Choice of for -Fold Cross-Validation in Least-Squares Density Estimation

Abstract

This paper studies -fold cross-validation for model selection in least-squares density estimation. The goal is to provide theoretical grounds for choosing in order to minimize the least-squares loss of the selected estimator. We first prove a non-asymptotic oracle inequality for -fold cross-validation and its bias-corrected version (-fold penalization). In particular, this result implies that -fold penalization is asymptotically optimal in the nonparametric case. Then, we compute the variance of -fold cross-validation and related criteria, as well as the variance of key quantities for model selection performance. We show that these variances depend on like , at least in some particular cases, suggesting that the performance increases much from to or , and then is almost constant. Overall, this can explain the common advice to take —at least in our setting and when the computational power is limited—, as supported by some simulation experiments. An oracle inequality and exact formulas for the variance are also proved for Monte-Carlo cross-validation, also known as repeated cross-validation, where the parameter is replaced by the number of random splits of the data.

Keywords: -fold cross-validation, Monte-Carlo cross-validation, leave-one-out, leave--out, resampling penalties, density estimation, model selection, penalization

1 Introduction

Cross-validation methods are widely used in machine learning and statistics, for estimating the risk of a given statistical estimator (Stone, 1974; Allen, 1974; Geisser, 1975) and for selecting among a family of estimators. For instance, cross-validation can be used for model selection, where a collection of linear spaces is given (the models) and the problem is to choose the best least-squares estimator over one of these models. Cross-validation is also often used for choosing hyperparameters of a given learning algorithm. We refer to Arlot and Celisse (2010) for more references about cross-validation for model selection.

Model selection can target two different goals: (i) estimation, that is, minimizing the risk of the final estimator, which is the goal of AIC and related methods, or (ii) identification, that is, identifying the smallest true model in the family considered, assuming it exists and it is unique, which is the goal of BIC for instance; see the survey by Arlot and Celisse (2010) for more details about this distinction. These two goals cannot be attained simultaneously in general (Yang, 2005).

We assume throughout the paper that the goal of model selection is estimation. We refer to Yang (2006, 2007) and Celisse (2014) for some results and references on cross-validation methods with an identification goal.

Then, a natural question arises: which cross-validation method should be used for minimizing the risk of the final estimator? For instance, a popular family of cross-validation methods is -fold cross-validation (Geisser, 1975, often called -fold cross-validation), which depends on an integer parameter , and enjoys a smaller computational cost than other classical cross-validation methods. The question becomes (1) which is optimal, and (2) can we do almost as well as the optimal with a small computational cost, that is, a small ? Answering the second question is particularly useful for practical applications where the computational power is limited.

Surprisingly, few theoretical results exist for answering these two questions, especially with a non-asymptotic point of view (Arlot and Celisse, 2010). In short, it is proved in least-squares regression that at first order, -fold cross-validation is suboptimal for model selection (with an estimation goal) if stays bounded, because -fold cross-validation is biased (Arlot, 2008). When correcting for the bias (Burman, 1989; Arlot, 2008), we recover asymptotic optimality whatever , but without any theoretical result distinguishing among values of in second order terms in the risk bounds (Arlot, 2008).

Intuitively, if there is no bias, increasing should reduce the variance of the -fold cross-validation estimator of the risk, hence reduce the risk of the final estimator, as supported by some simulation experiments (Arlot, 2008, for instance). But variance computations for unbiased -fold methods have only been made in the asymptotic framework for a fixed estimator, and they focus on risk estimation instead of model selection (Burman, 1989).

This paper aims at providing theoretical grounds for the choice of by two means: a non-asymptotic oracle inequality valid for any (Section 3) and exact variance computations shedding light on the influence of on the variance (Section 5). In particular, we would like to understand why the common advice in the literature is to take or , based on simulation experiments (Breiman and Spector, 1992; Hastie et al., 2009, for instance).

The results of the paper are proved in the least-squares density estimation framework, because we can then benefit from explicit closed-form formulas and simplifications for the -fold criteria. In particular, we show that -fold cross-validation and all leave--out methods are particular cases of -fold penalties in least-squares density estimation (Lemma 1).

The first main contribution of the paper (Theorem 5) is an oracle inequality with leading constant , with as for unbiased -fold methods, which holds for any value of . To the best of our knowledge, Theorem 5 is the first non-asymptotic oracle inequality for -fold methods enjoying such properties: the leading constant is new in density estimation, and the fact that it holds whatever the value of had never been obtained in any framework. Theorem 5 relies on a new concentration inequality for the -fold penalty (Proposition 4). Note that Theorem 5 implicitly assumes that the oracle loss is of order for some , that is, the setting is nonparametric; otherwise, Theorem 5 may not imply the asymptotic optimality of -fold penalization. Let us also emphasize that the leading constant is whatever for unbiased -fold methods, with independent from in Theorem 5. So, second-order terms must be taken into account for understanding how the model selection performance depends on . Section 4 proposes a heuristic for comparing these second order terms thanks to variance comparisons. This motivates our next result.

The second main contribution of the paper (Theorem 6) is the first non-asymptotic variance computation for -fold criteria that allows to understand precisely how the model selection performance of -fold cross-validation or penalization depends on . Previous results only focused on the variance of the -fold criterion (Burman, 1989; Bengio and Grandvalet, 2005; Celisse, 2008, 2014; Celisse and Robin, 2008), which is not sufficient for our purpose, as explained in Section 4. In our setting, we can explain, partly from theoretical results, partly from a heuristic argument, why taking, say, is not necessary for getting a performance close to the optimum, as supported by experiments on synthetic data in Section 6.

An oracle inequality and exact formulas for the variance are also proved for other cross-validation methods: Monte-Carlo cross-validation, also known as repeated cross-validation, where the parameter is replaced by the number of random splits of the data (Section 8.1), and hold-out penalization (Section 8.2).

Notation.

For any integer , denotes .

For any vector and any , denotes , denotes the cardinality of and .

For any real numbers , we define , and .

All asymptotic results and notation or are for the regime when the number of observations tends to infinity.

2 Least-Squares Density Estimation and Definition of -Fold Procedures

This section introduces the framework of the paper, the main procedures studied, and some useful notation.

2.1 General Statistical Framework

Let be independent random variables taking value in a Polish space , with common distribution and density with respect to some known measure . Suppose that , which implies that . The goal is to estimate from , that is, to build an estimator such that its loss is as small as possible, where for any , .

Projection estimators are among the most classical estimators in this framework (see, for example, DeVore and Lorentz, 1993 and Massart, 2007). Given a separable linear subspace of (called a model), the projection estimator of onto is defined by

| (1) |

where is the empirical measure; for any , . The quantity minimized in the definition of is often called the empirical risk, and can be denoted by

The function is called the least-squares contrast. Note that since .

2.2 Model Selection

When a finite collection of models is given, following Massart (2007), we want to choose from data one among the corresponding projection estimators . The goal is to design a model selection procedure so that the final estimator has a quadratic loss as small as possible, that is, comparable to the oracle loss . This goal is what is called the estimation goal in the Introduction. More precisely, we aim at proving that an oracle inequality of the form

holds with a large probability. The procedure is called asymptotically optimal when is much smaller than the oracle loss and , as . In order to avoid trivial cases, we will always assume that .

In this paper, we focus on model selection procedures of the form

where is some data-driven criterion. Since our goal is to satisfy an oracle inequality, an ideal criterion is

Penalization is a popular way of designing a model selection criterion (Barron et al., 1999; Massart, 2007)

for some penalty function , possibly data-driven. From the ideal criterion , we get the ideal penalty

| (2) | ||||

is the orthogonal projection of onto in . Let us finally recall some useful and classical reformulations of the main term in the ideal penalty (2), that proves in particular the last equality in Eq. (2): If and denotes an orthonormal basis of in , then

| (3) |

where the last equality follows from Eq. (30) in Appendix A.

2.3 -Fold Cross-Validation

A standard approach for model selection is cross-validation. We refer the reader to Arlot and Celisse (2010) for references and a complete survey on cross-validation for model selection. This section only provides the minimal definitions and notation necessary for the remainder of the paper.

For any subset , let

The main idea of cross-validation is data splitting: some is chosen, one first trains with , then test the trained estimator on the remaining data . The hold-out criterion is the estimator of obtained with this principle, that is,

| (4) |

and all cross-validation criteria are defined as averages of hold-out criteria with various subsets .

Let be a positive integer and let be some partition of . The -fold cross-validation criterion is defined by

Compared to the hold-out, one expects cross-validation to be less variable thanks to the averaging over splits of the sample into and .

2.4 Resampling-Based and -Fold Penalties

Another approach for building general data-driven model selection criteria is penalization with a resampling-based estimator of the expectation of the ideal penalty, as proposed by Efron (1983) with the bootstrap and later generalized to all resampling schemes (Arlot, 2009). Let be some random vector of independent from with

and denote by the weighted empirical distribution of the sample. Then, the resampling-based penalty associated with is defined as

| (5) |

where , denotes the expectation with respect to only (that is, conditionally to the sample ), and is some positive constant. Resampling-based penalties have been studied recently in the least-squares density estimation framework (Lerasle, 2012), assuming that is exchangeable, that is, its distribution is invariant by any permutation of its coordinates.

Since computing exactly has a large computational cost in general for exchangeable , some non-exchangeable resampling schemes were introduced by Arlot (2008), inspired by -fold cross-validation: given some partition of , the weight vector is defined by for some random variable with uniform distribution over . Then, so that the associated resampling penalty, called -fold penalty, is defined by

| (6) |

where is left free for flexibility, which is quite useful according to Lemma 1 below.

2.5 Links Between -Fold Penalties, Resampling Penalties and (Corrected) -Fold Cross-Validation

In this paper, we focus our study on -fold penalties because Lemma 1 below shows that formula (2.4) covers all -fold and resampling-based procedures mentioned in Sections 2.3 and 2.4.

First, when , the only possible partition is , and the -fold penalty is called the leave-one-out penalty . The associated weight vector is exchangeable, hence Eq. (2.4) leads to all exchangeable resampling penalties since they are all equal up to a deterministic multiplicative factor in the least-squares density estimation framework when , as proved by Lerasle (2012).

For -fold methods, let us assume is a regular partition of , that is,

| () |

Then, we get the following connection between -fold penalization and cross-validation methods.

Lemma 1

Remark 2

Eq. (7) was first proved by Arlot (2008) in a general framework that includes least-squares density estimation, assuming only (). Eq. (10) follows from Lerasle (2012, Lemma A.11) since belongs to the family of exchangeable resampling penalties, with weights and is randomly chosen uniformly over ; note that for these weights. It can also be deduced from Proposition 3.1 by Celisse (2014), see Section A.1.

Remark 3

It is worth mentioning here the cross-validation estimators studied by Massart (2007, Chapter 7). First, the unbiased cross-validation criterion defined by Rudemo (1982) is exactly (see also Massart, 2007, Section 7.2.1). Second, the penalized estimator of Massart (2007, Theorem 7.6) is the estimator selected by the penalty

for some such that (see Section A.1 for details).

So, in the least-squares density estimation framework and assuming only (), Lemma 1 shows that it is sufficient to study -fold penalization with a free multiplicative factor in front of the penalty for studying also -fold cross-validation (), corrected -fold cross-validation (), the leave--out ( and ) and all exchangeable resampling penalties. For any and some partition of into pieces, taking , the -fold penalization criterion is denoted by

| (11) |

A key quantity in our results is the bias . From Lemma 13 in Section A.2, we have

| (12) |

so that for any ,

| (13) |

In Sections 3–7, we focus our study on -fold methods, that is, we study the performance of the -fold penalized estimators , defined by

| (14) |

for all values of and . Additional results on hold-out (penalization) are given in Section 8.2 to complete the picture.

3 Oracle Inequalities

In this section, we state our first main result, that is, a non-asymptotic oracle inequality satisfied by -fold procedures. This result holds for any divisor of , any constant in front of the penalty with , and provides an asymptotically optimal oracle inequality for the selected estimator when (assuming the setting is non parametric). In addition, as proved by Section 2.5, it implies oracle inequalities satisfied by leave--out procedures for all .

3.1 Concentration of -Fold Penalties

Concentration is the key property to establish oracle inequalities. Let us start with some new concentration results for -fold penalties.

Proposition 4

Let be i.i.d. real-valued random variables with density , some partition of into pieces satisfying (), a separable linear space of measurable functions and an orthonormal basis of . Define

where is defined by Eq. (1), and for any ,

Then, an absolute constant exists such that for any , with probability at least , for any , the following two inequalities hold true

| (15) | ||||

| (16) |

Proposition 4 is proved in Section A.2. Eq. (15) gives the concentration of the -fold penalty around its expectation , see Eq. (12). Eq. (16) gives the concentration of the -fold penalty around the ideal penalty, see Eq. (2). Optimizing over , the first order of the deviations of around is driven by . The deviation term in Proposition 4 does not depend on and cannot therefore help to discriminate between different values of this parameter.

3.2 Example: Histogram Models

Histograms on provide some classical examples of collections of models. Let be a measurable subset of , denote the Lebesgue measure on and be some countable partition of such that for any . The histogram space based on is the linear span of the functions where and for every , . More precisely, we illustrate our results with the following examples.

Example 1 (Regular histograms on )

In Example 1, defining for every , for every , since is constant and equal to . Therefore, Proposition 4 shows that is asymptotically equivalent to when . Penalties of the form of are classical and have been studied for instance by Barron et al. (1999).

Example 2 (-rupture points on )

where , and for any such that and any , is defined as the union

In other words, splits into pieces (at the ), and then splits the -th piece into pieces of equal size.

In Example 2, the function is constant on each interval , equal to , therefore,

3.3 Oracle Inequality for -Fold Procedures

In order to state the main result, we introduce the following hypotheses:

-

•

A uniform bound on the norm of the ball of the models

() where we recall that and .

-

•

The family of the projections of is uniformly bounded.

() -

•

The collection of models is nested.

()

Hereafter, we define when () holds and when () holds. On histogram spaces, () holds if and only if , and () holds with .

Theorem 5

Let be i.i.d. real-valued random variables with common density , some partition of into pieces satisfying () and be a collection of separable linear spaces satisfying (). Assume that either () or () holds true. Let , and, for any ,

For every , let be the estimator defined by Eq. (1) and where

is defined by Eq. (14). Then, an absolute constant exists such that, for any , with probability at least , for any ,

| (17) |

Taking small enough in Eq. (17), Theorem 5 proves that -fold model selection procedures satisfy an oracle inequality with large probability. The remainder term can be bounded under the following classical assumption

| () |

For instance, () holds in Example 1 with and in Example 2 with . Under (), the remainder term in Eq. (17) is bounded by for some , which is much smaller than the oracle loss in the nonparametric case.

The leading constant in the oracle inequality (17) is by choosing , so the first-order behaviour of the upper bound on the loss is driven by . An asymptotic optimality result can be derived from Eq. (17) only if . The meaning of is the amount of bias of the -fold penalization criterion, as shown by Eq. (13). Given this interpretation of , the model selection literature suggests that no asymptotic optimality result can be obtained in general when in the nonparametric case (see, for instance, Shao, 1997). Therefore, even if the leading constant is only an upper bound, we conjecture that it cannot be taken as small as unless ; such a result can be proved in our setting using similar arguments and assumptions as the ones of Arlot (2008) for instance.

For bias-corrected -fold cross-validation, that is, hence , Theorem 5 shows a first-order optimal non-asymptotic oracle inequality, since the leading constant can be taken equal to , and the remainder term is small enough in the nonparametric case, under assumption (), for instance. Such a result valid with no upper bound on had never been obtained before in any setting.

-fold cross-validation is also analyzed by Theorem 5, since by Lemma 1 it corresponds to , hence . When is fixed, the oracle inequality is asymptotically sub-optimal, which is consistent with the result proved in regression by Arlot (2008). On the contrary, if has blocs, with , Theorem 5 implies under assumption () the asymptotic optimality of -fold cross-validation in the nonparametric case.

Assuming is necessary, according to minimal penalty results proved by Lerasle (2012). Assuming only simplifies the presentation; if , the same proof shows that Theorem 5 holds with replaced by .

An oracle inequality similar to Theorem 5 holds in a more general setting, as proved in a previous version of this paper (Arlot and Lerasle, 2012, Theorem 1); we state a less general result here for simplifying the exposition, since it does not change the message of the paper. First, assumption () can be relaxed into assuming the partition is close to regular, that is,

| () |

which can hold for any . Second, data can belong to a general Polish space , at the price of some additional technical assumption.

3.4 Comparison with Previous Works on -Fold Procedures

Few non-asymptotic oracle inequalities have been proved for -fold penalization or cross-validation procedures.

Concerning cross-validation, previous oracle inequalities are listed in the survey by Arlot and Celisse (2010). In the least-squares density estimation framework, oracle inequalities were proved by van der Laan et al. (2004) in the -fold case, but compared the risk of the selected estimator with the risk of an oracle trained with data. In comparison, Theorem 5 considers the strongest possible oracle, that is, trained with data. Optimal oracle inequalities were proved by Celisse (2014) for leave--out estimators with , a case also treated in Theorem 5 by taking and as shown by Lemma 1. If , , hence and we recover the result of Celisse (2014).

Concerning -fold penalization, previous results were either valid for only—by Massart (2007, Theorem 7.6) and Lerasle (2012) for least-squares density estimation, by Arlot (2009) for regressogram estimators—, or for bounded when tends to infinity—by Arlot (2008) for regressogram estimators. In comparison, Theorem 5 provides a result valid for all , except for the assumption that divides , which can be removed (Arlot and Lerasle, 2012). In particular, the loss bound by Arlot (2008) deteriorates when grows, while it remains stable in our result. Our result is therefore much closer to the typical behavior of the loss ratio of -fold penalization, which usually decreases as a function of in simulation experiments, see Section 6 and the experiments by Arlot (2008), for instance.

Theorem 5 may not satisfactorily address the parametric setting, that is, when the collection contains some fixed true model. In such a case, the usual way to obtain asymptotic optimality is to use a model selection procedure targetting identification, that is, taking when . For instance, Celisse (2014, Theorem 3.3) shows that is a sufficient condition for such a result.

4 How to Compare Theoretically the Performances of Model Selection Procedures for Estimation?

The main goal of the paper is to compare the model selection performances of several (-fold) cross-validation methods, when the goal is estimation, that is, minimizing the loss of the final estimator. In this section, we discuss how such a comparison can be made on theoretical grounds, in a general setting.

For some data-driven function , the goal is to understand how depends on when the selected model is

| (18) |

From now on, in this section, is assumed to be a cross-validation estimator of the risk, but the heuristic developed here applies to the general case.

Ideal comparison.

Ideally, for proving that is a better method than in some setting, we would like to prove that

| (19) |

with a large probability, for some .

Previous works and their limits.

When the goal is estimation, the classical way to analyze the performance of a model selection procedure is to prove an oracle inequality, that is, to upper bound (with a large probability or in expectation)

Alternatively, asymptotic results show that when tends to infinity, (asymptotic optimality of ) or (asymptotic equivalence of and ); see Arlot and Celisse (2010, Section 6) for a review of such results. Nevertheless, proving Eq. (19) requires a lower bound on (asymptotic or not), which has been done only once for some cross-validation method, to the best of our knowledge. In some least-squares regression setting, -fold cross-validation () performs (asymptotically) worse than all asymptotically optimal model selection procedures since with a large probability (Arlot, 2008).

The major limitation of all these previous results is that they can only compare to at first order, that is, according to , which only depends on the bias of () as an estimator of , hence, on the asymptotic ratio between the training set size and the sample size (Arlot and Celisse, 2010, Section 6). For instance, the leave--out and the hold-out with a training set of size cannot be distinguished at first order, while the leave--out performs much better in practice, certainly because its “variance” is much smaller.

Beyond first-order.

So, we must go beyond the first-order of and take into account the variance of . Nevertheless, proving a lower bound on is already challenging at first order—probably the reason why only one has been proved up to now, in a specific setting only—so the challenge of computing a precise lower bound on the second order term of seems too high for the present paper. We propose instead a heuristic showing that the variances of some quantities—depending on and on —can be used as a proxy to a proper comparison of and at second order. Since we focus on second-order terms, from now on, we assume that and have the same bias, that is,

| () |

In least-squares density estimation, given Lemma 1, this means that for ,

as defined by Eq. (11), with different partitions satisfying () with different , but the same constant ; corresponds to the unbiased case.

The variance of the cross-validation criteria is not the correct quantity to look at.

If we were only comparing cross-validation methods as estimators of for every single , we could naturally compare them through their mean squared errors. Under assumption (), this would mean to compare their variances. This can be done from Eq. (23) below, but it is not sufficient to solve our problem, since it is known that the best cross-validation estimator of the risk does not necessarily yield the best model selection procedure (Breiman and Spector, 1992). More precisely, the selected model defined by Eq. (18) is unchanged when is translated by any random quantity, but such a translation does change and can make it as large as desired. For model selection, what really matters is that

as often as possible for every , and that most mistakes in the ranking of models occur when is small, so that cannot be much larger than .

Heuristic.

The heuristic we propose goes as follows. For simplicity, we assume that is uniquely defined. If the goal was identification, we could directly state that for any , the smaller is for all , the better should be the performance of . In this paper, our goal is estimation, but a similar claim can be conjectured by considering “all sufficiently far from in terms of risk”, that is, all such that is significantly worse than . Indeed, for any “close to ” in terms of risk, selecting instead of does not significantly change the performance of ; on the contrary, for any “far from ” in terms of risk, selecting instead of does increase significantly the risk .

Then, our idea is to find a proxy for , that is, a quantity that should behave similarly as a function of and its “variance” properties. For all , let , some standard Gaussian random variable and, for all , . Then, for every

| (20) | ||||

| (21) | ||||

So, if for all “sufficiently far from ”, should be better than . Assuming () holds true and that

| () |

this leads to the following heuristic

| (22) |

Indeed, for every , assumption () implies that for , hence we can restrict the max in the definition of to all such that is positive. By assumption (), the numerator in the definition of does not depend on , hence the ratio is maximal when the denominator is minimal, which leads to Eq. (22). Let us make some remarks.

- •

- •

-

•

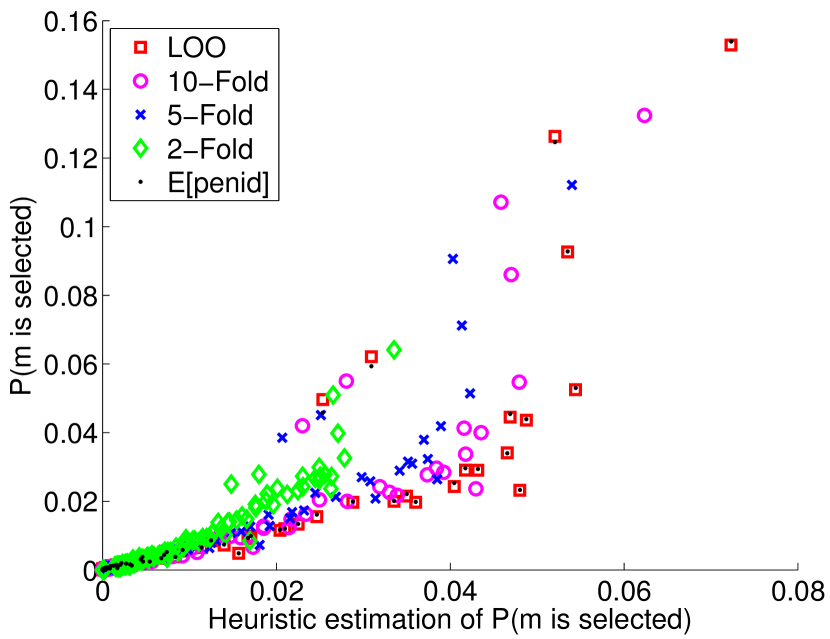

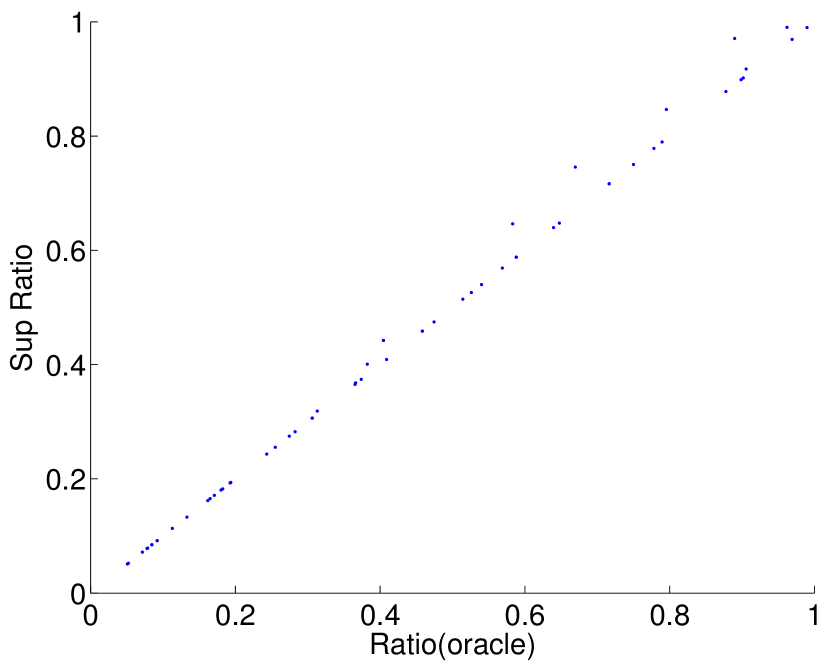

Assumption () is necessary: Figure 3 shows an example where a larger variance corresponds to better performance under assumption () alone.

-

•

As noticed above, the heuristic (22) should apply when the goal is estimation and when the goal is identification, provided that () and () hold true. What should depend on the goal is the suitable amount of bias for as an estimator of the risk .

-

•

Approximation (20) is the strongest one. Clearly, inequality holds true. The equality case occurs is for a very particular dependence setting, that is, when one among the events , , is included into all the others. In general, the left-hand side is significantly smaller than the right-hand side; we conjecture that they vary similarly as a function of .

-

•

The Gaussian approximation (21) for does not hold exactly, but it seems reasonable to make it, at first order at least.

- •

In the heuristic (22), all do not matter equally for explaining a quantitative difference in the performances of . First, we can fix , since intuitively, the strongest candidate against any is , which clearly holds in all our experiments, see Figures 18 and 24 in Section B.6. Second, as mentioned above, if and are very close, that is, is smaller than the minimal order of magnitude we can expect for with a data-driven , taking instead of does not decrease the performance significantly. Third, if is very small, increasing it even by an order of magnitude will not affect the performance of significantly; hence, all such that, say, for all , can also be discarded. Overall, pairs that really matter in (22) are pairs that are at a “moderate distance”, in terms of .

5 Dependence on of -Fold Penalization and Cross-Validation

Let us now come back to the least-squares density estimation setting. Our goal is to compare the performance of cross-validation methods having the same bias, that is, according to Section 2.5, with the same constant but different partitions , where is defined by Eq. (14).

Theorem 6

Unbiased case.

When , Theorem 6 shows that

for some depending on but not on . If we admit that the heuristic (22) holds true, this implies that the model selection performance of bias-corrected -fold cross-validation improves when increases, but the improvement is at most in a second order term as soon as is large. In particular, even if , the improvement from to or is much larger than from to , which can justify the commonly used principle that taking or is large enough.

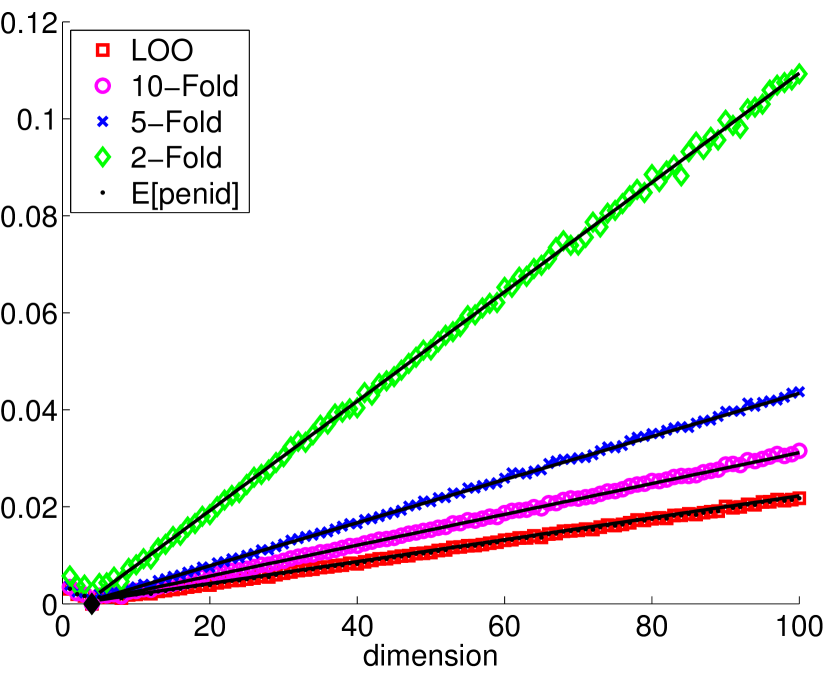

Assuming in addition that and are regular histogram models (Example 1 in Section 3.2) with that divides , then, by Lemma 19 in Section B.1.2,

When is at least as large as , we obtain that the first-order term in the variance is of the form where do not depend on and are of the same order of magnitude, as supported by the numerical experiments of Section 6. Then, increasing from to does reduce significantly the variance, by a constant multiplicative factor.

Let be the criterion we could use if we knew the expectation of the ideal penalty. From Proposition 17 in Section B.1,

which easily compares to formula (24) obtained for the -fold criterion when . Up to smaller order terms, the difference lies in the first term, where is replaced by when using the expectation of the ideal penalty instead of a -fold penalty. In other words, the leave-one-out penalty—that is, taking —behaves like the expectation of the ideal penalty.

We can also compare Eq. (23) with the asymptotic results obtained by Burman (1989), which imply that for any fixed model

with that depend on and . Here, putting in Eq. (23) yields a result with a similar flavour, valid for all , even if Eq. (23) computes the variance of a slightly different quantity.

Cross-validation criteria.

-fold cross-validation and the leave--out are also covered by Theorem 6, according to Lemma 1, respectively with and with and . As in the unbiased case, increasing decreases the variance, and if we admit that the heuristic (22) holds true, -fold cross-validation performs almost as well as the leave--out as soon as is larger than or .

Similarly, the variances of the -fold cross-validation and leave--out criteria, for instance, can be derived from Eq. (23). In the leave--out case, we recover formulas obtained by Celisse (2014) and Celisse and Robin (2008), with a different grouping of the variance components; Eq. (23) clearly emphasizes the influence of the bias—through —on the variance. For -fold cross-validation, we believe that Eq. (23) shows in a simpler way how the variance depends on , compared to the result of Celisse and Robin (2008) which was focusing on the difference between -fold cross-validation and the leave--out; here the difference can be written

A major novelty in Eq. (23) is also to cover a larger set of criteria, such as bias-corrected -fold cross-validation. Note that is generally much larger than

which illustrates again why computing the former quantity might not help for understanding the model selection properties of , as explained in Section 4. For instance, comparing Eq. (23) and (24), changing into in the second term can reduce dramatically the variance when and are close, which happens for the pairs that matter for model selection according to Section 4.

6 Simulation Study

This section illustrates the main theoretical results of the paper with some experiments on synthetic data.

6.1 Setting

In this section, we take and is the Lebesgue measure on . Two examples are considered for the target density and for the collection of models .

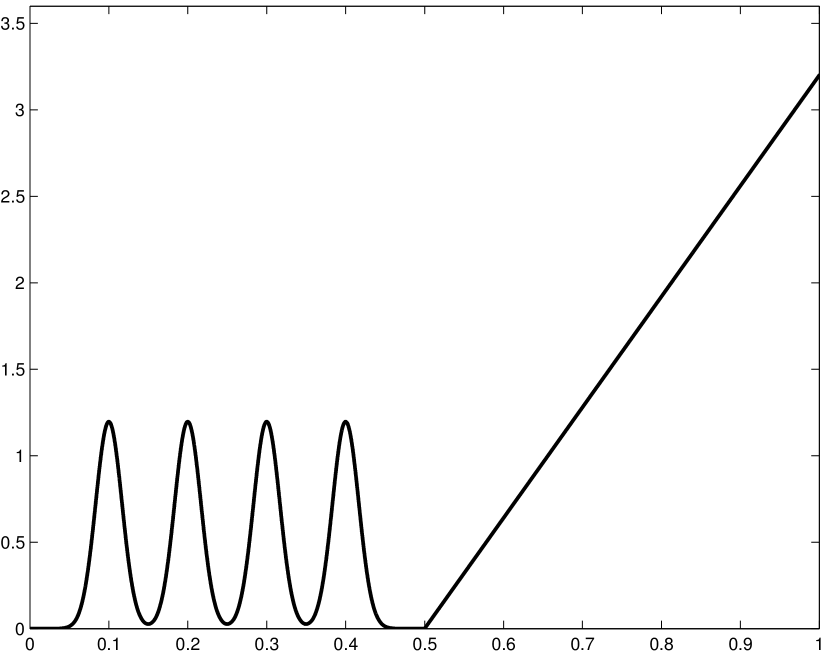

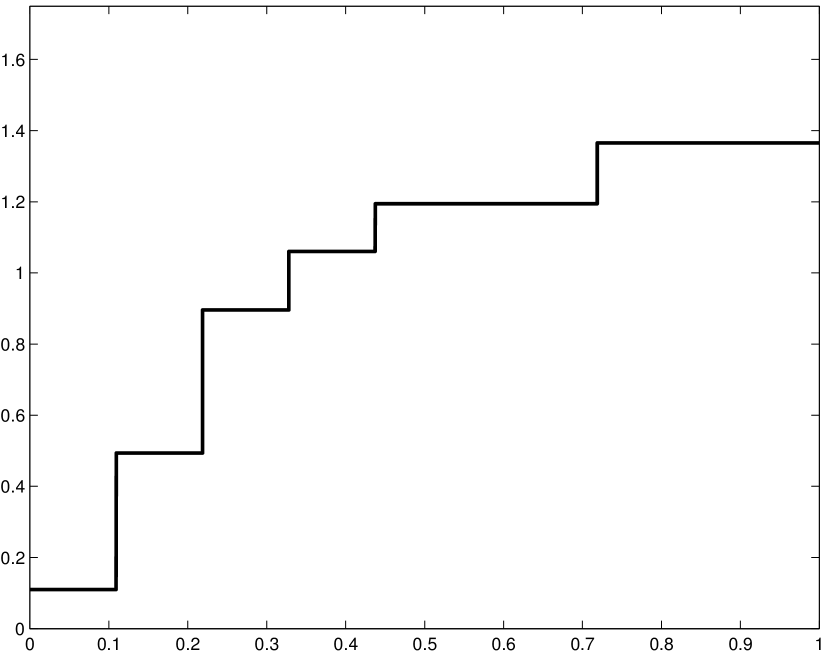

Two density functions are considered, see Figure 1:

-

•

Setting L: .

-

•

Setting S: is the mixture of the piecewise linear density (with weight 0.8) and four truncated Gaussian densities with means and standard deviation (each with weight 0.05).

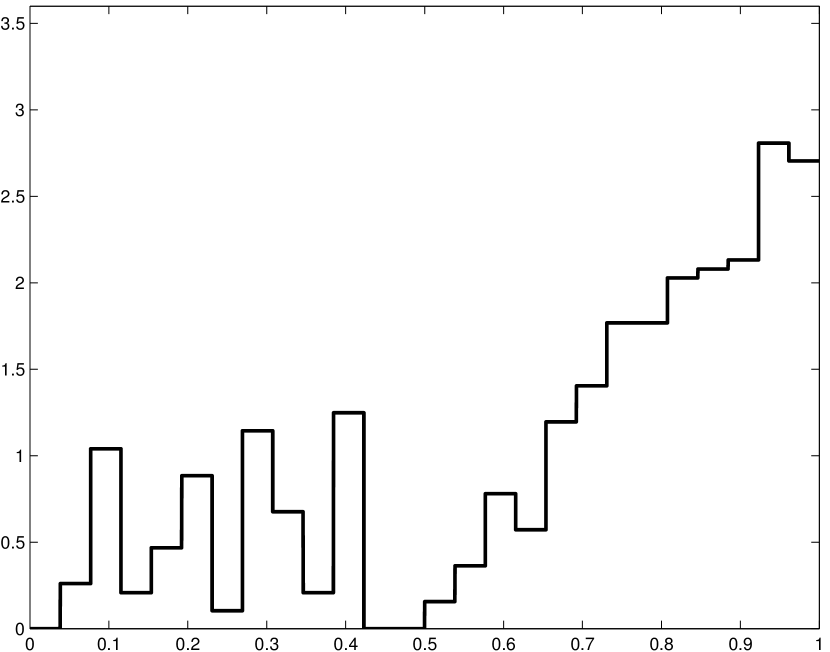

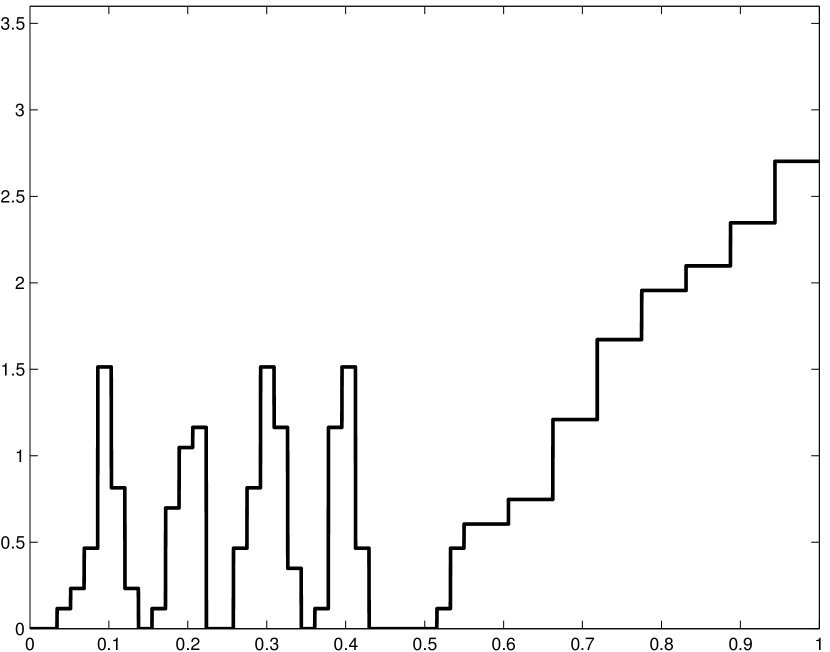

Two collections of models are considered, both leading to histogram estimators: for every , is the set of piecewise constant functions on some partition of .

-

•

“Regu” for regular histograms: where for every , is the regular partition of into bins.

-

•

“Dya2” for dyadic regular histograms with two bin sizes and a variable change-point:

where and for every , is the union of the regular partition of into pieces and the regular partition of into pieces.

The difference between “Regu” and “Dya2” can be visualized on Figure 2, on which the corresponding oracle estimators have been plotted for one sample in setting S, where

While “Regu” is one of the simplest and most classical collections for density estimation, the flexibility of “Dya2” allows to adapt to the variability of the smoothness of . Intuitively, in settings L and S, the optimal bin size is smaller on (where is varying fastly) than on (where is much smaller).

Another point of comparison of Regu and Dya2 is given by Table 1, that reports values of the quadratic risks obtained depending on the collection of models considered. Table 1 shows that in settings L and S, the collection Dya2 helps reducing the quadratic risk by approximately 20% (when comparing the best data-driven procedures of our experiment), and even more when comparing oracle estimators (30% in setting S, 59% in setting L). Therefore, in settings L and S, it is worth considering more complex collections of models (such as Dya2) than regular histograms.

| Setting | Oracle(Regu) | Oracle(Dya2) | Best(Regu) | Best(Dya2) |

|---|---|---|---|---|

| L | ||||

| S |

Let us finally remark that Dya2 does not reduce the quadratic risk in all settings as significantly as in settings L and S. We performed similar experiments with a few other density functions, sometimes leading to less important differences between Regu and Dya2 in terms of risk (results not shown). The oracle model was always better with Dya2, but in two cases, the risk of the best data-driven procedure with Dya2 was larger than with Regu by 6 to 8%.

6.2 Procedures Compared

In each setting, we consider the following model selection procedures:

6.3 Model Selection Performances

In each setting, all procedures are compared on independent synthetic data sets of size . For measuring their respective model selection performances, for each procedure we estimate

by the corresponding average over the simulated data sets; represents the constant that would appear in front of an oracle inequality. The uncertainty of estimation of is measured by the empirical standard deviation of divided by . The results are reported in Table 2 for settings L and S, with the collection Dya2.

| Procedure | L–Dya2 | S–Dya2 |

| pen2F | ||

| pen5F | ||

| pen10F | ||

| penLOO | ||

| 2FCV | ||

| 5FCV | ||

| 10FCV | ||

| LOO | ||

Results for Regu are not reported here since dimensionality-based penalties are already known to work well with Regu (Lerasle, 2012), so -fold methods cannot improve significantly their performance, with a larger computational cost. Complete results (including Regu, with and ) are given in Tables 3 and 4 in Section B.6, showing that the performances of and -fold methods indeed are very close.

Performance as a function of .

Let us first consider -fold penalization. In both settings L and S, as suggested by our theoretical results, decreases when increases. The improvement is large when goes from 2 to 5 (% for L, % for S) and small when goes from 5 to 10 and when goes from 10 to (each time, % for L, % for S). Since the main influence of is on the variance of the -fold penalty, these experiments support our interpretation of Theorem 6 in Section 5: increasing helps much more from 2 to 5 or 10 than from 10 to .

The picture is less clear for -fold cross-validation, for which almost no difference is observed among —less than —, and is minimized for . Indeed, increasing simultaneously decreases the bias and the variance of the -fold cross-validation criterion, leading to various possible behaviours of as a function of , depending on the setting. The same phenomenon has been observed in regression (Arlot, 2008).

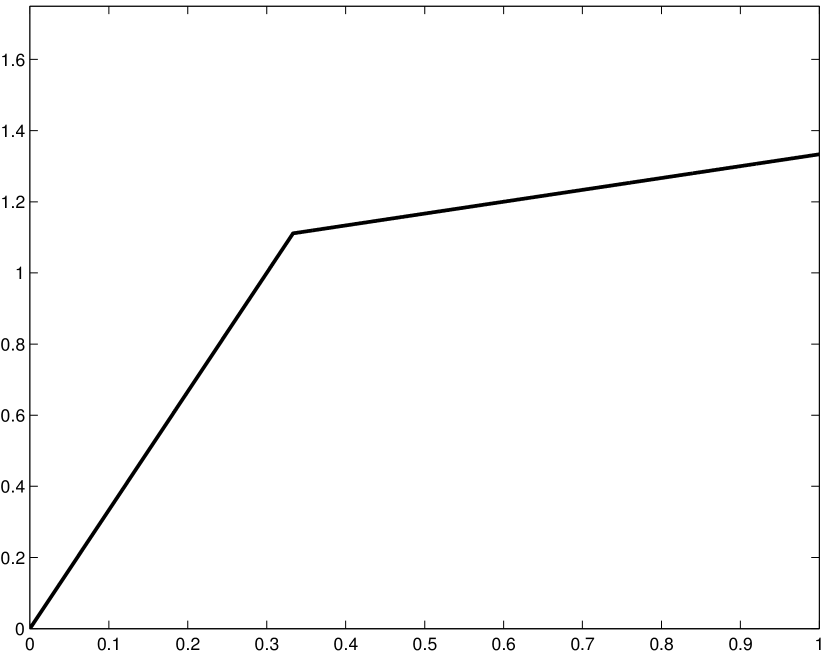

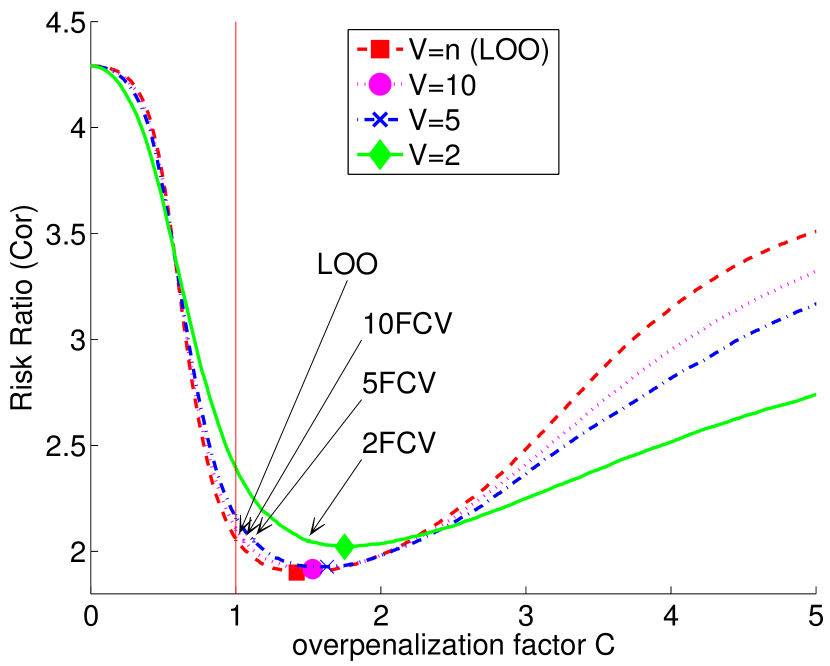

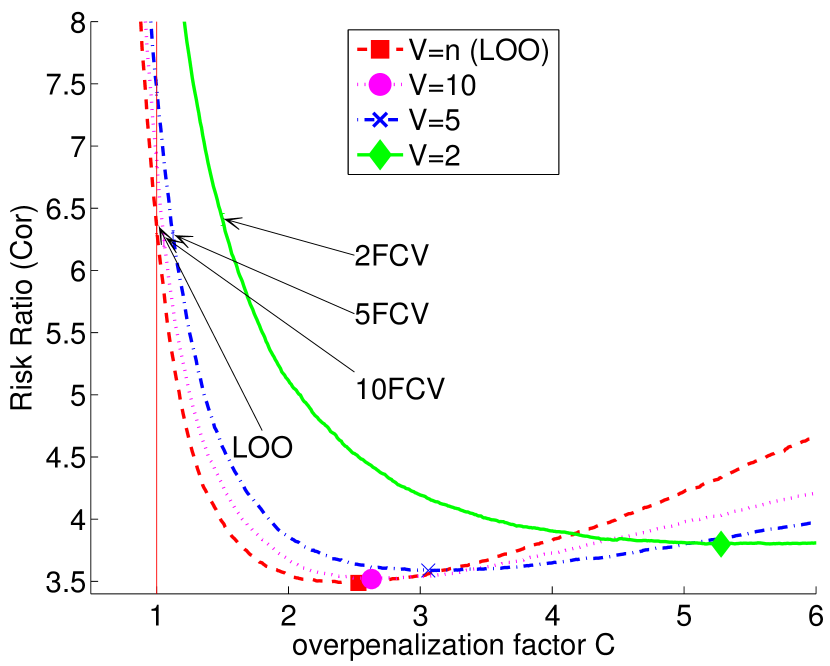

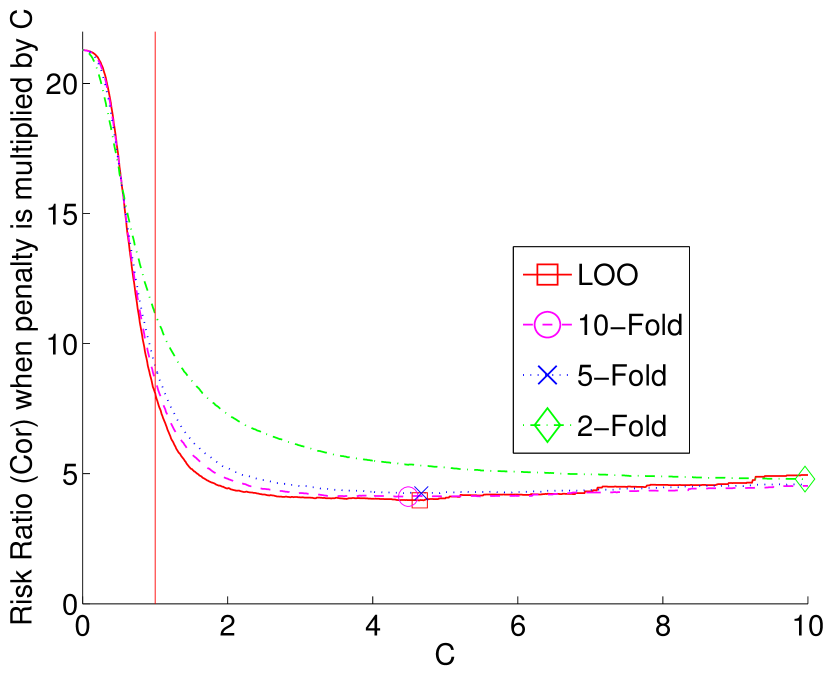

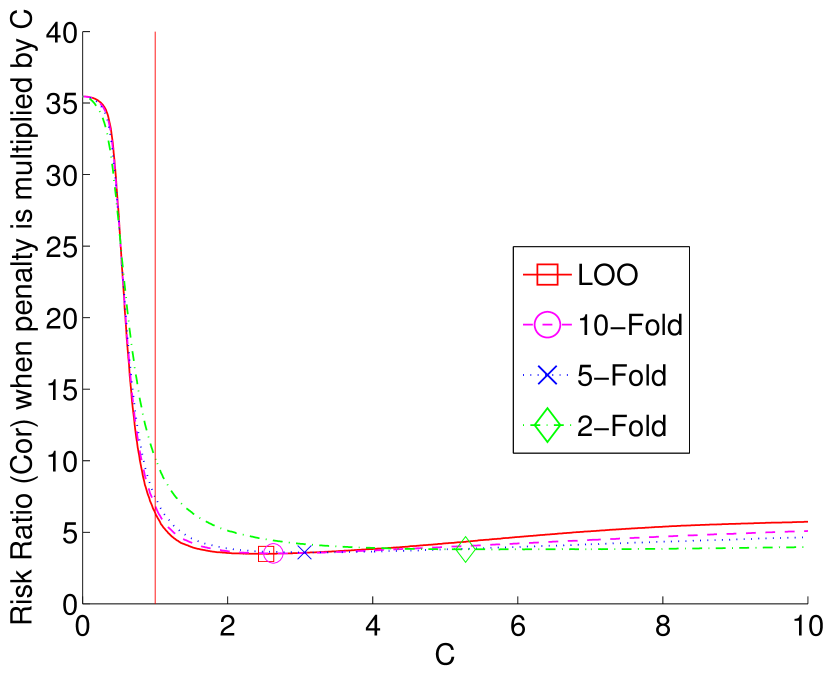

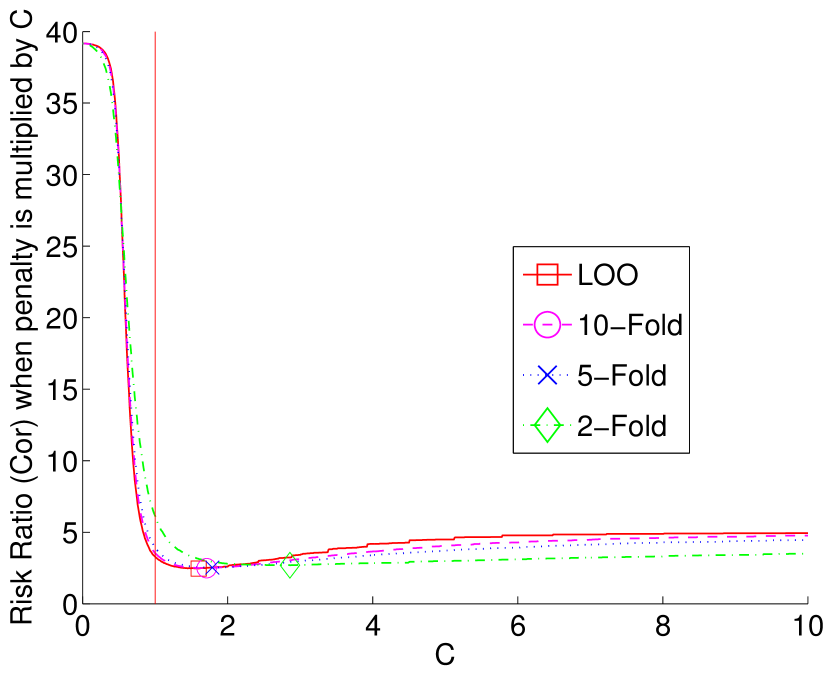

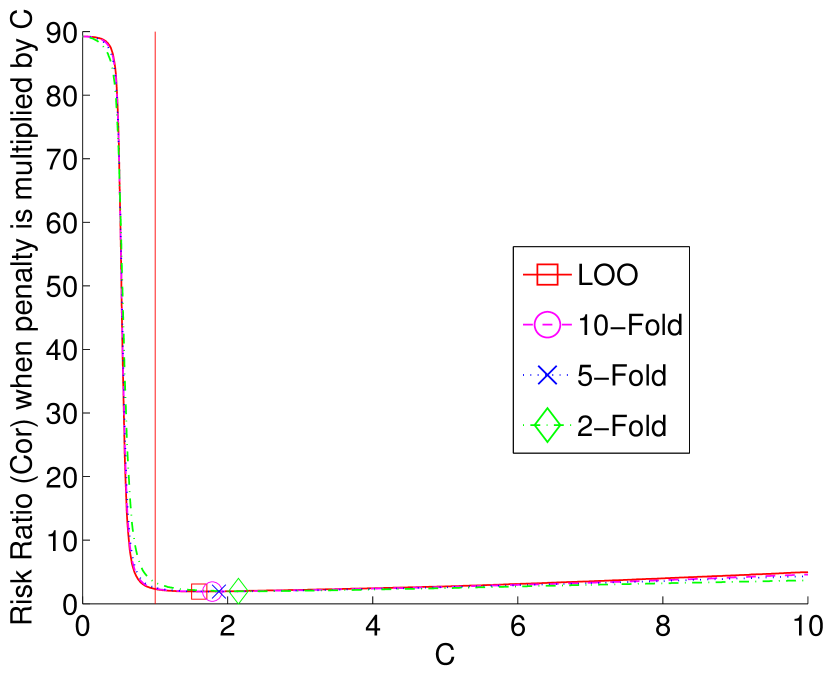

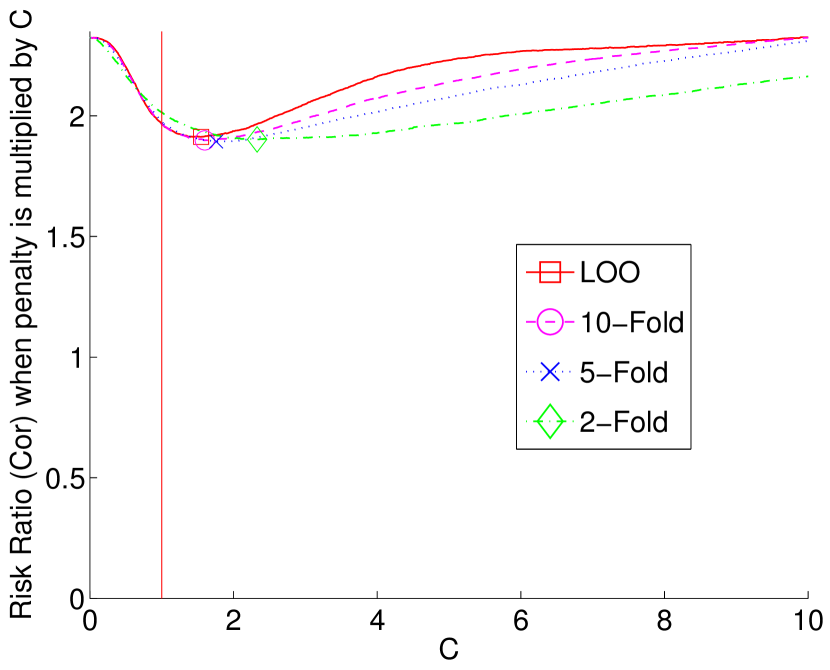

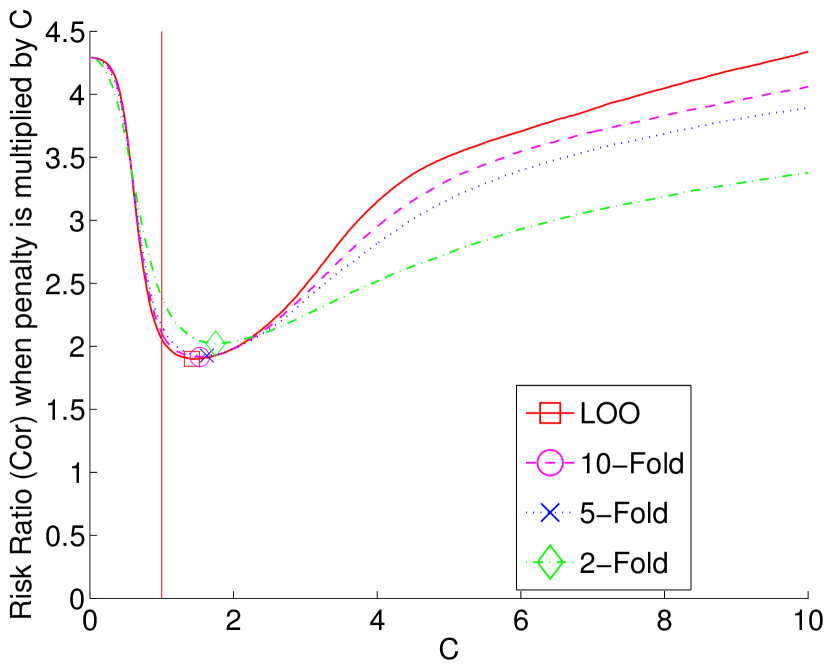

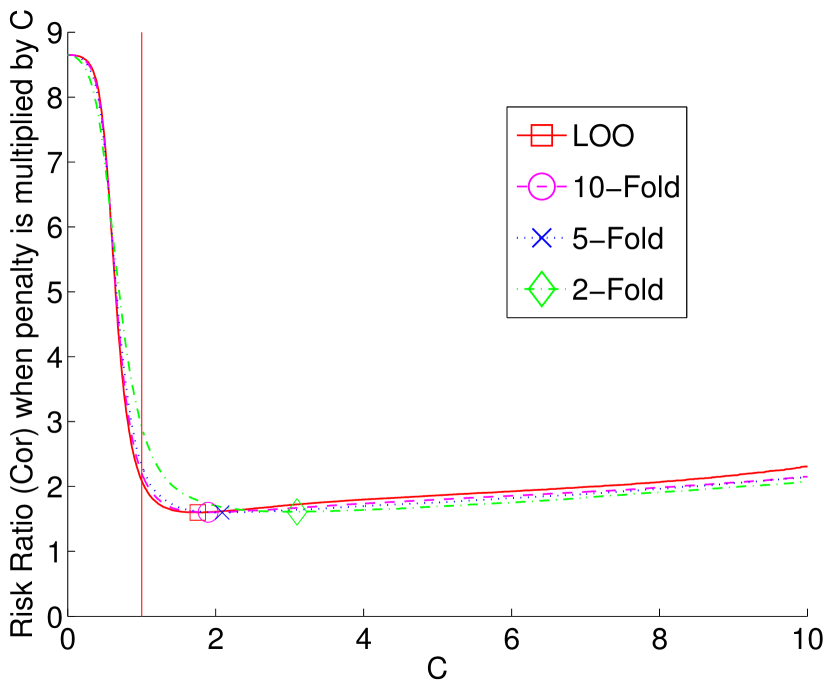

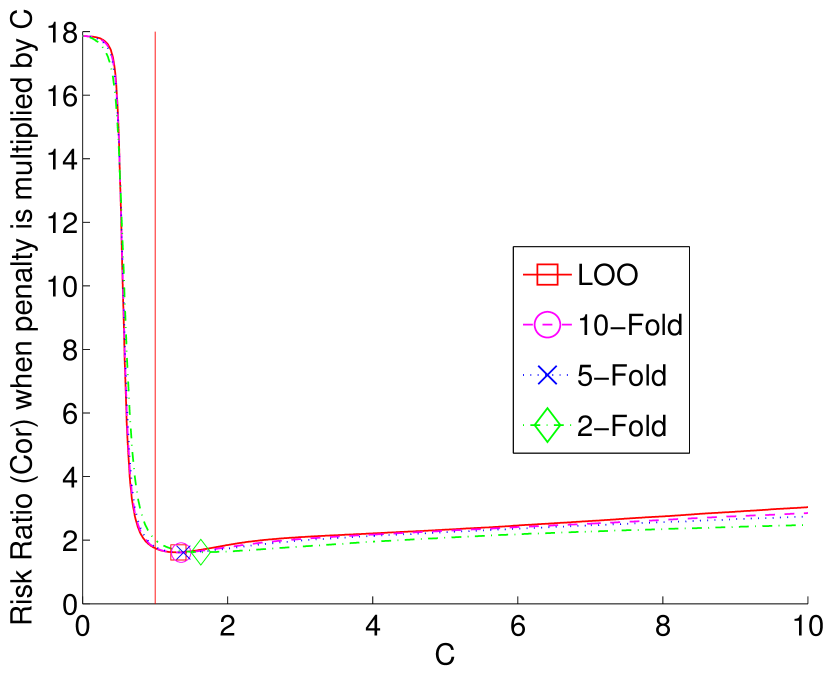

Overpenalization.

In all settings considered in this paper, -fold penalization performs much better when multiplying the penalty by , as illustrated by Figure 3. In particular, the best overpenalization factor for is for L-Dya2 and for S-Dya2, when . Such a phenomenon, which can also be observed in regression (Arlot, 2008), is related to the fact that some nonparametric model selection problems are “practically parametric”, using the terminology of Liu and Yang (2011), that is, BIC beats AIC and the optimal is closer to than to . For instance, Figure 3 shows that L-Dya2 is practically parametric, while S-Dya2 is practically nonparametric since AIC beats BIC and the optimal is close to 1.

Given an overpenalization factor close to its optimal value , -fold penalization performs significantly better than -fold cross-validation in settings S-Dya2 and L-Dya2 (Figure 3). Since -fold cross-validation corresponds to taking

according to Lemma 1, this mostly means that is not close to in these settings. In addition, when is fixed, increasing always improves the performance of -fold penalization, as predicted by the heuristic of Section 4 and the theoretical results of Section 5. Let us emphasize that this fact does not depend on the parametricness of the setting: although the value of is quite different for S-Dya2 and L-Dya2, in both cases, we observe qualitatively the same relationship between and the performance of the procedure.

The results reported in Section B.6 lead to similar conclusions in several other settings, as well as unshown results in a truly parametric setting, with a true model of dimension 2. Although a wider simulation study would be necessary to get general conclusions, this suggests at least that the heuristic of Section 4 and the theoretical results of Section 5 can be applied to both parametric and nonparametric settings.

Figure 3 also helps understanding how the performance of -fold cross-validation depends on in Table 2. Indeed, the performance of -fold cross-validation for each value of can be visualized on Figure 3 by taking the point of abscissa on the curve associated with -fold penalization. Two phenomena are coupled when , which always holds in our simulations for -fold cross-validation since and the estimated value of is always larger. (i) The performance improves when is fixed and gets closer to . (ii) The performance improves when is fixed and increases. Even if both phenomena (i) and (ii) seem quite universal, their coupling can result in various behaviours for -fold cross-validation as a function of , as shown by Table 3 in Section B.6 for instance.

Other comments.

- •

-

•

In other settings considered in a preliminary phase of our experiments, for -fold penalization, differences between and were sometimes smaller or not significant, but always with the same ordering (that is, the worse performance for when is fixed). In a few settings, for which the “change-point” in the smoothness of was close to the median of , we found among the best procedures with collection Dya2; then, -fold penalization and cross-validation always had a performance very close to . Both phenomena lead us to discard all settings for which there were no significant difference to comment.

6.4 Variance as a Function of

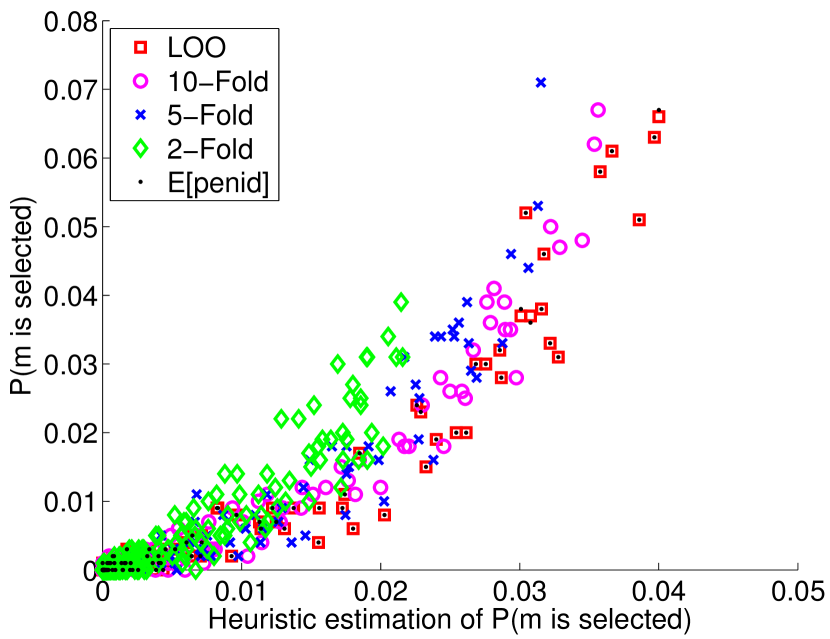

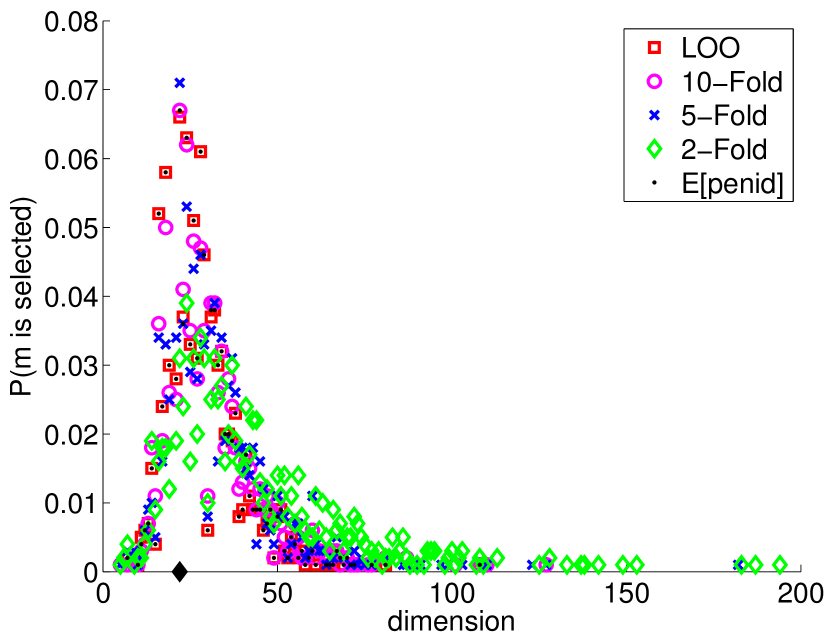

We now illustrate the results of Section 5 about the variance of -fold penalization and the heuristic of Section 4 about its influence on model selection. We focus on the unbiased case, that is, criteria with partitions satisfying (). Since the distribution of then only depends on , we write instead of by abuse of notation. All results presented in this subsection have been obtained from independent samples in setting S with a sample size and the collection Regu—for which models are naturally indexed by their dimension.

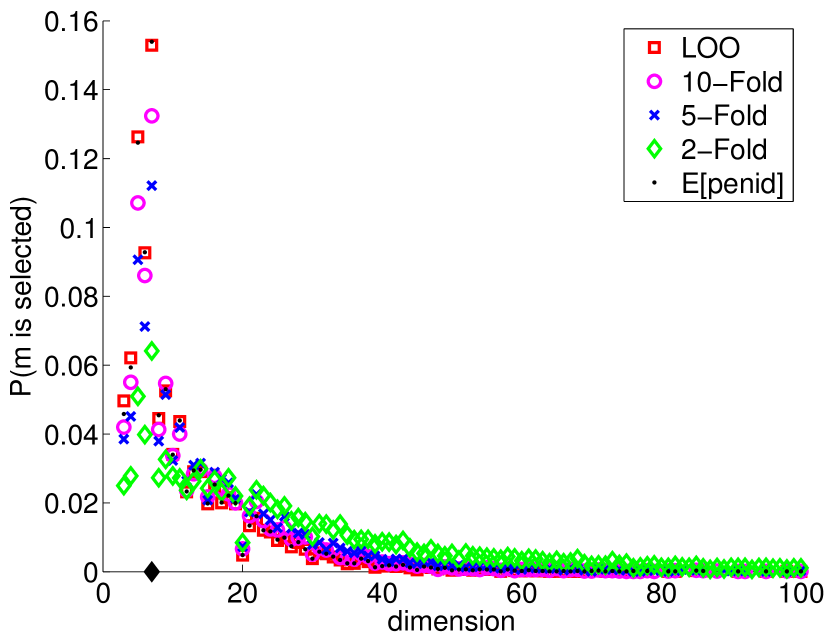

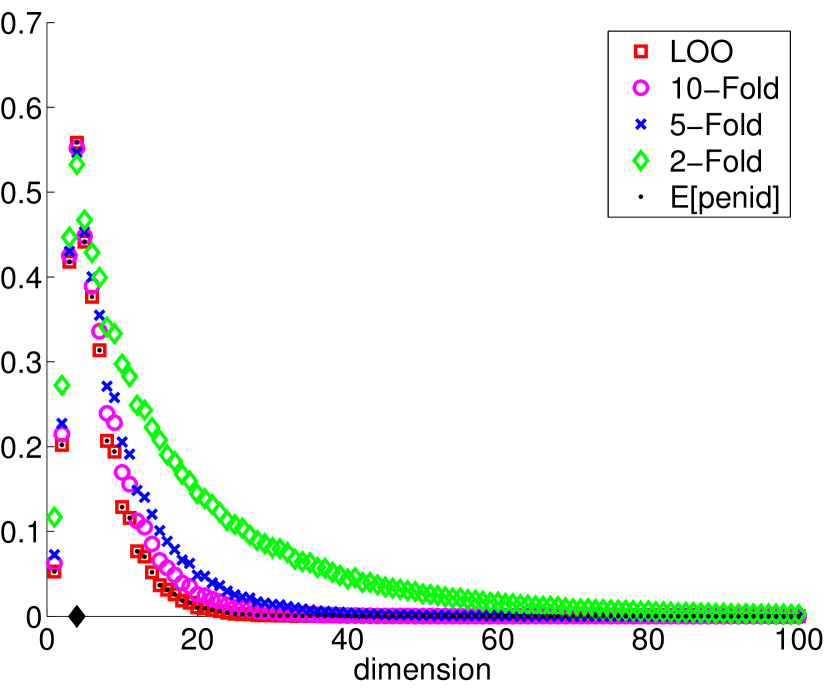

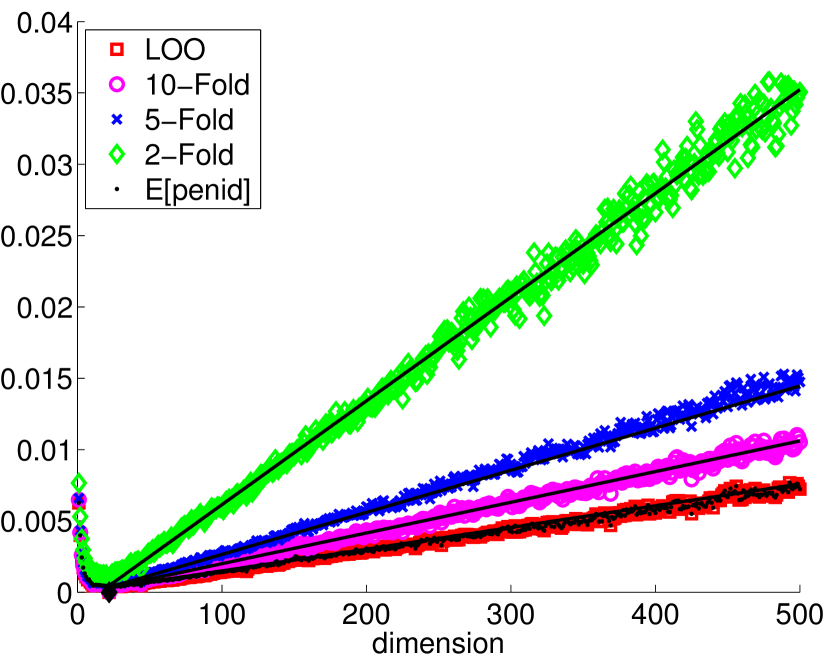

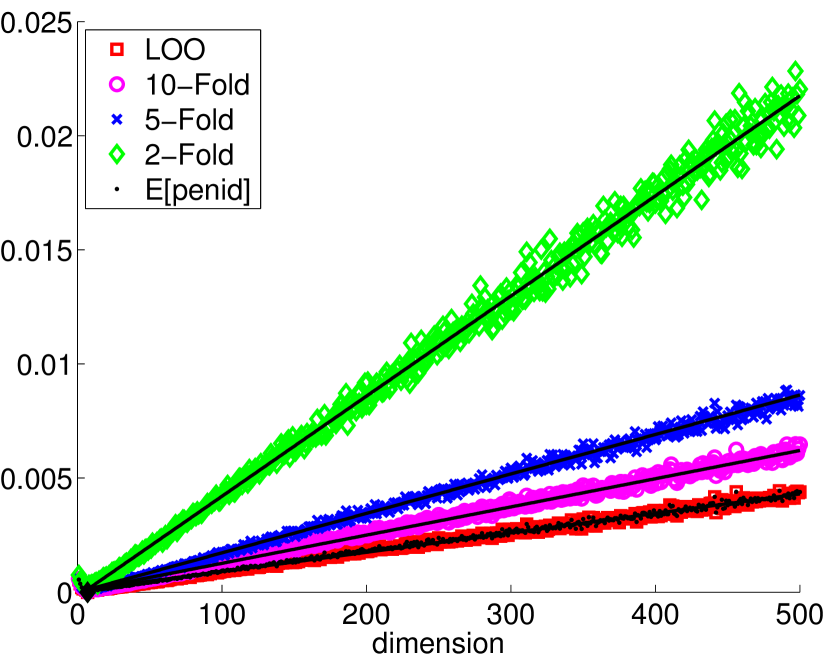

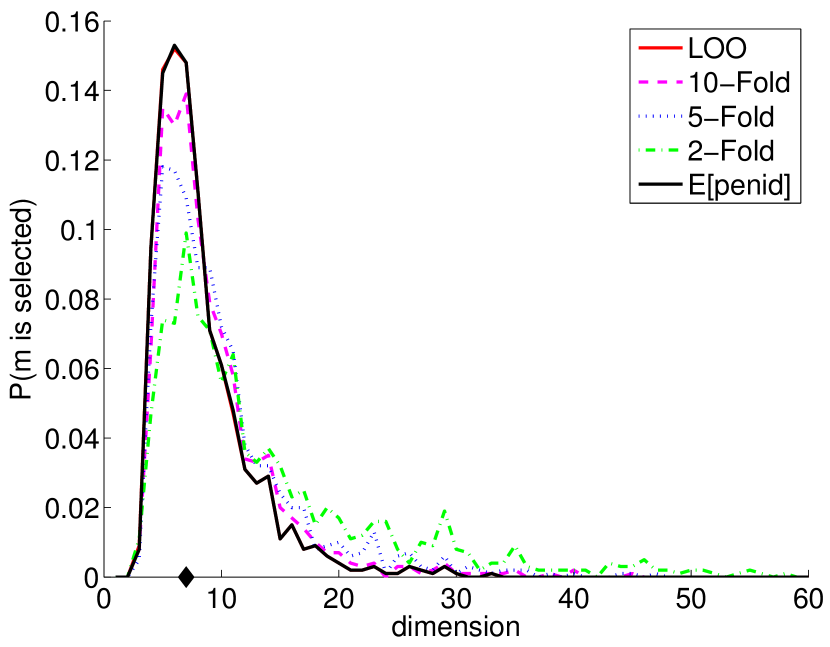

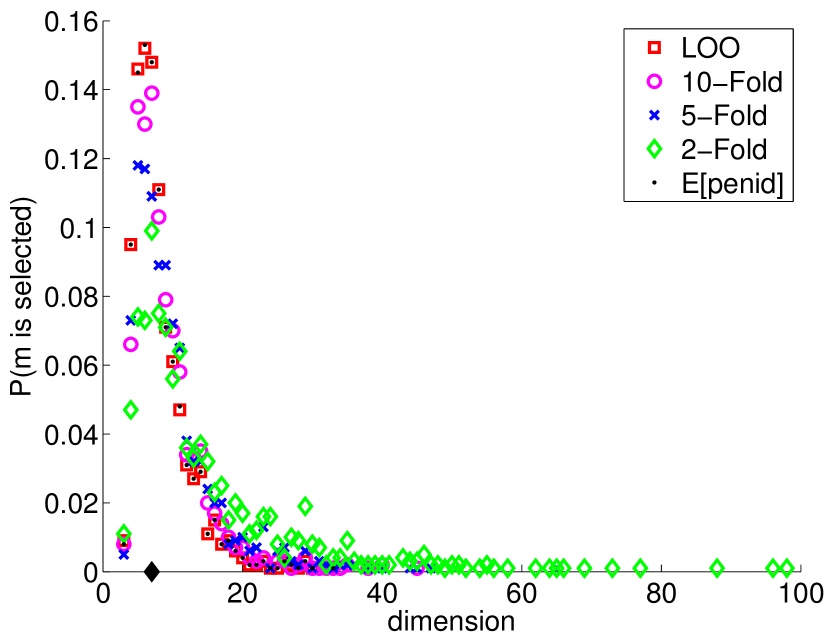

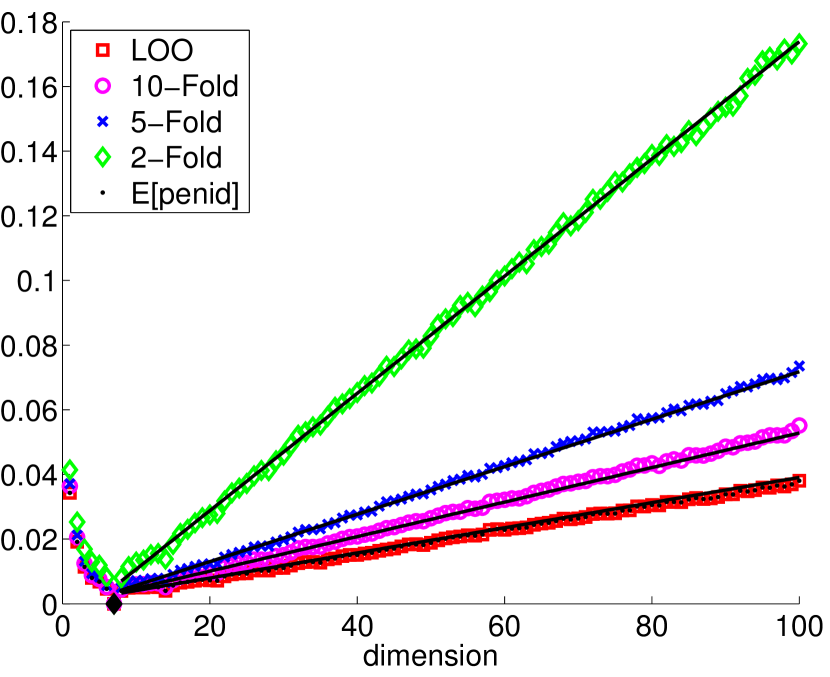

First, Figure 4 shows the variance of as a function of the dimension of , illustrating the conclusions of Theorem 6: the variance decreases when increases. More precisely, the variance decrease is significant between and , an order of magnitude smaller between and and between and , while the leave-one-out is hard to distinguish from the ideal penalized criterion . On Figure 4, we can remark that for

with , , and . The shape of the dependence on already appears in Theorem 6, the above formula clarifies the relative importance of the terms called and in Section 5, and their dependence on the dimension of . Remark that the same behaviour holds when with very close values for and (see Figure 25 in Section B.6), as well as in setting L with or with and (see Figures 19 and 30 in Section B.6). The fact that is close to in both settings supports that the term appearing Theorem 6 indeed drives how depends on .

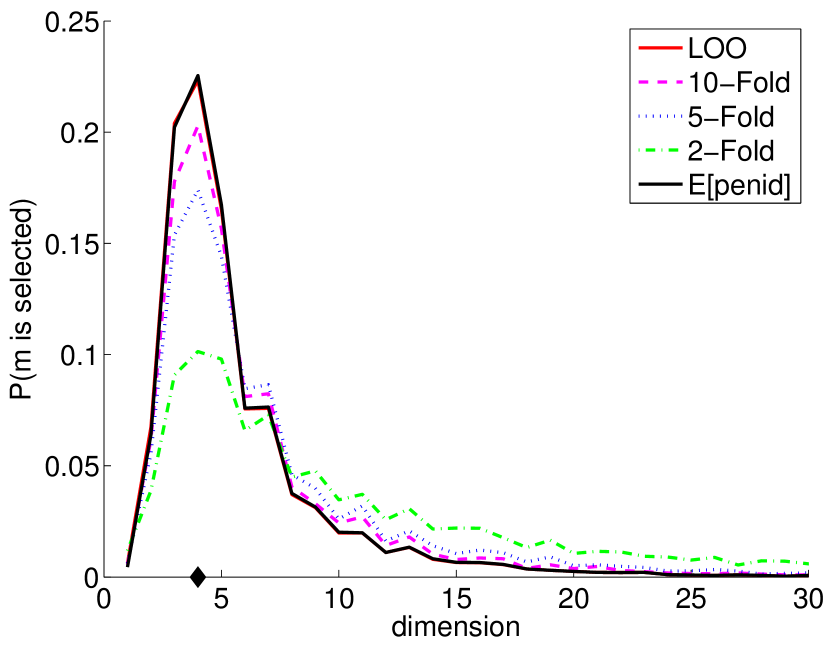

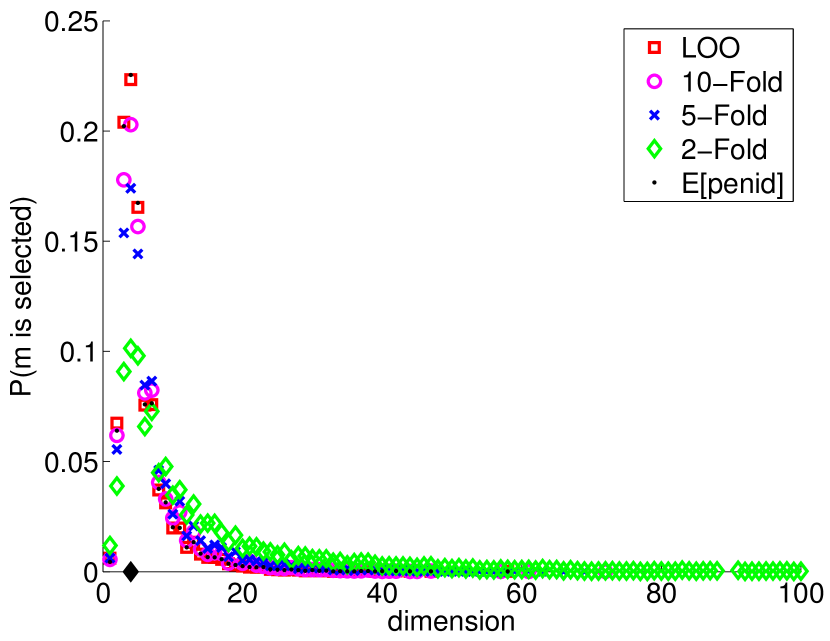

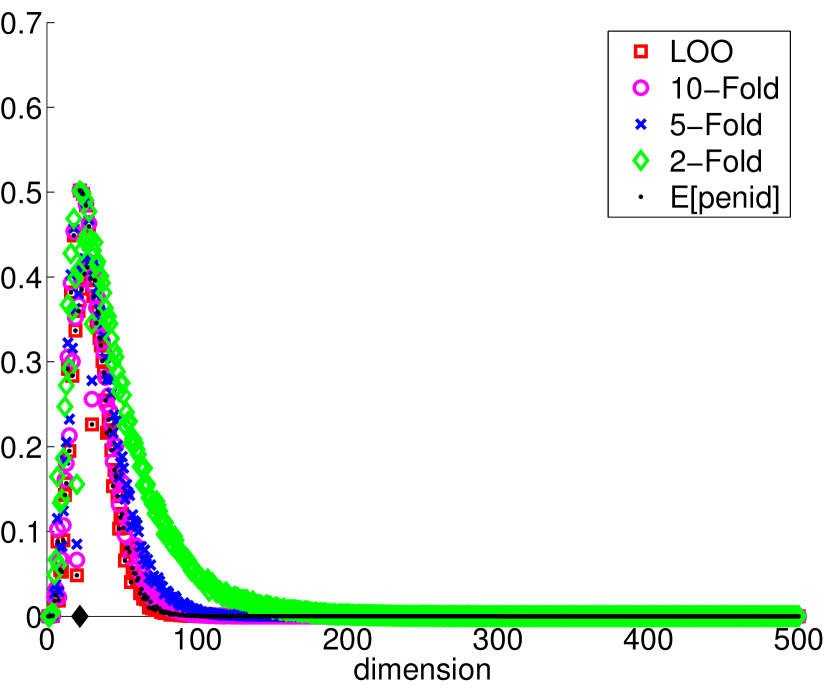

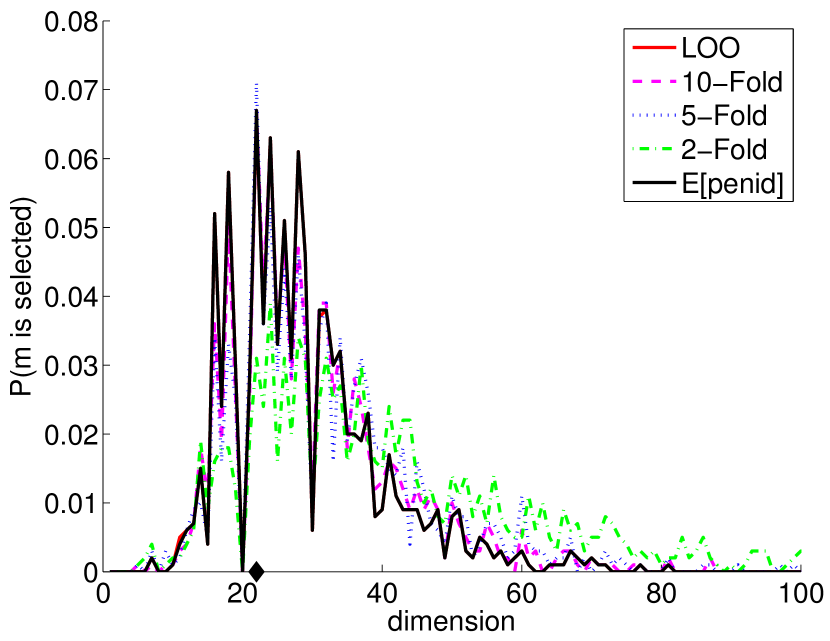

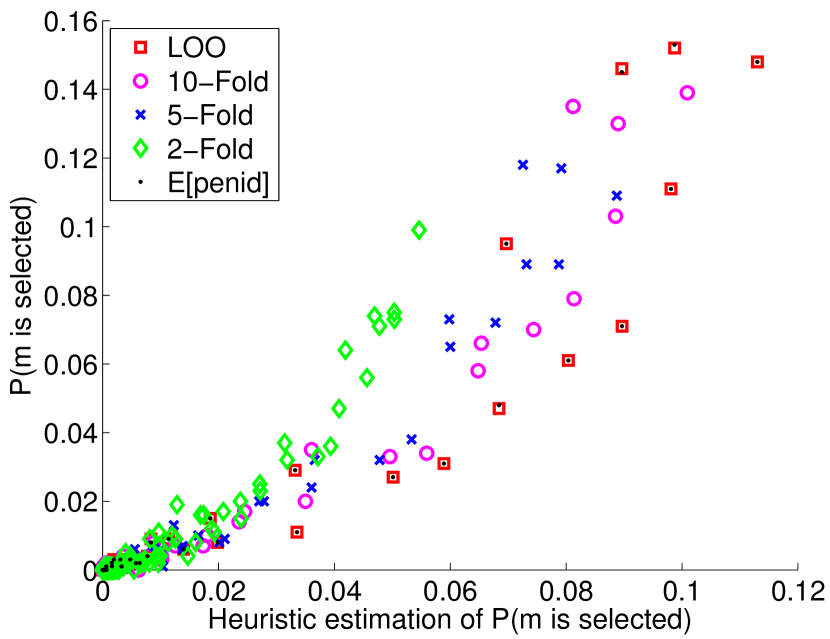

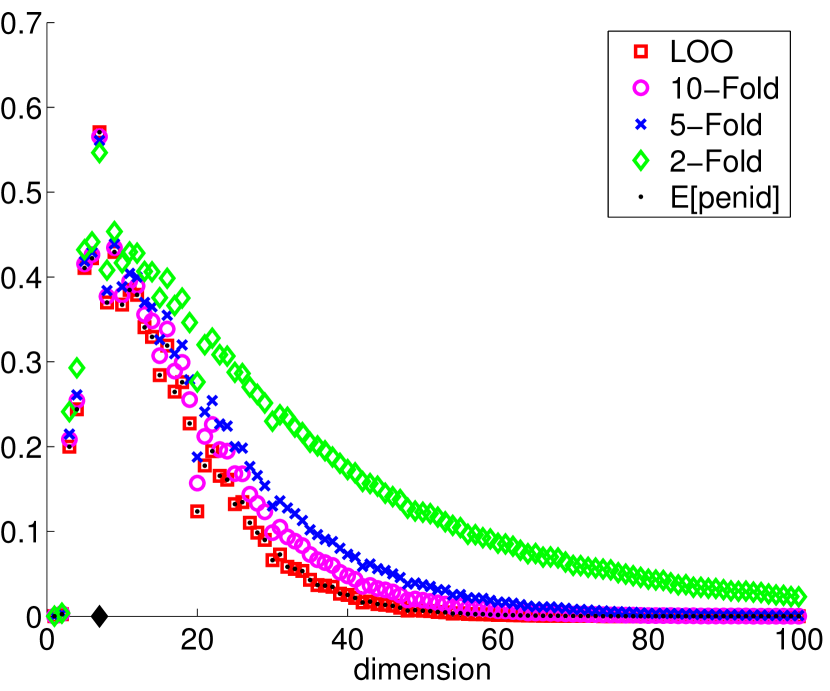

Figures 5 and 6 respectively show and its proxy as a function of for with and for . First, we remark that both quantities behave similarly as a function of and —see also Figure 16 in Section B.6—supporting empirically the heuristic of Section 4. The decrease of the variance observed on Figure 4 when increases here translates into a better concentration of the distribution of around , which can explain the performance improvement observed in Section 6.3. Figures 5–6 actually show how the decrease of the variance quantitatively influences the distribution of : is significantly more concentrated than , while the difference between and is much smaller and comparable to the difference between and ; is hard to distinguish from . Similar experiments with and in setting L are reported in Section B.6, leading to similar conclusions.

7 Fast Algorithm for Computing V-Fold Penalties for Least-Squares Density Estimation

Since the use of -fold algorithms is motivated by computational reasons, it is important to discuss the actual computational cost of -fold penalization and cross-validation as a function of . In the least-squares density estimation framework, two approaches are possible: a naive one—valid for all other frameworks—, and a faster one—specific to least-squares density estimation. For clarifying the exposition, we assume in this section that () holds true—so, divides . The general algorithm for computing the -fold penalized criterion and/or the -fold cross-validation criterion consists in training the estimator with data sets for and then testing each trained estimator on the data sets and/or . In the least-squares density estimation framework, for any model given through an orthonormal family of elements of , we get the “naive” algorithm described and analysed more precisely in Section B.4.1, whose complexity is of order .

Several simplifications occur in the least-squares density estimation framework, that allow to avoid a significant part of the computations made in the naive algorithm.

Algorithm 1

To the best of our knowledge, Algorithm 1 is new, even for computing the -fold cross-validation criterion. Its correctness and complexity are analyzed with the following proposition.

Proposition 8

Proposition 8 is proved in Section B.4.2. It shows that Algorithm 1 is significantly faster than the “naive” Algorithm 2 described in Section B.4.1, by a factor of order

Note that closed-form formulas are available for the leave--out criterion in least-squares density estimation (Celisse, 2014), allowing to compute it with a complexity of order in general, and smaller in some particular cases—for instance, for histograms.

8 Discussion

Before discussing how to choose when using -fold methods for model selection—or more generally for choosing among a given family of estimators—, we state some additional results and we discuss the model selection literature in least-squares density estimation.

8.1 Monte-Carlo Cross-Validation

Our analysis of -fold procedures for model selection can be extended to some other cross-validation procedures. We here present results for Monte-Carlo cross-validation (MCCV, Picard and Cook, 1984), also known as repeated cross-validation, where training samples of the same size are chosen independently and uniformly (see also Arlot and Celisse, 2010, Section 4.3.2). Formally, we consider the criterion

| (25) |

where are subsets of and we recall that the hold-out criterion is defined by Eq. (4). We make the following three assumptions throughout this subsection

| () | |||

| () | |||

| () |

where we recall that . Under these assumptions, we write as a shortcut for .

Theorem 9

Let be i.i.d. real-valued random variables with common density , some sequence of subsets of satisfying (), () and () and be a collection of separable linear spaces satisfying (). Assume that either () or () holds true. For every , let be the estimator defined by Eq. (1), and where

and is defined by Eq. (25). Let us define, for any , and

with under assumption () and under assumption (). Then, an absolute constant exists such that, for any , with probability at least , for any ,

| (26) |

Theorem 9 actually is a corollary of a more general result (Theorem 23 in Section B.2.3), which is valid without assumption () and extends therefore our previous results on -fold cross-validation).

Very few results exist in the literature about the model selection performance of MCCV with an estimation goal. Some asymptotic optimality result has been obtained by Burman (1990) for spline regression, and some oracle inequalities comparing the risk of the selected estimator with the risk of an oracle trained with data have been proved by van der Laan and Dudoit (2003) in a general framework and by van der Laan et al. (2004) for density estimation with the Kullback-Leibler loss. In comparison, Theorem 9 provides a precise non-asymptotic comparison to an oracle trained with data.

As in Theorem 5, the leading constant of the oracle inequality (26) is directly related to the bias, which is here quantified by instead of . The remainder term is also comparable to in Theorem 5: they differ by a factor between (when is large enough) and (when is small). In particular, let and assume that in Theorem 9, hence . Then, for the hold-out (), is larger than by a factor with . For , MCCV with can be called “Monte-Carlo -fold” (MCVF); then, with , we loose a factor at most for MCVF compared to -fold cross-validation. Finally, when is large enough, that is, larger than , and are of the same order.

The above comparison of remainder terms suggests a hierarchy between several cross-validation methods with a common training sample size : from the (presumably) worse to the (presumably) best procedure, the hold-out, Monte-Carlo CV with , -fold CV, Monte-Carlo CV with large and the leave--out. Nevertheless, upper bounds comparison can be misleading, so, following the heuristics (22) presented in Section 4, we compute below the variance of when is a Monte-Carlo CV criterion.

Theorem 10

Theorem 10 is proved in Section B.2.4, as a corollary of a more general result, Theorem 24, which holds for all models —not only regular histograms—and provides a formula for the variance of the criterion itself—not its increments. Let us make a few comments.

Eq. (27) is similar to the formula obtained for bias-corrected -fold and -fold penalization, see Eq. (24) in Theorem 6. In the particular case of regular histogram models, Eq. (24) even fits the general form of Eq. (27), with constants instead of .

Assuming the heuristics of Section 4 is valid, for which matter for model selection, the two terms and are of the same order of magnitude (see Section 5). Then, we can compare model selection performance of several cross-validation methods by comparing the values of the constants only.

In order to get a variance of the same order of magnitude as the one of bias-corrected -fold CV—that is, constants of order —, MCCV requires to take far enough from and , hence training and sample sets of comparable sizes, unless is large enough.

Eq. (27) allows to compare the hold-out () with the leave--out (), for a given value of the training sample size. Let us assume for simplicity that and . Then,

| whereas |

which shows an improvement at least by a constant factor in general. When tends to zero—leave-most-out—or —such as for the leave-one-out—, the improvement is by an order of magnitude. The fact that the leave--out has a smaller variance than the hold-out is not surprising at all—it holds in full generality, as a consequence of Jensen’s inequality—, but the exact quantification of the improvement given by Theorem 10 is new and can be useful in practice for choosing the number of splits when using Monte-Carlo cross-validation.

Eq. (27) also allows to compare -fold cross-validation, given by Theorem 6 with

with MCCV with and , which can be named “Monte-Carlo -fold” cross-validation. The only difference between the two methods is that the splits are chosen independently for “Monte-Carlo -fold”, whereas the usual -fold makes a balanced use of each observation—putting it exactly times in the training set. Let us assume for simplicity that while can vary with . Then, we have

Overall, we get that -fold cross-validation has a smaller variance than “Monte-Carlo -fold” for , at least for large enough, and that the improvement is by a constant factor between and . Since increasing cannot decrease the variance of (bias-corrected) VFCV by more than a small constant factor, the above difference between two methods with the same computational complexity is quite important. This supports strongly the use of -fold CV methods instead of “Monte-Carlo -fold”. Such an improvement was previously noticed in the asymptotic computations of Burman (1989); here we show that it holds in a non-asymptotic framework, where the models can depend on .

8.2 Hold-Out Criteria

Our analysis of cross-validation procedures for model selection can also be extended to hold-out criteria. First, let us emphasize that the hold-out criterion defined by Eq. (4) corresponds to taking in the results of Section 8.1, since choosing uniformly over , independently from , is equivalent to choosing some arbitrary of size before seeing the data .

Second, similarly to the definition of the hold-out criterion in Eq. (4), we can define the hold-out penalty by

| (28) |

that is, the hold-out estimator of which is equal to the expectation of the ideal penalty, see Eq. (2). We do not define by Eq. (2.4) with and —that is, the hold-out estimator of , which amounts to removing the centering term in Eq. (28)—because this would dramatically increase its variability. Note that adding such a term in Eq. (2.4) does not change the value of the -fold penalty under () since .

Denoting by as in Section 8.1, it comes from Lemma 26 in Section B.3.1 that

In the following, we choose so that corresponds to the unbiased case, as in the previous sections for the -fold penalty.

Remark 11

Since , by linearity of the estimator ,

which is symmetric in and , hence . In particular, if , the -fold penalty computed on the partition and the hold-out penalty coincide

Theorem 12

Let be i.i.d. real-valued random variables, their common density, with and be a collection of separable linear spaces satisfying (). Assume that either () or () holds true. Let and . For every , let be the projection estimator onto defined by Eq. (1), and where

Then, an absolute constant exists such that, for any , defining , with probability at least , for any ,

| (29) |

Theorem 12 extends Theorem 5 to hold-out penalties, under similar assumptions. As in Theorem 5, quantifies the bias of the hold-out penalized criterion, and plays the same role in the leading constant of the oracle inequality (29).

We can compare the results obtained for hold-out and -fold penalization in Theorems 5 and 12.

For this comparison, let be some divisor of , such that and choose the same so that both criteria have the same bias .

Then, the only difference lies in the remainder term, the one in Eq. (29) is larger than the one of Eq. (17) in Theorem 5 by a factor of order

when is large.

These only are upper bounds, but at least they are consistent with the common intuition about the stabilizing effect of averaging over folds.

We can also compare the results obtained for hold-out penalization in Theorem 12

and for the hold-out criterion in Theorem 9.

First, hold-out penalization gives a flexibility to choose an unbiased criterion and therefore to obtain asymptotically optimal oracle inequalities while hold-out criteria are always biased for fixed ,

hence a leading constant in the oracle inequality.

The loss in the remainder term is also smaller in Eq. (29) than in Eq. (26)

by a factor of order under assumption ().

8.3 Other Oracle Inequalities for Least-Squares Density Estimation

Although the primary topic of the paper is the study of -fold procedures, let us compare briefly our results to other oracle inequalities that have been proved in the least-squares density estimation setting. For projection estimators, Massart (2007, Section 7.2) proves an oracle inequality for some penalization procedures, which are suboptimal since the leading constant does not tend to 1 as goes to . Oracle inequalities have also been proved for other estimators: blockwise Stein estimators (Rigollet, 2006), linear estimators (Goldenshluger and Lepski, 2011) and some -estimators (Birgé, 2013). The models considered by Birgé (2013) are more general than ours, but the corresponding estimators are not computable in practice, and the oracle inequality by Birgé (2013) also has a suboptimal constant . Some aggregation procedures also satisfy oracle inequalities (Rigollet and Tsybakov, 2007; Bunea et al., 2010). Overall, under our assumptions, none of these results imply strictly better bounds than ours.

Let us finally mention that Birgé and Rozenholc (2006) propose a precise evaluation of the penalty term in the case of regular histogram models and the log-likelihood contrast. Their final penalty is a function of the dimension, only slightly modified compared to , performing very well on regular histograms. These performances are likely to become much worse on the collection Dya2 presented in Section 6. This can be seen, for example, in Table 3 in Section B.6, where we present the performances of with different over-penalizing constants.

8.4 Conclusion on the Choice of

This section summarizes the results of the paper in order to address the main question we would like to answer: How to choose a -fold procedure for model selection?

Generality of the results.

The results of the paper only hold for projection estimators in least-squares density estimation, but we conjecture that most of the statements below are valid much more generally. At least, they have been observed experimentally for projection estimators in least-squares regression (Arlot, 2008) and they are supported by theoretical results for kernel density estimators (Magalhães, 2015, Chapters 3–4). Nevertheless, it is reported in the literature that -fold cross-validation can behave differently in other settings (Arlot and Celisse, 2010), so we must keep in mind that the statements below may not be universal.

Choice of a model selection procedure.

Choosing among procedures of the form , as defined by Eq. (18), requires to take into account three quantities:

-

•

the bias of as an estimator of the risk of for every , or equivalently, the overpenalization factor , which usually drives the performance at first order when , as in Theorem 5. The simulation experiments of Section 6 also show that varying can strongly change the performance of the procedure. In all settings considered in the paper, some exists (the optimal overpenalization constant) such that the performance decreases for and increases for (Figure 3).

Note that strongly depends on the setting, and can also vary with when using -fold penalization (in particular from to ). In the nonparametric case, when , Theorem 5 shows that . On the contrary, in the parametric case, when , it is known that a BIC-type penalty performs better, hence . For a finite sample size, Section 6 and Liu and Yang (2011) show that some nonparametric settings can be “practically parametric”, that is, can be much larger than .

-

•

the variance of increments drives the performance at second order, according to the heuristic of Section 4, which suggests that this variance should be minimized, at least for a given “good enough” value of the overpenalization factor .

-

•

the computational complexity of the procedure , that we want to minimize—for a given statistical performance—, or on which some upper bound is given—fixed budget.

-fold cross-validation.

The paper analyzes how the aboves three terms depend on when is a -fold cross-validation procedure, under assumption (). First, by Lemma 1, its overpenalization factor is , which decreases to 1 as increases to . Second, by Theorem 6, its variance decreases as increases. Theoretical and empirical arguments in Sections 5 and 6 show that the variance almost reaches its minimal value by taking, say, or . Third, by Section 7, its computational complexity is proportional to in general; in the least-squares density estimation setting, it can be reduced to .

These three results can explain why the most common advices for choosing in the literature (for instance Breiman and Spector, 1992; Hastie et al., 2009, Section 7.10.1) are between and . Indeed, taking larger does not reduce the variance significantly—with almost no impact on the risk of the final estimator—, and it reduces the overpenalization factor although is often larger than or . So, if is not much larger than , which is likely to occur in many nonparametric settings, taking or can be close to be optimal.

Nevertheless, other situations can occur, for instance in (practically) parametric settings where is much larger, possibly leading to the failure of the heuristic “ is almost optimal”. More generally, understanding precisely how performs as a function of seems to be a difficult question: influences the performance in two opposite directions simultaneously, through the bias and the variance, so that various behaviours can result from this coupling of bias and variance, as shown in the simulation experiments.

-fold penalization.

Lemma 1 shows that a natural way to solve this difficulty is to consider instead a -fold penalization procedure , with overpenalization factor . The value corresponds to -fold cross-validation, but any other value of can also be considered, making it easier to understand. Indeed, the overpenalization factor is directly given by , while the variance and computational complexity of vary with —independently from —exactly as for -fold cross-validation. So, should be taken as large as possible—depending on the maximal computational budget available—, while should be taken as close as possible to .

Compared to -fold cross-validation, another interest of -fold penalization is the improvement of the performance for a given computational cost, that is, a given value of , because it is then possible to take closer to than . This is especially true in (practically) parametric settings for which for all .

Data-driven overpenalization factor .

Although the paper shows that choosing well is a key practical problem, making an optimal data-driven choice of remains an open question which deserves to be studied, even independently from the analysis of cross-validation procedures. We postpone such a study to future works, but we can already make two suggestions. First, an external cross-validation loop can be used for choosing , if the computational power is not a limitation. Second, a procedure built for choosing between AIC and BIC can be used in order to detect whether should be close to or significantly larger (see, for instance, Liu and Yang, 2011 and references therein).

Acknowledgments

The authors thank the two referees for their comments that allowed us to improve the paper.

The authors thank gratefully Yannick Baraud and Guillaume Obozinski for precious comments on an earlier version of the paper, and Nelo Magalhães for his careful reading and helpful remarks on this earlier version.

Let us also emphasize that this paper has changed a lot since its first version (Arlot and Lerasle, 2012),

and that the most recent results (Sections 8.1 and B.2)

and some aspects of the proofs (for instance, the systematic use of and )

have been strongly influenced by our ongoing collaboration with Nelo Magalhães (Chapters 3–4 Magalhães, 2015).

This work was done while the first author was financed by CNRS

and member of the Sierra team in the Departement d’Informatique de l’Ecole normale superieure (CNRS/ENS/INRIA UMR 8548),

45 rue d’Ulm, F-75230 Paris Cedex 05, France.

The authors acknowledge the support of the French Agence Nationale de la Recherche (ANR) under reference ANR-09-JCJC-0027-01 (Detect project) and ANR 2011 BS01 010 01 (projet Calibration).

The first author also acknowledges the support of the GARGANTUA project funded by the Mastodons program of CNRS,

and the support of Institut des Hautes Études Scientifiques (IHES, Le Bois-Marie, 35, route de Chartres,

91440 Bures-Sur-Yvette, France) during the last days of writing of this paper.

Appendix A Proofs

Before proving the main results stated in the paper, let us recall two simple results that we use repeatedly in the paper. First, if is a family of real numbers such that , then

| (30) |

The left-hand side is smaller than the right-hand side by Cauchy-Schwarz inequality, and considering shows that the converse inequality holds true. Second, for any probability distribution on ,

| (31) |

a result which provides in particular a formula for and for , by taking and , respectively.

A.1 Proof of Lemma 1

Let us first recall here the proof of Eq. (7)—coming from Arlot (2008)—for the sake of completeness. By (),

so that

Eq. (8) and (9) follow simultaneously from Eq. (35) below. Let be a set of subsets of such that

| (32) |

Let us consider the associated penalty

and the associated cross-validation criterion

When , we get the -fold penalty and the -fold cross-validation criterion , and Eq. (32) holds true with under assumption (). When , Eq. (32) always holds true and we get the leave--out penalty and the leave--out cross-validation criterion .

Let be some orthonormal basis of in . On the one hand, using Eq. (32), we get

| (33) |

On the other hand, using that by Eq. (32),

| (34) |

where we used again Eq. (32). Comparing Eq. (33) and (34) gives

| (35) |

which implies Eq. (8) and (9).

Eq. (10) follows by Lemma A.11 of Lerasle (2012).

Proof of Remark 2 We first note that Eq. (10) can also be deduced from Celisse (2014, Proposition 2.1), which proves

Elementary algebraic computations then show that

| (36) |

hence for any ,

In particular, when , from Eq. (9), since ,

Proof of Remark 3 Note first that the CV estimator of Massart (2007, Sec. 7.2.1, p. 204–205) is defined as the minimizer of

| (37) |

On the other hand, from Eq. (36) and (9) with , we have

Hence, from Eq. (37), the CV estimator is the minimizer of . Massart (2007, Theorem 7.6) studies the minimizers of the criterion

| (38) |

where for any . Let , so that . Then, the criterion (38) is equal to

A.2 Proof of Proposition 4

Note that the two formulas given for in the statement of Proposition 4 coincide by Eq. (30). The proof is decomposed into 3 lemmas.

Lemma 13

Proof Let and use the formulation (5) of the -fold penalty as a resampling penalty. Then,

| (42) |

we get that if and belong to the same block and otherwise. So,

and Eq. (40) follows by Eq. (3).

Eq. (41) directly follows from Eq. (40).

Lemma 14

Let be i.i.d. random variables taking values in a Polish space with common density , a separable linear subspace of and denote by an orthonormal basis of . Let , and assume that . An absolute constant exists such that, for any , with probability larger than , we have for every ,

Proof By Eq. (3), has expectation . In addition, for any ,

| (43) |

which gives the conclusion thanks to Proposition 29 in Section B.5.

Lemma 15

Assume that is a sequence of i.i.d. real-valued random variables with common density and is some partition of satisfying (). Let denote a separable subspace of with orthonormal basis such that

Let be the -statistics defined by Eq. (39). Using the notations of Lemma 14, an absolute constant exists such that, with probability larger than ,

Hence, an absolute constant exists such that, for any , with probability larger than , for any ,

Proof For any and , let us define

From Houdré and Reynaud-Bouret (2003, Theorem 3.4), an absolute constant exists such that, for any and ,

| (44) |

It remains to upper bound these different terms for proving the first inequality, and the second inequality follows. First,

| (45) |

so that

Second, let be functions in such that

Using successively the independence of the and that for every , for every ,

| (46) |

Now, we have, for every , using Eq. (30), Cauchy-Schwarz inequality and the fact that for every , ,

Plugging this bound in (46) yields

| (47) |

hence

Third, for every , let so that

Then,

| (48) |

Fourth, from Cauchy-Schwarz inequality, for every ,

| (49) |

Hence,

and we get the desired result.

A.3 Proof of Theorem 5

By construction, the penalized estimator satisfies, for any ,

Now, by Eq. (2) and (3), , hence

| (51) |

Let and . A union bound in Proposition 4 gives

| (52) |

and a union bound in Lemma 14 gives

| (53) |

It remains to bound uniformly over and in . In order to apply Bernstein’s inequality, we first bound the variance and the sup norm of for some . Since ,

Under assumption (), for some , hence by () we have

Therefore, by Bernstein’s inequality, for any , for any , with probability larger than , for any ,

for some absolute constant , where the last inequality is obtained by considering separately the cases () and (), and by using that for every , . A union bound gives that for any , with probability at least , for every and every ,

| (54) |

for some absolute constant . Plugging Eq. (52), (A.3) and (54) into Eq. (51) and using that yields that, with probability , for any ,

for some absolute constants . Since for all , we get

for every . Hence, with probability larger than , for any ,

| (55) |

for some absolute constant . To conclude, we remark that Eq. (17) clearly holds true when , so we can assume that . Therefore, for every , Eq. (55) holds true with probability at least

So, if we replace by in Eq. (55),

we get that

Eq. (17) holds true with probability at least

for some absolute constant ,

slightly larger than the one appearing in Eq. (55).

A.4 Proof of Theorem 6

For every and , let and remark that

| (56) |

For every , by Eq. (30), and, by independence, for every

hence, . For every , by Eq. (56),

| (57) | ||||

Moreover, by Eq. (42) in the proof of Lemma 13,

It follows that

| (58) |

Hence, up to the deterministic term , has the form of a function defined in Lemma 16 below with

It remains to evaluate the quantities appearing in Lemma 16 for these weights and function. First,

It follows that

Hence, from Lemma 16, for every ,

Therefore,

| and | |||

which concludes the proof.

Lemma 16

Let , where is defined by Eq. (56) and . For every , we have

Proof We develop the covariance to get

The proof is then concluded with the following remarks, which rely on the fact that the random variables are independent and identically distributed.

-

1.

unless , therefore

-

2.

By definition (56) of , unless , hence

-

3.

By definition (56) of , unless or or . It follows that

References

- Allen (1974) David M. Allen. The relationship between variable selection and data augmentation and a method for prediction. Technometrics, 16:125–127, 1974.

- Arlot (2008) Sylvain Arlot. -fold cross-validation improved: -fold penalization, February 2008. http://arxiv.org/pdf/0802.0566v2.pdf.

- Arlot (2009) Sylvain Arlot. Model selection by resampling penalization. Electronic Journal of Statistics, 3:557–624 (electronic), 2009.

- Arlot and Celisse (2010) Sylvain Arlot and Alain Celisse. A survey of cross-validation procedures for model selection. Statistics Surveys, 4:40–79, 2010.

- Arlot and Lerasle (2012) Sylvain Arlot and Matthieu Lerasle. -fold cross-validation and -fold penalization in least-squares density estimation, October 2012. http://arxiv.org/pdf/1210.5830v1.pdf.

- Audibert (2004) Jean-Yves Audibert. A better variance control for pac-bayesian classification. Technical Report 905b, Laboratoire de Probabilités et Modèles Aléatoires, 2004. Available electronically at http://imagine.enpc.fr/publications/papers/04PMA-905Bis.pdf.

- Barron et al. (1999) Andrew Barron, Lucien Birgé, and Pascal Massart. Risk bounds for model selection via penalization. Probability Theory and Related Fields, 113(3):301–413, 1999.

- Bengio and Grandvalet (2005) Yoshua Bengio and Yves Grandvalet. Bias in estimating the variance of -fold cross-validation. In Statistical Modeling and Analysis for Complex Data Problems, volume 1 of GERAD 25th Anniversary Series, pages 75–95. Springer, New York, 2005.

- Birgé (2013) Lucien Birgé. Model selection for density estimation with -loss. Probability Theory and Related Fields, pages 1–42, 2013.

- Birgé and Rozenholc (2006) Lucien Birgé and Yves Rozenholc. How many bins should be put in a regular histogram. ESAIM: Probability and Statistics, 10, 2006.

- Boucheron et al. (2013) Stéphane Boucheron, Gábor Lugosi, and Pascal Massart. Concentration Inequalities: A Nonasymptotic Theory of Independence. Oxford University Press, Oxford, 2013.

- Breiman and Spector (1992) Leo Breiman and Philip Spector. Submodel Selection and Evaluation in Regression. The X-Random Case. International Statistical Review, 60(3):291–319, 1992.

- Bunea et al. (2010) Florentina Bunea, Alexandre B. Tsybakov, Marten H. Wegkamp, and Adrian Barbu. Spades and mixture models. The Annals of Statistics, 38(4):2525–2558, 2010.

- Burman (1989) Prabir Burman. A comparative study of ordinary cross-validation, -fold cross-validation and the repeated learning-testing methods. Biometrika, 76(3):503–514, 1989.

- Burman (1990) Prabir Burman. Estimation of optimal transformations using -fold cross validation and repeated learning-testing methods. Sankhyā (Statistics). Series A, 52(3):314–345, 1990.

- Catoni (2007) Olivier Catoni. Pac-Bayesian Supervised Classification: The Thermodynamics of Statistical Learning, volume 56 of IMS Lecture Notes Monograph Series. Institute of Mathematical Statistics, 2007.

- Celisse (2008) Alain Celisse. Model Selection Via Cross-Validation in Density Estimation, Regression and Change-Points Detection. PhD thesis, University Paris-Sud 11, December 2008. Available electronically at http://tel.archives-ouvertes.fr/tel-00346320/.

- Celisse (2014) Alain Celisse. Optimal cross-validation in density estimation with the -loss. The Annals of Statistics, 42(5):1879–1910, 10 2014.

- Celisse and Robin (2008) Alain Celisse and Stéphane Robin. Nonparametric density estimation by exact leave--out cross-validation. Computational Statistics & Data Analysis, 52(5):2350–2368, 2008.

- DeVore and Lorentz (1993) Ronald A. DeVore and George G. Lorentz. Constructive Approximation, volume 303 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, 1993.

- Efron (1983) Bradley Efron. Estimating the error rate of a prediction rule: improvement on cross-validation. Journal of the American Statistical Association, 78(382):316–331, 1983.

- Geisser (1975) Seymour Geisser. The predictive sample reuse method with applications. Journal of the American Statistical Association, 70:320–328, 1975.

- Goldenshluger and Lepski (2011) Alexander Goldenshluger and Oleg Lepski. Bandwidth selection in kernel density estimation: oracle inequalities and adaptive minimax optimality. The Annals of Statistics, 39(3):1608–1632, 2011.

- Hastie et al. (2009) Trevor Hastie, Robert Tibshirani, and Jerome Friedman. The Elements of Statistical Learning. Springer Series in Statistics. Springer, New York, second edition, 2009. Data Mining, Inference, and Prediction.

- Houdré and Reynaud-Bouret (2003) Christian Houdré and Patricia Reynaud-Bouret. Exponential inequalities, with constants, for U-statistics of order two. In Stochastic Inequalities and Applications, volume 56 of Progress in Probability, pages 55–69. Birkhäuser, Basel, 2003.

- Lerasle (2011) Matthieu Lerasle. Optimal model selection for stationary data under various mixing conditions. The Annals of Statistics, 39(4):1852–1877, 2011.

- Lerasle (2012) Matthieu Lerasle. Optimal model selection in density estimation. Annales de l’Institut Henri Poincaré. Probabilités et Statistiques, 48(3):884–908, 2012.

- Liu and Yang (2011) Wei Liu and Yuhong Yang. Parametric or nonparametric? A parametricness index for model selection. The Annals of Statistics, 39(4):2074–2102, 2011.

- Magalhães (2015) Nelo Magalhães. Cross-Validation and Penalization for Density Estimation. PhD thesis, University Paris-Sud 11, May 2015. Available electronically at http://tel.archives-ouvertes.fr/tel-01164581/.

- Massart (2007) Pascal Massart. Concentration Inequalities and Model Selection, volume 1896 of Lecture Notes in Mathematics. Springer, Berlin, 2007. Lectures from the 33rd Summer School on Probability Theory held in Saint-Flour, July 6–23, 2003.

- Picard and Cook (1984) Richard R. Picard and R. Dennis Cook. Cross-validation of regression models. Journal of the American Statistical Association, 79(387):575–583, 1984.

- Rigollet (2006) Philippe Rigollet. Adaptive density estimation using the blockwise Stein method. Bernoulli, 12(2):351–370, 2006.

- Rigollet and Tsybakov (2007) Philippe Rigollet and Alexander B. Tsybakov. Linear and convex aggregation of density estimators. Mathematical Methods of Statistics, 16(3):260–280, 2007.

- Rudemo (1982) Mats Rudemo. Empirical choice of histograms and kernel density estimators. Scandinavian Journal of Statistics. Theory and Applications, 9(2):65–78, 1982.

- Shao (1997) Jun Shao. An asymptotic theory for linear model selection. Statistica Sinica, 7(2):221–264, 1997. With comments and a rejoinder by the author.

- Stone (1974) Mervyn Stone. Cross-validatory choice and assessment of statistical predictions. Journal of the Royal Statistical Society. Series B. Methodological, 36:111–147, 1974.

- van der Laan and Dudoit (2003) Mark J. van der Laan and Sandrine Dudoit. Unified cross-validation methodology for selection among estimators and a general cross-validated adaptive epsilon-net estimator: Finite sample oracle inequalities and examples. Working Paper 130, U.C. Berkeley Division of Biostatistics, November 2003. Available electronically at http://www.bepress.com/ucbbiostat/paper130.

- van der Laan et al. (2004) Mark J. van der Laan, Sandrine Dudoit, and Sunduz Keles. Asymptotic optimality of likelihood-based cross-validation. Statistical Applications in Genetics and Molecular Biology, 3:Art. 4, 27 pp. (electronic), 2004.