The solution of discretionary stopping problems with applications to the optimal timing of investment decisions111Research supported by

EPSRC grant nos. GR/S22998/01, EP/C508882/1222This is an Author’s Original Manuscript of an article submitted for consideration in the IMA Journal of Mathematical Control and Information

Timothy C. Johnson333Maxwell Institute for

Mathematical Sciences and Department of Actuarial Mathematics

and Statistics, Heriot-Watt University, Edinburgh EH14 4AS,

UK, t.c.johnson@hw.ac.uk

Abstract

We present a methodology for obtaining explicit solutions to infinite time horizon optimal stopping problems involving general, one-dimensional, Itô diffusions, payoff functions that need not be smooth and state-dependent discounting. This is done within a framework based on dynamic programming techniques employing variational inequalities and links to the probabilistic approaches employing -excessive functions and martingale theory. The aim of this paper is to facilitate the the solution of a wide variety of problems, particularly in finance or economics.

A fundamental problem in finance, economics and management science is to determine the optimal time to invest in a project in a random environment and to address these types of problems the theory of discretionary stopping has been widely employed following Karlin [24].

In order to solve some problems of this type we fix a filtered probability space, , satisfying the usual conditions and carrying a standard one-dimensional -Brownian motion, . We assume that the stochastic system we study is driven by the Itô diffusion given by the stochastic differential equation

Our objective is to select the -stopping-time, , that maximises

where is subject to the conditions in Assumption 2.4 and is a state-dependent discounting factor defined by

(2)

for some function satisfying the conditions of Assumption 2.3.

The majority of financial and economic models in the literature assume that the underlying asset’s value dynamics are modelled by a geometric Brownian motion, the associated payoff function is affine and the discounting rate is constant. The approach we employ relaxes all these assumptions.

Considering more general payoff functions allows for utility based decision making, which, apart from the work of Henderson and Hobson [19], and despite its fundamental importance, has not been widely discussed.

However, the main benefit of accommodating general payoffs in the modelling framework is the ability to incorporate compound payoffs into the payoff function, such as running payoffs or reversible decisions, as in Johnson and Zervos [22] or Guo and Tomecek [18]. For example, consider the case where a project is initiated at a cost and provides a running payoff given by . In this case we have that

(3)

for a stopping-time . Here, for example, could represent the demand for electricity and is the ‘stack’, a discontinuous function, representing the price of supplying the demand, or could be the value of an asset that is taxed at banded rates, modelled by and . In both these, practically important, cases will not be and the classical approach to solving stopping problems using variational inequalities cannot be used.

The framework we present accommodates systems driven by general Itô diffusions. This is essential in economics given that not all asset price processes should be modelled by a geometric Brownian motion, which, on average, grows exponentially. Beyond decisions driven by prices, extending the theory to a wider class of diffusions is important, for example in regime switching models such as in Dai, Zhang and Zhu [9] where the driving stochastic process represents a probability that the market is a bull or bear, and .

Employing state dependent discounting enables a more realistic modelling framework for investment decisions in the presence of default risk and the events following 2007 have highlighted the importance of including this feature in decision making.

One approach to addressing discretionary stopping problems is through dynamic programming and involves a set of variational inequalities. This is discussed by, amongst many others, El-Karoui [15], Krylov [26], Bensoussan and Lions [4], Davis and Karatzas [10], and Guo and Shepp [17]. The technique has become widespread in finance and economics since the introduction of so-called ‘real options’ theory by McDonald and Siegel [31], and has been described in Merton [32], Dixit and Pindyck [13] and Trigorgis [38]. However, taking this approach often involves making strong assumptions about the problem data in order to obtain explicit results.

A different approach has been to employ -excessive functions, functions that satisfy

This approach has been adopted by Dynkin [14], Shiryaev [36], Salminen [35], Alvarez [1] and Lempa [29], while Dayanik and Karatzas [12] and Dayanik [11] use a certain characterisation of -excessive functions, as the difference of two convex functions, to solve the stopping problem. These techniques, while powerful, are technical and are less accessible to a general audience in finance and economics unfamiliar with the details of probability theory.

Another approach uses martingale theory to locate the optimal boundaries between the stopping and continuation regions and is taken by, for example, Beibel and Lerche ([2], [3]), Lerche and Urusov [30], and Christensen and Irle [8] and is described informally in Shreve [37, Sec 8.3.2]. This approach, while relatively straightforward, is based on assuming the diffusion starts in the continuation region and considers the first time it hits the stopping region. However, as well as relying on the explicit problem data, this approach depends on the continuation region existing and an intuitive understanding of where it is located.

The approach we adopt is based on the familiar dynamic programming approach while providing the power of the probabilistic techniques. The connection between the different approaches is provided by Johnson and Zervos [21], where the Itô-Tanaka-Meyer formula is used to analyse the solution to the variational inequality as the difference of two convex functions, rather than as a function in . In using this result, the strong assumptions associated with the dynamic programming framework can be relaxed and explicit solutions that rely, only, on the problem data can be easily obtained. This approach has been taken in Rüschendorf and Urusov [34], Lamberton [27], Johnson and Zervos [22] and has been developed fully in Lamberton and Zervos [28].

The contribution of this paper is to demonstrate how the general theory, developed in Lamberton and Zervos [28], can be applied to obtain explicit solutions to a variety of discretionary stopping problems.

This paper is organised as follows. Section 2 is concerned with a formulation of the optimal stopping problem and a set of assumptions for our problem to be well-posed while in Section 3 we discuss the practical implications of these assumptions.

In Section 4 we present the methodology for identifying the boundaries for six ‘elementary’ problems and then, in Section 5, we demonstrate how these ‘elementary’ problems can be employed in solving more complex stopping problems. An Appendix provides a proof of a key result in solving the problem when a continuation region lies between two stopping regions.

2 Problem formulation and technical foundations

Definition 2.1.

Given an initial condition , a stopping strategy is any

pair such that

is a weak solution to (1) and is an -stopping-time.

We denote by the set of all such stopping

strategies.

We consider the optimal stopping problem whose value function, is defined by

(4)

where

Here, is the payoff function and a discounting function, discussed in Section 1. We shall now set out the Assumptions we require in order that this problem is well-posed.

To start this discussion, recall that in solving this problem through dynamic programming, we would associate the value function with a function that is the solution to the, so called, Hamilton-Jacobi-Bellman (HJB) equation,

(5)

The solution to the stopping problem involves splitting the interval into the stopping region, , and the continuation region, , with . For all , in order that (5) is satisfied, we require that

while for all ,

To develop an understanding of the general solution of the second-order linear homogeneous ODE, which features in (5), we assume that the data of the one-dimensional Itô diffusion, given by (1) in the introduction, satisfies the following assumptions.

Assumption 2.1.

The functions are -measurable,

and

With reference to Karatzas and Shreve [23, Section 5.5.C], the conditions appearing in this assumption are sufficient for the SDE (1) to have a weak solution that is unique in the sense of probability law up to a possible explosion time, for all initial conditions .

This assumption means that the boundaries and are inaccessible to the diffusion starting in , though the boundaries can be entrance boundaries.

Relative to the discounting factor , defined by (2), we make the following assumptions.

Assumption 2.3.

The function is -measurable and there exists such that , for all and

In the presence of Assumptions 2.1–2.3 the general solution of the ODE appearing in (5),

(6)

exists and is given by

(7)

for some constants .

The functions and are , their first derivatives are

absolutely continuous functions,

(8)

(9)

and

(10)

In this context, and are unique, modulo multiplicative

constants, and the Wronskian, , is defined as

Also, given any points in and weak solutions

, of the SDE

(1), the functions and satisfy

(11)

where denotes the first hitting time of ,

All of these claims are standard and can be found in various forms in

several references, such as Feller [16], Breiman [6], Itô and McKean [20], Karlin and Taylor [25], Rogers and Williams [33] and Borodin and Salminen [5].

In order to be able to address problems where the payoff is , but not necessarily , we will consider signed measures of -finite total variation, and we refer to them simply as “measures”. Given such a measure, , on we denote the total variation of by , where is the Jordan decomposition of . Also, we say that a measure is non-atomic if , for all .

A function is the difference of two convex functions if and only if its left-hand side derivative, , exists, is of finite variation, and its second distributional derivative is a measure, which we denote by . In this case we have the Lebesgue decomposition

where is absolutely continuous with respect to the Lebesgue measure and is mutually singular with the Lebesgue measure. On this basis, we define the measure , related to the ODE (6), by

(12)

Now, we define the finite variation, continuous processes by

where is the local-time process of at and we have that the Itô-Tanaka-Meyer formula gives

If is with a first derivative that is absolutely continuous with respect to the Lebesgue measure, , so that

we are able to recover the familiar Itô formula from the Itô-Tanaka-Meyer formula.

With this in mind and in order to place conditions on our payoff function, , such that our problem is well-posed and does not involve value functions that are infinite, we introduce -integrable measures.

Definition 2.2.

A measure on is a -integrable measure if

where the functions and are defined by

Necessary and sufficient conditions for a measure on to be -integrable are ([28, Theorem 12])

(13)

for all and all .

On this basis, and with reference to [28, Theorem 12], we make the following assumptions on .

Assumption 2.4.

The function is the difference of two convex functions, and the measure is -integrable.

In addition, has the following limiting behaviour

(14)

3 Implications of the problem formulation

The framework we adopt accommodates the commonly encountered Itô diffusions, including, Brownian motion, the Ornstein-Uhlenbeck process, geometric Brownian motion, the geometric Ornstein-Uhlenbeck process and the so-called Feller, square-root mean-reverting, or Cox-Ingersoll-Ross, process defined by

where , and are positive constants satisfying . This process has an entrance boundary at , and . When , the expressions for the general solutions (7) to the ODEs associated with all of these diffusions are all well known. In situations where and are not known, it is possible to approximate them through simulation and employing (11).

Turning our attention to the payoff functions that can be accommodated within our framework, we begin by observing that if is the difference of two convex functions and is bounded by some constant, it will be acceptable. Similarly, if for some then (13) will fail. In the case where or , condition (14) of Assumption 2.4 is a strong test as to the acceptability of .

For example, consider the case where is a geometric Brownian motion such that

and suppose that , for constants and . In this case it is well known that

where are given by

If , we need to establish what conditions on the problem data result in satisfying the conditions of Assumption 2.4.

Noting that

in order to establish the second condition in (13), we need to check the finiteness of

and is -integrable if

This result can be obtained more directly by noting that

which can be simplified to the previous inequality.

In fact, (14) will often be tautologous with the requirement that is -integrable, however, the condition (14) is important in that it excludes the cases where or .

With this in mind, under Assumptions 2.1–2.4 and setting

the following results have been established in Johnson and Zervos [21], Johnson and Zervos [22] or in Lamberton and Zervos [28].

The payoff function can be expressed analytically as

(15)

and probabilistically as the -potential of , specifically

and it satisfies Dynkin’s formula, i.e., given any

-stopping times ,

(16)

In additiion we have a transversality condition, namely,

given an increasing sequence of -stopping times

such that ,

This condition implies that our value function should be finite.

we can see that (17–18) are related to the slope of the function , while (19–20) relate to the slope of .

Finally, consider a function that is locally integrable with respect to the Lebesgue measure and define the measure on by

If is -integrable, then the function

is , has absolutely continuous first derivative and satisfies

This result enables problems involving running payoffs, such as those in the initialisation example, (3), to be tackled.

4 The solution to six elementary stopping problems

The methodology we employ is based on the results in Lamberton and Zervos [28, Section 6], where it is established that under Assumptions 2.1–2.3 and a weaker assumption on the payoff, that the value function, , associated with the optimal stopping problem and defined by (4), is of the form

(23)

is -excessive, and is a solution to the variational inequality

(24)

in the following sense.

Definition 4.1.

A function is a solution of the variational inequality (24) if is the difference of two

convex functions, the measure is -integrable,

(25)

(26)

and

(27)

Since Lamberton and Zervos consider only payoffs that are positive, in order to accommodate payoffs that are strictly negative, in particular for and , we need the following growth condition on the value function

(28)

for some constant . This condition, which is only relevant for , is found in the verification theorem in Johnson and Zervos [22, Theorem 3] and replaces (138) in the verification theorem in Lamberton and Zervos [28, Theorem 13].

This section of the paper presents a methodology for identifying the locations of the boundaries between the continuation region, , and the stopping region, , and as a consequence, the constants and . We shall consider six elementary cases in all; the cases are ‘elementary’ in that by combining them together, more complex problems can be addressed.

We start by observing that conditions (25) and (27) reveal immediately that if is positive in some interval, then that interval cannot be in the stopping region. On this basis we have the first, most basic, two cases.

CASE I

is positive for all .

CASE II

is negative for all .

We now consider two more cases constructed by combining Cases I and Cases II. To appreciate the relevance of the first of these new cases, consider the situation when the payoff, , is such that and increases in such a way that there is a single boundary point, , separating the continuation and stopping regions, so that and . In this situation, by (23) and (28), we must have .

In the standard approach, where is , to specify the parameters and , we would appeal to the so-called ‘smooth-pasting’ condition of

optimal stopping that requires the value function to be at the free

boundary point . This requirement yields the system of equations

which is equivalent to

where is defined by

using (19)–(20). We note that corresponds to a a stationary point of . Since , and from (25) we require that , we have the implication that is at either a maximal turning point or a falling point of inflection.

In the more general case that is not at the free boundary point , our objective is to find the parameter such that

At this point it is worth noting that the measure becomes central to obtaining the solution to the stopping problem, just as in Cases I–II. On this basis we present the next two cases.

CASE III

is positive in the interval and negative for all such that there is a maximal turning point of for some , with

but there is no maximal turning point of in . This case is associated with call option type payoffs.

CASE IV

is negative for all and positive in the interval such there is a maximal turning point of for some , with

but there is no maximal turning point of in . This case is associated with put option type payoffs.

Having constructed Cases III–IV by combining Cases I–II, we construct the final two cases by combining Cases III–IV.

CASE V

is positive for some and and negative for all such that achieves a maximal turning point for some while achieves a maximal turning point for some with

This case is associated with butterfly option type payoffs.

CASE VI

is negative for all and positive for some such that achieves a stationary point for some ,

while achieves a stationary point for some , with

(29)

This case is associated with straddle option type payoffs.

Observe that (17)–(20) imply that Case V occurs when we have , while Case VI occurs when .

Case VI is important in that it represents situations when the stopping problem is one of the first exit time of the diffusion from an interval, rather than the the cases when one boundary is inaccessible and the problem is one of locating the first hitting time of a point, which characterise Cases I–V. Practically this means that the continuation region has two boundaries, one on the left hand side, which we shall denote by , and the other on the right hand side, , and the following conditions need to be satisfied at the two boundaries

(30)

(31)

(32)

We note that (30)–(32) mean that the points define maximal turning points of the function

and that

These two observations are important in the martingale approach to solving stopping problems (such as in [2], [3], [8]).

In order to identify the locations of , and hence the values for and , observe that by using (17)–(20), (30)–(32) can be rearranged into the following set of equations

(33)

(34)

(35)

(36)

These are equivalent to the following system of equations

(37)

and

(38)

where

(39)

(40)

and

(41)

(42)

We need to strengthen our assumptions on in order to prove the existence and uniqueness of appearing in (37)–(37), this is done, along with some explanation, in Lemma A.1 in the Appendix.

We now solve the various control problems described in Cases I–VI by constructing explicit solutions of the variational inequalities (24) that satisfies the requirements of (23), Definition 4.1 and (28).

Theorem 4.1.

Suppose that Assumptions 2.1,2.2,2.3 and 2.4 hold. We have the following solutions to the discretionary stopping problem we have formulated as Cases I–VI.

Case I. Given any initial condition , then the value function is given by and . In this case there is no admissible stopping strategy; the optimal stopping time is .

Case II. Given any initial condition , then the value function is given by , and the optimal stopping time is .

Case III. Given any initial condition , then the value function is given by

(43)

with . Furthermore, given any initial

condition , the stopping strategy , where

is a weak solution to (1) and

is optimal.

Case IV. Given any initial condition , then the value function is given by

(44)

with . Furthermore, given any initial

condition , the stopping strategy , where

is a weak solution to (1) and

is optimal.

Case V. Given any initial condition , then and the value function is given by

(45)

with and . Furthermore, given any initial

condition , the stopping strategy , where

is a weak solution to (1) and

is optimal.

Case VI. If is a positive, non-atomic measure on and (29) is true, then there exist a unique pair such that (37)–(38) are true. In these circumstances, given any initial condition , then and the value function is given by

(46)

with

(47)

(48)

Furthermore, given any initial

condition , the stopping strategy , where

is a weak solution to (1) and

is optimal.

We immediately note that for to be the difference of two convex functions, we will require continuous fit at the boundaries between the continuation/stopping regions. This is satisfied by all of (43)–(46). On this basis, the measure will be -integrable given and since is -integrable by Assumption 2.4.

Proof of Case I. The stopping region cannot coincide with any interval in which is strictly positive, by (25), implying that and (27) is satisfied. To satisfy (23) and (28) we require that , implying . Equations (17)–(20) mean that is increasing (resp., is decreasing) for all , however, this and (14) in Assumption 2.4 implies that for all and (26) is satisfied.

Proof of Case II. Since is negative for all , Dynkin’s formula (16) implies that it would be optimal to stop immediately and that and (25) is true. Since for all , (26)–(27) and (28) are satisfied.

Note that equations (17)–(20) mean that is decreasing (resp., is increasing) for all . This, with (14) in Assumption 2.4 implies that for all and the value function is strictly positive.

Proof of Case III. Observe that as a consequence of being positive for all and negative for all and (19)–(20) we will have that . In addition, because is decreasing in and , the implication being that . Also, (43) satisfies (26) because

For given by (43), (27) is true and, similarly, (25) is true since and in this interval. Finally, (28) holds since .

Proof of Case IV. This is symmetric to Case III. Observe that as a consequence of being negative for all and positive for all and (17)–(18) we will have that implying, as with Case III, . Since

(44) satisfies (26)–(27), (25) is true since and in this interval. Finally, (28) holds since .

Proof of Case V. We can regard Case V as being composed of (moving from to ) Case III, Case II, and then Case IV. The proof of this case is a combination of the proofs of these more elementary cases.

Proof of Case VI. We begin by noting that Lemma A.1 proves the existence of a unique pair such that (37)–(38) are true. To see that (46) satisfies (26), recall that (37)–(38) imply that the points define maximal turning points of the function

and so

Also, for given by (46), (27) is true and, similarly, (25) is true since , while (28) holds since

with the final inequality being a consequence of being negative for all and

since is a maximum turning point of . Similar arguments show that .

Remark 4.1.

The justification for the ‘pasting’ of intervals in Case V comes from Lamberton and Zervos [28, i.e. Theorem 12], where the stopping problem is solved for the case of absorbing boundaries with the payoff at the boundaries being positive, with the result that the absorbing boundaries are in the stopping region. In Case V, the value function at the boundaries of the sub-intervals ( and ) identifies with the payoff and we can regard the open interval being made up of three separate stopping problems on , and with the diffusion being ‘absorbed’ at and .

Remark 4.2.

Notice that in Cases III–V, since it is not a requirement that in the waiting region, it is necessary and sufficient that there are maximal turning points at (resp., ) such that

Remark 4.3.

The existence of the stationary points and is sufficient, not necessary in Case VI. There will be cases when for some interval, but this will not lead to a stationary point of either of the functions or .

5 Examples

We finish with some concrete examples to develop the ideas presented in Section 4. In all the examples we shall consider the diffusion, , is given by a geometric Brownian motion with drift and volatility and there is a constant discount rate of . In this case, as presented in Section 3, we have that

In the first example, we consider a payoff function of the form

where is the Dirac probability measure, assigning mass 1 at the point .

This means that if , is a positive measure for all and we have the conditions of Case II. If we have the conditions for Case III. In the event that , we know we will be waiting at since and while we do not have the specific conditions for Case VI, in fact there is no stationary point of for , we can infer that the value function is going to be of the form (46), since in the cases when we do have a stationary point of ,

When , the boundaries of the stopping/continuation regions, , can be found either by solving the the smooth fit problem

or by finding the unique such that and where and solve

(49)

while and solve

(50)

One benefit of using (49)–(50) over ‘smooth fit’, is that it is immediately obvious that there is no solution with when , which is not obvious a priori from the four smooth fit equations. To appreciate how this method has advantages over the ‘martingale approach’, see [28, Example 5].

with and . By finding the crossing of and , we deduce that, in this case, the value function is given by

Our second example involves two functions that do not satisfy Assumption 2.4, but never the less demonstrate the usefullness of considering complex stopping problems in terms of Cases I–VI. Consider two ‘staircase’ type payoffs, as discussed in Bronstein, et al. [7],

Since these functions are not continuous, they do not satisfy the conditions of Assumption 2.4 apart from (14). However, Lamberton and Zervos make the observation that any points at which the payoff function is discontinuous will be part of the continuation region, and so it is possible to construct a value function that conforms with Definition 4.1. The analysis presented in this paper relies on Assumption 2.4 in the widespread use of expressions such as (17)–(20), which are applied, for example, in the proof of Lemma A.1. However the basic intuition of considering the sign of and stationary points of the functions and can still be helpful when considering these ‘staircase’ payoff functions.

There are turning points of at and , and we note that

while

These sequences mean that the solution to the two problems are very different. With there is a global maximum turning point at , and we have Case III with

Now, with we have the situation of a series of sub-intervals, as described in Remark 4.1. We have Case III in the interval , Case VI for the intervals and Case II for . To develop our understanding of the four versions of Case VI, define each jump location as . The right-hand boundary of the four intervals must be continuous fit at , while, employing (30)–(32), the left hand boundary will satisfy smooth fit (see also [7, Lemma 4]) if

If this condition is not satisfied, we will also have only continuous fit at the left hand boundary, . In the case under consideration, it can be deduced that and it is easy to establish that

Observe that the construction of Case VI means that we will have a maximum turning point of at and a maximum turning point of at with

(51)

Also, given is increasing for while is decreasing for , combined with (20) and (40), and (18) with (41), means that

(52)

and

(53)

Now, for any and , by decreasing or increasing , and will decrease. In addition, because we have maxima of and ,

(54)

(55)

and we can see that the maximum value that could possibly take on, is , while the minimum value could take on is . Similarly, there is a minimum value, , such that

(56)

and a maximum value, ,such that

(57)

As a consequence of (54)–(57), there exist mappings and such that

(58)

(59)

and

Finding a unique pair () is equivalent to showing that there exists a unique crossing point of and , where and .

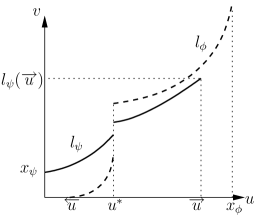

The first problem with proving this is that if the measure is atomic, meaning that could be discontinuous. In this case, there would be discontinuities in and and we could have the situation described in Figure 1, and it is ambiguous where the crossing point of and is (in respect to the second parameter). These issues do not occur if is non-atomic in .

Figure 1: The effect of an atom in at .

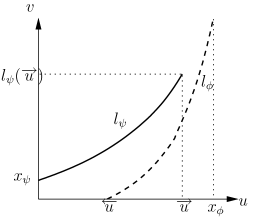

The second problem occurs if there is a significant gap between and resulting in the situation described in Figure 2, there is no actual crossing point. These issues do not occur if the boundaries and are natural, as assumed in Lempa [29, i.e. Lemma 2.1].

Figure 2: The effect of being too far from .

Lemma A.1.

Suppose that

Suppose that Assumptions 2.1,2.2,2.3 and 2.4 hold. In addition

1.

is non-atomic on , as defined above, and is a positive measure on .

2.

The following two inequalities hold:

(60)

then there exist a unique pair such that (37)–(38) are true.

Proof: Our aim is to show that there exist unique mappings (58–(59) such that

and there is a unique crossing point of and , where and , . In order to do this, let us first assume that such a and exist, and we shall first prove uniqueness.

We begin by noting that since , the points , if they exist, will be in .

Now, observe that since

then

and similarly from ,

with the inequalities being a consequence of the fact that in .

Comparing and we can see

Note that if there is a crossing of and at and with ,

since is a decreasing function while is increasing. This means that at a crossing and so if the crossing exists crosses from below . If this is the only way a crossing can occur, there can only be one such crossing.

We now show that a crossing exists. Noting that, if they cross, then crosses from below then the crossing point exists if

Let us consider the second inequality. We have that , and so if then this will hold. Now, given the definition of , will be true if and only if

with the final inequality being a consequence of the second inequality in (60).

The proof of follows symmetric arguments.

The condition (60) is sufficient, if it does hold it does not mean that the crossing point does not exist.

Remark A.1.

In the cases where and are given by functions such as confluent hypogeometric functions or cylinder parabolic functions, solving (37)–(38) may be difficult. Noting that solving (37)–(38) is equivalent to solving and we have expressions for , the approach taken here may facilitate the solution to the problem.

Acknowledgements

I would like to thank Professor Mihail Zervos for his care and inspiration. In addition I would like to thank, amongst others, Professor Damien Lamberton and the organisers of the Developments of Quantitative Finance Programme at the Isaac Newton Institute for Mathematical Sciences in Cambridge, 2005; Professor Goran Peskir, Doctor Pavel Gapeev and Professor Luis Alvarez and the organisers of the Symposium on Optimal Stopping with Applications in Manchester, January 2006; Professor Richard Stockbridge and and the organisers of the Stochastic Filtering and Control Workshop at Warwick, August 2007 for helpful comments and discussions. Finally, Catherine Donnelly has provided some helpful suggestions on the text.

References

Alvarez [2001]

L. H. R. Alvarez.

Reward functionals, salvage values, and optimal stopping.

Mathematical Methods of Operations Research, 54:315–337, 2001.

Beibel and Lerche [1997]

M. Beibel and H. R. Lerche.

A new look at optimal stopping problems related to mathematical

finance.

Statistica Sinica, 7:93–108, 1997.

Beibel and Lerche [2000]

M. Beibel and H. R. Lerche.

A note on optimal stopping of regular diffusions under random

discounting.

Theory of Probability and its Applications, 45:657–669, 2000.

Bensoussan and Lions [1982]

A. Bensoussan and J. L. Lions.

Applications of variational inequalities in stochastic

control., volume 12 of Studies in Mathematics and its Applications.

North Holland, 1982.

Borodin and Salminen [2002]

A. N. Borodin and P. Salminen.

Handbook of Brownian Motion - Facts and Formulae.

Birkhauser-Verlag, 2002.

Breiman [1968]

L. Breiman.

Probability.

Addison-Wesley, 1968.

Bronstein et al. [2005]

A. L. Bronstein, L. P. Hughston, M. R. Pistorius, and M. Zervos.

Discretionary stopping of one-dimensional Itô diffusions with a

staircase payoff function.

Journal of Applied Probability, 43:984–996, 2005.

Christensen and Irle [2011]

S. Christensen and A. Irle.

A harmonic function technique for the optimal stopping of diffusions.

Stochastics An International Journal of Probability and

Stochastic Processes, 83(4-6):347–363, 2011.

Dai et al. [2010]

M. Dai, Q. Zhang, and Q. J. Zhu.

Trend following trading under a regime switching model.

SIAM Journal on Financial Mathematics, 1:780–810,

2010.

Davis and Karatzas [1994]

M. H. A. Davis and I. Karatzas.

A deterministic approach to optimal stopping.

In F. P. Kelly, editor, Probability, Statistics and

Optimisation: A Tribute to Peter Whittle, Wiley Series in Probability and

Mathematical Statistics, pages 455–466. Wiley, 1994.

Dayanik [2008]

S. Dayanik.

Optimal stopping of linear diffusions with random discounting.

Mathematics of Operations Research, 33(3):645–661, 2008.

Dayanik and Karatzas [2003]

S. Dayanik and I. Karatzas.

On the optimal stopping problem for one-dimensional diffusions.

Stochastic Processes and their Applications, 107(2):173–212, 2003.

Dixit and Pindyck [1994]

A. K. Dixit and R. S. Pindyck.

Investment under Uncertainty.

Princeton University Press, 1994.

Dynkin [1963]

E. B. Dynkin.

Optimal choice of the stopping moment of a Markov process.

Doklady Akademii Nauk SSSR, 150:238–240, 1963.

El-Karoui [1979]

N. El-Karoui.

Les aspects probabilistes du contrôle stochastique.

In P. L. Hennequin., editor, Ecole d’Eté de Probabilités de

Saint-Flour IX-1979, Lecture notes in mathematics, 876, pages 73–238.

Springer-Verlag, 1979.

Feller [1952]

W. Feller.

The parabolic differential equations and the associated semi-groups

of transformations.

Annals of Mathematics, 55(3):468–519,

1952.

Guo and Shepp [2001]

X. Guo and L. A. Shepp.

Some optimal stopping problems with non-trivial boundaries for

pricing exotic options.

Journal of Applied Probability, 38:647–658, 2001.

Guo and Tomecek [2008]

X. Guo and P. Tomecek.

Connections between singular control and optimal switching.

SIAM Journal on Control and Optimization, 47(1):421–443, 2008.

Henderson and Hobson [2002]

V. Henderson and D. Hobson.

Real options with constant relative risk aversion.

Journal of Economic Dynamics and Control, 27(2):329–355, 2002.

Itô and McKean [1974]

K. Itô and H. P. McKean.

Diffusion Processes and their Sample Paths.

Springer-Verlag, 1974.

Johnson and Zervos [2007]

T. C. Johnson and M. Zervos.

The solution to a second order linear ordinary differential equation

with a non-homogeneous term that is a measure.

Stochastics, 2007.

Johnson and Zervos [2010]

T. C. Johnson and M. Zervos.

The explicit solution to a sequential switching problem with

non-smooth data.

Stochastics, 82(1):69–109, 2010.

Karatzas and Shreve [1991]

I. Karatzas and S. Shreve.

Brownian Motion and Stochastic Calculus.

Springer-Verlag, 1991.

ISBN 0387976558.

Karlin [1962]

S. Karlin.

Stochastic models and optimal policy for selling an asset.

In K. J. Arrow, S. Karlin, and H. Scarf, editors, Studies in

Applied Probability and Management Science. Stanford University Press, 1962.

Karlin and Taylor [1981]

S. Karlin and H. M. Taylor.

A Second Course in Stochastic Processes.

Academic Press, 1981.

Krylov [1980]

N. V. Krylov.

Controlled diffusion processes.

Springer-Verlag, 1980.

URL

Lamberton [2009]

D. Lamberton.

Optimal stopping with irregular reward functions.

Stochastic Processes and their Applications, 119(10):3253–3284, 2009.

Lamberton and Zervos [2012]

D. Lamberton and M. Zervos.

On the optimal stopping of a one-dimensional diffusion.

ArXiv e-print 1207.5491, July 2012.

Lempa [2010]

J. Lempa.

A note on optimal stopping of diffusions with a two–sided optimal

rule.

Operations Research Letters, 38(1):11–16,

2010.

Lerche and Urusov [2007]

H. R. Lerche and M. Urusov.

Optimal stopping via measure transformation: the beibel-lerche

approach.

Stochastics, 79(3–4):275–291, 2007.

McDonald and Siegel [1986]

R. McDonald and D. Siegel.

The value of waiting to invest.

The Quarterly Journal of Economics, 101(4):707–728, 1986.

Merton [1990]

R. C. Merton.

Continuous-time Finance.

Blackwell, 1990.

Rogers and Williams [1994]

L. C. G. Rogers and D. Williams.

Diffusions, Markov Processes and Martingales - Volume 2: Itô

Calculus.

Wiley, 2nd edition, 1994.

ISBN 0-471-91482-7.

Rüschendorf and Urusov [2008]

L. Rüschendorf and M. Urusov.

On a class of optimal stopping problems for diffusions with

discontinuous coefficients.

Annals of Applied Probability, 18(3):847–878, 2008.

Salminen [1985]

P. Salminen.

Optimal stopping of one-dimensional diffusions.

Mathematische Nachrichten, 124:85–101, 1985.

Shiryaev [1978]

A. N. Shiryaev.

Optimal stopping rules.

Springer-Verlag, 1978.

Shreve [2004]

S. E. Shreve.

Stochastic Calculus for Finance II: Continuous-Time Models.

Springer, 2004.

Trigeorgis [1996]

L. Trigeorgis.

Real Options: Managerial Flexibility and Strategy in Resource

Allocation.

MIT Press, 1996.