Mean Field Stochastic Adaptive Control

Abstract

For noncooperative games the mean field (MF) methodology provides decentralized strategies which yield Nash equilibria for large population systems in the asymptotic limit of an infinite (mass) population. The MF control laws use only the local information of each agent on its own state and own dynamical parameters, while the mass effect is calculated offline using the distribution function of (i) the population’s dynamical parameters, and (ii) the population’s cost function parameters, for the infinite population case. These laws yield approximate equilibria when applied in the finite population.

In this paper, these a priori information conditions are relaxed, and incrementally the cases are considered where, first, the agents estimate their own dynamical parameters, and, second, estimate the distribution parameter in (i) and (ii) above.

An MF stochastic adaptive control (SAC) law in which each agent observes a random subset of the population of agents is specified, where the ratio of the cardinality of the observed set to that of the number of agents decays to zero as the population size tends to infinity. Each agent estimates its own dynamical parameters via the recursive weighted least squares (RWLS) algorithm and the distribution of the population’s dynamical parameters via maximum likelihood estimation (MLE). Under reasonable conditions on the population dynamical parameter distribution, the MF-SAC Law applied by each agent results in (i) the strong consistency of the self parameter estimates and the strong consistency of the population distribution function parameters; (ii) the long run average stability of all agent systems; (iii) a (strong) -Nash equilibrium for the population of agents for all ; and (iv) the a.s. equality of the long run average cost and the non-adaptive cost in the population limit.

Index Terms:

adaptive control, mean field stochastic systems, Nash equilibria, stochastic optimal controlI Introduction

Overview

The control and optimization of large-scale stochastic systems is evidently of importance due to their ubiquitous appearance in engineering, industrial, social and economic settings. The complexity of these problems is amplified by the fact that for many such systems the agents involved have conflicting objectives; hence, it is appropriate to consider optimization methodologies based upon individual payoffs or costs. In particular, game theory has been formulated to capture such individual interest seeking behaviour of the agents in many social, economic and manmade systems. However, in a large-scale dynamic model, this approach results in an analytic complexity which is in general prohibitively high, and correspondingly leads to few substantive dynamic optimization results.

The optimization of large-scale linear control systems wherein (i) many agents are coupled with each other via their individual dynamics, and (ii) the costs are in an “individual to the mass” form was presented in [1, 2] where the theory of mean field (MF) control (previously termed Nash Certainty Equivalence) was introduced. It is to be noted that the dynamic large-scale cost coupled optimization structure of [2] is motivated by a variety of scenarios, for instance, those analysed in [3, 4, 5, 6].

In the literature, studies of stochastic dynamic games and team problems may be traced to the 1960s (see e.g. [7, 8, 9]) while within the optimal control context weakly interconnected systems were studied in [10], and in a two player noncooperative nonlinear dynamic game setting Nash equilibria were analysed in [11], where the coefficients for the coupling terms in the dynamics and costs are required to be small. In contrast to these studies, games with large populations are analyzed in [12, 13, 2]. In [2] the -Nash equilibrium properties are analysed for a system of competing agents where individual control laws use local information and the average effect of all agents taken together, henceforth referred to as the mass. Overall, the MF methodology for noncooperative LQG games with mean field coupling has been developed in [1, 2, 14] providing decentralized strategies which yield Nash equilibria. A nonlinear extension using McKean-Vlasov Markov process models is also presented in [15].

The central notion of MF theory is that for general classes of large population stochastic dynamic games there exist game theoretic Nash equilibria for the individual agents when each applies certain competitive strategies (i.e. control laws) with respect to the mass effect resulting from all the agents’ strategies. Here each agent is modelled by an individually controlled stochastic system and the systems interact through their individual cost functions and possibly via weak dynamical interaction. The key feedback nature of the mean field solutions is that the individual competitive actions against the mass, plus local feedback control, act so as to collectively reproduce that mass behaviour. The mass effect and associated feedback control laws are calculated offline for the infinite population case and yield approximate equilibria when applied in the finite population case.

For this class of game problems, a related approach has been independently developed in [16, 17], where the notion of oblivious equilibrium by use of a mean field approximation for models of many firm industry dynamics is proposed. The asymptotic equilibrium properties of a market with a large population of agents is studied in [18]. Another related work is [19] where a mean field Nash equilibrium is studied subject to the assumed existence of a factorizing mean field distribution corresponding to the propagation of chaos for the infinite population system. The work in [20] presents mean field control results for a Markov Decision Problem (MDP) formulation of evolutionary games and teams where the basic system hypothesis is the exchangeability of the underlying random processes.

Stochastic Adaptive Control

For discrete time dynamics the long run average (LRA) asymptotically optimal adaptive tracking problem was solved in [21]; subsequently, it was shown in [22] that strongly consistent parameter estimates may be obtained by the use of persistently excited controls. The LRA stochastic (sample path) mean square stability for continuous time linear stochastic adaptive systems was established in [23]. The weighted least squares (WLS) scheme introduced in [24] was shown in [25] to be convergent without stability and excitation assumption, and a LRA asymptotically optimal solution to the continuous time adaptive LQG control problem under controllability and observability assumptions using the WLS scheme for identification was subsequently obtained in [26] following [27, 28, 29] and [30].

MF Stochastic Adaptive Control

It is important to note that in the non-adaptive MF theory [1, 2] each agent uses its self state and self dynamical parameters (i.e. its own state and its own dynamical parameters) and statistical information on the dynamical parameters of the population in order to generate the control action. The natural initial problem in the development of adaptive MF stochastic system theory is that where each agent needs to estimate its own dynamical parameters, while its control actions are permitted to be explicit functions of the parameter distribution of the entire population of competing agents [31]. Subsequent problem generalizations are such that (i) each agent also needs to estimate the distribution parameter of the population’s dynamical parameters [32], and (ii) cost function parameters also vary over the population and this distribution parameter is unknown to each agent and hence needs to be estimated [33]. In this paper we provide a solution to the most general problem in this sequence.

The inclusion of learning procedures for the identification by a given agent of the dynamical and cost function parameters of other competing agents in a stochastic dynamic system, or of the statistical distribution of these parameters in a mass of competing agents, introduces new features into the system theoretic MF setup. In this connection we note that in the economics literature the so-called “privacy of information” on dynamical parameters and cost function parameters is an important issue [34, 35, 36].

This paper presents an MF stochastic adaptive control (SAC) law in which each agent observes a random subset of the population of agents. The MF-SAC Law specifies that the ratio of the cardinality of the observed set of agents to that of the population of agents is chosen so that it decays to zero as the population size tends to infinity. When the MF-SAC Law is applied by each member of the population, each agent estimates its self dynamical parameters via the recursive weighted least squares (RWLS) algorithm and the distribution of the population’s dynamical parameters via maximum likelihood estimation (MLE).

Under reasonable conditions on the population dynamical parameter distribution, the MF-SAC Law results in (i) the strong consistency of the self parameter estimates and the strong consistency of the population distribution function parameters; (ii) the long run average stability of all agent systems; (iii) a (strong) -Nash equilibrium for the population of agents for all ; and (iv) the a.s. equality of the long run average cost and the non-adaptive cost in the population limit.

Notation

We denote the set of nonnegative real numbers by , the set of nonnegative integers by , and the set of strictly positive integers by . The norm denotes the 2-norm of vectors and matrices, and . denotes the family of all bounded continuous functions, and for any , denotes the supremum norm: . denotes the trace, and denotes the transpose of a matrix .

II Problem Formulation and MF-SAC Law Specification

II-A Review of Non-Adaptive MF Stochastic Control

We consider a large population of stochastic dynamic agents which (subject to independent controls) are stochastically independent, but which shall be cost coupled, where the individual dynamics are defined by

| (1) |

where for agent , is the state, is the control input, is a standard Wiener process on a sufficiently large underlying probability space such that is progressively measurable with respect to . We denote the state configuration by , and (with an abuse of notation) the population average state by .

The long run average (LRA) cost function for the agent , is given by

| (2) |

w.p.1, where we assume the cost-coupling to be of the form . The coefficients will be called the dynamical and cost function parameters. The disturbance weight matrix and the control action penalizing matrix are constant matrices, which are assumed to be known by all agents, and assumed to be the same for all agents in the population. The choice of homogeneous parameters for and is only for notational brevity; the analysis is similar for varying and . The function is the control input of the agent and denotes the control inputs of the complementary set of agents .

For the basic MF control problem, the following assumptions are adopted.

A1: The disturbance processes , are mutually independent and independent of the initial conditions, and , where . ∎

A2: is an open set such that for each , is controllable and is observable. ∎

A3:

Let the parameter set be a compact set such that , and

, where , is the distribution parameter and is defined in the next hypothesis.

∎

A4: The cost-coupling is of the form: , where the function is Lipschitz continuous on with a Lipschitz constant , i.e. for all ∎

For dynamics (1) and cost function (2), a production output planning example is provided in [2] that satisfies the assumptions given above. Each agent’s production level is modeled by (1), and each agent’s cost function is of tracking type (2), where the tracked signal is a function of price, which is an averaging function of production levels: .

Following [2], the long run average (LRA) mean field (MF) problem is formulated in [37]. Each agent , obtains the positive definite solution to the algebraic Riccati equation

| (3) |

Moreover, for a given mass tracking signal the mass offset function is generated by the differential equation

| (4) |

Then, the optimal tracking control law [38] is given by

| (5) |

where solves , which is defined below by an abuse of notation:

Note that the procedure above assumes a given mass tracking signal . The equation system to calculate will be given subsequently.

We first define the empirical distribution associated with the first agents:

, , where is a set of random matrices on with the probability distribution , parameterized by , the population dynamical and cost function distribution parameter such that is compact and is an open set. Then we employ the following assumption.

A5: There exists a family of distribution functions , such that w.p.1 weakly on and uniformly over as . ∎

Each agent solves the equation system below to calculate the mass tracking signal , offline, for an infinite population of agents.

Definition II.1

Mean Field (MF) Equation System on :

| (6) | ||||

∎

The Global Observation Control Set : For the optimality analysis, we first introduce the global observation control set. The set of control inputs consists of all feedback controls adapted to , where is the -field generated by the set .

The Local Observation Control Set : The local observation control set of agent is the set of control inputs which consists of the feedback controls adapted to the set . The -field is generated by , and is the -field generated by the set .

Theorem II.1

Let AII-A-AII-A hold. The MF Stochastic Control Law (5) generates a set of controls with

| (7) |

such that

-

(i)

the MF equations (6) have a unique solution;

-

(ii)

all agent system trajectories are stable w.p.1;

-

(iii)

yields an -Nash equilibrium for all , i.e., for all , there exists such that for all

∎

Conceptually, Theorem II.1 may be paraphrased to say that individual competitive actions against the mass effect collectively produce the mass behaviour, and hence the -Nash equilibrium is obtained. In the proof of Theorem II.1, the results are first established for an infinite population and then are shown to be approximated by a large finite population with the approximation error decaying to zero as the population size goes to infinity; it is this which gives the -Nash property.

II-B MF Stochastic Adaptive Control (SAC)

In this section we first present the identification schemes to be used by each agent under the MF Stochastic Adaptive Control (SAC) Law to estimate both the self dynamical parameters and the population dynamical and cost function distribution parameter. In other words, the analysis concerns a family of agents whose control action at any instant is not permitted to be an explicit function of the self dynamical parameters and the dynamical and cost function distribution parameter . At time , the self dynamical parameters are estimated from the input-output sample path of ; in other words, each agent performs the identification based upon observations of its own trajectory. The distribution parameter is estimated from observations on a random subset of agents where , and as .

The Adaptive Agent Control Set : We next define the set of control inputs , the admissible control set of an adaptive agent , which consists of all feedback controls adapted to the set . The -field is generated by the agent’s own trajectory and control input, , and , is the observation -field generated by the trajectories and control inputs in the set , . For definiteness in this paper, the identification algorithms employed are recursive weighted least squares (RWLS) for the self dynamical parameter identification and maximum likelihood estimation (MLE) for the distribution parameter identification. However, any identification scheme which generates consistent estimates w.p.1 (subject to the given hypotheses) will also yield the system asymptotic equilibrium properties to be established.

II-B1 Self Dynamical Parameter Identification (SDPI)

We denote the self estimate of the matrix by , , and the estimate of by , where , and assume and are generated at by the identification algorithm. Note that the self cost function parameter is in the information set of agent , and is therefore not to be estimated. We adopt the notation for the true parameters in the system. At time , agent solves the RWLS equations with the measurement variable set as with the regression vector in order to obtain the estimates . To ensure controllability and observability of the estimates, a projection method is used; the estimates are projected onto the compact set , where given , is controllable and is observable. Note that is known to all agents in the system.

II-B2 Population Dynamical and Cost Function Distribution Parameter Identification

Population Dynamical Parameter Identification (PDPI)

At , agent estimates dynamical parameters of the agents in its observation set, . The admissible control set of agent is , consisting of observations of the trajectories and control inputs of all the agents in the set . Based upon this observation set, agent obtains estimates solving the RWLS equations using as the measurement variable with the regression vector .

Population Cost Function Parameter Identification (PCPI)

The solution to the RWLS equations with the inputs described above generates the estimates . The objective at this point for each agent is to obtain the estimates . The RWLS equations are then solved employing the observed control inputs such that agent calculates and sets as the measurement vector. Note that one needs the following additional assumption.

A6’: is invertible (and hence, necessarily, is controllable) for all . ∎

This rather restrictive assumption is only needed for the cost function parameter identification; therefore, PCPI will be given as an optional procedure in the MF-SAC Law. The observed control action is in the form (7); therefore arranging the variables in a certain way to be specified later, agent obtains the estimates . Solving the algebraic Riccati equation for agent obtains its estimates . The symmetry of is guaranteed. To ensure the positive definiteness of the obtained estimates , controllability, observability, and that the requirement in AII-A holds, the set is projected onto .

Distribution Parameter Identification (DPI)

Once the projected estimates , are obtained, agent forms the scaled log-likelihood-type function

calculates , the estimate of the distribution parameter, solving . Note that is known to all agents in the system.

Overall using the identification procedures explained above, agent obtains estimates and and forms the self estimated dynamical parameter vector .

II-B3 Certainty Equivalence Adaptive Control

At time , employing agent solves the MF Equation System (6) to obtain . Then using agent solves the Riccati equation (3), obtains and solves the mass offset differential equation (4) to obtain . The certainty equivalence adaptive control for the admissible control set is then given by .

To obtain the main MF-SAC result stated in Theorem II.2, we first establish the strong consistency for the family of estimates and .

II-B4 Control Excitation for Consistent Identification

In order to generate a consistent sequence of estimates w.p.1, a diminishing excitation is added to the adaptive control in (5) to give

| (8) |

where , and the process is an -valued standard Wiener process that is independent of . The sequence of random processes is assumed to be mutually independent and all members of the set have the same probability law on . Since the sequence converges to zero at a suitable rate, it will be established following [26] that the diminishing control excitation provides sufficient excitation for almost sure consistent identification and decreases sufficiently rapidly enough not to affect the limiting performance of the system with respect to , i.e. the non-adaptive case. In other words, the asymptotic performance achieved is equal to the one obtained in the non-adaptive case almost surely. The diminishing control excitation (8) was introduced in [27, 28], and it was shown in [26] to generate strongly consistent parameter estimates via RWLS for dynamical parameters of the system (1) under certainty equivalence adaptive control.

II-C The MF Stochastic Adaptive Control (SAC) Law

We observe that the control law (8) has three terms computed from the local state information, the self dynamical parameter estimates and the population distribution parameter estimate. It can be written for each agent , in the form of , , where is the LQG feedback for the system of agent based on local information; is the mass offset term based on local information and population information received from the observed set; and is the locally generated dither input. In this section we present the MF-SAC Law which generates the feedback control law , that leads to the -Nash equilibrium. The continuous time MF-SAC Law for agent with parameter , is summarized in three major steps in Table I.

Specification of the MF-SAC Law For agent : (i) Self parameter identification: Solve the RWLS equations (9) for the dynamical parameters: (subscript suppressed for clarity) (9) (10) (ii) Population-parameter identification: (a) Solve the RWLS equations (9) for the dynamical parameters . (b) Solve the RWLS equations (11) for the cost function parameters : (subscript suppressed for clarity) (11) solve the algebraic Riccati Equation (12) for , (12) set , and calculate (13) (c) Solve the MLE equation (14) at , to estimate via: (14) and solve the set of MF Equations (6) for all generating . (iii) Solve the MF Control Law Equation at and : (a) : Solve the Riccati Equation (15) at : (15) (b) : Solve the mass offset differential equation (16) at and : (16) (c) Obtain the Certainty Equivalence Adaptive Control at and : (17)

The function , in (9) is in the form of , where , and . The function is slowly increasing if it is increasing and satisfies and [26].

Note that a positive definite solution to the Riccati equation (15) exists as the projected estimate is in the set of controllable and observable dynamical parameters: .

II-D Asymptotic Properties of the MF-SAC Law

A key feature of the work in this paper is that the state aggregation integration in (6) is performed by use of the estimated distribution in place of the true distribution (see (18) below). Then the central results of this paper are the following: under the MF-SAC Law, asymptotically as the population tends to infinity, the competitive best response actions of the adaptive agents with no prior information on self dynamical parameters and no prior statistical information on dynamical and cost function parameters of the mass give rise to a unique Nash equilibrium. Moreover, the resulting cost for each agent from the MF-SAC Law is asymptotically almost surely equal to the cost resulting from the non-adaptive MF Stochastic Control Law.

Theorem II.2

MF-SAC Theorem

Then,

-

(a)

w.p.1 as (strong consistency);

-

(b)

w.p.1 as , and .

The MF-SAC Law generates a set of controls such that:

-

(c)

all agent system trajectories are stable w.p.1;

-

(d)

Nash Property: yields an -Nash Equilibrium for all , i.e., for all , there exists such that for all

-

(e)

Equal Adaptive and Non-adaptive MF Equilibrium Performance:

-

(f)

Adaptive Control Performance Equals Complete Information Performance:

∎

The proof consists of the unification of the principal Theorems III.2, III.3, IV.2 and the Propositions IV.4 and IV.5 that are presented in the remaining sections. The outline of the proof is given in Appendix D.

The technical plan of the paper is presented in three layers. The main theorem of the paper is Theorem II.2. In the first layer, Propositions IV.4, IV.5 and Theorems III.2, III.3 and IV.2 support Theorem II.2. In the second layer, Lemmas D.1, D.2, D.3, D.4, D.5, Theorem IV.3 and Proposition C.1 support Proposition IV.4 whereas Lemma III.1 supports Theorem III.2. In the third layer, Lemmas A.1, A.2, A.3 and Proposition IV.1 support Theorem IV.3.

III Convergence Properties of the MF-SAC Parameter Estimates

We show that for self dynamical parameter identification, the RWLS equations for dynamical parameters (9) with the projection method (10) provide strongly consistent, uniformly controllable and observable estimates. The population dynamical and cost function distribution parameter identification is handled in three steps. First, each agent obtains the dynamical parameter estimates for the agents in its observation set solving the RWLS equations (9). It is shown that the RWLS equations (9) with the projection method (10) applied on the observed agents’ controlled trajectories also provide strongly consistent, uniformly controllable and observable estimates. Secondly, another set of RWLS equations (11) are solved using the previously obtained dynamical parameter estimates as inputs; and finally cost function parameter estimates are obtained for the agents in the observation set (12). We show that the estimates obtained are positive definite and uniformly bounded by use of a projection method (13). Finally, we show that the MLE scheme (14) employed using these estimates provides strongly consistent population distribution parameter estimates.

III-A Asymptotic Convergence of the Dynamical Parameter Estimates

The RWLS algorithm is self-convergent [25], i.e., it converges to a certain random vector almost surely irrespective of the control law design, but there is no guarantee that the estimated dynamical parameters will be controllable and observable, or the cost function estimates will be positive definite. To ensure that the sequence of estimated dynamical parameters are controllable, observable, uniformly bounded and the sequence of estimated cost parameters are positive definite and uniformly bounded we use the projection method [23].

For self dynamical parameter identification, the self dynamical parameter estimates with the cost function parameter , ( known by agent ) is projected (denoted by in (10)) onto the compact set , where for the given , is controllable and is observable.

For the distribution parameter identification, the population dynamical parameter estimates together with the cost function parameter estimates are projected onto the compact subset of the set of controllable and observable dynamical parameters where, in addition, , is positive definite (for which the control law generated by (15) necessarily exists and is asymptotically stabilizing).

Lemma III.1

Let be a compact set such that . Set . Let be the estimate of obtained by the RWLS equations (9), and let be the estimate of obtained by the RWLS equations (11) and (12). Assume w.p.1 as . Then, (together with a co-ordinate ordering measurable tie breaking rule), satisfies w.p.1 for all , and w.p.1 as . In the SDPI case the corresponding result is achieved by setting for all . ∎

The Lemma is proved in Appendix B.

Now, given the projection method lemma, we show that the RWLS equations for dynamical parameters (9) and the RWLS equations for cost function parameters (11) generate strongly consistent estimates.

Theorem III.2

Let hypotheses AII-A-AII-A hold, , and let , be the process of estimates obtained by the RWLS equations (9), and be the process of estimates obtained by (12) along the controlled trajectory , generated by the control according to the MF-SAC Law (17). Furthermore, let , be the projected estimates according to Lemma III.1. Then,

-

(i)

the input process given in (17) is well defined,

-

(ii)

, ,

-

(iii)

with the optional assumption AII-B2’, w.p.1 as , .

∎

III-B Asymptotic Convergence of the Population Distribution Parameter Estimates

The MF-SAC Law specifies that the distribution parameter identification is such that each agent observes the control and state trajectories of a random subset of agents , and at each time iteration applies (9) to obtain the dynamical parameter estimates of each agent in its set. The MLE scheme (14) is then applied to these estimated parameters of the agents , for , to obtain an estimate of the distribution parameter. To obtain the strong consistency of the distribution parameter estimates we adopt the hypotheses AIII-B and AIII-B below.

A7: There exists a bounded continuous (on ) family of densities for the family of dynamical and cost function parameter distributions . Further, the distribution function is bounded away from 0 uniformly over , i.e., for some for all and . Moreover, for each , exists for all , and is uniformly bounded on , except possibly on a Lebesgue null set independent of . ∎

For (14), let be the likelihood function of at and let be the continuously differentiable monotonically decreasing function of given by the scaled log-likelihood function

A8: satisfies:

for all , where is the true parameter. ∎

Theorem III.3

The proof is given in Appendix B.

IV The Principal Asymptotic Results

IV-A Asymptotic Behaviour of the MF Equations

The MF Equations (6) that permit the calculation of the mass tracking signal , are dependent on the population distribution parameter . Correspondingly, the MF Equations of the MF-SAC Law on with the strongly consistent distribution parameter estimate , are given below.

Definition IV.1

MF-SAC Equation System on :

| (18) | ||||

∎

Proposition IV.1

For the system (1) let AII-A-AII-A, AIII-B, AIII-B hold. For agent , let: (i) be the solution to (10), be the solution to (14) in the MF-SAC Law; (ii) , be the solution to the MF-SAC Equation System (18); , be the solution to the MF Equation System (6); (iii) be the solution to (16) in the MF-SAC Law; and be the solution to the mass offset function differential equation (4). Then,

-

(i)

w.p.1, ,

-

(ii)

w.p.1, ,

-

(iii)

The input process given in (17) is well defined and is given at and by

∎

The result is proved in Appendix C.

IV-B Asymptotic Behaviour of System Trajectories

We show that under the hypotheses that the self dynamical parameter estimates and the population distribution parameter estimates converge to their true values, the trajectories of adaptive individual agents are stable in the sense. Moreover, these trajectories and the corresponding control actions converge to the non-adaptive values obtained with the true parameters.

Recall that is the set of controls generated by the non-adaptive MF Stochastic Control Law, while is the set of controls generated by the MF-SAC Law.

Using the notation , and , let be the state trajectory of agent , under the control law , and be the state trajectory of agent under the control law , where is the solution to (10), and is the solution to (14).

Proof:

The result is proved in Appendix C.

IV-C Asymptotic Behaviour of Cost Functions

In the population limit, the asymptotic cost of an agent performing the MF-SAC Law in a system within which all of the agents are adaptive is almost surely equal to the cost of an agent in a system of agents all of which are performing the non-adaptive MF-SC Law. This is shown in Proposition IV.4 whose proof is given in Appendix D. Moreover, Proposition IV.5 shows that in the population limit, the best response of an agent in a population of agents performing the MF-SAC Law is almost surely equal to the best response of an agent in a population of agents performing the non-adaptive MF-SC Law. The proof is given in Appendix D.

Proposition IV.4

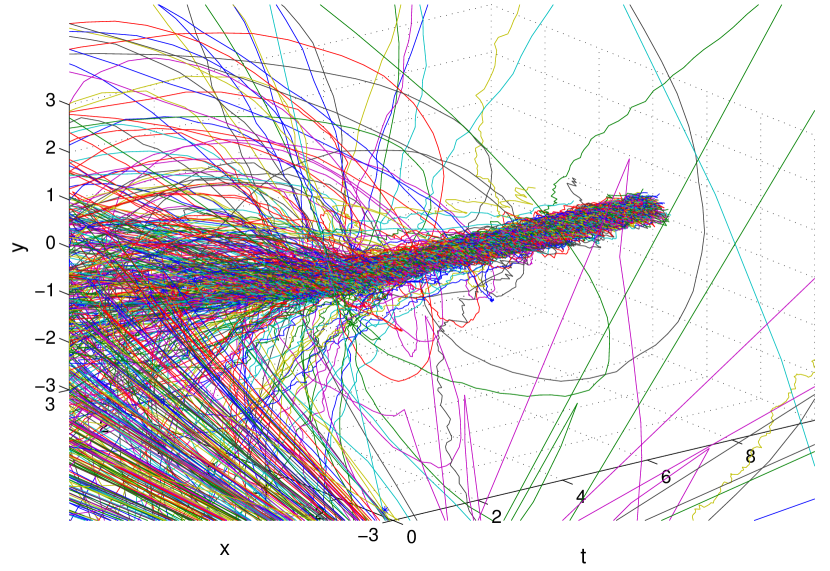

V Simulations

Consider a system of 400 agents where each agent is modeled by a 2 dimensional system. All agents apply the MF-SAC Law; each of 400 agents observes its own 20 randomly chosen agents’ outputs and control inputs, as well as its own trajectory. Rapid convergence of the state trajectories of all agents to the steady state values can be seen Fig. 1 where ‘x’ and ‘y’ represent the two dimensions of each agent’s state and ‘t’ denotes time. In order to plot the convergence of the self identification of dynamical parameters , we plot the norm trajectories of the estimates in Fig. 3. The symbol ‘*’ denotes the true value of the parameter for each agent. Only 10 randomly chosen agents are shown in Fig. 3 for clarity of presentation. In Fig. 3, we depict each agent’s estimate of the mean of the dynamical parameter (i.e., the mean of the random variable ), and we display 10 randomly chosen agents’ estimate trajectories for clarity. Again, the norm of the estimates and the true values are displayed in this diagram. The resulting parameter estimate is different for each agent due to the fact that each agent only observes 20 randomly chosen agents out of a system of 400 agents.

VI Conclusion

This paper presents a study of the mean field stochastic adaptive control problem where the cost functions of the agents in a population are coupled, and each agent estimates its own dynamical parameters based upon observations of its own trajectory, and furthermore estimates the distribution parameter of the population’s dynamical and cost function parameters by observing a randomly chosen fraction of the population. This work makes a contribution to the mean field literature by extending the established -Nash equilibrium results of a large population of egoistic agents to a large population of adaptive egoistic agents. The information requirement for each agent is kept limited in the sense that the distribution parameter is estimated only through an observed set of agents, where the ratio of the cardinality of the observed set to the number of agents in the population becomes negligible as the population size grows to infinity. The strong consistency of the self parameter estimates and the distribution parameter estimates, the stability of the all agent systems, and an -Nash Equilibrium property are all established in the paper.

Future research directions include: (i) investigation of the influence of various rates of observed population fraction decay and rates of convergence on the results in this paper, together with (ii) the extension of adaptive MF theory to (a) the currently developing areas of distance dependent cost function influence among agents [39], (b) altruist and egoist MF theory [40] and (c) problems involving partially observed systems.

Appendix A

Preparatory Lemmas on Asymptotic Dynamics and Dither Inputs

Four basic properties to be used in the sequel are given in the following lemmas.

Lemma A.1

Let be an asymptotically stable random matrix on for all except on a null set , and , be a bounded random matrix function of . If for all and all , there exists such that implies , i.e. w.p.1 as , then is an exponentially stable time varying matrix w.p.1, in the sense that its fundamental matrix satisfies the estimate for , where and .

Proof:

Suppressing mention of , whenever possible for simplicity of notation we consider,

| (21) | ||||

| (22) |

Since is asymptotically stable, we may form the Lyapunov function , where satisfies for some .

Now,

| (23) | ||||

| (24) | ||||

| (25) |

Then writing

| (26) |

we see that for all there exists sufficiently large such that for all ,

| (27) |

Therefore,

| (28) |

which implies where , which gives

| (29) |

Now, for the fundamental matrix, we have

| (30) |

Without loss of generality, take . Then,

| (31) | ||||

| (32) | ||||

| (33) | ||||

| (34) | ||||

| (35) | ||||

| (36) | ||||

| (37) |

∎

Lemma A.2

Let be a random bounded matrix sequence on , which converges almost surely to the asymptotically stable matrix as ; let be defined by , i.e. , and let with . Then the following limit holds:

Proof:

The proof is given in four steps below.

(i) Integral Representation :

For almost all , we have as , restricting attention to the probability 1 subset of on which a unique solution exists. Since

| (38) |

we have

| (39) | ||||

| (40) | ||||

| (41) |

Integrating we obtain,

| (42) |

with the initial condition . Therefore,

| (43) |

and so,

| (44) |

(ii) Convergence of :

Let us split the integrals in (44) as follows:

| (45) |

where the inner integrals are defined by ‘’ for brevity in this definition and is a random instant whose value is to be determined later.

We take the norm inside the integral in ; then by use of the Cauchy Schwarz Inequality (henceforth termed CS) we may bound above as in

| (46) |

where

Next, we may bound above by some for , and we may bound by , for some . Moreover , for all , for some , by the continuity of solutions to (38).

Then,

| (47) |

where and is a bounded continuous function of and . Hence for a fixed , . Therefore tends to 0 as tends to .

(iii) Convergence of

For the second integral in (45), we have

| (48) | ||||

| (49) | ||||

| (50) |

where we split the inner integral and use the notation for brevity.

Using the semi-group property of the state transition matrix, we may write for all . But we have , and we have . Therefore,

| (51) |

Concerning , the random time is chosen so that for (increasing the value over that used in (47) without affecting that argument), . Hence,

| (52) |

From Lemma A.1, satisfies the bound , where . Finally, bounding by yields

| (53) |

For simplicity, in the following we use and ; then,

| (54) | ||||

| (55) | ||||

| (56) |

for a suitable constant independent of , which tends to 0 as .

(iv) Convergence of : Employing the hypothesis w.p.1 as , we shall fix such that

For , applying Lemma A.1 for , we obtain

| (57) | ||||

| (58) | ||||

| (59) |

where is a bounded continuous function. Then, . Therefore .

Since we have established that w.p.1 as , we obtain .

Hence, we have proved that

| (60) |

∎

Lemma A.3

[26, Duncan et al. (1999)] Assume the process is an -valued standard Wiener process that is independent of , and assume the countable set of random processes to be mutually independent and all members of the set have the same probability law on . Then, for all :

∎

The proof is given in [26, Lemma 5].

Lemma A.4

[28, Chen and Guo (1991)] Let be an asymptotically stable matrix, and let . Then

Proof:

Consider the stochastic differential equation

| (61) |

Since is asymptotically stable, there exists a positive definite matrix such that

| (62) |

Following [28], applying the Itô formula to the Lyapunov function ,

| (63) | ||||

| (64) |

Integrating (64) and using the result in Lemma 4 of Christopeit [41] to estimate the third term on the RHS of (63), we obtain

| (65) |

and hence, .

We apply the Itô formula to the outer product ,

| (66) |

Integrating the outer product from yields

| (67) |

A “Lyapunav integral move” yields

| (68) | ||||

We deal with the second term of RHS of (68). Using Christopeit’s [41] estimate again we write,

| (69) | |||

| (70) | |||

| (71) |

As , we take the time average limit of (68) and get

which implies

| (72) |

Thus we obtain the desired result.∎

Appendix B

Proof of Lemma III.1

We drop the subscript for clarity. By definition, when is the solution to RWLS equations (9), satisfies , employing a co-ordinate ordering measurable tie breaking rule, if necessary. Since and , the definition of gives . But by hypothesis, ; therefore, w.p.1 as . ∎

Proof of Theorem III.2

(i) Since the solution , to the algebraic Riccati equation (3) parametrized by is a smooth function of (see [42]), and since , , satisfies w.p.1 for all . It is given that ; therefore, w.p.1 for evaluated along . Hence, given in (17) is well defined.

(ii) The strong consistency of the dynamical parameter estimates is shown in [26] under the controllability and observability of the true parameters (A1 and A2 in [26]) and the uniform controllability and observability of the estimates (Definition 1 in [26]). In our work, the controllability and observability assumptions are satisfied since is controllable and is observable for all by AII-A, and moreover, the uniform controllability and observability of the estimates are satisfied due to Lemma III.1.

(iii) Dropping the subscript for clarity we set the estimation vector and the regression vector as . The persistence of excitation is satisfied since

Setting the measurement vector to be and employing AII-B2’ we get w.p.1 as . Also, as shown in Part (i) w.p.1 as . Each estimated parameter in converges to its true value as . Hence, w.p.1 as .

We observe that instead of the random regularization method used in [25] and [26], we employ here the projection method (Lemma III.1), which guarantees the uniform controllability and observability of the estimates.

∎

Proof of Theorem III.3

Recall that is an independently selected subset of of cardinality , and , is an independently distributed sequence with each having the density , and hence possesses a density in product form. Consequently, the scaled log-likelihood function of at is given by , . Note that the subscript is suppressed for clarity. The maximum likelihood estimate of given is then given by .

Now, it has been established in Theorem III.2 that for each , constitutes a strongly consistent estimate of , i.e., w.p.1. Based upon this, the proof of the theorem consists of an analysis of the convergence (as and hence , and ) of the likelihood function with substituted for and hence of the associated sequence of estimators to .

First we present two lemmas that will be used in the sequel for the proof of Theorem III.3.

Convergence of the Likelihood Functions

Lemma B.2

for all , with equality holding if and only if . ∎

Convergence of the Functions

Now is a compact set, so it is sequentially compact [44], and the sequence has a convergent subsequence for all , for which , in the topology of . Further, we observe that is a -measurable -valued random variable. We will adopt the notation in order to denote the sequence of MLE estimates indexed by the size of the population.

We will show that for any . This, together with Lemma B.2 with set equal to gives . The Identifiability Condition AIII-B gives w.p.1 and we conclude that all subsequential limits of equal w.p.1, and hence w.p.1.

(i) To show : For any , there exists an almost surely finite random integer so that for all such that , the estimate lies in a neighbourhood of for which , for all , by the continuity of on . The uniform continuity of on is shown as follows: pick arbitrary such that lies in a coordinate neighborhood of . We have

Hence for some in the line segment , the Mean Value Theorem yields

| (73) |

But by AIII-B, for all . Then by (73), for each , there exists such that for all , implies . Hence, is uniformly continuous over .

(ii) To show for all for some random : Lemma B.1 assures us that we can pick an almost surely finite random integer so that for all , we have for all , where , as , and where . But, from the continuity of , we have for all , therefore the inequality holds.

(iii) To show : This follows from (14) since we have for all , where , and .

(iv) To show : Again, we employ Lemma B.1: pick an almost surely finite random integer so that for all we have for all , and let as .

Combining (i)-(iv), yields

for all .

Convergence of the Sequence of Estimators

Evaluating the relation above at yields w.p.1. But this expression is independent of , and is arbitrary. So, w.p.1 for all . However, as stated in Lemma B.2, w.p.1 for all , with equality holding if and only if . Therefore, w.p.1, implying w.p.1 by the Identifiability Condition AIII-B, and so all subsequential limits of equal w.p.1, or equivalently w.p.1. ∎

Proof of Lemma B.1

By AIII-B the family of densities exists for the family of dynamical and cost function parameter distributions . Let , where , be the likelihood function of at and let be the continuously differentiable function of , given by the scaled log-likelihood function

, where .

The random sequence ; converges w.p.1 for each [43], where is a compact set by AIII-B. Then, in order for the almost sure convergence of to be uniform over , it is sufficient that the process exists as a sequence of random variables which is w.p.1 bounded uniformly over , where . This may be shown as follows by the Mean Value Theorem:

where lies in an coordinate neighbourhood of and lies on the line segment . Consequently,

where the differentiability of follows from its definition. Let each such , choosing a smaller , possibly depending upon , if necessary. Then take an open cover of the compact set by these neighbourhoods and let be a finite subcover. By AIII-B for each , is bounded uniformly for all . Therefore, . Moreover, by the convergence of the sequences w.p.1 and the boundedness of by uniformly over , we obtain w.p.1 for all , for all for some random . But this shows that satisfies the Cauchy convergence criterion w.p.1 uniformly over P. Therefore w.p.1, as uniformly over , where , and hence as uniformly over . ∎

Appendix C

Proof of Proposition IV.1

1) Proof of w.p.1, :

Recall that , is the solution to the MF Equation System (6), and , is the solution to the MF-SAC Equation System (18). Note that the subscript is suppressed for clarity. A contraction mapping argument together with AII-A-AII-A ensure the existence and uniqueness of (see [2]). AII-A-AII-A also hold for , by Lemma III.1; therefore, the existence and uniqueness properties also hold for for . Since is a continuous function of on , and by Theorem III.3, w.p.1, , where as . Therefore,

2) Proof of w.p.1:

The solution to the differential equation (4) is given by

where , and is generated by the MF equation system (6), and . For the certainty equivalence offset function generated by the MF-SAC Law, we have

where . We adopt the notation and obtain

Adding and subtracting and , and using the triangle inequality we get

(i) Convergence of and : , where , as , and follows from Lemma A.1 and Part 1 of the proof.

(ii) Convergence : From the proof of Lemma A.2,

. Lemma A.1 yields the bound , and for the time invariant case, . For simplicity, set and let be such that . Then for we obtain

| (74) | ||||

where . The term (74) is satisfied for all arbitrarily small for all sufficiently large by use of the bounds , , and . Hence, . By Theorem III.2 as ; therefore, as , . Hence, we obtain w.p.1.

In conclusion we have shown that , and therefore w.p.1. In addition, and . Therefore, w.p.1. Hence, , and .

3) Proof of :

Proof of Theorem IV.3

We recall the following notation and basic assumptions: denotes the true dynamical parameter of agent in that parametrizes the matrices , which are to be estimated by agent , and is the estimated parameter of agent at time . Note that is in the information set of agent , therefore does not need to be estimated. We set , the sample path of the estimated parameter matrices from time to time . The population distribution parameter denoted by , where is the parameter set for , parametrizes . Further, the estimated population distribution parameter of agent is denoted as , and , is the sample path of the estimated distribution parameter from time to . As shown in Theorem III.2, under AII-A-AII-A, on the probability space , converges w.p.1 to as , and by Theorem III.3, under AIII-B and AIII-B, converges w.p.1 to as and . Note that for the optional PCPI, AII-B2’ also needs to be employed. In the sequel, will be used to denote the estimated dynamical parameters whereas denotes the solution to (15). Since the solution , to the algebraic Riccati equation (3) parametrized by , is a smooth function of (see [42]), , satisfies w.p.1 as . To establish the theorem we first observe , is the state of the system subject to the dithered MF Adaptive control law computed from the sum

| (75) |

where the control input due to the MF-SAC Law is given by

The term will be decomposed into four parts, and convergence properties will be established for each term. We have

and

Also, in the sequel for clarity we will suppress the subscript and adopt the notation: , . Displaying the dependence of the fundamental matrix on the parameter estimate trajectory, we use the integral representation and by use of the Cauchy Schwarz Inequality (henceforth termed CS)’s Inequality we obtain

| (76) | |||

| (77) | |||

| (78) | |||

| (79) | |||

We will show one by one that the limit supremums of (76), (78) and (79) are all 0 with probability 1, and the limit supremum of (77) is equal to 0 with probability 1.

-

(i)

Convergence of follows from Lemma A.2.

- (ii)

-

(iii)

Convergence of (78): We have

(80) We use the notation , . Consider the stochastic differential equations

where by AII-A. The difference , satisfies

Alternatively, one can write , giving . Hence we can write (80) as , and use the CS Inequality to obtain

Now , since ; therefore, . Let be such that implies . Then, . Following Lemma A.1 we write for . We also use the CS Inequality, and let as . We get and w.p.1. Therefore w.p.1.

- (iv)

Overall, we have shown that , , and . This implies w.p.1. Consequently, w.p.1, . ∎

Proposition C.1

Proof:

We have the term , which we separate into two parts as , where is a random instant to be determined later. We will only establish w.p.1 here, as w.p.1 is a simpler case of the same argument.

Convergence of

We have

Dropping the subscript , adopting the notation , and using the CS Inequality, we obtain

We set to be the random instant such that implies and . We obtain and from Section C 2.(i), which implies

∎

Appendix D

The following five lemmas will be used to prove Proposition IV.4 and Proposition IV.5. We use the notation , where is defined in AII-A.

Lemma D.1

Proof:

The same result has been shown to hold in [37] (Theorem 4.1) for control action in the form of using the notation defined in (75). We are going to repeat this result here for completeness.

(i) :

| (82) | ||||

| (83) |

Using the CS Inequality, we obtain the inequality:

| (84) | ||||

| (85) | ||||

| (86) | ||||

| (87) |

It is shown in [37] (Theorem 4.1) that uniformly for all .

Using Lemma A.4 we write

| (88) |

We use as shown in Lemma A.1 and get

| (89) |

Therefore,

| (90) |

(ii) : We have the MF Control Law

| (91) | ||||

| (92) |

Also, the mass offset function is

| (93) |

We employ AII-A and obtain , , , and . Then we obtain

| (94) |

Using (90), and the bounds given above, we write

| (95) |

Consequently, we get . As both and are independent of and , we obtain (81).

∎

Lemma D.2

We recall the definition w.p.1, where is the solution to the MF Equation System (6).

Proof:

Using the CS Inequality we write

| (96) | ||||

| (97) | ||||

| (98) |

For we employ AII-A, and LHS of (96) can be further bounded by

| (99) | ||||

| (100) |

Using the CS Inequality we write

| (101) | ||||

| (102) |

We have . For using the CS Inequality again we get

| (103) |

We have shown in Lemma D.1 that . Therefore we get the bound

| (104) |

We have shown that . Now we have shown that . Finally we define and finish the proof:

| (105) |

∎

Lemma D.3

Proof:

From (2) we have the cost function

| (106) |

Adding and subtracting , to the first integrand on the RHS, we get

| (107) | ||||

| (108) | ||||

| (109) | ||||

| (110) |

where,

| (111) |

It is shown in [37, Lemma 6.3] that and where as . Therefore,

| (112) |

Adding and subtracting to , and following the same steps above one obtains

| (113) |

Hence, one gets

| (114) |

∎

Proof:

Let be a feedback control action and be the corresponding closed loop solution. Then, from (2) we have the cost function

| (115) |

Adding and subtracting we get

| (116) | ||||

| (117) | ||||

| (118) | ||||

| (119) | ||||

| (120) | ||||

| (121) | ||||

| (122) |

It is shown in [37, Lemma 6.3] that where as .

For

:

We add and subtract and obtain

| (123) | ||||

| (124) | ||||

| (125) | ||||

| (126) |

It is shown in [37, Lemma 6.4] that and it is shown in [37, Lemma 6.4] that .

As is the optimal tracking solution to tracking signal (5), we obtain

| (127) |

Adding and subtracting to , and following the same steps above one obtains

| (128) |

Proof of Proposition IV.4

The cost function (19) is repeated here:

where and . We expand the term as

In the sequel we adopt the notation , , , , , , and get the inequality

| (130) | ||||

(i) Convergence of : We show in Theorem III.2 that w.p.1 as , , and in Theorem III.3 that w.p.1, as and ; therefore the hypotheses for Theorem IV.3 are satisfied and w.p.1.

(ii) & : equals to the the non-adaptive MF cost function; i.e., w.p.1.

(iv) Convergence of : We have

Applying the CS Inequality we obtain

We prove in Lemma D.2 that w.p.1. It is proved in Theorem III.2 that w.p.1 as and w.p.1 as and . Hence, we get w.p.1. Therefore,

Hence, .

(v) Convergence of : We have the equation

Applying the CS Inequality we obtain

We have shown in Theorem III.2 that w.p.1 as , and as and w.p.1. Hence, we get w.p.1. The convergence of was shown as w.p.1 in Lemma D.5. Therefore,

Hence, .

(vi) Convergence of : We have the equation

Applying the CS Inequality we obtain

Using Lemma D.2, we get w.p.1. The convergence of was shown as

in Lemma D.5. Therefore,

Hence, w.p.1.

(viii) Convergence of : We have the equation

Applying the CS Inequality we obtain

It is shown in Proposition C.1 that w.p.1. We obtain w.p.1 as shown in Lemma D.1. Therefore,

Hence, w.p.1.

Overall we have shown that

Using the same decomposition technique applied in (130) we also show that

Consequently,

∎

Proof of Proposition IV.5

Let be a feedback control action and be the corresponding closed loop solution. LHS of (20) is written as

where . By adding and subtracting

to the integrand, we get

| (131) |

Expanding (131) , we get

| (132) | ||||

We have ; therefore,

| (133) |

w.p.1.

(i) Convergence of : Lemma D.5 states that

(ii) Convergence of : Applying the CS Inequality we obtain,

Using Lemma D.2 we obtain w.p.1 and using Lemma D.5, we get

Therefore,

Hence, .

Proof of Theorem II.2

First, it is evident that Theorem III.2 gives (a), Theorem III.3 gives (b), and Theorem IV.2 gives (c). Second, using a technique similar to that used in [37, Theorem 6.2], it is shown in Proposition IV.4 that

| (135) |

where as . Then, Lemma D.4 gives

| (136) |

where as . Finally, Proposition IV.5 states that

| (137) |

w.p.1, , where as .

References

- [1] M. Huang, P. E. Caines, and R. P. Malhamé, “Individual and mass behaviour in large population stochastic wireless power control problems: centralized and Nash equilibrium solutions,” in 42nd IEEE Conference on Decision and Control, Maui, Hawaii, Dec. 2003, pp. 98–103.

- [2] ——, “Large population cost-coupled LQG problems with non-uniform agents: individual-mass behaviour and decentralized - Nash equilibria,” IEEE Transactions on Automatic Control, vol. 52, no. 9, pp. 1560–1571, Sep. 2007.

- [3] D. Helbing, I. Farkas, and T. Vicsek, “Simulating dynamic features of escape panic,” Nature, vol. 407, pp. 487–490, Sep. 2000.

- [4] H. G. Tanner, A. Jadbabaie, and G. J. Pappas, “Stable flocking of mobile agents, part i: fixed topology,” in 42nd IEEE Conference on Decision and Control, Maui, Hawaii, 2003, pp. 2010–2015.

- [5] Y. Liu and K. M. Passino, “Stable social foraging swarms in a noisy environment,” IEEE Transactions on Automatic Control, vol. 49, pp. 30–44, Jan. 2004.

- [6] D. J. Low, “Following the crowd,” Nature, vol. 407, pp. 465–466, Sep. 2000.

- [7] Y. C. Ho, A. E. Bryson Jr., and S. Baron, “Differential games and optimal pursuit-evasion strategies,” IEEE Transactions on Automatic Control, vol. 10, pp. 385–389, 1965.

- [8] P. P. Varaiya, “The existence of solutions to a differential game,” SIAM J. on Control, vol. 5, pp. 153–162, 1967.

- [9] H. S. Witsenhausen, “Alternatives to the tree model for extensive games,” in The Theory and Applications of Differential Games. The Netherlands: Reidel Publishing Company, 1975, pp. 77–84.

- [10] A. Bensoussan, Perturbation methods in optimal control. New York: Wiley, 1988.

- [11] R. Srikant and T. Basar, “Iterative computation of noncooperative equilibria in nonzero-sum differential games with weakly coupled players,” J. Optimization Theory Appl., vol. 71, no. 1, pp. 137–168, Oct. 1991.

- [12] R. J. Aumann, “Markets with a continuum of traders,” Econometrica, vol. 32, pp. 39–50, 1964.

- [13] B. Jovanovic and R. W. Rosenthal, “Anonymous sequential games,” J. of Math. Economics, vol. 17, pp. 77–87, 1988.

- [14] P. E. Caines, Mean Field Stochastic Control. Bode Lec. at the 48th IEEE Conf. on Decision and Control and 28th Chinese Control Conf., Dec. 2009. [Online]. Available: http://www.cim.mcgill.ca/%7Earman/Shanghai2009/Shanghai2009.zip

- [15] M. Huang, R. P. Malhamé, and P. E. Caines, “Large population stochastic dynamic games: Closed loop McKean-Vlasov systems and the Nash certainty equivalence principle,” Special issue in honour of the 65th birthday of Tyrone Duncan, Communications in Information and Systems, vol. 6, pp. 221–252, Nov. 2006.

- [16] G. Y. Weintraub, C. L. Benkard, and B. V. Roy, “Markov perfect industry dynamics with many firms,” Econometrica, vol. 76, no. 6, pp. 1375–1411, 2008.

- [17] S. Adlakha, R. Johari, G. Weintraub, and A. Goldsmith, “On oblivious equilibrium in large population stochastic games,” in 49th IEEE Conference on Decision and Control, 2010, pp. 3117–3124.

- [18] A. Bodoh-Creed, “Approximation of large games,” 2011, submitted.

- [19] J. M. Lasry and P.-L. Lions, “Mean field games,” Japan J. Math., vol. 2, no. 1, pp. 229–260, 2007.

- [20] H. Tembine, J.-Y. L. Boudec, R. El-Azouzi, and E. Altman, “Mean field asymptotics of Markov decision evolutionary games and teams,” in Int. Conf. on Game Theory for Networks (GameNets 2009), Istanbul, 2009, pp. 140–150.

- [21] G. C. Goodwin, P. J. Ramadge, and P. E. Caines, “Discrete time stochastic adaptive control,” SIAM J. on Control and Optimization, vol. 19, no. 6, pp. 829–853, Nov. 1981, erratum: Vol. 20, No. 6, p. 893, November 1982.

- [22] P. E. Caines and S. Lafortune, “Adaptive control with recursive identification for stochastic linear systems,” IEEE Transactions on Automatic Control, vol. 29, no. 4, pp. 312–321, Apr. 1984.

- [23] P. E. Caines, “Continuous time stochastic adaptive control: non-explosion, -consistency and stability,” Syst. Contr. Lett., vol. 19, pp. 169–176, 1992.

- [24] B. Bercu, “Weighted estimation and tracking for ARMAX models,” SIAM J. on Control and Optimization, vol. 33, pp. 89–106, 1995.

- [25] L. Guo, “Self-convergence of weighted least-squares with applications to stochastic adaptive control,” IEEE Transactions on Automatic Control, vol. 41, pp. 79–89, 1996.

- [26] T. E. Duncan, L. Guo, and B. Pasik-Duncan, “Adaptive continuous-time Linear Quadratic Gaussian control,” IEEE Transactions on Automatic Control, vol. 44, pp. 1653–1662, Sep. 1999.

- [27] H.-F. Chen and L. Guo, “Optimal stochastic adaptive control with quadratic index,” Int. J. of Control, vol. 43, no. 3, pp. 869–881, 1986.

- [28] ——, Identification and Stochastic Adaptive Control. Boston, MA: Birkhäuser, 1991.

- [29] A. J. Gao, “Self-convergence of weighted least squares for continuous-time armax model,” Ulam Quart., vol. 3, no. 2, pp. 25–40, 1996.

- [30] A. J. Gao and B. Pasik-Duncan, “Stochastic linear quadratic adaptive control for continuous-time first-order systems,” Systems and Control Letters, vol. 31, pp. 149–154, 1997.

- [31] A. C. Kizilkale and P. E. Caines, “Stochastic adaptive Nash certainty equivalence control: Self-identification case,” in 19th Intl. Symp. on Math. Theory of Networks and Systems (MTNS 2010), Jul. 2010, pp. 2093–2099.

- [32] ——, “Stochastic adaptive Nash certainty equivalence control: Population parameter distribution estimation,” in 49th IEEE Conference on Decision and Control, Dec. 2010, pp. 6169–6176.

- [33] ——, “Stochastic adaptive Nash certainty equivalence control with population dynamical and cost parameter estimation,” in 19th Latin American Congress of Automatic Control (ACCA 2010) Abstracts, Aug. 2010, p. 35.

- [34] V. Krishna, Auction Theory. Cambridge, UK: Academic Press, 2002.

- [35] A. Marcet and T. Sargent, “Convergence of least squares learning mechanisms in self-referential linear stochastic models,” Journal of Economic Theory, vol. 48, pp. 337–368, 1989.

- [36] P. Maskell and A. Malmberg, “Localised learning and industrial competitiveness,” Cambridge J. of Economics, vol. 23, pp. 167–185, 1999.

- [37] T. Li and J.-F. Zhang, “Asymptotically optimal decentralized control for large population stochastic multiagent systems,” IEEE Transactions on Automatic Control, vol. 53, no. 7, pp. 1643–1660, Aug. 2008.

- [38] A. Bensoussan, Stochastic Control of Partially Observable Systems. U. K.: Cambridge Univ. Press, 1992.

- [39] M. Huang, P. E. Caines, and R. P. Malhamé, “The NCE (mean field) principle with locality dependent cost interactions,” IEEE Transactions on Automatic Control, vol. 55, no. 12, pp. 2799–2805, 2010.

- [40] ——, “Social dynamics in mean field LQG control: Egoistic and altruistic agents,” in 49th IEEE Conference on Decision and Control, 2010, pp. 3140–3145.

- [41] N. Christopeit, “Quasi-least-squares estimation in semi-martingale regression models,” Stochastics, vol. 16, pp. 255–278, 1986.

- [42] D. Delchamps, “Analytic feedback control and the Algebraic Riccati Equation,” IEEE Transactions on Automatic Control, vol. 29, no. 11, pp. 1031–1033, Nov. 1984.

- [43] P. E. Caines, Linear Stochastic Systems. NYC, NY: John Wiley, Apr. 1988.

- [44] J. L. Kelley, General Topology, 3rd ed. New Jersey: Van Nostrand, 1955.