First-passage and escape problems in the Feller process

Abstract

The Feller process is an one-dimensional diffusion process with linear drift and state-dependent diffusion coefficient vanishing at the origin. The process is positive definite and it is this property along with its linear character that have made Feller process a convenient candidate for the modeling of a number of phenomena ranging from single neuron firing to volatility of financial assets. While general properties of the process are well known since long, less known are properties related to level crossing such as the first-passage and the escape problems. In this work we thoroughly address these questions.

pacs:

89.65.Gh, 02.50.Ey, 05.40.Jc, 05.45.TpI Introduction

Diffusion processes are Markovian random processes with continuous sample paths. From a mathematical point of view they are characterized, in one dimension, by two functions: the drift, , and a positive defined diffusion coefficient . The sample paths of any diffusion process can thus be pictured as the continuous trajectory resulting from the superposition of a deterministic evolution, governed by , and fluctuations around it, the latter determined by . Denoting the process by , the diffusion picture becomes apparent by the fact that the time evolution of is ruled by the stochastic differential equation

where is the Wiener process, that is, a Gaussian process with zero mean, unit variance and correlation function . In what follows all stochastic differentials are interpreted in the sense of Ito.

The Feller process is a special kind of diffusion process with linear drift and linear diffusion coefficient vanishing at the origin feller1 . The time evolution of the process is thus governed by

| (1) |

where , and are constant parameters.

Both Feller and Orstein-Uhlenbeck processes (diffusion processes also with linear drift but constant diffusion coefficient) have been widely used, with a marked prominence of the latter, in the modeling of countless physical phenomena. Both share a linear drift, , which for results in a restoring force that, in the absence of noise, makes both processes decay toward the value .

However, and contrary to the Ornstein-Uhlenbek process where diffusion is constant, the Feller process has a state-dependent diffusion coefficient, , which for large values of enhances the effects of noise while as goes to zero the effect of noise vanishes. Hence, when the process reaches the origin, the drift drags it toward the value . If the process, starting at some positive value, cannot reach the negative region which, in turn, renders the process always non-negative (otherwise the noise term in Eq. (1) would become imaginary). Therefore, for the Feller process the origin is a singular boundary that the process cannot cross.

A related question is whether or not the origin is accessible, in other words, whether the value can or cannot be attained by the process. This is a crucial question in many practical situations and, as we will prove later, the answer depends on the particular value taken by a parameter which balances the values of and . The problem of classifying the different types of boundaries appearing in diffusion processes was thoroughly studied by Feller himself during the 1950’s and we refer the reader to the literature for a more complete account on the subject feller2 ; feller3 ; gardiner .

Possessing a state-dependent diffusion and, most importantly, the fact that the process never attains negative values have made Feller process and ideal candidate for modeling a number of phenomena in natural and social sciences. Theoretical biology was one of the first places where the process was, during 1970’s, seriously considered ricciardibook . Perhaps the most prominent place is within the context of neurobiology in order to model firing of single neurons ricciardi ; gerstner ; lanska ; lansky1995 . The Feller neuronal model is one of the so-called stochastic integrate and fire models which are simple models aiming to reproduce the membrane potential fluctuations. Experimental progresses has lead to the possibility of fitting real data to the Feller neuronal model among many others lansky ; ditlevsen ; bibbona ; jolivet ; tchumatchenko .

In a different context Capocelli and Ricciardi capocelli considered the possibility of modeling biological population with the Feller process in order to include environmental randomness to the classic Malthusian growth rate murray . The approach capocelli ; azaele ; azaelenature represents in fact an alternative to the Lotka-Volterra models in ecosystems and the interest in this sort of problems is mostly focused on the extinction –that is, on the possibility of attaining the singular boundary – and also on the unrestricted growth azaele ; azaelenature .

Financial markets is another field where the Feller process is widely used. It was introduced in 1985 to model term structure of interest rates receiving the name of Cox, Ingersoll, Ross (CIR) model and successfully evaluate bond prices cox ; hull . The process is also being considered to provide a random character to the volatility of a given stock. Volatility obeying the Feller model jointly with a log-Brownian stochastic dynamics for the asset price evolution configure a two-dimensional diffusion market process called Heston model heston ; yakovenko which is a rather useful model specially for option pricing hull ; heston .

In all of the above mentioned situations susceptible to be modeled with a Feller process, the first-passage time events related, among others, to level-crossing and the triggering of a given signal are very significant phenomena for different reasons which depend on each context. This is for instance the case of the neuronal activity since a spike generation is due to the crossing of a threshold by the membrane potential signal. Additionally, population extinctions of any type or volatility bursts in financial markets are also important phenomena to model and study. First-passage time is, however, a difficult topic redner ; sokolov ; klafter ; shlesinger ; weiss . To our knowledge, for the Feller process this crucial facet has been scantily studied and only partially solved some years ago in the context of single neuron firing ricciardi ; lanska . It is our main objective to address the first-passage time properties of process (1).

This paper is organized as follows. In Section II, we introduce the general properties of the unrestricted probability density of the Feller model. Section III is devoted to the derivation of the first-passage time and escape probabilities with special attention to a couple of specific situations. Section IV is mostly focused on the derivation of the mean first-passage time. We finally summarize the results obtained in Section V.

II General properties of the Feller model

Before addressing the main issue of this paper, let us briefly review the main traits of the process and the role of the boundary at the origin.

For the rest of the paper in turns out to be convenient to scale time and the process itself in the following way (recall we have assumed )

| (2) |

so that the Langevin equation (1) reads

| (3) |

where is the only free parameter left. Its relation to and is

| (4) |

This parameter is called “saturation level” or “normal level” and it is the value to which the Feller process is attracted to. As we will shortly see, has a key role in the behavior of the process.

Let be the probability density function (pdf) for process (3) to be in state at time :

This density satisfies the (forward) Fokker-Planck equation (FPE) (as long as there is no confusion we will drop the prime in the time variable)

| (5) |

with initial condition

| (6) |

Recall that is a singular boundary of the process and no “particle” can either leave or enter through this boundary (see Sect. I). A sufficient condition for this to happen is that the probability flux of the process through is zero gardiner . We will thus search for solutions of the initial-value problem (5)-(6) that meet such a condition, that is,

| (7) |

The expression for the pdf of the process was first obtained by Feller himself many years ago using a tortuous procedure which involved the solution of a rather clumsy integral equation feller1 . In the Appendix A we present a simpler and more direct derivation based on the Laplace transform of the problem (5)-(6). The final expression reads

| (8) |

where is a modified Bessel function defined as mos

| (9) |

From Eq. (8) we easily get the stationary pdf of the process defined as

Indeed, taking into account that (cf. Eq. (9))

| (10) |

and from Eq. (8) we obtain the Gamma distribution:

| (11) |

III First-passage and escape probabilities

After reviewing the main traits of the Feller process we will now focus on level-crossing problems –a collective name embracing questions such as hitting, first-passage, escape and extreme values, among others– for that process. According to whether we are dealing with one-sided or two-sided barrier problems, we separate level crossing into two different issues. In one of them, the hitting or first-passage problem, we deal with the time that the process reaches some “critical” value, or “threshold”, for the first time. The second issue, albeit closely related to the first one, concerns the time when the process first leaves a given interval. This is the so-called escape or exit problem.

III.1 First-passage probability

Let us first address the first-passage problem for the Feller process. The problem is solved when one knows the first-passage probability to threshold . Let us denote by the probability of first reaching when the process starts at from the value .

As is well known gardiner ; redner ; weiss the first-passage probability satisfies the backward Fokker-Planck equation

| (14) |

with initial condition

| (15) |

and boundary condition

| (16) |

The difficulty of solving the initial-boundary problem (14)-(16) is decreased by taking the time Laplace transform,

which reduces the original problem to the solution of an ordinary differential equation (the Kummer equation mos ):

| (17) |

with boundary condition

| (18) |

Since is a probability it is obvious that any solution of the problem must be finite and non negative for all .

The general solution of the Kummer equation (17) is mos

| (19) |

where and are arbitrary constants and and are the confluent hypergeometric functions of first and second kind mos respectively defined by

| (20) |

and

| (21) |

In order to proceed further we need to specify whether the initial value is above or below the threshold :

III.1.1 Initial value below threshold ()

In this case can be arbitrarily small and taking into account that (see Eqs. (20)–(21))

| (22) |

we see that the solution to the problem staying finite for any initial position between the origin and and for any positive value of the parameter is

The boundary condition (18) fixes the value of and

| (23) |

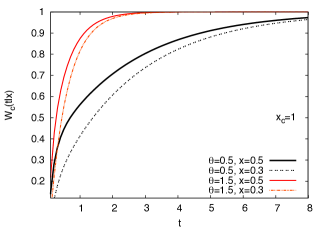

Figure 1 shows the numerical computation of this expression in the original Laplace space. We have used the well-known Stehfest algorithm stehfest and the results does not show any computational problem. As expected the closest to the threshold the fastest de first-passage time probability decays. And a greater , corresponds to a smaller as well.

III.1.2 Initial value above threshold ()

In such a case can be arbitrarily large. Hence, taking into account that

while stays finite for all positive values of mos , we see from Eq. (19) that the general solution of the problem which remains finite for all is

and from the boundary condition (18) we conclude

| (24) |

Numerical inversion of this result is again easy to compute with standard algorithms. The small difference lies on the fact that the hypergeometric function of second kind (21) is slightly more complicated than the hypergeometric function of first kind (20).

III.2 Reaching the origin

Another interesting quantity is the first-passage probability to threshold ; that is to say, the probability of first attaining the singular boundary of the process. This probability is relevant in the firing of neurons and it was addressed some years ago by by Capocelli and Ricciardi ricciardi (see also the work of Laska et al lanska ) . Let us denote by the first-passage probability to the origin. Since our process is always positive, , we must use Eq. (24) in order to evaluate . Setting in Eq. (24) and using Eq. (22) we obtain

| (25) |

We will now proceed to invert Eq. (25) thus obtaining the first-passage probability in real time, something that seem to be unfeasible for any value of the threshold , at least exactly (more on this below).

Using the property mos

we write for :

which, after using the following integral representation of the Kummer function mos

reads

Therefore,

where stands for Laplace inversion. Since roberts

| (26) |

where is the Heaviside step function, we have

Hence,

or, equivalently,

where is the incomplete gamma function mos

Finally,

| (27) |

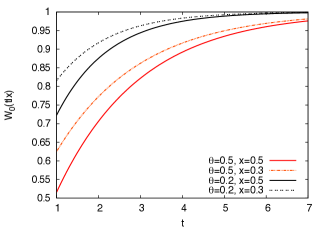

We remark (as shown already in Eq. (25)) that when the first-passage probability to the origin is zero in agreement with the fact, pointed out in Sect. II, that if is unattainable. The probability of first reaching the origin is represented in Fig. 2 where is shown as a function of time and for two different values of parameter model and initial value .

As and for the first-passage probability becomes equal to , as it is expected since if crossing the origin is a certain event as time grows. It is, however, interesting to see how approach the unity. To this end we use the following series expansion of the incomplete Gamma function mos

In the limit we then get

Therefore,

| (28) |

An interesting expression combining a power-law in and an exponential decay in time.

III.3 Large threshold

We will now study in some detail the interesting case of a large value of the threshold which is the opposite case considered above. It is clear that as the threshold becomes unreachable and the first-passage probability approaches zero. Let us see how is the limiting process. These results can be a really interesting for instance when one wants to control financial asset volatility. A large volatility corresponds to wild fluctuations in the asset price.

In the case under consideration the initial position is always below threshold and the starting point of the analysis must be Eq. (23):

Since now we use the following asymptotic expansion of the Kummer function mos

and

Our next step is the use of the following integral representation of mos

where is the following hypergeometric series mos

| (29) |

Hence, for large values of the threshold, we approximately have

We now proceed as in Sec. III.2. The Laplace inversion of the last equation reads

Since

then, recalling Eq. (26), we have

Therefore,

| (30) |

Using Eq. (29) we can give an alternative expression to Eq. (30) which is somewhat more convenient for numerical work. It reads

| (31) |

where is the incomplete Gamma function. This expression is particularly suited for small values of the initial position. Thus, for instance, when we write

| (32) |

where

is the exponential integral.

III.4 The escape probability

We close this section by briefly addressing the escape problem which, as mentioned before, is closely related with the first-passage problem studied above. The problem at hand consists in knowing whether or not the process , starting at some point inside an interval , has left this interval for the first time. The answer lies in the knowledge of the survival probability defined as the probability that, starting at , the process at time has not left the interval at that time or during any previous instant of time:

where is the starting point. The escape probability, i.e., the probability that at time the process has exited the interval for the first time, is then given by

As is well known gardiner ; redner ; weiss the survival probability obeys the backward Fokker-Planck equation

with initial and boundary conditions given by

Hence, the escape probability is the solution of the initial and boundary value problem (compare with Eqs. (14)–(16))

| (33) |

| (34) |

Following the same reasoning as before (see Eqs. (17) and (18)) we see that the time Laplace transform of the escape probability satisfies the boundary value problem

| (35) |

| (36) |

Again, The general solution of the Kummer equation (35) is mos

where and are arbitrary constants and and are defined in Eqs. (20) and (21).

Boundary conditions (36) determine the value of and and, after routine algebra, the final result for the escape probability reads

| (37) |

.

IV Long-time asymptotic behavior and mean first-passage times

In the previous section we have solved the hitting and escape problems for the Feller process by means of the evaluation of the first-passage and exit probabilities. We have obtained exact analytical expressions for the time-Laplace transform of these probabilities. Unfortunately exact inversion seems to be beyond reach except for the cases in Sec. III.2–when the threshold is located at the origin– and in the following Sec. IV.1 –with approximate expressions suitable for long times. In this section we will also obtain two important magnitudes associated with the problem: the mean first-passage time, , and the mean escape time, .

IV.1 Long-time behavior of the first-passage probability

Let be the first-passage time for the process, starting at , to reach some threshold for the first time. It is a random variable depending on each realization of the process. Formally

when the initial value is below threshold, and

when the initial value is above threshold.

We next relate the first-passage time with the hitting probability defined in the previous section. Note that if is the first-passage time, the hitting probability can be defined as

which shows that is the distribution function of the first-passage time. The corresponding probability density is thus defined

and it is related to the distribution by

| (38) |

The moments of this distribution are

and the mean first-passage time (MFPT) is the first moment:

Note that in terms of the Laplace transform

the first-passage moments are

which implies that, as long as () exist, the Laplace transform of the first-passage time density has the following expansion in powers of

| (39) |

On the other hand the Laplace transform of Eq. (38), along with the initial condition , yields

| (40) |

By combining Eqs. (39) and (40) we then have

| (41) |

expansion that furnishes the basis for the asymptotic analysis of the first-passage probability . Indeed, the so-called Tauberian theorems prove that the long-time behavior of a function is determined by the small behavior of its Laplace transform tauberian . For the case of the first-passage probability we see from Eq. (41) that the small behavior of is

| (42) |

where is the mean first-passage time. Note that expansion (42) may also be written, within the same level of approximation, as

| (43) |

which by the Tauberian theorems tauberian implies that the long-time behavior of the first-passage probability is given by the Laplace inversion of Eq. (43). That is,

| (44) |

We have thus obtained the long-time behavior of the first-passage probability to threshold and see that the MFPT determines the long-time behavior of the first-passage probability. We will next evaluate this average time for the Feller process.

IV.2 The mean first-passage time

In terms of the Laplace transform of first-passage probability obtaining the MFPT is straightforward. In effect from Eq. (42) we see that

| (45) |

Using the findings of Sec. III we know that the first-passage probability has different expressions as to whether the initial value of the process is above or below the threshold . Let us now treat these two cases including the special case .

IV.2.1 Initial value above threshold ()

In this case (cf Eq. (24))

and

| (46) |

The expansion in powers of of the Kummer function is presented in Appendix B where it is shown that

| (47) |

where

| (48) |

and is the psi function. We note that the function, defined as the indefinite integral:

cannot be reduced to another Kummer function mos nor, to the best of our knowledge, to any other tabulated function.

IV.2.2 MFPT to the origin

In Sects. II and III (see Eq. (25)) we have seen that when the origin is unattainable. However, if this singular boundary can be reached by the process. In this later case it is natural to ask which is the MFPT to the origin. The question has not only an academic interest but is relevant in mathematical biology where corresponds to the potential at which a neuron is fired ricciardi . Also in econophysics it is useful to know whether volatility or the interest rates can drop to zero and which is the average time expected to do so.

Since , the expression for the MFPT to the origin, denoted by , will be given by Eq. (49) with . Unfortunately setting in Eq. (49) is not possible because the integral is singular at the lower level.

We proceed as follows: start with the definition of the Kummer function given in Eq. (21), use the integration rule mos

and take into account the standard property of the Gamma function . We write

| (50) |

Substituting into Eq. (49) and taking the limit , we have

Using the value of the Kummer function at the origin, (cf Eq. (20)), we have

| (51) | |||||

Hence, if we get

and taking into account Eq. (50) we see that in this case the expression for the MFPT to the origin is given by Eq. (49) with :

| (52) |

However, we see from Eq. (51) that when as and the process takes an infinite average time to reach the origin

| (53) |

which confirms that when the singular boundary is unattainable.

IV.2.3 Initial value below threshold ()

Now (see Eq. (23))

Hence,

| (54) |

In the Appendix B we show that the expansion of powers of of the Kummer function is

| (55) |

where

| (56) |

Substituting Eqs. (55)-(56) into Eq. (54) yields

| (57) |

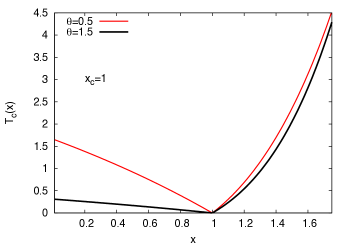

A result we obtained few years ago mp07 in another context and using a different approach. This result that applies for jointly with previous Eq. (49) that applies for are presented in Fig. 3. We show there the marked asymmetric behavior of the MFPT depending on whether the initial value is larger or smaller than the critical value

IV.3 The mean escape time

We close this section by obtaining the time taken by the process starting at to first leave a given interval , where . This is called the escape (or exit) time out of an interval, , and is formally defines as

The exit time is a random variable characterized by a distribution function,

which is precisely the escape probability discussed in Sec. III. The moments of the exit time are thus defined by

() and the mean escape time (MET) is the first moment:

Proceeding as in Sec. IV.1 we easily see that the Laplace transform of the escape probability can be written as (cf Eq. (41))

from which it follows that (cf Eq. (45))

| (58) |

Moreover, similarly to the first-passage problem discussed above, we can easily prove that the long-time behavior of the escape probability is also solely determined by the MET (see Eq. (44)):

| (59) |

Plugging the expression for given by Eq. (37) into Eq. (58) and taking into account the small development of the Kummer functions and , as expressed respectively by Eqs. (47)-(48) and Eqs. (55)-(56) we obtain after lengthy but otherwise straightforward algebra the following expression of the MET:

| (60) |

where

| (61) | |||||

and

| (62) |

V Summary and Conclusions

We have fully addressed the first-passage and escape problems for the Feller process. Let us now summarize the main results obtained. The process is an one-dimensional diffusion defined by a linear drift and a linear diffusion coefficient vanishing at the origin. Feller process has the property of being positive, a salient characteristic which has earned the process some popularity in modeling several phenomena, from neural activity to financial markets.

Perhaps the best way to define the process is by means of a stochastic differential equation. In the dimensionless units defined in Eq. (2) of Sec. II this reads

(we have dropped the prime in the time variable) where is the Wiener process and is the saturation or normal level to which is attracted to as increases. The origin is a singular boundary because the noise term vanishes there. In Sec. II we have reviewed the general properties of the processes which were mostly obtained by Feller many years ago. One of these properties refer to the attainability of the origin in which the normal level plays a crucial role. Thus if the origin is an accessible boundary while if it is not.

The bulk of the paper is developed in Secs. III and IV where the first-passage and escape properties of the Feller process are thoroughly analyzed. The first-passage problem refers to the crossing by the process of certain preassigned critical level or threshold while the escape problem refers to the departure of some interval .

The first-passage properties are fully characterized by the hitting, or first-passage probability, defined as the probability of first reaching the threshold by the process at time or before. We denote by this probability, where is the initial position of the process. This probability depends on whether the process is initially below () or above () threshold. We have obtained exact expressions for the Laplace transform of the hitting probability,

which are summarized as

where and are Kummer functions.

In general these expressions for the Laplace transform of the hitting probability cannot be inverted exactly in an analytical fashion and one has to resort to the numerical inversion. There are some instances, however, in which we have been able to obtain analytical expressions in real time. This is the case of hitting the origin which has a significant interest in the firing of neurons and also in the Heston volatility model of the financial analysis. We denote by the first-passage probability to threshold , we have shown that

where is the incomplete gamma function. If as . This the expected behavior since when crossing the origin is a sure event as time grows. The way approaches unity is explicitly given by the following combination of a power-law in the initial position and an exponential time decay

Another instance in which we have been able to obtain an (approximate) expression for the first-passage probability in real time is when threshold is large. In such a case

where is the incomplete Gamma function.

The escape problem is completely characterized by the escape probability, , defined as the probability of first leaving a given interval . It is complementary to the survival probability :

where is the probability that the process has not exited at time or during any previous instant of time. Formally,

For the Feller process we have been able to obtain the exact expression for the Laplace transform of the escape probability which turns out to be more involved than the first-passage probability. It reads

where , and and are Kummer functions.

We have next addressed the problem of the mean-first passage time (MFPT) and the mean exit time (MET). We have shown that in terms of the first-passage time moments () –of which the MFPT corresponds to , )– the Laplace transform of the hitting probability reads

The MFPT to the threshold is then given by

From these expressions we have been able to obtain, in terms of the MFPT, the following long-time asymptotic expression of the hitting probability

For the Feller process this analysis has led to different results according to whether initially the system is placed below or above the threshold:

The MFPT to reach the origin, , has also been analyzed with the result

which constitute an additional proof of the fact that when the singular boundary is unattainable.

The analysis of the MFPT can be exactly carried out for the MET. The resulting expressions relating the MET with the escape probability are formally the same as those relating the MFPT with the hitting probability as can be seen in Sec. IV.3. Thus, for instance,

and

where and are the escape probability and the MET respectively. In the case of the Feller process the explicit expression for the MET is given in Eqs. (60)-(62).

Let us finally mention that the extension of the above results to the study of the extreme values attained by the process, such as the maximum and minimum values, as well as their application to financial time series –in particular the volatility– is under present research and we expect getting a number of results very soon.

Acknowledgements.

Partial financial support from the Ministerio de Ciencia e Innovación under Contract No. FIS 2009-09689 is acknowledged.Appendix A The probability density function

The solution to problem (5)-(6) is more conveniently addressed by its Laplace transform with respect to :

| (63) |

Taking into account condition (7), the transformed problem (5)-(6) reads

| (64) |

| (65) |

Equation (64) is a linear partial differential equation of first order whose solution can be obtained by the method of characteristics courant . In effect, let the function be defined by the characteristic of Eq. (64), , that is

| (66) |

Then the solution of Eq. (64), as can be rightly seen by direct substitution, is courant

| (67) |

where is an arbitrary function to be determined by the initial condition (65), i.e.,

which implies, after inverting Eq. (66) to write in terms of , that

Substituting this into Eq. (67) we finally obtain

| (68) |

Let us now proceed to the Laplace inversion of Eq. (68). Calling

| (69) |

simple algebraic manipulations followed by a power expansion yield

Plugging into Eq. (68) we get

| (70) |

Let us denote by the operation of Laplace inverting and recall the standard property

and also

Then the Laplace inversion of Eq. (70) yields

which after simple manipulations reads

Appendix B Expansions for and

In terms of the Pochhammer’s symbol Kummer function is defined as the series mos

Since and

we have

| (71) |

In the sum of the right hand side we make the replacement and take into account that , we thus write

We can easily see that , hence

which, after recalling the definition of the confluent hypergeometric function , Eq. (20), yields

Substituting into Eq. (71) we get

| (72) |

where

| (73) |

The small expansion of the Kummer function of second kind is a bit more involved. We start from the definition of in terms of (cf Eq. (21))

| (74) |

then expand

| (75) | |||||

where is the psi function mos . Also abramovich

| (76) |

where is Euler’s constant. Plugging Eqs. (72), (75) and (76) into Eq. (74) we get

| (77) |

where

| (78) |

Let us finally show that a more convenient form for is given by

| (79) |

In effect, recalling the definition of given in Eq. (73) and using the integration rule , we have

where we have used the well known property to write and . Note that the integrand is precisely the Kummer function of second kind

(see Eq. (74) with and replaced by ). We have thus proved Eq. (79).

References

- (1) W. Feller, Two singular diffusion problems, Ann. Math. 54, 173-182 (1951).

- (2) W. Feller, The parabolic differential equations and the associated semi-group transformations, Ann. Math. 55, 468-519 (1952).

- (3) W. Feller, Diffusion processes in one dimension, Trans. Am. Math. Soc. 71, 1–31 (1954).

- (4) C.W. Gardiner, Handbook of Stochastic Methods (Springer-Verlag, Berlin, 1985).

- (5) L.M. Ricciardi, Diffusion Processes and Related Topics in Biology, (Springer-Verlag, Berlin, 1977).

- (6) R.M. Capocelli and L.M. Ricciardi, A Continuous Markovian Model for Neural Activity, J. Theor. Biol. 40, 369–387 (1973).

- (7) W. Gerstner and W.M. Kistler, Spiking Neuron Models (Cambridge University Press, Cambridge, 2002).

- (8) V. Lanska, P. Lansky, C.E. Smith, Synaptic transmission in a diffusion model for neural activity, J. Theor. Biol. 166, 393–406 (1994).

- (9) P. Lansky, L. Sacerdote, F. Tomassetti, On the comparison of Feller and Ornstein-Uhlenbeck models for neural activity, Biol. Cybern. 73, 457–465 (1995).

- (10) S. Ditlevsen, Estimation of the input parameters in the Feller neuronal model, Pys. Rev. E 73, 061910 (2006).

- (11) P. Lansky and S. Ditlevsen, A review of the methods for signal estimation in stochastic diffusion leaky integrate-and-fire neuronal models, Biol. Cybern. 99, 253–262 (2008).

- (12) E. Bibbona, P. Lansky, R. Sirovich, Estimating input parameters from intracellular recordings in the Feller neuronal model, Phys. Rev. E 81, 031916 (2010).

- (13) R. Jolivet, R. Kobayashi, A. Rauch, R. Naud, S. Shinomoto, W. Gerstner, A Benchmark test for a quantitative assessment of simple neuron models, J. Neurosci. Meth. 169, 417–424 (2008).

- (14) T. Tchumatchenko, A. Malyshev, Th. Geisel, M. Volgushev, and F. Wolf, Correlations and Synchrony in Threshold Neuron Models, Phys. Rev. Lett. 104, 058102 (2010).

- (15) R.M. Capocelli and L.M. Ricciardi, A Diffusion Model for Population Growth in Random Environment, Theoretical Population Biology 5, 28–41 (1974).

- (16) J.D. Murray, Mathematical Biology (Springer, Berlin, 2002).

- (17) S. Azaele, A. Maritan, E. Bertuzzo, I. Rodriguez-Iturbe, and A. Rinaldo, Stochastic dynamics of cholera epidemics, Phys. Rev. E 81, 051901 (2010).

- (18) S. Azaele, S. Pigolotti, J.R. Banavar, A. Maritan, Dynamical evolution of ecosystems, Nature 444, 926–928 (2006).

- (19) J.C. Cox, J.E. Ingersoll, S.A. Ross, A Theory of Term Structure of Interest Rates, Econometrica 53, 385–408 (1985).

- (20) J.C. Hull, Options, Futures and Other Derivatives (Prentice Hall, London, 2011).

- (21) S. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Review of Financial Studies 6, 327–343 (1993).

- (22) A. Dragulescu, V. Yakovenko, Probability distribution of returns in the Heston model with stochastic volatility, Quantitative Finance 2, 443–453 (2002).

- (23) S. Redner, A Guide to First-Passage Processes (Cambridge University Press, Cambridge, 2001).

- (24) T. Verechtchaguina, I.M. Sokolov, and L. Schimansky-Geier, First passage time densities in ressonant-and-fire models, Phys. Rev. E 73, 031108 (2006).

- (25) S. Condamin, O. Bénichou, V. Tejedor, R. Voituriez, J. Klafter, First-passage time in complex scale-invariant media, Nature 450 77–80 (2007).

- (26) M.F. Shlesinger, First Encounters, Nature 450 40–41 (2007).

- (27) G.H. Weiss, (2007) First Passage Time Problems in Chemical Physics, in Advances in Chemical Physics, Volume 13 (ed I. Prigogine) (J. Wiley, Hoboken, NJ, 2007). doi: 10.1002/9780470140154.ch1.

- (28) W. Magnus, F. Oberhettinger and R. P. Soni, Formulas and Theorems for the Special Functions of Mathematical Physics (Springer-Verlag, Berlin and New York, 1966).

- (29) H. Stehfest, Numerical inversion of Laplace transforms, Communications of the Association for Computing Machinery 13, 47 -49 (1970).

- (30) G. E. Roberts and H. Kaufman, Table of Laplace Transforms (W. B. Sauders, Philadelphia, 1966).

- (31) Handelsman, R. A., Lew, J. S., Asymptotic expansion of Laplace convolutions for large argument and tail densities for certain sums of random variables, SIAM Journal on Mathematical Analysis 5, 425-451 (1974).

- (32) J. Masoliver and J. Perelló, Extreme times for volatility processes, Phys. Rev. E 75, 046110 (2007).

- (33) F. Blake and W. Lindsay, Level-Crossing Problems for Random Processes, IEEEE Trans. Inf. Theor. IT-19, 295-315 (1973).

- (34) M. Abramowitz and I.A. Stegun Eds., Hanbook of Mathematical Functions (Dover, New York, 1972).

- (35) R. Courant and D. Hilbert, Methods of Mathematical Physics (Vol. 2) (J. Wiley-VCH, New York, 1989)