Measuring and Analysing Marginal Systemic Risk Contribution using : A Copula Approach

Abstract

This paper is devoted to the quantification and analysis of the marginal risk contribution of a given single financial institution to the risk of a financial system . Our work expands on the concept proposed by Adrian and Brunnermeier Adrian and Brunnermeier (2011) as a tool for the measurement of marginal systemic risk contribution. We first give a mathematical definition of . Our definition improves the concept by expressing as a function of a state and of a given probability level relative to and respectively. Based on copula theory we connect to the partial derivatives of Copula through their probabilistic interpretation (Conditional Probability). Using this we provide a closed formula for the calculation of for a large class of (marginal) distributions and dependence structures (linear and non-linear). Our formula allows a better analysis of systemic risk using in the sense that it allows us to define depending on the marginal distributions of the losses and of and respectively on the one hand and the copula of and on the other hand. We discuss the implications of this in the context of the quantification and analysis of systemic risk contributions. We will, for example, highlight some of the effects of the marginal distribution of , the dependence parameter , and the condition on .

keywords:

\sep\sepSystemic risk\sepCopula\sepConditional ProbabilityAMS subject classifications: 90A09, 91B30, 91B82, 91G10,91G40, 62H99, 62H20, 62P05.

rmkRemark \newproofpfProof \newproofpotProof of Theorem LABEL:thm2

1 Introduction

With the last crisis it became clear that the failure of certain financial institutions (the so called system relevant financial institutions) can produce an adverse impact on whole financial system. The inability of standard risk-measurement tools like Value-at-Risk () to capture this systemic nature of risk (since their focus is on an institution in isolation: micro risk management) poses a new risk-management challenge to the financial regulators and academics. We can summarise this into two questions:

-

1.

How to identify System-relevant Financial Institutions ?

-

2.

How to quantify the marginal risk contribution of one single financial institute to the system ?

As an academic response to this problems, Adrian and Brunnermeier proposed (Adrian and Brunnermeier (2011)) as a model to analyse the marginal adverse financial effect of a distressed single financial institution on the financial system. They defined the risk measure as the Value at Risk () of the financial system conditional to the state of the loss of a single institution and quantify the institution’s marginal risk contribution (how much an institution adds to the risk of the system) by the measure . This is defined as the difference between conditional to the institution under distress and the conditional to the institution in a normal state.

Thus the implementation of involves variables characterising a single financial institution (e.g. ) and the financial system (e.g. ) respectively and variables characterising the interdependency structure within the financial system and between single financial institutions and the financial system . This macro-dimension of allows the integration of the dependence structure of and in the risk-measurement contrary to the standard risk measures (”micro-risk measure” e.g. VaR) where only variables characterising the financial institution alone are considered. The concept can be thus used by regulatory institutions as a macro-prudential tool (or as a basis for the development of other tools) to identify systemically relevant financial institutions and to set the adequate capital requirements.

But its calculation represents an open problem.

But its computation represents an open problem. Although some approaches have been proposed, Adrian and Brunnermeier (2011) proposed for example an estimation method based on ”linear quantile regression”, Gauthier et al. (2012) adopted a simulation based approach, Jäger-Ambrożewicz (2010) developed a closed formula for the special case that the joint distribution of financial system characteristic variable is of the Gaussian type. In all these approaches there are some difficulties to flexibly model the stochastic behaviors of financial institution’s specific variables and their dependence structure (interconnection) within a financial system, since only linear dependence are considered.

Our aim is thus to provide a more flexible framework for the implementation of the concept which allows the integration of stylised features of marginal losses as skewness, fat tails and interdependence properties like linear, non-linear and positive or negative tail dependence. To do this we first propose an improved definition of which makes it mathematically tractable (see def. 3), and based on copula theory we propose a general analytical formula for (see Theorem 4). We use our formula to make some theoretical analyses and computations related to .

We conclude this article by applying our formula to compute the in the Gaussian copula (Section 5.1), t-copula (Section 5.2), and Gumbel copula setting (Section 5.3.1) respectively. We discuss the results of our computation and draw from this some interesting conclusions. We also give a general formula for in the Archimedian copula setting (Section 5.3).

1.1 Definition of and

We recall here the definition of the value at risk () in order to define the as a conditional following Adrian and Brunnermeier (Adrian and Brunnermeier (2011)).

Definition 1 (Value at Risk).

Given some confidence level the of a portfolio at the confidence level is given by the smallest number such that the probability that the loss exceeds is no larger than . Formally

In order to give a probabilistic interpretation of , we will employ the notation of quantiles as provided in the following definition (cf. McNeil et al. (2005) def. 2.12).

Definition 2 (Generalised inverse and quantile function ).

-

1.

Given some increasing function , the generalised inverse of is defined by .

-

2.

Given some distribution function , the generalised inverse is called the quantile function of . For we have

Note that, if is continuous and strictly increasing, we simply have

| (1) |

where is the (ordinary) inverse of . Thus suppose that the distribution of the loss is continuous and strictly increasing. It follows

| (2) |

We note that typical values taken for are 0.99 or 0.995.

Assumption 1.

Henceforth we consider only random variables which have strictly positive density function. Also in case we consider a bivariate joint distribution we assume that it has a density and its marginal distributions have strictly positive densities.

So due to this assumption all considered distribution functions are continuous and strictly increasing. Such an is thus invertible and denotes the unique inverse of . Let be the loss of the financial institution and the loss of the system without the institution . At least since the financial crisis it is clear that the dependency between the system and the institution must be analysed more seriously. A step towards such an analysis is done by explicitly defining . Adrian and Brunnermeier denote by the value of an institution (or a financial system) conditional on some event depending on the loss of an institution . Thus can be implicitly defined as the of the conditional probability of the system’s loss.

| (3) |

They analysed in their work Adrian and Brunnermeier (2011) the case that the condition refers to the loss of institution being exactly at its value at risk or more generally being exactly at some specific value . We have in this case in the context of (3) the following expression,

| (4) |

Due to assumption 1

However we can define in the context of assumption 1, a conditional probability of the form: for fixed as a function of as follows [cf. Breiman (1992) p. 72) orFeller (1968) p. 71 ].

| (5) |

Where is the marginal density of .

Note that is defined only when ; however, if , then .

{rmk}

Due to assumption 1 we have that,

-

•

the functions is well defined. (since ),

-

•

is strictly increasing and continuous.

As is strictly increasing, it follows that its is invertible. Based on this we provide a alternative definition for which is more tractable from a mathematical point of view than that proposed by Adrian and Brunnermeier.

Definition 3.

Assume that and have density which satisfy assumption 1 .Then for a given and for a fixed , is defined as:

| (6) |

Definition 4 ().

Adrian and Brunnermeier denote by the difference between condition on the institution being under distress and the condition on the institution having mean loss.

| (7) |

is used as measure to quantify the marginal risk contribution of a single institution to the risk of the system.

2 A Brief Introduction to Copulas

In this section we introduce the notion of copula and give some basic definitions and important properties needed later. Our focus is on properties that will be helpful when connecting copulas to conditional probabilities and analyzing and (for detailed analysis of copulas, we refer the reader to e.g. Joe (1997), McNeil et al. (2005), Nelsen (2006) or Roncalli (2009) and the references therein).

2.1 Preliminary

In order to introduce the concept of a copula, we recall some important remarks upon which it is built. {rmk}[cf. McNeil et al. (2005) proposition. 5.2]

-

1.

Quantile transformation. If is standard uniform distributed, then

-

2.

Probability transformation. Assume is a distribution function such that its inverse function is well defined. Let be a random variable with distribution function , then has a uniform standard distribution

2.2 Definition and basic properties of Copula

Definition 5 (2-dimensional copula (cf. Nelsen (2006) def. 2.2.2)).

A 2-dimensional copula is a (distribution) function with the following satisfying:

-

•

Boundary conditions:

-

1)

For every

-

2)

For every

-

1)

-

•

Monotonicity condition:

-

3)

For every we have

-

3)

Conditions (1) and (3) implies that the so defined 2-copula C is a bivariate joint distribution function (cf. Nelsen (2006) def. 2.3.2) and condition (2) implies that the copula C has standard uniform margins. We present now some important basic properties of copulas which we will use below (cf. Nelsen (2006) chap. 2). All this is summarised in the following theorem.

Theorem 1 (cf. Nelsen (2006) Thm. 2.2.7).

Let C be a copula. For any , the partial derivative exists for almost all , and for such and

Similarly, for any , the partial derivative exists for almost all , and for such u and v

Furthermore, the functions and are defined and nondecreasing everywhere on .

The following theorem makes the copula theory attractive as tool for stochastic modeling because it links joint distributions to one-dimensional marginal distributions.

Theorem 2 (Sklar’s theorem, cf. Nelsen (2006) Thm. 2.3.3).

Let be a joint distribution function with marginal distribution functions . Then there exists a copula such that for all

| (8) |

If and have density, then is unique. Conversely, if is a copula and and are distribution functions, then the function defined by (8) is a joint distribution function with margins and .

This theorem is very important because it asserts that, using copula function, it is possible to represent each bivariate distribution function as a function of univariate distribution function. Thus, we can use the copula to extract the dependence structure among the components and of the vector , independently of the marginal distribution and . This allows us to model the dependence structure and marginals separately. {rmk} Assume is a bivariate random variables with copula and joint distribution satisfying assumption 1, with marginals distribution function and . Then the transformed randoms variables and have standard uniform distribution and is the joint distribution of . In fact

3 Computing and Analysing systemic Risk Contribution with : A Copula Approach

In this section we provide a copula based framework for the calculation and the theoretical analysis of as tool for the measurement of systemic risk contribution. To do this we will relate the notion of conditional probability to copulas and rewrite the implicit definition of in terms of copula. Based on this we will derive some useful results. Specifically, we will obtain a closed formula which will provide a general framework for the flexible calculation and analysis of in many stochastic settings. Based on this formula we will highlight some important properties of and .

3.1 Computation of using Copula

We propose here in the following theorem a general framework for computing analytically. Our approach is based on the copula representation of conditional probability.

Theorem 4.

Let and be two random variables representing the loss of the system and institution with marginal distribution functions and respectively. Let be the joint distribution of and with the corresponding bivariate copula , i.e.

Let us assume assumption 1 and

is invertible with respect to the parameter . Then for all at level is given by

| (9) |

Recall that the implicit definition of is given by:

Let and i.e.

Due to assumption 1 it follows from remark 2.1 that and are standard uniform distributed. In this case we can refer to (Breiman (1992) eq. (4.4)) and (Roncalli (2009) p. 263)) and compute the conditional probability , as follows:

Now we are able to derive the explicit expressions of provided that, the function is invertible with respect to the ”non-conditioning” variable . In this case we can write as a function of , as follow

Using and we obtain

Thus

In practice the conditional level for the financial institution is implicitly defined by a given confidence level such that

| (10) |

is specified by the regulatory institution. It represents the probability with which the financial institution remains solvent over a given period of time horizon. Base on this information we can express as follow:

| (11) |

We remark that for a given marginal distribution of the system’s losses the above expression of has only as input parameter and . This motivates the following definition.

Definition 6.

Equation (11) is very important because it asserts that in the practice (or ) contrary to standard risk-measurement tools like Value-at-Risk () does not depend of the marginal distribution but depends only on the marginal distribution of the system’s losses and the copula between the financial institution and the financial system . {rmk} We can see from equation (9) that is nothing other than a quantile of the loss distribution of the system at the level i.e.

| (12) |

Equation (12) asserts that is just a value at risk of the whole financial system at a transformed level . This fact motivates the following corollary, which connects to the value at risk at the level of the financial system (). Recall that under assumption 1 the value at risk of the system at the level of is in this case given by

That is

Corollary 5.

Provided that the function is invertible with respect to the ”non-conditioning” variable , the equivalent confidence level , which makes the Value at Risk of a financial system equivalent to the at level is given by:

| (13) |

Hence, in general, given a condition quantile at the level , we can find the corresponding unconditional quantile by transforming the conditional level to a unconditional level through the transformation function . Based on the fact that can be expressed as a quantile. We can simplify the expression of in a linear function when is assumed to have a univariate normal distribution. In fact if a random variable follows a normal distribution with mean and standard deviation . Then the transformed random variable is standard normal distributed. This motivates the following proposition.

Proposition 1.

If the loss of the financial system is assumed to be normal distributed with mean and standard deviation . Then

| (14) |

with defined as in equation (13). Where denotes the standard normal distribution function.

That means is in this case a linear function with respect to the transformation . {pf} Assume that is normal distributed with mean and standard deviation . Let be the distribution function of then from (12) we have

And using the fact that any arbitrary normal distribution can be transformed to a standard normal distribution we obtain

Corollary 6.

Under the same conditions as the previous proposition, can be compute as follow

| (15) |

Where and are the transformed level defining according to the corollary 5 when institution is under distress and institution having mean loss respectively.

In the following remark we summarise some properties of as monetary measures of risk with particular attention to the concept of coherent risk measures [Artzner et al. (1999) Föllmer and Schied (2004) def. 4.5] . This summaries according to Artzner et al. (1999), properties that a good risk measure should have. {rmk} As can be expressed as quantile of the distribution of the system’s loss with respect to the transformed level . It follows that as a function of has the same properties like value at risk as a function of a level . In particular following properties.

Property 1.

One important advantage of our formula is that, the expression of (see eq. (9)) can be separated into two distinct components.

-

1.

On the one hand the marginal distributions and , which represent the purely univariate features of the single financial institution and the financial system respectively.

-

2.

On the other hand the function , which represents the dependency structure between the single financial institution and the system ).

This separation is very important for the analysis of systemic risk property of our formula. First, because it describes how the systemic contribution of one given financial institution depends on its marginal distributions and the marginal of the financial system . Secondly, because it allows us to appreciate the effect of the copula of the systemic risk contribution.

4 Tail Events and Systemic Crisis

As asserted by Adrian and Brunnermeier (2011), the main idea of Systemic risk measurement is to capture the potential for the spreading of financial distress across institutions by gauging the increase in tail comovement (e.g. The prefix Co in Adrian and Brunnermeier (2011) refers to conditional, contagion, or comovement).

Definition 7.

Forbes and Rigobon (1999) define contagion as a significant increase in cross-market linkages after a shock to one market (or a group of markets).

During the crisis, the contagion effect appears to amplify the concentration of the financial system leading to an increase in probability that single financial institutions fail together with the whole financial system or that a large number of financial institutions fail simultaneously.( see Figure 1).

The argumentation above highlights three important features of systemic risk.

-

1.

Systemic risk involves comovement.

-

2.

Systemic risk concerns a precise region of the involved losses distribution (e.g. the tail by Adrian and Brunnermeier (2011) or the Distress region by Segoviano Basurto and Goodhart (2009) and Hauptmann and Zagst (2011)). Bernard et al. (2012) and Hauptmann and Zagst (2011) have taken this fact into consideration and proposed alternative definitions of and systemic risk measure respectively.

-

3.

Systemic risk involves contagion.

Hence in the context of the analysis and the measurement of systemic risk. The dependence between the financial institution and the financial market have to be considered only in a determined region of their joint distribution. (e.g. in the Tail or in Distress region).

One way to do this would be to use dependence measures which allow the measurement of the dependence only in a defined region(cf. Malevergne and Sornette (2005) chap. 6). For example in the case where the dependence structure is controlled by the correlation coefficient , which is the case for elliptical copulas (e.g. Gaussian and t Copula). The conditional correlation coefficient has to be used instead of the unconditional correlation coefficient.

Definition 8 (cf. Malevergne and Sornette (2005) def. 6.2.1).

Let and be two real random variables and a subset of such that . The conditional correlation coefficient of and conditioned on is given by

Recall that the condition in Adrian and Brunnermeier (2011) refers to the loss being exactly at some specific value (e.g. ) and because of assumption 1 we have that for any . To circumvent this problem we proceed as follows. Instead of considering the set where is assume some fixed value we follows Feller (1968) p. 71 and consider the set where assumes values in an interval . We define

| (16) |

The use of the conditional correlation coefficient instead the unconditional allows the investigation of the effect of the Condition on the systemic risk contribution.

Another tool to measure the dependence of two random variables in one precise given region of their joint distribution is the so called quantile-quantile dependence measure introduced by cf. Coles et al. (1999). This is defined as

So according to the previous argumentation. The quantile-quantile dependence measure of and is per definition a natural indicator of the contagion between financial institutions over a threshold (Note that, the typical value of in our context are 0.99 or 0.995 ). , for example, could mean that there is no contagion between and over the threshold ).

Let us consider a ”lower-version” of the quantile-quantile dependence measure as defined by Roncalli (2009) (cf. Roncalli (2009) Remarque 58).

If we redefine the condition in the implicit definition of (see. eq.(3) and (4)) by replacing ”=” by ”” we have the interesting relation.

The asymptotic consideration of and leads to the following definitions.

Definition 9 (cf. McNeil et al. (2005) def. 5.30).

Let be a bivariate random variable with marginal distribution functions and , respectively. The upper tail dependence coefficient of and is the limit (if it exists) of the conditional probability that is greater than the percentile of given that is greater than the percentile of as approaches , i.e.

If (0, 1] then is said to show

upper tail dependence or extremal dependence in the upper tail; if , they are

asymptotically independent in the upper tail.

Similarly, the lower tail dependence coefficient is the limit (if it exists)

of the conditional probability that is less than or equal to the

percentile of given that is less than or equal to the

percentile of as approaches 0, i.e.

If does not show tail dependence (upper and lower) the extreme events of and appear to occur independently in each margin. This means that they are no-contagion betwenn and .

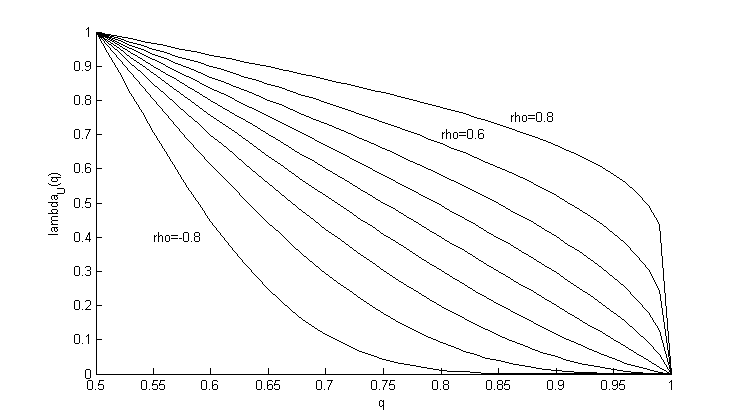

Let us consider the bivariate Gaussian copula as model for . One can show that the bivariate Gaussian copula does not have upper tail dependence when the corresponding correlation coefficient is smaller than one (see 5). As can be seen in Figure 2, regardless of how high a correlation we choose, if we go far enough into the tail, extreme events appear to occur independently in and . That means the Gaussian copula is related to the independence in the tail. Thus Gaussian copula is not a good model for the analysis of systemic risk contribution between and . This is the reason why we connect the concept to copula in order to develop a closed formula for allowing the analysis and the computation of systemic risk contribution for a more general stochastic setting than only the bivariate Gaussian setting as already done in (Jäger-Ambrożewicz (2010)).

5 Applications

In this section we apply the result developed in section 3 to compute and analyse and in some probabilistic settings. We first consider a general case where the joint behavior of and is modeled by a bivariate Gaussian copula. In particular we will analyse here the case where the margins and are assumed to be univariate normal distributed. This special case (Gauss copula and Gaussian margnis) was already considered in Jäger-Ambrożewicz (2010) but in a different approach. Jäger-Ambrożewicz (2010) assumes that the random vector follows a bivariate Gaussian distribution. Then, based on the properties of the conditional bivariate Gaussian distribution (cf. e.g. Feller (1968) eq. 2.6), he develops a closed formula for . This approach imposes thus the univariate normality of both margins ( and ). The method provided in this article is more flexible because it allows each margins independently of other to take a large class of distributions functions (for example we ca assume that is normal distributed and that is -distributed). One other restriction of the formula proposed in Jäger-Ambrożewicz (2010) and also the method presented in Adrian and Brunnermeier (2011) is that, both do not take into account tail events and tail comovements since the Gaussian is asymptotically independent in both tails i.e. . In fact we have (cf. Embrechts et al. (2003) p. 17).

| (17) |

from which it follows that

This presents a big gap since both phenomenons (tail events and tail comovements) are supposed to be the main features of systemic crisis (cf. Viral V. Acharya (2010)). Our formula covers this gap by allowing us to consider other dependence models, especially those which are appropriate for the modeling of the simultaneous (tail) behavior of losses during a financial crisis. So we will also consider the case where the dependence between and is modeled by a -Copula, Gumbel-Copula. At the end of this section we will describe how to develop a closed formula for the computation of for Archimedean copula.

5.1 Computation of in a Gaussian Copula Setting

We assume here that the interdependence structure between and is describe by a bivariate Gaussian copula. The bivariate Gaussian copula is defined as follows (cf. Nelsen (2006) eq. 2.3.6 ):

where denotes the bivariate standard normal distribution with linear correlation coefficient , and the univariate standard normal distribution.

Hence,

Note that can be express as

| (18) |

In fact let a standard Gaussian random vector with correlation . Then we have:

this implies that

where denotes the density of the standard univariate normal distribution. Therefore we have,

The expression of the bivariate Gaussian copula is then

By making the substitution , we obtain

By considering the expression (18) we have:

| (19) |

The function is strictly monotone with respect to .

To compute its inverse, we set and solve for .

If we set in the above equation , we obtain for all (see Figure 3)). This is not a surprise because zero correlation means independence under the normal copula setting. So according to theorem 4 and the development make in section 4 we have the following formula for when the dependence is modeled by a Gaussian copula.

Proposition 2.

Where and represent the univariate distribution function of and respectively.

Let us suppose as a particular case that and are Gaussian, that is and , where and are Gaussian distributions of the losses and with expected values , and standard deviation , (This correspond to the case considered in Jäger-Ambrożewicz (2010)). This h We obtain the following closed analytical expression of in the Gaussian setting (Gaussian Copula and Gaussian Margins)

| (21) |

In fact we have

And we have in this case (cf. Malevergne and Sornette (2005) eq. 6.1)

| (22) |

Note that can be either greater or smaller than since can be either greater or smaller than . This fact have to be considered when analysing the effect of the dependence parameter on . The consideration of highlights also the impact that the change in volatility can have on the systemic risk contribution. This a very important since the behavior of the volatility are not the same depending if we are in distress region or not. In fact one can observe that distress times are characterised by high volatility.

Corollary 7.

Assume that and are Gaussian distributed and centered at zero then.

If then

Let be the value at risk of the single institution at the level i.e. . Then we have the following expression of (see def. 6).

Corollary 8.

In the Gaussian setting, we have

| (23) |

We remark that unlike in equation 21 the expression of does not depend of the loss distribution’s characteristic (e.g. standard deviation and mean ) of the financial institution .

Corollary 9.

In the Gaussian setting. The map

is increasing with respect to its both parameters.

Now we refer to definition 4 to compute . The result of our computation is provided in the following proposition.

Proposition 3.

In the Gaussian setting, is given by

| (24) |

According to definition 4 we have

From equation (24) we observe that if the financial institution and the financial system are not correlated, the risk contribution of to is zero. Let us impose now that, the loss of the financial system alone follows normal univariate distribution. Then according to proposition 1, we have

Additionally if we also assume that is normal distributed. Then we have

In sum we have

and

Similary we can compute as follows. Recall (see corollary 6)

And we have

and

Hence

5.2 t-copula

The Student t copula represents a generalization of the normal copula by allowing for tail-dependence through the degrees of freedom parameter.

Definition 10 (bivariate t distribution).

The distribution function of a bivariate t-distributed random variable with correlation coefficient is given by:

where is the number of degrees of freedom.

The Student t copula can be consider as a generalization of the Gaussian copula. He has in addition to correlation coefficient a second dependence parameter, the degree of freedom , controls the heaviness of the tails. For , the variance does not exist and for , the fourth moment does not exist. The t copula and the the Gaussian copula are close to each other in their central part, and become closer and closer in their tail only when increases. Especially for both copulas are almost identic when freedom parameter.

Definition 11.

The bivariate t copula, is defined as

The tail-dependence coefficients the t Copula is given by (cf. e.g. McNeil et al. (2005) eq. (5.31)) Because of the symmetric property of distribution we have,

From which it follows that,

Provided that . The bivariate copula is thus able to capture the dependence of extreme values.

Following Roncalli (2009)(cf. e.g. Roncalli (2009) p. 299) , we can express the copula as follows:

| (25) |

Now based on theorem 4 we compute the expression of . We obtain

The function is invertible and its inverse is obtained by solving the equation

for . This leads to,

We obtain the following formula for and when the dependence is modeling by a t-copula.

Proposition 4.

and

Where and represent the univariate distribution function of and respectively. denotes the regulatory risk level of the financial institution .

If and are t distributed with degrees of freedom then

| (26) |

and we have in this case (cf. Malevergne and Sornette (2005) eq.6.B.31)

Note that the dependence in the Gaussian and t-copulas setting are essentially determined by the correlation coefficient (elliptical copula). The correlation coefficient is often considered as being a poor tool for describing dependence when the margins are non-normal (cf. McNeil et al. (2005). This motivates the next section.

5.3 Bivariate Archimedean Copulas

We can give in this section a general expression of the for some Archimedean Copulas. Archimedean copulas are often used in practice because of their analytical property, and ability to reproduce a large spectrum of dependence structures. Differently from the elliptical copulas, The definition of a bivariate copula are not derived from a given bivariate distribution. The construction of Archimedean copulas is based on special function (the so called generator). The generator of a Archimedean copula is a convex and strictly decreasing continuous function from to with .

Definition 12 (pseudo-inverse, cf. McNeil et al. (2005) def. 5.41).

define a pseudo-inverse of with domain by

Note that the composition of the pseudo-inverse with the generator gives the identity i.e.

If the generator is said to be strict and it is equivalent to the ordinary functional inverse .

Given a generator we can construct the corresponding Archimedean copula as follows

The lower and upper tail dependence coefficient of an Archimedean copula can be computed using following corollary.

Corollary 10 (Nelsen (2006) co. 5.4.3).

Let Let C be an Archimedean copula with a continuous, strictly, decreasing and convex generator . Then

Proposition 5.

Set and solver for , we obtain the inverse of . Namely:

Based on theorem 4 we derive the following proposition , which gives the expression of for some Archimedean copulas

Proposition 6.

Let Let C be an Archimedean copula with a continuous, strictly, decreasing and convex generator Let and be two random variables representing the loss of the system and institution with joint distribution defined by a bivariate copula with marginal distribution functions and respectively i.e.

If C is an Archimedean copula with a continuous, strictly, decreasing and convex generator , then the explicit (or closed) formula for the at level for a certain fixed value of is given by:

and

We are particular interested here by the archimedean copulas showing positive upper tail dependence(e.g. Gumbel copula).

5.3.1 Gumbel copula

Definition 13.

The bivariate Gumbel Copula function is given by (cf. Nelsen (2006) ex. 4.25)

where represents the strength of dependence. Note that:

-

•

For we have no dependency copula. i.e.

-

•

For we have the perfect dependence i.e. with m and M represented the Fr chet-Hoeffding lower and upper bound respectively.

The generator of the bivariate Gumbel is given by .

The tail dependence coefficient of the Gumbel copula is therefore given by:

and we have

| (27) |

Note that (27) is a strictly increasing with respect to . Its inverse is thus well defined. However its inverse cannot be expressed in an explicit form. Hence we cannot derive analytically, but we can use in this case we can use numerical methods.

5.3.2 Clayton Copula

The generator of the bivariate Clayton copula is given by:

According to proposition 6 we have the following expression for the

6 Conclusion

Managing and regulating the systemic risk is a fundamental problem for financial regulators and risk managers especially in the context of the current crisis. The must important challenge here is the modeling and the quantification of the potential contribution of one given individual financial institution to the financial system. One of the main approaches to solve this problem is the method proposed by Adrian and Brunnermeier in Adrian and Brunnermeier (2011). Where the financial system is defined as a portfolio of two items such that the loss of the system is represented by a random vector where is the loss of the focused financial institution and the loss of the financial system , and the marginal risk contribution of the bank to systemic risk is quantify by the risk measure which is defined as the difference between and (see def. 4 ). The problem of the computation and the analysis of the term for a given is thus very important for the implementation of especially in the non-Gaussian world, but still we do not get any definite solution. As an answer to this problem, we have developed our method, based on copula theory, an analytical framework for the implementation of the methodology where the risk measure is expressed in a closed form in terms of the marginal distributions and separately and the copula between the focused financial institution and the financial system . This framework provides an effective computation and analysis tool for the systemic risk using for a widely used class of distribution function and comovement dynamic(see Theorem 4), which captures not only linear correlation but also nonlinear tail dependencies between the banks in one financial system (which summarise the main features of loss distribution) as opposed to the ”linear quantile regression” and the formula in Jäger-Ambrożewicz (2010) where the dependence is modeled only by the linear correlation coefficient. In fact our approach allows to analyse the marginal effect of , and of the systemic risk. We show for example the systemic risk contribution of is independent of (see (11)) and highlight in remark 6 some properties of according to the nature of . Our approach can also be used to develop closed formulas for the computation of related macro-risk measures like (cf. Adrian and Brunnermeier (2011)), , (cf. Jäger-Ambrożewicz (2010)), and (cf. Jäger-Ambrożewicz (2010)).

Reference

References

- Acharya et al. [2010] V. V. Acharya, L. H. Pedersen, T. Philippon, and M. Richardson. Measuring systemic risk. Working paper, Federal Reserve Bank of Cleveland, 2010.

- Adrian and Brunnermeier [2011] T. Adrian and M. K. Brunnermeier. Covar. Working Paper 17454, National Bureau of Economic Research, October 2011. URL http://www.nber.org/papers/w17454.

- Albrecht [2004] P. Albrecht. Risk measures. Encyclopedia of Actuarial Science, pages 1493–1501, 2004.

- Alexander [2008] C. Alexander. Market Risk Analysis, Practical Financial Econometrics. Wiley Desktop Editions. Wiley, 2008. ISBN 9780470771037. URL http://books.google.de/books?id=D8WXrqfFWt4C.

- Alexander [2009] C. Alexander. Market Risk Analysis, Value at Risk Models. Wiley Desktop Editions. Wiley, 2009. ISBN 9780470745076. URL http://books.google.ca/books?id=j5l82vMfcbQC.

- Artzner et al. [1999] P. Artzner, F. Delbaen, J. M. Eber, and D. Heath. Coherent Measures of Risk. Mathematical Finance, 9(3), 1999. URL http://www.sam.sdu.dk/undervis/92227.E03/artzner.pdf.

- Ash [1972] R. B. Ash. Real analysis and probability [by] Robert B. Ash. Academic Press New York,, 1972. ISBN 0120652013.

- Balakrishnan and Lai [2009] N. Balakrishnan and C. Lai. Continuous Bivariate Distributions. Heidelberger Taschenbücher. Springer, 2009. ISBN 9780387096131. URL http://books.google.de/books?id=bxHmvSziRWwC.

- Bernard et al. [2012] C. Bernard, E. C. Brechmann, and C. Czado. Statistical assessments of systemic risk measures. SSRN eLibrary, 2012. URL http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2056619.

- Billingsley [1995] P. Billingsley. Probability and Measure. Wiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. John Wiley & Sons, 1995. ISBN 9780471007104. URL http://books.google.de/books?id=z39jQgAACAAJ.

- Boyer et al. [1999] B. H. Boyer, B. H. Boyer, M. S. Gibson, M. S. Gibson, M. Loretan, and M. Loretan. Pitfalls in tests for changes in correlations. In Federal Reserve Boars, IFS Discussion Paper No. 597R, page 597, 1999.

- Brahimi and Necir [2012] B. Brahimi and A. Necir. A semiparametric estimation of copula models based on the method of moments. Statistical Methodology, 9(4):467 – 477, 2012. ISSN 1572-3127. 10.1016/j.stamet.2011.11.003. URL http://www.sciencedirect.com/science/article/pii/S1572312711001195.

- Brahimi et al. [2011] B. Brahimi, F. Chebana, and A. Necir. Copula representation of bivariate l-moments : A new estimation method for multiparameter 2-dimentional copula models. 2011. URL http://arxiv.org/abs/1106.2887.

- Breiman [1992] L. Breiman. Probability. Society for Industrial and Applied Mathematics, Philadelphia, PA, USA, 1992. ISBN 0-89871-296-3.

- Brownlees and Engle [2010] C. T. Brownlees and R. F. Engle. Volatility, Correlation and Tails for Systemic Risk Measurement. Social Science Research Network Working Paper Series, May 2010. URL http://ssrn.com/abstract=1611229.

- Cherubini et al. [2004] U. Cherubini, E. Luciano, and W. Vecchiato. Copula Methods in Finance. The Wiley Finance Series. Wiley, 2004. ISBN 9780470863459. URL http://books.google.de/books?id=0dyagVg20XQC.

- Coles et al. [1999] S. Coles, J. Heffernan, and J. Tawn. Dependence measures for extreme value analyses. Etrems, 2(4):339–365, 1999. URL http://www.springerlink.com/content/t63831540647q730/.

- Darsow et al. [1992] W. F. Darsow, B. Nguyen, and E. T. Olsen. Copulas and Markov processes. Illinois J. Math., 36(4):600–642, 1992. ISSN 0019-2082. URL http://projecteuclid.org/getRecord?id=euclid.ijm/1255987328.

- Demarta and McNeil [2005] S. Demarta and A. J. McNeil. The t copula and related copulas. INTERNATIONAL STATISTICAL REVIEW, 73:111–129, 2005.

- Di Nunno and Øksendal [2011] G. Di Nunno and B. Øksendal. Advanced Mathematical Methods for Finance. Springer, 2011. ISBN 9783642184116. URL http://books.google.de/books?id=0xQBTj_R-0sC.

- Embrechts et al. [1999] P. Embrechts, A. McNeil, and D. Straumann. Correlation and dependence in risk management: Properties and pitfalls. In RISK MANAGEMENT: VALUE AT RISK AND BEYOND, pages 176–223. Cambridge University Press, 1999.

- Embrechts et al. [2003] P. Embrechts, F. Lindskog, and A. McNeil. Modelling Dependence with Copulas and Applications to Risk Management. Number 1 in Handbooks in Finance. In book; Handbook of Heavy Tailed Distributions in Finance, Springer chapter 8, 2003.

- Engle [2002] R. Engle. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business and Economic Statistics, 20:339–350, 2002.

- Feller [1968] W. Feller. An Introduction to Probability Theory and Its Applications, volume 1. Wiley, January 1968. ISBN 0471257087. URL http://www.amazon.ca/exec/obidos/redirect?tag=citeulike04-20{&}path=ASIN/0471257087.

- Föllmer and Schied [2004] H. Föllmer and A. Schied. Stochastic Finance: An Introduction in Discrete Time. De Gruyter Studies in Mathematics. De Gruyter, second edition, 2004. ISBN 9783110212075. URL http://books.google.at/books?id=UCebqhuNhw0C.

- Fong et al. [2009] T. Fong, L. Fung, L. Lam, and I.-w. Yu. Measuring the interdependence of banks in hong kong. Working Papers 0919, Hong Kong Monetary Authority, 2009. URL http://EconPapers.repec.org/RePEc:hkg:wpaper:0919.

- Forbes and Rigobon [1999] K. Forbes and R. Rigobon. No contagion, only interdependence: Measuring stock market co-movements. NBER Working Papers 7267, National Bureau of Economic Research, Inc, July 1999. URL http://ideas.repec.org/p/nbr/nberwo/7267.html.

- Gauthier et al. [2012] C. Gauthier, A. Lehar, and M. Souissi. Macroprudential capital requirements and systemic risk. Journal of Financial Intermediation, Jan. 2012. ISSN 10429573. 10.1016/j.jfi.2012.01.005. URL http://dx.doi.org/10.1016/j.jfi.2012.01.005.

- Gordy [2003] M. Gordy. A risk-factor model foundation for ratings-based bank capital rules. Journal of Financial Intermediation, 12(3):199–232, 2003. URL http://EconPapers.repec.org/RePEc:eee:jfinin:v:12:y:2003:i:3:p:199-232.

- Gudendorf and Segers [2009] G. Gudendorf and J. Segers. Extreme-Value copulas. Nov. 2009. URL http://arxiv.org/abs/0911.1015.

- Günther and Jüngel [2010] M. Günther and A. Jüngel. Finanzderivate mit MATLAB: Mathematische Modellierung und numerische Simulation. Vieweg+Teubner Verlag, 2010. ISBN 9783834808790. URL http://books.google.de/books?id=FR1h_j81FqIC.

- Härdle and Simar [2003] W. Härdle and L. Simar. Applied Multivariate Statistical Analysis. Springer, second edition, 2003. ISBN 9783540030799. URL http://books.google.de/books?id=xt31OYzJxnoC.

- Hauptmann and Zagst [2011] J. Hauptmann and R. Zagst. Systemic Risk, volume 1 of Computational Risk Management. In book; Quantitative Financial Risk Management, Springer p. 321-338, 2011. ISBN 9783642193385.

- Hull [2010] J. Hull. Risk Management and Financial Institutions. Wiley Finance. Wiley, second edition, 2010. ISBN 9781118286388. URL http://books.google.de/books?id=MqdrF2R5eTIC.

- Jäger-Ambrożewicz [2010] M. Jäger-Ambrożewicz. Closed form solutions of measures of systemic risk. SSRN eLibrary, 2010. URL http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1675435.

- Joe [1997] H. Joe. Multivariate Models and Multivariate Dependence Concepts. Monographs on Statistics and Applied Probability. Taylor & Francis, 1997. ISBN 9780412073311. URL http://books.google.de/books?id=iJbRZL2QzMAC.

- Klaassen and Van Eeghen [2009] P. Klaassen and I. Van Eeghen. Economic Capital: How It Works and What Every Manager Needs to Know. Elsevier Finance. Elsevier, 2009. ISBN 9780123749017. URL http://books.google.de/books?id=Z5mPNr3rTa4C.

- Kotz and Nadarajah [2004] S. Kotz and S. Nadarajah. Multivariate T-Distributions and Their Applications. Cambridge University Press, 2004. ISBN 9780521826549. URL http://books.google.de/books?id=dmxtU-TxTi4C.

- Lütkebohmert and Gordy [2007] E. Lütkebohmert and M. B. Gordy. Granularity adjustment for basel ii, 2007. URL http://ideas.repec.org/p/zbw/bubdp2/5353.html.

- Malevergne and Sornette [2005] Y. Malevergne and D. Sornette. Extreme Financial Risks: From Dependence to Risk Management. Springer Finance Series. Springer, 2005. ISBN 9783540272649. URL http://books.google.de/books?id=A7Z8rvZ8_JgC.

- Malevergne and Sornette [2006] Y. Malevergne and D. Sornette. Extreme Financial Risks: From Dependence to Risk Management. Springer, Berlin, 2006.

- McNeil et al. [2005] A. McNeil, R. Frey, and P. Embrechts. Quantitative Risk Management: Concepts, Techniques, and Tools. Princeton Series in Finance. Princeton University Press, 2005. ISBN 9780691122557. URL http://books.google.de/books?id=vgy98mM9zQUC.

- Mishkin and Eakins [2012] F. Mishkin and S. Eakins. Financial Markets and Institutions. The Prentice Hall Series in Finance. Pearson/Prentice Hall, seventh edition edition, 2012. ISBN 9780132136839. URL http://books.google.de/books?id=CgiycQAACAAJ.

- Nelsen [2006] R. B. Nelsen. An Introduction to Copulas (Springer Series in Statistics). Springer-Verlag New York, Inc., Secaucus, NJ, USA, 2006. ISBN 0387286594.

- Rachev [2003] S. Rachev. Handbook of Heavy Tailed Distributions in Finance. Handbooks In Finance. Elsevier, 2003. ISBN 9780444508966. URL http://books.google.at/books?id=sv8jGSVFra8C.

- Rohatgi and Saleh [2011] V. Rohatgi and A. Saleh. An Introduction to Probability and Statistics. Wiley Series in Probability and Statistics. John Wiley & Sons, 2011. ISBN 9781118165683. URL http://books.google.de/books?id=IMbVyKoZRh8C.

- Roncalli [2009] T. Roncalli. La Gestion des Risques Financiers. Collection Gestion. Série Politique générale, finance et marketing. Economica, second edition, 2009. ISBN 9782717848915. URL http://books.google.de/books?id=VMzEAQAACAAJ.

- Segoviano Basurto and Goodhart [2009] M. A. Segoviano Basurto and C. A. E. Goodhart. Banking stability measures. IMF Working Papers 09/4, International Monetary Fund, 2009. URL http://EconPapers.repec.org/RePEc:imf:imfwpa:09/4.

- Shiryaev [1995] A. N. Shiryaev. Probability (2nd ed.). Springer-Verlag New York, Inc., Secaucus, NJ, USA, 1995. ISBN 0-387-94549-0.

- Tasche [2000] D. Tasche. Risk contributions and performance measurement. Technical report, Research paper, Zentrum Mathematik (SCA, 2000.

- Viral V. Acharya [2010] C. T. W. I. a. Viral V. Acharya, Richardson M. Manufacturing tail risk a perspective in the financial crisis of 2007-09. Working paper, 2010.

- Wu [2011] D. Wu. Quantitative Financial Risk Management. Computational Risk Management. Springer, 2011. ISBN 9783642193385. URL http://books.google.de/books?id=0B53Myjyd4UC.