The European debt crisis: Defaults and market equilibrium

Abstract

During the last two years, Europe has been facing a debt crisis, and Greece has been at its center. In response to the crisis, drastic actions have been taken, including the halving of Greek debt. Policy makers acted because interest rates for sovereign debt increased dramatically. High interest rates imply that default is likely due to economic conditions. High interest rates also increase the cost of borrowing and thus cause default to be likely. In equilibrium markets, economic conditions are used by the market participants to determine default risk and interest rates, and these statements are mutually compatible. If there is a departure from equilibrium, increasing interest rates may contribute to—rather than be caused by—default risk. Here we build a quantitative equilibrium model of sovereign default risk that, for the first time, is able to determine if markets are consistently set by economic conditions. We show that over a period of more than ten years from 2001 to 2012, the annually-averaged long-term interest rates of Greek debt are quantitatively related to the ratio of debt to GDP. The relationship shows that the market consistently expects default to occur if the Greek debt reaches twice the GDP. Our analysis does not preclude non-equilibrium increases in interest rates over shorter timeframes. We find evidence of such non-equilibrium fluctuations in a separate analysis. According to the equilibrium model, the date by which a half-default must occur is March 2013, almost one year after the actual debt write-down. Any acceleration of default by non-equilibrium fluctuations is significant for national and international interventions. The need for austerity or other measures and bailout costs would be reduced if market regulations were implemented to increase market stability to prevent the short term interest rate increases that make country borrowing more difficult. We similarly evaluate the timing of projected defaults without interventions for Portugal, Ireland, Spain and Italy to be March 2013, April 2014, May 2014, and July 2016, respectively. The markets consistently assign a country specific debt to GDP ratio at which default is expected. All defaults are mitigated by planned interventions.

I motivation

Europe has been facing what the media has called “a ferocious debt crisis” since the beginning of 2010 Castle2011 . Several European governments have accumulated what many consider to be unsustainable levels of government debt Rastello2010 . Greece has been at the center of the crisis, with the highest levels of public debt in the Eurozone and one of the biggest budget deficits eurostat . Fears of default and its consequences Korowicz2012 have led to special bailout funds Nelson2011 , austerity programs in Greece OGrady2010 , and recently agreements by banks to voluntarily dismiss half of Greece’s debt Fidler2011 . Policy makers have taken action because of the dramatic increase in interest rates, which curtails the ability to borrow money from international capital markets. High interest rates imply that the market considers the risk of default to be high due to economic conditions, but they also increase the cost of borrowing and cause default to be more likely. Because interest rates both reflect expected default risk and cause default risk, it is not entirely clear which is the actual cause of default: economic conditions, i.e. an equilibrium market, or non-equilibrium market behavior.

In equilibrium economics, market prices are based upon value and value is determined by price. This self-consistency in equilibrium hides the important subtle causal loops of the interaction of price with value that become manifest when deviations from equilibrium occur. Among the causes of deviations from equilibrium are herd behaviors that cause price changes whose timing is not related to inherent changes in value, but only to the intrinsic dynamics of the market itself. Such deviations from equilibrium may play a role in fluctuations characterized by “volatility” (though volatility can also include variations in equilibrium prices and value) but the impact of fluctuations away from equilibrium is poorly understood because they depend on those poorly characterized causal loops.

In recent years, major market indices have varied widely, amid concerns about macroeconomic conditions that affect broadly the values of goods and services. In the case of markets whose values depends on macroeconomic conditions, the equilibrium market price reflects economic news. When market price is itself a causal factor in economic conditions, which it often is, the feedback to economic conditions can lead to inherent dynamics that are not found in the theory of equilibrium prices. Because markets are considered to represent economic conditions, the interpretation of market changes is used in policy setting for economic interventions. When non-equilibrium fluctuations of the market are interpreted as indicators of economic conditions for policy interventions, this misinformation can lead to policy actions that are not justified by economic conditions but only by the false signals given by market fluctuations. However, in some markets, prices directly impact on the economic system. This is the case in bond markets, where interest rates that are set by the market directly impact on the borrowing costs of countries. Whether the markets are or are not in equilibrium is therefore key to both economic conditions and correct policy response. Disentangling the perception of market fluctuations from economic conditions, and the possibility of market fluctuations determining rather than reflecting economic conditions is important to both economic theory and policy. While equilibrium prices are important components of the proper and constructive function of economic markets, the impact of non-equilibrium fluctuations may be destructive, and therefore should be the subject of policy attention, which can by careful choice limit both the size and impact of non-equilibrium volatility.

Here we build a simple equilibrium model of sovereign default risk that, for the first time, is able to directly quantify the consistency between interest rates and economic indicators, and serve as a basis for evaluating the role of non-equilibrium volatility in the bond market. The first answer we reach is that the equilibrium picture holds for an analysis of annually-averaged long-term interest rates. Looking more closely in a second analysis Lagi2012 , we show that this picture breaks down for timeframes less than a year long during which non-equilibrium speculator behavior plays a key role, leading to large interest rate fluctuations. In particular, bond prices dropped from 57% to 21% of their face value, from July to December 2011. A complex systems perspective suggests that near a transition large fluctuations between distinct states (in this case default and non-default) become possible. Under these conditions interest rate variations are both caused by, and cause, vulnerability to default. Such fluctuations can trigger substantial economic impacts and stronger interventions than would be justified by equilibrium markets. The extent of these fluctuations may be reduced by well chosen market regulations.

II overview

It is common practice for private corporations and governments to borrow in order to overcome shortfalls in operating expenses, deal with emergencies, or invest in economic growth. A primary mechanism for this borrowing is to sell interest bearing bonds. The question of how much governments can borrow from bond markets is related to the lenders’ concern about debt repayment and sustainability Eaton1981 ; Cooper1984 . The levels of government debt vary markedly from country to country, being the result of a mixture of policy decisions (if levels are low) and how much lenders will finance (if levels are high). The interest rates are set by the willingness of those who loan funds, either by direct negotiation or by auction. Only if the issuer becomes unable to repay, i.e. a default happens, are the payments reduced. The interest on the primary bond market therefore is, in first approximation, a measure of how high the risk of default is. The more likely those who loan the funds think default is, the higher interest rates are set, reflecting a greater investment risk. Different bonds provide more or less interest depending on their estimated relative risk of default.

Many researchers have addressed the question of why nations ever choose to pay off their debts, given sovereign immunity and no enforcing body to exact repayment Alfaro2005 ; Cole1998 ; Cooper1984 ; Panizza2009 ; Arraiz2006 ; Lindert1989 ; Eaton1981 ; Diaz-Alejandro1983 ; Mitchener2005 ; Tomz2007book ; DePaoli2006 ; Wright2011 ; Dooley2000 ; Sandleris2008 ; Cohen1992 ; Alichi2008 ; Perotti1996 ; Borensztein2009 ; Sturzenegger2007b . Most assume that there is some cost associated with defaulting, which may include loss of reputation in the international community Alfaro2005 ; Cole1998 ; Panizza2009 , trade sanctions Diaz-Alejandro1983 ; Wright2011 , harsher future credit terms Arraiz2006 ; Borensztein2009 ; Sturzenegger2007a , or outright exclusion from the world credit market Arraiz2006 ; Eaton1981 . Historically, military interventions may have served as an additional external deterrent Mitchener2005 ; Panizza2009 . However, some question the importance of such external repercussions, claiming that they may not be as stringently enforced or as effective as traditionally thought Lindert1989 ; Tomz2007book ; Panizza2009 . By whatever mechanism, it is clear from measures of economic growth that sovereign default correlates with subsequent reduced economic performance of the defaulting country DePaoli2006 ; Wright2011 ; Dooley2000 ; Sturzenegger2004 ; Panizza2009 .

A complementary body of literature attempts to identify the warning signs that precede sovereign default Aguiar2006 ; Arellano2007 ; Hernandez-Trillo2000 ; Kulatilaka1987 ; Manasse2005 ; Savona2008 ; Stein2001 ; Tomz2007 . Researchers have cited macroeconomic measures of insolvency and illiquidity as precursors to default; they consider GDP growth, debt-service payments, penalties for default, bond interest rates, interest volatility, consumption volatility, and a host of other factors Manasse2005 ; Kulatilaka1987 ; Savona2008 ; Arellano2007 . Some have validated their models on empirical data Arellano2007 ; Hernandez-Trillo2000 ; Manasse2005 ; Savona2008 ; Yue2010 . However, many of them include a large number of parameters, obscuring the relative importance of different factors.

Here we develop a quantitative model of sovereign default that identifies the debt ratio Domar1944 as the only relevant dynamic macroeconomic variable that European market participants have used over the last 10 years to estimate the likelihood of default of a country and, therefore, to set long-term interest rates. The model explicitly relates the annually-averaged long-term interest rates to the debt ratio with a simple 2-parameter fit, and is able to accomplish two major goals.

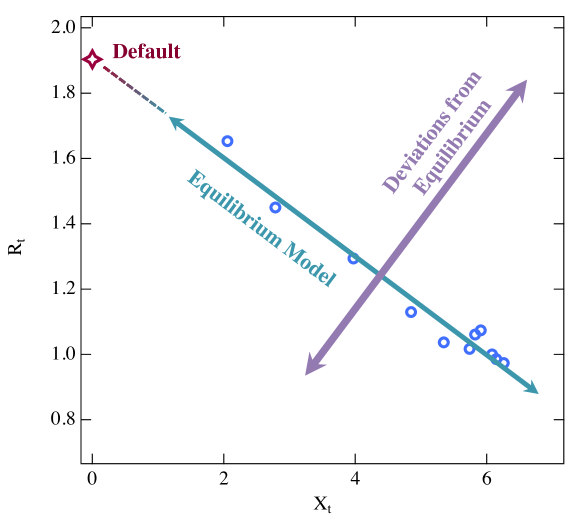

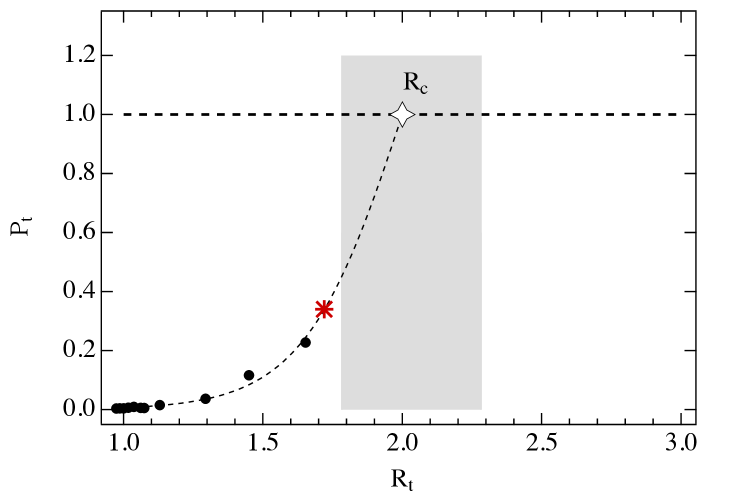

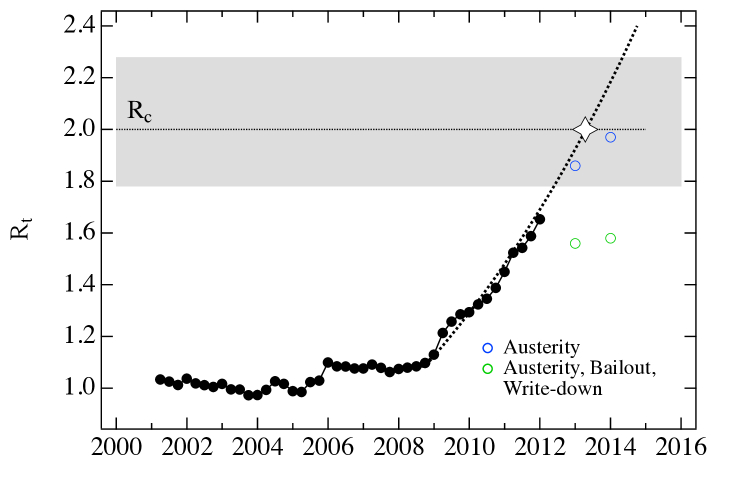

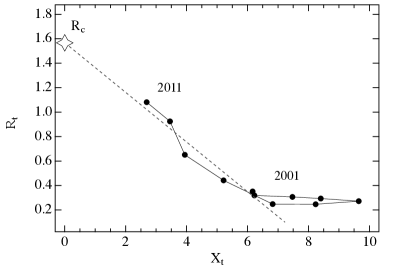

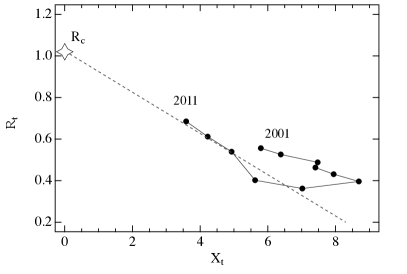

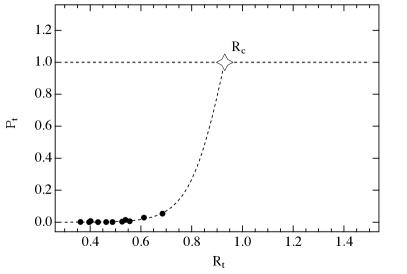

First, the equilibrium model provides a way of testing whether international capital markets are consistently basing interest rates on economic conditions. We show that interest rates reflect the expectation that default becomes certain as the debt to GDP ratio approaches a specific value, the default threshold. Although there is strong evidence for the existence of mechanisms able to drive prices away from equilibrium Litterick2002 ; food_prices , economic models usually assume that markets are reflecting economic information rather than considering it a hypothesis to be tested. We test the assumptions of the equilibrium picture by showing that the annually-averaged long-term interest rates for Greek bonds over the last 10 years are given by a well-defined function of the distance of the sovereign debt ratio from a fixed country-specific default threshold. Interest rates follow this function toward default as the debt ratio increases (see Fig. 1). Since the interest rates can be quantified as an explicit function of macroeconomic information, the model shows that annually-averaged long-term interest rates are consistent with this assumption of equilibrium models.

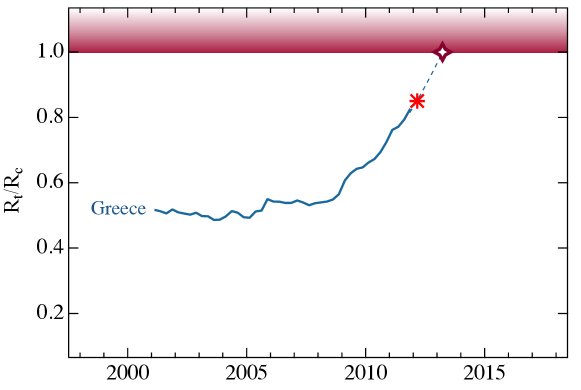

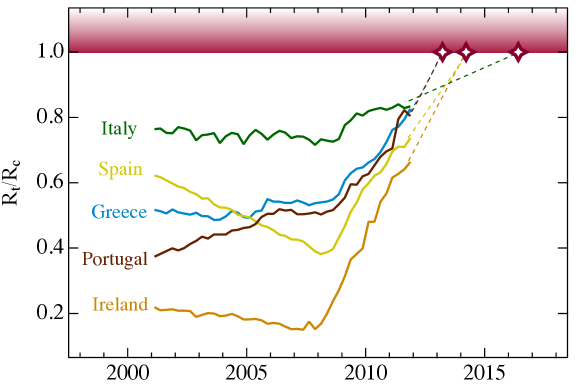

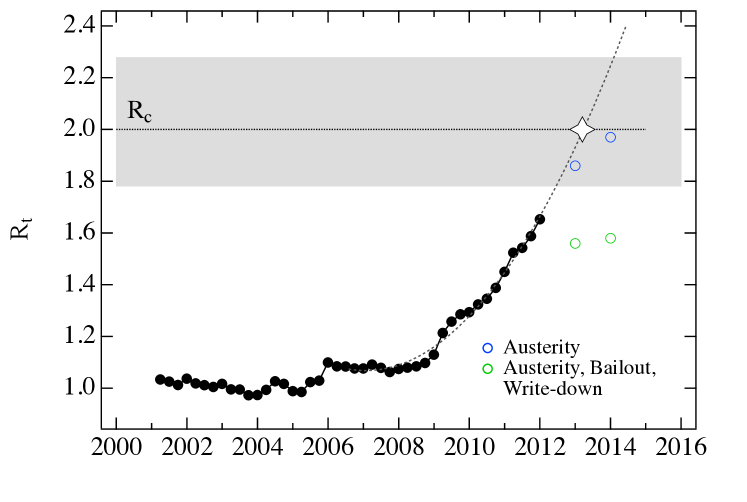

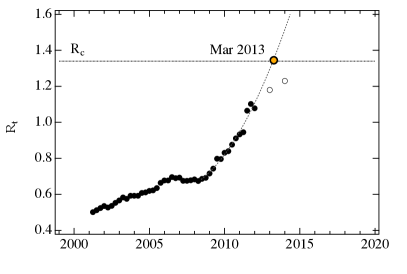

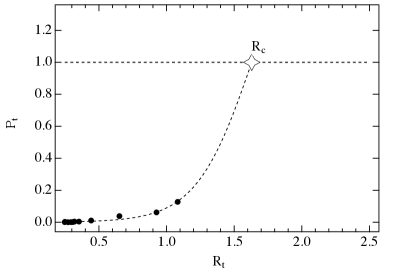

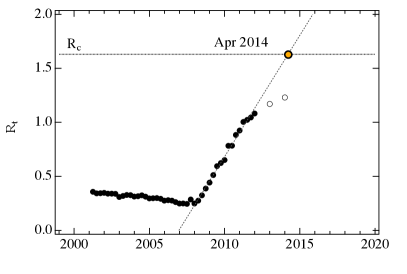

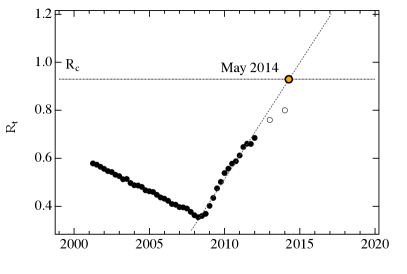

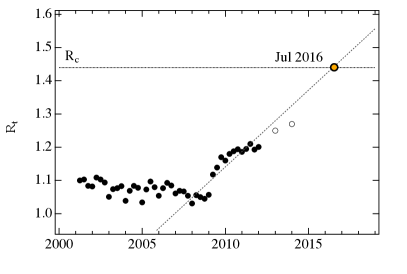

Second, the model can estimate the timing of a default event given its debt trajectory. Default becomes certain as the country debt approaches the debt threshold. Even when a country defaults a portion of the debt is typically honored, the amount of which is called the recovery rate, affecting the precise timing of the default. For Greece, we find that the model points to certain default with a 50% recovery rate in the first quarter of 2013 (Fig. 2, top). The “voluntary” write-down of half of the country’s debt by private creditors, which in effect corresponds to a partial default with 50% recovery, occurred one year earlier in March 2012 Gatopoulos2012 . The timing of default may be attributed to non-equilibrium market fluctuations in the secondary bond market and not to economic or other news. Thus, the equilibrium trajectory of default is preempted by market bandwagon effects. Results for other countries are summarized in the bottom panel of Fig. 2. The projected timing of default ranges from March 2013 for Portugal to July 2016 for Italy.

Our analysis shows, therefore, that the change of long-term interest rates follows fundamental expectations only over the long run, while it is subject to non-equilibrium effects in the short run. We discuss this in a second paper, where we show that shorter time variation in bond prices have been much more rapid than would be expected from economic fundamentals Lagi2012 . The results are consistent with the existence of price fluctuations due to trend following or market manipulation. These fluctuations are both caused by and cause vulnerability to default. When there is a concern about default, large fluctuations are created by herd behavior. When interest rates fluctuate upwards they can cause default. Under these conditions the causal relationships are reversed and markets drive fundamental economic outcomes. These effects shorten the time to default, causing a need for more aggressive austerity programs and debt write-downs than might otherwise be required. During a period of economic recovery from a recession these differences may be critical as a recovering economy may be better able to avoid default if it is not subjected to higher national interest rates and austerity measures than would be justified in equilibrium markets.

In considering the broader implications of our analysis of country default, it is important to note that our model was developed and validated in the context of the European debt crisis, which is an atypical context due to the common euro currency that prevents individual country currency devaluation for members of the Eurozone. Where currency devaluation is possible, devaluation may serve to reduce some of the pressure of paying back internal debt, also by making exports cheaper and generating growth Deo2011 . Thus, the European conditions may have distinctive properties and an analysis of European conditions may not be applicable elsewhere without modification.

In particular, one of our central findings is that only one macroeconomic variable is dynamically relevant, the debt ratio. The debt ratio has been recognized to be a common reference for lenders among measures that are expected to be important Cooper1984 . Our model allows for the possibility that other variables play a role in country default as long as they either do not change over time, and therefore contribute only to the static model parameters, or are not relevant in the specific context of the Eurozone countries we studied. Indeed, other variables must play a role in determining the value of the static country specific debt threshold. Our analysis does not reveal these variables. Still, the debt thresholds are in a limited range between 90% and 200% of GDP for the countries we studied—implying markets consider the GDP itself to be a first approximation to a reasonable debt threshold.

This conclusion may, however, be modified for other countries outside the Eurozone. A variable that may not be relevant in the Eurozone because of the common currency, but could be relevant in other areas, is the distinction between external and internal debt Buchanan1957 . Where one class of lender is substantially less likely to stop providing loans than others, an analysis may be best framed in terms of the distinct properties of the two levels of available debt. It is reasonable to expect that the internal debt plays a diminished role in the probability of default. If the ratio between the internal and external debt were constant over time, discounting the role of the internal debt in default would increase the value of the critical debt ratio, but would not otherwise affect our conclusions.

Thus, we can expect our findings to be modified for countries where internal debt is a large part of total debt, especially for countries outside of the Eurozone. For example, Japan has a high debt ratio of 230% but much of the debt is internal and owned by the postal system Oxford2009 . Much of the US debt is owned by the Federal Reserve Toscano2012 . In both these cases, interest rates are low despite debt ratios that are in the range of the Eurozone debt thresholds.

Finally, the applicability of the model is limited to countries in distress. We cannot know what the critical threshold of the debt ratio is when interest rates are low: the only way to test the model is when the probability of default is high enough to affect the annually-averaged long-term interest rates.

III model

We construct a mathematical model of sovereign default risk (details are in Appendix A) by considering a country to have the choice, at each time step, of being in a state of default or nondefault. Since the ability of a country to pay its debt depends on the size of the debt relative to its economic output, we assume that the choice of default is determined by its debt ratio, i.e. the ratio between the overall debt and the GDP. We also assume the existence of a critical threshold of the debt ratio, above which the country is likely to default. The value of the critical threshold depends on the cost of the penalties implicitly associated with defaulting; it differs from country to country and is the first parameter of our model.

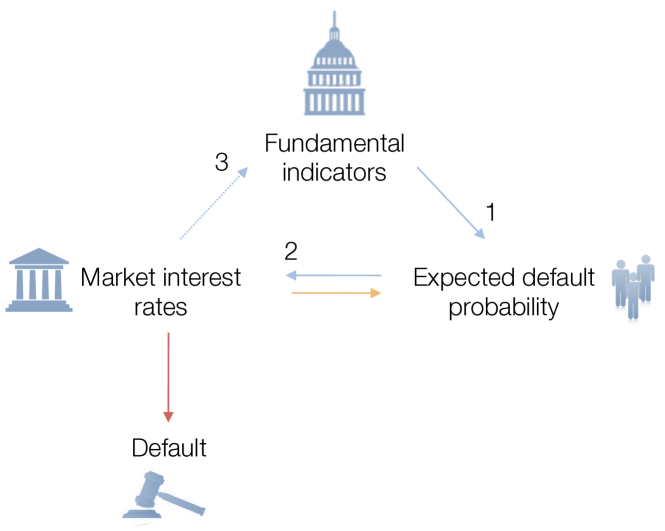

The expected probability of default is indicated by market participants through the setting of interest rates: the more likely they think default is across all possible future scenarios over the period of repayment, the higher interest rates are set, reflecting a greater investment risk. Since interest rates determine the debt burden, their increase also determines a higher probability of default. This positive feedback mechanism is shown as a blue dashed arrow in Fig. 3. Moreover, a sharp change in interest rates can alter investor perception of the default probability (orange arrow), thereby creating another feedback loop and pushing interest rates out of equilibrium. There are therefore two distinct feedback mechanisms, one fundamental and one behavioral. The model can test whether the behavioral feedback has an impact on the markets, or whether markets are self-consistently determining a default probability based on the fundamental feedback (blue arrows).

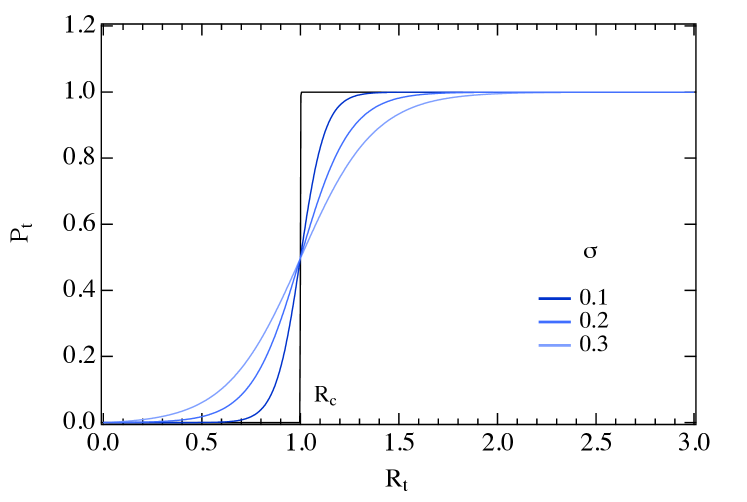

If all lenders had the same expectation about the time of default given by a default threshold, the interest rate would be the risk free value until the debt ratio reaches the critical default value. At this point, creditors would stop lending money and interest rates would effectively diverge. The resulting step-like profile for the probability of default is in practice smooth, since their expectations are heterogeneous. Many reasons contribute to this heterogeneity, including the limited amount of information available to the economic actors in the bond market, different estimates of the critical debt ratio, imperfect knowledge of the debt trajectory, different evaluations of the political decision-making process behind a possible default, different bond maturation periods and payment schedules, and disparate influence of other economic indicators. Heterogeneous expectations have been previously recognized to be important in describing the behavior of bond markets Xiong2010 . Nevertheless, the probability of default is low below and high above, so that the overall profile as a function of the debt ratio can be represented by a smooth sigmoidal transition,

| (1) |

where , the second parameter of our model, reflects the degree of smoothness, and is the extrinsically set recovery rate, i.e. the probability that the country will pay a share of the debt . The derivation of this equation can be found in Appendix A.

In summary, we consider the default process as one that follows a discrete jump at a particular value of the debt ratio, but we treat it as smoothed by uncertainty and heterogeneity. The model has only two parameters: the critical debt ratio , which represents the average value above which investors stop buying bonds, and the heterogeneity parameter , which incorporates market uncertainty. The model assumes that these parameters are well defined and consistently represented by the bond market over time.

These two parameters can also be used to evaluate if the market interest rates of a country are consistently set according to economic fundamentals. The probability of default increases as the interest rates increase, and it goes to 0 as they approach the risk-free interest rates , according to Calvo1989

IV results

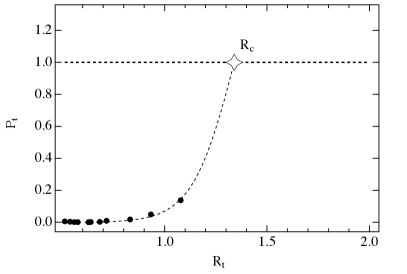

We tested the model on Greece over the last decade. Results are shown in Fig. 4 assuming a recovery rate of 50%, the average value on defaulted sovereign bonds over the last 30 years Moodys2010 . (The model parameters do not depend on the recovery rate used.) The figure shows the probability of default plotted against the debt ratio. As predicted by Eq. 1, the data lies on a sigmoidal curve, and the two model parameters can be extracted from this fit. We obtain a critical debt ratio , and a heterogeneity parameter . Therefore, the model estimates that when Greece’s debt reaches a level about twice its GDP, the market projects the country default probability to be 1.

Figure 5 shows how the time of certain default of a country can be estimated. We approximate Greece’s debt trajectory in one of two ways, using a numerical polynomial fit or an economic debt projection (Appendix B). Either way, the debt ratio would reach the default threshold in the first few months of 2013. Simulations with different intervention scenarios (Appendix D) show that the default could not have been prevented solely by meeting the austerity targets recently agreed upon Financial2012 . Indeed, global fears of a Greek default led to negotiations and to a coordinated intervention that resulted in a haircut, which can be considered tantamount to the partial default projected by our model. The debt write-down occurred at a time when the probability of default was 33%, one year before the projected certain default. A separate analysis shows that the timing of default can be attributed to non-equilibrium market fluctuations Lagi2012 . Negotiated partial defaults are more likely than a full default because of the harm to both lenders and borrowers Fane1995 . In this case, negotiations led to a 53% write-down of the debt by the private sector (in the form of a waiver of receivables) coupled with access to EFSF and IMF loans at preset interest rates and austerity measures. If the austerity measures are met, and its impacts on GDP are consistent with published expectations (Appendix C), this will allow the debt ratio to remain below the danger zone.

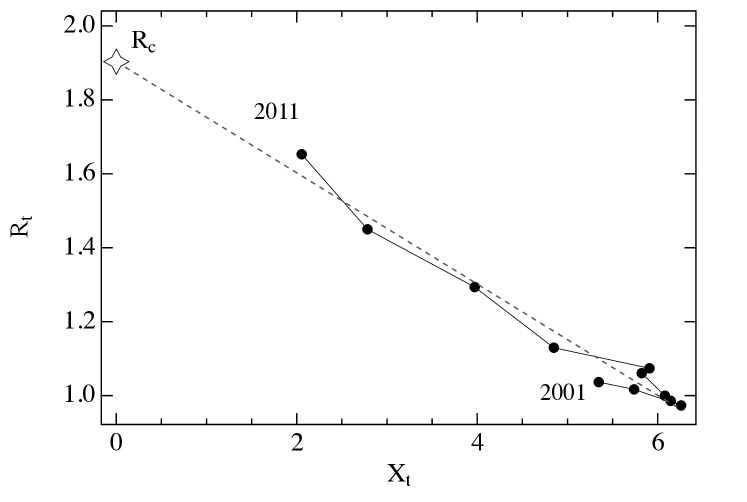

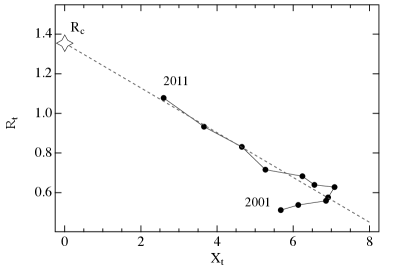

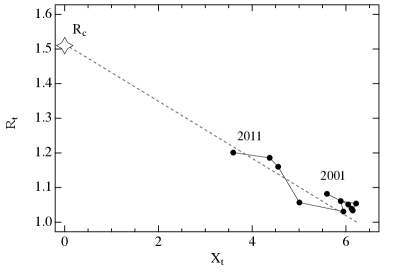

We can use our results to evaluate whether market interest rates are consistent with equilibrium assumptions over time. During the near-default period, bond rates change rapidly and are subject to higher uncertainty. In this scenario, the impact of large traders and trend following may become relevant. The fit of the default dynamics for Greece shown in Figures 4 and 7 is a test of market self-consistency: if the market did not set interest rates consistently with the valuation of the critical debt ratio in prior years, these relationships would not hold over time. For example, if the interest rates overestimated the probability of default of a country in a given year relative to the historical precedent, the corresponding point would lie above the fit in Fig. 4. The self-consistency condition can also be represented as a linear relationship between debt ratio and the distance of market interest rates from their default value (see Fig. 7). The good fits imply that the reference 10 year bond interest rates averaged over yearly time frames are consistent with market equilibrium. Shorter time frame behaviors deviate from these conclusions and are treated in a separate paper Lagi2012 .

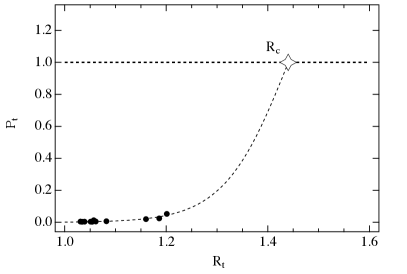

We also tested the model for the other European countries involved in the debt crisis: Portugal, Ireland, Spain and Italy (see Fig. 9-12 in Appendix D). As in the case of Greece, we found that markets self-consistently determined a definite value for the critical debt ratio for all countries. The time range over which a fit with a consistent value of is possible depends on the country: the model fits the last 11 years for Greece and Italy, 9 years for Portugal, and 5 years for Spain and Ireland.

As for the case of Greece, the equilibrium model portrays a situation which could be less severe than the one described by secondary markets and media Oakley2012 ; Post2012 ; Kavoussi2011 ; Elliott2011 . If the budget targets are met, Portugal could avoid a partial default at the beginning of 2013. Ireland and Spain have a larger buffer before a default, projected for mid-2014. Italy is still farther away from a possible default, projected by the model for mid-2016, if the current trend is maintained. In all cases an immediate large scale policy response to change the debt trajectory does not seem to be necessary.

The values of the critical debt ratio, , do not vary over orders of magnitude between countries. The values cluster around unity, which could imply that lenders believe a country is able to repay its debt when the debt is about the size of its GDP, but not significantly larger. The capacity of a country to borrow depends on a variety of factors, and reflects creditors’ concerns about solvency (long-run prospects), liquidity (short-run prospects) and repudiation risks Cooper1984 . The reasons why countries usually borrow lower-than-sustainable amounts, i.e. why is kept well below , have been discussed Cooper1984 . Even though we find there is only one scale for this parameter, varies among countries. The value of may depend on a variety of macroeconomic phenomena. Our analysis does not identify these dependencies. Sustainable growth rate, the coupling to other economies willing to help, considerations about the country’s hidden economy and its possibility to increase taxes are also factors that might contribute to the country-specific value of .

Finally, it is worth noting that the framework we presented here is a long-run model of default for European countries, but short timescales require a different picture. This is demonstrated by the deviation of 10-year Greek bond prices from their equilibrium trajectory after the summer of 2011, when they dropped from 57% to 21% of their face value in five months. One might think that this increase in interest rates would be justified by the default projections, even if they were about 1.5 years away according to our equilibrium model. But the corresponding probability of default at that time was around 0.3 (see Fig. 4), not large enough to explain such a high level of interest rates, nor to justify an imminent write-down. The equilibrium economics perspective is uncompromising: bond prices should follow the curve regardless of fluctuations—the trajectory has been defined. In contrast, a complex systems perspective predicts that once the system is near a critical point, multiple stable states (in this case default and non-default) become possible. In this regime, the market is not self-averaging, its finite size gives rise to fluctuations at all scales, and sensitivity to trend following and market manipulation increases. Both equilibrium and non-equilibrium mechanisms are therefore included in our framework and are not inconsistent, as they are acting at different timescales.

V conclusions

We developed a quantitative model of sovereign default for European countries that identifies the debt ratio as the fundamental parameter that investors use to set the persistent value of interest rates captured by annually-averaged values. Our analysis shows that the equilibrium model assumption that interest rates are set by economic conditions is satisfied, though we do not show that interest rates actually reflect potential losses due to default risk. Our model is able to address several questions. First, it gives an estimate of the debt sustainability of a country, i.e. how much creditors are willing to lend. In the case of Greece the maximum debt is twice the GDP, . Second, given the debt trajectory of the country, the model can identify the time the debt ratio goes beyond the threshold, triggering a default. Since default is itself determined by the time of diverging market interest rates, default is self-consistently determined by the market evaluation of the default probability. Third, the model can establish whether bond markets satisfy the equilibrium assumption that interest rates the market sets have a consistent relationship with fundamental indicators over time. We find this to be the case for Greece over the last 10 years.

The model identifies the time of certain default as occurring early in 2013. While this appears to be in reasonable agreement with the debt write-down, the timing is different by approximately a year and this is critical to a proper interpretation of events. The existence of non-equilibrium bandwagon effects that preempt the equilibrium default means that higher national interest rates and austerity measures than would be justified in equilibrium accelerated and exacerbated the default process. Without these effects, more modest measures and less social disruption could have been sufficient to avert default.

As it stands today, drastic measures taken by the government, international organizations and the private sector may avoid a complete default. These interventions have both an economic and social cost. By regulating markets to limit the non-equilibrium market fluctuations, the cost of interventions and their severity could be reduced for Greece and other European countries.

VI acknowledgements

We thank Karla Z. Bertrand for help with the literature review, Jeffrey Fuhrer, Richard Cooper, Yavni Bar-Yam and Dominic Albino for helpful comments.

Appendix A

Model Details

We consider a country that decides to borrow from international capital markets at interest rate . At every time period , the country is in one of two states: default or nondefault. Since the ability of the country to pay its debt depends on its economic output , the state of the country is determined by its debt ratio, . When is above a critical threshold , the value of which depends on the cost of the penalties associated with defaulting, the country is in the default state, and vice versa.

If is the probability of default with recovery rate , i.e. the probability that the country will pay a share of the debt , the expected return from a one-period loan would be Calvo1989 . By definition, is the contractual repayment at the end of the period per unit of loan and is the probability of full repayment. An investor, however, has the option of investing in risk-free bond markets and receive an expected return of at the end of the period, where is the risk-free interest rate. Thus, since in competitive equilibrium investors should be indifferent between those two alternatives, equating the two expressions for expected return and solving for we have

| (4) |

This equation establishes a relationship between the expected probability of default and interest rates. It is consistent with the intuition that the probability of default increases as the interest rates increase, and it goes to 0 as they approach the risk-free interest rates. Equation 4 can also be written as a function of bond prices, . For a one-period loan,

| (5) |

where is the initial value of the bond (face value) and the initial interest rate. Then, substituting in Eq. 4 we get

| (6) |

which relates the probability of default with the current bond price.

There are three reasons why is in general greater than : transaction costs, risk aversion and default risk Calvo1989 . For simplicity, let’s assume that transaction costs are small enough to be neglected and that lenders are risk neutral. If lenders had perfect knowledge of the time of default of the country, and the duration of the one-period loan is short enough to be neglected, they could keep until the debt reaches the critical default value . At the time of default, when the debt reached the critical default value, the interest rates would become infinite. Therefore, at each time this idealized bistable system can be summarized as a step function of the default probability:

| (7) |

We plot the default probability for the case in Fig. 6 (black curve). This step function is in practice smooth (blue curves), since the investment strategies are heterogeneous for a number of reasons: limited amount of information available to market participants, different estimates of the critical debt ratio, imperfect knowledge of the debt trajectory, different evaluations of the political decision-making process behind a possible default, different bond maturation periods and payment schedules, disparate influence of other economic indicators. Here we show how this smooth behavior naturally arises from a supply and demand model of capital markets that includes heterogeneous expectations. The result follows from the reasonable assumption that all dependencies are smooth other than the singular behavior of the default itself. Smoothness in the vicinity of the default justifies expanding all functional relationships to first order. The following derivation is illustrative and captures the eventual behavior.

If we assume a linear relationship between bond prices and quantity of debt supplied by the country () or demanded by investors () we have

| (8) |

| (9) |

and, since at equilibrium ,

| (10) |

assuming that supply and demand shocks would influence the intercepts—and not the slopes—of the linear dependences. The demand intercept depends on the overall liquidity available for financing the country’s debt, and therefore on the number of market participants. Rational investors are willing to lend money to the country as long as its debt ratio is below their estimate of . Due to all of the factors contributing to heterogeneity, we expect investor estimates of the critical value of default to have a distribution, whose form can be approximated by a normal distribution with average and standard deviation ,

| (11) |

where is the total number of investors. Since agents that estimate the default at a particular value of expect it also for any greater value of the debt ratio, is proportional to the cumulative distribution function

| (12) |

where is the error function. This expression can be well approximated with a sigmoid function Bryc2002 , according to

| (13) |

where is the parameter characterizing the heterogeneity. The bond supply intercept, , depends on the amount of money a country wants to borrow, and thus on its debt ratio. We expand this dependence around the critical value , keeping only the constant term. The effect of the absolute level of the debt ratio () on the supply (and more generally on bond prices) can be neglected compared to the effect of the sigmoidal function dependence (), i.e the distance of the debt ratio from its critical value. Substituting Eq. 13 into Eq. 10 we have

| (14) |

where and are constants that are functions of and . Their value can be inferred by imposing constraints on two limiting cases of Eq. 5:

-

•

, when

-

•

, when

Using these conditions we obtain

| (15) |

since . Inserting this expression in Eq. 6,

| (16) |

This equation relates the probability of default to the two parameters of our model, and . The family of curves vs at for different values of are shown in Fig. 6. The asymptotic behavior of the probability of default approaching 1 when the debt ratio goes to infinity is justified by theoretical Eaton1981 , empirical Reinhart2003 and numerical data Yue2010 .

| (17) |

When the debt ratio reaches the critical threshold, , the corresponding critical value for interest rates is

| (18) |

since risk-free interest rates are negligible compared to the interest rates of a country close to default. We can rewrite Eq. 17 as,

| (19) |

where is a measure of the distance between the current value of interest rates and the value at default. This linear relationship between and is verified empirically in Fig. 7 for Greece, and in Appendix D for Portugal, Ireland, Spain and Italy. While the slope of the linear fit gives the heterogeneity parameter, its intercept is the critical debt ratio of the country.

The debt threshold does not depend on the assumed amount of debt recovery, but the time of expected default does. Eq. 16 specifies the probability of default for different debt thresholds and implicitly the debt ratio at which the default probability reaches one, . For the generally observed case of 50% recovery, the critical debt ratio coincides with the debt threshold, .

Appendix B

Debt Feedback Loop

In this Appendix, we provide a quantitative description of the feedback loop in Fig. 3 (blue arrows). We are going to use this analysis to identify the expected change of the debt ratio over time, given policy options that provide below market interest rates such as austerity and bailouts.

The country’s debt trajectory is

| (20) |

where is the gross debt, is the market interest rates and is the primary deficit, i.e. government spending minus tax revenue. If we divide the previous equation by the economic output we have

| (21) |

where is the budget ratio. If we define the GDP growth as and note that , from the previous equation we have the accumulation equation,

| (22) |

This equation completes the feedback loop represented in Fig. 3: fundamental economic indicators determine the expected default probability (arrow 1 and Eq. 16), which influences market interest rates (arrow 2 and Eq. 6), which in turn influences the new value of economic indicators (arrow 3 and Eq. 22). This feedback loop reflects the role of interest payments themselves on the increase in country debt.

Finally, we show how we can solve Eq. 22 and fit the debt trajectory analytically. The following equations, which are not used anywhere else in the paper or in the default model, demonstrate that in order to avoid default in the not-too-long term, the GDP has to grow faster than borrowing. As we saw in Eq. 22, interest rates can affect the debt ratio, and the debt ratio grows very rapidly if , i.e. if the interest rates are larger than the rate of economic growth. To obtain a closed-form solution that shows the dependence of the debt ratio on the GDP change and interest rates, we assume that , and are not time dependent—this assumption is only used for the analytic fit in this Appendix, and not for our model or elsewhere in this paper—and solve Eq. 22 to give

| (23) |

where is the value of the debt ratio at time 0. The difference equation 22 can be transformed into a differential equation if the usual assumption of smoothness applies,

| (24) |

This equation can be solved to give

| (25) |

Equation 23 coincides with Eq. 25 for small values of , and either demonstrates how the debt ratio grows exponentially if . Since our model shows that there is a threshold debt ratio set by markets, an exponential growth is unsustainable. The fit of the time dependence of the Greek debt ratio with Eq. 25 is shown in Fig. 8. We emphasize that Equation 22, which includes the time dependence of , and , is more general than Equation 25. The latter is only used in this Appendix and not elsewhere in this paper.

Appendix C

Austerity Measures

In order to evaluate the effect of austerity measures on the debt ratio of a country, we use Eq. 22 to calculate given estimates by economic analysts for the GDP change and austerity targets for the budget ratio .

We assume the interest rates for the next two years are similar to current rates, , which is justified by the small absolute difference over time of the short-term interest rates, and the very few years over which the projection is being calculated.

Our purpose is solely to evaluate whether the magnitude of austerity measures that have been implemented may be able to avert a default, using available economic projections according to the debt threshold we obtained.

We report the estimates for and the targets for in Table 1.

The impact of the austerity programs on debt ratios are incorporated into the figures in Appendix D, showing their implications for averting defaults.

| Country | bailout | ||||

|---|---|---|---|---|---|

| Greece | 7.3 Financial2012 | 4.7 Financial2012 | -6.4 Baumann2012 | -1.9 Baumann2012 | yes |

| Portugal | 4.5 kowsmann2011 | 3.0 kowsmann2011 | -3.4 BancoDePortugal2012 | 0.0 BancoDePortugal2012 | yes |

| Ireland | 8.6 RTE2012 | 3.0 OCarroll2010 | 0.7 Finfacts2012 | 2.2 Thejournal2012 | yes |

| Spain | 5.3 Reis2012 | 3.0 Reis2012 | -3.0 RossThomas2012 | -1.9 RossThomas2012 | no |

| Italy | 1.7 irishtimes2012 | 0.5 Donadio2012 | -1.2 Brunsden2012 | 0.5 Donadio2012 | no |

Appendix D

Other Countries

VI.1 Portugal

VI.2 Ireland

VI.3 Spain

VI.4 Italy

References

- (1) S. Castle, In crisis, reminders of disputes in euro’s founding, The New York Times (Aug 17, 2011).

- (2) S. Rastello, Japan, Greece among nations close to having unsustainable debt, IMF says, Bloomberg (Sep 1, 2010).

- (3) European Commission, Eurostat Database (accessed in 2012).

- (4) D. Korowicz, Trade-off. Financial system supply-chain cross-contagion: A study in global systemic collapse, Metis Risk Consulting (2012).

- (5) R. M. Nelson, P. Belkin, D. E. Mix, Greece’s debt crisis: Overview, policy responses, and implication, Congressional Research Service R41167 (Aug 18, 2011).

- (6) S. O’Grady, Greece paves way for IMF rescue deal by agreeing savage cuts, The Independent (May 1, 2010).

- (7) S. Fidler, D. Enrich, EU forges Greek bond deal, The Wall Street Journal (Oct 17, 2011).

- (8) M. Lagi, Y. Bar-Yam, The European debt crisis: Bond markets out of equilibrium, in preparation (2012).

- (9) J. Eaton, M. Gersovitz, Debt with potential repudiation: Theoretical and empirical analysis, Review of Economic Studies 48, 289 (1981).

- (10) R. N. Cooper, J. D. Sachs, Borrowing abroad: The debtor’s perspective, NBER Working Paper 1427 (1984).

- (11) L. Alfaro, F. Kanczuk, Sovereign debt as a contingent claim: A quantitative approach, Journal of International Economics 65, 297 (2005).

- (12) H. L. Cole, P. J. Kehoe, Models of sovereign debt: Partial versus general reputations, International Economic Review 39, 55 (1998).

- (13) U. Panizza, F. Sturzenegger, J. Zettelmeyer, The economics and law of sovereign debt and default, Journal of Economic Literature 47, 651 (2009).

- (14) I. Arraiz, Default, settlement, and repayment history: A unified model of sovereign debt, SSRN (2006).

- (15) P. H. Lindert, P. J. Morton, How sovereign debt has worked, in Developing country debt and economic performance, Volume 1: The international financial system Jeffrey D. Sachs, ed. (University of Chicago Press, 1989), pp. 39–106.

- (16) C. F. D. Alejandro, Stories of the 1930s for the 1980s, in Financial policies and the world capital market: The problem of Latin American countries P. Armella, R. Dornbusch, M. Obstfeld, eds. (University of Chicago Press, 1983), pp. 5–40.

- (17) K. J. Mitchener, M. D. Weidenmier, Supersanctions and sovereign debt repayment, NBER Working Paper 11472 (2005).

- (18) M. Tomz, Reputation and international cooperation: Sovereign debt across three centuries (Princeton University Press, Princeton, 2007).

- (19) B. D. Paoli, G. Hoggarth, V. Saporta, Costs of sovereign default, Bank of England, Financial Stability Paper 1 (2006).

- (20) M. L. J. Wright, The theory of sovereign debt and default, UCLA Working Papers (2011).

- (21) M. P. Dooley, International financial architecture and strategic default: Can financial crises be less painful?, Carnegic-Rochester Conference Series on Public Policy 53, 361 (2000).

- (22) G. Sandleris, Sovereign defaults: Information, investment and credit, Journal of International Economics 76, 267 (2008).

- (23) D. Cohen, The debt crisis, a post mortem, in NBER Macroeconomics Annual 1992, Volume 7 O. Blanchard, S. Fischer, eds. (MIT Press, 1992), pp. 65–114.

- (24) A. Alichi, A Model of sovereign debt in democracies, IMF Working Paper WP/08/152 (2008).

- (25) R. Perotti, Redistribution and non-consumption smoothing in an open economy, Review of Economic Studies 63, 411 (1996).

- (26) E. Borensztein, U. Panizza, The costs of sovereign default, IMF Staff Papers 56, 683 (2009).

- (27) F. Sturzenegger, J. Zettelmeyer, Debt defaults and lessons from a decade of crises (MIT Press, Cambridge, MA, 2007).

- (28) F. Sturzenegger, J. Zettelmeyer, Creditors’ losses versus debt relief: Results from a decade of sovereign debt crisis, Journal of the European Economic Association 5, 343 (2007).

- (29) F. Stuzenegger, Tools for the analysis of debt problems, Journal of Reconstructing Finance 1, 1 (2004).

- (30) M. Aguiar, G. Gopinath, Defaultable debt, interest rates and the current account, Journal of International Economics 69, 64 (2006).

- (31) C. Arellano, Default risk and income fluctuations in emerging economies, American Economic Review 98, 690 (2008).

- (32) F. Hernandez-Trillo, A model-based estimation of the probability of default in sovereign credit markets, Journal of Development Economics 46, 163 (2000).

- (33) N. Kulatilaka, A. J. Marcus, A model of strategic default of sovereign debt, Journal of Economic Dynamics and Control 11, 483 (1987).

- (34) P. Manasse, N. Roubini, A. Schimmelpfennig, Predicting sovereign debt crises, IMF Working Paper WP/03/221 (2005).

- (35) R. Savona, M. Vezzoli, Multidimensional distance to collapse point and sovereign default prediction, CAREFIN Working Paper WP/12/08 (2008).

- (36) J. L. Stein, G. Paladino, Country default risk: An empirical assessment, CESifo Working Paper Series 469 (2001).

- (37) M. Tomz, M. L. J. Wright, Do countries default in “bad times”?, Journal of the European Economic Association 5, 352 (2007).

- (38) V. Z. Yue, Sovereign default and debt renegotiation, Journal of International Economics 80, 176 (2010).

- (39) E. D. Domar, The “burden of the debt” and the national income, The American Economic Review 34, 798 (1944).

- (40) D. Litterick, Billionaire who broke the Bank of England, The Telegraph (Sep 13, 2002).

- (41) M. Lagi, Y. Bar-Yam, K. Z. Bertrand, Y. Bar-Yam, The Food Crises: A quantitative model of food prices including speculators and ethanol conversion, arXiv:1109.4859v1 [q-fin.GN] (2011).

- (42) D. Gatopoulos, E. Becatoros, Greece secures biggest debt cut in history, Associated Press (Mar 9, 2012).

- (43) S. Deo, Greek devaluation: Is it such a good idea?, Consensus Economics (Oct 14, 2011).

- (44) J. M. Buchanan, External and internal public debt, The American Economic Review 47, 995 (1957).

- (45) O. Analytica, Japan’s debt financing program carries risks, Forbes (Jun 30, 2009).

- (46) P. Toscano, Biggest holders of US government debt, CNBC (Feb 3, 2012).

- (47) W. Xiong, H. Yan, Heterogeneous expectations and bond markets, The Review of Financial Studies 23, 1433 (2010).

- (48) A. Baumann, C. Broyer, A.-K. Petersen, R. Schneider, Scenarios on Greek government debt, Allianz, Economic Research and Corporate Development Working Paper 149 (2012).

- (49) Greece to get first payment before March 20, The Financial (Mar 2012).

- (50) G. A. Calvo, Debt relief and default penalties in an international context, IMF Working Paper WP/89/10 (1989).

- (51) M. Tudela, Sovereign default and recovery rates, 1983-2010, Moody’s Investors Service 132672 (2011).

- (52) G. Fane, C. Applegate, Sovereign default risk and the social cost of foreign debt, in The current account and foreign debt J. Pitchford, ed. (Routledge, London, 1995), pp. 161–170.

- (53) D. Oakley, R. Wigglesworth, Portugal slips into default territory, Financial Times (Jan 18, 2012).

- (54) Spain never so close to default, economist warns, Financial Post (Mar 21, 2012).

- (55) B. Kavoussi, Italy default fears grow as borrowing costs rise, The Huffington Post (Nov 9, 2011).

- (56) L. Elliott, Ireland: A dead cert for default, The Guardian (Apr 1, 2011).

- (57) W. Bryc, A uniform approximation to the right normal tail integral, Applied Mathematics and Computation 127, 365 (2002).

- (58) C. Reinhart, K. Rogo, M. Savastano, Debt intolerance, Munich Personal RePEc Archive 13932 (2003).

- (59) OECD, OECD Stat Extracts (accessed in 2012).

- (60) P. Kowsmann, J. T. Lewis, Portugal’s bailout comes with strict conditions; economy set to contract, The Wall Street Journal (Mar 13, 2011).

- (61) Projections for the Portuguese economy: 2012-2013, Banco De Portugal, Economic Bulletin (2012).

- (62) Sixth Troika review finds that Ireland is meeting bailout targets, RTE News (Apr 27, 2012).

- (63) L. O’Carroll, Ireland bailout: Full Irish government statement, The Guardian (Nov 28, 2010).

- (64) Irish economy 2012: Government cuts expected 2012 GDP growth to 0.7%, Finfacts Ireland (Apr 30, 2012).

- (65) Noonan stands by comments over “more difficult” budget if Ireland votes No, The Journal (May 2, 2012).

- (66) A. Reis, EU officials praise Spain budget, urge speedy implementation, Bloomberg Businessweek (Mar 31, 2012).

- (67) E. Ross-Thomas, S. Meier, Spain slips back into recession in first quarter: Economy, Bloomberg (Apr 30, 2012).

- (68) Italy delays balanced-budget target, Irish Times (Apr 18, 2012).

- (69) R. Donadio, G. Pianigiani, Italy pushes back balanced budget by 2 years, The New York Times (Apr 18, 2012).

- (70) J. Brunsden, Monti’s 2012 Italy budget in line with EU forecast, Bailly says, Bloomberg (Apr 19, 2012).