Funding Liquidity, Debt Tenor Structure,

and Creditor’s Belief: An

Exogenous

Dynamic Debt Run Model

Abstract

We propose a unified structural credit risk model incorporating both insolvency and illiquidity risks, in order to investigate how a firm’s default probability depends on the liquidity risk associated with its financing structure. We assume the firm finances its risky assets by mainly issuing short- and long-term debt. Short-term debt can have either a discrete or a more realistic staggered tenor structure. At rollover dates of short-term debt, creditors face a dynamic coordination problem. We show that a unique threshold strategy (i.e., a debt run barrier) exists for short-term creditors to decide when to withdraw their funding, and this strategy is closely related to the solution of a non-standard optimal stopping time problem with control constraints. We decompose the total credit risk into an insolvency component and an illiquidity component based on such an endogenous debt run barrier together with an exogenous insolvency barrier.

Key words: Structural credit risk model, debt run,

liquidity risk, first passage time, optimal stopping time

JEL Codes: G01, G20, G32, G33

1 Introduction

The recent financial crisis has dramatically shown that financial

markets are not ideal. In particular, refinancing in periods of

financial distress can be extremely costly or even impossible due to

liquidity drying up in the market. It has been shown, for example by

Adrian and Shin (2008, 2010) and Brunnermeier (2009),

that the heavy use of short-term debt was a key contributing factor

to the credit crunch of 2007/2008. Firms, however, often prefer

short-term debt financing as it is cheaper than long-term debt.

Moreover, as argued by He and Xiong (2012b), short-term debt can also

be regarded as a disciplinary device for firms and can be used to

mitigate adverse selection problems and to reduce the cost of

auditing firms. Hence, several reasons support the use of short-term

financing. However, most of the existing credit risk models do not

take into account the rollover risk (or liquidity risk) inherent in

short-term debt financing. It is the aim of this paper to provide a

unified framework that incorporates rollover risk as well as

insolvency risk. Within an extended structural credit risk model,

our approach allows to investigate how a firm’s default probability

depends on

the rollover risk inherent in its particular financing structure.

Structural credit risk models were initiated by Merton (1974) and

Black and Cox (1976). In these models default happens if the firm

fundamental falls below some exogenous default barrier which often

relates to the firm’s debt level. A huge part of the literature on

structural credit risk modeling focuses on how to model such an

exogenous default barrier, as in Longstaff and Schwartz (1995) and

Briys and de Varenne (1997), among others222Optimal capital structural

models are regarded as the second generation of structural credit

risk models, which were initiated by Leland (1994, 1998), and

Leland and Toft (1996). Therein the firm defaults when its equity value

drops to zero, and the default barrier is determined endogenously by

its equity holders. Hilberink and Rogers (2002) and Chen and Kou (2009) extend this model

by introducing jump risk, and recently, He and Xiong (2012a)

extended this framework by including an illiquid debt market.. In

the following we will call this exogenous default barrier the

insolvency barrier. Given this exogenous insolvency barrier,

in this paper we derive an endogenous threshold value below which

short-term creditors decide to withdraw their funding, i.e., to run

on the firm, and we will call this barrier the debt run

barrier. The latter depends on not only the firm’s

creditworthiness but also the creditors’ beliefs about the

likelihood of a debt run in the remaining rollover periods.

Determining this debt run barrier is the main problem of this paper.

There is a third barrier, called the illiquidity barrier,

which represents the critical value when the firm is unable to pay

off its creditors in case of a debt run, and which is determined

endogenously from the debt run barrier. In addition, we show that

the debt run barrier always dominates the illiquidity barrier, which

in turn dominates the insolvency barrier. This relationship among

all three barriers not only helps to decompose the total credit risk

into an insolvency component and an illiquidity component, but also

illustrates the phenomenon that most firms have defaulted due to

illiquidity rather than due to insolvency in the recent

credit crunch.

Our first contribution is the provision of a rigorous formulation

for a class of structural credit risk models that study debt runs.

The classic debt/bank run model of Diamond and Dybvig (1983) features a

static setting where all the depositors simultaneously decide

whether or not to withdraw their demand deposits from a solvent but

illiquid bank. Ericsson and Renault (2006) and Goldstein and Pauzner (2005) provide

further extensions that are, however, still in the static setting.

In this paper, we consider debt runs from a dynamic viewpoint. The

debt run model introduced by Morris and Shin (2010) focuses on a

two-period setting where short-term creditors face a binary decision

in terms of global games at an interim time point.

Liang et al. (2014) provide a structural credit risk model

that also takes liquidity risk into account, as short-term creditors

can decide at a finite number of decision dates whether to roll over

or to withdraw their funding. They derive a debt/bank run barrier

based on the comparison of binary strategies for a representative

short-term creditor. Technically, the generalization from the

two-period setting of Morris and Shin (2010) towards the multi-period

setting of Liang et al. (2014) relies on the dynamic

programming principle (DPP). In Liang et al. (2014) the DPP

was only applied informally by comparing the expected returns for

the two investment options of creditors at the rollover dates. In

this paper, by introducing an appropriate value function for a

representative short-term creditor, which describes the discounted

expected return over the remaining rollover periods and which is

calculated based on the DPP, we derive the unique threshold

strategy, i.e., the debt run barrier. The representative creditor

decides to withdraw her funding if the firm’s fundamental falls

below this barrier at any decision date. In contrast to

Liang et al. (2014), the corresponding dynamic programming

equations presented in this paper are more generic and transparent,

which in particular allows us to introduce flexible

debt maturity structures into our model.

The second contribution of this paper is the imbedding of flexible

debt tenor structures into such an extended structural credit risk

model. In Liang et al. (2014) a discrete tenor structure is

assumed such that the rollover dates of short-term debt are given by

a sequence of deterministic numbers. This implies that all

short-term debt expires and can be rolled over at the same time. The

problem is therefore equivalent to a one-creditor problem. In

reality, however, firms typically stagger the maturities for

short-term debt to finance their long-term risky assets. Rollover

risk is partially reduced in this way as at each maturity date only

a fraction of total debt is due. Nevertheless, due to the maturity

mismatch between the assets and the liabilities sides, the firm is

still exposed to significant liquidity risk. Our model covers both

the discrete tenor structure and the staggered tenor structure. The

latter was first introduced by Leland (1994, 1998), and

Leland and Toft (1996), with Hilberink and Rogers (2002) and Chen and Kou (2009) providing

further technical details. The main idea is to assume a random

duration of debt in order to reflect the maturity mismatch.

Recently, He and Xiong (2012b) applied the staggered maturity structure

to the debt run literature where debt maturities are modelled as

arrival times of a Poisson process, whose intensity can then be

interpreted as the inverse of average debt duration. In this paper,

we utilize a more general and flexible Cox process to model the

staggered tenor structure. The economic intuition of using the Cox

maturity structure is that the average duration of the short-term

debt which a firm issues should fluctuate and depend on some

economic factors such as the firm fundamental or even the underlying

systemic risk from the market.

The third contribution of this paper is that we use a reduced-form

approach to model the impacts of other creditors’ rollover decisions

on the representative short-term creditor’s rollover decision. In

general, such impacts and the resulting equilibria are complicated

as we need to consider not only the impact of other creditors’

current rollover decisions, but also the impact of their future

decisions. In Morris and Shin (2010), they concentrate on the former

impact, and resort to a reduced-form approach by modeling the

representative short-term creditor’s belief on the proportion of

creditors not rolling over their funding at each rollover date as a

uniformly distributed random variable exogenously. In

He and Xiong (2012b), they concentrate on the latter impact, and assume

at each small time interval, there is only a small proportion of

creditors whose contracts expire and need to be rolled over. In this

paper, we try to include both impacts. The former impact is modeled

in a similar way to Morris and Shin (2010) and

Liang et al. (2014) by assuming the representative

creditor’s belief exogenously. However, we take a more general model

in the sense that the representative creditor’s belief is a general

random variable, and we also compare the results with different

assumptions on the distribution of such a random variable. The

latter impact is included by considering the dynamic programming

equation of the representative creditor, which is in the same spirit

as He and Xiong (2012b).

Finally, our fourth contribution is to answer the question whether

the representative short-term creditor’s rollover decision is indeed

optimal. This question also arises in the existing dynamic debt run

models such as those in Morris and Shin (2010), He and Xiong (2012b), and

Liang et al. (2014), but has so far not been answered. In

both the discrete and the staggered tenor structures, we show that

the decision problem of the representative short-term creditor is

equivalent to a non-standard optimal stopping time problem with

control constraints. At each rollover date the representative

creditor faces the risk that the firm may fail due to a debt run

based on her belief. If the firm survives, the creditor can then

decide whether to withdraw her funding (stop) or to roll over her

contract (continue). If the firm fails due to other creditors’ runs,

the representative creditor is then forced to stop and faces the

recovery risk from bankruptcy. Therefore, the decision time for the

representative creditor must exclude the default time due to debt

runs. For the case of the staggered tenor structure, since the

maturity dates are the arrival times of a Cox process, the

representative creditor is only allowed to stop (i.e., to withdraw

her funding) at a sequence of Cox arrival times rather than at any

stopping time. In the literature, such kind of optimal stopping at

Poisson-type arrival times has been used to solve the standard

optimal stopping time problem by

Krylov (2008) as the so-called randomized stopping time technique.

The paper is organized as follows. Section 2 describes the assumptions on the firm’s capital structure and explains the rollover decision of a representative short-term creditor in the benchmark model. We also present the rigorous formulation of the rollover decision problem in terms of dynamic programming equations. In section 3 we use the creditor’s value function derived in the dynamic programming equations to determine the short-term creditor’s debt run barrier as well as the firm’s illiquidity barrier in case of both the discrete and the staggered debt structures. We reformulate the creditor’s decision problem in terms of the associated optimal stochastic control problem in section 4. Section 5 discusses the related literature and concludes.

2 Benchmark Debt Run Model

In this section, we propose a debt run model that incorporates rollover risk into the structural credit risk framework.

2.1 Capital Structure of a Firm

Consider a market defined over a complete probability space , which supports a standard Brownian motion with its natural filtration after augmentation. The market interest rate is assumed to be constant. In this market, consider a firm whose fundamental value of assets follows

with constant volatility . The constant denotes the expected return on the firm’s risky assets. We assume that the firm fundamental is publicly observable.

The firm finances its asset holdings in the duration by issuing short-term debt, such as asset-backed commercial papers and overnight repos, long-term debt such as corporate bonds, and equities and others. At initiation time an amount is borrowed long-term at rate until fixed maturity . Moreover, an amount is borrowed short-term at rate until maturity . When short-term debt matures it can be successively rolled over until the next rollover date. This produces a sequence of maturity dates (or rollover dates) for short-term debt. For the moment, we do not impose any structural conditions on the short-term debt maturities . They could be either deterministic or random.

If there is no default, the value of short-term debt follows

and the value of long-term debt follows

The ratio of long-term debt over short-term debt is denoted by and follows

Moreover, we introduce a process as the ratio of the firm’s asset value over the short-term debt value . Hence, follows

Short-term creditors have the opportunity to withdraw their funding at the rollover dates. When the firm is under financial distress or when an outside investment opportunity is more attractive they will make use of this option. Long-term creditors, however, are locked in once they lend money to the firm. They are exposed to a higher risk, and therefore, should be rewarded with a higher interest rate. Moreover, since creditors are exposed to the firm’s default risk, a risk premium should be paid on top of the market interest rate. We have the following assumption on different interest rates333The assumption of constant interest rates is imposed to simplify derivations. In reality, different rates not only vary in time, but also move differently, motivating the so called multi-curve modeling (see for example Crépy et al (2012))..

Assumption 2.1

The long-term interest rate is strictly greater than the short-term interest rate , while the latter is strictly greater than the market interest rate , i.e., we assume .

2.2 The Rollover Decision of a Representative Short-Term Creditor

Short-term creditors choose whether to renew their maturing contracts, that is, they need to decide whether to roll over or to withdraw their funding (i.e., to run) at the maturity times. Hence, they face a dynamic coordination problem.

Consider the decision problem of a representative short-term creditor. The first key factor to determine the representative short-term creditor’s rollover decision is the insolvency risk stemming from the deterioration of the firm fundamental. To include this factor, we follow the classic first-passage-time framework (see for example Black and Cox (1976)) by assuming an exogenously given insolvency barrier

where is a safety covenant function of the ratio . As long as the asset value at any time is greater than or equal to the total value of debt , the firm can be considered solvent. Hence, it is natural to assume that

| (2.1) |

such that

The bankruptcy time due to insolvency is then given by the following first-passage-time

To coordinate with other creditors, the representative creditor needs to take other creditors’ rollover decisions into account, and makes her own decision based on whether the firm will survive debt runs or not at each rollover date . Assume that the creditor believes that the proportion of short-term creditors not rolling over their funding at each rollover date is a random variable supported on with its conditional density given .

The firm will survive debt runs if it can raise enough funding to pay off its creditors who run on the firm and still keep solvent. In case of a debt run the firm has to issue collateralized debt by pledging its assets as collateral to raise the liquidity. The actual value of the collateral does not matter. It is the maximum value of the collateral that determines whether the firm is still liquid or not. The maximum collateral value of the assets is expressed in terms of the fire-sale price with the fire-sale rate 444The constant is the fire-sale rate of the firm fundamental when the firm is in a distressed state, i.e., it represents the amount that can be borrowed by pledging one unit of the risky assets as collateral. For a detailed discussion of how to endogenously determine the fire-sale rate by the leverage of the firm, we refer to Liang et al. (2014). . If , the firm is able to pay off its creditors who run on the firm, so a potential debt run at time would not lead to a default. Hence, the second key factor determining the creditor’s rollover decision is her belief about the probability that the firm survives the debt run at the rollover date , which equals

| (2.2) |

conditional on the firm being solvent at , i.e. on the event . In both Morris and Shin (2010) and Liang et al. (2014), the random variable is simply assumed to be uniformly distributed on , so that and

This assumption is justified by global games theory as

it has been shown in Morris and Shin (2003) that this is a limiting

case of the situation with unobservable firm fundamental when the

variance of the noise term tends to zero. In section

3.2, we will show that the uniform distribution

assumption is relatively robust by comparing

it to a family of truncated normal distributions with the same mean but different variances.

The third key factor for the representative short-term creditor’s rollover decision is the recovery rate when the firm defaults either due to debt runs or due to insolvency. If the firm defaults at some time , the firm is exposed to certain bankruptcy costs. Suppose these are proportional to the firm fundamental value, and for , is the firm value after having paid the bankruptcy costs. Then, the value will be divided among all the creditors, so the representative short-term creditor obtains the proportion of her funding and she gets at most her debt value back. Thus, we define the recovery rate as

| (2.3) |

Note that in case of a default due to a debt run, it can happen that the asset value is larger than . Therefore, we have to cut off the recovery rate by However, if the firm defaults due to insolvency at the first-passage-time , the asset value by definition equals the insolvency barrier . In this case the recovery rate equals

which is less than 1 by condition (2.1).

We assume that rollover decisions are solely determined by the aforementioned factors, which we summarize as follows.

Assumption 2.2

The following three factors determine the rollover decision of a representative short-term creditor.

-

(i)

Insolvency risk is reflected by the first-passage-time when the firm’s asset value falls below the insolvency barrier .

-

(ii)

Rollover risk is reflected by the representative short-term creditor’s belief on the probability that the firm survives the debt run at the rollover date .

-

(iii)

Recovery risk is reflected by the fraction of funding that the representative short-term creditor obtains in case of a default at time .

We further impose the following condition on the safety covenant function for technical convenience.

Assumption 2.3

The safety covenant function in the definition of the insolvency barrier has the linear form for some positive constant .

2.3 Dynamic Programming Equations

In this section we derive dynamic programming equations for the short-term creditor’s rollover decision problem. We consider a representative short-term creditor who invests an amount normalized to 1 monetary unit at time . Her discounted expected return over the remaining time period is described by the value function given the current ratio of asset value over short-term debt value, and she discounts at the market rate . To investigate the creditor’s value function we go backwards in time starting with her last rollover date prior to terminal time . Suppose that her rollover date is the closest one prior to the maturity of long-term debt, that is, and . Figure 1 illustrates the maturities of the short- and long-term debt. If the maturities are random (as in section 3.2), then what we do in the following is to condition on one realization of so that . By abuse of notation, we continue to write for in such a case.

At the terminal time , the representative short-term creditor faces the insolvency risk that the firm may not pay back her funding, and her value function at the terminal time is555The probability of the insolvency time equal to the terminal time is zero, so at the terminal time the firm only faces the insolvency risk stemming from the final workout of the firm’s risky project. For this reason the recovery rate at time is redefined as .

| (2.4) |

which represents the insolvency risk stemming from the final workout of the firm fundamental as in Merton (1974).

During the last time period , all of the creditors are locked in, so there is no rollover risk, and the representative short-term creditor only faces the insolvency risk with the associated recovery risk. Her value function for is

| (2.5) |

where the first term in the bracket captures the insolvency risk from the firm fundamental falling below the insolvency barrier during the time period , and the second term captures the insolvency risk from the final workout of the firm’s risky project at time . Hence, (2.3) represents the insolvency risk due to the deterioration of the firm fundamental as in Black and Cox (1976).

To determine the value function at we take a closer look at the rollover decision problem. At the rollover date , if the firm survives a debt run, the representative short-term creditor will compare the expected return from rolling over her funding with the expected market return, and will choose whatever results in a higher return for her. If the firm defaults due to a debt run, she will receive the recovery value in any case, regardless of whether she decides to roll over her funding or not. Hence, the creditor can only make her rollover decision conditional on the firm surviving the current debt run. Therefore, the value function given in equation (2.3) also describes her discounted expected return at time for the remaining time period .

In general, during the time period for , the representative short-term creditor is exposed not only to the insolvency risk arising from the deterioration of the firm fundamental in the period but also to the rollover risk caused by other creditors’ rollover decisions at time . Table 1 summarizes her payoff at maturity .

| Decision | Solvency in , | Solvency in , | Insolvency in . |

|---|---|---|---|

| at | no default due to run at . | default due to run at . | |

| Run | |||

| Rollover |

At maturity if there is no default, the representative short-term creditor either withdraws her funding to get or renews her contract to receive . If the firm defaults due to a debt run at time , the creditor just gets the fraction of her funding back. Since the creditor believes that the firm survives a debt run at time with probability , her discounted expected return at time can be described by the following value function

| (2.6) |

The first term on the right hand side captures the insolvency risk within the time period , whereas the second term captures the rollover risk at time as well as the insolvency and rollover risks in . Therefore, the first term in the second line of (2.3) represents the future rollover risk (and insolvency risk) as in He and Xiong (2012b), and the second term in the second line of (2.3) represents the current rollover risk as in Morris and Shin (2010). Note that if the maturities are random, then both (2.3) and (2.3) are understood as conditioning on one realization of so that .

The dynamic programming equations (2.3) and (2.3) for the value function are the drivers to determine the debt run barrier in our model, which will be discussed later. By the Feynman-Kac formula, we have the following partial differential equation (PDE) representation for the value function .

Proposition 2.1

Suppose Assumptions 2.1, 2.2, and 2.3 are satisfied. For , let be the unique solution to the following PDE Dirichlet problem on

| (2.7) |

For , let be the unique solution to the following Dirichlet problem on

| (2.8) |

where is the infinitesimal generator for the ratio process given by

Then the value function is given by concatenating together

Based on the Green’s function technique, we further have the following analytical representation for the value function where .

Proposition 2.2

(Green’s Representation) For , denote and respectively as the boundary condition and the terminal condition of the corresponding PDE for the value function on , where for convenience. Then

| (2.9) |

on , where is the Green’s function for the operator defined as

on the domain given by

Proof. See Appendix A.1.

3 Threshold Strategies of Debt Run Model

In this section, we use the dynamic programming equations (2.3) and (2.3) to determine the debt run barrier as well as the illiquidity barrier for the representative short-term creditor. Our main objective is to show the monotonic relationship among the debt run barrier, the illiquidity barrier, and the exogenously given insolvency barrier.

3.1 Discrete Tenor Structure: Revisit of Liang et al. (2014)

In this subsection, we extend the main results in Liang et al. (2014) to our general setup. Liang et al. (2014) show that there exists a threshold, called the debt run barrier such that the representative short-term creditor will withdraw her funding whenever the firm fundamental falls below this barrier at a rollover date. The debt run barrier is only a finite sequence of numbers, since the creditor only has a finite number of rollover dates to decide whether to run or not. In our general setting we define the debt run barrier for any as the critical asset value such that the representative short-term creditor is indifferent in terms of running or rolling over her debt, i.e., it is defined via the unique value such that in the maximum term in dynamic programming equation (2.3). The debt run barrier is then determined by

Since such a debt run barrier is determined by the representative short-term creditor, it is actually the debt run barrier for all of the short-term creditors, who will then run on the firm if . Although the representative creditor (so every short-term creditor) holds the belief that proportion of them will run on the firm at each date , they will actually run at the same time based on such a debt run barrier strategy. In fact, such kind of debt run barrier strategy also appears in dynamic debt run models such as Morris and Shin (2010), He and Xiong (2012b) and Liang et al. (2014).

In the following, we show that such a debt run barrier always dominates the insolvency barrier. Note that the value function is obviously increasing with respect to , and when the firm goes bankrupt due to insolvency at a rollover date , the value function is

Due to Assumption 2.3 we have so that . Hence we have .

This means the insolvency barrier at any rollover date

is dominated by the debt run barrier, i.e., for Note that

this dominance always holds in Liang et al. (2014), since

the recovery rate is

assumed to be zero therein.

A debt run does not necessarily trigger a default, for example in the case where the firm can raise enough funding to pay off its maturing short-term debt. The firm will survive the debt run at the rollover date , if conditional on . Motivated by this observation we introduce a third barrier, which we call an illiquidity barrier , and which is defined as follows

| (3.1) |

Hence, an illiquidity default only occurs if there is a debt run and the firm is not able to raise enough funds to pay off its maturing short-term debt or not able to remain solvent at the debt run.

In the following, we show that the insolvency barrier at is also dominated by the illiquidity barrier, i.e., for Indeed, we always have

Theorem 3.1

Due to this relationship, the debt run barrier, the illiquidity

barrier and the insolvency barrier determine four possible scenarios

at each of the rollover dates

which are illustrated in the flowchart in Figure 2.

[Insert Figure 2 here.]

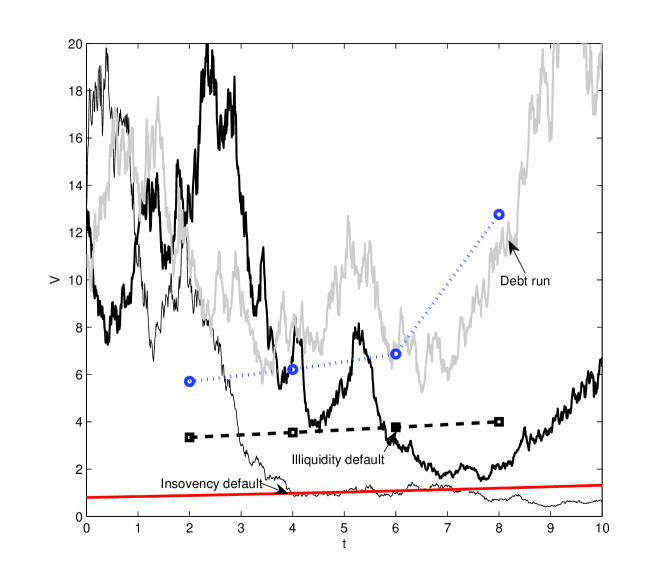

Figure 3 shows different scenarios in

our debt run model with the discrete tenor structure for three

simulated asset value paths. Here we assume is uniformly

distributed, and rollover dates at times and .

The dotted line shows the debt run barrier, the dashed line the

illiquidity barrier, and the solid line the insolvency barrier. Note

that in this discrete setting, the debt run barrier and the

illiquidity barrier are not continuous functions. They consist only

of the marked points. The black asset value path falls below the

insolvency barrier shortly before time At the rollover date

prior to this time, the asset value is larger than the debt

run barrier. Hence, in this simulation the firm will default shortly

before time due to insolvency. The dark black path falls below

the illiquidity barrier at the third rollover date at time ,and

before time it always stays above the insolvency barrier.

Thus, in this simulation the firm defaults due to illiquidity at

time . Finally, the grey path shows a scenario where a debt run

occurs at the last rollover date . At that time, however, the

asset value is still larger than the illiquidity barrier, meaning

that the firm is able to raise enough funds to pay off its

short-term creditors. Hence,

the firm survives the debt run.

[Insert Figure 3 here.]

3.2 Staggered Tenor Structure

In Liang et al. (2014) it is assumed that short-term debt rollover dates are given by a deterministic sequence of numbers and that they are the same for all short-term creditors. This assumption is rather restrictive. The firm is highly exposed to rollover risk in such a setting where all short-term funding expires at the same date. In practice, however, firms tend to spread out their debt expirations across time to reduce their exposure to liquidity risk. In this section, we introduce a more flexible debt maturity structure. Among others, Leland (1994, 1998) and Leland and Toft (1996) introduced the so-called staggered maturity structure to capture this fact. The idea is to use the arrival times of a Poisson process to model the maturities of short-term debt. In other words, the duration of short-term debt has an exponential distribution. While the random duration assumption appears different from the standard debt contract with a predetermined maturity, it captures the staggered debt maturity structure of a typical firm. For the application of such a Poisson maturity structure in the literature of debt runs, we refer to the recent work by He and Xiong (2012b).

The crucial parameter under the aforementioned Poisson maturity structure framework is the intensity . Its inverse can be interpreted as the average duration of short-term debt. We consider a Cox maturity structure, meaning that the maturity of short-term debt follows a more general and flexible Cox process. Recall that a Cox process is a generalization of Poisson processes in which the intensity is allowed to be random but in such a way that if we condition on a particular realization of the intensity, the process becomes an inhomogeneous Poisson process with intensity . The economic intuition of using the Cox maturity structure is that the average duration of the short-term debt that the firm issues should depend on some time-dependent economic factors such as the firm fundamental , the ratio of the firm fundamental over the short-term debt, or even some underlying states of the economy. In the following we therefore assume that the average maturity is a function of the ratio process .

We construct the short-term debt maturities by so-called canonical construction. Let be a sequence of independent identically distributed (i.i.d.) exponential random variables on some complete probability space , and define the enlarged probability space by

We assume the intensity has the form , where is a smooth function with compact support. Then the maturities of short-term debt are constructed recursively as

We summarize the above construction in the following assumption.

Assumption 3.1

(Cox maturity structure) The maturities of the short-term debt are the arrival times of a Cox process with intensity .

Under the Cox maturity structure, we still employ the representative short-term creditor’s dynamic programming equations (2.3) and (2.3) to determine her value function . Letting the ratio process start from and the short-term debt maturities start from , we synthesize the dynamic programming equations (2.3) and (2.3) into the following succinct form on the event :

| (3.2) |

By using the distribution of the first arrival time , and applying the Feynman-Kac formula, we derive the following PDE representation for the value function under the Cox maturity structure.

Proposition 3.2

Proof. See Appendix A.2.

In Appendix B, we provide a numerical algorithm to approximate the solution of the above PDE (3.3). In the rest of this section, we show that PDE (3.3) implies a unique threshold for the representative short-term creditor, i.e., there exists a unique debt run barrier such that she will run on the firm whenever both the firm’s asset value falls below such a barrier and her contract expires at some maturity . Thus, the debt run time in our model is characterized endogenously by the following first-passage-time

where is the threshold we shall derive in the remainder of this section. Recall that is the ratio of the firm fundamental over the short-term debt, so the debt run barrier is given as

We derive a free-boundary problem to determine first the threshold and secondly the debt run barrier based on the semi-linear PDE (3.3).

-

(i)

If , the representative short-term creditor will keep lending her money to the firm because either the debt is not due yet or if the debt is due she decides to roll over her funding. Her value function , and (3.3) reduces to

(3.4) The third term in the above equation represents the creditor’s premium of the return, the fourth term represents the expected effect of the rollover risk if the creditor rolls over her funding, and the last term represents the expected effect of recovery risk associated with a potential debt run.

-

(ii)

If , the representative short-term creditor will run on the firm if the debt is due. Her value function , and (3.3) reduces to

(3.5) While the third term and the last term in (3.5) have the same meanings as those in (3.4), the fourth term captures the expected effect of rollover risk from the representative short-term creditor’s own run.

-

(iii)

Finally, by the continuity of , the creditor’s value function at the threshold should be equal to , and the following smooth-pasting condition should be satisfied

In summary, we obtain the following two-phase free-boundary problem to determine the threshold (i.e., the debt run barrier) of the representative short-term creditor (so every short-term creditor).

Proposition 3.3

Proof. We only need to prove the smooth-pasting condition, which is straightforward since PDE

(3.3) admits a unique classical solution.

Similar to the case of the discrete tenor structure in section 3.1, a debt run does not necessarily trigger the firm’s default. The firm will not default due to a debt run if the firm can raise enough funding to pay off its short-term creditors who run on the firm, and remain solvent at the debt run, i.e., if conditional on . Therefore, we define the firm’s illiquidity barrier as

However, such a barrier only acts at a sequence of Cox arrival times . At each infinitesimal time interval with probability , the short-term debt matures, and an illiquidity default will happen if . With probability , the short-term debt does not mature yet, so all of the short-term creditors are locked in, and an illiquidity default will not occur even if . We have a similar relationship among the barriers as in the case of the discrete tenor structure.

Theorem 3.4

Suppose that Assumptions 2.1, 2.2, 2.3, and 3.1 are satisfied. Then at any time , the debt run barrier is greater than or equal to the illiquidity barrier, while the latter is greater than or equal to the insolvency barrier

The above relationship gives us the following four possible scenarios at any rollover date

-

(i)

: Default due to insolvency;

-

(ii)

: Debt run occurs and triggers a default due to illiquidity;

-

(iii)

: Debt run occurs, but no default caused by the run;

-

(iv)

: The creditor rolls over to the next maturity .

Proof. The proof is essentially the same as the proof for

Theorem 3.1, so we omit it.

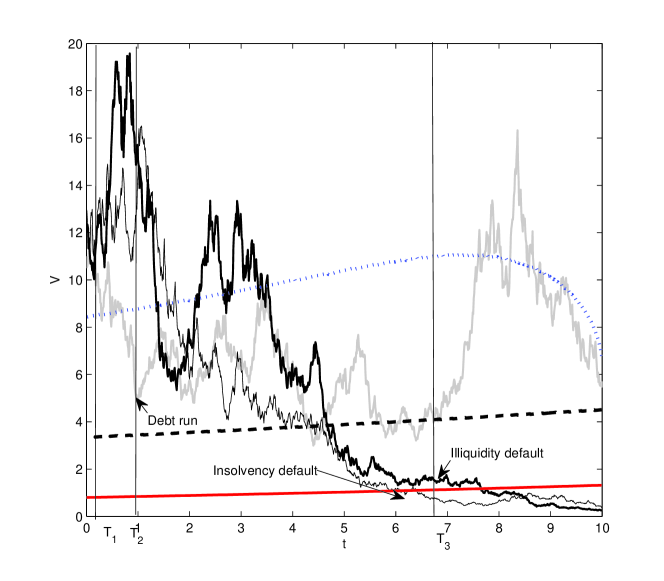

Figure 4 illustrates different scenarios in our debt run model with the staggered tenor structure of short-term debt and the uniform distribution on the proportion of short-term creditors not rolling over their funding at each rollover date. Here the intensity of the Cox process is chosen to be . The dotted line shows the debt run barrier, the dashed line the illiquidity barrier and the solid line the insolvency barrier, all of which are continuous functions in this model setting. The marked times , , and are one realization of the arrival times of the Cox process, which are smaller than the final date . At the first rollover date all three asset value paths are above the debt run barrier. Hence, all of the creditors roll over their contracts. The black asset value path is above all of the three barriers at , but falls below the insolvency barrier before the third rollover date . Hence, the firm will default at that time point before . At the second rollover date , the grey path falls below the debt run barrier but is still above the illiquidity barrier. This means that a debt run occurs at that date, but the firm is able to pay off its creditors and survives. At the last rollover date the dark black path is below the illiquidity barrier, which means that a debt run occurs and the debt run actually triggers an illiquidity default. Note that all three paths fall below the debt run and the illiquidity barriers already much earlier in time. However, as these times are not rollover dates for the representative short-term creditor, she cannot withdraw her funding at these dates.

The figure also illustrates the relation between different barriers,

which has been theoretically proved in Theorem 3.4; the

debt run barrier is always greater than or equal to the illiquidity

barrier, which in turn is always greater than or equal to the

insolvency barrier.

[Insert Figure 4 here.]

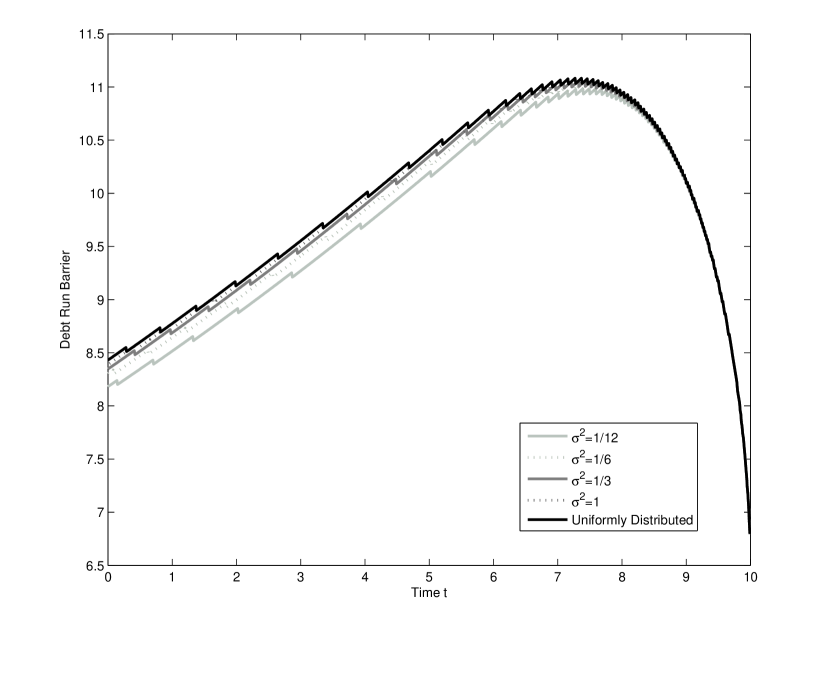

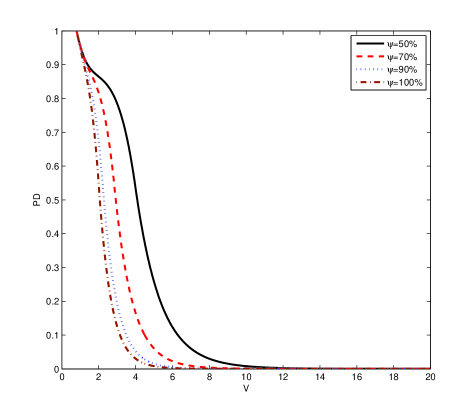

Finally, we show in Figure 5 the debt run barrier with different assumptions on the random variable , the representative short-term creditor’s belief on the proportion of short-term creditors not rolling over their funding. The top line shows the debt run barrier when is uniformly distributed: . From the next top line to the bottom line, they correspond to the debt run barrier with following normal distribution truncated on with mean and variance on . That is, has the conditional density

where and are the density function and the cumulative

distribution function of a normal random variable

respectively. The top line and the bottom line have the same mean

and the same variance , which illustrates that the

uniform distribution assumption is more conservative for the

creditors compared to the normal distribution assumption. On the

other hand, for the normally distributed with the same mean,

the larger the variance is, the higher the debt run barrier.

[Insert Figure 5 here.]

3.3 Comparison of the Discrete and the Staggered Tenor Structures

This section compares different debt tenor structures, i.e., the discrete and the staggered tenor structures. We first calculate the survival probabilities under both tenor structures. For the calculation of the survival probability under the discrete tenor structure setting, we refer to Liang et al. (2014). The calculation of the survival probability under the staggered tenor structure is tricky, as the number of Cox arrival times happening during the time interval is random. Inspired by the recursive formula (3.2) for the calculation of the value function, we also calculate the survival probability in a recursive way. Let be the corresponding survival probability at time given the current ratio . Then on the event ,

where . By Lemma A.1, the survival probability can be calculated as

Therefore, the Feynman-Kac formula gives the following semilinear PDE representation for the survival probability :

| (3.7) |

Its solution can be numerically approximated in a similar way to the

numerical approximation for (3.3) in Appendix

B. Given the survival probability , the default

probability can then be calculated as .

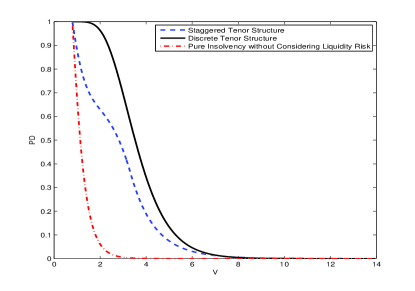

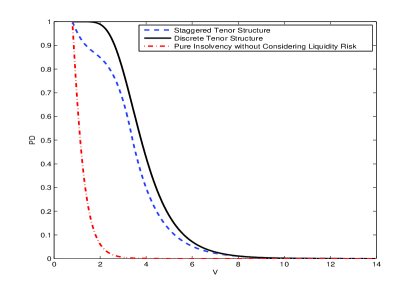

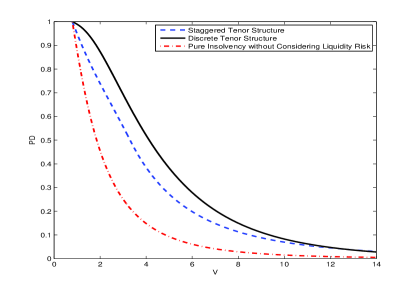

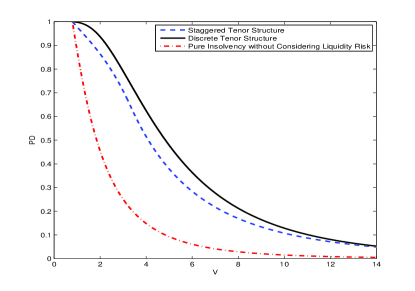

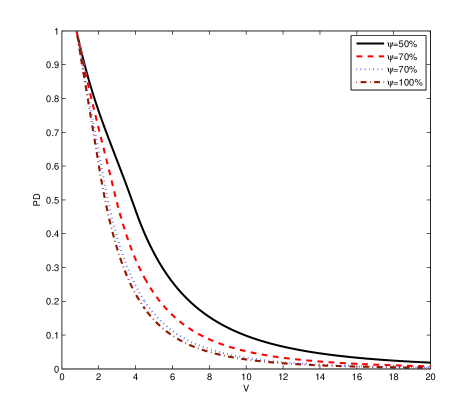

In Figure 6 we show the default

probabilities under both the discrete and the staggered tenor

structures with uniformly distributed . The dashed-dotted line

is the default probability without taking rollover risk into

account, which corresponds to the default probability in the setting

of Black and Cox (1976). Hence, the areas between the dashed-dotted line

and the other two lines represent the rollover risks induced by debt

runs under the staggered tenor structure and under the discrete

tenor structure, resp. The results show that the default probability

is increasing with increasing volatility as the asset value becomes

more risky. Furthermore, the figure supports the intuition that

replacing the discrete tenor structure by a staggered tenor

structure reduces liquidity risk.

[Insert Figure 6 here.]

In Figures 6(a) and 6(b) we see a kink in the

default probability for the staggered tenor structure. This kink is

less noticeable in Figures 6(c) and 6(d) and

does not appear in the discrete tenor structure case. This indicates

that this feature is due to the different specifications in the

intensity function of the Cox process and the volatility

of the firm fundamental. For very low asset values

with high probability, the insolvency component

determines the profile of the default probability in the staggered

tenor structure case. For higher asset values can be smaller

than . In this case there exists a critical asset value

such that creditors will very likely decide to withdraw when the

asset value is below this level and a run will most likely induce an

illiquidity default. This implies an almost flat default probability

for asset values below this critical level.

For higher asset values a debt run does not necessarily imply an illiquidity default and thus the default probability is monotonically decreasing for increasing asset value. The same feature is noticeable in Figure 7(a) which we will discuss below.

[Insert Figure 7 here.]

When creditors fear that the firm will be unable to repay their

debt, they will withdraw their funding simultaneously at a rollover

date and thereby, they might trigger an illiquidity induced default.

The key quantity in our model that determines the creditors’

behavior is their beliefs on the survival probability of the debt

run . When is close to one, creditors are

optimistic to get paid off. This is the case when either the firm’s

asset value and the fire-sale rate are high or when the short-term

debt notional is very low. Figure 7

shows

that the illiquidity component of the default probability

dramatically increases when fire-sale rate decreases. Thus,

creditors’ might withdraw their funding because they have a very

pessimistic view on the firm’s ability to repay them (low fire-sale

rate induces low ) although the firm’s asset value might be

well above the insolvency barrier. This supports the idea that debt

runs can occur as a result of pure coordination failures where

can be interpreted as a coordination

parameter.666Arifovic et al. (2013) study how coordination

problems can affect the occurrence of bank runs in controlled

laboratory

environments.

A natural question to ask is, what will happen with the discrete tenor structure when the number of rollover dates increases to infinity, meaning that creditors can decide to roll over or to withdraw their funding at any time ? Intuitively, one would expect that with increasing rollover frequency, one should approximate the staggered tenor structure model. However, there is another important difference between the two debt tenor structures. In the case of the discrete tenor structure we implicitly assume that all creditors have the same rollover dates, whereas in the staggered tenor structure model at each rollover date, corresponding to a Cox arrival time, only a fraction of total debt is due. Different short-term creditors hence have different rollover dates in that situation.

In the following, we will first study the impact of the intensity

of the Cox process on the creditor’s value

function. We assume the function to be constant and thus

independent of the ratio process . The intensity of the Cox

process not only specifies the creditor’s rollover dates but also

affects the average duration of short-term debt. For the average duration of debt is equal to ,

and in an infinitesimal time interval a fraction of

debt is maturing. The larger is , the more debt is maturing at

the same rollover date, and the larger is the rollover frequency of

short-term debt. Therefore, for large enough the staggered tenor

structure model and the discrete tenor structure model should result

in approximately the same value function for the short-term

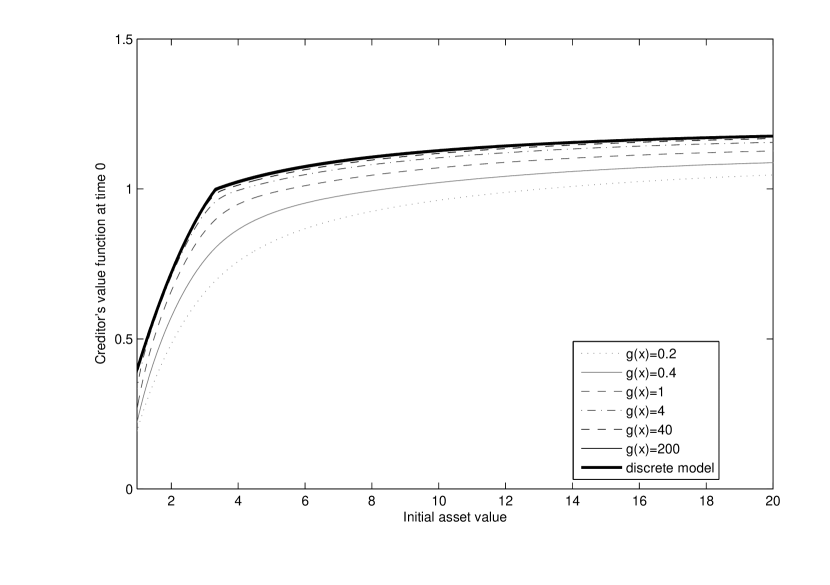

debt. This result is numerically validated in Figure 8. The number of rollover dates in the discrete

tenor structure model is fixed at , and the intensity of the

Cox process in the staggered

tenor structure model varies from to . This supports our previous discussion of the kink in the default probabilities for the staggered tenor structure visible in Figures 6(a) and 6(b) where . When increasing the intensity to as in Figures 6(c) and 6(d) the above discussed effect becomes less prominent and the default probability in the staggered tenor structure and the discrete tenor structure case are much closer.

[Insert Figure 8 here.]

In section 3.1, we derived the debt run barrier for the

discrete tenor structure by determining the threshold ratio

such that , i.e., the creditor is indifferent

between rolling over and withdrawing her funding. Similarly in

Proposition 3.3, we derived the debt run

barrier for the staggered tenor structure by solving the

free-boundary problem (3.6). Next, we will

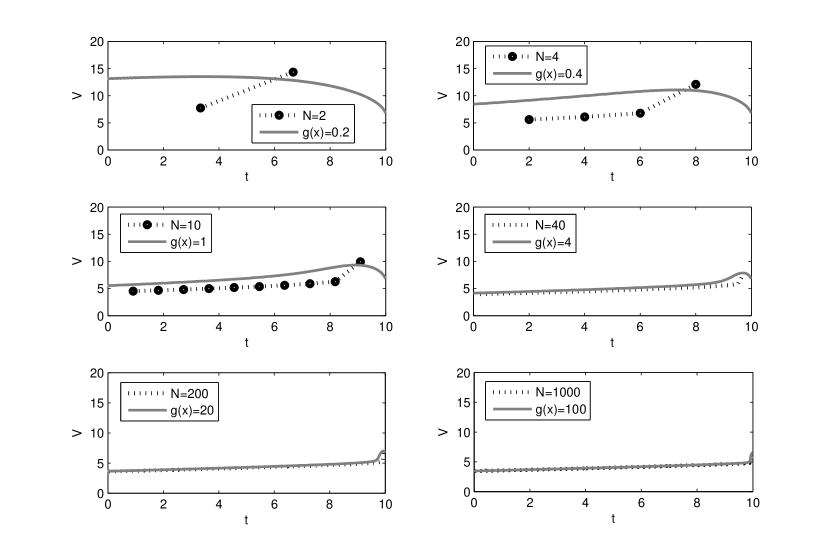

investigate in Figure 9 the

impact of the Cox intensity and the rollover frequency on

the debt run barrier. The graphs show that the discrete tenor

structure model with high rollover frequency approximates the

staggered tenor structure model with large intensity .

[Insert Figure 9 here.]

4 Optimal Stochastic Control Formulation

In this section we are concerned with whether the representative short-term creditor’s decision is optimal. Intuitively, since the creditor’s decision follows the DPP, her decision should be optimal. The question then is, what is the corresponding optimal stochastic control problem? To answer this question we first investigate the case of the discrete tenor structure and then discuss the staggered debt structure.

4.1 Discrete Tenor Structure

Let us first consider the case of the discrete tenor structure, i.e., short-term debt maturities are a sequence of deterministic numbers. Recall that at each rollover date , the creditor believes that there is a probability that the firm may default due to debt runs. Let denote the time that the firm defaults due to a debt run. Hence, is a random time taking value in .

Let be the time at which the representative short-term creditor decides to withdraw her funding and to run on the firm. This is an -stopping time. We first consider the case , i.e., the firm fails due to insolvency before its project expires. If , the creditor withdraws her funding before an illiquidity or insolvency default happens. In this case she will obtain the payoff

If , the firm fails due to the debt run before the creditor decides to withdraw her money and before an insolvency happens. Hence, the creditor will obtain the payoff

Finally, if , the firm defaults due to insolvency before the illiquidity default takes place and before the creditor decides to withdraw her funding. Then, the creditor will obtain the payoff

On the other hand, on the event , i.e., no insolvency happens before the project ends, the creditor will obtain the payoff

Table 2 summarizes the aggregate payoff of the representative creditor.

| Insolvency time | Decision time | Payoff |

|---|---|---|

For any where could be either or , we define the aggregate discounted payoff from time to as777Recall that as defined in (2.4).

The creditor will choose an optimal -stopping time to maximize her expected payoff

| (4.1) |

The following theorem states that the creditor’s value function defined by the dynamic programming equations (2.3) and (2.3) is indeed optimal.

Theorem 4.1

Proof. See Appendix A.3.

4.2 Staggered Tenor Structure

Next we consider the case of the staggered tenor structure, i.e., the maturities are the arrival times of a Cox process with intensity . Similar to the discrete tenor structure, we define as the default time due to a debt run. Since is chosen among the Cox arrival times with probability , it is well known that is the first arrival time of another Cox process with intensity . Let again denote the rollover date at which the representative short-term creditor decides to withdraw her funding and to run on the firm. This is a -stopping time under the staggered tenor structure with , i.e., must be chosen from the arrival times of the Cox process,

The representative short-term creditor will choose an optimal -stopping time to maximize her expected payoff

| (4.2) |

In contrast to the previous section on the discrete tenor structure, the optimal stopping time problem (4.2) can now only be stopped at the Cox random times . Hence, knowing only the Brownian filtration is certainly not enough to decide when to stop; one has to know the additional filtration from the Cox process in order to determine when to stop. Similar to the case of the discrete tenor structure, we can show that the solution to this optimal stopping time problem is given by the dynamic programming equation (3.2).

Theorem 4.2

Proof. See Appendix A.4.

4.3 Another Look at Default Mechanism

By deriving the debt run barrier and illiquidity barrier from the DPP, together with the exogenous insolvency barrier, we obtain the default mechanism in both Theorems 3.1 and 3.4. In this section, from the optimal stopping representation of debt runs in both Theorems 4.1 and 4.2, we can interpret the default mechanism from the optimal stochastic control viewpoint as follows. The representative creditor will choose an optimal rollover date to withdraw her funding, i.e. to run on the firm. For the case of discrete tenor structure, the creditor will choose an optimal stopping time from a sequence of deterministic times. For the case of staggered tenor structure, the creditor will choose an optimal stopping time from a sequence of Cox arrival times. At each rollover date, she can only make her decision if the firm is solvent up to that date, and if the firm survives the debt run by other creditors (based on her belief ). What we have shown is that the DPP used to derive the debt run barrier strategy corresponds to a non-standard optimal stopping time problem. Therein, the bankruptcy time due to debt runs is based on the creditor’s belief , so it is not necessarily the real bankruptcy time, and the creditor can choose to run either before or after . The creditor will then decide her debt run barrier based on her belief , or equivalently . Since we consider the decision problem of a representative short-term creditor, all of the short-term creditors will run on the firm if .

5 Discussion and Conclusion

In this paper, we provide a rigorous formulation for a class of structural credit risk models that take into account not only insolvency risk but also illiquidity risk due to possible debt runs. We show that there exists a unique threshold strategy, i.e., a debt run barrier for short-term creditors to decide when to withdraw their funding. This allows us to decompose the total credit risk into an illiquidity component based on the endogenous debt run barrier and an insolvency component based on the exogenous insolvency barrier.

The default mechanism in dynamic debt run models is mainly triggered by creditors’ runs as shown in Morris and Shin (2010), He and Xiong (2012b), and Liang et al. (2014). This is different from traditional structural credit risk models where the default mechanism is usually triggered by equity holders as they either exogenously set a default barrier or endogenously determine an optimal default barrier. Cheng and Milbradt (2012) consider decision problems of both creditors and equity holders in the dynamic debt run setting. In this paper, we consider that the equity holders exogenously set the insolvency barrier, while the creditors endogenously determine the debt run barrier and the illiquidity barrier. On the other hand, most of dynamic debt run models are based on the DPP, but up to now the corresponding optimal stochastic control problem for the DPP in dynamic debt run models has not been specified. In this paper, we prove that the DPP is in fact derived from a non-standard optimal stopping time problem with control constraints and we explicitly state the associated optimal control problem. This may help us better understand the default mechanism of debt runs.

In dynamic debt run models, one crucial assumption is the maturity structure of short-term debt. Both He and Xiong (2012b) and Cheng and Milbradt (2012) utilize the Poisson random maturity assumption to capture the staggered tenor structure, whereas Liang et al. (2014) assume a sequence of deterministic rollover dates generalizing the two-period model of Morris and Shin (2010). In this paper, we consider both discrete and staggered tenor structures. Moreover, we show that the two tenor structures converge to each other when the rollover frequency goes to infinity.

Finally, the representative short-term creditor’s belief about other creditors’ current and future rollover decisions also characterizes a dynamic debt run model. In Morris and Shin (2010) and Liang et al. (2014) such a belief is modeled by a uniformly distributed random variable. In this paper, we generalize this assumption by modeling such a belief as a general random variable. Furthermore, the impact of the creditors’ future rollover decisions are included by considering the dynamic programming equation of the representative short-term creditor, which is in the same spirit as He and Xiong (2012b). Notwithstanding, our model only takes account of other creditors’ rollover decisions on a representative creditor, but not vice vera, by assuming her belief exogenously, because in practice such a belief may depend on various factors that are not present in the model such as monetary policy and the states of the economy. Hence, in this sense our debt run model is an exogenous model rather than an equilibrium model. The corresponding equilibrium model could be more challenging, and is left for the future research.

Acknowledgements

We thank the Editor-in-Chief, Ulrich Horst, a Co-Editor, an Associate Editor, and a Referee for their valuable comments and suggestions. The article was previously circulated under the title A Continuous Time Structural Model for Insolvency, Recovery, and Rollover Risks. This work was supported by the Oxford-Man Institute of Quantitative Finance, University of Oxford, and by the Excellence Initiative through the project “Pricing of Risk in Incomplete Markets” within the Institutional Strategy of the University of Freiburg. The financial support is gratefully acknowledged by the first and the second authors. Several helpful comments and suggestions from Lishang Jiang, Yajun Xiao, and Qianzi Zeng are very much appreciated. We also thank the participants at the Conference on Liquidity and Credit Risk in Freiburg 2012, the INFORMS International Meeting in Beijing 2012, the 4th Berlin Workshop on Mathematical Finance for Young Researchers in Berlin 2012, the 2013 International Conference on Financial Engineering, in Suzhou 2013, the 6th Financial Risks International Forum on Liquidity Risk in Paris 2013, the IMA Conference on Mathematics in Finance in Edinburgh 2013, the 30th French Finance Association Conference in Lyon 2013, and the European Financial Management Association 2013 Annual Meetings in Reading 2013, as well as seminar participants at the University of Oxford, Imperial College, University of Texas at Austin, and Tongji University for several insightful remarks.

A Appendix for Proofs

A.1 Proof of Proposition 2.2

The proof is essentially the same as Lemma 3.2 and 3.3 in Liang and Jiang (2012), so we only sketch it.

First, note that under the new coordinate , the PDEs (2.7) and (2.8) become on a regular domain . The Green’s function for the operator on is the solution to the following PDE problem

| (A.1) |

By making the transformation , , and

it is easy to verify that satisfies a heat equation on the half plane. Its solution can be easily obtained by the standard image method.

Next, given the Green’s function , we derive the solution to on the domain with the boundary and terminal data and by applying integration by parts. Consider the adjoint problem of (A.1) on

| (A.2) |

where is the adjoint operator of

Since satisfies and satisfies the adjoint equation , applying integration by parts to the integral

and using the boundary and terminal data and for

will give us the Green’s representation formula

(2.9).

A.2 Proof of Proposition 3.2

We have the following property for the first arrival time (i.e., the first short-term debt maturity) , the proof of which can be found for example in Bielecki and Rutkowski (2002).

Lemma A.1

The process defined by for is an -hazard process associated with , that is,

Moreover, for any -adapted process and -stopping time , on the event ,

| (A.3) |

| (A.4) |

In the following, we employ the distribution of given by Lemma A.1 to calculate (3.2). For the first and the third terms, by using (A.4), we obtain

For the second term, based on (A.3), we obtain

For the last term, by employing (A.3) again, we obtain

By combing the above three equalities, we finally derive

A.3 Proof of Theorem 4.1

For , we consider a sequence of optimal stopping time problems

where is an -stopping time taking value in . Then the value of the optimal stopping time problem (4.1) is given by , and we want to show that .

Obviously we have , since there is no optimization problem involved in which is

The idea is to introduce a sequence of auxiliary optimal stopping time problems whose optimal stopping times are also permitted to stop at the initial time .

We have the following relationship between and (see Liang (2013)):

| (A.5) |

For , by taking conditional expectation on in , we obtain

where we used the Markovian property for in the last equality. Note that the first term in the bracket does not involve the stopping time , so the supremum over only takes action on the second term and is equal to

which, according to the definition of , is

By the relationship (A.5), we obtain the recursive formulation for :

We recognize that the above equation is just the dynamic programming

equation for in (2.3). Since

we have already proved , by proceeding

backwards we obtain

.

A.4 Proof of Theorem 4.2

The proof is essentially the same as the proof for Theorem 4.1. For any , by letting start from and start from , we consider a family of optimal stopping problems

where is

a -stopping time taking value in . Therefore, is not allowed to stop at the

starting time . The value of the optimal stopping time problem

(4.2) is given by , and we want to

prove that .

Similarly to the case of the discrete tenor structure, we introduce

a family of auxiliary optimal stopping time problems where the

optimal stopping times are also allowed to stop at the starting time

We have the following relationship between and (see Liang (2013)):

| (A.6) |

Taking expectations conditional on in and using the strong Markov property for , we obtain for any

which by the definition of is equal to

The result then follows from the relationship

(A.6).

B Appendix for the Numerical Approximation of the Solution to PDE (3.3)

We first transform PDE (3.3) by defining and . Then PDE (3.3) reduces to

| (B.1) |

where

with boundary and initial conditions

In the following, we derive the implicit finite difference equation for PDE (B.1). Let denote the step size between two updates of the value function in the time dimension. Similarly, denotes the step size between grid points in the space dimension of the value function . The relevant range of two variables is taken to be

where is a large constant such that realization of outside the region occurs with negligible probability. At each grid point, we define

and the implicit finite difference equation for is

| (B.2) |

where

for and . The corresponding boundary and initial conditions are

where and , with abuse of notation, denote the vectors containing the discrete values of the boundary and initial conditions, respectively.

The implicit finite difference equation (B) can be rewritten as the following nonlinear algebraic equation:

| (B.3) |

where , and is a tridiagonal matrix:

with

References

- Adrian and Shin (2008) Adrian, T., and Shin, H.S. (2008): Liquidity and financial contagion. Financial Stability Review, Special issue on liquidity, No. 11, Banque de France.

- Adrian and Shin (2010) Adrian, T., and Shin, H.S. (2010): Liquidity and leverage. Journal of Financial Intermediation 19(3), 418–437.

- Arifovic et al. (2013) Arifovic, J., Jiang, J.H., and Xu, Y. (forthcoming): Experimental evidence of bank runs as pure coordination failures. Journal of Economic Dynamics and Control.

- Bielecki and Rutkowski (2002) Bielecki, T.R., and Rutkowski, M. (2002): Credit risk: Modeling, valuation and hedging. Springer.

- Black and Cox (1976) Black, F. and Cox, J. (1976): Some effects of bond indenture provisions. Journal of Finance 31, 351–367.

- Briys and de Varenne (1997) Briys, E. and de Varenne, F. (1997): Valuing risky fixed rate debt: An extension. Journal of Financial and Quantitative Analysis 32, 239–249.

- Brunnermeier (2009) Brunnermeier, M. (2009): Deciphering the liquidity and credit crunch 2007-08. Journal of Economic Perspectives 23, 77–100.

- Chen and Kou (2009) Chen, N. and Kou, S. (2009): Credit spread, implied volatility, and optimal capital structures with jump risk and endogenous defaults, Mathematical Finance, 19, 343–378.

- Cheng and Milbradt (2012) Cheng, I. H. and Milbradt, K. (2012): The hazards of debt: Rollover freezes, incentives, and bailouts. Review of Financial Studies 25(4), 1070–1110.

- Crépy et al (2012) Crépey, S., Grbac, Z. and Nguyen, H.N. (2012): A multiple-curve HJM model of interbank risk. Mathematics and Financial Economics 6(3) 155-190.

- Diamond and Dybvig (1983) Diamond, D. and Dybvig, P. (1983): Bank runs, deposit insurance and liquidity. Journal of Political Economy 91, 401–419.

- Ericsson and Renault (2006) Ericsson, J. and Renault, O. (2006): Liquidity and credit risk. Journal of Finance 61, 2219–2250.

- Goldstein and Pauzner (2005) Goldstein, I. and Pauzner, A. (2005): Demand-deposit contracts and the probability of bank runs. Journal of Finance 60, 1293-1327.

- He and Xiong (2012a) He, Z. and Xiong, W. (2012): Rollover risk and credit risk. Journal of Finance 67, 391–429.

- He and Xiong (2012b) He, Z. and Xiong, W.(2012): Dynamic debt runs. Review of Financial Studies 25 (6), 1799–1843.

- Hilberink and Rogers (2002) Hilberink, B. and Rogers, L.C.G. (2002): Optimal capital structure and endogenous default. Finance and Stochastics 6, 237–263.

- Krylov (2008) Krylov, N.V. (2008): Controlled diffusion processes. Springer, 2nd printing edition.

- Leland (1994) Leland, H.E. (1994): Corporate debt value, bond covenants, and optimal capital structure. Journal of Finance 49, 1213–1252.

- Leland (1998) Leland, H.E. (1998): Agency costs, risk management, and capital structure. Journal of Finance 53, 1213–1243.

- Leland and Toft (1996) Leland, H.E. and Toft, K. (1996): Optimal capital structure, endogenous bankruptcy, and the term structure of credit spreads. Journal of Finance 51, 987–1019.

- Liang (2013) Liang, G. (2013): Stochastic control representations for penalized backward stochastic differential equations, Working paper.

- Liang and Jiang (2012) Liang, G. and Jiang, L. (2012): A modified structural model for credit risk. IMA Journal of Management Mathematics 23, 147–170.

- Liang et al. (2014) Liang, G., Lütkebohmert, E. and Xiao, Y. (2014): A multi-period bank run model for liquidity risk. Review of Finance 18(2), 803–842.

- Longstaff and Schwartz (1995) Longstaff, F. and Schwartz, E. (1995): A simple approach to valuing risky fixed and floating rate debt. Journal of Finance 50, 789-819.

- Merton (1974) Merton, R.C. (1974): On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance 29, 449–470.

- Morris and Shin (2010) Morris, S. and Shin, H.S. (2010): Illiquidity component of credit risk. Working Paper.

- Morris and Shin (2003) Morris, S. and Shin, H.S. (2003): Global Games: Theory and Applications. in Advances in Economics and Econometrics (Proceedings of the Eighth World Congress of the Econometric Society), edited by M. Dewatripont, L. Hansen and S. Turnovsky, Cambridge University Press.

The figure shows three simulated asset value paths in the model with a discrete tenor structure, where volatility , expected return rate , market interest rate , short-term rate , and long-term rate . The initial values of short- and long-term debt are set to and , respectively. The safety covenant parameter , the bankruptcy cost parameter , and the fire-sale rate is set to . The time horizon is years. In this discrete tenor structure setting the number of rollover dates is set to . The dotted line describes the debt run barrier, the dashed line the illiquidity barrier, and the solid line the insolvency barrier.

The figure shows three simulated asset value paths in the model with a staggered tenor structure where volatility , expected return rate , market interest rate , short-term rate , and long-term rate . The initial values of short- and long-term debt are set to and , respectively. The safety covenant parameter , the bankruptcy cost parameter , and the fire-sale rate is set to . The time horizon is years. In this staggered tenor structure setting the intensity of the Cox process is chosen to be . The dotted line describes the debt run barrier, the dashed line the illiquidity barrier, and the solid line the insolvency barrier.

The figure shows debt run barriers with different assumptions on the random variable , the creditor’s belief on the proportion of short-term creditors not rolling over their funding at each rollover date. The top line corresponds to the uniformly distributed , and from the second top to the bottom lines, they correspond to the truncated normal distribution with mean and diminishing variances. Other parameters are the same as in Figure 4.

The figure shows the default probabilies under the discrete tenor structure and the staggered tenor structure. The dotted line is the default probability without including rollover risk. Other parameters are the same as in Figure 3 and Figure 4 apart from and and with volatility and intensity as specified below the graphs.

The figure shows the default probabilies for different fire-sale rates. Other parameters are the same as in Figure 3 and Figure 4 apart from and and with volatility and intensity as specified below the graphs.

The figure shows the representative creditor’s value function at time for increasing initial asset value in the discrete tenor structure model with rollover dates and for the staggered tenor structure model for different intensities of the Cox process. Other parameters are the same as in Figure 4.

The figure shows the debt run barrier depending on time for different rollover frequencies in the discrete tenor structure model and for different intensities of the Cox process in the staggered tenor structure model. Other parameters are the same as in Figure 4.