The Transition from Brownian Motion to Boom-and-Bust Dynamics

in Financial and Economic Systems

Abstract

Quasi-equilibrium models for aggregate variables are widely-used throughout finance and economics. The validity of such models depends crucially upon assuming that the systems’ participants behave both independently and in a Markovian fashion.

We present a simplified market model to demonstrate that herding effects between agents can cause a transition to boom-and-bust dynamics at realistic parameter values. The model can also be viewed as a novel stochastic particle system with switching and reinjection.

pacs:

89.65.Gh, 89.75.Fb, 89.75.DaI Introduction

In the physical sciences using a stochastic differential equation (SDE) to model the effect of exogenous noise upon an underlying ODE is often straightforward. The noise consists of many uncorrelated effects whose cumulative effect is well-approximated by a Brownian process and the ODE is replaced by an SDE .

However, in financial and socio-economic systems the inclusion of

exogenous noise (ie new information entering the system) is more

problematic — even if the noise can

be legitimately modeled as a Brownian process. This is because such

systems are themselves the aggregation of many individuals or trading

entities (referred to as agents) who typically

a) have differing

interpretations of the new information,

b) act differently depending upon their own recent history (ie

non-Markovian behaviour), and

c) may not act

independently of each other.

The standard approach in neoclassical economics and modern finance is simply to ‘average away’ these awkward effects by assuming the existence of a single representative agent as in macroeconomics Kirman , or by assuming that the averaged reaction to new information is correct/rational, as in microeconomics and finance m61 ; f65 . In both cases, the possibility of significant endogenous dynamics is removed from the models resulting in unique, Markovian, (quasi)-equilibrium solutions.

In reaction to this, many Heterogeneous Agent Models (HAMs) have been developed Hommes that simulate the agents directly. These have demonstrated that it is relatively easy to generate aggregate output data, such as the price of a traded asset, that approximate reality better than the standard averaging-type models. In particular the seemingly universal ‘stylized facts’ ms00 ; c01 of financial markets such as heteroskedasticity (volatility clustering) and leptokurtosis (fat-tailed price-return distributions resulting from booms-and-busts) have been frequently reproduced. However, the effects of such research upon mainstream modeling have been minimal perhaps, in part, because some HAMs require fine tuning of important parameters, others are too complicated to analyze, and the plethora of different HAMs means that many are mutually incompatible.

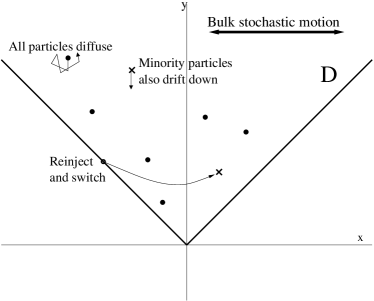

The purpose of this report is to investigate the range of validity of the quasi-equilibrium solutions obtained by ignoring endogenous effects such as a), b) and c) above. We do this by introducing a simplified version of the modeling framework introduced in ls08 ; l10 that can also be described as a particle system in two dimensions (Figure 1).

II A stochastic particle system with reinjection and switching

We define the open set by There are signed particles (with states or ) that move within subject to three different motions. Firstly there is a bulk Brownian forcing in the -direction that acts upon every particle. Secondly, each particle has its own independent two-dimensional diffusion process. Thirdly, for agents in the minority state only, there is a downward (negative -direction) drift that is proportional to the imbalance.

When a particle hits the boundary it is reinjected into with the opposite sign according to some predefined probability measure. Finally, when a particle does switch the position of the other particles is kicked in the -direction by a (small) amount where the kick is positive if the switching particle goes from the state to and negative if the switch is in the opposite direction. Note that the particles do not interact locally or collide with one another111A web-based interactive simulation of the model can be found at http://math.gmu.edu/harbir/PRLmarket.html.

II.1 Financial market interpretation

We take as our starting point the standard geometric Brownian motion (gBm) model of an asset price at time with . It is more convenient to use the log-price which for constant drift and volatility is given by the solution to the SDE

| (1) |

Note that the solution depends only upon the value of the exogenous Brownian process at time and not upon . This seemingly trivial observation implies that is Markovian and consistent with various notions of market efficiency. Thus gBm can be considered a paradigm for all economic and financial models in which the aggregate variables are in a quasi-equilibrium reacting adiabatically to new information.

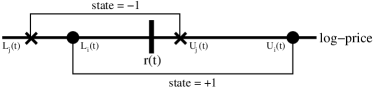

The instantaneous translation of new information into price changes is effected by ‘fast’ agents who will not be modeled directly. However, we posit the existence of ‘slow’ agents who are primarily motivated by price changes rather than new information and act over much longer timescales (weeks or months). At time the slow agent is either in state (owning the asset) or (not owning the asset) and the sentiment is defined as The slow agent is deemed to have an evolving strategy that at time consists of an open interval containing the current log-price (see Figure 2). The agent switches state whenever the price crosses either threshold, ie or , and a new strategy interval is generated straddling the current price.

We assume in addition that each threshold for every slow agent has its own independent diffusion with rate (corresponding to slow agents’ independently evolving strategies) and those in the minority (whose state differs from ) also have their lower and upper thresholds drift inwards each at a rate .

These herding constants are crucial as they provide the only (global) coupling between agents. The inward drift of the minority agents’ strategies makes them more likely to switch to join the majority. Herding, and other mimetic effects, appear to be a common feature of financial and economic systems. Some causes are irrationally human while others may be rational responses by, for example, fund managers not wishing to deviate too far from the majority opinion and thereby risk severely underperforming their average peer performance. The reader is directed to l10 for a more detailed discussion of these and other modeling issues.

Finally, changes in the sentiment feed back into the asset price so that gBm (1) is replaced with

| (2) |

where and the ratio is a measure of the relative impact upon of exogenous information versus endogenous dynamics. Without loss of generality we let and by setting the risk-free interest rate to zero and rescaling time.

One does not need to assume that all the slow agents are of equal size, have equal strategy-diffusion, and equal herding propensities. But if one does set and then one obtains the particle system simply by defining the position of the particle as . In other words, the bulk stochastic motion is due to exogenous noise; the individual diffusions are caused by strategy-shifting of the slow agents; the downward drift of minority agents is due to herding effects; the reinjection and switching are the agents changing investment position; and the kicks that occur at switches are due to the change in sentiment affecting the asset price via a linear supply/demand-price assumption.

II.2 Limiting values of the parameters

There are different parameter limits that are potentially of interest.

1) In the continuum limit the

particles are replaced by a pair of evolving density functions

and representing the density of each

agent state on — such a mesoscopic Fokker-Planck description of

a related, but simpler, market

model can be found in glc12 . The presence of nonstandard boundary

conditions, global coupling, and bulk stochastic motion present

formidable analytic challenges for even the most basic questions of

existence and uniqueness of solutions. However, numerical simulations

strongly suggest that, minor discretization effects aside, the behaviour of

the system is independent of for .

2) As the external information stream is

reduced the system settles into a state where is close to

either . Therefore this potentially useful simplification is

not available to us.

3) or In the limit the particles do

not diffuse ie. the agents do not alter their thresholds between

trades/switches. This case was examined in cgls05 and the lack of

diffusion does not significantly change the boom-bust behaviour shown

below. On the other hand, for the diffusion

dominates both the exogenous forcing and the herding/drifting and

equilibrium-type dynamics is re-established. This

case is unlikely in practice since slow agents will

alter their strategies more slowly than changes in the price of the asset.

4) This limit is the focus of

the report. When the particles are uncoupled and if the system

is started with approximately equal distributions of states

then remains close to 0. Thus (2) reduces to

(1) and the particle system becomes a standard equilibrium

model — agents have differing expectations about the future which

causes them to trade but on average the price remains ‘efficient’

. In Section III we shall observe that endogenous

dynamics arise as is increased and the equilibrium solution is no

longer stable.

5) For one

agent switching can cause an avalanche of similar switches, especially

when the system is highly one-sided with close to 1.

When the particles

no longer provides kicks (or affect the price) when they switch

although they are still coupled via

. The sentiment can still drift between and

over long timescales but switching avalanches and large, sudden, price

changes do not occur.

III Parameter estimation, Numerical Simulations and instability

In all the simulations below we use and discretize using a timestep which corresponds to approximately 1/10 of a trading day if one assumes a daily standard deviation in prices of due to new information. The price changes of 10 consecutive timesteps are then summed to give daily price return data making the difference between synchronous vs asynchronous updating relatively unimportant.

We choose so that slow agents’ strategies diffuse less strongly than the price does. A conservative choice of means that the difference in price between neutral () and polarized markets is, from (2), .

After switching, an agent’s thresholds are chosen randomly from a Uniform distribution to be within 5% and 25% higher and lower than the current price. This allows us to estimate by supposing that in a moderately polarized market with a typical minority agent (outnumbered 3–1) would switch due to herding pressure after approximately 80 trading days (or 3 months, a typical reporting period for investment performance)ss90 . The calculation gives . Finally, we note that no fine-tuning of the parameters is required for the observations below.

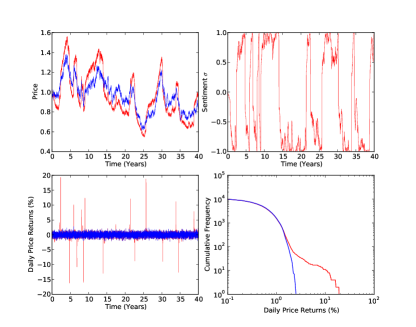

Figure 3 shows the results of a typical simulation, started close to equilibrium with agents’ states equally mixed and run for 40 years. The difference in price history between the above parameters and the equilibrium gBm solution is shown in the top left. The sudden market reversals and over-reactions can be seen more clearly in the top right plot where the market sentiment undergoes sudden shifts due to switching cascades. These result in price returns (bottom left) that could quite easily bankrupt anyone using excessive financial leverage and gBm as an asset pricing model! Finally in the bottom right the number of days on which the magnitude of the price change exceeds a given percentage is plotted on log-log axes. It should be emphasized that this is a simplified version of the market model in l10 and an extra parameter that improves the statistical agreement with real price data (by inducing volatility clustering) has been ignored.

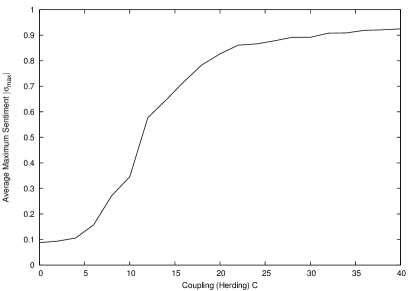

To conclude we examine the stability of the equilibrium gBm solution using the herding parameter as a bifurcation parameter. In order to quantify the level of disequilibrium in the system we record the maximum value of ignoring the first 10 years of the simulation (to remove any possible transient effects caused by the initial conditions) and average over 20 runs each for values of . All the other parameters and the initial conditions are kept unchanged.

The results in Figure 4 show that for values of as low as 20 the deviations from the equilibrium solution are as large as the system will allow, with the large majority of agents being in the same state at some point during the simulation. This is lower than the value of estimated above by a significant margin and it should be noted that there are other phenomena, such as new investors and money entering the asset market after a bubble has started, and localized interactions between certain subsets of agents that might cause further destabilization.

IV Conclusions

Financial and economic systems are subject to many different kinds of inter-dependence between agents and potential positive feedbacks. However, even those mainstream models that attempt to quantify such effectsss90 assume that the result will be a shift of the equilibria to nearby values without qualitatively changing the nature of the system. However we have demonstrated that at least one such form of coupling (herding) results in dis-equilibrium. Furthermore the new dynamics occurs at realistic parameters and is clearly recognizable as ‘boom-and-bust’. It is characterized by long periods of low-level endogenous activity (long enough, certainly, to convince equilibrium-believers that the system is behaving adiabatically) followed by large, sudden, reversals involving cascades of switching agents triggered by price changes.

The model presented here is compatible with existing (non-mathematized) critiques of equilibrium theory by Minsky and Sorosm74 ; soros03 . Furthermore, work on related models to appear elsewhere shows that positive feedbacks can result in similar non-equilibrium dynamics in more general micro and macro-economic situations.

Finally, the model has interesting links to other areas of mathematics and physics. In l10 it was shown that the switching cascades can be described using Queueing theory, with the price changes being equivalent to the busy-period of a queue. The model also shares similarities with other self-organizing systems such as the OFC earthquake modelofc92 . And if one considers agents to be evolving hysteretic operators then results concerning the interaction of stochastic processes and hysteresismd05 and phase transitions may provide valuable insights into the price dynamics.

The author thanks Michael Grinfeld and Rod Cross for numerous enlightening conversations and Julian Todd for writing the browser-accessible simulation of the particle system. The author also thanks Arjun Sanghvi for his additional computations and the NSF for his support.

References

- (1) A. Kirman, Journal of Economic Perspectives 6, 117 (1992)

- (2) J. Muth, Econometrica 6 (1961)

- (3) E. Fama, Journal of Business 38, 34 (1965)

- (4) C. H. Hommes (Elsevier, 2006) pp. 1109 – 1186, http://www.sciencedirect.com/science/article/pii/S157400210502023X

- (5) R. Mantegna and H. Stanley, An Introduction to Econophysics (CUP, 2000)

- (6) R. Cont, Quantitive Finance 1, 223 (2001)

- (7) H. Lamba and T. Seaman, Phys. A 387, 3904 (2008)

- (8) H. Lamba, Eur. Phys. J. B 77, 297 (2010)

- (9) A web-based interactive simulation of the model can be found at http://math.gmu.edu/harbir/PRLmarket.html

- (10) M. Grinfeld, H. Lamba, and R. Cross, “A mesoscopic market model with hysterestic agents,” To appear, Discr. Cont. Dyn. Sys. B

- (11) R. Cross, M. Grinfeld, H. Lamba, and T. Seaman, Phys. A 354, 463 (2005)

- (12) D. Scharfstein and J. Stein, The American Economic Review 80, 465 (1990), ISSN 00028282

- (13) H. Minsky, The Jerome Levy Institute Working Paper 74 (1992)

- (14) G. Soros, The alchemy of finance (John Wiley & Sons Inc, 1987)

- (15) Z. Olami, H. Feder, and K. Christensen, Phys. Rev. Lett. 68, 1244 (1992)

- (16) I. D. Mayergoyz and M. Dimian, Journal of Physics: Conference Series 22, 139 (2005), http://stacks.iop.org/1742-6596/22/i=1/a=009