Semiparametric Relative-risk Regression for Infectious Disease Data

Abstract

This paper introduces semiparametric relative-risk regression models for infectious disease data based on contact intervals, where the contact interval from person to person is the time between the onset of infectiousness in and infectious contact from to . The hazard of infectious contact from to is , where is an unspecified baseline hazard function, is a relative risk function, is an unknown covariate vector, and is a covariate vector. When who-infects-whom is observed, the Cox partial likelihood is a profile likelihood for maximized over all possible . When who-infects-whom is not observed, we use an EM algorithm to maximize the profile likelihood for integrated over all possible combinations of who-infected-whom. This extends the most important class of regression models in survival analysis to infectious disease epidemiology.

keywords:

[class=AMS]keywords:

t1The author is grateful for the comments of M. Elizabeth Halloran and Ira M. Longini, Jr. The Los Angeles County Department of Public Health generously allowed the use of their data in Section 4. This research was supported by National Institute of Allergy and Infectious Diseases (NIAID) grant K99/R00 AI095302. The content is solely the responsibility of the author and does not necessarily represent the official views of NIAID or the National Institutes of Health.

1 Introduction

Infectious diseases remain an important threat to human health and commerce, and understanding the effects of covariates on infection transmission is crucial to the design of public health interventions. The statistical analysis of infectious disease data is complicated by the fact that the outcomes (infections) are inherently dependent (Becker, 1989; Andersson and Britton, 2000). This problem is especially pronounced for diseases transmitted directly from person to person, such as influenza and SARS. Epidemiologists have dealt with this problem in three ways. Most commonly, they model susceptibility to disease using standard statistical methods, such as logistic or Cox regression, that ignore this dependence. A second approach is to use discrete-time chain binomial models (Rampey et al., 1992) to estimate the probability of escaping infectious contact from infected members of close-contact groups such as households, classrooms, or hospital wards. The third and most recent approach is to model the spread of disease as a branching process where infectees are the offspring of their infectors (Wallinga and Teunis, 2004; White and Pagano, 2008). The time intervals between the infection of an infector and the infection of his or her infectees are called generation intervals. Generation intervals in the branching process are assumed to be independent and identically distributed (iid) samples from a known or estimated distribution.

To understand transmission, it is crucial to separate the effects of covariates on the risk of transmission (i.e., infectiousness and susceptibility) from their association with exposure to infected people (Rhodes, Halloran and Longini, 1996). Chronic-disease models cannot do this, inherently conflating susceptibility and exposure. At the other extreme, generation and serial interval methods model the transmission of disease as a process that creates a population, not a process of spread through a preexisting population. Since infected people are the offspring of an infectious parent, these models ignore competing risks of infection from multiple infectors (Svensson, 2007; Kenah, Lipsitch and Robins, 2008). Since the generation intervals are iid, these models force the implicit assumption of constant latent and infectious periods (Kenah, 2012) and cannot be extended easily to model covariate effects. Discrete-time chain binomial models are a statistically sound response to the problem of dependence, and they separate the effects of covariates on the risk of transmission from their association with exposure to infectious persons. However, their use is limited in two ways: First, they are not implemented in standard statistical software—a problem solved partially by the publicly-available package TranStat (www.epimodels.org/midas/transtat.do). Second, they force the use of discrete time. Since infectious disease data are usually recorded by the day or week, this is not unnatural. However, continuous-time models corrected for ties may offer a more natural and more flexible modeling framework.

Kenah (2011) showed that parametric methods from survival analysis could be extended to analyze infectious disease data by modeling the contact interval. The contact interval in the ordered pair is the time between the onset of infectiousness in and the first infection contact from to , where infectious contact is defined as a contact sufficient to infect a susceptible individual. It is right-censored if the infectious period of ends before makes infectious contact with or if is infected by someone other than . The distribution of provides a concise summary of the evolution of infectiousness over time in person because its hazard function equals the hazard of infectious contact with . These methods solve the problem of dependence by treating pairs of individuals, not the individuals themselves, as the units of analysis. Kenah (2012) showed that the contact interval distribution could be estimated nonparametrically by extending the Nelson-Aalen estimator from standard survival analysis. These methods assume a homogeneous population which the contact interval distribution is the same for all ordered pairs where transmission from to is possible. As such, they are unable to address many important questions in infectious disease epidemiology.

The goal of this paper is to extend the nonparametric estimators in Kenah (2012) to obtain a relative-risk regression model similar to that of Cox (1972) that will allow the semiparametric estimation of the effects of covariates on the hazard of infectious contact. For the ordered pair , the covariate vector can include infectiousness covariates for , susceptibility covariates for , and pairwise covariates.

The rest of Section 1 reviews nonparametric estimation of the contact interval distribution, and Section 2 extends this to relative risk regression models. Our derivations are based on counting processes and martingales. Good introductions to these ideas are given in Kalbfleisch and Prentice (2002) and Aalen, Borgan and Gjessing (2009); Fleming and Harrington (1991) and Andersen et al. (1993) have more detailed discussions. Section 3 explores the performance of the regression models in simulations, and Section 4 uses them to analyze data from Los Angeles County during the 2009 influenza A(H1N1) pandemic. Section 5 discusses the promise and peril of semiparametric relative risk regression in infectious disease epidemiology.

1.1 Stochastic S(E)IR epidemic model

Consider a closed population of individuals assigned indices . Each individual is in one of four states: susceptible (S), exposed (E), infectious (I), or removed (R). Person moves from S to E at his or her infection time , with if is never infected. After infection has a latent period of length , during which he or she is infected but not infectious. At time , moves from E to I, beginning an infectious period of length . At time , moves from I to R. Once in R, can no longer infect others or be infected. The latent period is a nonnegative random variable, the infectious is a strictly positive random variable, and both have finite mean and variance.

An epidemic begins with one or more persons infected from outside the population, which we call imported infections. For simplicity, we assume that epidemics begin with one or more imported infections at time and there are no other imported infections.

After becoming infectious at time , person makes infectious contact with at time , where the infectious contact interval is a strictly positive random variable with if infectious contact never occurs. Since infectious contact must occur while is infectious or never, or . We define infectious contact to be sufficient to cause infection in a susceptible person, so .

For each ordered pair , let if infectious contact from to is possible and otherwise. We assume that the infectious contact interval is generated in the following way: A contact interval is drawn from a distribution with hazard function . If and , then . Otherwise, . In this paper, we assume the contact intervals in all ordered pairs are independent and have finite mean and variance.

Following Wallinga and Teunis (2004), let denote the index of the person who infected person , with for imported infections and for persons not infected at or before time . The transmission network is the directed network with an edge from to for each such that . It can be represented by a vector . Let denote the set of possible infectors of person , which we call the infectious set of person . Let denote the set of all possible consistent with the observed data. A can be generated by choosing a for each non-imported infection .

Our population has size , and we observe the times of all (infection), (onset of infectiousness), and (removal) transitions in the population between time and time . For all ordered pairs such that is infected, we observe .

1.2 Censoring

We assume that we can observe only if is infected by at time . Clearly, can be observed only if . The following processes can right-censor

-

1.

indicates whether remains infectious at infectiousness age . Thus, makes infectious contact with at infectiousness age only if .

-

2.

indicates whether remains susceptible when reaches infectiousness age . Thus, can be infected by at time only if .

-

3.

Assume that infection in person can be observed until time . Then indicates whether infection in can be observed when reaches infectiousness age , so infectious contact from to can be observed at time only if .

Since , , and are left-continuous,

| (1) |

is a left-continuous process that indicates the risk of an observed infectious contact from to when reaches infectiousness age .

The assumptions made in the stochastic S(E)IR model above ensure that and independently censor . The methods in this paper also assume that independently censors . When who-infects-whom is observed, can be any stopping time with respect to the history generated by , , and other processes that independently censor . Our assumptions can be relaxed as long as independent censoring of is preserved (Kenah, 2012). When who-infected-whom is not observed, we require that for all for each non-imported infection .

1.3 Nonparametric survival analysis of epidemic data

Assume there is a hazard function such that for each such that . Let be the corresponding cumulative hazard function. Kenah (2012) extended the Nelson-Aalen estimator to obtain a nonparametric marginal Nelson-Aalen estimator of . This derivation used counting processes and martingales defined in infectiousness age.

For each ordered pair , let indicate whether infectious contact from to occurs by infectiousness age in person , with for all if is never infected. Then is continuous from the right with left-hand limits (cadlag) and , so

| (2) |

is a mean-zero martingale. Since we can observe infectious contact from to only if is susceptible and under observation,

| (3) |

counts observed infectious contacts from to and

| (4) |

is a mean-zero martingale.

1.3.1 Who-infects-whom is observed

The number of contact intervals of length that were observed is

| (5) |

which is decreasing and left-continuous. When who-infects-whom is observed, we can calculate the Nelson-Aalen estimator

| (6) |

where . For all such that , this is an unbiased estimator of because

| (7) |

where is a mean-zero martingale. When the contact interval distribution is continuous, the variance of can be estimated using its optional variation process

| (8) |

1.3.2 Who-infects-whom is not observed

When who-infected-whom is not observed, we cannot calculate the Nelson-Aalen estimate because we do not know which contact intervals are censored and which are observed. Fortunately,

| (9) |

by the law of iterated expectation, so we can estimate by estimating the mean of the possible Nelson-Aalen estimates. When the contact interval distribution is continuous, the probability that was infected by person given the observed history up to time is

| (10) |

Since the infector of each infected can be chosen independently given the observed data (Kenah, Lipsitch and Robins, 2008), the probability of is

| (11) |

Let denote the that we would have calculated had we observed the transmission network . Then

| (12) |

is an unbiased estimate of for all such that . We call this the marginal Nelson-Aalen estimate.

Since the true hazard function is unknown, we cannot use equation (12) directly. Instead, we use it as part of an EM algorithm that starts from an initial guess at the hazard function. Given a hazard function , let

| (13) |

Then the marginal Nelson-Aalen estimate given is

| (14) |

where . We can smooth the increments of to estimate a new hazard function , and so on. Iterating from an initial leads to Algorithm 1, which turns out to be EM algorithm. The limit of the sequence is the marginal Nelson-Aalen estimate (Kenah, 2012).

The variance of can be estimated using the conditional variance formula. Conditioning on the transmission network , we have

| (15) |

where is the Nelson-Aalen estimate from equation (6) and is the variance estimate from equation (38) that we would have calculated had we observed the transmission network . This reduces to (Kenah, 2012)

| (16) |

2 Methods

The methods of Section 1.3 assume a homogeneous population in the sense that is the same for all such that . Now consider a semiparametric relative-risk model like that of Prentice and Self (1983) in which

| (17) |

where is an unspecified baseline hazard function, is a relative risk function, is an unknown coefficient vector, and is a predictable covariate process taking values in a set . We assume that has continuous first and second derivatives, , and is bounded on . Letting gives us a loglinear relative risk regression model like that of Cox (1972), and letting gives us a linear relative risk regression model.

To fit these semiparametric models, we adapt the nonparametric estimators from Kenah (2012) to account for the relative risk function. First, we consider the case where who-infects-whom is observed. Then we describe an EM algorithm to handle the case where who-infects-whom is not observed.

2.1 Who-infects-whom is observed

Let . For a given , the Breslow estimator (Breslow, 1972) of is

| (18) |

where

| (19) |

This estimator has two desirable properties. First, is an unbiased estimator of . For all such that ,

| (20) |

where

| (21) |

is a mean-zero martingale. Second, maximizes the log likelihood

| (22) |

over all step functions . Substituting into , we get the log profile likelihood

| (23) |

where . The first term is similar to the log partial likelihood from Cox (1972) and the second term does not depend on . Dropping the second term, let

| (24) |

be the log partial likelihood for . This derivation of the partial likelihood as a profile likelihood follows that of Johansen (1983). Let denote the value of that maximizes , and let denote the corresponding Breslow estimate of the baseline cumulative hazard.

2.1.1 Partial likelihood score process

We can rewrite as a sum of stochastic integrals:

| (25) |

The corresponding score process is

| (26) |

where

| (27) |

is the expected value of over the risk set at when each pair is weighted by its hazard of transmission at . By the Doob-Meyer decomposition, there is a mean-zero martingale for each such that

| (28) |

Expanding equation (26) using this decomposition and simplifying, we get

| (29) |

Since it is a sum of integrals of predictable processes with respect to martingales, is a mean-zero martingale.

2.1.2 Observed and expected information

Since the do not jump simultaneously in continuous time, the predictable variation process of is

| (30) |

where

| (31) |

is the variance of over the risk set at when each pair is weighted by its hazard of transmission at .

Let be the observed information. Then

| (32) |

where for a column vector ( for scalar ). Expanding via the Doob-Meyer decomposition (28) and simplifying, we get

| (33) |

The second term has expectation zero, so is an unbiased estimate of the variance of .

Another estimate of is obtained by substituting the increments of the Breslow estimator (18) for in equation (30). This gives us the (estimated) expected information

| (34) |

Expanding using the Doob-Meyer decomposition and simplifying, we get

| (35) |

The second term has expectation zero, so is also an unbiased estimate of the variance of . may be a better estimator of than because it is guaranteed to be positive semidefinite (Prentice and Self, 1983) and it depends only on aggregates over risk sets (Aalen, Borgan and Gjessing, 2009).

When as in the Cox model, for all and so

| (36) |

Since

| (37) |

for all and , we have . Therefore, for all . For general , and are asymptotically equivalent under weak regularity conditions (see Appendix A).

2.1.3 Large-sample estimation of and

Appendix A outlines sufficient conditions for the asymptotic normality of and as , where is the number of pairs at risk of transmission. These are the same conditions required for asymptotic normality in standard survival data, except for the requirement that is much larger than the largest number of infectors to which any single susceptible is exposed. Under these conditions, hypothesis tests and confidence intervals for can be obtained using score, Wald, or likelihood ratio statistics.

Given , the Breslow estimator of is . Its variance is consistently estimated by

| (38) |

which is derived in Appendix B.1. can be replaced by . Using the martingale central limit theorem and a log transformation, we get the approximate pointwise confidence limits

| (39) |

Point and interval estimates for the baseline survival function can be obtained using the product integral (Aalen, Borgan and Gjessing, 2009) or using . These estimates are asymptotically equivalent, but the latter is more consistent with the derivation of the partial likelihood as a profile likelihood.

2.2 Who-infects-whom is not observed

If we observe infection but not who-infects-whom, we cannot calculate the partial likelihood or the Breslow estimate because we do not know which contact intervals are observed and which are censored. However, we can use an EM algorithm similar to that of Kenah (2012) to obtain consistent and asymptotically normal estimates of and .

Given a coefficient vector and a baseline hazard function , we can calculate for each (Kenah, Lipsitch and Robins, 2008). If is infected at time , the probability that was infected by given and is

| (40) |

The infectors of different infected persons can be chosen independently, so the probability of a transmission network given , , and the observed data is

| (41) |

Note that these equations assume a continuous contact interval distribution, so simultaneous infectious contacts have probability zero.

Let be the log partial likelihood that we would have calculated had we observed the transmission network . Given a coefficient vector and a baseline hazard function , the expected log likelihood is

| (42) |

where . Now let be the value of that we would have calculated had we observed the transmission network and let the corresponding Breslow estimate be

| (43) |

Then the the marginal Breslow estimate given and is

| (44) |

where .

For the relative risk function , the expected log partial likelihood is the log partial likelihood of a weighted Cox regression model (Therneau and Grambsch, 2000) with two copies of each pair : an uncensored copy with weight and a censored copy with weight . The baseline hazard estimate from this model is the marginal Breslow estimate , where .

2.2.1 EM algorithm

When who-infects-whom is not observed, the semiparametric regression model can be fit using the ECM algorithm of Meng and Rubin (1993), which is an extension of the EM algorithm of Dempster, Laird and Rubin (1977). In each iteration, we first estimate using the expected log partial likelihood and then calculate the marginal Breslow estimator of . We then use these new estimates to re-weight the possible . The entire process is described in Algorithm 2.

To show that this is an ECM algorithm, we must show that the CM1 and CM2 steps are conditional maximizations of the expected log likelihood. Since the CM1 step is a conditional maximization by definition, it remains to show that the CM2 step is a conditional maximization. Given a coefficient vector and a hazard function , the expected log likelihood is

| (45) |

Differentiating with respect to for each and shows that, for a fixed , is maximized over all step functions by setting

| (46) |

exactly as in the marginal Breslow estimator . Therefore, Algorithm 2 is an ECM algorithm. When it is known that , it reduces to Algorithm 1, which shows that convergence of both and should be monitored to ensure convergence of the ECM algorithm.

2.2.2 Large-sample estimation of

Let denote the estimate of to which the ECM algorithm converges, and let denote the corresponding estimate of . Let and denote the score and the observed information that we would have calculated had we observed the transmission network . Using the methods of Louis (1982), the observed information is

| (47) |

where denotes an expectation taken under the assumption that the true coefficient vector is and the true baseline hazard function is . The first term in (47) is

| (48) |

where . This is the observed information matrix from a weighted regression model where each has an uncensored copy with weight and a censored copy with weight . To evaluate the second term in (47), let

| (49) |

be the expected score contribution from individual as a susceptible. Then is

| (50) |

because , each infected person has only one infector in any , and the infectors of different individuals can be chosen independently.

2.2.3 Large-sample estimation of

Let be the marginal Breslow estimate obtained after convergence of the ECM algorithm. Its variance is consistently estimated by

| (51) | ||||

| (52) |

where (see Appendix B.2). Using the martingale central limit theorem and a log transformation, we get the approximate pointwise confidence limits

| (53) |

As before, point and interval estimates for the baseline survival function can be obtained using the product integral (Aalen, Borgan and Gjessing, 2009; Kenah, 2012) or using .

3 Simulations

The performance of the methods from section 2 was tested with a series of network-based epidemic simulations. All epidemics took place on a Watts-Strogatz small-world network (Watts and Strogatz, 1998), which mimics the high clustering and low diameter of real human contact networks. Starting with a ring of nodes, each node was connected to its nearest neighbors and each edge was rewired to a randomly chosen node with probability . A new contact network was built for each simulation.

All epidemic models were written in Python 2.7 (www.python.org) using the packages NetworkX 1.6 (networkx.lanl.gov), NumPy 1.6, and SciPy 0.9 (www.scipy.org). Statistical analysis was done in in R 2.15 (www.r-project.org) via the Rpy2 2.2 package (rpy.sourceforge.net). The code for the models is available as Online Supplementary Information.

3.1 Transmission model

The transmission model had a latent period of zero and an exponential infectious period with mean one. The baseline contact interval distribution was Weibull(, ), where is the shape parameter and is the rate parameter. simulations had a Weibull(, ) distribution, which has . The other had a Weibull(, ) distribution, which has . These distributions gave in a null model.

In the transmission model, each person had an infectiousness covariate and a susceptibility covariate . Each pair connected by an edge had a pairwise covariate . All covariates were independent Bernoulli() random variables. For a connected pair , the hazard of transmission from to at infectiousness age of was

| (54) |

For each parameter , there were simulations where its true value was chosen from a uniform distribution on . Of these, simulations used the Weibull(, ) baseline hazard and used the Weibull(, ) baseline hazard. Of the simulations for each baseline hazard, had the other two set to and had the other two set to .

Each simulated epidemic began with a single person infected at time . Data from the next infections was used to fit two regression models, one using information on who-infected-whom as in Section 2.1 and one using an EM algorithm as in Section 2.2. The EM algorithm used a minimum of and a maximum of iterations. At each iteration, a weighted Cox model was run using the last parameter estimates as the initial parameter estimate. Convergence was defined as a change less than in the expected log likelihood (tighter convergence criteria yielded nearly identical parameter estimates). After convergence, a Cox model was run using the final weights and initial parameters .

After each simulation, we recorded true values, estimates, and confidence intervals for each in the model and baseline hazard estimates and confidence intervals at the , , , , and percentiles of all possible (censored and uncensored) contact intervals. We also recorded the and of the baseline hazard function and the number of EM iterations.

3.2 Results

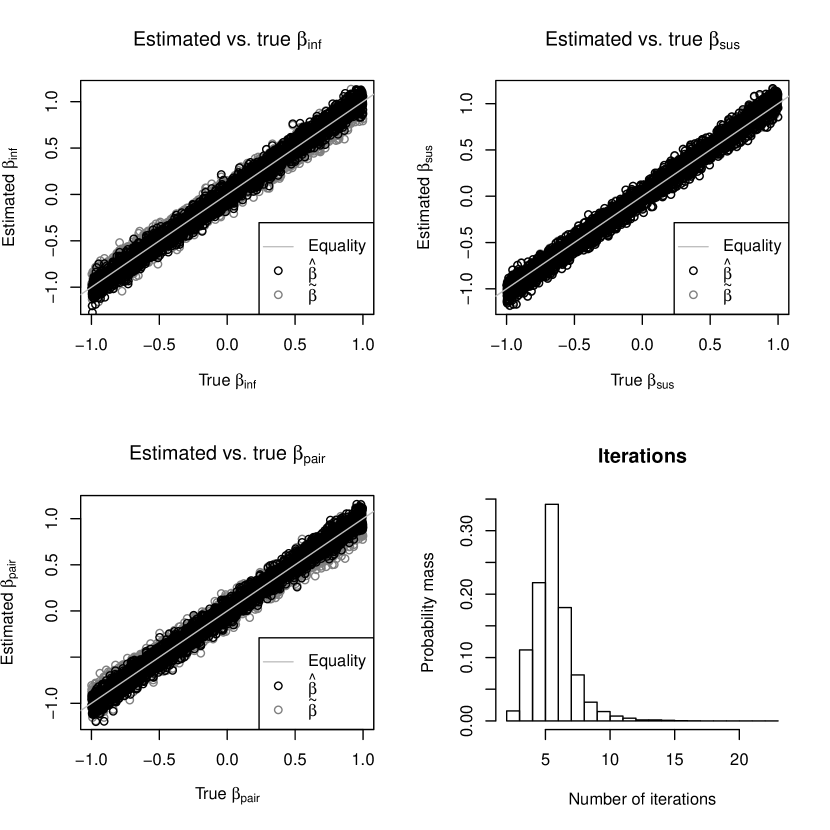

Figure 1 shows good agreement between the estimated and true , , and for both and . Table 1 shows 95% confidence interval coverage probabilities above for all combinations of baseline hazards and parameters. The lower right panel of Figure 1 shows that this was achieved with relatively few iterations. The median number of iterations was , of simulations required iterations, and only out of simulations failed to converge.

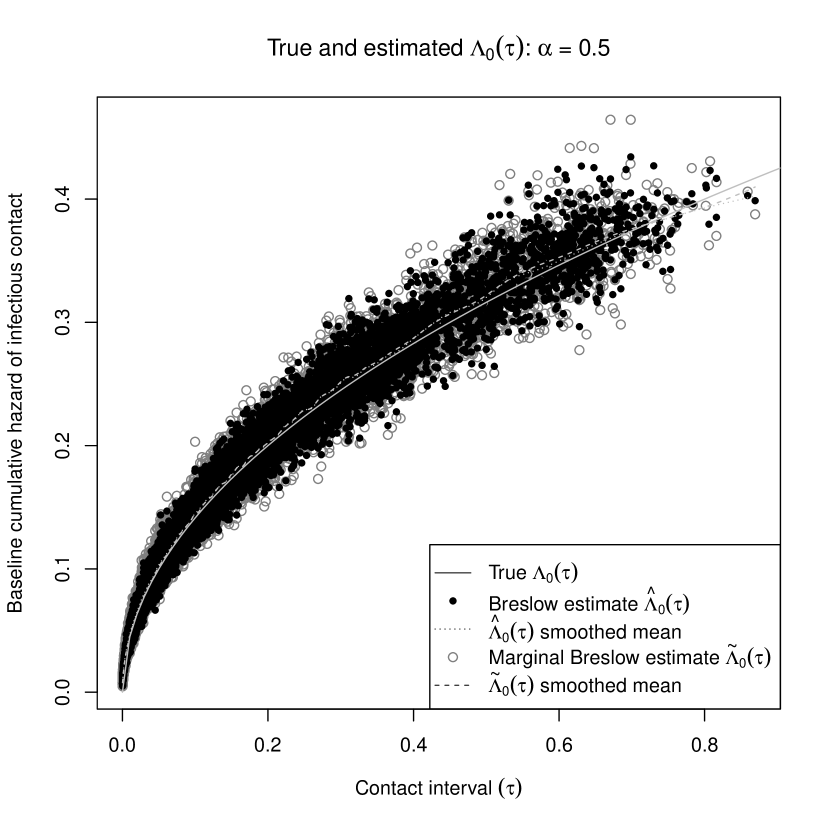

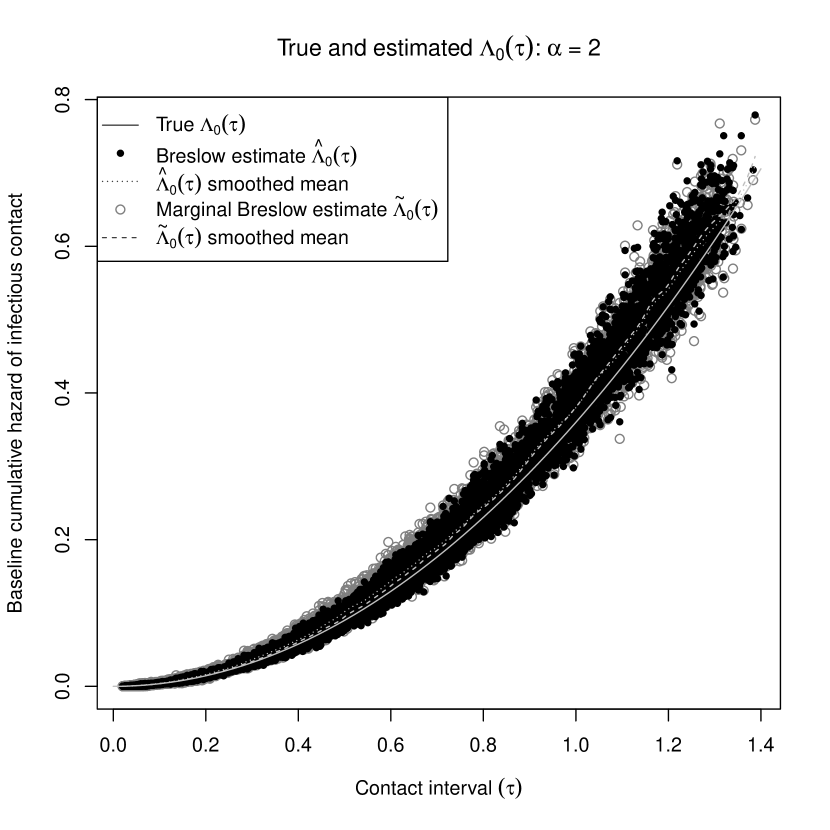

Figures 2 and 3 show good agreement between the estimated and true baseline hazard for both and . The smoothed means show almost no bias in or for and a slight upward bias at high for . Table 2 shows good 95% confidence interval coverage probabilites for the baseline hazard with shape parameter but much poorer coverage probabilities for the baseline hazard with . When , the baseline hazard function is changing fastest at high , where there is the least data. Also, the estimated and its confidence limits were evaluated as step functions; coverage probabilities may have been higher had smoothing or interpolation been used.

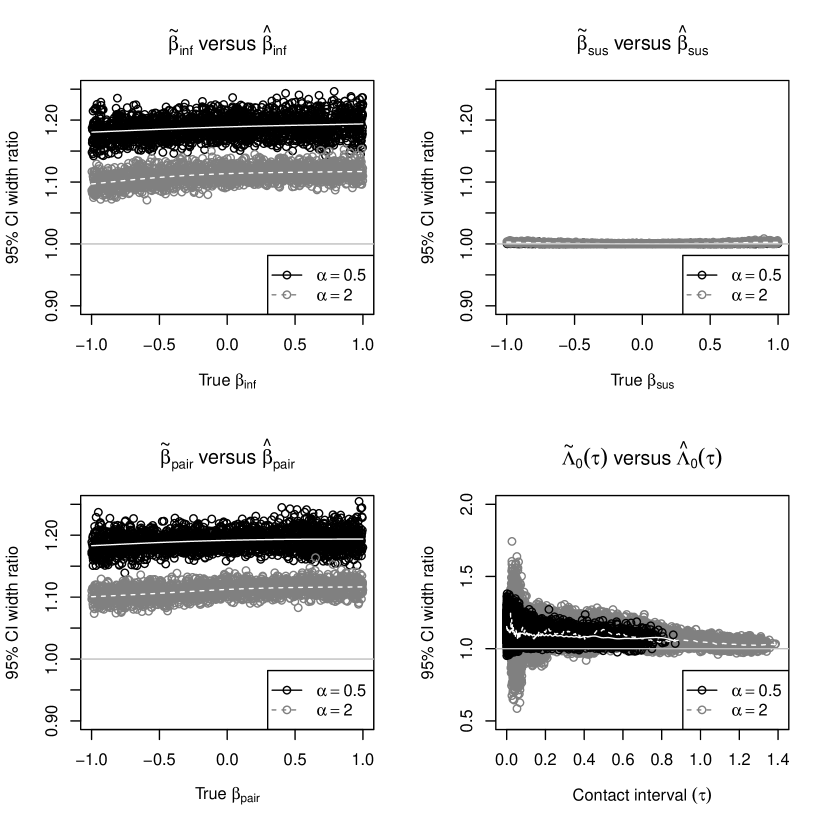

Figure 4 shows the widths of confidence intervals for versus , versus , versus , and versus . Knowledge of who-infects-whom improves the precision of and estimates but not estimates; it slightly improves the precision of estimates. The baseline hazard plays an important role in determining how much precision is gained, with a larger gain for than for . The confidence intervals for , , , and have slightly lower coverage probabilities than those for , , , and (see Tables 1 and 2), so these plots underestimate the true precision gained when who-infects-whom is observed.

Knowledge of who-infected-whom allows point estimates that are closer to the truth and interval estimates with better coverage probabilities. However, it is remarkable how much information can be recovered by the EM algorithm when who-infected-whom is not observed, making the iterative regression model of Section 2.2 a promising tool for infectious disease epidemiology.

4 Data Analysis

To show how the methods of Section 2 can be applied, we will look at the effect of antiviral prophylaxis and age on the transmission of pandemic influenza A(H1N1) in Los Angeles County in 2009. The Los Angeles County Department of Public Health (LACDPH) collected household surveillance data between April 22 and May 19, 2009 according to the following protocol (Sugimoto et al., 2011):

-

1.

Nasopharyngeal swabs and aspirates were taken from individuals who reported to the LACDPH or other health care providers with acute febrile respiratory illness (AFRI), defined as a fever plus cough, core throat, or runny nose. These specimens were tested for influenza, and the age, gender, and symptom onset date of the AFRI patient were recorded.

-

2.

Patients whose specimens tested positive for pandemic influenza A(H1N1) or for influenza A of undetermined subtype were enrolled as index cases. Each of them was given a structured phone interview to collect the following information about his or her household contacts: age, gender, type of contact (household, intimate, in-home daycare, non-home daycare), and high risk status (pregnant, child on long-term aspirin therapy, immunosuppressed, or history of a chronic cardiac, pulmonary, renal, liver, or neurologic condition). The interviewer also recorded whether prophylactic antiviral medication was being taken by the household contacts. They were asked to report the symptom onset date of any AFRI episodes among their household contacts.

-

3.

When necessary, a follow-up interview was given 14 days after the symptom onset date of the index case to assess whether any additional AFRI episodes had occurred in the household, including their illness onset date.

There were 58 households with a total of 299 members. There were 99 infections, of whom 62 were index cases (4 of the 58 households had co-primary cases) and 27 were household contacts with an AFRI. For simplicity, we assume these were all influenza A(H1N1) cases and that all household members were susceptible to infection.

Our natural history assumptions are adapted from Yang et al. (2009) and identical to those in Kenah (2012). In the primary analysis, we assume an incubation period of 2 days, a latent period of 0 days, and an infectious period of 6 days. Under these assumptions, a person with symptom onset at time was infected at time and will stop being infectious at time . Under these assumptions, person can transmit infection on days to . In a sensitivity analysis, we vary the latent period from to days, and the infectious period from to days.

Here, we use the regression model of Section 2.2 to estimate the influenza transmission hazard ratios for age in the infectious and the susceptible and the hazard ratio for antiviral prophylaxis in the susceptible. We then estimate transmission probabilities for different combinations of covariates in infectious/susceptible pairs. The variables in the regression models are: age if the infectious person is years old and otherwise, age if the susceptible is years old and otherwise, and proph if the susceptible is not on antiviral prophylaxis and otherwise. Since antiviral prophylaxis was initiated after the initial case in each household, it was considered only as a susceptibility covariate. All statistical analysis was done in R 2.15 (www.r-project.org).

4.1 Results

There were people aged years and aged years, with no missing age data. There were people taking antiviral prophylaxis and not taking prophylaxis, with missing prophylaxis data for people. When who-infects-whom is not observed, a complete-case analysis requires the removal of all rows corresponding to infectious-susceptible pairs where and any member of is missing data. Otherwise, the remaining members of get too much credit for the infection of .

In the main analysis, there were people infected from outside the household (i.e., no possible infector in the household), with possible infector, with possible infectors, with possible infectors, and with possible infectors, giving us possible transmission trees. The pairwise data contains infectious-susceptible pairs with a total of pair-days at risk of infection. Of these, rows represent possible infection events. All models used the Efron approximation for the partial likelihood with tied failure times.

The top panel of Table 3 shows the results of seven models. All of the models including prophylaxis suggested that antiviral prophylaxis reduced the hazard of transmission by about 60%, with low p-values. Multivariable and stratified models with interaction suggest a stronger effect of antiviral prophylaxis on transmission to and from adults than on transmission to and from children. However, the interaction term coefficients had high p-values and wide confidence intervals (not shown). In all models, adults appeared more infectious and less susceptible than children. However, the coefficients for the main effect of age also had high p-values and wide confidence intervals. The bottom panel of Table 3 shows the results of a sensitivity analysis with the multivariable model without interaction. Varying the latent and infectious periods has relatively little effect on the results of the model.

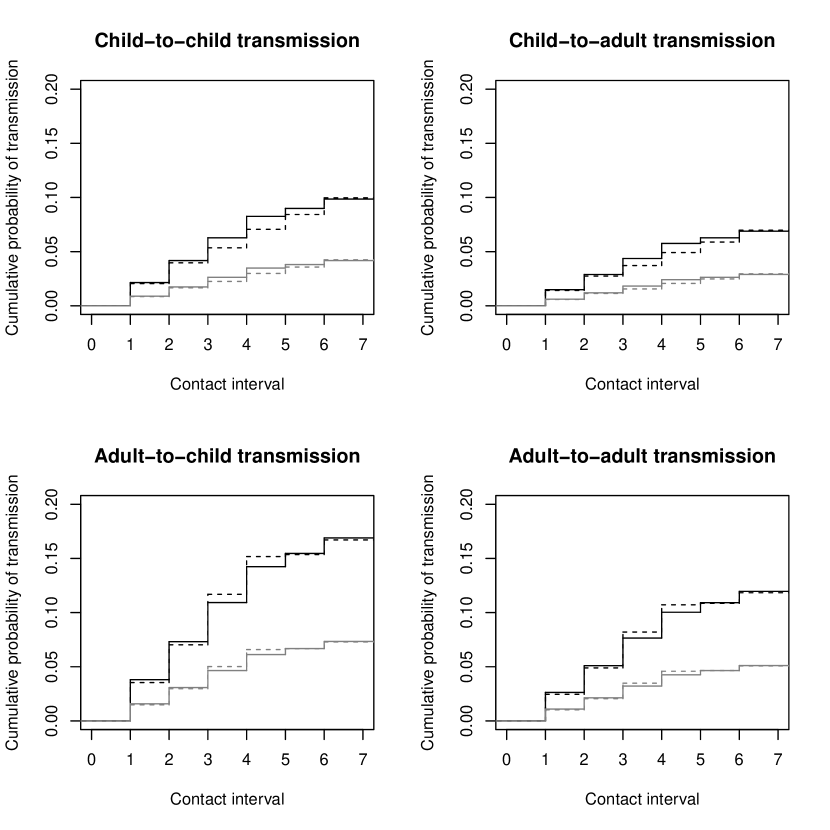

Figure 5 shows estimates of the cumulative transmission probability based on the multivariable and stratified models without interaction. The results of the two models are similar, but the stratified model generally showed slightly lower probabilities of transmission from children and higher probabilities of transmission from adults than the multivariable model. All four panels clearly show the estimtated effect of antiviral prophylaxis. Comparing the top and bottom rows shows that children are estimated to be less infectious than adults. Comparing the left and right columns shows that children are estimated to be more susceptible than adults. All curves show bigger jumps on the first four days after infection than on days and , which is consistent with the results of Kenah (2012).

This data analysis has been intended primarily to illustrate the flexibility of the regression modeling framework for the analysis transmission data. There are several important limitations of the analysis itself. The data set is not large, so there is limited power to estimate the effects of age and antiviral prophylaxis. The age classification is crude, so it may not accurately capture the true effects of age. The prophylaxis variable was missing for many pairs and it was modeled as a binary variable, allowing no consideration of the timing of prophylaxis relative to exposure. Earlier analyses of household transmission of influenza A(H3N2) found greater child-to-child than adult-to-adult transmission (Addy, Longini and Haber, 1991). In our analysis of influenza A(H1N1), we found that children are less infectious and more susceptible than adults. This could be a difference between the H3N2 and H1N1 subtypes of influenza A, or it could be a bias caused the failure to account for infection from outside the household. In either case, this analysis shows the need for two important extensions to the modeling framework: The ability to handle missing data more flexibly and the ability to model infection from outside the household.

5 Discussion

Compared to the discrete-time chain binomial model of Rampey et al. (1992), the regression model framework proposed here has several advantages. It can be fit using standard statistical software in a way that resembles a standard regression model. It offers all of the modeling tools available in a multivariable Cox regression framework, such as stratification and interaction. Standard software can be used to convert the results into curves representing the cumulative probability of transmission in pairs of individuals with specific characteristics. This ease of use will encourage the adoption of these methods in biomedical and public health research.

There are two immediate extensions that will be required before the relative-risk regression models presented here can become truly useful tools in infectious disease epidemiology. First, we must be able to simultaneously model the process of infection from outside the household and transmission within the household. The discrete-time chain binomial model can include a per-time-unit probability of escaping infection from outside the household. In the iterative regression model, this could be achieved by fitting two models in each step of the EM algorithm: a pairwise contact interval model within the household and an individual-level absolute-time model for infection from outside the household. In iteration of the EM algorithm, an individual who got infected would have a probability that he or she was infected from outside the household. The weights of the possible infectors within the household would add up to . At each step, the weights would be recalculated based on covariates, coefficient estimates, the baseline hazard of the contact interval distribution, and the baseline hazard of infection from outside the household. Second, we must be able to handle missing data flexibly but rigorously. Missing data on infection times, latent periods, and infectious periods is the rule, not the exception, in infectious disease epidemiology. For simple missing data (such as the missing data on antiviral prophylaxis in Section 4), the EM algorithm could be extended to calculate the expected log likelihood over the possible values of the missing data as well as who-infected-whom. A more general solution for missing data, especially missing infection and removal times, would be to use a profile sampler (Lee, Kosorok and Fine, 2005) for the model coefficients, treating the baseline hazards as a nuisance parameter.

Other extenions of the theory and methods presented here would make the regression framework presented here more broadly applicable. The SEIR framework is best suited to acute, immunizing diseases that spread directly from person to person. Many foodborne and waterborne diseases, pneumococcal and meningococcal diseases, and other infectious diseases of major public health importance do not fit easily into this framework. The first limitation could be addressed by allowing individuals to experience multiple events (first infection, the second infection, etc.) and allowing individuals to experience different types of events (new carriage, new infection, relapse, etc.). In this paper, we assumed that contact intervals are independent of infectious periods. In some cases, there may be a covariate process such that and are independent given . If not, infectious contact and the infectious period could be modeled as a multivariate survival process. The flexibility of the theory of counting processes and martingales will be valuable in extending the model to more complex diseases.

Finally, there are technical issues that deserve more study. The smoothing step is crucial to the iterative regression model. Here, we used cubic smoothing splines because they were convenient and worked well. However, these do not guarantee that the smoothed hazard function is monotonically increasing and do not have a convenient interpretation in terms of the likelihood. A penalized likelihood estimator that guarantees monotonicity (Anderson and Senthilselvan, 1980) would be more consistent with the theoretical justification of the EM algorithm. A more careful study of the asymptotics of this model would also be useful, especially as the model is extended to more complex applications. Since most infectious disease data is discrete (by day, by week, etc.), a detailed comparison of regression models with correction for ties versus the discrete-time chain-binomial model is important.

Despite these limitations, semiparametric relative-risk regression is a powerful new framework for the analysis of infectious disease data. Its flexibility will allow statistical methods in infectious disease epidemiology to develop in concert with advances in molecular biology. Since all calculations in the EM algorithm are sums over possible combinations of who-infected whom, phylogenetic data can be incorporated directly by restricting the sums to transmission trees compatible with the phylogenetic tree. By placing the analysis of infectious disease data on the theoretical foundation of survival analysis, this approach may help clarify causal inference in infectious disease epidemiology, allowing better design of observational studies and intervention trials. Statistical methods that help improve the response to emerging or re-emerging infections could protect human health and commerce from unknown but possibly tremendous dangers.

References

- Aalen, Borgan and Gjessing (2009) {bbook}[author] \bauthor\bsnmAalen, \bfnmOdd O.\binitsO. O., \bauthor\bsnmBorgan, \bfnmØrnulf\binitsØ. and \bauthor\bsnmGjessing, \bfnmHakon\binitsH. (\byear2009). \btitleSurvival and Event History Analysis: A Process Point of View. \bseriesStatistics for Biology and Health. \bpublisherSpringer-Verlag, \baddressNew York. \endbibitem

- Addy, Longini and Haber (1991) {barticle}[author] \bauthor\bsnmAddy, \bfnmCheryl L.\binitsC. L., \bauthor\bsnmLongini, \bfnmIra M.\binitsI. M. \bsuffixJr and \bauthor\bsnmHaber, \bfnmMichael\binitsM. (\byear1991). \btitleA generalized stochastic model for the analysis of infectious disease final size data. \bjournalBiometrics \bvolume47 \bpages961–974. \endbibitem

- Andersen and Borgan (1985) {barticle}[author] \bauthor\bsnmAndersen, \bfnmPer Kragh\binitsP. K. and \bauthor\bsnmBorgan, \bfnmØrnulf\binitsØ. (\byear1985). \btitleCounting process models for life history data: A review. \bjournalScandinavian Journal of Statistics \bvolume12 \bpages97–158. \endbibitem

- Andersen and Gill (1982) {barticle}[author] \bauthor\bsnmAndersen, \bfnmPer Kragh\binitsP. K. and \bauthor\bsnmGill, \bfnmRichard D.\binitsR. D. (\byear1982). \btitleCox’s regression model for counting processes: A large sample study. \bjournalAnnals of Statistics \bvolume10 \bpages1100–1120. \endbibitem

- Andersen et al. (1993) {bbook}[author] \bauthor\bsnmAndersen, \bfnmPer Kragh\binitsP. K., \bauthor\bsnmBorgan, \bfnmØrnulf\binitsØ., \bauthor\bsnmGill, \bfnmRichard D.\binitsR. D. and \bauthor\bsnmKeiding, \bfnmNiels\binitsN. (\byear1993). \btitleStatistical Models Based on Counting Processes. \bseriesSpringer Series in Statistics. \bpublisherSpringer-Verlag, \baddressNew York. \endbibitem

- Anderson and Senthilselvan (1980) {barticle}[author] \bauthor\bsnmAnderson, \bfnmJ. A.\binitsJ. A. and \bauthor\bsnmSenthilselvan, \bfnmA.\binitsA. (\byear1980). \btitleSmooth estimates for the hazard function. \bjournalJournal of the Royal Statistical Society, Series B \bvolume42 \bpages322-327. \endbibitem

- Andersson and Britton (2000) {bbook}[author] \bauthor\bsnmAndersson, \bfnmHåkan\binitsH. and \bauthor\bsnmBritton, \bfnmTom\binitsT. (\byear2000). \btitleStochastic Epidemic Models and Their Statistical Analysis. \bseriesLecture Notes in Statistics. \bpublisherSpringer, \baddressNew York. \endbibitem

- Becker (1989) {bbook}[author] \bauthor\bsnmBecker, \bfnmNiels G.\binitsN. G. (\byear1989). \btitleAnalysis of Infectious Disease Data. \bseriesMonographs on Statistics and Applied Probability. \bpublisherChapman & Hall/CRC, \baddressBoca Raton, FL. \endbibitem

- Breslow (1972) {barticle}[author] \bauthor\bsnmBreslow, \bfnmN.\binitsN. (\byear1972). \btitleContribution to discussion of paper by D. R. Cox. \bjournalJournal of the Royal Statistical Society B \bvolume34 \bpages216–217. \endbibitem

- Cox (1972) {barticle}[author] \bauthor\bsnmCox, \bfnmDavid R.\binitsD. R. (\byear1972). \btitleRegression models and life-tables. \bjournalJournal of the Royal Statistical Society, Series B \bvolume34 \bpages187–220. \endbibitem

- Cox (1975) {barticle}[author] \bauthor\bsnmCox, \bfnmDavid R.\binitsD. R. (\byear1975). \btitlePartial likelihood. \bjournalBiometrika \bvolume62 \bpages269–276. \endbibitem

- Dempster, Laird and Rubin (1977) {barticle}[author] \bauthor\bsnmDempster, \bfnmA. P.\binitsA. P., \bauthor\bsnmLaird, \bfnmN. M.\binitsN. M. and \bauthor\bsnmRubin, \bfnmD. B.\binitsD. B. (\byear1977). \btitleMaximum likelihood from incomplete data via the EM algorithm. \bjournalJournal of the Royal Statistical Society, Series B \bvolume39 \bpages1–38. \endbibitem

- Fleming and Harrington (1991) {bbook}[author] \bauthor\bsnmFleming, \bfnmThomas R.\binitsT. R. and \bauthor\bsnmHarrington, \bfnmDavid P.\binitsD. P. (\byear1991). \btitleCounting Processes & Survival Analysis. \bseriesWiley Series in Probability and Mathematical Statistics. \bpublisherJohn Wiley & Sons, \baddressNew York. \endbibitem

- Johansen (1983) {barticle}[author] \bauthor\bsnmJohansen, \bfnmS\oren\binitsS. (\byear1983). \btitleAn extension of Cox’s regression model. \bjournalInternational Statistical Review \bvolume51 \bpages165–174. \endbibitem

- Kalbfleisch and Prentice (2002) {bbook}[author] \bauthor\bsnmKalbfleisch, \bfnmJohn D.\binitsJ. D. and \bauthor\bsnmPrentice, \bfnmRoss L.\binitsR. L. (\byear2002). \btitleThe Statistical Analysis of Failure Time Data, \beditionsecond ed. \bseriesWiley Series in Probability and Statistics. \bpublisherJohn Wiley & Sons, \baddressHoboken, NJ. \endbibitem

- Kenah (2011) {barticle}[author] \bauthor\bsnmKenah, \bfnmEben\binitsE. (\byear2011). \btitleContact intervals, survival analysis of epidemic data, and estimation of . \bjournalBiostatistics \bvolume12 \bpages548–566. \endbibitem

- Kenah (2012) {barticle}[author] \bauthor\bsnmKenah, \bfnmEben\binitsE. (\byear2012). \btitleNonparametric survival analysis of epidemic data. \bjournalJournal of the Royal Statistical Society, Series B. \bnoteIn press; preprint at arXiv:1104.4438. \endbibitem

- Kenah, Lipsitch and Robins (2008) {barticle}[author] \bauthor\bsnmKenah, \bfnmEben\binitsE., \bauthor\bsnmLipsitch, \bfnmMarc\binitsM. and \bauthor\bsnmRobins, \bfnmJames M.\binitsJ. M. (\byear2008). \btitleGeneration interval contraction and epidemic data analysis. \bjournalMathematical Biosciences \bvolume213 \bpages71–79. \endbibitem

- Lee, Kosorok and Fine (2005) {barticle}[author] \bauthor\bsnmLee, \bfnmBee Leng\binitsB. L., \bauthor\bsnmKosorok, \bfnmMichael R.\binitsM. R. and \bauthor\bsnmFine, \bfnmJason P.\binitsJ. P. (\byear2005). \btitleThe profile sampler. \bjournalJournal of the American Statistical Association \bvolume100 \bpages960–969. \endbibitem

- Louis (1982) {barticle}[author] \bauthor\bsnmLouis, \bfnmThomas A.\binitsT. A. (\byear1982). \btitleFinding the observed information matrix when using the EM algorithm. \bjournalJournal of the Royal Statistical Society, Series B \bvolume44 \bpages226–233. \endbibitem

- Meng and Rubin (1993) {barticle}[author] \bauthor\bsnmMeng, \bfnmXiao-Li\binitsX.-L. and \bauthor\bsnmRubin, \bfnmDonald\binitsD. (\byear1993). \btitleMaximum likelihood estimation via the ECM algorithm: A general framework. \bjournalBiometrika \bvolume80 \bpages267–278. \endbibitem

- Prentice and Self (1983) {barticle}[author] \bauthor\bsnmPrentice, \bfnmRoss L.\binitsR. L. and \bauthor\bsnmSelf, \bfnmSteven G.\binitsS. G. (\byear1983). \btitleAsymptotic distribution theory for Cox-type regression models with general relative risk form. \bjournalAnnals of Statistics \bvolume11 \bpages804–813. \endbibitem

- Rampey et al. (1992) {barticle}[author] \bauthor\bsnmRampey, \bfnmAlvin H.\binitsA. H. \bsuffixJr, \bauthor\bsnmLongini, \bfnmIra M.\binitsI. M. \bsuffixJr, \bauthor\bsnmHaber, \bfnmMichael\binitsM. and \bauthor\bsnmMonto, \bfnmArnold S.\binitsA. S. (\byear1992). \btitleA discrete-time model for the statistical analysis of infectious disease incidence data. \bjournalBiometrics \bvolume48 \bpages117–128. \endbibitem

- Rhodes, Halloran and Longini (1996) {barticle}[author] \bauthor\bsnmRhodes, \bfnmPhilip H.\binitsP. H., \bauthor\bsnmHalloran, \bfnmM. Elizabeth\binitsM. E. and \bauthor\bsnmLongini, \bfnmIra M.\binitsI. M. \bsuffixJr (\byear1996). \btitleCounting process models for infectious disease data: Distinguishing exposure to infection from susceptibility. \bjournalJournal of the Royal Statistical Society B \bvolume58 \bpages751–762. \endbibitem

- Sugimoto et al. (2011) {barticle}[author] \bauthor\bsnmSugimoto, \bfnmJonathan D.\binitsJ. D., \bauthor\bsnmYang, \bfnmYang\binitsY., \bauthor\bsnmHalloran, \bfnmM. Elizabeth\binitsM. E., \bauthor\bsnmDean, \bfnmBrandon\binitsB., \bauthor\bsnmOiulfstad, \bfnmBrit\binitsB., \bauthor\bsnmBagwell, \bfnmDee Ann\binitsD. A., \bauthor\bsnmMascola, \bfnmLaurene\binitsL., \bauthor\bsnmBancroft, \bfnmElizabeth\binitsE. and \bauthor\bsnmLongini, \bfnmIra M.\binitsI. M. \bsuffixJr (\byear2011). \btitleAccounting for unobserved immunity and asymptomatic infection in the early household transmission of the pandemic influenza A (H1N1) 2009. \bnoteSubmitted to American Journal of Epidemiology. \endbibitem

- Svensson (2007) {barticle}[author] \bauthor\bsnmSvensson, \bfnmÅke\binitsÅ. (\byear2007). \btitleA note on generation times in epidemic models. \bjournalMathematical Biosciences \bvolume208 \bpages300–311. \endbibitem

- Therneau and Grambsch (2000) {bbook}[author] \bauthor\bsnmTherneau, \bfnmTerry M.\binitsT. M. and \bauthor\bsnmGrambsch, \bfnmPatricia M.\binitsP. M. (\byear2000). \btitleModeling Survival Data: Extending the Cox Model. \bseriesStatistics for Biology and Health. \bpublisherSpringer-Verlag, \baddressNew York. \endbibitem

- Tsiatis (1981) {barticle}[author] \bauthor\bsnmTsiatis, \bfnmAnastasios A.\binitsA. A. (\byear1981). \btitleA large-sample study of Cox’s regression model. \bjournalAnnals of Statistics \bvolume9 \bpages93–108. \endbibitem

- Wallinga and Teunis (2004) {barticle}[author] \bauthor\bsnmWallinga, \bfnmJacco\binitsJ. and \bauthor\bsnmTeunis, \bfnmPeter\binitsP. (\byear2004). \btitleDifferent epidemic curves for Severe Acute Respiratory Syndrome reveal similar impacts of control measures. \bjournalAmerican Journal of Epidemiology \bvolume160 \bpages509–516. \endbibitem

- Watts and Strogatz (1998) {barticle}[author] \bauthor\bsnmWatts, \bfnmDuncan J.\binitsD. J. and \bauthor\bsnmStrogatz, \bfnmSteven H.\binitsS. H. (\byear1998). \btitleCollective dynamics of ‘small-world’ networks. \bjournalNature \bvolume393 \bpages440–442. \endbibitem

- White and Pagano (2008) {barticle}[author] \bauthor\bsnmWhite, \bfnmL. Forsberg\binitsL. F. and \bauthor\bsnmPagano, \bfnmMarcello\binitsM. (\byear2008). \btitleA likelihood-based method for real-time estimate of the serial interval and reproductive number of an epidemic. \bjournalStatistics in Medicine \bvolume27 \bpages2999–3016. \endbibitem

- Yang et al. (2009) {barticle}[author] \bauthor\bsnmYang, \bfnmYang\binitsY., \bauthor\bsnmSugimoto, \bfnmJonathan\binitsJ., \bauthor\bsnmHalloran, \bfnmM. Elizabeth\binitsM. E., \bauthor\bsnmBasta, \bfnmNicole E.\binitsN. E., \bauthor\bsnmChao, \bfnmDennis L.\binitsD. L., \bauthor\bsnmMatrajt, \bfnmLaura\binitsL., \bauthor\bsnmPotter, \bfnmGail\binitsG., \bauthor\bsnmKenah, \bfnmEben\binitsE. and \bauthor\bsnmLongini, \bfnmIra M.\binitsI. M. \bsuffixJr (\byear2009). \btitleThe transmissibility and control of pandemic influenza A(H1N1) virus. \bjournalScience \bvolume326 \bpages729–733. \endbibitem

Appendix A Consistency and asymptotic normality

The conditions for the consistency and asymptotic normality of and in the Cox model were given in Andersen and Gill (1982), which used martingales to simplify and generalize the asymptotic results of Cox (1975) and Tsiatis (1981). Conditions for the more general relative risk model were given in Prentice and Self (1983). Here, we outline the most important of these conditions and point out their implications for the use of relative risk regression models in infectious disease epidemiology.

A.1 Regularity conditions

Assume all observations take place at infectiousness ages in for some finite . Let be the number of pairs that were at risk of infectious contact from to while under observation. Let denote the number of individuals that constitute the pairs. Define the following functions (Prentice and Self, 1983):

Note that is real-valued, is vector-valued, and is matrix-valued. Now let

| (55) | ||||

| (56) |

be the values of and , respectively, based on observations of pairs at risk of transmission.

For consistency and asymptotic normality of , we have the following sufficient conditions (Andersen and Gill, 1982; Prentice and Self, 1983):

-

A.

(Finite interval) .

-

B.

(Regression function positivity) There exists a neighborhood of such that is locally bounded away from zero for all and all .

-

C.

(Asymptotic stability) There exists a neighborhood of and functions defined on such that

(57) for . Here, is for real , for vector , and for matrix . Asymptotic properties of the Cox model depend only on convergence of these three functions. For more general relative risk functions, convergence of four additional functions is also required (Prentice and Self, 1983).

-

D.

(Asymptotic regularity) The functions are bounded on and continuous in uniformly in . In addition, is bounded away from zero and has first and second derivatives with respect to on . Finally, let and . Then

(58) is positive definite.

-

E.

(Asymptotic stability of the observed information matrix)

(59) -

F.

(Lindeberg condition)

(60) where the supremum is over all and all such that .

Condition F is automatically fulfilled if the covariates are bounded. In the Cox model, conditions B and E are automatically fulfilled because and for all real . With only slight modification, these conditions also guarantee consistency and asymptotic normality in a stratified relative-risk regression model (Andersen and Borgan, 1985).

For the methods in this paper, the most important constraint is that is bounded away from zero. This has two implications for infectious disease data that have no counterpart in standard survival data. First, the infectious period must be with positive probability. Second, the number of infectors to which the susceptible in a randomly chosen pair at risk of transmission is exposed must have a finite mean as . Let

| (61) |

Now let be the number of infectors to which is exposed if was at risk of transmission and otherwise. If we randomly choose a pair at risk of transmission and look at the number of infectors to which is exposed, its expected value is

| (62) |

For to be bounded away from zero, we must have

| (63) |

If not, the hazard of infection in from a randomly chosen at risk of transmission becomes infinite as . Each susceptible will be infected at a contact interval approaching zero, so the contact interval distribution cannot be estimated. In practice, this means that large-sample distributions are useful when the number of pairs and the number of susceptibles are both large and the largest value of .

There is no similar constraint on the number of susceptibles exposed to each infectious person. In theory, we could have susceptibles exposed to a single infectious person without violating the regularity conditions (as long as his or her infectious period was ). This is because the contact intervals in all pairs for a fixed are assumed to be independent of each other and independent of the infectious period of conditional on the covariate processes .

A.2 Asymptotic properties of , , and

Let denote the score process based on observations of pairs at risk of transmission when who-infects-whom is observed, let denote the corresponding maximum partial likelihood estimate, and let denote the corresponding Breslow estimate of the baseline hazard. Under the conditions of the last section, we have the following results as (Andersen and Gill, 1982; Prentice and Self, 1983):

-

1.

Asymptotic normality of the score: .

-

2.

Consistency of and : and .

-

3.

Consistency of : .

-

4.

Asymptotic normality of : .

-

5.

Consistency of and : and .

-

6.

Convergence of to a mean-zero Gaussian process with independent increments.

-

7.

Asymptotic independence of and .

-

8.

Continuity of : if .

Appendix B Variance of baseline hazard estimates

Andersen and Gill (1982) showed that converges to a mean-zero Gaussian martingale in the Cox model for standard survival data, and this result was extended to more general relative risk functions by Prentice and Self (1983). Under the conditions given in Appendix A, these derivations extend directly to infectious disease data.

B.1 Who-infects-whom is observed

Expanding gives us

| (64) |

where . By a first-order Taylor expansion, the first term in (64) is

| (65) |

for some on the line segment between and . Using the Doob-Meyer decomposition, the second term in (64) can be written

| (66) |

which is a martingale with the optional variation process

| (67) |

The third term in (64) is zero For all such that . Under the regularity conditions of Appendix A, the first and second terms are asymptotically independent, so the asymptotic variance of (64) is

| (68) |

for all such that .

B.2 Who-infects-whom is not observed

By an expansion similar to that in equation (64),

| (69) |

The fourth term in (69) is zero for all at which .

By a first-order Taylor expansion, the first term in (69) equals

| (70) |

for some on the line segment between and , where

| (71) |

Its contribution to the variance is

| (72) |

The second term in (69) can be rewritten

| (73) |

For each , we have if was infected and otherwise. Thus, the term in parentheses is the sum a subset of the random variables , which have sum zero for each . Since the are asymptotically independent for different and , the integral behaves asymptotically like a mean of independent random variables with mean zero and variance . Therefore, the second term of (69) is and converges in probability to zero as .

The third term in (69) can be evaluated using the conditional variance formula. The expression inside the parentheses has the variance

| (74) |

where

| (75) |

Since each infected person has only one infector and infectors can be chosen independently given the observed data,

| (76) |

where . Therefore, the total variance contribution of the third term in (69) reduces to

| (77) |

Since only the first and third terms of (69) are asymptotically nonzero, all that remains is to look at their covariance. Let denote the value of that we would have calculated had we observed the transmission network . Then the corresponding value of the score is

| (78) |

and the corresponding covariance of and is

| (79) |

By the conditional covariance formula,

| (80) |

By an argument similar to that leading to (77), this reduces to

| (81) |

In the limit of large , both terms in (81) act like means of random variables with mean zero and finite variance, so they converge in probability to zero. Since is a function of the expected score, this implies that the first and third terms of equation (69) are asymptotically independent.

Combining all of these results, the asymptotic variance of (69) is

| (82) |

| Parameter: | ||||

| Baseline hazard | ||||

| .958 | .956 | .945 | .940 | |

| .939 | .932 | .938 | .920 | |

| Parameter: | ||||

| Baseline hazard | ||||

| .945 | .943 | .946 | .952 | |

| .918 | .921 | .932 | .932 | |

| Parameter: | ||||

| Baseline hazard | ||||

| .949 | .928 | .952 | .940 | |

| .950 | .941 | .951 | .934 | |

| Baseline hazard | ||||

|---|---|---|---|---|

| Quantile | ||||

| 10% | .944 | .925 | .956 | .846 |

| 25% | .947 | .923 | .942 | .809 |

| 50% | .946 | .924 | .930 | .792 |

| 75% | .945 | .917 | .908 | .793 |

| 90% | .942 | .922 | .887 | .797 |

Covariates Model age age prophy Interaction terms Univariable 1.53 (0.66, 3.54) 0.41 (0.20, 0.85) 0.43 (0.18, 1.02) Multivariable 1.78 (0.69, 4.62) 0.69 (0.29, 1.64) 0.41 (0.17, 0.98) age:age 0.66 () Multivariable 1.59 (0.32, 7.84) 0.63 (0.14, 2.73) 0.04 (0.00, 9.62) age:proph 9.28 () + interaction age:proph 2.72 () Likelihood ratio Stratified strata 0.69 (0.29, 1.64) 0.41 (0.17, 0.99) Stratified strata 0.52 (0.29, 1.64) 0.23 (0.05, 1.16) age:proph 2.37 () + interaction Likelihood ratio Sensitivity analysis (multivariable model without interaction) Latent period day 1.44 (0.64, 3.26) 0.83 (0.36, 1.93) 0.35 (0.15, 0.80) Infectious period days 1.59 (0.60, 4.20) 0.64 (0.27, 1.55) 0.45 (0.18, 1.07) days 1.45 (0.62, 3.40) 0.89 (0.38, 2.04) 0.34 (0.17, 0.87)