Recent advances in ambit stochastics with a view towards tempo-spatial stochastic volatility/intermittency

Abstract

Ambit stochastics is the name for the theory and applications of ambit fields and ambit processes and constitutes a new research area in stochastics for tempo-spatial phenomena. This paper gives an overview of the main findings in ambit stochastics up to date and establishes new results on general properties of ambit fields. Moreover, it develops the concept of tempo-spatial stochastic volatility/intermittency within ambit fields. Various types of volatility modulation ranging from stochastic scaling of the amplitude, to stochastic time change and extended subordination of random measures and to probability and Lévy mixing of volatility/intensity parameters will be developed. Important examples for concrete model specifications within the class of ambit fields are given.

Keywords: Ambit stochastics, random measure, Lévy basis, stochastic volatility, extended subordination, meta-times, non-semimartingales.

MSC codes: 60G10, 60G51, 60G57, 60G60,

1 Introduction

Tempo-spatial stochastic models describe objects which are influenced both by time and location. They naturally arise in various applications such as agricultural and environmental studies, ecology, meteorology, geophysics, turbulence, biology, global economies and financial markets. Despite the fact that the aforementioned areas of application are very different in nature, they pose some common challenging mathematical and statistical problems. While there is a very comprehensive literature on both time series modelling, see e.g. Hamilton (1994); Brockwell & Davis (2002), and also on modelling purely spatial phenomena, see e.g. Cressie (1993), tempo-spatial stochastic modelling has only recently become one of the most challenging research frontiers in modern probability and statistics, see Finkenstädt et al. (2007); Cressie & Wikle (2011) for textbook treatments. Advanced and novel methods from statistics, probability, and stochastic analysis are called for to address the difficulties in constructing and estimating flexible and, at the same time, parsimoniously parametrised stochastic tempo-spatial models. There are various challenging issues which need to be addressed when dealing with tempo-spatial data, starting from data collection, model building, model estimation and selection, and model validation up to prediction. This paper focuses on building a flexible, dynamic tempo-spatial modelling framework, in which we develop the novel concept of tempo-spatial stochastic volatility/intermittency which allows one to model random volatility clusters and fluctuations both in time and in space. Note that intermittency is an alternative name for stochastic volatility, used in particular in turbulence. The presence of stochastic volatility is an empirical fact in a variety of scientific fields (including the ones mentioned above), see e.g. Amiri (2009); Huang et al. (2011); Shephard & Andersen (2009). Despite its ubiquitousness and importance, however, this important quantity has so far been often overlooked in the tempo-spatial literature. Possibly this is due to the fact that stochastic volatility induces high mathematical complexity which is challenging both in terms of model building as well as for model estimation.

The concept of stochastic volatility needs to be defined with respect to a base model, which we introduce in the following. While the models should be the best realistic description of the underlying random phenomena, they also have to be treatable for further use in the design of controls, or risk evaluation, or planning of engineering equipment in the areas of application in which the tempo-spatial phenomenon is considered. Stochastic models for such tempo-spatial systems are typically formulated in terms of evolution equations, and they rely on the use of random fields. We focus on such random fields which are defined in terms of certain types of stochastic integrals with respect to random measures which can be regarded as a unifying framework which encompasses many of the traditional modelling classes. We will work with random fields denoted by with , where denotes the temporal parameter and denotes the spatial parameter, where . Typically, we have representing, for instance, longitude, latitude and height. Note that by choosing continuous parameters , we can later allow for considerable flexibility in the discretisation of the model (including in particular the possibility of irregularly spaced data). This maximises the potential for wide applications of the model. We expect that the random variables and are correlated as soon as the points and are “proximate” according to a suitable measure of distance. This idea can be formalised in terms of a set such that for all , the random variables and are correlated. The set is sometimes referred to as causality cone and more recently as ambit set, see Barndorff-Nielsen & Schmiegel (2004), describing the sphere of influence of the random variable . A concrete example of an ambit set would, for instance, be given by a light cone or a sound cone.

As the base model for a tempo-spatial object, we choose

| (1) |

where is an infinitely divisible, independently scattered random measure, i.e. a Lévy basis. Under suitable regularity conditions, our base model (1) can be linked to solutions of certain types of stochastic partial differential equations, which are often used for tempo-spatial modelling, see Barndorff-Nielsen, Benth & Veraart (2011) for details. The kernel function needs to satisfy some integrability conditions to ensure the existence of the integral, which we will study in detail in Section 2. Note that the covariance structure of the base model is fully determined by the choice of the kernel function and the set , see Barndorff-Nielsen et al. (2010). In particular, by choosing a certain bounded set , one can easily construct models which induce a covariance structure with bounded support; such models are typically sought after in applications, which feature a certain decorrelation time and distance. Under suitable regularity assumptions on and on , see Barndorff-Nielsen, Benth & Veraart (2011), the random field defined in (1) will be made stationary in time and homogeneous in space. It should be noted that in any concrete application, one needs to account for components in addition to the base model, such as a potential drift, trend and seasonality, and observation error on the data level.

One of the key questions we try to answer in this paper is the following one: How can stochastic volatility/intermittency be introduced in our base model (1)? We propose four complementary methods for tempo-spatial volatility modulation. First, stochastic volatility can be introduced by stochastically changing the amplitude of the Lévy basis . This can be achieved by adding a stochastic integrand to the base model. This method has frequently been used in the purely temporal case to account for volatility clusters. In the tempo-spatial case, one needs to establish a suitable stochastic integration theory, which allows for stochastic integrands in the form of random fields. Moreover, suitable models for tempo-spatial stochastic volatility fields need to be developed.

In the purely temporal, examples typically used to model stochastic volatility are e.g. constant elasticity of variance processes, in particular, square root diffusions, see Cox (1975); Cox et al. (1985), Ornstein-Uhlenbeck (OU) processes, see Uhlenbeck & Ornstein (1930) and more recently Barndorff-Nielsen & Shephard (2001), and supOU processes, see Barndorff-Nielsen (2000); Barndorff-Nielsen & Stelzer (2011). Second, stochastic volatility can be introduced by extended subordination of the Lévy basis. This concept can be viewed as an extension of the concept of stochastic time change as developed by Bochner (1949), see also Veraart & Winkel (2010) for further references, to a tempo-spatial framework. Last, volatility modulation can be achieved by randomising a volatility/intensity parameter of the Lévy basis . Here we will study both probability mixing and the new concept of Lévy mixing, which has recently been developed by Barndorff-Nielsen, Perez-Abreu & Thorbjørnsen (2012). We will show how these two mixing concepts can be used to account for stochastic volatility/intermittency.

Altogether, this paper contributes to the area of ambit stochastics, which is the name for the theory and application of ambit fields and ambit processes. Ambit stochastics is a new field of mathematical stochastics that has its origin in the study of turbulence, see e.g. Barndorff-Nielsen & Schmiegel (2004), but is in fact of broad applicability in science, technology and finance, in relation to modelling of spatio-temporal dynamic processes. E.g. important applications of ambit stochastics include modelling turbulence in physics, see e.g. Barndorff-Nielsen & Schmiegel (2004, 2009); Hedevang (2012), modelling tumour growth in biology, see Barndorff-Nielsen & Schmiegel (2007); Jónsdóttir et al. (2008), and applications in financial mathematics, see Barndorff-Nielsen, Benth & Veraart (2012); Veraart & Veraart (2012); Barndorff-Nielsen et al. (2010).

The outline for the remainder of this article is as follows. Section 2 reviews the concept of Lévy bases and integration with respect to Lévy bases, where the focus is on the integration theories developed by Rajput & Rosinski (1989) and Walsh (1986). Integrals with respect to Lévy bases are then used to establish the notion for our base model (1) and for general ambit fields and ambit processes in Section 3. In addition to reviewing the general framework of ambit fields, we establish new smoothness and semimartingale conditions for ambit fields. An important sub-class of ambit fields – the so-called trawl processes, which constitute a class of stationary infinitely divisible stochastic processes – are then presented in Section 4. Section 5 focuses on volatility modulation and establishes four complementary concepts which can be used to model tempo-spatial stochastic volatility/intermittency: Stochastic scaling of the amplitude through a stochastic integrand, time change and extended subordination of a random measure, and probability and Lévy mixing. Finally, Section 6 concludes and gives an outlook on future research.

2 Background

Ambit fields and ambit processes are constructed from so-called Lévy bases. We will now review the definition and key properties of such Lévy bases and then describe how stochastic integrals can be defined with respect to Lévy bases.

2.1 Background on Lévy bases

Our review is based on the work by Rajput & Rosinski (1989); Pedersen (2003), where detailed proofs can be found.

Throughout the paper, we denote by a probability space. Also, let denote a Lebesgue-Borel space where denotes a Borel set in for a , e.g. often we choose . Moreover is the Borel -algebra on and denotes the Lebesgue measure. In addition, we define

which is the subset of that contains sets which have bounded Lebesgue measure. Note that since is -finite, we can deduce that , see Peccati & Taqqu (2008, p. 399). Also, the set is closed under finite union, relative complementation, and countable intersection and is therefore a -ring.

2.1.1 Random measures

Random measures play a key role in ambit stochastics, hence we start off by recalling the definition of a (full) random measure.

Definition 1.

-

1.

By a random measure on we mean a collection of -valued random variables such that for any sequence of disjoint elements of satisfying we have a.s..

-

2.

By a full random measure on we mean a random object whose realisations are measures on a.s..

Note here that a realisation of a random measure is in general not an ordinary signed measure since it does not necessarily have finite variation. That is why we also introduced the term of a full random measure. Other articles or textbooks would sometimes call the quantity we have defined as a random measure as random noise to stress that it might not be a (signed) measure, see Samorodnitsky & Taqqu (1994, p. 118) for a discussion of this aspect.

In some applications, we work with stationary random measures, which are defined as follows.

Definition 2.

A (full) random measure on is said to be stationary if for any and any finite collection of elements (of ) of the random vector

has the same law as .

The above definition ensures that a random measure is stationary in all components. One could also study stationarity in the individual components separately.

2.1.2 Lévy bases

In this paper, we work with a special class of random measures, called Lévy bases. Before we can define them, we define independently scattered random measures.

Definition 3.

A random measure on is independently scattered if for any sequence of disjoint elements of , the random variables are independent.

Recall the definition of infinite divisibility of a distribution.

Definition 4.

The law of a random variable on is infinitely divisible (ID) if for any , there exists a law on such that , where denotes the -fold convolution of with itself.

In the following, we are interested in ID random measures, which we define now.

Definition 5.

A random measure on is said to be infinitely divisible if for any finite collection of elements of the random vector is infinitely divisible.

Let us study one relevant example.

Example 1.

Assume that is an absolutely continuous full random measure on with a density and suppose that the stochastic process is non-negative and infinitely divisible. Then is an infinitely divisible full random measure.

Now we can give the definition of a Lévy basis.

Definition 6.

-

1.

A Lévy basis on is an independently scattered, infinitely divisible random measure.

-

2.

A homogeneous Lévy basis on is a stationary, independently scattered, infinitely divisible random measure.

2.1.3 Lévy-Khintchine formula and Lévy-Itô decomposition

Since a Lévy basis is ID, it has a Lévy-Khintchine representation. I.e. let and , then

| (2) | ||||

where, according to Rajput & Rosinski (1989, Proposition 2.1 (a)), is a signed measure on , is a measure on , and is the generalised Lévy measure, i.e. is a Lévy measure on for fixed and a measure on for fixed .

Next, we define the control measure as introduced in Rajput & Rosinski (1989, Proposition 2.1 (c), Definition 2.2).

Definition 7.

Let be a Lévy basis with Lévy-Khintchine representation (2). Then, the measure is defined by

| (3) |

where denotes the total variation. The extension of the measure to a -finite measure on is called the control measure measure of .

Based on the control measure we can now characterise the generalised Lévy measure further, see Rajput & Rosinski (1989, Lemma 2.3, Proposition 2.4). First of all, we define the Radon-Nikodym derivatives of the three components of , which are given by

| (4) |

Hence, we have in particular that . Without loss of generality we can assume that is a Lévy measure for each fixed and hence we do so in the following.

Definition 8.

We call a characteristic quadruplet (CQ) associated with a Lévy basis on provided the following conditions hold:

-

1.

Both and are functions on , where is restricted to be non-negative.

-

2.

For fixed , is a Lévy measure on , and, for fixed , it is a measurable function on .

-

3.

The control measure is a measure on such that is a (possibly signed) measure on , is a measure on and is a Lévy measure on for fixed .

We have seen that every Lévy basis on determines a CQ of the form . And, conversely, every CQ satisfying the conditions in Definition 8 determines, in law, a Lévy basis on .

In a next step, we relate the notion of Lévy bases and CQs to the concept of Poisson random measures and their compensators.

Definition 9.

A Lévy basis on is dispersive if its control measure satisfies for all .

For a dispersive Lévy basis on with characteristic quadruplet there is a modification with the same characteristic quadruplet which has following Lévy-Itô decomposition:

| (5) |

for and for a Gaussian basis (with characteristic quadruplet , i.e. ), and a Poisson basis (independent of ) with compensator where , cf. Pedersen (2003) and Barndorff-Nielsen & Stelzer (2011, Theorem 2.2)

It is also possible to write (5) in infinitesimal form by

| (6) |

This is particularly useful in the context of the Lévy-Khintchine representation, which can then also be expressed in infinitesimal form by

| (7) | ||||

where denotes the Levy seed of at . Note that is defined as the infinitely divisible random variable having Lévy-Khintchine representation

| (8) |

Remark 1.

We can associate a Lévy process with any Lévy seed. In particular, let denote the Lévy seed of at . Then, denotes the Lévy process generated by , which is defined as the Lévy process whose law is determined by .

Definition 10.

Let denote a Lévy basis on with CQ given by .

-

1.

If does not depend on , we call factorisable.

-

2.

If is factorisable and if is proportional to the Lebesgue measure and and do not depend on , then is called homogeneous. In that case we write for a positive constant and where denotes the Lebesgue measure.

In order to simplify the exposition, we will throughout this paper assume that in the case of a homogeneous Lévy basis the constant is set to 1, i.e. the measure is given by the Lebesgue measure.

2.1.4 Examples of Lévy bases

Let us study some examples of Lévy bases on with CQ .

Example 2 (Gaussian Lévy basis).

When , then constitutes a Gaussian Lévy basis with , for . If, in addition, is homogeneous, then .

Example 3 (Poisson Lévy basis).

When and and , where denotes the Dirac measure with point mass at 1 and is the intensity function, then constitutes a Poisson Lévy basis. If, in addition, is factorisable, i.e. does not depend on , then , for all .

Example 4 (Gamma Lévy basis).

Suppose that , and the (generalised) Lévy measure is of the form , where . In that case, we call the corresponding Lévy basis a gamma Lévy basis. If, in addition, is factorisable, i.e. the function does not depend on the parameter , then has a gamma law for all .

Example 5 (Inverse Gaussian Lévy basis).

Suppose that , and the (generalised) Lévy measure is of the form , where . Then we call the corresponding Lévy basis an inverse Gaussian Lévy basis. If, in addition, is factorisable, i.e. the function does not depend on the parameter , then has an inverse Gaussian law for all .

Example 6 (Lévy process).

If , i.e. is a Lévy basis on , then , is a Lévy process.

2.2 Integration concepts with respect to a Lévy basis

In order to build relevant models based on Lévy bases, we need a suitable integration theory. In the following, we will briefly review the integration theory developed by Rajput & Rosinski (1989) and also the one by Walsh (1986), and we refer to Barndorff-Nielsen, Benth & Veraart (2011) for a detailed overview on integration concepts with respect to Lévy bases, see also Dalang & Quer-Sardanyons (2011) for a related review and Basse-O’Connor et al. (2012) for details on integration with respect to multiparameter processes with stationary increments.

2.2.1 The integration concept by Rajput & Rosinski (1989)

According to Rajput & Rosinski (1989, p.460), integration of suitable deterministic functions with respect to Lévy bases can be defined as follows. First define an integral for simple functions:

Definition 11.

Let be a Lévy basis on . Define a simple function on , i.e. let , where , for , are disjoint. Then, one defines the integral, for every , by

The integral for general measurable functions can be derived by a limit argument.

Definition 12.

Let be a Lévy basis on . A measurable function is called -measurable if there exists a sequence of simple function as in Definition 11, such that

-

•

a.e. (i.e. -a.e., where is the control measure of ),

-

•

for every , the sequence of simple integrals converges in probability, as .

For integrable measurable functions, define

Rajput & Rosinski (1989) have pointed out that the above integral is well-defined in the sense that it does not depend on the approximating sequence . Also, the necessary and sufficient conditions for the existence of the integral can be expressed in terms of the characteristics of and can be found in Rajput & Rosinski (1989, Theorem 2.7), which says the following. Let be a measurable function. Let be a Lévy basis with CQ . Then is integrable w.r.t. if and only if the following three conditions are satisfied:

| (9) |

where for ,

Note that such integrals have been defined for deterministic integrands. However, in the context of ambit fields, which we will focus on in this paper, we typically encounter stochastic integrands representing stochastic volatility, which tends to be present in most applications we have in mind. Since we often work under the independence assumption that the stochastic volatility and the Lévy basis are independent, it has been suggested to work with conditioning to extend the definition by Rajput & Rosinski (1989) to allow for stochastic integrands. An alternative concept, which directly allows for stochastic integrands which can be dependent of the Lévy basis, is the integration concept by Walsh (1986), which we study next.

2.2.2 Integration w.r.t. martingale measures introduced by Walsh (1986)

The integration theory due to Walsh (1986) can be regarded as Itô integration extended to random fields. In the following we will present the integration theory on a bounded domain and comment later on how one can extend the theory to the case of an unbounded domain.

Here we treat time and space separately, which allows us to work with a natural ordering (introduced by time) and to relate the integrals w.r.t. to Lévy bases to martingale measures. In the following, we denote by a bounded Borel set in for a (where ) and denotes the Borel -algebra on . Since is bounded, we have in fact .

Let denote a Lévy basis on for some . For any and , we define

Here is a measure-valued process, and for a fixed set , is an additive process in law. In the following, we want to use the as integrators as in Walsh (1986). In order to do that, we work under the square-integrability assumption, i.e.:

- Assumption (A1):

-

For each , we have that .

In the following, we will, unless otherwise stated, work without loss of generality under the zero-mean assumption on , i.e.

- Assumption (A2):

-

For each , we have that .

Next, we define the filtration by

| (10) |

and where denotes the -null sets of . Note that is right-continuous by construction. One can show that under the assumptions (A1) and (A2) and for fixed , is a (square-integrable) martingale with respect to the filtration . Note that these two properties together with the fact that a.s. ensure that is a martingale measure with respect to in the sense of Walsh (1986). Furthermore, we have the following orthogonality property: If with , then and are independent. Martingale measures which satisfy such an orthogonality property are referred to as orthogonal martingale measures by Walsh (1986), see also Barndorff-Nielsen, Benth & Veraart (2011) for more details. Note that orthogonal martingale measure are worthy, see Walsh (1986, Corollary 2.9), a property which makes them suitable as integrators. For such orthogonal martingale measures, Walsh (1986) introduces their covariance measure by

| (11) |

for . Note that is a positive measure and is used by Walsh (1986) when defining stochastic integration with respect to .

Walsh (1986) defines stochastic integration in the following way. Let be an elementary random field , i.e. it has the form

| (12) |

where , , is bounded and -measurable, and . For such elementary functions, the stochastic integral with respect to can be defined as

| (13) |

for every . It turns out that the stochastic integral becomes a martingale measure itself in (for fixed ). Clearly, the above integral can easily be generalised to allow for integrands given by simple random fields, i.e. finite linear combinations of elementary random fields. Let denote the set of simple random fields and let the predictable -algebra be the -algebra generated by . Then we call a random field predictable provided it is -measurable. The aim is now to define stochastic integrals with respect to where the integrand is given by a predictable random field.

In order to do that Walsh (1986) defines a norm on the predictable random fields by

| (14) |

which determines the Hilbert space , which is the space of predictable random fields with , and he shows that is dense in . Hence, in order to define the stochastic integral of , one can choose an approximating sequence such that as . Clearly, for each , is a Cauchy sequence in , and thus there exists a limit which is defined as the stochastic integral of .

Then, this stochastic integral is again a martingale measure and satisfies the following Itô-type isometry:

| (15) |

see (Walsh, 1986, Theorem 2.5) for more details.

2.2.3 Relation between the two integration concepts

The relation between the two different integration concept has been discussed in Barndorff-Nielsen, Benth & Veraart (2011, pp. 60–61), hence we only mention it briefly here.

Note that the Walsh (1986) theory defines the stochastic integral as the -limit of simple random fields, whereas Rajput & Rosinski (1989) work with the -limit. Barndorff-Nielsen, Benth & Veraart (2011) point out that deterministic integrands, which are integrable in the sense of Walsh, are thus also integrable in the Rajput and Rosinski sense since the control measure of Rajput & Rosinski (1989) and the covariance measure of Walsh (1986) are equivalent.

3 General aspects of the theory of ambit fields and processes

In the following we will show how stochastic processes and random fields can be constructed based on Lévy bases, which leads us to the general framework of ambit fields. This section reviews the concept of ambit fields and ambit processes. For a detailed account on this topic see Barndorff-Nielsen, Benth & Veraart (2011) and Barndorff-Nielsen & Schmiegel (2007).

3.1 The general framework

The general framework for defining an ambit process is as follows. Let with denoting a stochastic field in space-time . In most applications, the space is chosen to be for or . Let denote a curve in . The values of the field along the curve are then given by . Clearly, denotes a stochastic process. Further, the stochastic field is assumed to be generated by innovations in space-time with values which are supposed to depend only on innovations that occur prior to or at time and in general only on a restricted set of the corresponding part of space-time. I.e., at each point , the value of is only determined by innovations in some subset of (where ), which we call the ambit set associated to . Furthermore, we refer to and as an ambit field and an ambit process, respectively.

In order to use such general ambit fields in applications, we have to impose some structural assumptions. More precisely, we will define as a stochastic integral plus a drift term, where the integrand in the stochastic integral will consist of a deterministic kernel times a positive random variate which is taken to express the volatility of the field . More precisely, we think of ambit fields as being defined as follows.

Definition 13.

Using the notation introduced above, an ambit field is defined as a random field of the form

| (16) |

provided the integrals exist, where , and are ambit sets, and are deterministic functions, is a stochastic field referred to as volatility or intermittency, is also a stochastic field, and is a Lévy basis.

Remark 2.

Note that compared to the base model (1) we introduced in the Introduction, the ambit field defined in (16) also comes with a drift term and stochastic volatility introduced in form of a stochastic integrand. In Section 5, we will describe in detail how such a stochastic volatility field can be specified and what kind of complementary routes can be taken in order to allow for stochastic volatility clustering.

The corresponding ambit process along the curve is then given by

| (17) |

where and .

In Section 3.2, we will formulate the suitable integrability conditions which guarantee the existence of the integrals above.

Of particular interest in many applications are ambit processes that are stationary in time and nonanticipative and homogeneous in space. More specifically, they may be derived from ambit fields of the form

| (18) |

Here the ambit sets and are taken to be homogeneous and nonanticipative, i.e. is of the form where only involves negative time coordinates, and similarly for . In addition, and are chosen to be stationary in time and space and to be homogeneous.

3.2 Integration for general ambit fields

Ambit fields have initially been defined for deterministic integrands using the Rajput & Rosinski (1989) integration concept. Their definition could then be extended to allow for stochastic integrands which are independent of the Lévy basis by a conditioning argument. As discussed before, the integration framework developed by Walsh (1986) has the advantage that it allows for stochastic integrands which are potentially dependent of the Lévy basis and enables us to study dynamic properties (such as martingale properties). Let us explain in more detail how the Walsh (1986) integration concept can be used to define ambit fields using an Itô-type integration concept.

One concern regarding the applicability of the Walsh (1986) framework to ambit fields might be that general ambit sets are not necessarily bounded, and we have only presented the Walsh (1986) concept for a bounded domain. However, the stochastic integration concept reviewed above can be extended to unbounded ambit sets using standard arguments, cf. Walsh (1986, p. 289). Also, as pointed out in Walsh (1986, p. 292), it is possible to extend the Walsh (1986) integration concept beyond the -framework, cf. Walsh (1986, p. 292).

Note that the classical Walsh (1986) framework works under the zero mean assumption, which might not be satisfied for general ambit fields. However, we can always define a new Lévy basis by setting , which clearly has zero mean. Then we can define the Walsh (1986) integral w.r.t. , and we obtain an additional drift term which needs to satisfy an additional integrability condition.

However, the main point we need to address is the fact that the integrand in the ambit field does not seem to comply with the structure of the integrand in the Walsh-theory. More precisely, for ambit fields with ambit sets , we would like to define Walsh-type integrals for integrands of the form

| (19) |

The original Walsh’s integration theory covers integrands which do not depend on the time index . Clearly, the integrand given in (19) generally exhibits -dependence due to the choice of the ambit set and due to the deterministic kernel function .

Suppose we are in the simple case where the ambit set can be represented as , where does not depend on , and where the kernel function does not depend on , i.e. . Then the Walsh-theory is directly applicable, and provided the integrand is indeed Walsh-integrable, then (for fixed and fixed ) the process

is a martingale.

Note that the -dependence (and also the additional -dependence) for general integrands in the ambit field is in the deterministic part of the integrand only, i.e. in . Now in order to allow for time - (and -) dependence in the integrand, we can define the integrals in the Walsh sense for any fixed and for fixed . Note that we treat as an additional parameter which does not have an influence on the structural properties of the integral as a stochastic process in .

It is clear that in the case of having -dependence in the integrand, the resulting stochastic integral is, in general, not a martingale measure any more. However, the properties of adaptedness, square-integrability and countable additivity carry over to the process

(for fixed ) since it is the -limit of a stochastic process with the above mentioned properties.

In order to ensure that the ambit fields (as defined in (16)) are well-defined (in the Walsh-sense), throughout the rest of the paper we will work under the following assumption:

Assumption 1.

Let denote a Lévy basis on , where denotes a not necessarily bounded Borel set in for some . Define the new Lévy basis . We extend the definition of the covariance measure of , see (11), to an unbounded domain and, next, we define a Hilbert space with norm as in (14) (extended to an unbounded domain) and, hence, we have an Itô isometry of type (15) extended to an unbounded domain. We assume that, for fixed and ,

satisfies

-

1.

,

-

2.

.

-

3.

Remark 3.

Note that alternatively, we could work with the càdlàg elementary random fields

where is assumed to be -adapted and the remaining notation is as in (12). Next, one can construct a -algebra from the corresponding simple random fields and one would then define the stochastic integral for , since clearly adaptedness and the càdlàg property of implies predictability of .

3.3 Cumulant function for stochastic integrals w.r.t. a Lévy basis

Next we study some of the fundamental properties of ambit fields. Throughout this subsection, we work under the following assumption:

Assumption 2.

The stochastic fields and are independent of the Lévy basis .

Now we have all the tools at hand which are needed to compute the conditional characteristic function of ambit fields defined in (16) where and are assumed independent and where we condition on the -algebra which is generated by the history of , i.e.

Proposition 1.

Assume that Assumption 2 holds. Let denote the conditional cumulant function when we condition on the volatility field . The conditional cumulant function of the ambit field defined by (16) is given by

| (20) | ||||

where denotes the Lévy seed and is the control measure associated with the Lévy basis , cf. (8) and (3).

Proof.

The proof of the Proposition is an immediate consequence of Rajput & Rosinski (1989, Proposition 2.6). ∎

Corollary 1.

In the case where is a homogeneous Lévy basis, equation (LABEL:CharFct) simplifies to

3.4 Second order structure of ambit fields

Next we study the second order structure of ambit fields. Throughout the Section, let

| (21) |

where is independent of , i.e. Assumption 2 holds, and is the Lévy seed associated with .

Proposition 2.

Let and let be an ambit field as defined in (21). The second order structure is then as follows. The means are given by

The variances are given by

where . The covariances are given by

Proof.

From the conditional cumulant function (LABEL:CharFct), we can easily deduce the second order structure conditional on the stochastic volatility. Integrating over and using the law of total variance and covariance leads to the corresponding unconditional results. ∎

Note that it is straightforward to generalise the above results to allow for an additional drift term as in (16).

The second order structure provides us with some valuable insight into the autocorrelation structure of an ambit field. Knowledge of the autocorrelation structure can help us to study smoothness properties of an ambit field, as we do in the following section. Also, from a more practical point of view, we could think of specifying a fully parametric model based on the ambit field. Then the second order structure could be used e.g. in a (quasi-) maximum-likelihood set-up to estimate the model parameters.

3.5 Smoothness conditions

Let us study sufficient conditions which ensure smoothness of an ambit field.

3.5.1 Some related results in the literature

In the purely temporal (or null-spatial) case, which we will discuss in more detail in Section 3.7, smoothness conditions for so-called Volterra processes have been studied before. In particular, Decreusefond (2002) shows that under mild integrability assumptions on a progressively measurable stochastic volatility process, the sample-paths of the volatility modulated Brownian-driven Volterra process are a.s. Hölder-continuous even for some singular deterministic kernels. Note that Decreusefond (2002) does not use the term stochastic volatility in his article, but the stochastic integrand he considers could be regarded as a stochastic volatility process. Also, Mytnik & Neuman (2011) study sample path properties of Volterra processes.

In the tempo-spatial context, or generally for random fields, smoothness conditions have been discussed in detail in the literature. For textbook treatments see e.g. Adler (1981), Adler & Taylor (2007) and Azaïs & Wschebor (2009). Important articles in this context include the following ones. Kent (1989) formulates sufficient conditions on the covariance function of a stationary real-valued random field which ensure sample path continuity.

Rosinski (1989) studies the relationship between the sample-path properties of an infinitely divisible integral process and the properties of the sections of the deterministic kernel. The study is carried out under the assumption of absence of a Gaussian component. In particular, he shows that various properties of the section are inherited by the paths of the process, which include boundedness, continuity, differentiability, integrability and boundedness of th variation.

Marcus & Rosinski (2005) extend the previous results to derive sufficient conditions for boundedness and continuity for stochastically continuous infinitely divisible processes, without Gaussian component.

3.5.2 Sufficient condition on the covariance function

In the following, we write

where the covariance is given as in Proposition 2. We can apply the key results derived in Kent (1989) to ambit fields.

Let and and . For each we assume that is -times continuously differentiable with respect to for a . We write for the polynomial of degree which is obtained from a Taylor expansion of about for each . In the following, we denote by the Euclidean norm.

Proposition 3.

For each suppose that is -times continuously differentiable with respect to and that there exists a constant such that

| (22) |

as , where the supremum is computed over being in each compact subset of . Then there exists a version of the random field which has almost surely continuous sample paths.

Proof.

The result is a direct consequence of Kent (1989, Theorem 1 and Remark 6). ∎

Remark 4.

3.6 Semimartingale conditions

Next we derive sufficient conditions which ensure that an ambit field is a semimartingale in time. This is interesting since in financial applications we typically want to stay within the semimartingale framework whereas in applications to turbulence one typically focuses on non-semimartingales.

We will see that a sufficient condition for a semimartingale is linked to a smoothness condition on the kernel function. When studying the semimartingale condition, we focus on ambit sets which factorise as , which is in line with the Walsh (1986)-framework. We start with a preliminary Lemma.

Lemma 1.

Let be a Lévy basis satisfying (A1) and (A2) and be a predictable stochastic volatility field which is integrable w.r.t. . Then

| (23) |

is an orthogonal martingale measure.

Proof.

See Walsh (1986, p. 296) for a proof of the lemma above. ∎

Assumption 3.

Assume that the deterministic function is differentiable (in the second component) and denote by the derivative with respect to the second component. Then for we have the representation

| (24) |

provided that exists. Further, we assume that both components in the representation (24) are Walsh (1986)-integrable w.r.t. and and satisfy , , for .

Proposition 4.

Then is a semimartingale with representation

| (25) |

Clearly, the first term in representation (25) is a martingale measure in the sense of Walsh and the second term is a finite variation process.

Proof.

The result follows from the stochastic Fubini theorem for martingale measures, see Walsh (1986, Theorem 2.6). In the following, we check that the conditions of the stochastic Fubini theorem are satisfied. Let denote a finite measure space. Concretely, take and . Note that has finite first derivative at all points, hence its derivative is -measurable. Also, the indicator function is -measurable since the corresponding interval is an element of . Overall we have that the function

is -measurable and

where is the covariance measure of . Then

∎

3.7 The purely-temporal case: Volatility modulated Volterra processes

The purely temporal, i.e. the null-spatial, case of an ambit field has been studied in detail in recent years. Here we denote by a Lévy process on . Then, the null–spatial ambit field is in fact a volatility modulated Lévy-driven Volterra () process denoted by , where

| (26) |

where is a constant, and are are real–valued measurable function on , such that the integrals above exist with for , and and are càdlàg processes.

Of particular interest, are typically semi–stationary processes, i.e. the case when the kernel function depends on and only through the difference . This determines the class of Lévy semistationary processes (), see Barndorff-Nielsen, Benth & Veraart (2012). Specifically,

| (27) |

and are non-negative deterministic functions on with for . Note that an process is stationary as soon as and are stationary processes. In the case that is a Brownian motion, we call a Brownian semistationary () process, see Barndorff-Nielsen & Schmiegel (2009).

The class of processes has been used by Barndorff-Nielsen & Schmiegel (2009) to model turbulence in physics. In that context, intermittency, which is modelled by , plays a key role, which has triggered detailed research on the question of how intermittency can be estimated non-parametrically. Recent research, see e.g. Barndorff-Nielsen et al. (2009); Barndorff-Nielsen, Corcuera & Podolskij (2011, 2012), has developed realised multipower variation and related concepts to tackle this important question.

The class of processes has subsequently been found to be suitable for modelling energy spot prices, see Barndorff-Nielsen, Benth & Veraart (2012); Veraart & Veraart (2012). Moreover, Barndorff-Nielsen, Benth, Pedersen & Veraart (2012) have recently developed an anticipative stochastic integration theory with respect to processes.

4 Illustrative example: Trawl processes

Ambit fields and processes constitute a very flexible class for modelling a variety of tempo-spatial phenomena. This Section will focus on one particular sub-class of ambit processes, which has recently been used in application in turbulence and finance.

4.1 Definition and general properties

Trawl processes are stochastic processes defined in terms of tempo-spatial Lévy bases. They have recently been introduced in Barndorff-Nielsen (2011) as a class of stationary infinitely divisible stochastic processes.

Definition 14.

Let be a homogeneous Lévy basis on for . Then, using the same notation as before,

Further, for an , we define . Then

| (28) |

defines the trawl process associated with the Lévy basis and the trawl .

The assumption in the definition above ensures the existence of the integral in (28) as defined by Rajput & Rosinski (1989).

Remark 6.

If , then the trawl process belongs to the class of ambit processes.

The intuition and also the name of the trawl process comes from the idea that we have a certain tempo-spatial set – the trawl – which is relevant for our object of interest. I.e. the object of interest at time is modelled as the Lévy basis evaluated over the trawl . As time progresses, we pull along the trawl (like a fishing net) and hence obtain a stochastic process (in time ). For the time being, we have in mind that the shape of the trawl does not change as time progresses, i.e. that the process is stationary. This assumption can be relaxed as we will discuss in Section 5.

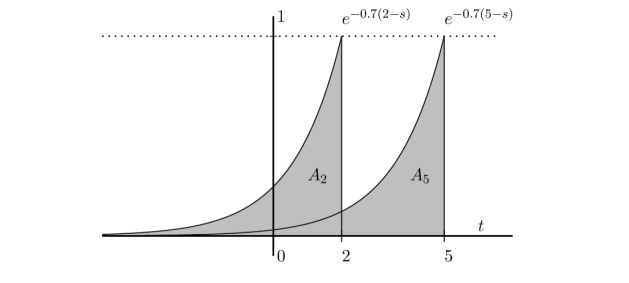

Example 7.

Let and suppose that the trawl is given by . Figure 1 illustrates the basic framework for such a process. It depicts the trawl at different times . The value of the process at time is then determined by evaluating the corresponding Lévy basis over the trawl .

4.2 Cumulants and correlation structure

From Barndorff-Nielsen (2011) we know that the trawl process defined above is a strictly stationary stochastic process, and we can easily derive the cumulant transform of a trawl process, which is given by

| (29) |

From the equation (29), we see immediately that the law of the trawl process is infinitely divisible since the corresponding Lévy seed has infinitely divisible law.

Remark 7.

We can now easily derive the cumulants of the trawl process which are given by , for , provided they exist. In particular, the mean and variance are given by

Marginally, we see that the precise shape of the trawl does not have any impact on the distribution of the process. The quantity which matters here is the size, i.e. the Lebesgue measure, of the trawl. So two different specifications of the ambit set, which have the same size, are not identified based on the marginal distribution only.

However, we will see that the shape of the trawl determines the autocorrelation function. More precisely, the autocorrelation structure is given as follows. Let , then

| (30) |

For the autocorrelation, we get

4.3 Lévy-Itô decomposition for trawl processes

In the following we study some of the sample path properties of trawl processes. First of all, we study a representation result for trawl process , where we split the process into a drift part, a Gaussian part and a jump part in a similar fashion as in the classical Lévy-Itô decomposition. Recall that is a homogeneous Lévy basis on . In the following, denotes the one dimensional temporal variable and denotes the -dimensional spatial variable.

From the Lévy-Itô decomposition, see (5), we get the following representation result for the trawl process defined in (28), i.e.

| (31) | ||||

where and and .

Example 8.

Suppose the trawl process is defined based on a Lévy basis with characteristic quadruplet . Then it can be written as

Assume further that and that the trawl is given by , for a positive constant . Then , hence and the autocorrelation function is given by , for .

4.4 Generalised cumulant functional

We have already studied the cumulant function of Lévy bases and ambit fields. Here, we will in addition focus on the more general cumulant functional of a trawl process, which sheds some light on important properties of trawl processes.

Definition 15.

Let denote a stochastic process and let denote any non-random measure such that

where the integral should exist a.s.. The generalised cumulant functional of w.r.t. is defined as

When we compute the cumulant functional for a trawl process, we obtain the following result.

Proposition 5.

Let denote a trawl process and let denote any non-random measure such that , a. s.. Given the trawl , we will further assume that for all ,

and that is integrable with respect to the Lévy basis . Then the cumulant function of is given by

| (32) | ||||

where is the measure on obtained by lifting the Lebesgue measure on to by the mapping .

Proof.

An application of Fubini’s theorem (see e.g. Barndorff-Nielsen & Basse-O’Connor (2011)) yields

From this we find that the cumulant function of , i.e. the generalised cumulant functional of w.r.t. , is given by

Note that the latter part, i.e. the jump part of , can be recast as

where is the measure defined as above. Then the result follows. ∎

In the following, we mention three relevant choices of the measure . Let denote the Dirac measure at . We start with a very simple case:

Example 9.

Suppose for a fixed . Hence

and clearly, is integrable with respect to . Then

This is exactly the result we derived in Section 4.2 above. More interesting is the case when is given by a linear combination of different Dirac measures, since this allows us to derive the joint finite dimensional laws of the trawl process and not just the distribution for fixed .

Example 10.

Finally, another case of interest is the integrated trawl process, which we study in the next example.

Example 11.

Let for an interval of . Then (32) determines the law of .

Remark 8.

The last example is particularly relevant if the trawl process is for instance used for modelling stochastic volatility. Note that such an application is feasible since the trawl process is stationary and we can formulate assumptions which would ensure the positivity of the process as well (e.g. if we work with a Lévy subordinator as the corresponding Lévy seed). In that context, integrated volatility is a quantity of key interest.

4.5 The increment process

Finally, we focus on the increments of a trawl process. Note that whatever the type of trawl, we have the following representation for the increments of the process for ,

| (33) |

Due to the independence of and , we get the following representation for the cumulant function of the returns

| (34) | ||||

4.6 Applications of trawl processes

Trawl processes constitute a class of stationary infinitely divisible stochastic processes and can be used in various applications. E.g. we already pointed out above that they could be used for modelling stochastic volatility or intermittency. In a recent article by Barndorff-Nielsen, Lunde, Shephard & Veraart (2012), integer-valued trawl processes have been used to model count data or integer-valued data which are serially dependent. Speaking generally, trawl processes can be viewed as a flexible class of stochastic processes which can be used to model stationary time series data, where the marginal distribution and the autocorrelation structure can be modelled independently from each other.

5 Tempo-spatial stochastic volatility/intermittency

Stochastic volatility/intermittency plays a key role in various applications including turbulence and finance. While a variety of purely temporal stochastic volatility/intermittency models can be found in the literature, suitable tempo-spatial stochastic volatility/intermittency models still need to be developed.

Volatility modulation within the framework of an ambit field can be achieved by four complementary methods: By introducing a stochastic integrand (the term in the definition of an ambit field), or by (extended) subordination or by probability mixing or Lévy mixing. We will discuss all four methods in the following.

5.1 Volatility modulation via a stochastic integrand

Stochastic volatility in form of a stochastic integrand has already been included in the initial definition of an ambit field, see (16). The interesting aspect, which we have not addressed yet, is how a model for the stochastic volatility field can be specified in practice. We will discuss several relevant choices in more detail in the following.

There are essentially two approaches which can be used for constructing a relevant stochastic volatility field: Either one specifies the stochastic volatility field directly as a random field (e.g. as another ambit field), or one starts from a purely temporal (or spatial) stochastic volatility process and then generalises the stochastic process to a random field in a suitable way. In the following, we will present examples of both types of construction.

5.1.1 Kernel-smoothing of a Lévy basis

First, we focus on the modelling approach where we directly specify a random field for the volatility field. A natural starting point for modelling the volatility is given by kernel-smoothing of a homogeneous Lévy basis – possibly combined with a (nonlinear) transformation to ensure positivity. For instance, let

| (35) |

where is a homogeneous Lévy basis independent of , is an integrable kernel function satisfying for and is a continuous, non-negative function. Note that defined by (35) is stationary in the temporal dimension. As soon as for some function in (35), then the stochastic volatility is both stationary in time and homogeneous in space.

Clearly, the kernel function determines the tempo-spatial autocorrelation structure of the volatility field.

Let us discuss some examples next.

Example 12 (Tempo-spatial trawl processes).

Suppose the kernel function is given by

where . Further, let ; hence is a homogeneous and nonanticipative ambit set. Then

Note that the random field can be regarded as a tempo-spatial trawl process.

Example 13.

Let

for an integrable kernel function and where . Further, let . Then

| (36) |

which is a transformation of an ambit field (without stochastic volatility).

Let us look at some more concrete examples for the stochastic volatility field.

Example 14.

A rather simple specification is given by choosing to be a standard normal Lévy basis and . Then would be positive and pointwise -distributed with one degree of freedom.

Example 15.

Example 16.

A non-Gaussian example would be to choose as an inverse Gaussian Lévy basis and to be the identity function.

Example 17.

We have already mentioned that the kernel function determines the autocorrelation structure of the volatility field. E.g. in the absence of spatial correlation one could start off with the choice for mimicking the Ornstein-Uhlenbeck-based stochastic volatility models, see e.g. Barndorff-Nielsen & Schmiegel (2004).

5.1.2 Ornstein-Uhlenbeck volatility fields

Next, we show how to construct a stochastic volatility field by extending a stochastic process by a spatial dimension. Note that our objective is to construct a stochastic volatility field which is stationary (at least in the temporal direction). Clearly, there are many possibilities on how this can be done and we focus on a particularly relevant one in the following, namely the Ornstein-Uhlenbeck-type volatility field (OUTVF). The choice of using an OU process as the stationary base component is motivated by the fact that non-Gaussian OU-based stochastic volatility models, as e.g. studied in Barndorff-Nielsen & Shephard (2001), are analytically tractable and tend to perform well in practice, at least in the purely temporal case. In the following, we will restrict our attention to the case , i.e. that the spatial dimension is one-dimensional.

Suppose now that is a positive OU type process with rate parameter and generated by a Lévy subordinator , i.e.

We call a stochastic volatility field on an Ornstein-Uhlenbeck-type volatility field (OUTVF), if it is defined as follows

| (37) |

where is the spatial rate parameter and where is a family of Lévy processes, which we define more precisely in the next but one paragraph.

Note that in the above construction, we start from an OU process in time. In particular, is an OU process. The spatial structure is then introduced by two components: First, we we add an exponential weight in the spatial direction, which reaches its maximum for and decays the further away we get from the purely temporal case. Second, an integral is added which resembles an OU-type process in the spatial variable . However, note here that the integration starts from rather than from , and hence the resulting component is not stationary in the spatial variable . (This could be changed if required in a particular application.)

Let us now focus in more detail on how to define the family of Lévy processes . Suppose is a stationary, positive and infinitely divisible process on . Next we define as the so-called Lévy supra-process generated by , that is is a family of stationary processes such that has independent increments, i.e. for any the processes are mutually independent, and such that for each the cumulant functional of equals times the cumulant functional of , i.e.

where

with , denoting an ‘arbitrary’ signed measure on . Then at any the values of at time as runs through constitute a Lévy process that we denote by . This is the Lévy process occurring in the integral in (37).

Note that is stationary in and that as .

Example 18.

Now suppose, for simplicity, that is an OU process with rate parameter and generated by a Lévy process . Then

If, furthermore, and then for fixed and the autocorrelation function of is

This type of construction can of course be generalised in a variety of ways, including dependence between and and also superposition of OU processes.

Note that the process is in general not predictable, which is disadvantageous given that we want to construct Walsh-type stochastic integrals. However, if we choose to be of OU type, then we obtain a predictable stochastic volatility process.

5.2 Extended subordination and meta-times

An alternative way of volatility modulation is by means of (extended) subordination. Extended subordination and meta-times are important concepts in the ambit framework, which have recently been introduced by Barndorff-Nielsen (2010) and Barndorff-Nielsen & Pedersen (2012), and we will review their main results in the following. Note that extended subordination generalises the classical concept of subordination of Lévy processes to subordination of Lévy bases. This in turn will be based on a concept of meta-times.

5.2.1 Meta-times

This section reviews the concept of meta-times, which we will link to the idea of extended subordination in the following section.

Definition 16.

Let be a Borel set in . A meta-time on is a mapping from into such that

-

1.

and are disjoint whenever are disjoint.

-

2.

whenever are disjoint and .

A slightly more general definition is the following one.

Definition 17.

Let be a Borel set in . A full meta-time on is a mapping from into such that

-

1.

and are disjoint whenever are disjoint.

-

2.

whenever are disjoint.

Suppose is a measure on and let be a full meta-time on . Define as the mapping from into given by for any . Then is a measure on . We speak of as the subordination of by . Similarly, if is a meta-time on we speak of for as the subordination of by .

Let us now recall an important result, which says that any measure, which is finite on compacts, can be represented as the image measure of the Lebesgue measure of a meta-time.

Lemma 2.

Barndorff-Nielsen & Pedersen (2012, Lemma 3.1) Let be a measure on satisfying for all Then there exists a meta-time such that, for all , we have

We speak of as a meta-time associated to .

Remark 9.

can be chosen so that where is the inverse of a measurable mapping determined from . Here integration under subordination satisfies

Suppose is open and that is a measure on which is absolutely continuous with density . If we can find a mapping from to sending Borel sets into Borel sets and such that the Jacobian of exists and satisfies

then given by , is a natural choice of meta-time induced by . In fact, by the change of variable formula,

verifying that is a meta-time associated to .

Remark 10.

is not uniquely determined by and two different meta-times associated to may yield different subordinations of one and the same measure .

5.2.2 Extended subordination of Levy bases

Let us now study the concept of subordination in the case where we deal with a Lévy basis. Let be a full random measure on . Then, by Lemma 2, there exists a.s. a random meta-time determined by and with the property that , for all . There are two cases of particular interest to us. First, is induced by a Lévy basis on that is non-negative, dispersive and of finite variation. Second, is induced by an absolutely continuous random measure on with a non-negative density satisfying for all .

Definition 18.

Let be a Lévy basis on and let , independent of , be a full random measure on . The extended subordination of by is the random measure defined by

for all and where is a meta-time induced by (in which case ).

Note that the Lévy basis may be -dimensional. We shall occasionally write for , which is a random measure on .

In the case that is a homogeneous Lévy basis and since is assumed to be independent of , is a (in general not homogeneous) Lévy basis, whose conditional cumulant function satisfies

| (38) |

for all and where is the Lévy seed of . On a distributional level one may, without attention to the full probabilistic definition of presented above, carry out many calculations purely from using the identity established in (38).

Remarks

The two key formulae and show that the concepts of extended subordination and meta-time together generalise the classical subordination of Lévy processes. Provided that is homogeneous we have that

and hence

Hence we can deduce the following results.

-

•

The values of the subordination of are infinitely divisible provided the values of are infinitely divisible and is homogeneous.

-

•

If is homogeneous and if is a homogeneous Lévy basis then is a homogeneous Lévy basis.

-

•

In general, is not uniquely determined by . Nevertheless, provided the Lévy basis is homogeneous the law of does not depend on the choice of meta-time .

Lévy-Itô type representation of

We have already reviewed the Lévy-Itô representation for a dispersive Lévy basis , see (5). It follows directly that the subordination of by the random measure with associated meta-time has a Lévy-Itô type representation

Lévy measure of

Suppose for simplicity that is non-negative. According to Barndorff-Nielsen (2010), the Lévy measure of is related to the Lévy measure of by

5.2.3 Extended subordination and volatility

In the context of ambit stochastics one considers volatility fields in space-time, typically specified by the squared field . So far, we have used a stochastic volatility random field in the integrand of the ambit field to introduce volatility modulation.

A complementary method consists of introducing stochastic volatility by extended subordination. The volatility is incorporated in the modelling through a meta-time associated to the measure on and given by

A natural choice of meta-time is , where is the mapping given by

and where

The above construction of a meta-time in a tempo-spatial model is very general. One can construct a variety of models for the random field , which lead to new model specifications. Essentially, this leads us back to the problem we tackled in the previous Subsection, where we discussed how such fields can be modelled. For instance, one could model by an Ornstein-Uhlenbeck type volatility field or any other model discussed in Subsection 5.1. Clearly, the concrete choice of the model needs to be tailored to the particular application one has in mind.

5.3 Probability mixing and Lévy mixing

Volatility modulation can also be obtained through probability mixing as well as Lévy mixing.

The main idea behind the concept of probability or distributional mixing is to construct new distributions by randomising a parameter from a given parametric distribution.

Example 19.

Consider our very first base model (1). Now suppose that the corresponding Lévy basis is homogeneous and Gaussian, i.e. the corresponding Lévy seed is given by with and . Now we use probability mixing and suppose that in fact is random. Hence, the conditional law of the Lévy seed is given by . Due to the scaling property of the Gaussian distribution, such a model can be represented as (16) and, hence, in this particular case probability mixing and stochastic volatility via a stationary stochastic integrand essentially have the same effect. Suppose that the conditional variance has a generalised inverse Gaussian (GIG) distribution rather than being just a constant, then follows in fact a generalised hyperbolic (GH) distribution. Such a construction falls into the class of normal variance-mean mixtures.

In this context it is important to note that probability/distributional mixing does not generally lead to infinitely divisible distributions, see e.g. Steutel & van Harn (2004, Chapter VI). Hence Barndorff-Nielsen, Perez-Abreu & Thorbjørnsen (2012) propose to work with Lévy mixing instead of probability/distributional mixing. Lévy mixing is a method which (under mild conditions) leads to classes of infinitely divisible distributions again. Let us review the main idea behind that concept.

Let denote a factorisable Lévy basis on with CQ . Suppose that the Lévy measure depends on a possibly multivariate parameter , say, where denotes the parameter space. In that case, we write . Then, the generalised Lévy measure of is given by . Now let denote a measure on and define

where we assume that

| (39) |

Then there exists a Lévy basis which has as its generalised Lévy measure. We call the Lévy basis the Lévy basis obtained by Lévy-mixing with the measure .

Let us study a concrete example of Lévy mixing in the following.

Example 20.

Suppose is a homogeneous Lévy basis with CQ given by with for . I.e. the corresponding Lévy seed is given by . Now we do a Lévy-mixing of the intensity parameter . Let

for a measure satisfying condition (39). Let be the Lévy basis with CQ . In that case, the base model (1) would be transferred into a model of the form

Example 21.

Let us consider the example of a (sup)OU process, see Barndorff-Nielsen (2000), Barndorff-Nielsen & Stelzer (2011) and Barndorff-Nielsen, Perez-Abreu & Thorbjørnsen (2012). Let denote a subordinator with Lévy measure (and without drift) and consider an OU process

A straightforward computation leads to the following expression for its cumulant function (for ):

is a mixture of with the Lebesgue measure. A Lévy mixing can be carried out with respect to the parameter , i.e.

where is a measure on satisfying . Then is a Lévy measure again. Now, let be the Lévy basis with extended Lévy measure

and define the supOU process w.r.t. by

Then the cumulant function of is given by

Hence, we have seen that a supOU process can be obtained from an OU process through Lévy-mixing.

5.4 Outlook on volatility estimation

Once a model is formulated and data are available the question of assessment of volatility arises and while we do not discuss this in any detail, tools for this are available for some special classes of ambit processes, see Barndorff-Nielsen et al. (2009); Barndorff-Nielsen, Corcuera & Podolskij (2011, 2012) and also Barndorff-Nielsen & Graversen (2011). Extending these results to general ambit fields and processes is an interesting direction for future research.

6 Conclusion and outlook

In this paper, we have given an overview of some of the main findings in ambit stochastics up to date, including a suitable stochastic integration theory, and have established new results on general properties of ambit field. The new results include sufficient conditions which ensure the smoothness of ambit fields. Also, we have formulated sufficient conditions which guarantee that an ambit field is a semimartingale in the temporal domain. Moreover, the concept of tempo-spatial stochastic volatility/intermittency within ambit fields has been further developed. Here our focus has been on four methods for volatility modulation: Stochastic scaling, stochastic time change and extended subordination of random measures, and probability and Lévy mixing of the volatility/intensity parameter.

Future research will focus on applications of the general classes of models developed in this paper in various fields, including empirical research on turbulence modelling as well as modelling e.g. the term structure of interest rates in finance by ambit fields. In this context, it will be important to establish a suitable estimation theory for general ambit fields as well as inference techniques.

Acknowledgement

Financial support by the Center for Research in Econometric Analysis of Time Series, CREATES, funded by the Danish National Research Foundation is gratefully acknowledged by O. E. Barndorff-Nielsen. F. E. Benth acknowledges financial support from the Norwegian Research Council through the project ”Energy markets: modelling, optimization and simulation” (EMMOS), eVita 205328. A. E. D. Veraart acknowledges financial support by CREATES and by a Marie Curie FP7 Integration Grant within the 7th European Union Framework Programme.

References

- (1)

- Adler (1981) Adler, R. J. (1981), The geometry of random fields, John Wiley & Sons Ltd., Chichester. Wiley Series in Probability and Mathematical Statistics.

- Adler & Taylor (2007) Adler, R. J. & Taylor, J. E. (2007), Random fields and geometry, Springer Monographs in Mathematics, Springer, New York.

- Amiri (2009) Amiri, E. (2009), Bayesian modelling volatility of growth rate in atmospheric carbon dioxide concentrations, in ‘Proceedings of the 2009 Second International Conference on Environmental and Computer Science’, ICECS ’09, IEEE Computer Society, Washington, DC, USA, pp. 86–90.

- Azaïs & Wschebor (2009) Azaïs, J.-M. & Wschebor, M. (2009), Level sets and extrema of random processes and fields, John Wiley & Sons Inc., Hoboken, NJ.

- Barndorff-Nielsen (2000) Barndorff-Nielsen, O. E. (2000), ‘Superposition of Ornstein-Uhlenbeck type processes’, Rossiĭskaya Akademiya Nauk. Teoriya Veroyatnosteĭ i ee Primeneniya 45(2), 289–311.

- Barndorff-Nielsen (2010) Barndorff-Nielsen, O. E. (2010), Lévy bases and extended subordination. Thiele Centre Research Report No. 12, Aarhus University.

- Barndorff-Nielsen (2011) Barndorff-Nielsen, O. E. (2011), ‘Stationary infinitely divisible processes’, Brazilian Journal of Probability and Statistics 25, 294–322.

- Barndorff-Nielsen & Basse-O’Connor (2011) Barndorff-Nielsen, O. E. & Basse-O’Connor, A. (2011), ‘Quasi Ornstein-Uhlenbeck Processes’, Bernoulli 17(3), 916–941.

- Barndorff-Nielsen, Benth, Pedersen & Veraart (2012) Barndorff-Nielsen, O. E., Benth, F. E., Pedersen, J. & Veraart, A. E. D. (2012), On stochastic integration for volatility modulated Lévy-driven Volterra processes. Preprint available at http://arxiv.org/abs/1205.3275v1.

- Barndorff-Nielsen et al. (2010) Barndorff-Nielsen, O. E., Benth, F. E. & Veraart, A. E. D. (2010), Modelling electricity forward markets by ambit fields. Preprint.

- Barndorff-Nielsen, Benth & Veraart (2011) Barndorff-Nielsen, O. E., Benth, F. E. & Veraart, A. E. D. (2011), Ambit processes and stochastic partial differential equations, in G. Di Nunno & B. Øksendal, eds, ‘Advanced Mathematical Methods for Finance’, Springer, pp. 35–74.

- Barndorff-Nielsen, Benth & Veraart (2012) Barndorff-Nielsen, O. E., Benth, F. E. & Veraart, A. E. D. (2012), ‘Modelling energy spot prices by volatility modulated Lévy-driven Volterra processes’, Bernoulli . To appear.

- Barndorff-Nielsen et al. (2009) Barndorff-Nielsen, O. E., Corcuera, J. & Podolskij, M. (2009), ‘Power variation for Gaussian processes with stationary increments’, Stochastic Processes and Their Applications 119, 1845–1865.

- Barndorff-Nielsen, Corcuera & Podolskij (2011) Barndorff-Nielsen, O. E., Corcuera, J. & Podolskij, M. (2011), ‘Multipower variation for Brownian semistationary processes’, Bernoulli 17(4), 1159–1194.

- Barndorff-Nielsen, Corcuera & Podolskij (2012) Barndorff-Nielsen, O. E., Corcuera, J. & Podolskij, M. (2012), Limit theorems for functionals of higher order differences of Brownian semistationary processes, in A. E. Shiryaev, S. R. S. Vayadhan & E. Presman, eds, ‘Prokhorov and Contemporary Probability’. To appear.

- Barndorff-Nielsen & Graversen (2011) Barndorff-Nielsen, O. E. & Graversen, S. E. (2011), ‘Volatility determination in an ambit process setting’, Journal of Applied Probability 48A, 263–275. New frontiers in applied probability: a Festschrift for Søren Asmussen.

- Barndorff-Nielsen, Lunde, Shephard & Veraart (2012) Barndorff-Nielsen, O. E., Lunde, A., Shephard, N. & Veraart, A. E. D. (2012), Integer-valued trawl processes: A class of stationary infinitely divisible processes. Preprint.

- Barndorff-Nielsen & Pedersen (2012) Barndorff-Nielsen, O. E. & Pedersen, J. (2012), ‘Meta-times and extended subordination’, Theory of Probability and its Applications 56(2), 319–327.

- Barndorff-Nielsen, Perez-Abreu & Thorbjørnsen (2012) Barndorff-Nielsen, O. E., Perez-Abreu, V. & Thorbjørnsen, S. (2012), Lévy mixing. Preprint.

- Barndorff-Nielsen & Schmiegel (2004) Barndorff-Nielsen, O. E. & Schmiegel, J. (2004), ‘Lévy-based tempo-spatial modelling; with applications to turbulence’, Uspekhi Mat. NAUK 59, 65–91.

- Barndorff-Nielsen & Schmiegel (2007) Barndorff-Nielsen, O. E. & Schmiegel, J. (2007), Ambit processes: with applications to turbulence and cancer growth, in F. Benth, G. Di Nunno, T. Lindstrøm, B. Øksendal & T. Zhang, eds, ‘Stochastic Analysis and Applications: The Abel Symposium 2005’, Springer, Heidelberg, pp. 93–124.

- Barndorff-Nielsen & Schmiegel (2009) Barndorff-Nielsen, O. E. & Schmiegel, J. (2009), Brownian semistationary processes and volatility/intermittency, in H. Albrecher, W. Rungaldier & W. Schachermeyer, eds, ‘Advanced Financial Modelling’, Radon Series on Computational and Applied Mathematics 8, W. de Gruyter, Berlin, pp. 1–26.

- Barndorff-Nielsen & Shephard (2001) Barndorff-Nielsen, O. E. & Shephard, N. (2001), ‘Non–Gaussian Ornstein–Uhlenbeck–based models and some of their uses in financial economics (with discussion)’, Journal of the Royal Statistical Society Series B 63, 167–241.

- Barndorff-Nielsen & Stelzer (2011) Barndorff-Nielsen, O. E. & Stelzer, R. (2011), ‘Multivariate SupOU processes’, Annals of Applied Probability 21(1), 140–182.

- Basse-O’Connor et al. (2012) Basse-O’Connor, A., Graversen, E. & Pedersen, J. (2012), Multiparameter processes with stationary increments. Preprint.

- Bochner (1949) Bochner, S. (1949), ‘Diffusion equation and stochastic processes’, Proceedings of the National Academy of Sciences of the United States of America 35, 368–370.

- Brockwell & Davis (2002) Brockwell, P. J. & Davis, R. A. (2002), Introduction to time series and forecasting, Springer Texts in Statistics, second edn, Springer-Verlag, New York.

- Cox (1975) Cox, J. (1975), Notes on Option Pricing I: Constant Elasticity of Diffusions. Unpublished draft, Stanford University.

- Cox et al. (1985) Cox, J. C., Ingersoll, Jr., J. E. & Ross, S. A. (1985), ‘A theory of the term structure of interest rates’, Econometrica 53(2), 385–407.

- Cressie (1993) Cressie, N. (1993), Statistics for Spatial Data, Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics, Wiley, New York.

- Cressie & Wikle (2011) Cressie, N. & Wikle, C. K. (2011), Statistics for spatio–temporal data, Wiley Series in Probability and Statistics, John Wiley & Sons Inc., Hoboken, NJ.

- Dalang & Quer-Sardanyons (2011) Dalang, R. C. & Quer-Sardanyons, L. (2011), ‘Stochastic integrals for spde’s: A comparison’, Expositiones Mathematicae 29(1), 67 – 109.

- Decreusefond (2002) Decreusefond, L. (2002), ‘Regularity properties of some stochastic Volterra integrals with singular kernel’, Potential Analysis 16, 139–149.

- Finkenstädt et al. (2007) Finkenstädt, B., Held, L. & Isham, V., eds (2007), Statistical methods for spatio-temporal systems, Vol. 107 of Monographs on Statistics and Applied Probability, Chapman & Hall/CRC, Boca Raton, FL. Papers from the 6th Séminaire Européen de Statistique held in Bernried, December 12–18, 2004.

- Hamilton (1994) Hamilton, J. D. (1994), Time series analysis, Princeton University Press, Princeton, NJ.

- Hedevang (2012) Hedevang, E. (2012), Stochastic modelling of turbulence with applications to wind energy, PhD thesis, Aarhus University.

- Huang et al. (2011) Huang, W., Wang, K., Breidt, F. J. & Davis, R. A. (2011), ‘A class of stochastic volatility models for environmental applications’, Journal of Time Series Analysis 32(4), 364–377.

- Jónsdóttir et al. (2008) Jónsdóttir, K. Ý., Schmiegel, J. & Vedel Jensen, E. B. (2008), ‘Lévy-based growth models’, Bernoulli 14(1), 62–90.

- Kent (1989) Kent, J. T. (1989), ‘Continuity properties for random fields’, The Annals of Probability 17(4), 1432–1440.

- Marcus & Rosinski (2005) Marcus, M. B. & Rosinski, J. (2005), ‘Continuity and boundedness of infinitely divisible processes: A Poisson point process approach’, Journal of Theoretical Probability 18, 109–160.

- Mytnik & Neuman (2011) Mytnik, L. & Neuman, E. (2011), ‘Sample Path Properties of Volterra Processes’, ArXiv e-prints .

- Peccati & Taqqu (2008) Peccati, G. & Taqqu, M. S. (2008), ‘Limit theorems for multiple stochastic integrals’, ALEA. Latin American Journal of Probability and Mathematical Statistics 4, 393–413.

- Pedersen (2003) Pedersen, J. (2003), The Lévy–Itô decomposition of an independently scattered random measure. MaPhySto preprint MPS–RR 2003–2.

- Rajput & Rosinski (1989) Rajput, B. & Rosinski, J. (1989), ‘Spectral representation of infinitely divisible distributions’, Probability Theory and Related Fields 82, 451–487.

- Rosinski (1989) Rosinski, J. (1989), ‘On path properties of certain infinitely divisible processes’, Stochastic Processes and their Applications 33(1), 73–87.

- Samorodnitsky & Taqqu (1994) Samorodnitsky, G. & Taqqu, M. S. (1994), Stable non-Gaussian random processes: Stochastic models with infinite variance, Stochastic Modeling, Chapman & Hall, New York.