Irregularities and Scaling in Signal and Image Processing: Multifractal Analysis

Abstract:

B. Mandelbrot gave a new birth to the notions of scale invariance, selfsimilarity and non-integer dimensions, gathering them as the founding corner-stones used to build up fractal geometry.

The first purpose of the present contribution is to review and relate together these key notions, explore their interplay and show that they are different facets of a same intuition.

Second, it will explain how these notions lead to the derivation of the mathematical tools underlying multifractal analysis.

Third, it will reformulate these theoretical tools into a wavelet framework, hence enabling their better theoretical understanding as well as their efficient practical implementation.

B. Mandelbrot used his concept of fractal geometry to analyze real-world applications of very different natures.

As a tribute to his work, applications of various origins, and where multifractal analysis proved fruitful, are revisited to illustrate the theoretical developments proposed here.

Keywords: Scaling, Scale Invariance, Fractal, Multifractal, Fractional dimensions, Hölder regularity, Oscillations, Wavelet, Wavelet Leader, Multifractal Spectrum, Hydrodynamic Turbulence, Heart Rate Variability, Internet Traffic, Finance Time Series, Paintings

1 Introduction

As many students, before and after us, we first met Benoît Mandelbrot through his books [127, 128]; indeed, they were scientific bestsellers, and could be found in evidence in most scientific bookshops. A quick look was sufficient to realize that Benoît was an unorthodox scientist; these books radically differed from what we were used to, and were trespassing several taboos of the time: First, they could not be straightforwardly associated with any of the standardly labelled fields of science, which had been taught to us as separate subjects. This could already be inferred from their titles: The fractal geometry of nature [128] constitutes a statement that mathematics and natural sciences are intrinsically mixed, and that the purpose will not be to disentangle them artificially, but rather to explore their interactions. The contents of these books confirmed this first feeling: Though they contained a large proportion of very serious mathematics, they did not follow the old definition-theorem-proof articulation we were used to. The focus was directly on the observation of figures and on their pertinence for modeling; the mathematics were there to help and comfort the deep geometric intuition that Benoît had developed. This does not mean that he considered mathematics as an ancillary discipline. To the contrary, many testimonies confirm how enthusiastic he was when one of his mathematical intuitions was proven correct, and how he immediately incorporated the new mathematical methods in his own toolbox, which then helped him to sharpen his intuition and go further.

Another revolutionary point was that these books reversed the classical focusses: While one did find familiar mathematical objects (the nowhere differentiable Weierstrass functions, or the devil’s staircase had been encountered before), the role he made them play was radically different: So far, they had only been counterexamples, or pathological objects pedagogically used to shed light on possible pitfalls; instead of this restrictive role, Benoît used them as the key examples and cornerstones to found a new geometry based on roughness and selfsimilarity. These books were opening a subject, and drawing tracks through a new territory; their purpose was not to give the usual polished, final description of a well understood area, but to open windows on how science advances, and they had a strong influence on our vocations to research.

Later, personal meetings played a decisive role; let us only mention one such occasion: At the end of his PhD, one of us (S. J.) met Benoît who was visiting Ecole Polytechnique. Benoît had heard of wavelets, which, at the time, were a new tool still in infancy, and immediately envisaged possible interactions between wavelets and fractal analysis. A key feature of fractals is scaling invariance, and, because wavelets can be deduced one from the others by translations and dilations of a given function, their particular algorithmic structure should reveal the scaling invariance properties of the analyzed objects. Driven by his insatiable curiosity, Benoît wanted to learn everything about wavelets (which was actually not so much at the time!) and then, with his characteristic generosity, he shared with this student he barely knew his intuitions on the subject. Thus, the present contribution can be read as a tribute to some of the scientific lines Benoît had dreamed about at the time: It will show how and why wavelet techniques yield powerful tools for analyzing fractal properties of signals and images, and thus supply new collections of tools for their classification and modeling.

1.1 Scale invariance and self similarity

Exact (or deterministic) self similarity. Fractal analysis can roughly be thought of as a way to characterize and investigate the properties of irregular sets. Note that irregularity is a negatively defined word; the description of the scientific domain it covers is therefore not clearly feasible, and had not been tried before B. Mandelbrot developed the concepts of fractal geometry. One of his leading ideas was a notion of regularity in irregularity or selfsimilarity: The object is irregular, but there is some invariance in its behavior across scales. For some sets, the notion of selfsimilarity replaces the notion of smoothness. For instance, the triadic Cantor set is selfsimilar, in the sense that it is made of two pieces which are the same as the whole set is shrunk by a factor 3. The purpose of multifractal analysis is to transpose this idea from the context of geometrical sets to that of functions. Sometimes, this transposition can be directly achieved, when the geometrical set consisting of the graph of the function also displays some selfsimilarity. Consider the example of the Weierstrass-Mandelbrot functions (a slight variant of the famous Weierstrass functions, see [128] pp. 388-390):

| (1) |

(note that the series converges when because and when because and ). Those functions clearly satisfy the exact selfsimilarity relationship

| (2) |

Note that selfsimilar functions associated with a selfsimilarity exponent can be obtained using slight variants: For instance, the function

is selfsimilar with a selfsimilarity exponent , which can go up to 2; and the function

is selfsimilar with a selfsimilarity exponent which can go up to 3. Note that this “renormalization technique” can be pushed further to deal with higher and higher values of , yielding smoother and smoother functions: One thus obtains functions that are everywhere and nowhere .

Random (or statistical) self similarity. Functions satisfying (2) are very rare; therefore the notion of exact selfsimilarity can be considered too restrictive for real world data modeling. Fruitful generalizations of this concept can be developed into several directions. A first possibility lies in weakening the exact deterministic relationship (2) into a probabilistic one: The (random) functions do not coincide sample path by sample path, but share the same statistical laws. A stochastic process is said to be selfsimilar, with selfsimilarity exponent iff

| (3) |

(see Definition 5 where the precise definition of equality in law of processes is recalled).

The first example of such selfsimilar processes is that of fractional Brownian motion (hereafter referred to as fBm), introduced by Kolmogorov [105]. Its importance for the modeling of scale invariance and fractal properties in data was made explicit and clear by Mandelbrot and Van Ness in [138]. This article is characteristic of Mandelbrot’s genius, which could perceive similarities between very distant disciplines: Motivations simultaneously rose from hydrology (cumulated water flow), economic time series and fluctuations in solids. Notably, B. Mandelbrot explained that fBm (with ) was well-suited to model long term dependencies, or long memory effects, in data, a property he liked to refer to as the Joseph effect in a colorful and self-speaking metaphoric comparison to the character of the Bible (cf. e.g., [139]). Selfsimilar processes have since been the subject of numerous exhaustive studies, see for instance the books [4, 55, 65, 168]. Note also that B. Mandelbrot put selfsimilarity (which he actually more accurately called selfaffinity) as a central notion in the study stochastic processes in views of applications, see [136] for a panorama of his works in this direction.

1.2 Selfsimilarity and Wavelets

Let us now briefly come back to B. Mandelbrot’s intuition and see how wavelet analysis can reveal relationships such as (2) or (3), as well as other important probabilistic properties of stochastic processes. In its simplest form, an orthonormal wavelet basis of is defined as the collection of functions

| (4) |

and the wavelet is a smooth, well localized function. Wavelet coefficients are further defined by

A -normalization is used (rather than the classical -normalization), as it is better suited to express scale invariance relationships, as shown in (5) below.

Let denote a function satisfying (2) with , i.e. such that

then, clearly, its wavelet coefficients satisfy

Similarly, in the probabilistic setting, if (3) holds, then the (infinite) sequences of random vectors satisfy the following property:

| (5) |

Other probabilistic properties have simple wavelet counterparts; let us mention a few of them.

Let be a Markov process, i.e. a stochastic process satisfying the property

typical examples of Markov processes are supplied by Brownian motion, or, more generally, by Lévy processes, i.e. processes with stationary and independent increments. Because wavelets have vanishing integrals, the Markov property implies that, if the supports of the are disjoint, then the corresponding coefficients are independent random variables.

Recall that a stochastic process has stationary increments iff

typical examples are fractional Brownian motions, or Lévy processes. If has stationary increments, then

| (6) |

Note that this property holds for each given , but implies no relationship between wavelet coefficients at different scales; however, if is a selfsimilar process of exponent with stationary increments, then it follows from (5) and (6) that the random variables all share the same law (for all and ).

A random variable has a stable distribution iff

where and are independent copies of . A random process is stable if all linear combinations of the are stable. This property implies that the wavelet coefficients of a stable process are stable random variables. Further, it can actually be shown that any finite collection of wavelet coefficients forms a stable vector (cf. e.g., [7, 162, 163, 175]).

Finally, if is a Gaussian process, then any finite collection of its wavelet coefficients is a Gaussian vector. Note however a common pitfall: Unless some additional stationarity property holds, the sole Gaussianity hypothesis for the marginal distribution of the process does not imply that the empirical distributions of the coefficients are close to Gaussian: It can only be said that they will consist of Gaussian mixtures (which can strongly depart from a Gaussian distribution). The statistical properties of wavelet coefficients of fBm were studied in depth in the seminal works of P. Flandrin [71, 72] that significantly contributed to the popularity of wavelet transforms in the analysis of scale invariance.

Among the results that we mentioned above, it is important to draw a difference between those that are a consequence of the sole fact that wavelet coefficients are defined as a linear mapping, and therefore would hold for any other basis (Gaussianity and stability) and those that are the consequence of the particular algorithmic nature of wavelets (selfsimilarity and stationarity). These (rather straightforward) results are either implicit or explicit in the literature concerning wavelet analysis of stochastic processes; however, in order to give a flavor of the ideas and methods involved, we give a proof of (5) at the end of Section 4.1.

Further, let us mention that all these wavelet properties do not constitute exact characterizations of the probabilistic properties of the corresponding processes, but only implications, because of a deficiency of wavelet expansions that will be explained in Section 4.1.

1.3 Beyond selfsimilarity: Multifractal analysis

Beyond selfsimilarity. An obvious drawback of using exact probabilistic properties, such as selfsimilarity, or independence of increments is that, though they can relevantly model physical properties of the underlying data, they usually do not hold exactly for real-life signals.

Two limitations of selfsimilarity can classically be pointed out.

First, the scaling properties may not hold for all scales (as required by the mathematical definition of selfsimilarity).

This may be due to noise corruption or it may also result from the fact that the physical phenomena implying those properties intrinsically act over a finite range of scales only.

Second, the appealing property of selfsimilarity (the sole selfsimilarity parameter contains the essence of the model) may also constitute its limitation: Can one really expect that the complexity of real-world data can be accurately encapsulated in one single parameter only?

Let us examine such issues.

Multiplicative Cascades. As mentioned above, B. Mandelbrot coined fBm as one of the major candidates to model scale invariance. However, combining selfsimilarity and stationary increments implies that all finite moments of the increments of fBm (and of any process whose definition gathers these two properties) verify, for all s such that [168, 65],

| (7) |

Though very powerful, this result can also be regarded as a severe limitation for applications, where empirical estimates of moments, , computed on the data assuming ergodicity, may instead behave as: , for a range of , and where is, by construction, a concave function, but is not necessarily linear.

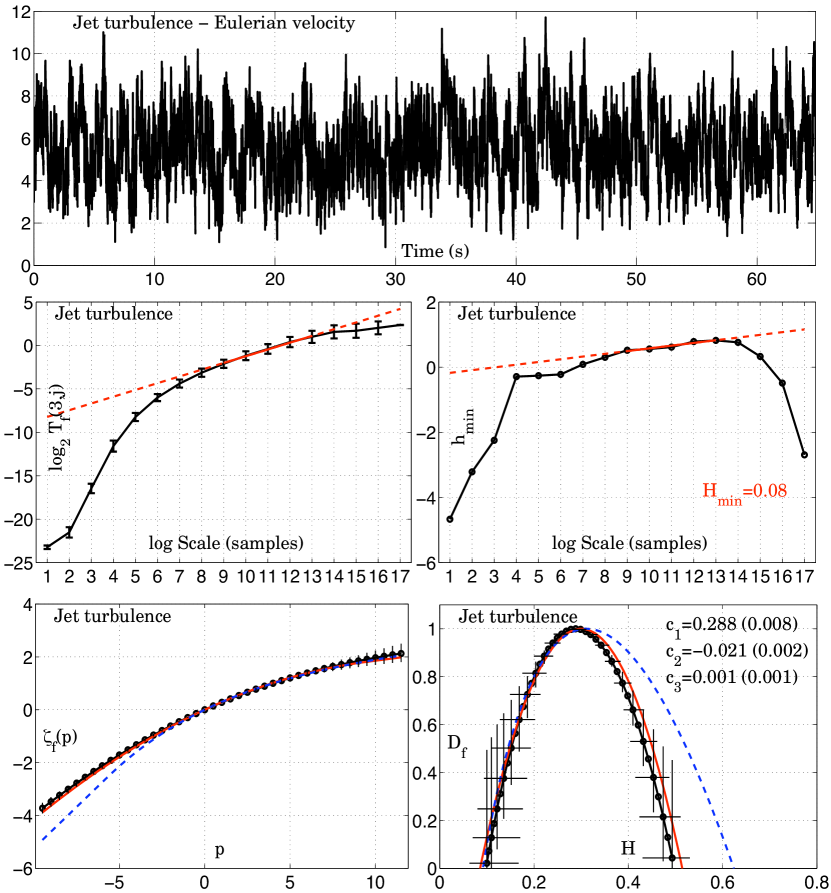

This is notably the case when analyzing velocity or dissipation fields in the study of hydrodynamic turbulence where strictly concave scaling functions were obtained (cf. e.g., [76] for a review of experimental results).

This was justified by a celebrated argument due to Kolmogorov and Obukhov in 1962 [108, 149, 186]:

Navier-Stokes equation, governing fluid motions, implies that the (third power of the) gradient of the velocity is proportional to the mean of the local energy dissipated into a bulk of size : .

If is constant, then any power scales as .

But, in turbulence, is not constant over space and should rather be regarded as a random variable, hence implying: which naturally implies a general scaling of the form , with which is likely to depart from the linear behavior which is implied by the selfsimilarity hypothesis.

To account for this form of observed scale invariance, new stochastic models have been proposed: Multiplicative cascades. Numerous declinations of cascades were proposed in the literature of hydrodynamic turbulence to model data, see e.g., [76] (on the mathematical side, see the book [26] for a detailed review, and also the contribution of J. Barral and J. Peyrière [32] in the present volume, for a lighter introduction). For the sake of simplicity, the simplest (1D) formulation is presented here; however, it contains the key ingredients present in all other more general cascade models. Starting from an interval (arbitrarily chosen as the unit interval), a cascade is constructed as the repetition of the following procedure ( being an arbitrary integer): At iteration , each of the sub-intervals , obtained at iteration , is split into intervals of the same length ; a mean- positive random variable (drawn independently and with identical distribution) is associated with each . After an infinite number of iterations, the cascade is defined as the limit (in the sense of measures) of the finite products

Mathematically, this sequence of measures converges under mild conditions on the distribution of the multipliers (cf. [103]). Such constructions and variations have been massively used to model the Richardson energy cascade implied by the Navier-Stokes equation [164] (cf. [76] for a review of such models). One of the major contributions of B. Mandelbrot to the field of hydrodynamic turbulence was proposed in [124], where he presented the themes and variations on multiplicative cascades in a single framework and studied their common properties, notably in terms of scale invariance. This celebrated contribution paved the way towards the creation of the word multifractal, to the notions of multifractal processes and multifractal analysis, where multi here refers to the fact that instead of a single scaling exponent , a whole family of exponents are needed for a better description of the data. B. Mandelbrot also discussed the importance of the distribution of the multipliers and how multiplicative cascades may significantly depart from log-normal statistics that could be obtained from a simplistic argument:

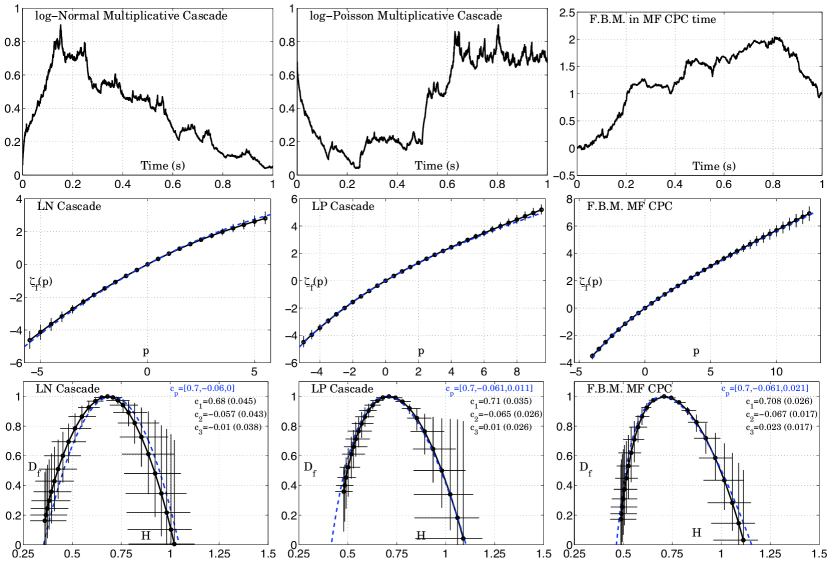

where tends to a normal distribution, hence should tend to a log-normal distribution (cf. [132, 123], and also [186]). This opened many research tracks proposing alternatives to the log-normal model, the most celebrated one being the log-Poisson model [172]. This will be further discussed in Section 6.1. Much later, multiplicative cascades were connected to Compound Poisson cascades and further to Infinitely Divisible Distributions (cf. e.g., [148]). Mandelbrot himself contributed to these latter developments with the earliest vision of Compound Poisson Cascades [30] and also with his celebrated fBm in multifractal time [135], which will be considered in Section 6.2. This gave birth to multiple constructions of processes with multifractal properties (cf. e.g., [19, 23, 24, 33, 34, 48, 49]).

Compared with the concept of selfsimilarity (and in particular fBm), which is naturally related to random walks and hence to additive constructions, cascades are, by construction, tied to a multiplicative structure.

This deep difference in nature explains why practitioners, for real-world applications, are often eager to distinguish between these two classes of models.

This distinction is however often misleadingly confused with the opposition of mono- versus multi-fractal processes.

This will be further discussed in Section 5.4.

Scaling functions and scaling exponents. The empirical observations of strictly concave scaling exponents, made on hydrodynamic turbulence data, led to the design of a new tool for analysis: Scaling functions. Let . The Kolmogorov scaling function of (see [107]) is the function implicitly defined by the relationship

| (8) |

the symbol meaning that

| (9) |

Note that this limit does not necessarily always exist; when it does, it reflects the fact that shows clear scaling properties (and it is needed to hold in order to numerically compute scaling functions). However, we are not aware of any simple and general mathematical assumption implying that it does; therefore, it is important to formulate a mathematical and slightly more general definition of the scaling function, which is well defined for any function :

| (10) |

It is important to note that, if data are smooth (i.e., if one obtains that ), then one has to use differences of order 2 or more in (9) and (10) in order to define correctly the scaling function.

For application to real-world data, which are only available with a finite time or space resolution, (9) can be interpreted as a linear regression of the log of the left hand side of (8) vs. .

The same remark holds for the other scaling functions that we will meet.

Multifractal analysis. In essence, multifractal analysis consists in the determination of scaling functions (variants to the original proposition of Kolmogorov will be considered later). Such scaling functions can then be involved into classification or model selection procedures. Scaling functions constitute a much more flexible analysis tool than the strict relation (2). For many different real-world data stemming from applications of various natures, relationships such as (8) are found to hold, while this is usually not the case for (2), see Section 6 for illustrations on real world data.

An obvious key advantage of the use of the scaling function is that its dependence in can take a large variety of forms, hence providing versatility in adjustment to data. Therefore, multifractal analysis, being based on a whole function (the scaling function , or some of its variants introduced below), rather than on the single selfsimilarity exponent, yields much richer tools for classification or model selection. The scaling function however satisfies a few constraints, for example, it has to be a concave non-decreasing function (cf. e.g., [99, 183]).

Another fundamental difference between the selfsimilarity exponent and the scaling function lies in the fact that, for stochastic processes, the selfsimilarity exponent is, by definition, a deterministic quantity, whereas the scaling function is constructed for each sample path, and therefore is a priori defined as a random quantity.

And, indeed, even if the limit in (10) turns out to be deterministic for many examples of stochastic processes (such as fBm, Lévy processes, or multiplicative cascades, for instance), it is not always the case, as shown, for instance, by the example of fairly general classes of Markov processes, such as the ones studied in [27].

Note that, if a stationarity assumption can be reasonably assumed, then one can define a deterministic quantity by taking an expectation instead of a space average in (10), which leads to a definition of the scaling function through moments of increments.

Under appropriate ergodicity assumptions, time (or space) averages can be shown to coincide with ensemble averages, and, in this case, both approaches lead to the same scaling functions, see [165] for a discussion (checking such ergodicity assumptions for experimental data does, however, not seem feasible and can become an intricate issue, cf. [112]).

1.4 Data analysis and Signal Processing

In its early ages, the concept of scale invariance has been deeply tied to that of -processes, that is, to second order stationary random processes whose power spectral density behave as a power law with respect to frequency over a broad range of frequencies: , where the frequency satisfies , with . From that starting point, spectrum analysis was regarded as the natural tool to analyze scale invariance and estimate the corresponding scaling parameter . In that context, the contribution of B. Mandelbrot and J. Van Ness [138] can be regarded as seminal since, elaborating on [85], it put forward fBm, and its increment process, fractional Gaussian noise (fGn), as a model that extends and encompasses -processes: fGn is a -process, with , fBm is a non-stationary process that shares the same scale invariance intuition. This change of paradigm immediately raised the need for new and generic estimation tools for measuring the parameter from real world data, which were no longer based on classical spectrum estimation. Relying strongly on the intuitions beyond selfsimilarity and long memory (a concept deeply tied with selfsimilarity, cf. e.g. [36]), the R/S estimator (for Range-Scale Statistics) has been the first such tool proposed in the literature, to the study of which B. Mandelbrot also contributed [134, 139, 140]. The R/S estimator has notably been used in finance and economy, in particular by D. Strauss-Kahn and his collaborators, (see e.g., [82, 157]). Later, in the 90s, with the advent of wavelet transforms, seminal contributions studied the properties of the wavelet coefficients of fBm [71, 72, 177] and opened avenues towards accurate and robust wavelet-based estimations of the selfsimilarity parameter [3, 8, 179, 180].

To some extent, the present contribution can be read as a tribute to ideas and tracks originally addressed by B. Mandelbrot (and others) aiming at estimating the parameters characterizing scale invariance in real world data: The wavelet based formulations of multifractal analysis (i.e., of the estimation from data of scaling functions and multifractal spectra) devised in Sections 4 and 5 can be read as continuations and extensions of these pioneering works towards richer models and refined variations on the characterization of scale invariance.

1.5 Goals and Outline

In Section 2, it is explained how various paradigms pertinent in fractal geometry, such as selfsimilarity or fractal dimension, can be shifted to the setting of functions, thus leading to the introductions of several scaling functions. In Section 3, it is shown how such scaling functions can be reinterpreted in terms of function space regularity: On one hand, it allows to derive some of their properties; on other hand, it paves the way towards equivalent formulations that will be derived later. Section 4 introduces wavelet techniques, which allow to reformulate these former notions in a more efficient setting, from both a theoretical and pratical point of view. Section 5 introduces the multifractal formalism, which offers a new interpretation for scaling functions in terms of fractal dimensions of the sets of points where the functions considered has a given pointwise smoothness. Applications of the tools and techniques developed here will be given in Section 6, aiming at illustrating the various aspects of multifractal analysis addressed in the course of this contribution. Such applications are chosen either because B. Mandelbrot significantly contributed to their analysis and/or because they illustrate particularly well some concepts which will be developed here. The selected applications stem from widely different backgrounds, ranging from Turbulence to Internet, Heart Beat Variability and Finance (in 1D), and from natural textures to paintings by famous masters (in 2D), thus showing the extremely rich possibilities of these new techniques.

2 From fractals to multifractals

2.1 Scaling and Fractals

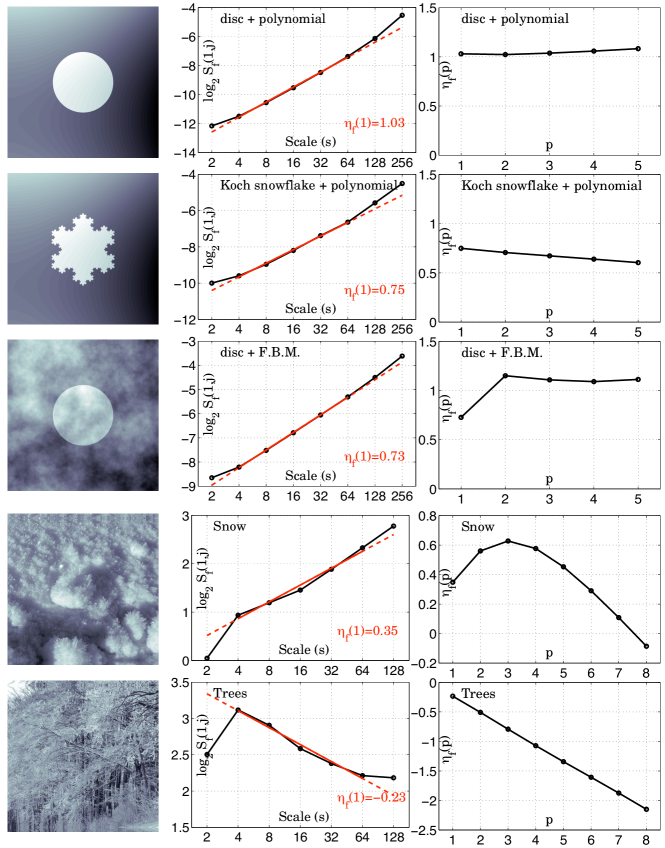

Dynamics versus Geometry. One of the major contributions of B. Mandelbrot has been to understand the benefits of using mathematical tools and objects already defined in earlier works but regarded as incidental, such as fractal dimensions, in order to explore the world of irregular sets, to classify them and to study their properties. A key example is supplied by the Von Koch curve (cf. e.g., [155, 170] and Fig. 1). The important role that B. Mandelbrot gave to this curve is typical of his way of diverting a mathematical object from its initial purpose and of making it fit to his own views; indeed, it was initially introduced as an example of the graph of a continuous, nowhere differentiable function (see the book by G. Edgar [64], which made available many classic articles of historical importance in fractal analysis). B. Mandelbrot shifted the status of this curve from a peripherical example of strange set to a central element in the construction of his theory, and he baptized it the Von Koch snowflake, a typical example of the poetic accuracy that B. Mandelbrot displayed for coining new names (other examples, being the devil’s staircase, Lévy flights, Noah or Joseph effects,…). This example will be revisited below in Section 4.2 to validate a numerical method for multifractal analysis.

Two features — dynamics and geometry — are intimately tied into the Von Koch snowflake: It is constructed from (and hence invariant under) a dynamical system consisting of the iterative repetition of a split and reproduce procedure (highly reminiscent of the split and multiply procedure entering the definition of multiplicative cascades, cf. Section 1.3 earlier); the resulting geometrical set has well defined geometrical properties that can

be put into light through the determination of its box dimension, whose definition we now recall.

Dimensions.

Definition 1

Let be a bounded subset of ; if , let be the smallest number such that there exists a covering of by balls of radius .

The upper and lower box dimension of are respectively given by

| (11) |

When both limits coincide (as it is the case for the Von Koch snowflake), they are referred to as the box dimension of the set :

| (12) |

This implies that displays an approximate power-law behavior with respect to scales:

| (13) |

a major feature that makes the box dimension useful for practical applications, as it can be computed through a linear regression in a log-log plot.

The strong similarity (in a geometric setting) between the box dimension and the Kolmogorov scaling function (10) can now clearly be seen. The latter is also defined as a linear regression in log-log plots (log of the -th moments vs. the log of the scales): Both objects hence fall under the general heading of scale invariance.

This relationship between geometric and analytic quantities is not only formal: On one hand, the determination of scaling functions has important consequences in the numerical determination of the fractal dimensions of graphs, and related quantities, such as the -variation, see Section 2.2 ; on other hand, the multifractal formalism, exposed in Section 5, allows to draw relationships between scaling functions and the dimensions of other types of sets, defined in a different way: They are the sets of points where the function considered has a given pointwise smoothness (see Definition 3). Note however that the notion of dimension used in the context of the multifractal formalism differs from the box dimension: One has to use the Hausdorff dimension which is now defined (see [66]).

Definition 2

Let be a subset of . If and , let

where is an -covering of , i.e. a covering of by bounded sets of diameters . (The infimum is therefore taken on all -coverings.)

For any , the -dimensional Hausdorff measure of is

One can show that there exists such that

This critical is called the Hausdorff dimension of , and is denoted by .

An important convention, in view of the use of these dimensions in the context supplied by the multifractal formalism, is that, if is empty, then .

In contradistinction with the box dimension, the Hausdorff dimension is not obtained through a regression on log-log plots of quantities that are computable on real-life data; therefore it is fitted to theoretical questions and can not be used directly in signal or image processing; however, we will see that the multifractal formalism allows to bypass this problem by supplying an indirect way to compute such dimensions.

Scaling, dimensions and dynamics. The discussions in this section aimed at illustrating the interplay between three different notions: The signal processing notion of scaling, or scale invariance, the geometrical notion of dimension and the dynamic notion of constructive split/multiply or split/reproduce procedures. Note that the relationships between fractals and dynamics have been investigated by B. Mandelbrot, see [137] for a panorama. The dynamic constructive procedures of geometrical sets (e.g., Von Koch snowflake) or of functions (e.g., multiplicative cascades) result in geometrical properties of the constructed object. These geometrical properties can be theoretically characterized using dimensions. These dimensions can be measured practically if they additionally imply the existence of power law behaviours (or scaling) (such as those reported in (13) or (8)). When the constructive procedure underlying the geometrical sets or functions analyzed are known and parametrized, the measure of geometrical dimension may enable to recover the corresponding dynamic parameters. However this is certainly no more true outside of a parametric model: Many different dynamic constructions may yield the same dimensions. Therefore, the inverse problem of identifying the nature of the dynamic or even its existence from the sole measure of dimensions is ill-posed and can not be achieved in general. Specifically, a concave scaling function, that hence departs from linearity in , does not prove the existence of an underlying cascade mechanism in data.

2.2 From graph box-dimensions to -variation: The oscillation scaling function

From graphs to functions. For data analysis purposes, an obvious difference between the determination of the fractal dimension of a set and the scaling function of a function has already been pointed out: While the former reduces to a single number, the latter consists of a whole function of the variable , hence yields a much richer tool for classification and identification.

However, the gap can easily be bridged in the case where the geometrical set consists of the graph, denoted , of the function .

Let us examine how a slight extension of the notion of box dimension of a graph allows to introduce a dependency on a variable , and hence a family of exponents whose definition bears some similarity with the Kolmogorov scaling function.

Oscillations. Let be a continuous function (the set plays no specific role and is taken here just to fix ideas). If , let denote the oscillation of on the set , i.e.

Note that this notion defines only first order oscillation; if is a convex set, second order oscillation (which has to be used for smooth functions) is defined as

(and so on for higher order oscillation). Let denote the dyadic cube of width that contains ; will denote the set of such dyadic cubes of width . Let now be given. The -oscillation at scale of is defined as

| (14) |

This quantity allows to define the oscillation scaling function of as

| (15) |

Box dimension of graphs versus the oscillation scaling function. Since is continuous, the graph of is a bounded subset of . First, note that, in the definition of the upper box dimension (11), one can rather consider coverings by dyadic cubes of side ; indeed each optimal ball of width used in the covering is included in at most dyadic cubes of width ; and, in the other way, a dyadic cube is contained in the ball of same center and width . Therefore using dyadic cubes (instead of optimally positioned balls) only changes prefactors in and not scaling exponents.

Let us now consider the dyadic cubes used in the covering of the graph of and which stand above a dyadic cube of dimension and width included in . Their number clearly satisfies:

This, together with the definition of the oscillation scaling function, implies that for ,

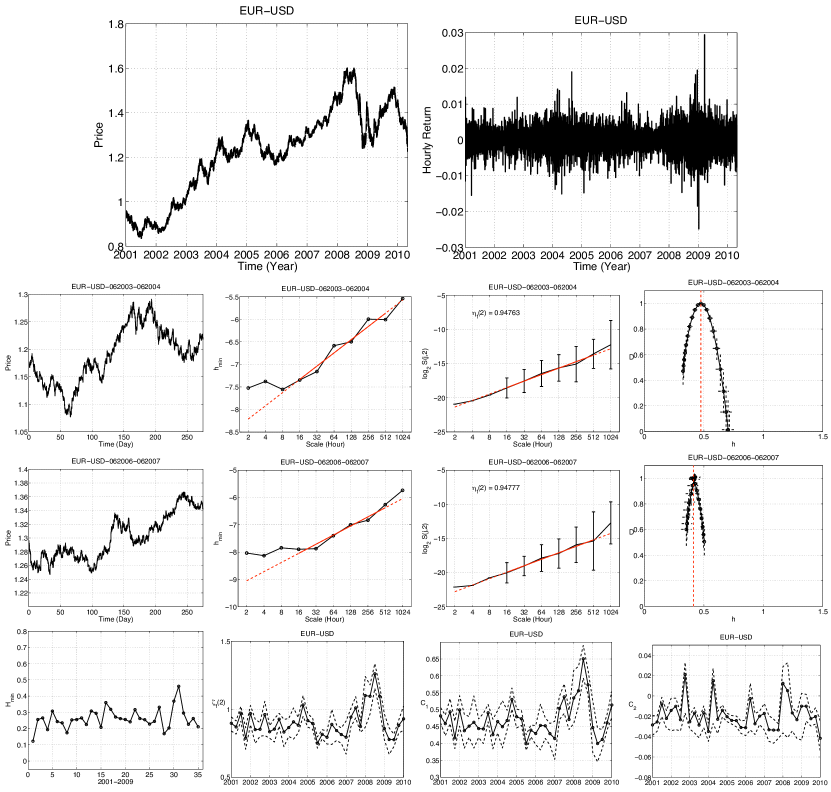

However, the oscillation scaling function can be used for other (positive) values of , and therefore yields a classification tool with similar potentialities as those offered by the Kolmogorov scaling function. We will see an example of its use in finance, in order to estimate quadratic variations, see Section 6.2.

An extension of the oscillation scaling function will be defined later, defined through wavelet quantities: The leader scaling function, cf. Section 4.4.

Box dimension and selfsimilarity exponent. For some selfsimilar functions and processes, a direct relationship between the box dimension of their graphs and their selfsimilarity exponent can be drawn. For instance, one-dimensional fBm of selfsimilarity index has a graph of box dimension , and the same result holds in a deterministic setting for the graphs of the Weierstrass-Mandelbrot functions, which have box dimension (see [67, 68] where similar results can also be found for Hausdorff dimensions of graphs). Note that B. Mandelbrot himself had already drawn connections between selfsimilarity and fractal dimension (cf. e.g., [129, 130, 131]).

3 Geometry vs. Analysis

The shift from fractal geometry to multifractal analysis essentially consists in replacing the study of selfsimilarity, and of geometric properties of sets, by the study of analytic properties of functions. This shift has several facets: First, in Section 3.1, we will explore relationships between selfsimilarity and pointwise regularity, two concepts which are often confused, and actually have subtle interplays which are far from being fully understood today. Second, in Section 3.2, we will give the interpretation of scaling functions in terms of function space regularity, which allows to use the full apparatus of functional analysis. Finally, in Section 5, the multifractal formalism is introduced: It allows to interpret the (Legendre transform of the) scaling function in terms of dimensions of sets of points where has a given pointwise Hölder regularity.

3.1 Pointwise Hölder regularity

Hölder exponent. Selfsimilarity of either deterministic functions or stochastic processes is intimately related with their local regularity. Before explaining these relationships, let us start by recalling the notion of pointwise Hölder regularity (alternative notions of pointwise regularity, have also been considered, allowing to deal with functions that are not locally bounded, see [95, 96, 97, 102]).

Definition 3

Let be a locally bounded function, and let ; belongs to if there exist , and a polynomial of degree less than such that

The Hölder exponent of at is

When Hölder exponents lie between and , the Taylor polynomial boils down to and the definition of the Hölder exponent heuristically means that,

For these cases, a relationship can be drawn with the local oscillation considered in Section 2.2. Indeed, let denote the dyadic cube of width that contains , and the cube of same center and 3 times wider (it therefore contains dyadic cubes of width ). One easily checks that, if , then

| (16) |

This formula puts into light the fact that the Hölder exponent can theoretically be obtained through linear regressions on log-log plots of the oscillations versus the log of the scale.

However, in practice, this formula has found little direct applications for two reasons:

One is that alternative formulas based on wavelet leaders (cf. Section 4.4) are numerically more stable, and the other is that many types of signals display an extremely erratic Hölder exponent, so that the instability of its determination is intrinsic, no matter which method is used.

We will see in Section 4.4 how to turn this deeper obstruction.

Implications of selfsimilarity on regularity and dimensions. The Hölder exponent sometimes coincides with the selfsimilarity exponent, hence resulting in a confusing identification of the two quantities. This is the case for two frequently used examples: Weierstrass-Mandelbrot functions and fBm sample paths have everywhere the same and constant Hölder exponent, . The theoretical definition of such examples essentially relies on a single parameter, and therefore it comes as no surprise that, for such simple functions with a constant Hölder exponent, both their selfsimilarity and their local regularity are governed by this sole parameter (and coincide). Similarly, their scaling functions are linear in , and therefore are governed by one parameter only, the slope of this linear function, which, for these two examples, is .

However, one should not infer hasty conclusions from these examples: Selfsimilar processes with stationary increments do not always possess a single Hölder exponent that corresponds to the selfsimilarity exponent, as shown by the example of stable Lévy processes: These processes are selfsimilar of exponent , where is the stability parameter. In addition, their scaling function is linear in only for small enough:

This is intimately related with the fact that their Hölder exponent is not constant: Sample paths of a stable Lévy process have, for each , a dense set of points where their Hölder exponent takes the value (cf. [91] for Lévy processes, and [63] for Lévy sheets indexed by ). Thus, their Hölder exponents jump in a very erratic manner from point to point, as a consequence of the high variability of the increments: Indeed, their distributions only have power-law decay, and therefore (in strong contradistinction with Gaussian variables) can take extremely large values with a relatively large probability; the importance of this phenomenon in applications was largely undervalued in the past, until B. Mandelbrot pointed out its possibly dramatic consequences, referring to them in a colorful way as Noah’s effect.

Let us now be more explicit concerning the relationships between selfsimilarity and Hölder regularity. A first result relates selfsimilarity with uniform regularity of sample paths.

Proposition 1

Assume that is a selfsimilar process of exponent , with stationary increments, and such that for some . Then,

| (17) |

The proof follows directly from the Kolmogorov-Chentsov theorem: Recall that this theorem asserts that, if is a random process satisfying

then,

(see [55]). But, if is selfsimilar, then

| (18) |

and the proposition follows.

We will reinterpret this result in Section 4.3 when the uniform Hölder exponent will be introduced. The following result goes in the opposite direction: It relates selfsimilarity with irregularity of sample paths.

Proposition 2

Let be a selfsimilar process of exponent , with stationary increments, and which satisfies , i.e. the law of at time (or at any other time ) does not contain a Dirac mass at the origin. Then

| (19) |

Proof: We first prove the result for . The assumption implies the existence of a decreasing sequence which converges to 0 and satisfies

Let . Then . Therefore

The Borel-Cantelli lemma implies that a.s. a finite number of these events happens, and therefore . By the stationarity of increments, this argument holds the same at each , i.e.

and Fubini’s theorem allows to conclude that (19) holds.

In particular, assume that satisfies the assumptions of Proposition 2, and also of Proposition 1 for any . Then, both results put together show that, in this case, (17) is optimal. Relationships between selfsimilarity and Hölder exponents for selfsimilar processes will be further investigated in Section 5.4.

Note that, without additional assumptions, one can not expect results more precise than those given by Propositions 1 and 2, as shown by the subcase of stable, selfsimilar processes with stationary increments, see [109, 168]: Let denote the selfsimilarity index of such a process, and its stability index. First, note that there is no direct relationship between , and Hölder regularity: They always satisfy

the case of fBm is misleadingly simple since it satisfies

however Lévy processes satisfy and takes all values in .

Finally, Lévy fractional stable processes have nowhere locally bounded stable sample paths if , and continuous sample paths if (see Section 4.3 for a more precise result).

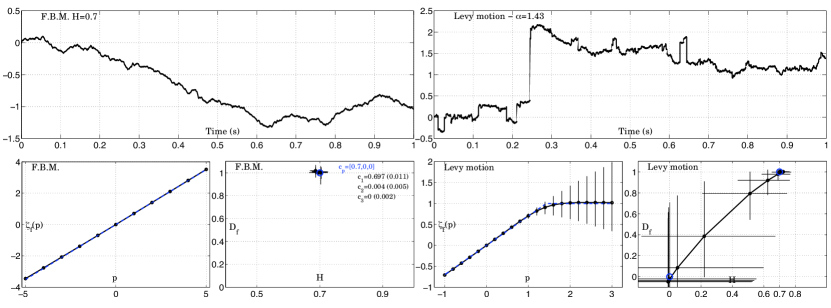

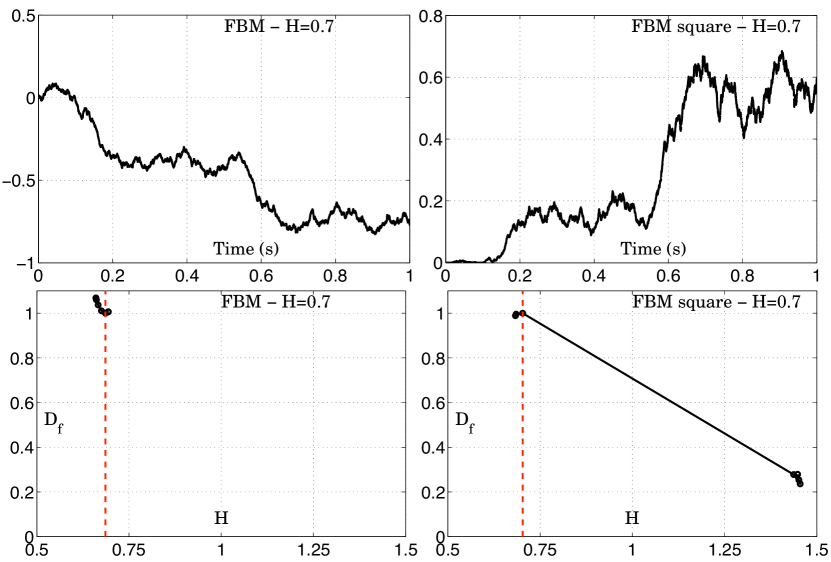

Sample paths of selfsimilar processes (with stationary increments) together with their scaling functions (and multifractal spectra) are illustrated in Fig. 2 in Section 5.2.

Let us now mention a few results concerning the relationship between selfsimilarity and fractional dimensions. We start with fBm which again is the simplest and best understood case. Such results are of two types:

- •

-

•

Relationship between the Hausdorff dimension of a set and of its image (see see [173] and references therein)

(20)

We will see that this second result has important consequences for the multifractal analysis of some finance models proposed by L. Calvet, A. Fisher, and B. Mandelbrot, see (51).

Partial results of these two types also hold for other selfsimilar processes, see [173].

Regularity versus dimension: The mass distribution principle. The example of stable Lévy processes suggests that the most fruitful connection to be drawn does not involve the notion of selfsimilarity, but rather should connect scaling functions with pointwise regularity. This is precisely what the multifractal formalism performs, as it establishes a relationship between scaling functions and the Hausdorff dimensions of the isohölder sets of defined by

| (21) |

The multifractal formalism will be detailed in Section 5. A clue which shows that such relationships are natural can however be immediately given, via the mass distribution principle which goes back to Besicovitch (see Proposition 3 below). This principle establishes a connection between the dimension of a set and the regularity of the measures that this set can carry. The motivation for it stems from the following remark. Mathematically, it is easy to obtain upper bounds for the Hausdorff dimension of a set : Indeed, any well chosen sequence of particular -coverings (for a sequence ) yields an upper bound. To the opposite, obtaining a lower bound by a direct application of the definition is more difficult, since it requires to consider all possible -coverings of . The advantage of the mass distribution principle is that it allows to obtain lower bounds of Hausdorff dimensions by just constructing one measure carried by the set . Recall that a measure is carried by if . Note, however, that a set satisfying such a definition is not unique; In particular, this notion should not be mistaken with the more usual one of support of the measure, which is uniquely defined as the intersection of all closed sets carrying . For example, consider the measure

(where denotes the Dirac mass at the point ). The support of this measure is the interval , but it is (also) carried by the (much smaller) set .

Proposition 3

Let be a probability measure carried by . Assume that there exists , and such that, for any ball of diameter less than , satisfies the following uniform regularity assumption

Then the -dimensional measure of satisfies: , and therefore .

Proof: Let be an arbitrary -covering of . Then

The result follows by passing to the limit when .

3.2 Scaling functions vs. function spaces

From scaling functions to function spaces. Kolmogorov scaling function

(as defined by (10)) receives a

function space interpretation, which is important for several reasons.

On one hand, it allows to derive a number of its mathematical properties, and on other hand, it points towards variants and extensions of this scaling function, yielding sharper information on the singularities existing in data, and therefore offering a deeper understanding of the multifractal formalism.

Function space interpretation. The function space interpretation of the Kolmogorov scaling function can be obtained through the use of the spaces defined as follows.

Definition 4

Let , and ; if and

| (22) |

Note that larger smoothness indices are reached by replacing in the definition the first-order difference by higher and higher order differences: ,… (which is coherent with the remark just after the introduction of Kolmogorov scaling function (10), where, there too, higher order differences have to be introduced in order to deal with smooth functions ).

It follows from (8) and (22) that,

| (23) |

In other words, the scaling function allows to determine within which spaces data are contained, for . The reformulation supplied by (23) has several advantages: It will lead to a better numerical implementation, based on wavelet coefficients, and it will have the additional advantage of yielding a natural extension of these function spaces to ; this, in turn, will lead to a scaling function also defined for , therefore supplying a more powerful tool for classification, see Section 4.2. Note that the reason why Kolmogorov scaling function cannot be directly extended to is that spaces and the spaces which are derived from them (such as ) do not make sense for ; indeed Definition 4 for leads to mathematical inconsistencies (spaces of functions thus defined would not necessarily be included in spaces of distributions).

Another advantage of the function space interpretation of the scaling function is that it allows to draw relationships with areas of modeling where the a priori assumptions which are made are function space regularity assumptions.

Let us mention two famous examples, which will be further used as illustrations for the wavelet methods developed in the next section: Bounded Variations (BV) modeling in image processing (cf. Section 4.2), and bounded quadratic variation hypothesis in finance (cf. Sections 4.4 and 6.2, this latter case being related with the determination of the oscillation scaling functions (15)).

Bounded variations and image processing. A function belongs to the space BV, i.e., has bounded variation, if its gradient, taken in the sense of distributions, is a finite (signed) measure.

A standard assumption in image processing is that real-world images can be modeled as the sum of a function which models the cartoon part, and another term which accounts for the noise and texture parts (for instance, the first “ model”, introduced by Rudin, Osher and Fatemi in 1992 ([111]) assume that , see also [129, 130]).

The BV model is motivated by the fact that if an image is composed of smooth parts separated by contours, which are piecewise smooth curves, then its gradient will be the sum of a smooth function (the gradient of the image inside the smooth parts) and Dirac masses along the edges, which are typical finite measures. On the opposite, characteristic functions of domains with fractal boundaries usually do not belong to BV, see Fig. 1 for an illustration). Therefore, a natural question in order to validate such models is to determine whether an image (or a portion an image) actually belongs to the space BV or not.

We will see in Section 4.2 how this question can be given a sharp answer using a direct extension of Kolmogorov scaling function.

Bounded quadratic variations. Another motivation for function space modeling is supplied by the finite quadratic variation hypothesis in finance. In contradistinction with the previous image processing example, this hypothesis is not deduced from a plausible intrinsic property of financial data, but rather constitutes an ad hoc regularity hypothesis which (considering the actual state of the art in stochastic analysis) is required in order to use the tools of stochastic integration. There exist several slightly different formulations of this hypothesis. One on them, which we consider here, is that the -oscillation is uniformly bounded at all scales. This means that , assumed to be defined on , satisfies

(where was defined by (14)). The definition of the oscillation scaling function (15) shows that, if , then has finite quadratic variation, and if , then this hypothesis is not valid. This will be further discussed in Section 4.2 and illustrated in Section 6.2 and Fig. 7.

4 Wavelets: A natural tool to measure global scale invariance

The general considerations developed in Section 3.2 emphasized the importance of scaling functions as a data analysis tool. To further develop this program, reformulations of scaling functions which are numerically more robust than the Kolomogorov and oscillation scaling functions introduced so far are of both practical and theoretical interests. Motivations for introducing wavelet techniques for this purpose were already mentioned in Section 1.2. We now introduce these techniques in a more detailed way, and develop and explain the benefits of rewriting scaling functions in terms of wavelet coefficients.

4.1 Wavelet bases

Orthonormal wavelet bases on exist under two slightly different forms. First, one can use functions with the following properties: The functions

| (24) |

form an orthonormal basis of . Therefore, ,

| (25) |

where the are the wavelet coefficients of , and are given by

| (26) |

Note that, in practice, discrete wavelet transform coefficients are generally not computed through the integrals (26), but instead using the discrete time convolution filter bank based pyramidal and recursive algorithm (cf. [120]), referred to as the Fast Wavelet Transform (FWT).

However, the use of such bases rises several difficulties as soon as one does not have the a priori information that .

For instance, if the only assumption available is that is a continuous and bounded function, then one can still compute wavelet coefficients of using (26) (indeed, these integrals still make sense), however, the series at the right-hand side of (25) may converge to a function which differs from .

This is due to the fact that certain special functions (which do not belong to ) have all their wavelet coefficients that vanish, and therefore, such possible components of functions will always be missed in the reconstruction formula (25).

These special functions always include polynomials, however, in the case of Daubechies compactly supported wavelets, other fractal-type functions also have this property, see [167].

This explains why, at the end of Section 1, we mentioned that the properties of wavelet coefficients of certain processes that we obtained were not characterizations: Indeed information on these special functions, as possible components of the processes, is systematically missed, whatever the information on the wavelet coefficients is.

However, this drawback can be turned by using a slightly different basis, which we now describe.

The alternative wavelet bases that will systematically be used from now on are of the following form: There exists a function and functions with the following properties: The functions

| (for and ( for and ) | (27) |

form an orthonormal basis of . In practice, we will use Daubechies compactly supported wavelets [56], which can be chosen arbitrarily smooth. Since these functions form an orthonormal basis of , it follows, as previously, that

| (28) |

the are still given by (26) and

| (29) |

This choice of basis enables to answer the following important data analysis questions (which was not permitted by the previous choice (24)): In real-world data, the a priori assumption that does not need to hold (for instance, the sample paths of standard models, such as Brownian motion, do not belong to ). As already mentioned, the sole information that the series of coefficients of a function on an orthonormal basis is square summable, does not imply that (consider the example of and the basis (24)). However, for the alternative basis given by (27), the following property now holds: Assume that is a function in with slow growth, i.e. satisfies

| (30) |

where denotes the ball of center and radius ; then the wavelet expansion (28) of converges to almost everywhere. Additionally, if the wavelet coefficients of are square summable, then (in contradistinction with what happens when using the basis (24)). Note that the slow growth assumption is a very mild one, since it is satisfied by all standard models in signal processing, and actually is necessary, in order to remain in the mathematical setting supplied by tempered distributions.

Note that one can even go further: (26) and (29) make sense even if is not a function; indeed, if one uses smooth enough wavelets, these formulas can be interpreted as a duality product between smooth functions (the wavelets) and tempered distributions. This rises the problem of determining if the series (28) converges in other functional settings, and it is indeed one of the most remarkable properties of wavelet expansions that it is very often the case. Wavelet characterizations of function spaces are detailed in [143]. Let us mention a property which is particularly useful, and shows that convergence properties of wavelet expansions are “as good as possible”: Suppose that is continuous with slow growth, i.e. that it satisfies

| (31) |

then the wavelet expansion of converges uniformly on every compact set.

However, while the differences that we pointed out between the two types of wavelet bases are important for reconstruction, they are not for the type of analysis that we will perform: Indeed, properties will be deduced from the inspection of asymptotic behaviors of wavelet coefficients at small scale, where both bases (24) and (27) coincide.

As an example of the fruitful interplay between the algorithmic structure of wavelet bases and the concept of selfsimilarity, we now prove (5). We start by recalling the definition of equality in law of stochastic processes.

Definition 5

Two vectors of : and share the same law if, for any Borel set , .

Two processes and share the same law if, , for any finite set of time points , the vectors of

share the same law.

We apply this definition to the two processes and (such as stated in (3)), which are assumed to share the same law. Taking for the domain between two parallel hyperplanes, this, in turns, implies that any finite linear combinations

share the same law. Therefore, if is a selfsimilar process of exponent , then (3) means that

| (32) |

Assume now that for almost every , the sample path of is Riemann integrable. The coefficient

is a limit of the Riemann sums

| (33) |

using (32), it follows that (33) has the same law as

which, writing , can be written

which is a Riemann sum of the integral

Passing to the limit when the largest spacing between sampling points (and therefore ) tends to 0, we obtain that

The argument that we developed for one coefficient can be reproduced similarly for an arbitrary vector of coefficients, hence (5) holds.

4.2 Wavelet Scaling Function

We now investigate properties which arise as consequences of the wavelet characterizations of function spaces.

Notations. Compact notations are used for indexing wavelets.

Instead of the three indices , dyadic cubes are used:

.

In order to keep notations as simple as possible, the index is dropped in formulas and notations, with the implicit convention that sums or suprema over indices are also taken on the index .

Accordingly, and .

The wavelet is localized near the cube :

Since we use Daubechies compactly supported wavelets,

such that

(where denotes the cube of same center as and times wider).

Finally, let denote the set of dyadic cubes which index a wavelet of scale , i.e. wavelets

of the form (note that is a subset of the dyadic cubes of size

), and will denote the union of the for .

Wavelet scaling function. A key property of wavelet expansions is that many function spaces have a simple characterization by conditions bearing on wavelet coefficients. This property has a direct consequence on the determination of the Kolmogorov scaling function. Let

| (34) |

Classical embeddings between function spaces imply that, if the wavelets are smooth enough, then the Kolmogorov scaling function can be re-expressed as (cf. [88])

| (35) |

This formulation, which, again, yields the scaling function through linear regressions in log-log plots, has several advantages when compared to the earlier version (10).

First, it allows to extend the Kolmogorov scaling function to the range ; it will be shown in Section 4.4 how to go even further and define scaling functions for negative s (see also [100] for an extension of to ).

We will call this extension of the Kolmogorov scaling function the wavelet scaling function,

but we will keep the same notation. By construction, is a concave increasing function, of derivative at most , see [99].

Wavelet regularity. Let us say a few words about the required smoothness of wavelets. The rule of thumb is that wavelets should be smoother and have more vanishing moments than the regularity index appearing in the definition of the function space. In signal processing, one is not necessarily aware beforehand of the regularity of the data. In practice, one uses smoother and smoother wavelets, and when the results do not vary, this means that smooth enough wavelets are used. (Note that this is reminiscent of the definition of the Kolmogorov scaling function where, in theory, one has to use higher and higher order differences and stop when the results are numerically stabilized.) In the following we will never specify the required smoothness, and always assume that smooth enough wavelets are used (the minimal regularity required being always easy to infer).

Note that, in the wavelet setting, one should also draw a difference between (35), which allows to define the wavelet scaling function of any function , and its use in data analysis, where scaling properties need to hold to enable measurements based on linear regressions in log-log plots.

Function space interpretation. Let us examine how the wavelet scaling function can be used in order to validate the function space assumptions discussed in Section 3.2. For instance, regarding the model, where and , the values taken by wavelet scaling function at and allow practitioners to determine if data belong to or :

-

•

If , then , and if , then

-

•

If , then and if , then .

Thus wavelet techniques allow to check if the function space assumptions which are made, e.g., in certain denoising algorithms relying on then model, are valid.

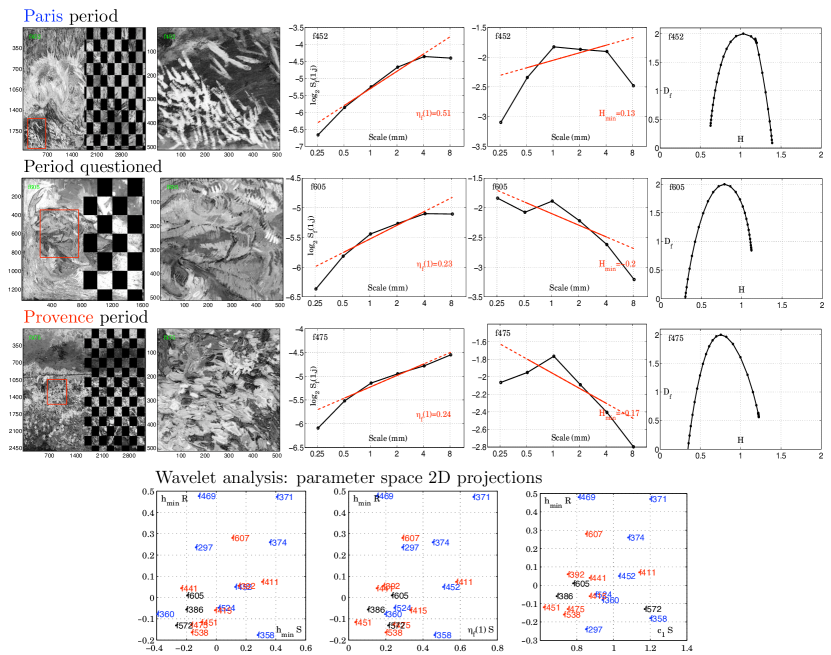

Examples of synthetic and natural images are shown in Fig. 1, together with the corresponding measures of and . The image consisting of a simple discontinuity along a circle and no texture, (i.e., a typical cartoon part of the image in the decomposition) is in BV, while the image of textures or discontinuities existing on a complicated support (such as the Von Koch snowflake) are not. Y. Gousseau and J.-M. Morel were the first authors to rise the question of finding statistical tests to verify if natural images belong to BV [77]. Our results confirm that the BV requirement is seldom met; actually, images often turn out not to be even in , as illustrated in Fig. 1 (bottom row).

4.3 Uniform Hölder exponent

It has been shown in the previous section that the Kolmogorov scaling function can be rewritten and extended as a wavelet coefficient based version.

It is hence natural to ask whether the same can be performed for the oscillation scaling function (15).

Because oscillations are defined only if is locally bounded, this condition needs to be checked in practice.

This test can be performed using the uniform Hölder exponent, which constitutes the subject of this subsection.

However, before entering technicalities, the following general question concerning function space modeling needs to be addressed.

Function space modeling. The issue of determining whether experimental data, acquired by a physical device, can be modeled by a bounded function, or not, may appear meaningless at first sight. Indeed, data can be collected only with finite size and resolution, and hence consist of finite, and thus bounded, sequences. For images, a common pitfall is to conclude that images are grey-levels, so that they necessarily take values in , and, therefore, by construction, are appropriately modeled by bounded functions. The issue is even more general regarding the whole strategy of functional space modeling: Given any finite resolution and size sequence of data practically available, they can always be extrapolated by a function, that thus belongs to any possible function space. The resolution of this paradox requires the use of the notion of scale invariance. Let us consider again the example of image modeling and address the issue of deciding whether a digital image can be modeled by a bounded function or not: It is clear that if the image is analyzed only at its finest scale, then the answer is positive. However, following the point of view that we developed until now, the problem can be reinterpreted in terms of analysis of scaling properties, over a range of available scales, and will therefore amount to determine whether an observed scaling exponent fits with those that are compatible with bounded functions, or not. The uniform Hölder exponent, which will be considered in this section, answers this question.

More generally, numerical results, obtained from finite resolution and size data, leading to conclude that data belong to certain function spaces and not to others, should actually be understood in the following way:

The function space regularity thus determined holds under the hypothesis that scaling that are observed on the range of available scales would continue to hold at finer scales if they were available.

Uniform Hölder exponent: Definition. The mathematical idea behind testing whether data are locally bounded or not is to consider boundedness as a particular case in the whole range of Lipschitz spaces, which corresponds to the regularity exponent . Let us be more specific.

The Lipschitz spaces are defined for by the conditions :

and

If , they are then defined by recursion on by the condition: if and if all its partial derivatives (taken in the sense of distributions) (for ) belong to . If , then the spaces are composed of distributions, also defined by recursion on as follows: if is a finite sum of partial derivatives (in the sense of distributions) of order 1 of elements of . This allows to define the spaces for any (note that a consistent definition using the Zygmund classes can also be supplied for , see [143], however we will not need to consider these specific values in the following). We can now define the parameter that we will use for determining boundedness.

Definition 6

The uniform Hölder exponent of a tempered distribution is

| (36) |

This definition does not make any a priori assumption: The uniform Hölder exponent is defined for any tempered distribution, and it can be positive and negative. Note that we have already met this notion: Proposition 1 can be reinterpreted as stating that, if , then . In particular the remark following the proof of Proposition 2 allows to recover the fact that, for fBm, ; additionally, it yields that the same result holds for the Rosenblatt process (see [160, 159] for the definition and the properties of the wavelet expansion of this process).

The values taken by the uniform Hölder exponent have the following interpretation:

-

•

If , then is a locally bounded function,

-

•

if , then is not a locally bounded function.

Typical examples are supplied by Lévy fractional stable processes which already appeared in Section 3.1; they satisfy , and therefore (as already mentioned) they have nowhere locally bounded stable sample paths if , and continuous sample paths if .

The importance of this exponent lies in the fact that it does not only play the role of a prerequisite (i.e., a parameter whose value has to be positive if one wants to determine the oscillation scaling function), but also that it turns out to be a very efficient parameter for discrimination.

As will be illustrated later (cf. Section 6), the classification of several types of data can actually be based on the determination of their uniform Hölder exponent.

Uniform Hölder exponent and wavelets. In practice, can be derived directly from the wavelet coefficients of through a simple regression in a log-log plot; indeed, it follows from the wavelet characterization of the spaces that:

| (37) |

This estimation procedure has been studied in more detail in [97].

Uniform Hölder exponent and applications. In Section 6, which reviews a number of real-world applications, we will see that

can be found either positive or negative depending on the nature of the application.

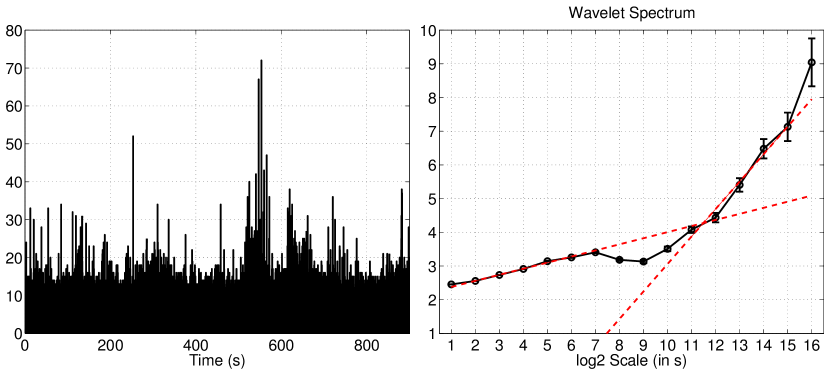

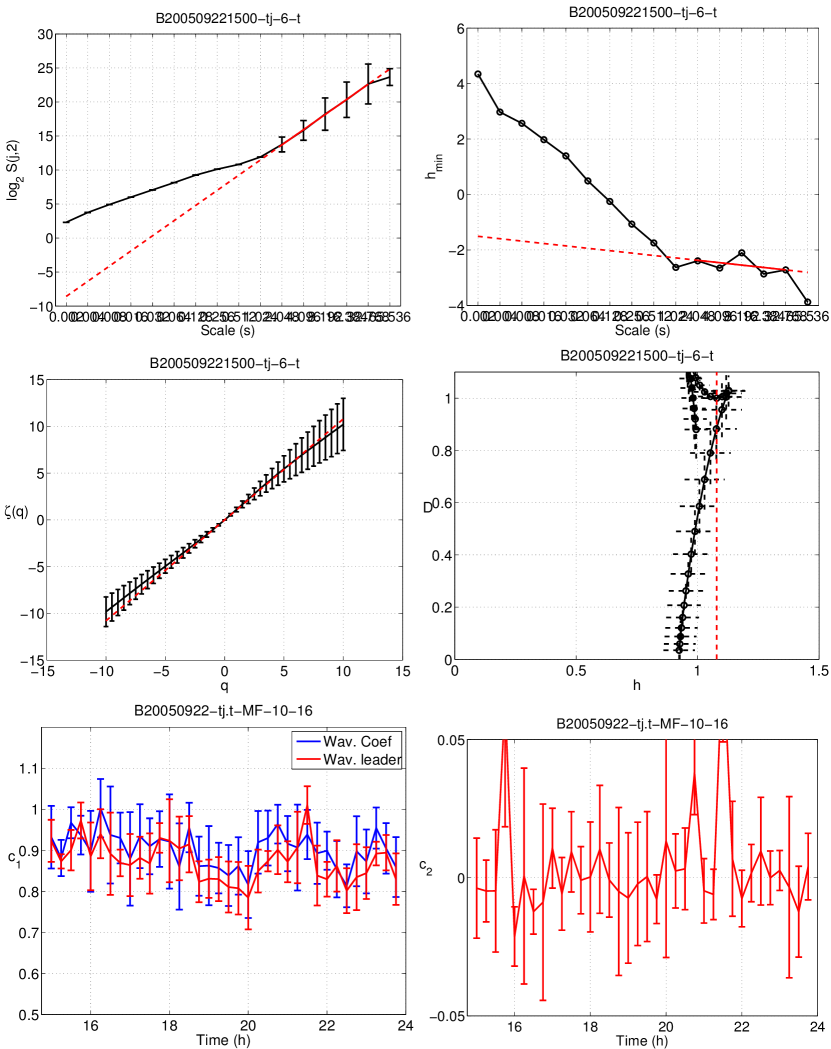

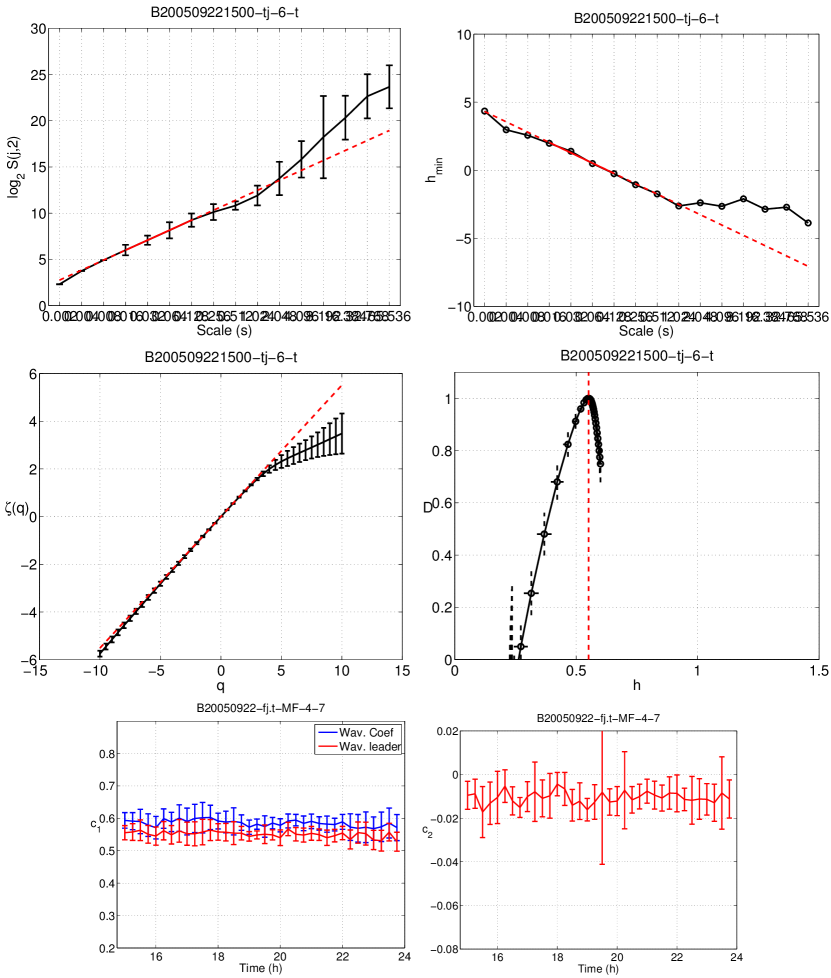

For instance, velocity turbulence data (cf. 6.1 and Fig. 6, middle row, left plot) and price time series in finance (cf. 6.2 and Fig. 7, 2nd and 3rd row row, second plots and bottom row, first plot) are found to always have , while aggregated count Internet traffic time series always have (cf. 6.4 and Figs. 10 and 11, top row, left plots).

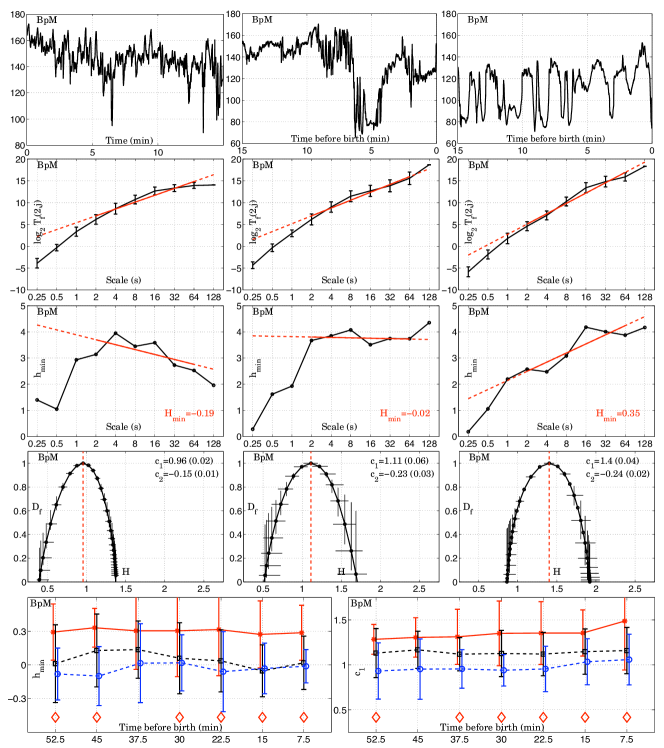

For biomedical applications (cf. e.g., fetal hear rate variability as in Section 6.3 and Fig. 8, 3rd row), as well as for image processing (cf. Section 6.5 and Fig. 12, 4th column), can commonly be found either positive or negative.

For these last two examples, is found to be a highly relevant parameter for classication purposes (cf. Fig. 8, bottom row, and Fig. 12, bottom row, respectively).

Functions that are not locally bounded and fractional integration. The examples listed above indicate that it is not uncommon in real-world application to find that . However, this does not imply that further analyses which require that (and will be described in the following) are impossible and should be discarded. Indeed, fractional integration offers a one to one way to associate with any distribution (with potentially negative ) a function , whose exponent is positive, and therefore classification can then be operated on this new function rather than on the initial data . We now expose this procedure, both from a theoretical and a practical point of view. Note that there exist many variants of the definition of fractional integration, which would however all lead to the same definition for the exponents used here, see [161] for a discussion of fractional integration, especially in the context of stochastic processes.

Definition 7

Let be a tempered distribution. Fractional integral of order of , denoted by , is defined as convolution operator which, in the Fourier domain, is the multiplication by the function .

Numerically, fractional integration is intricate to perform (because of finite size and border effect issues). However, for our purpose here, these difficulties can be circumvented by instead using pseudo-fractional integration, defined as follows.

Definition 8

Let , let be a wavelet basis whose elements belong to with ; let be a function, or a distribution, with wavelet coefficients . The pseudo-fractional integral (in the basis ) of of order , denoted by , is the function whose wavelet coefficients (on the same wavelet basis) are

This operation is numerically straightforward, and the following result shows that it retains the same pointwise and multifractal properties as exact fractional integration, see [97, 98, 99, 113].

Proposition 4

Let be a tempered distribution; then

Additionally, the pointwise Hölder exponents satisfy

This last property also holds for the leader scaling functions which will be introduced in Section 4.4 (under the same condition , so that those quantities are well defined). Therefore, in practice, for multifractal analysis, pseudo-fractional integration is preferred to exact fractional integration. These results point toward a natural strategy in order to perform the multifractal analysis of a function which is not locally bounded (or of a distribution): First determine its exponent ; then, if , perform a pseudo-fractional integration of order ; it follows that the uniform regularity exponent of is positive, and therefore that it is a bounded function, to which multifractal analysis can be applied. Yet, this strategy rises an important problem: There is no canonical choice for the fractional integration order, and the shape of the wavelet leader scaling function (see Definition 10 below) obtained after fractional integration may depend on this choice. In practice, when multifractal properties of a collection of data have to be studied, one follows the following strategy: One first determines the exponent of each signal in the database; if some of them have negative , one picks an exponent such that is positive for all signals. Under these constraints, should be picked as small as possible, so that data are modified by a fractional integration of order as small as possible. The rule of thumb practically used is to select as the smallest multiple of ensuring that is positive for all signals and to perform a pseudo-fractional integration of the same order for all signals.

4.4 Wavelet leaders

From oscillations to wavelet leaders. Our purpose is now to obtain a wavelet reformulation of the oscillation scaling function (15) (in the same way as the wavelet scaling function is the wavelet reformulation of the Kolmogorov scaling function). This requires the introduction of wavelet leaders, which are local suprema of wavelet coefficients. Let us start with a heuristic argument showing that they are natural candidates to estimate oscillation. Recall that, if denotes a dyadic cube, then denotes the cube with same center and three times wider.

Definition 9

Let be a locally bounded function satisfying (31). The wavelet leaders of are the coefficients

| (38) |

The fact that the supremum in (38) is finite is a consequence of the boundedness assumption for . Therefore, checking that is an absolute prerequisite prior to computing leaders.

Let us now sketch the reason why wavelet leaders allow to estimate the oscillation. Consider a wavelet coefficient . Since we use compactly supported wavelets,

Since wavelets have vanishing integral,

Consider now a given cube ; this argument works for any wavelet whose support is included in , so that each wavelet coefficient is bounded by . This explains why wavelet leaders are bounded by the local oscillation.

Converse estimates follow form the following argument: From (25), we get

Let be such that .

The low frequency terms () are estimated using the smoothness of the wavelets, which makes the difference small.

The terms such that (where has to be chosen correctly) are estimated using the bound of the wavelet coefficients supplied by the wavelet leader.

Finally, high frequency terms () are estimated using the uniform regularity of . This allows to obtain the required converse estimates. Note that subtle relationships between oscillations and wavelet coefficients have recently been obtained by M. Clausel and her collaborators, see e.g. [54] and references therein.

Leader scaling function. The previous heuristic argument motivates the introduction of a new scaling function, constructed on the model of the wavelet scaling function, but replacing wavelet coefficients by wavelet leaders.

Definition 10

Let be a locally bounded function with slow growth (i.e. satisfying (31)), and let

| (39) |

The leader scaling function is given by

| (40) |

The relationship between the leader scaling function and the oscillation scaling function is very similar to the one mentioned to exist between the wavelet scaling function and the Kolmogorov scaling function: They coincide when ; therefore the former extends the later for , see [93].

Let us discuss two consequences of this result: First, the fact that they coincide for implies that, if , then the upper box dimension of the graph of can be derived from the leader scaling function, see [90]:

Second, when , one can determine whether has bounded quadratic variation or not by inspecting its leader scaling function for , indeed:

-

•

If , then has bounded quadratic variation,

-

•

if , then the quadratic variation of is unbounded.

Discussion of the condition . One may wonder if the condition is really necessary in order to obtain such results. It is actually the case, and one can not obtain estimates of the quadratic variation (or of any -variation) using wavelet methods for functions which are locally bounded but do not have some uniform smoothness for the following reason: Recall that the Hilbert transform is defined as the convolution with (or alternatively as the Fourier multiplier by the function ) and consider as an example the sawtooth function which is bounded and has discontinuities at the integers. It obviously has bounded -variation for any . However, after applying the Hilbert transform to it, discontinuities are transformed into logarithmic singularities, and therefore the property of bounded -variation is lost for any value of . Since the Hilbert transform does not modify the wavelet-based quantities that we have considered, such as , , it is clear that wavelet methods can not estimate -variations of functions that have discontinuities, and therefore some uniform regularity assumption is indeed required.

In finance, for instance, checking whether is positive or not is of double importance:

First, it suggests to reject jump models for price;

second, it enables to probe the finiteness of quadratic variations, a requested property to validate the use of stochastic integration on such data.

This is further discussed in Section 6.2 and illustrated in Fig. 7.

The bonus of negative s. The leader scaling function can also be given a function space interpretation for in the framework of oscillation spaces, studied in [94, 89]. In particular, embeddings between these spaces and other, more classical, function spaces (such as Besov spaces) allow to derive an important relationship between the two scaling functions constructed through wavelet coefficients, see [93].

Proposition 5

Let be a function satisfying . Then

Let be the “critical exponent” defined by the condition , then

An important property of the leader scaling function is that it is well defined also for , although it can no longer receive a function space interpretation. By well defined, it is meant that it has the following robustness properties if the wavelets belong to the Schwartz class (partial results still hold otherwise), see [98, 99]:

-

•

is independent of the wavelet basis.

-

•

is invariant under the addition of a perturbation.

-

•

is invariant under a change of variable.

The invariance under a smooth change of variable is a mandatory property for texture classification: Indeed, it is needed that natural textures can be recognized even after the deformation produced by setting them on smooth surfaces.

The possibility of involving negative s in analysis can turn crucial: A celebrated example is that of hydrodynamic turbulence where two multiplicative cascade models are classically in competition. Using positive s only, the Kolomogorov and the wavelet scaling functions computed from experimental data fail to discriminate between the two models. However, the leader scaling function, enabling the use of negative s, permits to show that one model is unambiguously preferred by data. This is discussed in Section 6.1 and illustrated in Fig. 6 (bottom row plots).