UPDATE July 2012 — The Food Crises: The US Drought

Abstract

Recent droughts in the midwestern United States threaten to cause global catastrophe driven by a speculator amplified food price bubble. Here we show the effect of speculators on food prices using a validated quantitative model that accurately describes historical food prices. During the last six years, high and fluctuating food prices have lead to widespread hunger and social unrest. While a relative dip in food prices occurred during the spring of 2012, a massive drought in the American Midwest in June and July threatens to trigger another crisis. In a previous paper, we constructed a model that quantitatively agreed with food prices and demonstrated that, while the behavior could not be explained by supply and demand economics, it could be parsimoniously and accurately described by a model which included both the conversion of corn into ethanol and speculator trend following. An update to the original paper in February 2012 demonstrated that the model previously published was predictive of the ongoing price dynamics, and anticipated a new food crisis by the end of 2012 if adequate policy actions were not implemented. Here we provide a second update, evaluating the effects of the current drought on global food prices. We find that the drought may trigger the expected third food price bubble to occur sooner, before new limits to speculation are scheduled to take effect. Reducing the amount of corn that is being converted to ethanol may address the immediate crisis. Over the longer term, market stabilization requires limiting financial speculation.

The current global crisis in food prices and the vulnerability of the limited food supply to environmental and other disruptions is a matter of ongoing concern worldbank_foodcrisis . Recent food price peaks in 2007-08 and 2010-11 have resulted in food riots and are implicated in triggering widespread revolutions known as the Arab Spring food_crises . The underlying vulnerability of the global food supply system is being tested again this summer by a severe drought in the Midwestern United States which is responsible for a large portion of the global food supply drought_monitor ; NOAA_drought_June ; Reuters_drought ; source_grains .

In a paper published in September 2011 food_prices , we built a quantitative model that, for the first time, was able to precisely match the monthly FAO food price index over the last 8 years. The model showed that, of all the factors proposed to be responsible for the recent dramatic spikes and fluctuations in global food prices, rapid increases in the amount of corn-to-ethanol conversion and speculation on futures markets were the only factors which could justifiably be held responsible. Each of these causes in turn results from particular acts of government intervention or deregulation. Thus, while the food supply and prices may be vulnerable to global population increases and environmental change, the existing price increases are due to specific governmental policies. In order to prevent further crises in the food market, we recommended the halting of government support for ethanol conversion and the reversal of commodities market deregulation, which enables unlimited financial speculation.

Since the publication of our analysis, a few changes in these directions have been made. At the end of 2011, ethanol subsidies were allowed to expire Pear2012 ; Krauss2011 . However, a government-guaranteed demand for 37% of the US corn crop is still in place Smith2012 . It is unclear what effect this partial change in policy will have on the percentage of corn converted to ethanol, which is currently about 40%. New position limits on speculative activity by the US Commodities Futures Trading Commission are scheduled to come into effect by the end of 2012, as required by the Dodd-Frank Act doddfrank ; FedReg . It remains to be seen how effective these new regulations will be, as there are those who consider them too watered-down PattersonTrindle2011 , and market participants are seeking to dilute them further PattersonTrindle2011 ; Trindle2012 ; Brush2012 ; Donahue2010 ; Damgard2011 .

In a subsequent update published in February 2012 feb_update , we showed that the model continued to fit current data, up to January 2012, which had not been available at the time of the construction of the model. We further observed that extrapolating model prices into the future yielded the prediction of another speculative bubble starting by the end of 2012 and causing food prices to rise even higher than recent peaks.

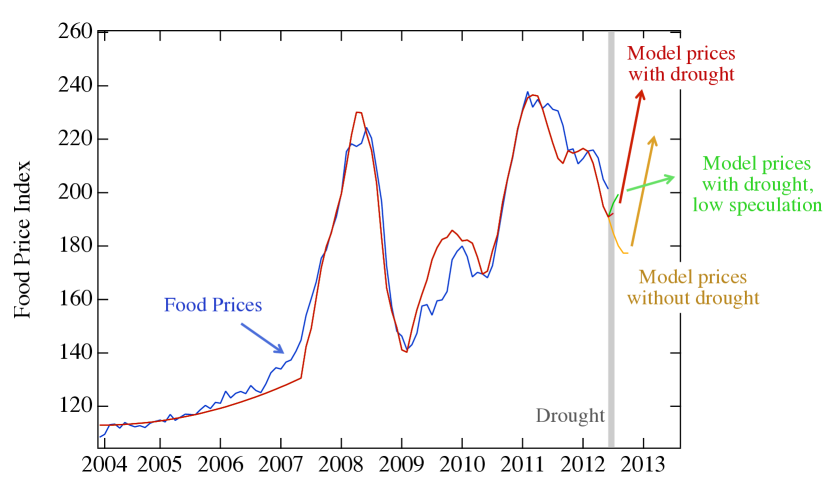

This season, the American Midwestern agricultural region has experienced debilitating droughts and high temperatures, the most severe in at least 50 years, leading to rapidly rising corn and wheat prices in anticipation of a poor yield NOAA_drought_June ; Reuters_drought . Here we include this as a shock in our established model. We find that through the mechanism of speculative activity, the drought may trigger a third massive price spike to occur earlier than otherwise expected, beginning immediately, and sooner than could be prevented by the anticipated new regulations. This spike may raise prices well beyond an increase justified by the reduced supply caused by the droughts.

In Fig. 1 we plot our model predictions for different scenarios. The central comparison is between the drought triggered speculative bubble (red line) compared to the same shock with reduced speculation (green line). While the drought causes only a limited price shock, the impact on prices is amplified by the speculative activity. Fig. 1 shows the quantitative impact of speculators given the current level of market speculation as validated by prior analysis of food prices.

The speculative bubble is modeled starting from a price shock driven by the drought, which is expected to occur based upon existing grain price increases Reuters_drought though it has not yet been specified by the FAO. The price increase then causes the upcoming price spike to come sooner than would have otherwise occurred. The level of earlier riot-inducing bubbles is reached before the end of 2012 and prices continue to rise much higher. Without the drought (yellow line), the rise in prices would be just as dramatic, but is predicted to occur several months later, possibly in time for the new regulations to prevent it. On the other hand, if speculation were to be curbed immediately, starting from July 2012, the model shows (green curve) that the price increase due to the drought would be far smaller, and would not lead to another dramatic price spike. An alternative intervention, eliminating the government mandated ethanol quota for this year worstall2012 , would would result in a new market shock and could cause a sudden drop in prices. This may alleviate the immediate concerns though its effect is subject to speculator-driven bandwagon effects.

We note that in our original paper food_prices , we evaluated the suggestion that droughts in Australia had been responsible for the increase of food prices in 2008. We concluded that they could not have been, because the Australian production of grain is not a sufficiently large portion of the global production of grain. The same analysis yields a different answer for the US drought. US production of grain is consistently an order of magnitude larger than that of Australia source_grains . Moreover, changes in the global production of grain correlate with changes in US production (see Fig. 2). The two time series have a Pearson’s correlation coefficient over the last 22 years of compared to for the correlation with Australia’s time series.

We thank Peter Timmer for helpful conversations. This work was supported in part by AFOSR under grant FA9550-09-1-0324, ONR under grant N000140910516.

References

- (1) The World Bank Food crisis, Global food crisis response program (2008-2012)

- (2) M. Lagi, K. Z. Bertrand, Y. Bar-Yam, The food crises and political instability in North Africa and the Middle East, arXiv:1108.2455v1 [physics.soc-ph] (2011).

- (3) National Drought Summary – July 17, 2012, US Drought Monitor (Jul 19, 2012).

- (4) State of the Climate, Drought, June 2012, National Oceanic and Atmospheric Administration, National Climatic Data Center (Jun, 2012).

- (5) S. Nelson, US drought spreads, boosts corn to record price, Reuters (Jul 19, 2012).

- (6) Production, supply and distribution online, U.S. Department of Agriculture, Foreign Agricultural Service (accessed on Jul 2012).

- (7) M. Lagi, Y. Bar-Yam, K. Z. Bertrand, Y. Bar-Yam, The Food Crises: A quantitative model of food prices including speculators and ethanol conversion, arXiv:1109.4859v1 [q-fin.GN] (2011).

- (8) R. Pear, After three decades, tax credit for ethanol expires, The New York Times (Jan 1, 2012).

- (9) C. Krauss, Ethanol subsidies besieged, The New York Times (Jul 7, 2011).

- (10) A. Smith, Children of the corn: The renewable fuels disaster, The American (Jan 4, 2012).

- (11) The Dodd–Frank Wall Street Reform and Consumer Protection Act (Pub.L. 111-203, H.R. 4173)

- (12) Position limits for futures and swaps, Federal Register 76, 71626 (2011).

- (13) S. Patterson, J. Trindle, CFTC raises bar on betting, Wall Street Journal (Oct 19, 2011).

- (14) J. Trindle, CFTC may change application of speculative limits, Market Watch – The Wall Street Journal (May 17, 2012).

- (15) S. Brush, CFTC proposes easing of Dodd-Frank speculation limit rules, Bloomberg (May 18, 2012).

- (16) C. S. Donahue, Re: CFTC Proposed Rulemaking on “Federal Speculative Position Limits for Referenced Energy Contracts and Associated Regulations,” 75 Fed. Reg. 4144 (Jan. 26, 2010), CME Group (2010).

- (17) J. M. Damgard, Re: Position Limits for Derivatives (RIN 3038-AD15 and 3038-AD16), Futures Industry Association (2011).

- (18) M. Lagi, Y. Bar-Yam, K. Z. Bertrand, Y. Bar-Yam, UPDATE February 2012 The Food Crises: Predictive validation of a quantitative model of food prices including speculators and ethanol conversion, arXiv:1203.1313 [physics.soc-ph] (2012).

- (19) FAO food price index, Food and Agriculture Organization of the United Nations (accessed on Jul 2012).

- (20) T. Worstall, Drought, climate change, corn prices, ethanol and biofuels, Forbes (Jul 20, 2012)