Singular Forward-Backward Stochastic Differential Equations and Emissions Derivatives

Abstract.

We introduce two simple models of forward-backward stochastic differential equations with a singular terminal condition and we explain how and why they appear naturally as models for the valuation of CO2 emission allowances. Single phase cap-and-trade schemes lead readily to terminal conditions given by indicator functions of the forward component, and using fine partial differential equations estimates, we show that the existence theory of these equations, as well as the properties of the candidates for solution, depend strongly upon the characteristics of the forward dynamics. Finally, we give a first order Taylor expansion and show how to numerically calibrate some of these models for the purpose of CO2 option pricing.

2000 Mathematics Subject Classification:

Primary1. Introduction

This paper is motivated by the mathematical analysis of the emissions markets, as implemented for example in the European Union (EU) Emissions Trading Scheme (ETS). These market mechanisms have been hailed by some as the most cost efficient way to control Green House Gas (GHG) emissions. They have been criticized by others for being a tax in disguise and adding to the burden of industries covered by the regulation. Implementation of cap-and-trade schemes is not limited to the implementation of the Kyoto protocol. The successful US acid rain program is a case in point. However, a widespread lack of understanding of their properties, and misinformation campaigns by advocacy groups more interested in pushing their political agendas than using the results of objective scientific studies have muddied the water and add to the confusion. More mathematical studies are needed to increase the understanding of these market mechanisms and raise the level of awareness of their advantages as well as their shortcomings. This paper was prepared in this spirit.

In a first part, we introduce simple single-firm models inspired by the workings of the electricity markets (electric power generation is responsible for most of the CO2 emissions worldwide). Despite the specificity of some assumptions, our treatment is quite general in the sense that individual risk averse power producers choose their own utility functions. Moreover, the financial markets in which they trade emission allowances are not assumed to be complete.

While market incompleteness prevents us from identifying the optimal trading strategy of each producer, we show that, independently of the choice of the utility function, the optimal production or abatement strategy is what we expect by proving mathematically, and in full generality (i.e. without assuming completeness of the markets), a folk theorem in environmental economics: the equilibrium allowance price equals the marginal abatement cost, and market participants implement all the abatement measures whose costs are not greater than the cost of compliance (i.e. the equilibrium price of an allowance).

The next section puts together the economic activities of a large number of producers and searches for the existence of an equilibrium price for the emissions allowances. Such a problem leads naturally to a forward stochastic differential equation (SDE) for the aggregate emissions in the economy, and a backward stochastic differential equation (BSDE) for the allowance price. However, these equations are ”coupled” since a nonlinear function of the price of carbon (i.e. the price of an emission allowance) appears in the forward equation giving the dynamics of the aggregate emissions. This feedback of the emission price in the dynamics of the emissions is quite natural. For the purpose of option pricing, this approach was described in [5] where it was called detailed risk neutral approach.

Forward backward stochastic differential equations (FBSDEs) of the type considered in this section have been studied for a long time. See for example [14], or [19]. However, the FBSDEs we need to consider for the purpose of emission prices have an unusual pecularity: the terminal condition of the backward equation is given by a discontinuous function of the terminal value of the state driven by the forward equation. We use our first model to prove that this lack of continuity is not an issue when the forward dynamics are strongly elliptic in the neighborhood of the singularities of the terminal condition, in other words when the volatility of the forward SDE is bounded from below in the neighborhood of the discontinuities of the terminal value. However, using our second equilibrium model, we also show that when the forward dynamics are degenerate (even if they are hypoelliptic), discontinuities in the terminal condition and lack of strong ellipticity in the forward dynamics can conspire to produce point masses in the terminal distribution of the forward component, at the locations of the discontinuities. This implies that the terminal value of the backward component is not given by a deterministic function of the forward component, for the forward scenarios ending at the locations of jumps in the terminal condition, and justifies relaxing the definition of a solution of the FBSDE.

Even though we only present a detailed proof for a very specific model for the sake of definiteness, we believe that our result is representative of a large class of models. Since from the point of view of the definition of ”aggregate emissions”, the degeneracy of the forward dynamics is expected, this seemingly pathological result should not be overlooked. Indeed, it sheds new light on an absolute continuity assumption made repeatedly in equilibrium analyses, even in discrete time models. See for example [4] and [3]. This assumption was regarded as an annoying technicality, but in the light of the results of this paper, it looks more intrinsic to these types of models. In any case, it fully justifies the need to relax the definition of a solution of a FBSDE when the terminal condition of the backward part jumps.

A vibrant market for options written on allowance futures/forward contracts has recently developed and increased in liquidity. See for example [5] for details on these markets. Reduced formed models have been proposed to price these options. See [5] or [6]. Several attempts have been made at matching the smile (or lack thereof) contained in the quotes published daily by the exchanges. Section 5 develops the technology needed to price these options in the context of the equilibrium framework developed in the present paper. We identify the option prices in terms of solutions of nonlinear partial differential equations and we prove when the dynamics of the aggregate emissions are given by a geometric Brownian motion, a Taylor expansion formula when the nonlinear abatement feedback is small. We derive an explicit integral form for the first order Taylor expansion coefficient which can easily be computed by Monte Carlo methods. We believe that the present paper is the first rigorous attempt to include the nonlinear feedback term in the dynamics of aggregate emissions for the purpose of emissions option pricing.

The final Section 5 was motivated by the desire to provide practical tools for the efficient computation of option prices within the equilibrium framework of the paper. Indeed, because of the nonlinear feedback created by the coupling in the FBSDE, option prices computed from our equilibrium model differ from the linear prices computed in [6], [21] and [5] in the framework of reduced form models. We derive rigorously an approximation based on the first order asymptotics in the nonlinear feedback. This approximation can be used to compute numerically option prices and has the potential to efficiently fit the implied volatility smile present in recent option price quotes. The final subsection 5.3 illustrates numerically the properties of our approximation.

2. Two Simple Models of Green House Gas Emission Control

We first describe the optimization problem of a single power producer facing a carbon cap-and-trade regulation. We assume that this producer is a small player in the market in the sense that his actions have no impact on prices and that a liquid market for pollution permits exists. In particular, we assume that the price of an allowance is given exogenously, and we use the notation for the (stochastic) time evolution of the price of such an emission allowance. For the sake of simplicity we assume that is a single phase of the regulation and that no banking or borrowing of the certificates is possible at the end of the phase. For illustration purposes, we analyze two simple models. Strangely enough, the first steps of these analyses, namely the identifications of the optimal abatement and production strategies, do not require the full force of the sophisticated techniques of optimal stochastic control.

2.1. Modeling First the Emissions Dynamics

We assume that the source of randomness in the model is given by , a finite family of independent one-dimensional Wiener processes , . In other words, for each fixed . All these Wiener processes are assumed to be defined on a complete probability space , and we denote by the Brownian filtration they generate. Here, is a fixed time horizon representing the end of the regulation period.

We will eventually extend the model to include firms, but for the time being, we consider only the problem of one single firm whose production of electricity generates emissions of carbon dioxyde, and we denote by the cumulative emissions up to time of the firm. We also denote by the perception at time (for example the conditional expectation) of what the total cumulative emission will be at the end of the time horizon. Clearly, and can be different stochastic processes, but they have the same terminal values at time , i.e. . We will assume that the dynamics of the proxy for the cumulative emissions of the firm are given by an Itô process of the form:

| (1) |

where represents the (conditional) expectation of what the rate of emission would be in a world without carbon regulation, in other words in what is usually called Business As Usual (BAU for short), while is the instantaneous rate of abatement chosen by the firm. In mathematical terms, represents the control on emission reduction implemented by the firm. Clearly, in such a model, the firm only acts on the drift of its perceived emissions. For the sake of simplicity we assume that the processes and are adapted and bounded. Because of the vector nature of the Brownian motion , the volatility process is in fact a vector of scalar volatility processes . For the purpose of this section, we could use one single scalar Wiener process and one single scalar volatility process as long as we allow the filtration to be larger than the filtration generated by this single Wiener process. This fact will be needed when we study a model with more than one firm.

Notice that the formulation (1) does not guarantee the positiveness of the perceived emissions process, as one would expect it to be. This issue will be discussed in Proposition 3 below, where we provide sufficient conditions on the coefficients of (1) in order to guarantee the positiveness of the process .

Continuing on with the description of the model, we assume that the abatement decision is based on a cost function which is assumed to be continuously differentiable ( in notation), strictly convex and satisfy Inada-like conditions:

| (2) |

Note that exists because of the assumption of strict convexity. Since can be interpreted as the cost to the firm for an abatement rate of level , without any loss of generality we will also assume . Notice that (2) implies that .

Example 1.

A typical example of abatement cost function is given by the quadratic cost function for some used in [21], or more generally the power cost function for some and .

The firm controls its destiny by choosing its own abatement schedule as well as the quantity of pollution permits it holds through trading in the allowance market. For these controls to be admissible, and need only to be progressively measurable processes satisfying the integrability condition

| (3) |

We denote by the set of admissible controls . Given its initial wealth , the terminal wealth of the firm is given by:

| (4) |

The first integral in the right hand side of the above equation gives the proceeds from trading in the allowance market. Recall that we use the notation for the price of an emission allowance at time . The next term represents the abatement costs, and the last term gives the costs of the emission regulation. Recall also that at this stage, we are not interested in the existence or the formation of this price. We merely assume the existence of a liquid and frictionless market for emission allowances, and that is the price at which each firm can buy or sell one allowance at time . The risk preferences of the firm are given by a utility function , which is assumed to be , increasing, strictly concave and satisfying the Inada conditions:

| (5) |

The optimization problem of the firm can be written as the computation of:

| (6) |

where denotes the expectation under the historical measure , and is the set of abatement and trading strategies admissible to the firm. The following simple result holds.

Proposition 1.

The optimal abatement strategy of the firm is given by:

Remark 1.

Notice that the optimal abatement schedule is independent of the utility function. The beauty of this simple result is its powerful intuitive meaning: given a price for an emission allowance, the firm implements all the abatement measures which make sense economically, namely all those costing less than the current market price of one allowance (i.e. one unit of emission).

Proof.

By an immediate integration by parts in the expression (4) of the terminal wealth, we see that:

so that with

where the modified control is defined by , and

Notice that depends only upon without depending upon while depends only upon without depending upon . The set of admissible controls is equivalently described by varying the couples or , so when computing the maximum

one can perform the optimizations over and separately, for example by fixing and optimizing with respect to before maximizing the result with respect to . The proof is complete once we notice that is increasing and that for each and each , the quantity is maximized by the choice .∎

Remark 2.

The above result argues neither existence nor uniqueness of an optimal admissible set of controls. In the context of a complete market, once the optimal rate of abatement is implemented, the optimal investment strategy should hedge the financial risk created by the implementation of the abatement strategy. This fact can be proved using the classical tools of portfolio optimization in the case of complete market models. Indeed, if we introduce the convex dual of defined by:

and the function by so that and if we denote by and respectively the expectations with respect to and the unique equivalent measure under which is a martingale (we write for its volatility given by the martingale representation theorem), then from the a.s. inequality

valid for any admissible , and , we get

after taking expectations under . Computing by integration by parts we get:

if we use the optimal rate of abatement. So if we choose as the unique solution of:

it follows that

and finally, if the market is complete, the claim is attainable by a certain . This completes the proof.

2.2. Modeling the Electricity Price First

We consider a second model for which again, part of the global stochastic optimization problem reduces to a mere path-by-path optimization. As before, the model is simplistic, especially in the case of a single firm in a regulatory environment with a liquid frictionless market for emission allowances. However, this model will become very informative later on when we consider firms interacting on the same market, and we try to construct the allowance price by solving a Forward-Backward Stochastic Differential Equation (FBSDE). The model concerns an economy with one production good (say electricity) whose production is the source of a negative externality (say GHG emissions). Its price evolves according to the following Itô stochastic differential equation:

| (7) |

where the deterministic functions and are assumed to be with bounded derivatives. At each time , the firm chooses its instantaneous rate of production and its production costs are where is a function which is assumed to be and strictly convex. With these notations, the profits and losses from the production at the end of the period , are given by the integral:

The emission regulation mandates that at the end of the period , the cumulative emissions of each firm be measured, and that one emission permit be redeemed per unit of emission. As before, we denote by the process giving the price of one emission allowance. For the sake of simplicity, we assume that the cumulative emissions up to time are proportional to the production in the sense that where the positive number represents the rate of emission of the production technology used by the firm, and denotes the cumulative production up to and including time :

At the end of the time horizon, the cost incurred by the firm because of the regulation is given by . The firm may purchase allowances: we denote by the amount of allowances held by the firm at time . Under these conditions, the terminal wealth of the firm is given by:

| (8) |

where as before, we used the notation for the initial wealth of the firm. The first integral in the right hand side of the above equation gives the proceeds from trading in the allowance market, the next term gives the profits from the production and the sale of electricity, and the last term gives the costs of the emission regulation. We assume that the risk preferences of the firm are given by a utility function , which is assumed to be , increasing, strictly concave and satisfying the Inada conditions (5) stated earlier. As before, the optimization problem of the firm can be written as:

| (9) |

where denotes the expectation under the historical measure , and is the set of admissible production and trading strategies . This problem is similar to those studied in [2] where the equilibrium issue is not addressed. As before, for these controls to be admissible, and need only be adapted processes satisfying the integrability condition

| (10) |

Proposition 2.

The optimal production strategy of the firm is given by:

Remark 3.

As before, the optimal production strategy is independent of the risk aversion (i.e. the utility function) of the firm. The intuitive interpretation of this result is clear: once a firm observes both prices and , it computes the price for which it can sell the good minus the price it will have to pay because of the emission regulation, and the firm uses this corrected price to choose its optimal rate of production in the usual way.

Proof.

A simple integration by part (notice that is of bounded variations) gives:

| (11) |

so that with

which depends only upon and

which depends only upon without depending upon . Since the set of admissible controls is equivalently described by varying the couples or , when computing the maximum

one can perform the optimizations over and separately, for example by fixing and optimizing with respect to before maximizing the result with respect to . The proof is complete once we notice that is increasing and that for each and each , the quantity is maximized by the choice . ∎

3. Allowance Equilibrium Price and a First Singular FBSDE

The goal of this section is to extend the first model introduced in section 2 to an economy with firms, and solve for the allowance price.

3.1. Switching to a Risk Neutral Framework

As before, we assume that is the price of one allowance in a one-compliance period cap-and-trade model, and that the market for allowances is frictionless and liquid. In the absence of arbitrage, is a martingale for a measure equivalent to the historical measure . Because we are in a Brownian filtration,

for some sequence of adapted processes. By Girsanov’s theorem, the process defined by

is a Wiener process for so that equation (1) giving the dynamics of the perceived emissions of a firm now reads:

under , where the new drift is defined by for all .

3.2. Market Model with Firms

We now consider an economy comprising firms labelled by , and we work in the risk neutral framework for allowance trading discussed above. When a specific quantity such as cost function, utility, cumulative emission, trading strategy, depends upon a firm, we use a superscript i to emphasize the dependence upon the -th firm. So in equilibrium (i.e. whenever each firm implements its optimal abatement strategy), for each firm we have

with given initial perceived emissions . Consequently, the aggregate perceived emission defined by

satisfies

where

Again, since we are in a Brownian filtration, it follows from the martingale representation theorem that there exists a progressively measurable process such that

| and |

Furthermore, in order to entertain a concrete existence and uniqueness result, we assume that is one-dimensional and that there exist deterministic continuous functions and such that and , for all , -a.s.

Consequently, the processes , , and satisfy a system of Forward Backward Stochastic Differential Equations (FBSDEs for short) under , which we restate for the sake of later reference:

| (12) |

The fact that the terminal condition for is given by an indicator function results from the equilibrium analysis of these markets. See [4] and [3]. is the global emission target set by the regulator for the entire economy. It represents the cap part of the cap-and-trade scheme. is the penalty that firms have to pay for each emission unit not covered by the redemption of an allowance. Currently, this penalty is euros in the European Union Emission Trading Scheme (EU ETS). Notice that since all the cost functions are strictly convex, is strictly increasing. We shall make the following additional assumptions:

| (13) | |||

| (14) | |||

| (15) |

We denote by the collection of all -valued progressively measurable processes on , and we introduce the subsets:

| and |

3.3. Solving the Singular Equilibrium FBSDE

The purpose of this subsection is to prove existence and uniqueness of a solution to FBSDE (12).

Theorem 1.

Proof.

For any function , we write FBSDE() for the FBSDE (12) when the function appearing in the terminal condition in the backward component of (12) is replaced by .

(i) We first prove uniqueness. Let and be two solutions of FBSDE (12). Clearly it is sufficient to prove that . Let us set:

Notice that and are bounded processes. By direct calculation, we see that

where

Since and , because is nondecreasing, this implies that

Since and is (strictly) increasing, this implies that a.e. and therefore by continuity.

(ii) We next prove existence. Let be an increasing sequence of smooth non-decreasing functions with and such that .

(ii-1) We first prove the existence of a solution when the boundary condition is given by . For every , the FBSDE() satisfies the assumption of Theorems 5.6 and 7.1 in [15] with , , , (by (15)) and (since is non-decreasing) so that Condition (5.11) in [15] holds with and for any . By Theorem 7.1 in [15], the FBSDE() has a unique solution . Moreover, it holds , , for some deterministic function . In contrast with [15], the function is not a random field but a deterministic function since the coefficients of the FBSDE are deterministic. We refer to [17] for the general construction of when the coefficients are deterministic. Since the sequence is increasing we deduce from the comparison principle [15, Theorem 8.6], which applies under the same assumption as [15, Theorem 7.1], that, for any , the sequence of functions is non-decreasing. By [15, Theorem 8.6] again, is non-decreasing in and non-increasing in . Since is -valued and , we deduce that is -valued as well. Since the sequence of functions is non-decreasing, we may then define:

Clearly, is -valued and is a non-decreasing function for any . Moreover, is non-decreasing in and non-increasing in .

By Theorem 6.1– and Theorem 7.1– in [15], we know that, for every , the function is Lipschitz continuous with respect to , uniformly in . Actually, we claim that, for any , the function is Lipschitz continuous in , uniformly in and in . The proof follows again from Theorem 6.1– and Theorem 7.1– in [15]. To be more specific, we need to establish a uniform upper bound for the bounded solutions to the first ODE in [15, (3.12)] associated with an arbitrary positive terminal condition . Namely, for given bounded (measurable) functions and , with , we are seeking an upper bound for any bounded satisfying

Here is understood as an upper bound for the derivative of with respect to , and as a lower bound for the derivative of with respect to . As long as doesn’t vanish, we deduce from a simple computation that

Since the right-hand side above is always (strictly) positive, we conclude that it is indeed a solution for any . Therefore, there exists a constant , independent of , such that for any . By in Theorem 6.1 and in Theorem 7.1 in [15], we deduce that, for any , the function is Lipschitz continuous with respect to , uniformly in and . Letting tend to , we deduce that the same holds for .

Notice that the process solves the (forward) stochastic differential equation

where here and in the following, we use the notation for the composition of the functions and . Since is increasing and the sequence is non-decreasing, it follows from the comparison theorem for (forward) stochastic differential equations that the sequence of processes is non-increasing. We may then define:

(ii-2) To identify the dynamics of the limiting process , we introduce the process defined on as the unique strong solution of the stochastic differential equation

The fact that the function is bounded and Lipschitz-continuous in space (locally in time), together with our assumptions on , and guarantee the existence and uniqueness of such a strong solution. Since is at most of linear growth and is bounded, the solution cannot explode as tend to , so that the process can be extended by continuity to the closed interval . Since is Lipschitz continuous with respect to , uniformly in for any , we deduce from the classical comparison result for stochastic differential equations that for any . Letting tend to , it also holds . Since, for any , , for , and is a non-decreasing function, we deduce that is a non-decreasing function as well. Obviously, the same holds for . We then use the fact that together with the increase of to compute, using Itô’s formula, that, for any :

| (16) |

by the Lipschitz property of the coefficients and . Taking expectation, we deduce

Then

where , by the dominated convergence theorem. Therefore it follows from Gronwall’s inequality that as tends to . Repeating the argument, but using in addition the Burkhölder–Davis–Gundy inequality in (16), we deduce that in , and as a consequence, .

(ii-3) The key point to pass to the limit in the backward equation is to prove that . Given a small real , we write

| (17) |

where is as in (14). (Here, the notation means that for any .) On the event , the process coincides with , solution to

where is a given bounded and continuous function which is Lipschitz continuous with respect to , which satisfies , and which coincides with on .

Since is bounded and is bounded on , we may introduce an equivalent measure under which the process , , is a Brownian motion. Then solves the stochastic differential equation

| (18) |

By Theorem 2.3.1 in [16], the conditional law, under , of given the initial condition has a density with respect to the Lebesgue measure. Consequently, , and the same holds true under the equivalent measure . Therefore,

By (17), we deduce

As tends to 0, the right-hand side above tends to 0, so that

| (19) |

which implies that we can use instead of in (12). Moreover, we also have:

| (20) |

for each . The fact that implies:

as by (20). On the other hand, since , it follows from the non-decrease of , the dominated convergence theorem, and (20) that

Hence . Now, let be such that

Notice that takes values in , and therefore . Similarly, using the increase and the decrease of the sequences and respectively, together with the increase of the functions and and the continuity of the function for , we see that for :

Since , this shows that on , and the proof of existence of a solution is complete. ∎

Impact on the model for emission control. As expected, the previous result implies that the tougher the regulation (i.e. the larger and/or the smaller ), the higher the emission reductions (the lower ). In particular, in the absence of regulation which corresponds to , the aggregate level of emissions is at its highest.

We also notice that the assumptions in Theorem 1 can be specified in such a way that the aggregate perceived emission process takes non-negative values, as expected from the rationale of the model.

Proposition 3.

Proof.

By (15), we know that for . Since the process is -valued, we deduce from the comparison principle for forward SDEs that the forward process is dominated by the solution to the SDE:

Observe that our conditions on and imply that, whenever , we have and therefore . Then , so that . Similarly, , for any and .

As a consequence, for any initial condition , we can write in the forward equation in (12) as

where the ratio , for , is uniformly bounded in and in in compact subsets of since is Lipschitz-continuous in space, uniformly in time in compact subsets of , see Point (ii-1) in the proof of Theorem 1. Similarly, the processes

| and |

are adapted and bounded, by the Lipschitz property of the coefficients in uniformly in , and the fact that . We then deduce that may be expressed as

with , . ∎

Remark 4.

Using for additional estimates from the theory of partial differential equations, we may also prove that appearing in the above proof of Proposition 3 grows up at most as when . This implies that is integrable on the whole and thus, that as well when . Since this result is not needed in this paper, we do not provide a detailed argument.

4. Enlightening Example of a Singular FBSDE

We saw in the previous section that the terminal condition of the backward equation can be a discontinuous function of the terminal value of the forward component without threatening existence or uniqueness of a solution to the FBSDE when the forward dynamics are non-degenerate in the neighborhood of the singularity of the terminal condition. In this section, we show that this is not the case when the forward dynamics are degenerate, even if they are hypoelliptic and the solution of the forward equation has a density before maturity. We explained in the introduction why this seemingly pathological mathematical property should not come as a surprise in the context of equilibrium models for cap-and-trade schemes. Motivated by the second model given in subsection 2.2, we consider the FBSDE:

| (21) |

with the terminal condition

| (22) |

for some real number . Here, is a one-dimensional Wiener process. This unrealistic model corresponds to quadratic costs of production, and choosing appropriate units for the penalty and the emission rate to be . (For notational convenience, the martingale measure is denoted by instead of as in Section 3, and the associated Brownian motion by instead of ).

Below, we won’t discuss the sign of the emission process as we did in Proposition 3 above for the first model. Our interest in the example (21)–(22) is the outcome of its mathematical analysis, not its realism! We prove the following unexpected result.

Theorem 2.

Given , there exists a unique progressively measurable triple satisfying (21) together with the initial conditions and , and

| (23) |

Moreover, the marginal distribution of is absolutely continuous with respect to the Lebesgue measure for any , but has a Dirac mass at when . In other words:

In particular, may not satisfy the terminal condition . However, the weaker form (23) of terminal condition is sufficient to guarantee uniqueness.

Before we engage in the technicalities of the proof we notice that the transformation

| (24) |

maps the original FBSDE (21) into the simpler one

| (25) |

with the same terminal condition . Moreover, the dynamics of can be recovered from those of since in (21) is purely autonomous. In particular, except for the proof of the absolute continuity of for , we restrict our analysis to the proof of Theorem 2, for solution of (25) since and have the same terminal values at time .

We emphasize that system (25) is doubly singular at maturity time : the diffusion coefficient of the forward equation vanishes as tends to and the boundary condition of the backward equation is discontinuous at . Together, both singularities make the emission process accumulate a non-zero mass at at time . This phenomenon must be seen as a stochastic residual of the shock wave observed in the inviscid Burgers equation

| (26) |

with as boundary condition. As explained below, equation (26) is the first-order version of the second-order equation associated with (25).

Indeed, it is well-known that the characteristics of (26) may meet at time and at point . By analogy, the trajectories of the forward process in (25) may hit at time with a non-zero probability, then producing a Dirac mass. In other words, the shock phenomenon behaves like a trap into which the process (or equivalently the process ) may fall with a non-zero probability. It is then well-understood that the noise plugged into the forward process may help it to escape the trap. For example, we saw in Section 3 that the emission process did not see the trap when it was strongly elliptic in the neighborhood of the singularity. In the current framework, the diffusion coefficient vanishes in a linear way as time tends to maturity: it decays too fast to prevent almost every realization of the process from falling into the trap.

As before, we prove existence of a solution to (25) by first smoothing the singularity in the terminal condition, solving the problem for a smooth terminal condition, and obtaining a solution to the original problem by a limiting argument. However, in order to prove the existence of a limit, we will use PDE a priori estimates and compactness arguments instead of comparison and monotonicity arguments. We call mollified equation the system (25) with a terminal condition

| (27) |

given by a Lipschitz non-decreasing function from to which we view as an approximation of the indicator function appearing in the terminal condition (22).

4.1. Lipschitz Regularity in Space

Proposition 4.

Assume that the terminal condition in (25) is given by (27) with a Lipschitz non-decreasing function with values in . Then, for each , (25) admits a unique solution satisfying and . Moreover, the mapping

is -valued, is of class on and has Hölder continuous first-order derivative in time and first and second-order derivatives in space.

Finally, the Hölder norms of , , and on a given compact subset of do not depend upon the smoothness of provided is -valued and non-decreasing. Specifically, the first-order derivative in space satisfies

| (28) |

In particular, is non-decreasing for any .

Finally, for a given initial condition , the processes and , solution to the backward equation in (25) (with as boundary condition), are given by:

| (29) |

Proof.

The problem is to solve the system

| (30) |

with as terminal condition and as initial condition. The drift in the first equation, i.e. , is decreasing in , and Lipschitz continuous, uniformly in . By Theorem 2.2 in Peng and Wu [18] (with , and therein), we know that equation (30) admits at most one solution. Unfortunately, Theorem 2.6 in Peng and Wu (see also Remark 2.8 therein) does not apply to prove existence directly.

To prove existence, we use a variation of the induction method in Delarue [7]. In the whole argument, stands for the generic initial time at which the process starts. The proof consists in extending the local solvability property of Lipschitz forward-backward SDEs as the distance increases, so that the value of will vary in the proof. Recall indeed from Theorem 1.1 in [7] that existence and uniqueness hold in small time. Specifically, we can find some small positive real number , possibly depending on the Lipschitz constant of , such that (30) admits a unique solution when belongs to the interval . Remember that the initial condition is . As a consequence, we can define the value function . By Corollary 1.5 in [7], it is known to be Lipschitz in space uniformly in time as long as the initial time parameter remains in . The diffusion coefficient in (30) being uniformly bounded away from on the interval , by Theorem 2.6 in [7], (30) admits a unique solution on when is assumed to be in . Therefore, we can construct a solution to (30) in two steps when : we first solve (30) on with as initial condition and as giving the terminal condition, the solution being denoted by ; then, we solve (30) on with the previous as initial condition and with as giving the terminal condition, the solution being denoted by . We already know that matches . To patch and into a single solution over the whole time interval , it is sufficient to check the continuity property as done in Delarue [7]. This continuity property is a straightforward consequence of Corollary 1.5 in [7]: on , has the form . In particular, . This proves the existence of a solution to (30) with as initial condition.

We conclude that, for any , (30) admits a unique solution satisfying and . In particular, the value function (i.e. the value at time of the solution under the initial condition ) can be defined on the whole .

From Corollary 1.5 in [7] and the discussion above, we know that the mapping is Lipschitz continuous when is less than and that, for any , has the form when is less than . In particular, on any , being less than , (30) may be seen as a uniformly elliptic FBSDE with a Lipschitz boundary condition. By Theorem 2.1 in Delarue and Guatteri [9] (together with the discussion in Section 8 therein), we deduce that belongs to , that is bounded on the whole and that is bounded on every compact subset of 111Specifically, Theorem 2.1 in [9] says that belongs to and that is bounded on every compact subset of . In fact, by Corollary 1.5 in Delarue [7], we know that belongs to and that is bounded on for small enough.. Moreover, (29) holds.

By the martingale property of , it is well-seen that is -valued. To prove that it is non-decreasing (with respect to ), we follow the proof of Theorem 1. We notice that satisfies the SDE:

which has a Lipschitz drift with respect to the space variable. In particular, for , , so that .

We now establish (28). For , the forward equation in (30) has the form

| (31) |

Since is in space on with bounded Lipschitz first-order derivative, we can apply standard results on the differentiability of stochastic flows (see for example Kunita’s monograph [11]). We deduce that, for almost every realization of the randomness and for any , the mapping is differentiable and

| (32) |

In particular,

| (33) |

Since is non-decreasing, we know that on so that belongs to . Since is also bounded on the whole , we deduce by differentiating the right-hand side in (31) with that exists as well and that . To complete the proof of (28), we then notice that for any ,

so that taking expectations we get:

Now, differentiating with respect to , we have:

which concludes the proof of (28).

It now remains to investigate the Hölder norms (both in time and space) of , , and . We first deal with itself. For ,

From (28), we deduce

since . So for , is 1/2-Hölder continuous in time , uniformly in space and in the smoothness of .

Now, by Theorem 2.1 in Delarue and Guatteri [9], we know that satisfies the PDE

| (34) |

with as boundary condition. On , , equation (34) is a non-degenerate second-order PDE of dimension 1 with as drift, this drift being -continuous independently of the smoothness of . By well-known results in PDEs (so called Schauder estimates, see for example Theorem 8.11.1 in Krylov [10]), for any small , the -norm of on is independent of the smoothness of . ∎

4.2. Boundary Behavior

Still in the framework of a terminal condition given by a smooth (i.e. non-decreasing Lipschitz) function with values in , we investigate the shape of the solution as approaches .

Proposition 5.

Assume that there exists some real such that on . Then, there exists a universal constant such that for any

| (35) |

In particular, as uniformly in in compact subsets of .

Similarly, assume that there exists an interval such that on . Then, for any ,

| (36) |

In particular, as uniformly in in compact subsets of .

Proof.

We only prove (35), the proof of (36) being similar. To do so, we fix and consider the following system

with as initial condition for the forward equation and as terminal condition for the backward part. The solution given by Proposition 4 with and satisfies for any so that almost surely for . Now, since is non-decreasing, almost surely, namely . Setting , recall that is deterministic, we see that:

| (37) |

Now, since

with , by choosing as in the statement of Proposition 5 we get:

and we complete the proof by applying standard estimates for the decay of the cumulative distribution function of a Gaussian random variable. Note indeed that if we use the notation for the variance of a random variable . ∎

The following corollary elucidates the boundary behavior between and with and as above.

4.3. Existence of a Solution

We now establish the existence of a solution to (25) with the original terminal condition. We use a compactness argument giving the existence of a value function for the problem.

Proposition 6.

There exists a continuous function satisfying

-

(1)

belongs to and solves (34),

-

(2)

is non-decreasing and -Lipschitz continuous for any ,

- (3)

- (4)

and for any initial condition , the strong solution of

| (40) |

is such that is a martingale with respect to the filtration generated by .

Proof.

Choose a sequence of -valued smooth non-decreasing functions such that for and for , , and denote by the corresponding sequence of functions given by Proposition 4. By Proposition 4, we can extract a subsequence, which we will still index by , converging uniformly on compact subsets of . We denote by such a limit. Clearly, satisfies (1) in the statement of Proposition 6. Moreover, it also satisfies (2) because of Proposition 4, (3) by Proposition 5, and (4) by Corollary 1. Having Lipschitz coefficients, the stochastic differential equation (40) has a unique strong solution on for any initial condition . If we denote the solution by , Itô’s formula and (34), imply that the process is a local martingale. Since it is bounded, it is a bona fide martingale. ∎

We finally obtain the desired solution to the FBSDE in the sense of Theorem 2.

Proposition 7.

and being as above and setting

the process has an a.s. limit as tends to . Similarly, the process has an a.s. limit as tends to , and the extended process is a martingale with respect to the filtration generated by . Morever, -a.s., we have:

| (41) |

and

| (42) |

Notice that is not defined for .

Proof.

The proof is straightforward now that we have collected all the necessary ingredients. We start with the extension of up to time . The only problem is to extend the drift part in (40), but since is non-negative and bounded, it is clear that the process

is almost-surely increasing in , so that the limit exists. The extension of up to time follows from the almost-sure convergence theorem for positive martingales.

To prove (41), we apply (3) in the statement of Proposition 6. If , then we can find some such that for close to , so that for close to , i.e. . Since , we deduce that

In the same way,

This proves (41). Finally (42) follows from Itô’s formula. Indeed, by Itô’s formula and (34),

By definition, , . By part (2) in the statement of Proposition 6, it is in . Therefore, the Itô integral

makes sense as an element of . This proves (42). ∎

4.4. Improved Gradient Estimates

Using again standard results on the differentiability of stochastic flows (see again Kunita’s monograph [11]) we see that formulae (32) and (33) still hold in the present situation of a discontinuous terminal condition. We also prove a representation for the gradient of of Malliavin-Bismut type.

Proposition 8.

For , admits the representation

| (43) |

In particular, there exists some constant such that

| (44) |

Proof.

For , Proposition 7 yields

The bounds we have on and justify the exchange of the expectation and integral signs. We obtain:

Similarly, we can exchange the expectation and the partial derivative so that

Since is a martingale, we deduce:

Letting tend to zero and applying dominated convergence, we complete the proof of the representation formula of the gradient.

To derive the bound (44), we emphasize that, for away from (say for example ), the probability that hits is very small and decays exponentially fast as tends to . On the complement, i.e. for , we know that tends to as tends to . Specifically, following the proof of Proposition 5, there exists a universal constant such that for any and

the last line following from maximal inequality (IV.37.12) in Rogers and Williams [20].

The same argument holds for by noting that (43) also holds for . ∎

Remark 7.

The stochastic integral in the Malliavin-Bismut formula (43) is at most of order . Therefore, the typical resulting bound for in the neighborhood of is . Obviously, it is less accurate than the bound given by Propositions 4 and 6. This says that the Lipschitz smoothing of the singularity of the boundary condition obtained in Propositions 4 and 6, namely , follows from the first-order Burgers structure of the PDE (34) and that the diffusion term plays no role in it. This is a clue to understand why the diffusion process feels the trap made by the boundary condition. On the opposite, the typical bound for we would obtain in the uniformly elliptic case by applying a Malliavin-Bismut formula (see Exercice 2.3.5 in Nualart [16]) is of order , which is much better than .

Nevertheless, the following proposition shows that the diffusion term permits to improve the bound obtained in Propositions 4 and 6. Because of the noise plugged into , the bound cannot be achieved. This makes a real difference with the inviscid Burgers equation (26) which admits

as solution, with for . (See for example (10.12’) in Lax [13].)

Proposition 9.

For any , it holds .

Proof.

Given , we consider as in the statement of Proposition 7. As in the proof of Proposition 4, we start from

Therefore, for any initial condition ,

Unfortunately, we do not know whether is differentiable with respect to . However,

Using (33), the non-negativity of and Fatou’s lemma,

Consequently, in order to prove that , it is enough to prove that:

| (45) |

is finite with non-zero probability. To do so, the Lipschitz bound given by Proposition 4 is not sufficient since the integral of the bound is divergent. To overcome this difficulty, we use (44): with non-zero probability, the values of the process at the neighborhood of may be made as large as desired. Precisely, for as in Proposition 8, it is sufficient to prove that there exists small enough such that . For , we deduce from the boundedness of the drift in (40) that

By independence of the increments of the Wiener integral, we get

The first probability in the above right-hand side is clearly positive for . The second one is equal to

Using maximal inequality (IV.37.12) in Rogers and Williams [20], the above right hand-side is always positive. By (44), we deduce that, with non-zero probability, the limsup in (45) is finite. ∎

4.5. Distribution of for .

We finally claim:

Proposition 10.

Proof.

Obviously, we can assume , so that . (For simplicity, we will write for .) We start with the absolute continuity of at time . Since is smooth away from , we can compute the Malliavin derivative of . (See Theorem 2.2.1 in Nualart [16].) It satisfies

for . In particular,

| (46) |

By Proposition 9, we deduce that for any . By Theorem 2.1.3 in Nualart [16], we deduce that the law of has a density with respect to the Lebesgue measure.

To prove the existence of a point mass at time , it is enough to focus on since the latter is equal to . We prove the desired result by comparing the stochastic dynamics of to the time evolution of solutions of simpler stochastic differential equations. With the notation used so far, is a solution of the stochastic differential equation:

| (47) |

so it is natural to compare the solution of this equation to solutions of stochastic differential equations with comparable drifts. Following Remark 6, we are going to do so by comparing with the solution of the inviscid Burgers equation (26). To this effect we use once more the function defined by introduced earlier. As said in Remark 7, the function is a solution of the Burgers equation (26) which, up to the diffusion term (which decreases to like when ), is the same as the partial differential equation satisfied by . Using (35) and (36) with and , we infer that and are exponentially close as tends to when or ; using (38) and (39) with and , we conclude that the distance between and is at most of order with respect to as tends to when . In any case, we have

| (48) |

for some universal constant . We now compare (47) with

| (49) |

with as initial conditions. Clearly,

| (50) |

Knowing that when , we anticipate that scenarios satisfying can be viewed as solving the stochastic differential equations:

with as initial conditions. This remark is useful because these equations have explicit solutions:

| (51) |

We define the event by:

and we introduce the quantities and defined by

so that

whenever . For such a choice of , since

it is easy to see that if we choose such that is small enough for to hold, then

on the event . This implies that and coincide on , and consequently that and hence on by (50). This completes the proof for these particular choices of and . In fact, the result holds for any and any . Indeed, since has a strictly positive density at any time , if we choose so that , then using the Markov property we get

which completes the proof in the general case. ∎

Remark 8.

We emphasize that the expression for given in (46) can vanish with a non-zero probability when replacing by . Indeed, the integral

may explode with a non-zero probability since the derivative is expected to behave like as tends to and to . Indeed, is known to behave like the solution of the Burgers equation when close to the boundary, see (48). As a consequence, we expect to behave like the gradient of the solution of the Burgers equation. The latter is singular in the neighborhood of the final discontinuity and explodes like in the cone formed by the characteristics of the equation.

However, in the uniformly elliptic case, the integral above is always bounded since is at most of order as explained in Remark 7.

4.6. Uniqueness

Our proof of uniqueness is based on a couple of comparison lemmas.

Lemma 1.

Proof.

Applying Itô’s formula to , we obtain

Therefore,

In particular,

which completes the proof. ∎

The next lemma can be viewed as a form of conservation law.

Lemma 2.

Let be a non-increasing sequence of non-decreasing smooth functions matching on some intervals and on some intervals and converging towards , then the associated solutions , given by Proposition 4 converge towards constructed in Proposition 6.

The conclusion remains true if is a non-decreasing sequence converging towards .

Proof.

Each is a solution of the conservative partial differential equation (34). Considering as in the proof of Proposition 6, we have for any

Notice that the integrals are well-defined because of Proposition 5. Since as for , we deduce that

Since the right hand side converges towards 0 as tends to , so does the left hand side, but since by Lemma 1 (choosing ), we must also have:

Since is equicontinuous (by Proposition 4), we conclude that . The proof is similar if . ∎

To complete the proof of uniqueness, consider a sequence as in the statement of Lemma 2. For any solution of (25) with , Lemma 1 yields

Passing to the limit, we conclude that

Choosing a non-decreasing sequence , instead, we obtain the reverse inequality, and hence, we conclude that for . By uniqueness to (40), we deduce that , so that . We easily deduce that as well.

Remark 9.

We conjecture that the analysis performed in this section can be extended to more general conservation laws than Burgers equation. The Burgers case is the simplest one since the corresponding forward - backward stochastic differential equation is purely linear.

5. Option Pricing and Small Abatement Asymptotics

In this section, we consider the problem of option pricing in the framework of the first equilibrium model introduced in this paper.

5.1. PDE Characterization

Back to the risk neutral dynamics of the (perceived) emissions given by (12), we assume that the emissions of the business as usual scenario are modeled by a geometric Brownian motion, so that and . As explained in the introduction, this model has been used in most of the early reduced form analyses of emissions allowance forward contracts and option prices (see [6] and [5] for example). The main thrust of this section is to include the impact of the allowance price on the dynamics of the cumulative emissions. As we already saw in the previous section, this feedback is the source of a nonlinearity in the PDE whose solution determines the price of an allowance. Throughout this section, we assume that under the pricing measure (martingale spot measure) the cumulative emissions and the price of a forward contract on an emission allowance satisfy the forward-backward system:

| (52) |

with as in (15) with and . For notational convenience, the martingale measure is denoted by instead of as in Section 3 and the associated Brownian motion by instead of .

Theorem 1 directly applies here, so that equation (52) is uniquely solvable given the initial condition . In particular, we know from the proof of Theorem 1 that the solution of the backward equation is constructed as a function of the solution of the forward equation. Moreover, since we are assuming that , it follows from Proposition 3 that the process takes positive values.

Referring to [17], we notice that the function is the right candidate for being the viscosity solution to the PDE

| (53) |

Having this connection in mind, we consider next the price at time of a European call option with maturity and strike on an allowance forward contract maturing at time . It is given by the expectation

which can as before, be written as a function of the current value of the cumulative emissions, where the notation in superscript indicates that . Once the function is known and/or computed, for exactly the same reasons as above, the function appears as the viscosity solution of the linear partial differential equation:

| (54) |

which, given the knowledge of , is a linear partial differential equation. Notice that in the case of infinite abatement costs, except for the fact that the coefficients of the geometric Brownian motion were assumed to be time dependent, the above option price is the same as the one derived in [5].

5.2. Small Abatement Asymptotics

Examining the PDEs (53) and (54), we see that there are two main differences with the classical Black-Scholes framework. First, the underlying contract price is determined by the nonlinear PDE (53). Second, the option pricing PDE (54) involves the nonlinear term , while still being linear in terms of the unknown function . Because the function is determined by the first PDE (53), this nonlinearity is inherent to the model, and one cannot simply reduce the PDE to the Black-Scholes equation.

In order to understand the departure of the option prices from those of the Black-Scholes model, we introduce a small parmater , and take the abatement rate to be of the form for some fixed non-zero increasing continuous function . We denote by and the corresponding prices of the allowance forward contract and the option. Here, what we call Black-Scholes model corresponds to the case . Indeed, in this case, both (53) and (54) reduce to the linear Black-Scholes PDE, differing only through their boundary conditions. This model was one of the models used in [5] for the purpose of pricing options on emission allowances based on price data exhibiting no implied volatility smile.

For , the nonlinear feedback given by the abatement rate disappears and we easily compute that, for ,

| (55) | |||||

| (56) |

where is the geometric Brownian motion:

| (57) |

used as a proxy for the cumulative emissions in business as usual, with the initial condition . See for example [5] for details and complements. The main technical result of this section is the following first order Taylor expansion of the option price.

Proposition 11.

Proof.

The proof divided into four parts.

(i) We first prove that the functions and , with and on and respectively, belongs to and respectively.

By (55), we know that is on . Obviously on the whole since . Using the bound

we deduce that

for . This shows that decays towards faster than any polynomial. In particular . Differentiating (55) with respect to , we conclude by the same argument that and decay towards faster than any polynomial, so that the first and second-order derivatives in space are continuous on . Obviously, for any and, by differentiating (55) with respect to , we can also prove that is continuous on . Since on , we deduce that is of class on .

All in all, the computation of the first-order derivatives yields

for and . The above right-hand side is less than for away from , the constant being independent of . When is close to ,

so that the bound

| (58) |

is always true. As a by-product, we deduce that , so that

In particular,

By the same argument as the one used for , we see that and its partial derivatives with respect to and decay towards as tends to , at a faster rate than any polynomial one. In particular, setting for and , we deduce that belongs to .

(ii) We use the smoothness of and apply Itô’s formula to , where denotes the forward process in (52), when and under the initial condition , . Using the fact that belongs to together with (58), we deduce that, for any ,

Clearly, as , for . Since , see (ii-3) in the proof of Theorem 1, we deduce that as . Therefore,

| (59) |

the right-hand side above making sense because of the bound (58). By a similar argument, we get

| (60) |

Notice that is bounded since is Lipschitz-continuous so that the integral above is well-defined. By (58) and (59), we know that , for a constant independent of and . Therefore,

where stands for the Landau notation. By (60), we finally get

| (61) |

(iii) We now prove that:

for . For any ,

By continuity with respect to parameters of solutions of stochastic differential equations, we see that that a.s. as . Therefore, by the porte-manteau theorem, it holds for any ,

On the interval , with small enough so that , the function is continuously differentiable with a non-zero derivative and thus defines a -diffeomorphism. Moreover, since , the random variable has a smooth density on the interval . Therefore, the random variable has a continuous density on the interval . We conclude that

(iv) We now have all the ingredients needed to complete the proof. From (61), we have:

Since, for any , converges towards uniformly as tends to 0, and since , we deduce from (58) and from Lebesgue dominated convergence theorem that

The final result then follows from the identity:

which can be derived by differentiation of (56) and making use of the equality .∎

5.3. Numerical results

In this final subsection we provide the following numerical evidence of the accuracy of the small abatement asymptotic formula derived above:

-

(1)

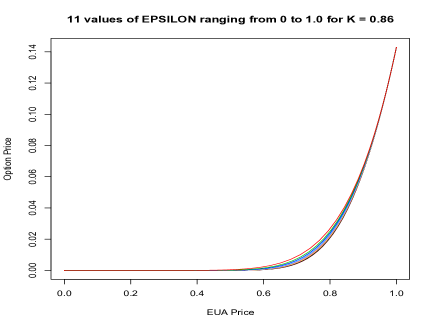

We compute numerically with high accuracy, and we then compute values of using the values of so computed. We used an explicit finite difference monotone scheme (see for example [1] for details). The left pane of Figure 1 gives a typical sample of results. For the sake of illustration we used the abatement function corresponding to quadratic costs of abatement. The penalty, cap, emission volatility and emission rate in BAU were chosen as , , and where the length of the regulation period was year. The prices of the allowances and were computed on a regular grid in the time log-emission space. The mesh of the time subdivision was . The grid of log-emission was regular, centered around with mesh connected to by the standard stability condition. We considered an option with maturity and strike . We computed and over this grid for values of , , and we plotted the option prices against the corresponding allowance prices . The graphs decrease as increases from to .

Figure 1. European call option prices for . We plotted against in order to show how the option price depends upon the value of the underlying allowance.

-

(2)

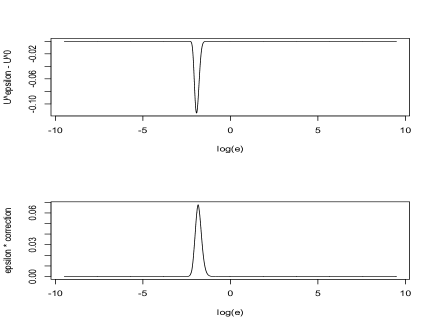

We also computed the expectation appearing as the coefficient of in the first order expansion of Proposition 11. We used a plain Monte Carlo computation of the expectation with sample paths. The right pane of Figure 1 shows the potential of the approximation for . The top plot shows the difference between the exact option value and the linear approximation given by setting and ignoring the feedback effect. Both option values were computed by solving the partial differential equations as explained at the beginning of the section. The lower plot shows the first order correction as identified in Proposition 11, showing the potential of the approximation.

References

- [1] G. Barles and P.E. Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Analysis, 4:271–283, 1991.

- [2] R. Belaouar, A. Fahim, and N. Touzi. Optimal Production Policy under Carbon Emission Market. Preprint.

- [3] R. Carmona, F. Fehr, J. Hinz, and A. Porchet. Market designs for emissions trading schemes. SIAM Review, 52:403–452, 2010.

- [4] R. Carmona, M. Fehr, and J. Hinz. Optimal stochastic control and carbon price formation. SIAM Journal on Control and Optimization, 48(12):2168–2190, 2009.

- [5] R. Carmona and J. Hinz. Risk neutral modeling of emission allowance prices and option valuation. Technical report, Princeton University, 2009.

- [6] M Chesney and L. Taschini. The endogenous price dynamics of the emission allowances: An application to CO2 option pricing. Technical report, 2008.

- [7] F. Delarue. On the existence and uniqueness of solutions to FBSDEs in a non-degenerate case. Stochastic Processes and Applications, 99:209–286, 2002.

- [8] F. Delarue. Estimates of the solutions of a system of quasi-linear PDEs. A probabilistic scheme. Séminaire de Probabilités, XXXVII, 290–332, 2003.

- [9] F. Delarue and G. Guatteri. Weak Existence and Uniqueness for FBSDEs. Stochastic Processes and Applications, 116:1712–1742, 2006.

- [10] N. Krylov. Lectures on Elliptic and Parabolic Equations in Hölder Spaces, volume 12 of Graduate Studies in Mathematics. American Mathematical Society, 1996.

- [11] H. Kunita. Stochastic Flows and Stochastic Differential Equations. Cambridge Studies in Advanced Mathematics. Cambridge University Press, 1990.

- [12] O.A. Ladyzenskaja, V.A. Solonnikov and N. N. Ural’ceva, Linear and quasi-linear equations of parabolic type. American Mathematical Society, 1968.

- [13] P. Lax Hyperbolic Differential Equations. Courant Lecture Notes. American Mathematical Society, 2006.

- [14] J. Ma and J. Yong. Forward-Backward Stochastic Differential Equations and their Applications, volume 1702 of Lecture Notes in Mathematics. Springer Verlag.

- [15] J. Ma, Z. Wu, D. Zhang and J. Zhang. On wellposedness of forward-backward SDEs – a unified approach. Preprint.

- [16] D. Nualart. The Malliavin Calculus and Related Topics. Probability and its Applications. Springer Verlag, 1995.

- [17] E. Pardoux and S. Peng. Backward Stochastic Differential Equations and Quasilinear Parabolic Partial Differential Equations. Lecture Notes in CIS, 176:200–217, 1992.

- [18] S. Peng and Z. Wu. Fully Coupled Forward-Backward Stochastic Differential Equations and Applications to Optimal Control. SIAM Journal on Control and Optimization, 37:825–843, 1999.

- [19] H. Pham. Continuous-time Stochastic Control and Optimization with Financial Applications. Stochastic Modelling and Applied Probability. Springer Verlag, 2009.

- [20] L.C.G. Rogers and D. Williams Diffusions, Markov Processes and Martingales. Volume 2. 2nd Edition. Cambridge University Press, 1994.

- [21] J. Seifert, M. Uhrig-Homburg, and M. Wagner. Dynamic behavior of carbon spot prices. Theory and empirical evidence. Journal of Environmental Economics and Management, 56:180–194, 2008.

- [22] Z. Wu and M. Xu. Comparison theorems for forward backward sdes. Statistics and Probability Letters, 79:426–435, 2009.