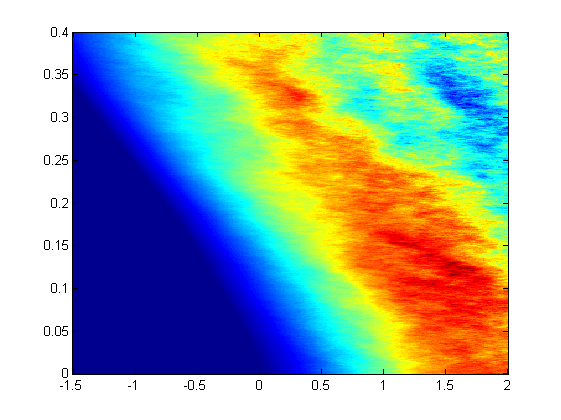

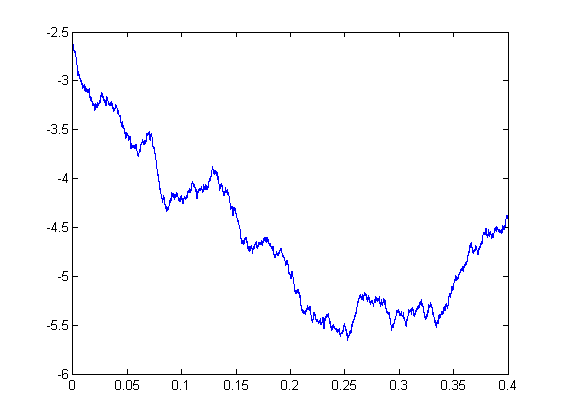

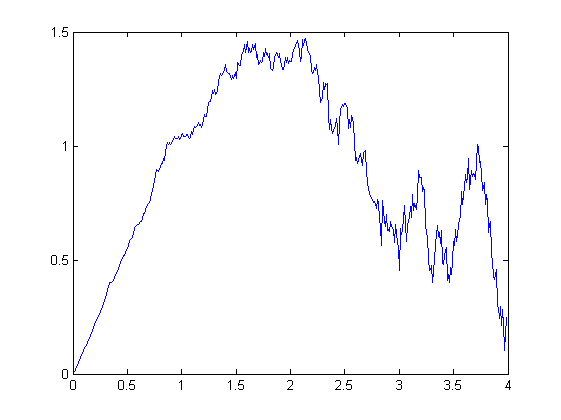

Since the existence and uniqueness of the problem is shown we can indeed simulate the solution and its boundary numerically. The simulation uses finite-difference Euler approximation scheme described in [1]. To guarantee numerical robustness in our simulation we assume the space and time increment steps satisfy .

In this simulation we apply the following simulation parameters:

The consequent numerical results are illustrated as follows.

-

(1)

Figure 2 illustrates the weak solution ;

-

(2)

Figure 3 illustrates the boundary derivative ;

-

(3)

Figure 4 illustrates the typical shape of the solution at a particular time , from which we see that is smoother as gets closer to the boundary (shifted and denoted by ), and is differentiable at the boundary.

5 Summary

In this section we summarize the main results obtained in the previous sections. Throughout this section we fix a probability space , and suppose is a standard 2-dimensional Brownian sheet. In this paper we studied 3 types of stochastic equations.

5.1 A Stochastic Stefan Problem with Spatially Colored Noise

The solution to the stochastic Stefan equation

| (12) |

exists and is unique for where .

5.2 Boundary Regularity of the Stochastic Heat Equation

The solution to the stochastic heat equation

| (13) |

exists and is unique; Moreover, define , then -a.s.,

If we further define , then -a.s., is -Hölder continuous on for .

5.3 A Stochastic Stefan Problem with Space-Time Brownian Noise

Let be a regular scaling function (see the definition given in Section 4). Then the solution to the stochastic Stefan equation

| (14) |

exists and is unique for for where ; Moreover, -a.s., and is -Hölder continuous for .

References

- [1] A. M. Davie and J. G. Gaines. Convergence of numerical schemes for the solution of parabolic stochastic partial differential equations. Mathematics of Computation, 2001.

- [2] Avner Friedman. Partial differential equations of parabolic type. Prentice-Hall Inc., 1964.

- [3] Ioannis Karatzas and Steven E. Shreve. Brownian Motion and Stochastic Calculus. Springer-Verlag, 1991.

- [4] Ioannis Karatzas and Steven E. Shreve. Methods of Mathematical Finance. Springer-Verlag, 1998.

- [5] Kunwoo Kim, Carl Mueller, and Richard B. Sowers. A stochastic moving boundary value problem. Illinois Journal of Mathematics, 2009.

- [6] Kunwoo Kim, Zhi Zheng, and Richard B. Sowers. A stochastic stefan problem. Journal of Theoretical Probability, 2011.

- [7] John B. Walsh. An introduction to stochastic partial differential equations. École d’été de probabilités de Saint-Flour, XIV, 1986.