Hidden symmetries and equilibrium properties of multiplicative white–noise stochastic processes

Abstract

Multiplicative white-noise stochastic processes continuously attract the attention of a wide area of scientific research. The variety of prescriptions available to define it difficults the development of general tools for its characterization. In this work, we study equilibrium properties of Markovian multiplicative white-noise processes. For this, we define the time reversal transformation for this kind of processes, taking into account that the asymptotic stationary probability distribution depends on the prescription. Representing the stochastic process in a functional Grassman formalism, we avoid the necessity of fixing a particular prescription. In this framework, we analyze equilibrium properties and study hidden symmetries of the process. We show that, using a careful definition of equilibrium distribution and taken into account the appropriate time reversal transformation, usual equilibrium properties are satisfied for any prescription. Finally, we present a detailed deduction of a covariant supersymmetric formulation of a multiplicative Markovian white-noise process and study some of the constraints it imposes on correlation functions using Ward-Takahashi identities.

pacs:

05.40.-a, 02.50.Ey, 05.10.Ggams:

60H40,82B30, 82B31, 82C311 Introduction

From the early studies of Brownian motion, more than a hundred years ago [1], the use of stochastic differential equations to model a wide variety of dynamical systems has grown dramatically. Applications can be found along a wide area of scientific research, from physics and chemistry [2, 3], through biology and ecology [4, 5], to economy and social sciences [6, 7].

In the original formulation of Brownian motion, the influence of the medium on a diffusive particle is modeled by splitting its effect in two parts: a deterministic one, given by an homogeneous viscous force, and a stochastic part, given by a random force with zero expectation value. In this way, fluctuations exhibit as an additive noise and, consequently, the considered model represents an additive stochastic process described by a Langevin equation. However, the viscous force could have non-homogeneous contributions, for instance, in the presence of boundary conditions, such as a diffusion of a Brownian particle near a wall [8, 9]. If the diffusion is not homogeneous, fluctuations could depend on the state of the system and they can be regarded as the product of a random force and a function of the state variable. In that situation, multiplicative noise is defined and the model is known as a multiplicative stochastic process. Another interesting example of multiplicative noise is the stochastic Landau-Lifshitz-Gilbert equation [10], used to describe dynamics of classical magnetic moments of individual magnetic nano-particles. In this case, the noisy fluctuations of the magnetic field couple the magnetic moment in a multiplicative way. The classification of additive or multiplicative noise should be considered in the more general context of external and internal noise [2, 11]. In the former case, dissipation and noise can be considered as two effects with different microscopic origin. In other words, in the absence of noise, the classical deterministic system is perfectly well defined. However, in the latter case, dissipation and fluctuation have the same intrinsic origin and it is not possible to “turn off” one of these effects.

The theory of stochastic evolution provides a beautiful connection between dynamics and statistical physics. In general, Einstein relation or, more generally, fluctuation-dissipation relations associate dynamical properties of the system with thermodynamical equilibrium. However, stochastic dynamics not necessarily model physical systems, where the long time evolution should conduce to thermodynamical equilibrium. In fact, it is possible to have more general stationary state distributions that represent an equilibrium state in the stochastic dynamical sense, not related to thermodynamics. Moreover, stochastic dynamics provide an interesting approach to out-of-equilibrium statistical mechanics [12, 13]. Interestingly, it is possible to attribute thermodynamical concepts like heat, entropy or free energy to each trajectory of an stochastic evolution, given rise to the research field usually called stochastic thermodynamics [14].

In this work, we would like to present a study of equilibrium properties of Markovian multiplicative white-noise processes. A prototype of these processes is represented by the Langevin equation (1). It is well known that, due to the Gaussian white-noise distribution, the continuum limit of the discretized time evolution of multiplicative processes is not unique. In fact, there are different prescriptions to perform this limit. Perhaps, the most popular prescriptions are the Itô [15] and the Stratonovich [16] ones, each one producing a different stochastic evolution and forcing different rules of calculus. We will discuss in detail equilibrium properties in the more general prescription called Generalized Stratonovich convention [17] (also called “-convention” [18] in the field theory literature). In this prescription, a continuum parameter is defined in such a way that each value of the parameter corresponds to a different discretization rule of the stochastic differential equation. The value corresponds with the Itô prescription while is the Stratonovich one.

The concept of equilibrium is tightly related with the concept of time reversal symmetry. For this reason, it is essential to carefully define the time reversal transformation of the stochastic process. In multiplicative white-noise processes, the forward and backward stochastic trajectories evolve with different prescriptions (except when considering Stratonovich convention). For instance, if Itô convention () is defined for the forward evolution, the backward trajectory evolves with the so called Hänggi-Klimontovich [17, 19, 20, 21] prescription (). In general, we will show that the prescription is the time reversal conjugate of . In addition, since the asymptotic stationary probability distribution also depends on the chosen prescription, the correct definition of time reversal transformation, compatible with a unique equilibrium distribution, is quite involved.

It is very useful to use, instead of the Langevin or Fokker-Planck approach, a path integral formalism [22], in which the central object of the theory is a set of stochastic trajectories. Using this formalism, we will analyze equilibrium properties, such as detailed balance relations, microscopic reversibility and entropy production. We will show that, due to a careful definition of equilibrium distribution and taken into account the appropriate time reversal transformation, usual equilibrium properties are satisfied for any value of . Even thought the path integral representation of the stochastic process is suitable for the computation of correlation functions and responses, specific calculations are very cumbersome, since each value of defines different differentiation and integration rules. In particular, the “chain rule” to compute total derivatives of a stochastic process depends on . We make a generalization of the Itô formula for any value of the discretization parameter. In this work, we explicitly show the importance of this “generalized chain rule”, in the path integral formalism.

The stochastic process can also be represented as a path integral in an extended functional space, by introducing auxiliary commutative as well as anti-commutative Grassman variables. The main advantage of this extension for multiplicative noisy systems resides in the prescription independent character of the formulation. While in the original path integral formulation the prescription appears as a continuum limit ambiguity, in the functional Grassman formalism, the ambiguity appears in the definition of equal-time Grassman Green functions [22]. In this way, provided we do not integrate the Grassman variables, we can perform any calculation without specifying a particular prescription. In some sense, all the difficulty introduced by the generalized Itô calculus is being codified in a simpler Grassman algebra.

As a by-product, it is possible to study hidden symmetries of the stochastic process. Indeed, the class of systems we have studied in this paper is invariant under linear transformations in the extended functional space. This hidden symmetry, called supersymmetry (SUSY), was recognized in other stochastic processes several years ago [23, 24, 25]. SUSY properties have been extensively studied for additive stochastic processes [26, 27] and for non-Markovian multiplicative processes [28]. In another hand, for Markovian multiplicative white-noise systems, important progresses have recently been reported [29]. The main difficulty in the SUSY formulation of a Markov multiplicative process is related with the great variety of prescriptions available to define the Wiener integral, which produces several stochastic evolutions with different final steady states. Moreover, time reversal transformations mix different prescriptions.

In this paper, we deduce a covariant supersymmetric formulation of a multiplicative Markov process showing in detail the importance of the prescription dependent equilibrium distribution and the correct definition of time reversal transformation.

Physically, SUSY encodes equilibrium properties of the system. Some of the constraints it imposes on correlation functions (Ward-Takahashi identities) are related to fluctuation-dissipation theorems [30]. This property has acquired a refreshing interest due to the growing importance of stochastic out-of-equilibrium systems [31]. In this sense, it is possible to understand out-of-equilibrium dynamics as a symmetry breaking mechanism. We analyze in detail Ward-Takahashi identities specially related with fluctuation-dissipation theorems. We show that this theorem is fulfilled independently of the chosen prescription to define the process. However, the linear response, fluctuations, as well as the equilibrium distribution, do depend on the specific prescription.

The paper is organized as follows: In Sect. 2 we define our model by means of a Langevin equation with multiplicative noise. In Sect. 3 we carefully study the problem of time reversal symmetry and the equilibrium probability distribution. With these results, we analyze properties such as detailed balance and entropy production in Sect. 4. In Sect. 5, we present a covariant supersymmetric formulation of the stochastic process and we deduce the fluctuation-dissipation theorem for arbitrary prescriptions. Finally, we discuss our conclusions in Sect. 6, leading for A some details of the calculations.

2 Multiplicative white–noise stochastic evolution

The main purpose of this section is to define the model and to establish the concepts and the notation we use in the rest of the paper. For simplicity, we consider a single random variable satisfying a first order differential equation given by

| (1) |

where is a Gaussian white noise,

| (2) |

The drift term and the square root of the diffusion function are, in principle, arbitrary smooth functions of . The only restrictive condition is that should be “invertible”, i. e., .

As it is very well known, to completely define equation (1), it is necessary to give sense to the ill-defined product , since is delta correlated. The problem can be easily understood looking at the integral

| (3) |

where we have defined the Wiener process as . By definition, the Riemann-Stieltjes integral is

| (4) |

where is taken in the interval and the limit is taken in the sense of mean-square limit [3]. For a smooth measure , the limit converges to a unique value, regardless the value of . However, is not smooth, in fact, it is nowhere integrable. In any interval, white noise fluctuates an infinite number of times with infinite variance. Therefore, the value of the integral depends on the prescription for the choice of . There are several prescriptions to define this integral that can be summarized in the so called “generalized Stratonovich prescription” [17] or “-prescription” [18], for which we choose

| (5) |

In this way, corresponds with the pre-point Itô interpretation and coincides with the (mid-point) Stratonovich one. Moreover, the post-point prescription, , is also known as the kinetic or the Hänggi-Klimontovich interpretation [17, 19, 20, 21].

In principle, each particular choice of fixes a different stochastic evolution. In many physical applications, a weakly colored Gaussian-Markov noise with a finite variance [32] is considered. In this case, there is no problem with the interpretation of equation (1) and we can take the limit of infinite variance at the end of the calculations. This regularization procedure is equivalent to the Stratonovich interpretation, [2, 26]. However, in other applications, like chemical Langevin equations [2] or econometric problems [6, 7], the noise can be considered principally white, since it could be a reduction of jump-like or Poisson like processes. In such cases, the Itô interpretation () should be more suitable. Hence, the interpretation of equation (1) depends on the physics behind a particular application. Once the interpretation is fixed, the stochastic dynamics is unambiguously defined. Summarizing, in order to completely define the stochastic process described by equation (1) we need to fix a couple of functions and the parameter .

3 Equilibrium distribution and time reversal

The -prescription introduces some difficulties in the proper definition of time reversal evolution that we describe in this section.

3.1 Fokker-Planck approach

Using equation (1) and the -prescription, it is immediate to obtain [33] a Fokker-Planck equation for the probability distribution :

| (6) |

where . This equation can be cast into a continuity equation,

| (7) |

whith the probability current given by

| (8) |

Then, the probability distribution is given by the solution of the Fokker-Planck equation (6) supplemented with the initial condition and two boundary conditions. We can fix, for instance, the values of at two boundary points , where eventually they can be taken as . However, due to the fact that is normalized to one, for any value of , then .

We suppose that, at long times, the probability rapidly converges to a steady state , given by

| (9) |

with the normalization constant . In this state, the stationary current gets the form

| (10) |

and the stationary Fokker-Planck equation acquires the simpler form

| (11) |

or, simply, .

Thus, for a given value of , we could have a stationary state characterized by the function . The stationary probability density does not represent, in general, an equilibrium state. An equilibrium state is characterized by a net zero stationary current (). When , although the current is already conserved, there is a stationary probability flux, characterizing an out-of-equilibrium regime. In most physical applications, the diffusion function is a polynomially growing function for large . In these cases (and for a single variable), the only possible solution is the equilibrium one . However, for exponentially growing functions, out-of-equilibrium steady state solutions are possible.

Let us focus on the equilibrium state, defined as the solution of the stationary Fokker-Planck equation with zero current probability. Thus, for , there is an obvious solution of equations (10) and (11), given by

| (12) |

Therefore, given the functions and , supplemented by a value of , the probability density tends at long times to the equilibrium distribution

| (13) |

where is given by equation (12), provided is integrable to define the normalization constant .

In the case that equation (1) models a conservative physical system, i. e. , if the otherwise deterministic system is characterized by an energy potential , the drift function does not depend explicitly on time and is given by

| (14) |

This equation relates fluctuations (given by ) with dissipation, therefore it can be considered as a local generalization of Einstein relation for Brownian motion. Using this expression, the equilibrium “potential” has the form:

| (15) |

As expected, the equilibrium distribution depends, not only on the given functions or, alternatively, on , but also on the value of the -prescription which defines the Wiener integral. If equation (1) is used to model a physical system, which is expected to asymptotically converge to thermodynamic equilibrium (), the only possible choice is the Hänggi-Klimontovich interpretation ; for this reason, the election of is sometimes called “thermal prescription”. Recently, an experimental evaluation of was reported [34, 35] in the study of a falling colloidal particle near a wall. In this work, the value of was recognized as the proper one to make the correctly identification of the microscopic forces acting on the colloidal particle. With any other choice, the equilibrium potential , including the usual Itô () and Stratonovich () prescriptions.

Except for the Stratonovich prescription , each value of is associated with different calculus rules. For this reason, in most physical literature, Stratonovich prescription is preferred, because it enables “normal” rules of derivation and integration. Despite the Hänggi-Klimontovich convention being the only one which guarantees the convergence to the termodynamic equilibrium, calculations can be particularly cumbersome in this interpretation. However, if we prefer to work in any other different fixed prescription, and we insist in modeling a physical system which converges to Boltzmann’s equilibrium, we need to modify equation (1). It is done by adding a “spurious drift force” [33] which cancels the last term of equation (15). That is, if we define a new -dependent “potential” , then, the equilibrium distribution , for any value of .

In this work, we will not adopt this point of view. We will consider a stochastic process completely defined by fixing in eq. (1). Thus, the probability distribution flows, at long times, to an -dependent equilibrium distribution given by equation (12) or alternatively equation (15) . In this way, we are able to study, in a unique formalism, model systems with general equilibrium distributions that go from Boltzmann thermal equilibrium to power-law distributions. A simple example of the latter case is to consider a pure noisy system with . In that case, the equilibrium distribution is .

We will show that this set of distributions, characterized by asymptotically zero current probability, is consistent with all the usual properties of equilibrium evolution, like, for instance, detailed balance and entropy production.

3.2 Time reversal

Consider, for instance, the Langevin equation (1), in the simplest case of . Naively, we could compute the backward evolution of the stochastic variable by just changing the sign on the velocity , in such a way that, for a given noise configuration, the particle turns back on its own feet. However, the situation is not so simple. Let us look more closely. Consider a time interval . The forward evolution is obtained by integrating equation (1) between the initial and final times and respectively,

| (16) |

while the backward evolution is simply obtained by changing the initial and final integration limits,

| (17) |

where we use the notation , just to differentiate backward from forward evolution. If the integrals were “normal” integrals, we could use the trivial property . In that case, there would be no need to differentiate backward and forward variables, since equations (16) and (17) would be the same equation and . However, the integrals are Wiener integrals and need to be carefully defined. As we saw in the last section,

| (18) |

with

| (19) |

The time reversal integral is obtained by changing in equation (18). The important point is that also depends on . Then,

| (20) |

with

| (21) |

where was obtained from equation (19), by replacing or, equivalently, . Therefore, the time reversed stochastic evolution is characterized by the transformations

| (22) |

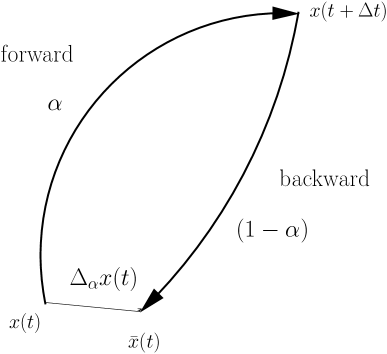

In this sense, we say that the prescription is the time reversal conjugate (TRC) of . Then, the post-point Hänggi-Klimontovich interpretation is the TRC of the pre-point Itô one, and vice versa. The only time reversal invariant prescription is the Stratonovich one, . This means that, except for the Stratonovich case, the backward and forward stochastic paths do not have the same end points. This is illustrated in figure (1), where we compute a “time-loop” evolution. Consider we want to compute the evolution of the system starting at , going forward a time interval and, then, turning back in time the same interval .

The forward path in figure (1) can be computed from equation (16) considering as an initial condition,

| (23) |

Then, the backward path is computed from equation (17) considering as an initial condition

| (24) |

Replacing equation (23) into (24),

| (25) |

and using equations (18) and (20) we find

| (26) |

We see that, in general, since the backward and forward evolutions develop with different dual prescriptions. In the Stratonovich case, , and .

This fact is reflected in the -dependence of the equilibrium stationary state (equation (12) or equation (15)). While the stationary state in the forward evolution is , the stationary state reached by the backward one is given by , and (except for the Stratonovich prescription) . Thus, this is not the backward evolution we are interested in. The key point is to determine the backward stochastic process which, at long times, converges to the same equilibrium distribution as the forward one. To obtain it we write the time reversed Fokker-Planck equation as

| (27) |

where we made the substitutions , and in equation (6). In equation (27), represents the backward probability distribution of the event . Now, we need to specify the drift which produces a backward evolution that asymptotically converges to the equilibrium distribution , with given by equation (15). Setting and , we solve equation (27) for , obtaining

| (28) |

Therefore, the time reversal transformation which makes physical sense, meaning that it produces a backward evolution which converges to a unique equilibrium distribution, is given by

| (29) |

Notice that, since is odd under the transformation , the time reversal operator defined in this way satisfies , as it should be. As we have previously stressed, in the Stratonovich prescription and , so, the time reversal operator simply corresponds to change . In any other prescription the definition of is more involved, given by equation (29). Although we have defined the time reversal transformation to match the correct equilibrium distribution in the long time limit , this transformation also gives the correct answer in the stationary out-of-equilibrium case . In this case, the stationary forward and backward probabilities are different, and they are related by . That is, as can be easily seen by applying the transformation (29) to the Fokker-Planck equation (7) and (8).

4 Detailed balance, microscopic reversibility and entropy production

In this section we check that the concept of -dependent equilibrium and the time reversal transformation introduced in the previous sections are consistent with the usual concepts of detailed balance, microscopic reversibility and entropy production. To do this, we use the path integral formalism, which turns out to be very convenient for handling stochastic trajectories.

4.1 Path Integral formulation

The transition probability represents the conditional probability of finding the system in the state at time provided the system was in the state at time . In the path integral approach, it can be written as [22]

| (30) |

with the boundary conditions and and the “action” given by

| (31) |

The probability for the time reversal process is obtained by applying the time reversal transformation of equation (29) to the forward probability, equations (30) and (31),

| (32) |

with the boundary conditions and and the time reversed “action” .

In order to compute , it is interesting to write in another form to make explicit its properties under the time reversal transformation. Expanding the integrand of equation (31) and considering a conservative system (equation (14)) we find

| (33) | |||||

The last term can be transformed in a total time derivative. However, for arbitrary values of , we need to apply the proper chain rule, since usual calculations rules are valid only for the Stratonovich convention . In the general case, for an arbitrary differentiable function of a random variable , the chain rule reads

| (34) |

Clearly, for , equation (34) is the usual chain rule. For , this formula is known as the Itô formula. For the Hänggi-Klimontovich prescription, , the latter differentiation rule differs from the Itô formula just in the sign of the last term. This is because both prescriptions are time reversal conjugate. In fact, the second derivative term is odd under , as it should be, since all terms in (34) should be odd under time reversal.

The most important property which results from equations (35) and (36) is that is time reversal invariant, . Therefore, by using equation (35), the time reversed action can be easily determined:

| (37) |

Thus, for an arbitrary , the variation of the action under a time reversal transformation is just a total derivative term. Using equations (35) and (37), it is immediate to show that

| (38) |

with given by equation (15).

4.2 Detailed balance

One of the consequences of the time reversal operator (29) is that the conditional probabilities . However, using equations (30), (32), (35) and (37), it is simple to show that

| (39) |

satisfying the detailed balance relation

| (40) |

So, we have shown that forward and backward conditional probabilities, with the definition of equilibrium state given by the effective potential of equation (15), satisfy the detailed balance relation, equation (40), for arbitrary values of . In the special case of , , and equation (40) is the usual detailed balance relation.

4.3 Microscopic reversibility and entropy production

It is not difficult to analyze the previous results from the perspective of stochastic thermodynamics [36]. The detailed balance relation (40) represents a connection between a transition probability and its time reversed one. Moreover, the transition probability was obtained by integrating over all possible stochastic trajectories. However, there is also a relation between the probabilities associated with each individual stochastic trajectory, that is usually called microscopic reversibility [12]. To show up this relation explicitly, we can assign to each stochastic trajectory , with end points and , a weight

| (41) |

The heat dissipated into the environment , and thus, the increase of entropy in the medium associated with one specific trajectory, is given by [37]

| (42) |

Hence, for each stochastic trajectory beginning in a state with initial distribution and ending with a different distribution , the total entropy production is

| (43) |

or, using equation (38),

| (44) |

Thus, in the absence of an explicit time dependent driving force, the stochastic entropy is a state function which depends only on the initial and final states. Moreover, if we prepare the initial state in equilibrium , we immediately conclude that for each stochastic trajectory and for arbitrary value of . The relevance of the potential in the entropy production was recently pointed out in [38] for the Stratonovich prescription. Here, we generalize this concept to the general case of the -prescription where the time reversed process is not trivial. It is interesting to note that a similar expression to (44), however quite cumbersome, could be obtained for a stationary out-of-equilibrium potential. The complication in this case is that the stationary potential depends on , and the action does not transform as easily as in equation (38) under time reversal, since .

5 Correlation functions, Grassman variables and hidden symmetries

In order to push forward our analysis of equilibrium properties it is convenient to have a formalism to compute correlations and response functions. However, the action of equation (35) and the difficulties introduced by the generalize Itô calculus (eq. (34)) make the functional formalism in quite cumbersome. For this reason it is convenient to introduce auxiliary stochastic variables (a function and two Grassman functions ) extending in this way the functional space of stochastic functions. The immediate consequence is a formalism that does not depend on the explicit value of , simplifying its mathematical properties. As a by-product, hidden symmetries of the system can be put in evidence. These symmetries impose non-perturbative constraints on correlations functions and are related to equilibrium properties of the system like, for instance, the fluctuation-dissipation theorem.

5.1 Generating functional

We are interested in the calculation of correlations of functions of the stochastic variable at equal or different times. For instance, we could want to compute , where is an arbitrary function of , or two point functions .

In the path integral approach these mean values can be written as

| (45) |

where is given by equation (31) and . This equation takes a simpler form if we consider that the system is prepared in equilibrium at . In this case, . Assuming an ergodic evolution, we consider that

| (46) |

for an arbitrary value of . Therefore, using equation (45) and equation (46) we can write the mean value as

| (47) |

where we have extended the time integration from to and, now, there are no more constraints in the functional integration. It is important to recall that this simpler expression is only possible because we sample the initial condition with the equilibrium distribution . Provided this is satisfied, we can compute any mean value or correlation function from the generating functional

| (48) |

where is a source with compact domain, that is, it adiabatically goes to zero away from an interval where we will compute the correlation functions.

In this context, any total derivative term in does not contribute to the dynamics of any observable. A total derivative term only contributes to a constant prefactor of a correlation function. In this way, a system described by equation (48) is automatically invariant under time reversal since and differ just in a total time derivative term. On the other hand, if we impose the constraint , the action is truly time reversal invariant . Again, it is important to observe that this happens because we have prepared the system at equilibrium at some initial time and we are computing correlation functions at later times . For any other initial distribution we need to go back to equation (45) to compute mean values.

5.2 Time reversal and entropy production in terms of Grassman variables

Equation (48) can be used to study general correlation and response functions of a white-noise multiplicative stochastic process whose dynamics is driven by equation (1). The -dependence of the final equilibrium distribution, the structure of and the fact that for general the usual rules of calculus do not apply, make this method cumbersome. Nevertheless, we have shown [22] that, introducing an auxiliary “bosonic” variable , and a couple of conjugate Grassman variables , we can avoid this inconvenience by alternatively using the generating functional formalism in this extended space. The generating functional can be cast in the following form,

| (49) |

where the “action” is given by

| (50) | |||||

This action in the extended functional space is completely equivalent to the usual formalism presented in §4.1. In fact, functional integrating over Grassman variables and over the variable we get the generating functional (48), with the action given by equation (31). The advantage of this extended formulation is that it does not depend explicitly of the -parameter and then, the calculus rules are the usual ones for any . Hence, all the complication of the stochastic calculus associated with the definition of the Wiener integral is now codified in the anti-commuting Grassman algebra, implying, for instance, that . Of course, the parameter reappears when we need to properly define Grassman retarded Green’s functions. In fact, equal-time correlations functions are ill-defined, forcing us to set . One of the advantages of this procedure is that, while the Grassman variables are not integrated, we can work out any calculation without explicitly indicate an specific convention. This is particularly useful to study Markovian white-noise processes, where the equilibrium distribution depends on . This situation is very different from non-Markov processes [28], in which .

The time reversal transformation, equation (29), has a simpler form in terms of Grassman variables,

| (51) |

where are the time reversed Grassman variables. There is a subtlety in these transformations which involves the extremal values of the Grassman variables. While , the time reversed variables satisfy . This fact has no importance at all when computing correlation functions. However, it is relevant to analyze entropy production and other relations that depend on total derivatives.

The real advantage of the Grassman representation is that almost any important symmetry becomes a linear transformation. It is simple to check that, in this representation, and

| (52) |

Then, the entropy production , associated with each trajectory, is given by

| (53) |

We see that, in the extended space of trajectories , the entropy production associated with each trajectory is not zero. This is due to the apparently extra degrees of freedom introduced by the Grassman variables. On the other hand, upon functional integration we have that

| (54) |

due to fermionic number conservation and the total entropy production is zero, as it should be in an equilibrium evolution. This opens the interesting possibility of interpreting an entropy production as a spontaneous breaking of fermionic phase (Gauge) invariance like, for instance, in superconducting phase transition. This effect cannot happen in our example of one stochastic variable, but in multiple variables systems [39], there are quartic interactions between Grassman variables opening this attractive possibility.

5.3 Linear response

It is interesting to compute the linear response of the system to an external perturbation. To see this, we slightly perturb the system out of equilibrium

| (55) |

and compute the dynamic susceptibility

| (56) |

Introducing (55) into (50) and computing equation (56) we find

| (57) |

In the case of additive noise, where , the response function has the simpler form, . For this reason, the auxiliary function is usually called the response variable. However, for multiplicative noise, the response is more complex since involves, not only correlations functions of , but also contributions from the Grassman sector of the model. This is a direct consequence of multiplicative white-noise since a variation of the “external” potential is modifying the fluctuations properties of the system. This means that the susceptibility explicitly depends on . From equation (57), it is immediate to recognize a “natural response variable”

| (58) |

in such a way that,

| (59) |

We will show that has a key role in the supersymmetric formulation of the model.

5.4 Supersymmetry and covariant (superfield) representation

The path integral formalism is useful to make evident symmetries of the stochastic process. For instance, the action given by eq.(50) is invariant under the transformation,

| (60) | |||||

| (61) |

where is an anticommuting parameter. This nilpotent transformation () is the famous BRS [40] symmetry, discovered in the context of quantization of Gauge theories. In the present context, it simply enforces probability conservation, .

There is another set of important symmetries related with equilibrium properties which is called supersymmetry. To display it explicitly, it is convenient to work with the natural response variable introduced in equation (58). Therefore, we make in equations (49) and (50) the funcional change of variables , defined by

| (62) | |||||

| (63) | |||||

| (64) |

The last two transformations make the Jacobian trivial, , since and the fermionic measure reads .

The generating functional is then given by

| (65) |

where the action reads

| (66) | |||||

where we have drop-off function’s arguments just to simplify notation.

At first sight, this action written in the space seems to be more complex than the preceding one. However, these new physical variables can be rearranged in order to explicitly display SUSY.

First, it is convenient to write and in terms of two “potentials”, and , defined as follows

| (67) | |||||

| (68) |

Then, we collect the variables , in the definition of the superfield

| (69) |

where we have introduced two “temporal” Grassman variables and .

The generating functional, equation (66), can be re-written in terms of as

| (70) |

where depends on the potentials and by

| (71) |

We have defined the covariant derivatives

| (72) |

which satisfy and . The action (71), when written in components form, is completely equivalent to equation (50) or, after integration of the Grassman variables, to equation (36), as it is shown in the Appendix.

It is now immediate to verify that (71) is invariant under transformations of the supersymmetry group [26], whose generators are

| (73) |

The symplicity of the superfield representation resides in the fact that each SUSY transformation is a translation of the temporal variables .

Then, the invariance of the last term of equation (71) is trivial, since does not depend explicitly on . To demonstrate the invariance of the kinetic part of the action, it is useful to have in mind the graded algebra,

| (74) | |||||

| (75) | |||||

Thus,

| (76) |

On the other hand, , where is an arbitrary Grassman parameter and may represent or defined in equation (73). In this way,

| (77) |

Finally, using the algebra (74), we find,

| (78) |

which is a total derivative term, demonstrating in this way, the invariance of .

For additive processes, the diffusive potential is linear, , and eq.(71) reduces to the usual action defined with a single superpotential . In this case, the tadpole theorem [22] guarantees that the stochastic evolution does not depend on . However, multiplicative processes (non-linear ) induce derivative couplings in the superfield. These couplings are responsible for the -dependent evolution which leads to the equilibrium distribution of equation (15).

5.5 SUSY Ward-Takahashi identities and equilibrium

The study of the symmetries of the action enables us to deduce properties of equilibrium dynamics of the system. Each of the three generators of SUSY, , imposes several non-perturbative constraints on correlation functions. To obtain these constraints, we will use the Ward-Takahashi identities

| (79) |

where is an arbitrary parameter and is one of the generators of SUSY. Note that, if is or , then is a Grassman parameter, while, if , is a commutative parameter.

The Ward-Takahashi identity related with the generator reads,

| (80) |

implying time-translation invariance as

| (81) |

Then, any two-point correlation function depends on time differences . This is a necessary condition for an equilibrium evolution.

On the other hand, the generator of translations, , induces the identity

| (82) |

that, when written in components, imposes the relations

| (83) | |||||

| (84) |

All components, involving only one of the Grassman variables, and , vanish because of fermionic number conservation. The first equation relates the physical linear response of the system with the Grassman two-point correlation function. Since the physical response is causal, i. e. , for , (see equation (59)), we are forced to choose the retarded prescription in computing Green’s functions of Grassman variables. On the other hand, the equal-time Green function is not well defined, forcing us to adopt a prescription , where is an arbitrary initial value. This presciption, when written in the original variables, is , allowing us to identify with the needed prescription to define the Wiener integral. Notice that, in the case of non-Markovian processes, , without any ambiguity.

Finally, the invariance of the action generated by , which arise from the identity

| (85) | |||||

results in the non-perturbative constraints,

| (86) | |||||

| (87) |

This constraints imply another important equilibrium property, the fluctuation-dissipation theorem, which relates the spontaneous fluctuations of the system with its response to an external perturbation. To explicitly see this, we substitute relation (83) into (86), obtaining

| (88) |

Using the equilibrium time translations invariance of the correlation function , this identity becomes

| (89) |

which, bearing causality in mind, can be rewritten as

| (90) |

where is the Heaviside step function. Equation (90) is a traditional form of the fluctuation-dissipation theorem. A more commonly used form of equation (90) is given in terms of the Fourier transform of the response function,

| (91) |

Then, the fluctuation-disipation theorem can be understood as a direct consequence of supersymmetry. We have shown that, even thought the correlation functions and the responses depend on in a multiplicative process, the fluctuation-dissipation theorem is satisfied for any value of , provided we correctly identify the equilibrium distribution, equation (15) and the time reversal transformation, equation (29). These physical concepts are mathematically codified in the invariance under supersymmetry transformations, that we have explicitly shown in this section.

It is very interesting to note that extensions of the fluctuation-dissipation theorem, for out-of-equilibrium steady states, can be formulated [41]. A natural arising question is whether a related SUSY exists for these out-of-equilibrium states.

6 Discussion and conclusions

We have presented a detailed study of equilibrium properties of a Markovian multiplicative white-noise stochastic process. The stochastic process was modeled in its simplest version of a single stochastic variable, by means of the Langevin equation (1), defined by a drift term and a diffusion function . We have completed the definition of the stochastic differential equation by using the Generalized Stratonovich Convention, characterized by a parameter .

The asymptotic equilibrium distribution was found by solving the stationary Fokker-Planck equation, imposing an asymptotic zero current probability. This naturally conduce to an equilibrium potential (Eq. (15)) which explicitly depends on . For (Hänggi-Klimontovich interpretation), the potential coincides with the classical deterministic one, , in agreement with the Boltzmann distribution for thermodynamical equilibrium. However, for any other convention, the equilibrium potential is more general, including, for instance, power-law distributions. Thus, the definition of equilibrium in the stochastic dynamical sense not necessarily coincides with the thermodynamical equilibrium concept. We have shown that, even for this generalized definition of equilibrium, the system satisfies the usual equilibrium properties such as detailed balance, microscopic reversibility and the fluctuation-dissipation theorem.

Time reversal properties of the stochastic process are quite interesting. We have shown that, if the forward stochastic trajectory evolves with a definite value of , the time reversed trajectory evolves with the conjugated prescription . Therefore, in order to have a unique equilibrium distribution, the definition of time reversed stochastic process is given by the transformation (29), where we need to change not only the velocity sign, but also the prescription and the drift force.

We have shown that, using the equilibrium potential and the time reversal transformation of equation (29), the stochastic process satisfies detailed balance relations for any value of the parameter . It is convenient to note that, in equation (40), the forward transition probability is not equal to the backward one, except for the Stratonovich convention , where forward and backward trajectories coincide. We have also shown that, if the initial and final states of a finite time evolution are prepared in equilibrium, the entropy production of each stochastic trajectory vanishes for arbitrary prescriptions, verifying the related principle of microscopic reversibility. In order to show these properties, we have used the path integral representation of the stochastic process, where the central object is the hole stochastic trajectory. Also, we were forced to intensively use an -generalized Itô calculus, summarized in the -dependent “chain rule” of equation (34).

Related with equilibrium properties, there are hidden symmetries in the stochastic process that can be better analyzed in the path integral approach, formulated in an extended functional space composed of commutative as well as anti-commutative Grassman variables. The advantage of this formulation is that it is prescription independent. That is, ambiguities in the definition of the multiplicative stochastic processes can be understood, not as a continuum limit ambiguity, but as a necessity to define equal time Grassman Green’s functions. Then, provided the Grassman variables are not integrated out, it is not necessary to fix any prescription. In this way, we can use ordinary calculus rules, but instead we need to work with anti-commuting variables. In some sense, all the complexity of the Itô calculus is codified in the Grassman algebra in this formulation.

In this context, we have computed the entropy for each stochastic trajectory (in the extended space) and we have shown that it is not zero, but proportional to a time derivative of the Grassman variables density (equation (53)). This is due to the extra degrees of freedom we have added to extend the functional space. However, integrating over the Grassman variables, we immediately recognize that the entropy production is zero, as it should be for an equilibrium evolution. Interestingly, this cancellation is due to “fermionic number conservation”, in other words, due to the invariance under phase transformations. This allows us to speculate about the very attractive possibility of interpreting an out-of-equilibrium evolution, i. e. , a non-zero entropy production, as a consequence of a gauge symmetry breaking, very similar with a superconducting transition. Of course, this cannot happen in our present example, since we only have one stochastic variable and, consequently, the Grassman variables are not-interacting. Nevertheless, in multiple variable systems, quartic terms in the Grassman variables are certainly possible.

Another interesting symmetry which appears in this formulation is supersymmetry (SUSY), expressed as a linear transformation, mixing commuting as well as anti-commuting variables. We have presented a supersymmetric covariant representation of the stochastic process. While this representation was known for additive processes and multiplicative non-Markov processes, the present case of Markovian multiplicative white noise was quite difficult to treat due to the different prescriptions available to define it, connected by a time reversal transformation. In this representation, the non-trivial time reversal transformation is represented by a simple linear transformation. The difficulty of the time conjugated prescriptions are confined to boundary conditions, irrelevant in the computation of correlation functions.

Using this SUSY covariant formalism we have analyzed two-point Ward-Takahashi identities. One of them relates linear responses and fluctuations. We have shown that, while the linear response function and fluctuations are -dependent, they satisfy the fluctuation-dissipation theorem for arbitrary values of the prescription . Therefore, similar to the additive case, supersymmetry is a consequence of equilibrium evolution, even thought we have different equilibrium evolutions for different prescriptions.

Summarizing, we have presented a compact path integral formalism to deal with Markovian multiplicative white-noise systems, independently of the prescription used to define the Wiener integral. In its supersymmetric covariant form, it automatically encodes equilibrium properties. Therefore, it is very appropriate to organize perturbative calculations, since supersymmetry imposes non-perturbative constraints that should be verified at any order of perturbation theory. On the other hand, keeping in checked equilibrium properties, we can safely go forward in the study of out-of-equilibrium fluctuation relations described by this type of stochastic processes.

Acknowledgedments

The Brazilian agencies, Fundação de Amparo à Pesquisa do Rio de Janeiro, FAPERJ and Conselho Nacional de Desenvolvimento Científico e Tecnológico, CNPq are acknowledged for partial financial support. Z.G.A. was partially supported by the Latin American Center of Physics, CLAF, under the collaborative doctoral program ICTP-CLAF.

Appendix A

In this appendix we explicitly show that the action, written in the super-field formalism, equation (71), is in fact equivalent to the time reversal invariant action , given by equation (36).

Let us define the scalar super-field

| (92) |

and the super-potentials and , that we expand in powers of the temporal Grassman variables and as,

| (93) |

and

| (94) |

The system Lagrangian is given by the components in the form

| (97) |

Then, using equations (94), (95) and (96),

| (98) | |||||

and

| (99) |

Replacing these expressions into equation (97) we find

| (100) | |||||

We make the following change of variables in the functional integral: first, we shift the variable ,

| (101) |

whose Jacobian is one, since it is just a translation. Then, we rescale in the following way,

| (102) | |||||

| (103) | |||||

| (104) |

The Jacobian of the first two transformations is and the Jacobian of the last transformation is , then the two Jacobians cancel each other and the Lagrangian in the new variables reads,

| (105) | |||||

Considering that, by definition, and, thus, , we obtain

| (106) | |||||

The last term is a total derivative. This term appears making a trivial transformation like in the term. This is because a supersymetric Lagrangian is invariant up to a total derivative under SUSY transformations. This is a general feature of SUSY. A transformed supersymmetric action is invariat up to boundary terms.

Rewriting this last expression in terms of the original functions and we finally get

| (107) |

Upon integration and realizing that the last term is a total derivative one, we find

| (108) |

Where is the action of equation (50) and, then, is equal to equation (36), as can be seen comparing (108) with (35), as we want to demonstrate.

To compute correlation functions the range of integration is infinite and . However, for finite time we see that the supersymmetric action is equivalent to the time reversal invariant action .

References

References

- [1] Hänggi P and Marchesoni F 2005 Chaos: An Interdisciplinary Journal of Nonlinear Science 15 026101

- [2] van Kampen N G 2007 Stochastic Processes in Physics and Chemistry (London, UK: Elsevier)

- [3] Gardiner C W 1996 Handbook of stochastic methods for physics, chemistry and the natural sciences (Berlin Heidelberg: Springer-Verlag)

- [4] Freund J A and Pöschel T 2000 Stochastic Processes in Physics, Chemistry and Biology (Berlin, Heidelberg: Springer-Verlag)

- [5] Murray J D 2002 Mathematical Biology. I. An introduction (Berlin, Heidelberg: Springer-Verlag)

- [6] Mantegna R N and Stanley H E 2000 An introduction to econophysics: correlations and complexity in finance (Cambridge, UK: Cambridge University Press)

- [7] Bouchaud J P and Potters M 2003 Theory of financial risk and derivative pricing: from statistical physics to risk management (Cambridge University Press)

- [8] Lançon P, Batrouni G, Lobry L and Ostrowsky N 2001 EPL (Europhysics Letters) 54 28

- [9] Lançon P, Batrouni G, Lobry L and Ostrowsky N 2002 Physica A: Statistical Mechanics and its Applications 304 65 – 76

- [10] García-Palacios J L and Lázaro F J 1998 Phys. Rev. B 58(22) 14937–14958

- [11] Gitterman M 2005 The noisy oscillator: The first hundred years, from Einstein until now (World Scientific Publishing Co.)

- [12] Crooks G E 1999 Phys. Rev. E 60(3) 2721–2726

- [13] Seifert U 2005 Phys. Rev. Lett. 95(4) 040602

- [14] Seifert U 2008 The European Physical Journal B - Condensed Matter and Complex Systems 64(3) 423–431

- [15] Itô K 1951 J. Math. Soc. Japan 3(3) 157–169

- [16] Stratonovich R L 1966 J. SIAM control 4 362–371

- [17] Hänggi P 1978 Helv. Phys. Acta 51 183

- [18] Janssen H K 1992 Topics in Modern Statistical Physics (Singapore: World Scientific)

- [19] Hänggi P 1980 Helv. Phys. Acta 53 491

- [20] Hänggi P and Thomas H 1982 Phys. Rep. 88 207

- [21] Klimontovich Y L 1994 Physics-Uspekhi 37 737

- [22] Arenas Z G and Barci D G 2010 Phys. Rev. E 81(5) 051113

- [23] Parisi G and Sourlas N 1979 Phys. Rev. Lett. 43

- [24] Feigel’man M V and Tsvelik A M 1982 Zh. Eksp. Teor. Fiz. 83 1430–1443

- [25] Parisi G and Sourlas N 1982 Nuclear Physics B 206 321 – 332

- [26] Zinn-Justin J 2002 Quantum field theory and critical phenomena (USA: Oxford University Press)

- [27] Bouchaud J P, Cugliandolo L, Kurchan J and Mézard M 1996 Physica A: Statistical Mechanics and its Applications 226 243 – 273

- [28] Aron C, Biroli G and Cugliandolo L F Journal of Statistical Mechanics: Theory and Experiment 2010 P11018

- [29] Arenas Z G and Barci D G 2012 Phys. Rev. E 85(4) 041122

- [30] Chaturvedi S, Kapoor A K and Srinivasan V 1984 Zeitschrift für Physik B Condensed Matter 57(3) 249–253

- [31] Corberi F, Lippiello E and Zannetti M 2007 Journal of Statistical Mechanics: Theory and Experiment 2007 P07002

- [32] Hänggi P 1989 Z. Physik B 75 275

- [33] Lau A W C and Lubensky T C 2007 Phys. Rev. E 76 011123

- [34] Volpe G, Helden L, Brettschneider T, Wehr J and Bechinger C 2010 Phys. Rev. Lett. 104(17) 170602

- [35] Brettschneider T, Volpe G, Helden L, Wehr J and Bechinger C 2011 Phys. Rev. E 83(4) 041113

- [36] Hatano T and Sasa S 2001 Phys. Rev. Lett. 86 3463

- [37] Crooks G E 2000 Phys. Rev. E 61 2361–2366

- [38] Lev B I and Kiselev A D 2010 Phys. Rev. E 82(3) 031101

- [39] Crisanti A, Puglisi A and Villamaina D 2012 Phys. Rev. E 85 061127; Puglisi A and Villamaina D 2009 EPL (Europhysics Letters) 88 30004

- [40] Bechi C, Rouet A and Stora S 1976 Phys. Lett. B 52 344

- [41] Marconi U M B, Puglisi A, Rondoni L and Vulpiani A 2008 Physics Reports 461 111