Generalised arbitrage-free SVI volatility surfaces

Abstract.

In this article we propose a generalisation of the recent work by Gatheral-Jacquier [12] on explicit arbitrage-free parameterisations of implied volatility surfaces. We also discuss extensively the notion of arbitrage freeness and Roger Lee’s moment formula using the recent analysis by Roper [21]. We further exhibit an arbitrage-free volatility surface different from Gatheral’s SVI parameterisation.

Key words and phrases:

SVI volatility surface, calendar spread arbitrage, butterfly arbitrage, static arbitrage1. Introduction

European option prices are usually quoted in terms of the corresponding implied volatility, and over the last decade a large number of papers (both from practitioners and academics) has focused on understanding its behaviour and characteristics. The most important directions have been towards (i) understanding the behaviour of the implied volatility in a given model [1, 2, 9, 14] and (ii) deciphering its behaviour in a model-independent way, as in [19, 21, 23]. These results have provided us with a set of tools and methods to check whether a given parameterisation is free of arbitrage or not. In particular, given a set of observed data (say European Calls and Puts for different strikes and maturities), it is of fundamental importance to determine a methodology ensuring that both interpolation and extrapolation of this data are also arbitrage-free. Such approaches have been carried out for instance in [4, 8, 24]. Several parameterisations of the implied volatility surface have now become popular, in particular [10, 15, 17], albeit not ensuring absence of arbitrage.

Recently, Gatheral and Jacquier [12] proposed a new class of implied volatility parameterisation, based on the previous works by Gatheral [10]. In particular they provide explicit sufficient and—in a certain sense—almost necessary conditions ensuring that such a surface is free of arbitrage. We shall recall later the exact definition of arbitrage, and see that it can be decomposed into two elements: butterfly arbitrage and calendar spread arbitrage. This new class depends on the maturity and can hence be used to model the whole volatility surface, and not a single slice. It also depends on the at-the-money total implied variance , and on a positive function such that the total variance as a function of time-to-maturity and log-(forward)-moneyness is given by , where is the classical (normalised) SVI parameterisation from [12], and an asymmetry parameter (essentially playing the role of the correlation between spot and volatility in stochastic volatility models).

In this work, we generalise their framework to volatility surfaces parameterised as for some (general) functions , , . We obtain (Sections 3 and 4) necessary and sufficient conditions coupling the functions and that preclude arbitrage. This allows us to obtain (i) the exact set of admissible functions in the symmetric () SVI case, and (ii) a constraint-free parameterisation of Gatheral-Jacquier functions satisfying the conditions of [12]. In passing (Section 4.4), we extend the class of possible functions by allowing for non-smooth implied volatility functions. Finally (Section 5), we exhibit examples of non-SVI arbitrage-free implied volatility surfaces.

Notations: We consider here European option prices with maturity and strike , written on an underlying stock . Without loss of generality we shall always assume that and that interest rates are null, and hence the log (forward) moneyness reads . We denote by

| (1.1) |

the Black-Scholes value for a European Call option with strike and total variance , where denotes the Gaussian cumulative distribution function and ; more generally, we shall write for (any) European Call prices with strike and maturity . For any , the corresponding implied volatility is denoted by and the total variance is defined by . With a slight abuse of language (commonly accepted in the finance jargon), we refer to the two-dimensional map as the (implied) volatility surface. Finally, for two functions and not null almost everywhere, we say that at whenever . We shall also use the notations and , and use the convention .

2. Absence of arbitrage and volatility parameterisations

This preliminary section serves several purposes: we first recall the very definition of ‘arbitrage freeness’ and its characterisation in terms of implied volatility. We then state and prove a few results (which are also of independent interest) related to this notion of arbitrage. We finally quickly review the parameterisation proposed in [12] and introduce an extension, which is our new contribution.

2.1. Absence of arbitrage

As defined in [5], absence of static arbitrage corresponds to the existence of a non-negative local martingale (on some probability space) such that European Call options (on this local martingale) can be written as risk-neutral expectations of their final payoffs. Armed with this definition, it is however not easy to check whether a given set of (Call) option prices yields an arbitrage or not. A more practical route follows Roper’s [21] arguments (or equivalently [12]), who provide sufficient and almost111The ‘almost’ refers to [21, Theorem 2.15], where smoothness and strict positivity of the implied volatility are required. necessary conditions for a given two-dimensional function (of strike and maturity) to be a proper implied volatility surface, i.e. to generate arbitrage-free European option prices. Note that Cox and Hobson’s definition [5] allows for strict local martingales, whereas Roper’s framework only considers true martingales, his argument being that the implied volatility is ill-defined for strict local martingales, in particular through the failure of Put-Call parity. Following collateralisation arguments developed in [5], the recent paper [18] restores Put-Call parity in strict local martingale models and clarifies the definition and properties of the implied volatilities (differently generated from Put and from Call options). Pursuing the goal set up in [12], we shall exclude here in our modelling framework the strict local martingale case, and understand ‘static arbitrage’ as a restriction to true martingales.222For a true martingale , it is easy to see that, for a fixed maturity , the map is decreasing, convex and tends to zero at infinity, properties that still hold in the strict local martingale setting. However, as shown by Pal and Protter [20], Call prices are not necessarily increasing in maturity in strict local martingale models, and therefore the corresponding total implied variance, whenever defined, need not be an increasing map any longer. We now define these terms precisely, and refer to [21] for full details.

Definition 2.1.

Given a map , we say that there is no static arbitrage if there exists a non-negative martingale on some filtered probability space such that for each .

Consider now a two-dimensional map representing a total variance surface; it is then natural to wonder whether the Call price surface defined by is free of static arbitrage. Introduce the operator acting on functions by

| (2.1) |

Note that even though does not act on the second component of the function, we shall keep this notation for clarity. For fixed , the total variance may in principle be null for some , which might break the well-posedness of the right-hand side of (2.1). However, it is easy to show that is strictly positive whenever belongs to the support of the log stock price at time , and the restriction is therefore sensible, which is imposed in model (2.3) with Assumption 2.7(iii). At , the total variance is equal to zero everywhere, and the definition of the operator shall not be needed. Roper [21, Theorem 2.9] proved the following theorem:

Theorem 2.2.

If the two-dimensional map satisfies

-

(i)

is of class for each ;

-

(ii)

for all ;

-

(iii)

is non-decreasing for each ;

-

(iv)

for each , is non-negative;

-

(v)

for all ;

-

(vi)

, for each .

Then the corresponding Call price surface is free of static arbitrage.

Conditions (i), (ii) and (v) are usually easy to check. The other conditions motivate the following weaker notions of arbitrage commonly used in practice, in the maturity and in the strike directions:

Definition 2.3.

Butterfly arbitrage corresponds to the convexity of option prices, which can be read as a condition on the behaviour of the implied volatility surface ([12, Definition 2.3] and [12, Lemma 2.2]). If represents the (Dupire) local volatility, the relationship , for all is now standard (see [11, Chapter 1, Equation (1.10)]). Therefore absence of static arbitrage implies that both the numerator and the denominator are non-negative quantities. Condition (vi) in Theorem 2.2 is called the ‘Large-Moneyness Behaviour’ (LMB) condition, and is equivalent to Call option prices tending to zero as the strike tends to (positive) infinity, as proved in [23, Theorem 5.3]. The following lemma however shows that other asymptotic behaviours of and hold in full generality. This was proved by Rogers and Tehranchi [23] in a general framework, and we include here a short self-contained proof.

Lemma 2.4.

Let be any positive real function. Then

-

(i)

;

-

(ii)

.

Proof.

The arithmetic-geometric mean inequality reads , when , which implies (i), and (ii) follows using , when . ∎

The missing statements in Lemma 2.4 are the LMB Condition (Condition (vi) in Theorem 2.2) and the Small-Moneyness Behaviour (SMB): . To investigate further, let us remark that the framework developed in [21] encompasses situations where the underlying stock price can be null with positive probability. This can indeed be useful to model the probability of default of the underlying. Computations similar in spirit to [21] show that the marginal law of the stock price at some fixed time has no mass at zero if and only if , which is a statement about a ’small-moneyness’ behaviour. This can be fully recast in terms of implied volatility, and the above missing conditions then come naturally into play in the following proposition, the proof of which is postponed to Appendix A.1:

Proposition 2.5.

(Symmetry under small-moneyness behaviour) Let be a real function satisfying

-

(I)

and for all ;

-

(II)

(SMB Condition);

-

(III)

(LMB Condition).

Define the two functions and by . Then

-

(1)

and define two densities of probability measures on with respect to the Lebesgue measure, i.e. ;

-

(2)

, so that ;

-

(3)

is the density of probability associated to Call option prices with implied volatility , in the sense that , and is the density of probability associated to Call option prices with implied volatility .

The strict positivity of the function in Assumption (I) ensures that the support of the underlying distribution is the whole real line. One could bypass this assumption by considering finite support as in [23]. In the latter—slightly more general—case, the statements and proofs would be very analogous but much more notationally inconvenient. Symmetry properties of the implied volatility have been investigated in the literature, and we refer the interested reader to [3, 13, 22]. This proposition has been intentionally stated in a maturity-free way: it is indeed a purely ‘marginal’ or cross-sectional statement, which does not depend on time. A natural question arises then: can such a function , satisfying the assumptions of Proposition 2.5, represent the total implied variance smile at time associated to some martingale (issued from at time zero)? The answer is indeed positive and this can be proved as follows. Consider the natural filtration of a standard (one-dimensional) Brownian motion . Let be the cumulative distribution function associated to characterised in Proposition 2.5, and the Gaussian cumulative distribution function. Then the random variable has law , and . Set now , then is a martingale issued from . Note that is even a Brownian martingale and therefore a continuous martingale. The associated Call option prices uniquely determine a total implied variance surface such that .

2.2. Volatility parameterisations

In [10], Gatheral proposed a parameterisation for the implied volatility, the now famous SVI (‘Stochastic Volatility Inspired’). However, finding necessary and sufficient conditions preventing static arbitrage have been inconclusive so far. Recently, Gatheral and Jacquier [12] extended this approach and introduced the following parameterisation for the total implied variance :

| (2.2) |

with for and is a smooth function from to and . The main result in their paper (Corollary 5.1) is the following theorem, which provides sufficient conditions for the implied volatility surface to be free of static arbitrage:

Theorem 2.6.

The surface (2.2) is ‘free of static arbitrage’ if the following conditions are satisfied:

-

(1)

for all ;

-

(2)

for all ;

-

(3)

for all ;

-

(4)

for all ;

-

(5)

for all .

A few remarks are in order here:

-

(1)

the conditions in Theorem 2.6 are sufficient, but not necessary;

-

(2)

the full characterisation of the functions guaranteeing absence of (static or not) arbitrage in the symmetric SVI case is left open;

- (3)

In this paper, we try to settle all these points, and state our results in a more general framework, not tied to the specific shape of the SVI model, by considering implied volatility surfaces of the form

| (2.3) |

together with the following assumptions:

Assumption 2.7.

-

(i)

, is not constant, , and is well defined in ;

-

(ii)

, and is well defined in ;

-

(iii)

with and is not constant;

-

(iv)

for any , .

The time-dependent function models the at-the-money total variance;

the assumption on its behaviour at the origin is thus natural.

A constant function corresponds to deterministic time-dependent volatility,

a trivial case we rule out here.

Likewise, were assumed to be constant, it would be null everywhere,

which we shall also not consider.

Assumption (iv) ensures that at maturity, European Call option prices are equal to their payoffs.

We can recast it in terms of assumptions on and , for example:

Assumption (iv’): converges to a non-negative constant as .

Indeed (iv’), together with (iii), clearly implies (iv).

We shall present another alternative below with the help of the ‘asymptotic linear’ property of

(Definition 3.4 and Assumption 3.5).

Assumption (iii) may look strong from a purely theoretical point of view, but is always satisfied in practice.

In Section 4.4 though, we partially relax it (Assumption 4.10)

to allow for possible kinks.

The main goal here is to provide sufficient conditions on the triplet that will guarantee absence of static arbitrage.

Note that the SVI parameterisation (2.2)

corresponds to the case ,

which clearly satisfies Assumption 2.7(iii).

In the sequel, we shall refer to this case as the SVI case.

The next sections provide necessary and sufficient conditions on and

to prevent static arbitrage.

3. Elimination of calendar spread arbitrage

We first concentrate on determining (necessary and sufficient) conditions on the triplet to eliminate calendar spread arbitrage.

3.1. The first coupling condition

The quantity in Definition 2.3 is nothing else than the numerator of the local volatility expressed in terms of the implied volatility, i.e. Dupire’s formula (see [11]). Define now the functions and by

| (3.1) |

They will play a major role in our analysis, and Assumption 2.7(iii) implies that at the origin and . Note that and can be recovered through the identities

for some arbitrary constant . The following proposition gives new conditions for absence of calendar spread arbitrage.

Proposition 3.1 (First coupling condition).

The surface (2.3) is free of calendar spread arbitrage if and only if the following two conditions hold:

-

(i)

is non-decreasing;

-

(ii)

for any and .

Proof.

By Definition 2.3, the surface defined by (2.3) is free of calendar spread arbitrage if and only if

| (3.2) |

where . Since is strictly positive by Assumption 2.7(iii), the inequality (3.2) is equivalent to for all , , with and defined in (3.1). For we get for all . Otherwise (ii) is necessary and sufficient for the surface to be free of calendar spread arbitrage. ∎

Remark 3.2.

We do not assume here that is infinite. In most popular stochastic volatility models with or without jumps, is infinite. Rogers and Tehranchi [23] showed that for a non-negative martingale the equality is equivalent to the almost sure equality (where the limit exists by the martingale convergence theorem). However, it may occur that . As a corollary of coupling properties of stochastic volatility models, Hobson [16] provides instances where such a phenomenon appears, for example the SABR [15] model with .

Remark 3.3.

Motivated by the celebrated moment formula in [19] (see also Theorem B.1), which forces the function to be at most linear at (plus/minus) infinity, let us propose the following definition:

Definition 3.4.

The function is said to be asymptotically linear if .

With this definition, we can replace Assumption 2.7(iv) by

Assumption 3.5.

is asymptotically linear and .

We now obtain a necessary condition on the behaviour of the function in (2.3).

Proposition 3.6.

If is asymptotically linear and if there is no calendar spread arbitrage, then the map is non-decreasing on .

Proof.

Note that if then the limit of the function at (plus or minus) infinity does not necessarily exist. Whenever it does, since is decreasing as , the limit can take any value in .

3.2. Application to SVI

In the SVI case (2.2), we have with , so that is asymptotically linear with and . Therefore Proposition 3.6 applies, and a necessary condition is that is not decreasing. In [12, Theorem 4.1], this condition, together with being non-increasing, are shown to be sufficient to avoid calendar spread arbitrage. In the case of the symmetric SVI model, the following corollary relates our conditions to those in [12].

Corollary 3.7.

In the symmetric SVI case, the necessary condition of Proposition 3.6 is also sufficient.

Proof.

In the symmetric case , we can compute explicitly

| (3.3) |

and therefore

It is then clear that the even function is strictly increasing on and strictly decreasing on with a global minimum attained at the origin for which . In light of Remark 3.3, we have and . By Proposition 3.1 there is hence no calendar spread arbitrage if and only if , which is equivalent to being non-decreasing. ∎

4. Elimination of butterfly arbitrage

We now consider butterfly arbitrage which, probably not surprisingly, is more subtle to handle. We first start with a general result (Section 4.1), which is unfortunately not that tractable in practice. When the function is asymptotically linear, however, more elegant formulations are available, and we provide necessary and sufficient conditions precluding static arbitrage (Section 4.2). In the particular example of the symmetric SVI function (Section 4.3), we put these results in action, where everything is computable explicitly. Finally, in Section 4.4, we address a delicate issue, allowing for the possibility of non-smooth functions, thereby enlarging the class of arbitrage-free volatility surfaces.

4.1. The second coupling condition

We consider here the positivity condition from Definition 2.3, and reformulate the butterfly arbitrage condition in our setting. We first start with a general formulation, and then consider the asymptotically linear case (for the function ), which turns out to be more tractable. For any , define the set

| (4.1) |

as well as the function by

| (4.2) |

Proposition 4.1 (Second coupling condition, general formulation).

The surface given in (2.3) is free of butterfly arbitrage if and only if

| (4.3) |

4.2. The asymptotically linear case

We now consider the case where is asymptotically linear (Definition 3.4). Define the sets

| (4.5) |

together with the complement in : , as well as the, possibly infinite, quantity

| (4.6) |

The following proposition, proved in Appendix A.2, is a reformulation of Proposition 4.1 in the asymptotically linear case, and provides sufficient and necessary conditions for the surface (2.3) to be free of butterfly arbitrage.

Proposition 4.2.

Assume that is asymptotically linear and there is no calendar spread arbitrage. Then is neither empty nor bounded from above. Moreover, there is no butterfly arbitrage if and only if the following two conditions hold (recall that the functions and are defined in (4.1) and (4.2)):

-

(i)

-

(ii)

for any , .

Remark 4.3.

Case (ii) actually includes two cases: and . On the former, the function is well defined and the infimum can be searched for without any confusion. On , however, the function reduces to , which is always strictly positive. Note further that, from (4.4), if , then positivity of is automatically guaranteed.

The following corollary is an immediate consequence of this proposition, in the case .

Corollary 4.4.

If is asymptotically linear and , then (allowing infinity)

is a necessary condition for absence of butterfly arbitrage. In particular .

A little work on the proposition above yields the following sufficient condition preventing butterfly arbitrage, which is easier to check in practice.

Corollary 4.5.

Assume that is asymptotically linear, that there is no calendar spread arbitrage and that . Assume further that for any , the inequality in Proposition 4.2(ii) is strict. Then the corresponding implied volatility surface is free of static arbitrage.

Proof.

In our setting ( asymptotically linear), , so that we only need to prove that , since clearly implies the LMB condition. For any (defined in (4.5)), note that

Applying this to a sequence in diverging to infinity yields and the result follows. ∎

4.3. Application to symmetric SVI

As in Section 3.2 above, we show that in the symmetric SVI case (), all our expressions above are easily computed and give rise to simple formulations. It is clear that the set defined in (4.5) is empty in this case. Let us define the functions , and by

| (4.7) |

Of course we only define these functions on their effective domains, the forms of which we omit for clarity. The following proposition makes the conditions of Proposition 4.2 explicit in the symmetric SVI case.

Proposition 4.6.

In the symmetric SVI (2.2) case , there is no butterfly arbitrage if and only if

Proof.

Define ; then

Since for all , the first equation implies that defined in (4.5) is equal to . For any fixed , the function appearing on the right-hand side of Proposition 4.2(ii) simplifies to given in (4.7). In particular and . For any , we have

where . When , is concave on with , and hence the map is decreasing on and its infimum is equal to . For , the strict convexity of and the inequality implies that the equation has a unique solution in , which in fact is equal to given in (4.7). Then the map is decreasing on and increasing on . Its infimum is attained at and is equal to defined in (4.7). ∎

Remark 4.7.

In [12], the authors prove that the two conditions (altogether) and (for all ) are sufficient to prevent butterfly arbitrage in the uncorrelated () case. These two conditions can be combined to obtain . A tedious yet straightforward computation shows that is increasing on and maps this interval to . Notwithstanding the fact that our condition is necessary and sufficient, it is then clear that

-

(i)

for , it is also weaker than the one in [12] whenever ;

-

(ii)

for (which accounts for most practically relevant cases) it is weaker whenever .

In particular, item (ii) could be used as a sufficient and necessary lower bound condition (depending on ) for the function on .

4.4. Non-smooth implied volatilities

The formulation of arbitrage freeness in [21, Theorem 2.1] is minimal in the sense that the regularity conditions on the Call option prices are necessary and sufficient: to be convex in the strike direction and non-decreasing in the maturity direction. The implied volatility formulation ([21, Theorem 2.9, condition IV.1] and Theorem 2.2(i) above) however, assumes that the total variance is twice differentiable in the strike direction. This regularity is certainly not required; in fact, the author [21, Theorem 2.9] proves the latter by checking the necessary assumptions on the behaviour of the Call price ([21, Theorem 2.1]) defined by , with defined in (1.1). More precisely, Roper uses the regularity assumption in of in order to define pointwise the second derivative of this Call price function with respect to the strike. He then proves that the latter is positive, henceforth obtaining the convexity of the price with respect to the strike [21, Theorem 2.1, Assumption A.1]. It turns out that the same result can be obtained without this regularity assumption. Let denote the space of strictly positive, continuous, functions on the real line, differentiable except possibly at finitely many points, and with derivatives in , the space of locally essentially bounded measurable functions. Introduce then the functional on by

| (4.8) |

Proposition 4.8.

For any , the following hold:

-

(1)

the functional in (4.8) is well defined in , hence in the sense of distributions;

-

(2)

let denote the second derivative of in the sense of distributions. Then the map is convex if and only if is a positive distribution.

We abuse the notation slightly by considering the same symbol for the operator here and in (2.1), although they do not act on the same spaces; this should however not create any confusion.

Proof.

The first statement follows from the fact that is positive continuous and . Consider now a strictly positive smooth function with compact support, which integrates to one, and regularise by convolution as . Then is a smooth strictly positive function, and Roper’s computation [21, Theorem 2.9] applies:

where is defined pointwise, and where denotes the derivative of the function with respect to its second component. It follows that for any with compact support on ,

| (4.9) | ||||

where the boundary terms cancel since has compact support. Mapping , the last integral reads

When tends to zero, converges pointwise to , to almost everywhere, and to in the sense of distribution. It follows that the map converges to in the sense of distribution (on ). Now the first line of (4.9) converges to

where is the second derivative of in the sense of distribution, and the duality bracket. Therefore, , so that is a positive distribution on if and only if is a positive distribution on . Finally, the function is convex if and only if is a positive distribution; since is positive continuous, is a positive distribution if and only if is, which concludes the proof.

∎

Let us finally note that our assumptions on are indeed minimal: conversely, if we start from an option price convex in , its first derivative is defined almost everywhere, and so is that of (in or ) since the Black-Scholes mapping in total variance is smooth. Assumption 2.7 imposes some (mild yet sometimes unrealistic) conditions on the volatility surface. It turns out that our results are still valid under weaker conditions on the function . Recall first the following definition:

Definition 4.9.

A continuous function is said to be of class if there exist (for some ), such that , and such that the right and left limits and exist for each .

Consider now the following alternative to Assumption 2.7:

Assumption 4.10.

Assumption 2.7(i), (ii) and (iv) are unchanged, but (iii) is replaced by the weaker version: , with , not constant.

Let denote the (possibly empty) set of discontinuity of . Under our assumption, in the distribution sense is defined as a sum of a continuous measure on and of Dirac masses at each point of discontinuity . We extend the results of Section 4 in the following way: recall the sets and in (4.5) and (4.1), and define

| (4.10) |

Proposition 4.11 (Second coupling condition, general formulation).

Proof.

Similarly to the proof of 4.1, the continuous part of has a density given by

for any and , and the first part of the proposition follows. The remaining part of the distribution is the sum of the disjoint Dirac masses . By localisation it is clear that the distribution is positive if and only if its continuous part on is positive and each of its point mass distribution is positive. Since is non-negative if and only if has a non-negative jump at , the rest of the proposition follows. ∎

Likewise, the analogue of Proposition 4.2 holds as follows:

Proposition 4.12.

If is asymptotically linear and if there is no calendar spread arbitrage, then is neither empty nor bounded from above. Moreover, there is no butterfly arbitrage if and only if the jumps of are non-negative and Proposition 4.2(i)-(ii) hold with and instead of and .

5. The quest for a non-SVI function

In order to find examples of pairs , with different from the SVI parameterisation (2.2), observe first that the second coupling condition (Proposition 4.1) is more geared towards finding out given than the other way round. We first start with a partial result (proved in Appendix A.3) in the other direction, assuming that is asymptotically linear.

Proposition 5.1.

Using this proposition, we now move on to specific examples of non-SVI families.

5.1. First example of non-SVI function

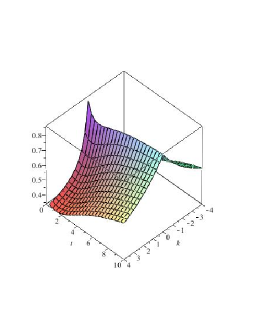

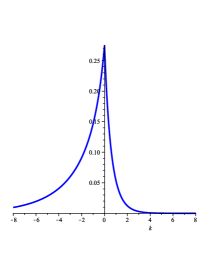

We here provide a triplet , different from the SVI form (2.2), which characterises an arbitrage-free volatility surface via (2.3). Let and

A few remarks are in order:

-

•

the function is continuous on ;

-

•

;

-

•

the map is increasing and its limit is ;

- •

With these functions, the total implied variance (2.3) reads

and the following proposition (proved in Appendix A.5) is the main result here:

Proposition 5.2.

The surface is free of static arbitrage.

5.2. Second example of non-SVI function

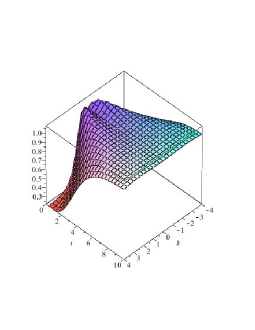

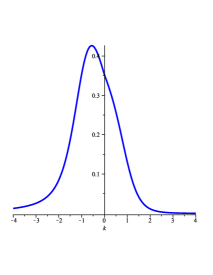

We propose a new triplet characterising an arbitrage-free volatility surface via (2.3). Let and

where and with . Note that when , modulo a constant, the function corresponds to SVI. We could in principle let depend on . The reason for the construction above is that we want to show that the corresponding implied volatility surface is free of static arbitrage for all . The same remarks as in the example in Section 5.1 hold: is continuous on , , is increasing to and is symmetric and continuous on . It is also on , on , and asymptotically linear. The derivative has a positive jump at 0, so that we are back in the framework of Propositions 4.11 and 4.12. With these functions, the total implied variance (2.3) reads

and we can check all the conditions preventing arbitrage (the proof is postponed to Appendix A.4):

Proposition 5.3.

The surface is free of static arbitrage.

Appendix A Proofs

A.1. Proof of Proposition 2.5

The functions and are clearly well-defined and non-negative. Consider first . It is readily seen that the function is a primitive of . We now proceed to prove that is indeed a density. Let denote the cumulative distribution function of the standard Gaussian distribution. An explicit computation yields (the reverse one can be found in [12, Lemma 2.2])

where and their derivatives are evaluated at , and where we have used the identity . Evaluating the right-hand side at , using , we obtain

Therefore if

| (A.1) |

then

where we have used the SMB Condition in Assumption (II) and Lemma 2.4(i). We now prove (A.1), and consider first the case when tends to (positive) infinity. From Lemma 2.4(i), tends to zero. The key point is that is the primitive of a non-negative function, therefore is non-decreasing with a (generalised) limit as . Since converges to zero by Lemma 2.4(ii), we deduce that also converges to . From [23, Proof of Theorem 5.3], the inequality holds for any so that is necessarily non-positive. Assume that is negative; since , then is eventually decreasing. Since it is bounded from below by zero, there exists a sequence going to infinity such that converges to zero by the mean value theorem, and hence .

Let us now consider the case where tends to negative infinity. Using similar arguments, the quantity tends to . Assume that . Then is decreasing for small enough. Since is positive, this implies that for some and small enough. In particular is bounded. Since for all by [23, Theorem 5.1], then for small enough, the inequalities hold, and the term outside the exponential in (A.1) is bounded. Since the exponential converges to zero by Lemma 2.4(ii), we obtain . If , then is increasing for small enough. We conclude as above by the mean value theorem since is increasing and bounded from below. Therefore and the limit (A.1) holds.

So far we have proved that is the density of probability associated to Call option prices with implied volatility . Consider now the function . Then for all , , and it follows by inspection that . Consider the function associated to , i.e.

Now , so that . In order for to be a genuine density, we need to check conditions symmetric to those ensuring that is a density. The condition symmetric to the SMB assumption (II) is precisely Condition (i) in Lemma 2.4, and the condition symmetric to the Lemma 2.4(ii) is precisely the LMB assumption (III). Therefore is also a density, associated to a Call option price with implied variance . Finally the identity follows immediately from the equality .

A.2. Proof of Proposition 4.2

Assume that is asymptotically linear and that there is no calendar spread arbitrage. The proof relies on the decomposition of the real line into the disjoint unions , for any . As in the proof of Proposition 4.1, butterfly arbitrage is precluded on , so that we are left with and .

Consider first Case (ii). If , the inequality in the proposition follows from (4.4). When , in view of (4.4), the inequality is equivalent to . Since is strictly negative on , and non-negative on , absence of butterfly arbitrage on is equivalent to

where the inequalities are trivial (bounds equal to ) whenever . In fact, on , this inequality is trivially satisfied, and the result holds.

Consider now Case (i) in the proposition, which corresponds to the set . We can in fact restrict our attention to since is empty; the map is non-decreasing on by Proposition 3.6. On the map is clearly also non-decreasing on . Therefore is a non-decreasing family of sets and thus, in view of (4.4), absence of butterfly arbitrage () on this set is equivalent to

when , which in turn is equivalent to

When , the previous infimum is precisely . Now, the set is not empty, and therefore the last upper bound is also equal to .

We note in passing that is not empty. Otherwise, the asymptotic linearity of allows us to choose such that for all . Therefore for all , which in turn yields . The integral diverges to infinity as tends to infinity since whereas the right-hand side is bounded by Definition 3.4. The same argument shows that is not bounded from above.

A.3. Proof of Proposition 5.1

In the generalised SVI case (2.3), the function is asymptotically linear (see Definition 3.4) with , and . From subsection 4.2 the condition holds for all . Since , we can define

and therefore

| (A.2) |

Note that , and let . Since the continuous function is increasing on , we can define its inverse , and hence from the equality , Equation (A.2) reads

where all the inequalities on the right-hand side are considered for . The third line is obtained by integration between and on both sides of second line. Let and . We then obtain the condition

| (A.3) |

Note that remains non-negative if we increase or decrease ; indeed , so that the condition is equivalent to . Finally let us translate condition (A.3) into conditions on . Fix and denote , then , which is equivalent to . The discriminant is equal to and is clearly non-negative. Condition (A.3) is therefore equivalent to

Given (equivalently ) we obtain where and .

A.4. Proof of Proposition 5.3

The function defined in (3.1) therefore reads , with and is strictly decreasing from to . Regarding the function , it is clearly continuous, increasing from to and for all , with . Since is increasing and for all , the first coupling conditions in Proposition 3.1 are satisfied, and the volatility surface is free of calendar spread arbitrage. We now need to check the second coupling condition, namely Proposition 4.1. For , is , and we can indeed apply Proposition 4.1. Since is asymptotically linear, we can alternatively check Proposition 4.2. The equality

| (A.4) |

holds for all and hence the sets and defined in (4.5) are equal to and , where . The two conditions in Proposition 4.2 read

| (A.5) |

From the proof of Proposition 4.2, we know that when , the first condition simplifies to

| (A.6) |

Now, immediate computations yield which, as a function of is defined on , is strictly increasing on and strictly decreasing on . Therefore, its infimum over the interval is precisely attained at (by symmetry) and is equal to . Since by construction , Inequality (A.6) is thus equivalent to . This inequality is clearly not true for any and ; however straightforward considerations show that there exists a unique such that the map is strictly increasing on and strictly decreasing on with and . Therefore the inequality is satisfied for all if and only if .

We now check the second inequality (A.5) above. Straightforward computations show that

which increases on from to and decreases on from to . The map is decreasing on , increasing on and maps the real line to . Therefore, for any , , we have

with defined in (A.4). Now a quick look at the function shows that it is bounded above by , with . Define the function by . There exists a unique such that is strictly increasing on and strictly decreasing on with . Setting , the inequality is clearly satisfied for any and all . To conclude, note that for , the second derivative has a mass at the origin, but is convex which implies that this mass is positive and that in the distributional sense following Section 4.4. Therefore the implied volatility surface is free of static arbitrage and the proposition follows.

A.5. Proof of Proposition 5.2

The function in (3.1) here reads , and is decreasing from to . The function in (3.1) is clearly continuous, increasing from to and

with . By Proposition 3.1, straightforward computations then show that the volatility surface is free of calendar-spread arbitrage. Now, for any , we have

which is a decreasing function of with limit equal to zero. Therefore , and for any , . Let us check that the generalised SVI surface parameterised by the previous triplet satisfies as a distribution. Indeed we only checked that as a function defined everywhere except at the origin (where as usual in distribution notations, is a function defined where is defined). Here (where stands for the Dirac mass at the origin), so that , which is positive since . Finally,

decreases to . Since , the condition suffices to prevent butterfly arbitrage.

Appendix B Lee’s moment formula in the asymptotically linear case

In Section 2 we stressed that, following Roper or the variant in Proposition 2.5, the positivity of the operator in (2.1) guarantees the existence of a martingale explaining market prices. As a consequence, the celebrated moment formula [19] holds:

Theorem B.1 (Roger Lee’s moment formula [19]).

Let represent the stock price at time , assumed to be a non-negative random variable with positive and finite expectation. Let and . Then and .

We show here that, at least in the asymptotically linear case (Definition 3.4), this moment formula can be derived in a purely analytic fashion.

Proposition B.2.

Consider a function satisfying the following conditions:

-

(1)

and for all ;

-

(2)

;

-

(3)

.

Let be a random variable with density , associated to by Proposition 2.5. Then and

Proof.

Condition (1) implies Proposition 2.5(I), and Conditions (2) and (3) imply the SMB and LMB limits in Proposition 2.5(II)-(III). Therefore by Proposition 2.5, the centred probability density is well defined on and, for any , we have , where

As tends to infinity, straightforward computations show that and . Since is a second-order strictly convex polynomial with , the function is integrable as long as , i.e. , or . In other words, we have proved that . ∎

References

- [1] S. Benaim and P. Friz. Regular Variation and Smile Asymptotics. Mathematical Finance, 19(1):1-12, 2009.

- [2] H. Berestycki, J. Busca and I. Florent. Computing the implied volatility in stochastic volatility models. Communications on Pure and Applied Mathematics, 57(10): 1352-1373, 2004.

- [3] P. Carr and R. Lee. Put-Call Symmetry: Extensions and Applications. Mathematical Finance, 19(4): 523-560, 2009.

- [4] P. Carr and L. Wu. A new simple approach for for constructing implied volatility surfaces. Preprint available at papers.ssrn.com/sol3/papers.cfm?abstract_id=1701685, 2010.

- [5] A. Cox and D. Hobson. Local martingales, bubbles and option prices. Finance and Stochastics, 9: 477-492, 2005.

- [6] E. Ekstrom and D. Hobson. Recovering a time-homogeneous stock price process from perpetual option prices. Annals of Applied Probability, 21(3): 1102-1135, 2011.

- [7] E. Ekstrom, D. Hobson, S. Janson and and J. Tysk. Can time-homogeneous diffusions produce any distribution? Probability Theory and Related Fields, 155: 493-520, 2013.

- [8] M. Fengler. Arbitrage-free smoothing of the implied volatility surface. Quantitative Finance, 9(4): 417-428, 2009.

- [9] P. Friz, S. Gerhold, A. Gulisashvili and S. Sturm. Refined implied volatility expansions in the Heston model. Quantitative Finance, 11(8): 1151-1164, 2011.

- [10] J. Gatheral. A parsimonious arbitrage-free implied volatility parameterization with application to the valuation of volatility derivatives. Presentation at Global Derivatives, 2004.

- [11] J. Gatheral. The Volatility Surface: A Practitioner’s Guide. Wiley Finance, 2006.

- [12] J. Gatheral and A. Jacquier. Arbitrage-free SVI volatility surfaces. Quantitative Finance, 14(1): 59-71, 2014.

- [13] A. Gulisashvili. Asymptotic formulas with error estimates for Call pricing functions and the implied volatility at extreme strikes. SIAM Journal on Financial Mathematics, 1: 609-614, 2010.

- [14] A. Gulisashvili and E. Stein. Asymptotic behavior of the stock price distribution density and implied volatility in stochastic volatility models. Applied Mathematics & Optimization, 61(3):287-315, 2008.

- [15] P. Hagan, D. Kumar, A. Lesniewski and D. Woodward. Managing smile risk. Wilmott Magazine: 84-108, 2002.

- [16] D. Hobson. Comparison results for stochastic volatility models via coupling. Finance and Stochastics, 14(1): 129-152, 2010.

- [17] P. Jäckel and C. Kahl. Hyp hyp hooray. Wilmott Magazine: 70-81, 2008.

- [18] A. Jacquier and M. Keller-Ressel. Implied volatility in strict local martingale models. arXiv: 1508.04351, 2015.

- [19] R. Lee. The Moment Formula for Implied Volatility at Extreme Strikes. Mathematical Finance, 14(3): 469-480, 2004.

- [20] S. Pal and P. Protter. Analysis of continuous strict local martingales via h-transforms. Stochastic Processes and Applications, 120(8): 1424-1443, 2010.

- [21] M. Roper. Arbitrage-free implied volatility surfaces. Preprint, 2010.

- [22] E. Renault and N.Touzi. Option hedging and implied volatilities in a stochastic volatility model. Mathematical Finance, 6(3): 279-302, 1996.

- [23] C. Rogers and M. Tehranchi. Can the implied volatility surface move by parallel shift? Finance and Stochastics 14(2): 235-248, 2010.

- [24] Zeliade Systems. Quasi-explicit calibration of Gatheral’s SVI model. www.zeliade.com/whitepapers/zwp-0005-SVICalibration.pdf, 2009.