Strong Convergence for Euler-Maruyama and Milstein Schemes with Asymptotic Method

Abstract

Motivated by weak convergence results in the paper of Takahashi and Yoshida (2005), we show strong convergence for an accelerated Euler-Maruyama scheme applied to perturbed stochastic differential equations. The Milstein scheme with the same acceleration is also discussed as an extended result. The theoretical results can be applied to analyzing the multi-level Monte Carlo method originally developed by M.B. Giles. Several numerical experiments for the SABR stochastic volatility model are presented in order to confirm the efficiency of the schemes.

Keywords: Strong convergence; asymptotic method; multi-level Monte Carlo

1 Introduction

We investigate an asymptotic method that accelerates numerical schemes for perturbed random variables. The general concept is as follows. Suppose that is a random variable depending on a small parameter . Let us consider an approximation for independently with respect to . Then the bias may be close to the bias , since has a small effect on the value of . Therefore, we expect that

| (1.1) |

In particular, our interest is to study the above property when is a functional of a stochastic process and comes from time discretization for it. In many cases, is a simpler model than and its exact distribution is well-known (e.g. Gaussian random variables or functionals of Gaussian processes). Even if the exact distribution of is unknown, it seems to be possible to provide a new scheme with another more efficient scheme for (see Section 3.1 as an example).

In general, we consider the following three error structures:

-

•

Strong error:

(1.2) -

•

Weak error:

(1.3) -

•

Monte Carlo bias estimator for where be an i.i.d. sampling of :

(1.4)

Notice that in the case of Monte Carlo bias (1.4), the term works as a control variates method. For applications in strong error (1.2), we need an exact or accurate numerical simulation method for . On the other hand, in the cases of weak error (1.3) and Monte Carlo bias (1.4), we have to know the value of , and therefore we need a closed formula or an accurate numerical scheme for such as the fast Fourier transform in one dimension.

When denotes a functional of a stochastic differential equation , corresponds to a certain time discretization scheme (: number of partition). Takahashi-Yoshida [16] derived the following results in weak error sense (1.3) and Monte Carlo bias sense (1.4) for the Euler-Maruyama scheme :

and hence the total error (the root-mean-squared error; RMSE) is equal to

Here they assumed some appropriate conditions for and the coefficients of . This is the case where and in (1.3), and in (1.4). In order to make the total error with weak and Monte Carlo bias, the standard Euler-Maruyama scheme with i.i.d. sampling requires the computational cost , and in contrast, the accelerated Euler-Maruyama scheme with i.i.d. sampling requires the cost . That is, the asymptotic method (1.1) for the Euler-Maruyama scheme is -times faster than the standard method. Moreover, we can construct a sampling scheme whose computational cost turns out to be for any and Lipschitz continuous function via the multi-level Monte Carlo method (See Theorem 4.5).

In this paper, we develop the error analysis for the Euler-Maruyama and Milstein schemes with the asymptotic method in strong sense (1.2). Under suitable conditions, we will show that for any ,

| (1.5) |

with for the Euler-Maruyama (Milstein, resp.) scheme . Although strong convergence is usually very slow, the asymptotic method (1.1) helps to improve the speed of convergence.

A simplest example of (1.5) is for the case where the SDE becomes the ODE when , namely,

However, from the viewpoint of applications, we can also consider the (th-order) -expansion around linear models like Black-Scholes (See an analytical expansion in Kunitomo-Takahashi [11] and Takahashi-Yamada [15]). Indeed, we can treat a perturbed stochastic differential equations such as

Notice that becomes the Black-Scholes model with time-dependent coefficients. Therefore there are many applications in the models of dynamic assets with stochastic volatility and/or stochastic interest rate. In particular, we will discuss more general stochastic differential equations so-called local-stochastic volatility type models.

This paper is organized as follows: Section 2 is devoted to state theoretical results for strong convergence (1.5). In Section 3 we discuss pathwise simulation of stochastic volatility models. In Section 4, we introduce the multi-level Monte Carlo method and its acceleration by the asymptotic method. In Section 5 some numerical experiments for the SABR stochastic volatility model are given. In Appendix we give some mathematical results including the proof of main claims in Section 2 and 4.

2 Strong convergence results

As seen in the previous intruduction, the asymptotic method (1.1) for discretizing stochastic processes is very natural to speed up the discretization procedure. We state here the basic setting to discuss the approximation schemes. Let us consider a stochastic differential equation (SDE) of the form

| (2.1) |

where , , and is a -dimensional standard Brownian motion on a probability space with a filtration satisfying usual conditions. Throughout the paper, we use the equidistant partition , . The Euler-Maruyama and Milstein schemes will be considered with some smoothness conditions for the coefficients of the SDE.

2.1 The Euler-Maruyama scheme with asymptotic method

Let be the Euler-Maruyama scheme for the SDE (Maruyama [13]): For ,

| (2.2) |

The implementation of (2.2) is very simple. Indeed, practitioners only need to know how to simulate normal random variables. The error of the scheme has been analyzed deeply by many researchers (see e.g. [17], [10], [4]). Roughly speaking, the strong order of convergence is equal to , and the weak order is equal to .

We now prepare the assumptions for .

- ():

-

- ():

-

- ():

-

- ():

-

For every , and

The above constant is independent of .

Let us define the accelerated Euler-Maruyama scheme as

The property (1.1) for strong convergence is formulated rigorously as follows.

Theorem 2.1.

Suppose that - hold. Then for any , there exists a constant such that

In particular, if we consider the small volatility model and the ODE , then intuitively speaking, cancels out the error from the drift term (except the effect of ), and the error from small volatility only remains. Hence the total error is proportional to .

Of course, more general situations can be considered, for example, if and depends on time , then some smoothness assumptions with respect to are needed in addition to -. We will not attempt to prove this, but basically the asymptotic method works as well.

Remark 2.2.

The rate of convergence of the Euler-Maruyama scheme basically relies on the smoothness (or the Lipschitz continuity) of coefficients of SDEs. If the coefficients are not smooth but Hölder continuous, the speed of convergence may be slow, as seen in the paper by Yan [18]. For obtaining the strong rate of convergence with (), a modified Euler-type scheme (called a symmetrized Euler scheme) was developed by Berkaoui et al. ([2]). We should mention that the Euler-Maruyama scheme may not converge strongly when the coefficients are non-globally Lipschitz continuous. For example, in [9] a sufficient condition that the scheme explodes is given.

2.2 The Milstein scheme with asymptotic method

We next discuss the Milstein scheme which has a higher order rate of convergence than the Euler-Maruyama scheme in strong sense. Just for notational convenience, we only consider the case . Of course, in general dimensional setting with commutative vector fields , we can use the (accelerated) Milstein scheme as well.

Throughout this section, we assume the following smoothness.

-

•

For every ,

The Milstein scheme for the SDE is defined by

for .

We use the (stronger) assumptions for .

- ():

-

&

- ():

-

&

- ():

-

&

- ():

-

&

Let us define the accelerated Milstein scheme as

Then we can get the higher order convergence rate.

Theorem 2.3.

Suppose that - hold. Then for any , there exists a constant such that

3 Application to pathwise simulation of stochastic volatility models

Our goal in this section is to construct a faster pathwise approximation for perturbed stochastic differential equations which appear in financial modeling of volatility.

3.1 An accelerated scheme for SABR model

In financial modeling, the SABR model plays a role to fit the implied volatility especially in short time. The model is given by the SDE (Hagan et al. [8])

The volatility is not a mean-reversion process, hence this model does not suit for pricing long-dated options. If , as far as the authors know, there is no exact pathwise simulation method for the above SDE. In weak sense, several accurate simulation methods via Bessel processes are known.

To avoid that the volatility process becomes negative in approximation procedures, we use a logarithmic transform for .

Consider . Since we do not know exact pathwise simulation methods for , we substitute the Milstein scheme for . Therefore, we can use an -scheme defined by

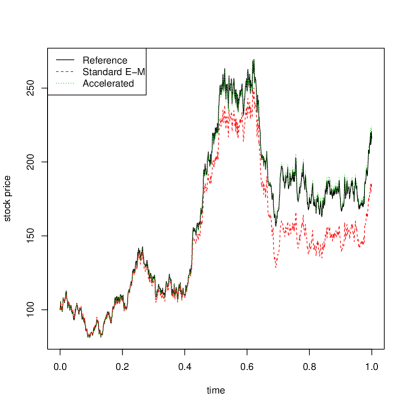

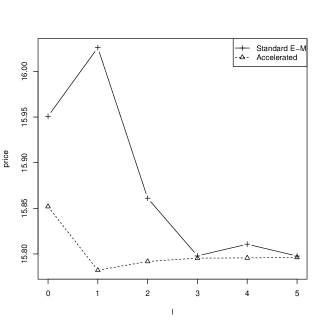

When is small enough, a typical sample path is like Figure 1. Here we use for the standard Euler-Maruyama scheme (Standard E-M) and the above accelerated scheme (Accelerated).

We next turn to consider another formal approximation scheme. Formally, when and especially . Thus consider the scaling , .

Here is just a constant coming from the scaling, thus we do not change the constant even when . The accelerated scheme that we want to use is

Since is a log-normal process, it is useful to compute the path and . We will check the efficiency of through a numerical test later.

3.2 General stochastic volatility models

The following model is an extension of local-stochastic volatility models applicable to both short and long term contingent claims in financial markets.

where is a compound Poisson process, which is often used to adapt especially short-dated large volatility smile/skew.

We remark that it is difficult to fit short-dated volatility smile/skew under the Heston model (, , ), and then can take very large value. On the other hand, under general models with and , the parameter need not to be so large.

Let be the random jump times associated to and consider a new time partition . On the time interval we can regard the approximation problem for as the one for a continuous SDE. In particular by taking , the model becomes the CEV model with time-dependent coefficients. For a technical reason, we should consider some carefull treatments around zero of the function (See [3, 2, 12]).

4 Application to multi-level Monte Carlo method

The theoretical results we obtained in previous can be applied to the multi-level Monte Carlo method (MLMC in short). We propose an accelerated Monte Carlo sampling for Takahashi-Yoshida’s weak convergence method.

4.1 The basic methodology of MLMC

We forget the parameter for the time being, and denote by the continuous SDE defined by (2.1). Let us define and , and consider the time-step size for a fixed . Let and the sampling of multi-level Monte Carlo is defined by

| (4.1) |

where each is independently distributed and is given by

with i.i.d. sampling or , . The most important point is to use the same Brownian motion path for simulating and , and so the concept of the multi-level Monte Carlo method concerns the strong (pathwise) convergence rate.

Clearly we show that

therefore the weak rate of convergence depends only on the last number . Moreover, we obtain from the independence of ,

and by definition . Suppose some suitable conditions for and . Then one can obtain

The last estimate is the strong convergence result in , which is discussed in this paper.

The total computational cost is determined by the level , the number of sampling , and the number of partition so that

Suppose that the required RMSE is . Then by choosing , the total variance is of . Now if we set , then the total time discretization error . Consequently for the required accuracy .

4.2 Accelerated MLMC sampling (with smooth payoffs)

From now on, we reconsider the sampling of the accelerated Euler-Maruyama scheme introduced by Takahashi and Yoshida from the standard Monte Carlo method

to the multi-level Monte Carlo method via

Remark 4.1.

We can also consider another MLMC sampling method via

whose computational cost is for Lipschitz functions . However, in this case we cannot take advantage of the explicit formula for the term .

Giles [6] assumed that is Lipschitz continuous to analyze the variance of estimator. On the other hand, we need in order to use the asymptotics with respect to (Notice that in general). Our analysis follows from the lemma below.

Lemma 4.2.

For ,

Proof.

This can be proved immediately by using the mean value theorem twice (See also Lemma A3). ∎

Then we have the following variance estimate.

Proposition 4.3.

Assume that - hold. For , we have

Proof.

For the use of the multi-level Monte Carlo method, we have obtained the results as follows.

So the estimator for has an equivalent effect to the one for with the required error . Consequently we get the order of computational cost . Both the asymptotic method and multi-level Monte Carlo method are very easily computable, so that practitioners will get large benefit only with small additional implementation cost.

Remark 4.4.

Clearly, we can also check the variance estimate for the accelerated Milstein scheme. Let . By a similar argument, we derive that under - and ,

| (4.2) |

We have not obtained weak convergence results for the accelerated Milstein scheme yet. However, we guess that from the basic proof of Takahashi-Yoshida [16], it holds that

| (4.3) |

under some smoothness conditions for and the coefficients of . Thus combining the results (4.2), (4.3) and the discussion in Giles [6, 5], we finally conclude that the total computational cost is .

4.3 Lipschitz payoffs

Let us consider the first component as an asset dynamics. Our interest is pricing an option with Lipschitz payoffs . Set Then we can obtain an upper bound estimate as follows.

Theorem 4.5.

Assume - and is a Lipschitz continuous function whose weak derivative has bounded variation in . In addition, suppose has a bounded density, and also has a bounded density uniformly with respect to . Then we have for any small ,

Proof.

See B. ∎

This theorem implies that the required computational cost turns out to be , with and .

We now summarize strong rate of convergence for and in Table 1.

4.4 Localization for irregular payoffs

The regularity of seems to be essential for the accelerated MLMC method introduced in previous. For example, we will see through computational experiments that the acceleration with discontinuous functions does not work so well.

We now propose a localization technique for this problem. Let us define a decomposition

where is a smooth (at least Lipschitz continuous) function with . Then we apply the accelerated MLMC to the smooth part and the standard MLMC to the irregular part . In other words, we consider the MLMC method for

The standard MLMC for discontinuous functions was studied in Avikainen [1] and Giles et al. [7].

5 Simulations

5.1 Numerical experiments for SABR model

In this section, we want to study an estimator of -norm for the SABR model. As a reference path, we use instead of .

We set the parameters as follows.

-

•

, , , , ,

-

•

, .

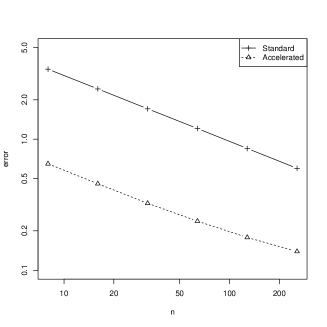

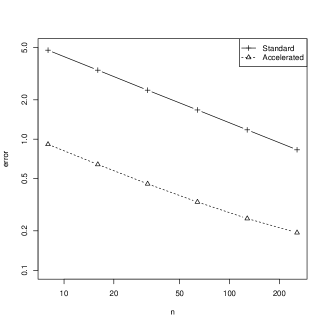

Here we considered a scaling for (via ). The number of simulation for the test is . The results are given in Figure 2. The accelerated scheme is faster than the standard method in both cases of -error.

|

|

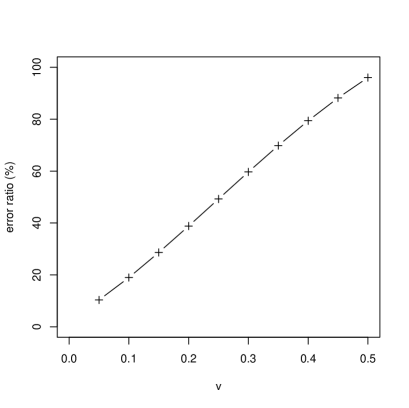

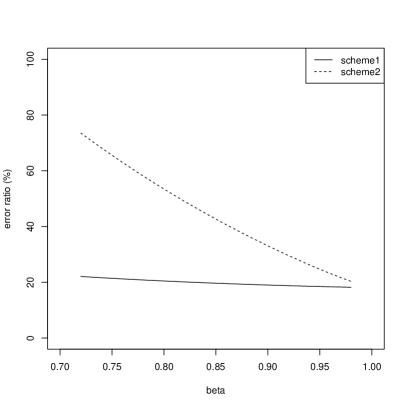

We next study the case with several . Let us compute the -error ratio for a random variable which is defined as

We fix the other parameters in the previous. In Figure 4, we can check the efficiency of the asymptotic method (only) when is small enough.

Finally we compare and with different . Figure 4 shows that the efficiency of is very close to that of as . Therefore if , we can apply the analytical tractability of to pathwise simulation, computing expectations, or so on.

5.2 Numerical tests for MLMC

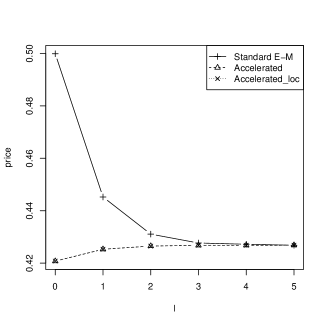

To show that the accelerated method is more efficient than the standard method with MLMC, we take a numerical test for , and under the SABR model with small parameter . Let us consider payoff functions (European and digital options)

and the parameters

-

•

, , , , ,

The level structure of MLMC is given by , i.e., . As a localization for digital option, we use

Here we set .

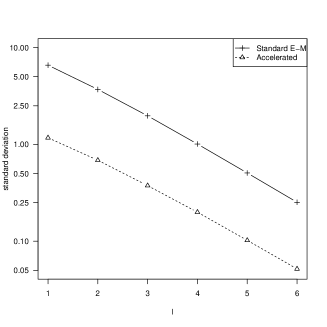

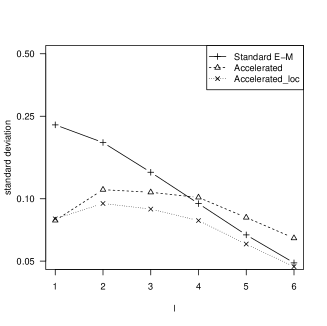

Figure 6 and 6 show the numerical results. We used the number of simulation for the left, and for the right. The results basically imply that the accelerated method works better than the standard one as in preceding numerical experiments. Remarkably the accelerated method performs worse in the case of variance estimates for digital option, likely due to discontinuity of the payoff function. In contrast, the localized scheme (Accelerated_loc) performs better than the others to some extent. We note that for general , the (semi-)analytical formula for CEV option pricing model can be used in order to compute (See [14]).

|

|

6 Discussion: small extension

By the accelerated method, the Euler-Maruyama scheme can be faster with a parameter small enough. But of course, if is not so small, the method does not work effectively (See Figure 4).

To improve the efficiency of the method, we consider a natural extended scheme

where to keep the rate of convergence. For example, the optimal with respect to -error is given by

However, since the value of is unknown, we can not estimate directly. In general it does not seem easy to choose an appropriate and computable . This issue is left for future work.

Appendix A Proof of Theorem 2.1 and 2.3

We use the following notations.

-

•

if .

-

•

, .

We will apply the Burkholder-Davis-Gundy (BDG) inequality

to the proofs below: Here and is a continuous local martingale.

Using the BDG inequality and Gronwall inequality, we can show the following moment estimates. (See [10] for the proof in the case of -norm.)

Lemma A1.

(i) Suppose that the assumptions - hold. Then for any , we have

(ii) Suppose that the assumptions - hold. Then for any , we have

We now give an important lemma for the proof of the main theorems.

Lemma A2.

(i) Under -, we have for any ,

| (A.1) |

and

| (A.2) |

(ii) Under -, for any ,

(iii) Under -, for any ,

Proof.

(i): We first note that

and by the BDG inequality for the stochastic integral term,

Using the conditions - for the above, we have immediately

Here the constants and do not depend on . Thus from the Gronwall inequality we obtain (A.1).

The proofs for (ii) and (iii) are straightforward as in (A.1). ∎

The following lemma will be used such as the Lipschitz continuous property.

Lemma A3.

(i) Assume that - hold. Then

(ii) Assume that - hold. Then

Proof.

We only prove for . By the mean value theorem,

where . Taking the difference again in the right hand side, we have

Finally, using the assumption for , we obtain the result. ∎

Now we shall prove the theorems.

Proof of Theorem 2.1.

Let us define

By using the Gronwall inequality, our goal becomes to show the following:

where and depend only on .

We now compute

where

and

For , we obtain from Lemma A3,

and

Hence the integral term in is evaluated by

By using the BDG inequality, the stochastic integral term in also has the same bound (except the size of constant ). Consequently, we have by Lemma A1, A2,

Applying a similar calculus to , we also get

This finishes the proof of Theorem 2.1. ∎

Appendix B Proof of Theorem 4.5

Throughout this section, we use the following notations without confusion:

-

•

, .

-

•

.

-

•

.

We say has bounded variation in if .

The following lemma plays a crucial role in the proof of the theorem.

Lemma B1 (Avikainen [1], Theorem 2.4).

Let and be real valued random variables with . In addition, suppose has a bounded density. Then for any function of bounded variation in and , there exists a constant depending on , and the essential supremum for a density of such that

By the next lemma, we can obtain an approximation sequence of the payoff .

Lemma B2.

Let be a bounded Lipschitz continuous function whose weak derivative has bounded variation in . Then there exists a sequence such that

Proof.

The approximate sequence can be constructed by mollifier convolutions , that is, with the conditions (i) , (ii) , (iii) , and (iv) . ∎

Proof of Theorem 4.5.

Assume that is a bounded function whose derivative has bounded variation. As seen in Proposition 4.3, note that

The final line is bounded by , and thus we turn to focus on the estimate for the second line. The second line is bounded by

for any such that . Now using Lemma B1, we have

To obtain the result, we choose small and large such that .

Finally, for general , consider for as a first approximation, and apply Lemma B2 to . Then we obtain the desired result by taking the limit. ∎

Acknowledgement

The authors would like to thank Arturo Kohatsu-Higa and Akihiko Takahashi for their helpfull comments. The first author was supported by JSPS Research Fellowships for Young Scientists, and this work was supported by JSPS KAKENHI Grant Number 12J03138.

References

- [1] R. Avikainen, On irregular functionals of SDEs and the Euler scheme, Finance Stoch. 13 (2009) 381-401.

- [2] A. Berkaoui, M. Bossy and A. Diop, Euler scheme for SDEs with non-Lipschitz diffusion coefficient: strong convergence ESAIM Probab. Stat. 12 (2008) 1-11.

- [3] M. Bosy and A. Diop, An efficient discretisation scheme for one dimensional SDEs with a diffusion coefficient function of the form , (INRIA Working Paper, 2004).

- [4] V. Bally and D. Talay, The law of the Euler scheme for stochastic differential equations (I):convergence rate of the distribution function, Probab. Theory Related Fields 104 (1995) 43-60.

- [5] M.B. Giles, Improved multilevel Monte Carlo convergence using the Milstein scheme, Monte Carlo and Quasi-Monte Carlo Methods 2006 (2007) 343-358.

- [6] M.B. Giles, Multilevel Monte Carlo path simulation, Oper. Res. 56 (2008) 607-617.

- [7] M.B. Giles, D.J. Higham and X. Mao, Analyzing multi-level Monte Carlo for options with non-globally Lipschitz payoff, Finance Stoch. 13 (2009) 403-414.

- [8] P. Hagan, D. Kumar, A. Lesniewski and D. Woodward, Managing smile risk, Wilmott magazine 1 (2002) 84-108.

- [9] M. Hutzenthaler, A. Jentzen and P. Kloeden, Strong and weak divergence in finite time of Euler’s method for stochastic differential equations with non-globally Lipschitz coefficients, Proc. Roy. Soc. London A, 467 (2011) 1563-1576.

- [10] P.E. Kloeden and E. Platen, Numerical Solution of Stochastic Differential Equations (Springer, 1992).

- [11] N. Kunitomo and A. Takahashi, On Validity of the Asymptotic Expansion Approach in Contingent Claim Analysis, Annals of Applied Probability 13 (2003) 914-952.

- [12] R. Load, R. Koekkoek and D. Van Dijk, A comparison of biased simulation schemes for stochastic volatility models, Quantitative Finance 10 (2010) 177-194.

- [13] G. Maruyama, Continuous Markov processes and stochastic equations, Rendiconti del Circolo Matematico di Palerm 4 (1955) 48-90.

- [14] M. Schroder, Computing the constant elasticity of variance option pricing formula, J. of Finance 211 (1989) 211-219.

- [15] A. Takahashi and T. Yamada, An asymptotic expansion with push-down of Malliavin weights, SIAM J. Finan. Math. 3 (2012) 95-136.

- [16] A. Takahashi and N. Yoshida, Monte Carlo simulation with asymptotic method, J. Japan Statist. Soc. 35 (2005) 171-203.

- [17] D. Talay and L. Tubaro, Expansion of the global error for numerical schemes solving stochastic differential equations, Stochastic Analysis and Applications 8 (1990) 94-120.

- [18] B.L. Yan, The Euler scheme with irregular coefficients, Ann. Probab. 30 (2002) 1172-1194.