GARCH models are useful tools in the investigation of phenomena, where volatility changes are prominent features, like most financial data. The parameter estimation via quasi maximum likelihood (QMLE) and its properties are by now well understood. However, there is a gap between practical applications and the theory, as in reality there are usually not enough observations for the limit results to be valid approximations. We try to fill this gap by this paper, where the properties of a recent bootstrap methodology in the context of GARCH modeling are revealed. The results are promising as it turns out that this remarkably simple method has essentially the same limit distribution, as the original estimatorwith the advantage of easy confidence interval construction, as it is demonstrated in the paper.

The finite-sample properties of the suggested estimators are investigated through a simulation study, which ensures that the results are practically applicable for sample sizes as low as a thousand. On the other hand, the results are not 100% accurate until sample size reaches 100 thousands - but it is shown that this property is not a feature of our bootstrap procedure only, as it is shared by the

original QMLE, too.

Keywords: asymptotic distribution, bootstrap, confidence region, GARCH model, quasi maximum likelihood

László Varga

Department of Probability Theory and Statistics, Eötvös

Loránd University, Budapest, Hungary

E-mail: vargal4@math.elte.hu

András Zempléni

Department of Probability Theory and Statistics, Eötvös

Loránd University, Budapest, Hungary

E-mail: zempleni@math.elte.hu

1 Introduction

We investigate bootstrap estimation of the parameters of GARCH processes, which are

known to be able to capture the main stylized facts

of observed financial series. In these models, the conditional variance is

expressed as a linear function of the squared

past values of the series.

Definition 1

is called a GARCH(p,q) process if

(1)

(2)

where are

i.i.d. (0,1) random variables,

for and for .

It defines a stationary process for a well characterized parameter space,

its most important features are presented in Section 2.

The most important question in modeling is the parameter estimation. In case of GARCH models,

the QMLE estimation is the most popular one. This assumes Gaussian distribution

for the observations, providing reasonable approximations even in the case of

other distributions for the innovation . We conclude Section 2 with presenting

the properties of this estimator.

Of course, there are other estimation methods considered in the literature. The oldest and numerically simplest estimation method for GARCH models is the ordinary least squares (OLS). It performs poorer than the QML method and even for ARCH models the method requires moments of order 8 for the original process (Francq and Zakoian (2010), Chapter 6). An other well known method is the least absolute deviations (LAD) estimation, which outperforms the QML estimator if the innovations are Student’s distributed with 3 or 4 degrees of freedom (Peng and Yao (2003)).

Ling (2007) proposed a self-weighted QML estimator for the parameters which is close in some aspects to our considerations. There are also several extensions of these estimators, see Berkes and Horvath (2004) and Francq and Zakoian (2010), Chapter 9.

Section 3 deals with the main objective of this paper, namely the investigation of bootstrap methods.

Although there are different approaches

for bootstrapping the GARCH models, (these will be explained in more detail in Section 3) we suggest the

multiplier bootstrap approach recently proposed by Kojadinovic and Holmes (2011) for goodness of fit tests for copulas.

This is a simple generalization of the standard bootstrap procedure, where the

bootstrap sample is denoted by .

This method is usually called weighted bootstrap and was investigated as early as in the 1990s (Barbe and Bertail, 1995; Præstgaard and Wellner, 1993).

The bootstrap weights are supposed

to be independent from the process. We show the asymptotic normality of the

bootstrap estimators under conditions, which are fulfilled in the majority of

practical examples. The weighted bootstrap OLS and LAD estimators for AR(1) and ARCH processes were investigated by Bhattacharya and Bose (2012).

Other bootstrap methods for GARCH models proposed in the literature are the residual bootstrap (for instance, see Hall and Yao (2003)) and the block bootstrap (Corradi and Iglesias (2008)). These are tools for constructing confidence intervals for the parameters or for functionals of the parameters (Chen et al. (2011), Luger (2011), Pascual et al. (2006)) and for evolving goodness-of-fit tests (Luger (2011), Horvath et al. (2004)). Bootstrap methods are especially needed if the errors are heavy-tailed and this is the case in most financial applications.

Section 4 presents the results of a simulation study, where for simplicity we focus on ARCH(1) models. Here we also investigate the small-sample properties of the QMLE estimators, together with their bootstrap counterparts.

This approach is practical as both the similarities and differences can be demonstrated.

We give the conclusions in Section 5. The proofs can be found in the Appendix.

2 GARCH models

In this Section we summarize the needed fundamentals from the theory of GARCH processes (see Francq and Zakoian (2010) for example).

We denote the parameter vector by

which belongs to the parameter space .

The true value of the parameters,

is unknown.

Theorem 1

If there exists a GARCH(,) process (1) - (2),

which is second-order stationary, and if , then

(3)

If (3) holds, the unique strictly stationary solution of model (1) - (2) is a weak white

noise.

Definition 2

Let be a strictly stationary sequence of random matrices, and

E. The (top) Ljapunov exponent of the sequence is

The GARCH(,) process can be written in vector representation

where

,

, .

Theorem 2

Let denote the Ljapunov exponent of the matrix sequence . Then

The following theorem shows that the Ljapunov exponent – thus the strict stationarity – is in connection with the existence of moments of the GARCH process, which will be helpful to verify the main results.

Theorem 3

Let denote the Ljapunov exponent of the matrix sequence . Then

where is the strictly stationary solution of the GARCH(,) model.

From now on we will concentrate on the maximum likelihood estimation of the parameters. Assume that are observations from a GARCH(p,q) process

(strictly stationary solution of the model).

The Gaussian quasi-likelihood function, conditional on the

initial values, is

where the are recursively defined by the following equation:

The QMLE of is defined as the solution of

(4)

To maximize the Gaussian likelihood function, we have to minimize the following function:

Let and be the

generating functions

The following assumptions A1-A6 are sufficient for the quasi-maximum likelihood estimator to have a Normal limit

distribution (see Francq and Zakoian (2004)):

A1:

A2:

A3:

A4:

A5:

A6:

.

Theorem 4

Let be a sequence of QMLEs satisfying (4), with initial conditions

(5)

Under assumptions A1-A4

Theorem 5

Under assumptions A1-A6

(6)

where

(7)

With different assumptions, Theorem 4 was first proved by Berkes et al. (2003).

Theorem 5 was proved by Berkes et al. (2003) and by Hall and Yao (2003).

Hall and Yao (2003) also generalized the result to the case in which and the distribution of is in the domain of attraction of a Gaussian or stable law with exponent .

3 Bootstrap methods

3.1 Weighted bootstrap

We define the bootstrap weights as a triangular sequence of random variables

independent from the process:

To verify the main results, we need some natural assumptions B1-B6 for the bootstrap weights:

B1:

the weights are independent from the GARCH process

B2:

B3:

for all , the first four moments of , , are finite and equal

B4:

B5:

B6:

if .

The usual bootstrap procedure (corresponding to a multinomial distribution) provides a

suitable choice for weights, as it satisfies the six assumptions above.

This holds for the following weights as well (we shall use the first two in the paper):

Calculating the Gaussian likelihood function for the weighted sample, we get the following modified negative loglikelihood function, to be minimized:

For example if the weights are then the second element of the sample is taken twice but the third one is omitted etc.

The bootstrap QMLE of the parameter is defined as the solution of

(8)

Theorem 6

Let be a sequence of bootstrap QMLEs satisfying (8), with initial conditions (5). Under assumptions A1-A4 and B1-B4

Theorem 7

Under assumptions A1-A6 and B1-B6

(9)

where

The proofs of Theorems 6 and 7 can be found in the Appendix.

3.2 Residual bootstrap

A residual bootstrap method was proposed by Hall and Yao (2003), who also constructed one-sided bootstrap confidence intervals and analyzed its coverage percentages by simulations for stationary ARCH(2) and GARCH(1,1) processes.

The construction of the residual bootstrap sample consists of the following steps, which turns out to be useful if

the sample is in its stationary distribution and we apply a suitable burn-in period:

1.

Given a sample , compute the QMLE :

.

2.

Estimate the conditional variance of the process

.

3.

Estimate the residuals

.

4.

Calculate the standardized residuals

.

5.

Draw a bootstrap sample with replacement from the standardized residuals:

.

6.

Using and , let us compute the residual boostrap sample

of the process

By means of this residual bootstrap procedure, also confidence intervals for future values of the time series and for the volatilities can be constructed (Pascual et al., 2006).

4 Simulations

Although the GARCH(1,1) models perform usually better and surprisingly well against other, more sophisticated models (see Hansen and Lunde, 2005), for the sake of simplicity we decided to illustrate the main results for stationary ARCH(1) models (special case =0, =1 of Definition 1). So suppose that is generated by the ARCH(1) process

where are

i.i.d. (0,1) random variables, and , , are the true parameters.

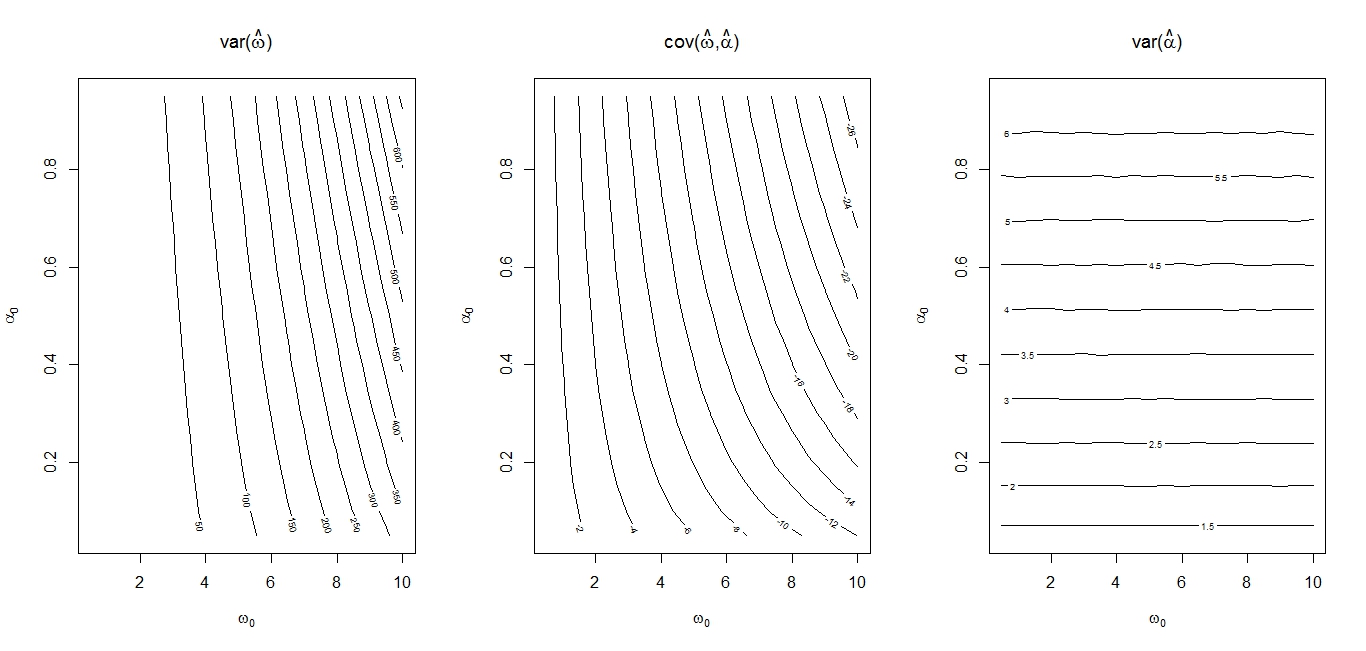

The covariance matrix of the limit distribution of the QMLE depends on the true parameters. We analyzed this dependence in stationary ARCH(1) processes, where the parameters are and .

The matrix itself can only be approximated via simulations derived from (7): for large and simulated data ,

Figure 1 displays the contours of the elements of the limiting covariance matrix if the innovations are Gaussian, based on simulations, which provides accurate results up to at least four digits. The variance of and the covariance between and are both more sensitive to changes in than in . The variance of the estimated parameter does not seem to depend on the true parameter value . This is not trivial from the theoretical results, as from (7) we get

which needs further investigation.

Figure 1: Contours of the elements of the limiting covariance matrix, ARCH(1) process

From now on we will concentrate on the ARCH(1) process with parameters and .

Then the limiting covariance matrix of the QML estimation is

(10)

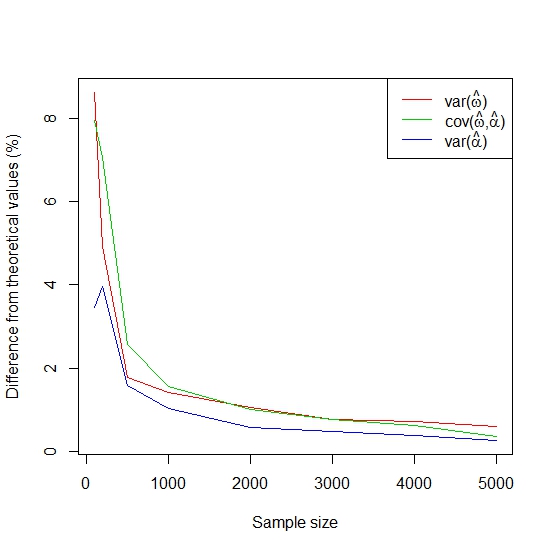

Unfortunately (minimum) replications are needed to confidently estimate the matrix, which

takes several hours for an i7 computer with 8 GB RAM memory. We will see that even the bootstrap can’t help much if we draw too few samples.

We drew samples with Gaussian innovations of size 100 to 5000 and calculated the covariance matrix of the QML estimations.

Figure 2 shows that the rate of convergence drastically improves until the sample size is under 1000 and just slightly after that.

We found also for other pairs of parameters that with simulations of sample size 2000, the covariance matrix can be estimated quite well, within a 1% margin.

Figure 2: Convergence of the sample covariance matrix, ARCH(1) process, and

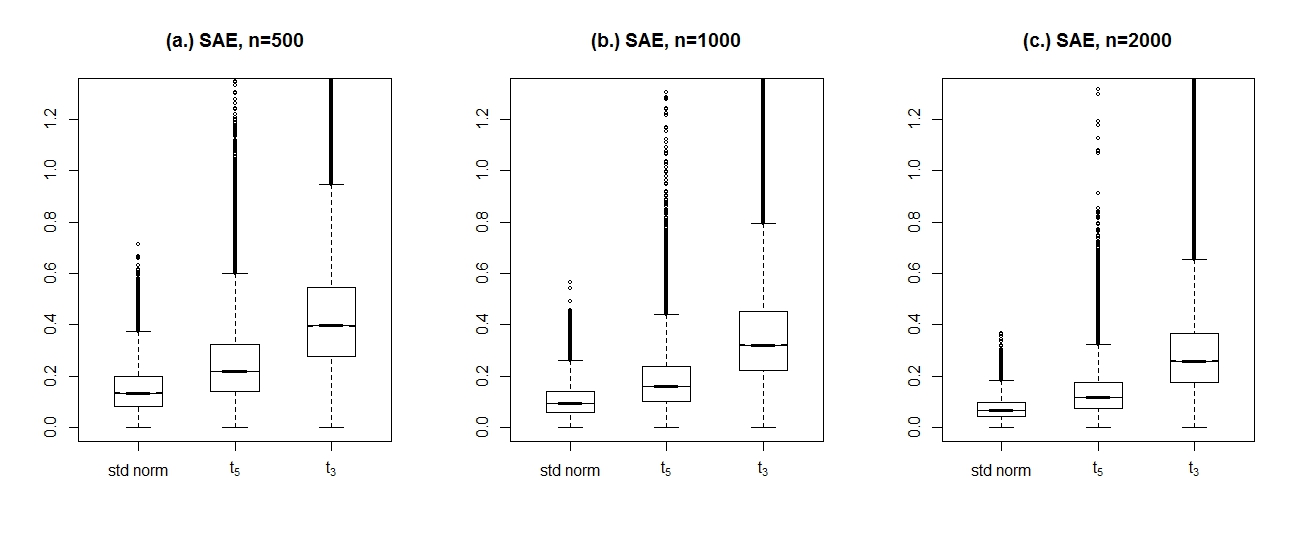

After that, 50000 samples of size n=500, 1000 and 2000 were generated with standard Gaussian and Student’s distributed innovations with 5 and 3 degrees of freedom, and we estimated the parameters with

the QML method, described in Section 2. Boxplots of the sum of absolute errors (SAE) are depicted in Figure 3. The SAE is defined as . We can see that the heavier tailes the innovations have, the larger the SAE is. Note that the Student’s errors with 3 degrees of freedom have infinite fourth moment – so Theorem 5 does not work –, but the quasi maximum likelihood estimates are fairly close on average to the original parameters. As the sample size increases, the SAEs of course become smaller. Figure 3 doesn’t display all SAE values for the Student’s innovations,

the results for some samples are so bad

that the SAE of the estimated parameters is more than 100.

Figure 3: Boxplots of the sum of absolute errors (SAE) of the parameters if the innovations are standard Gaussian, Student’s with 5 and 3 degrees of freedom for different sample sizes: (a.) n=500; (b.) n=1000; (c.) n=2000

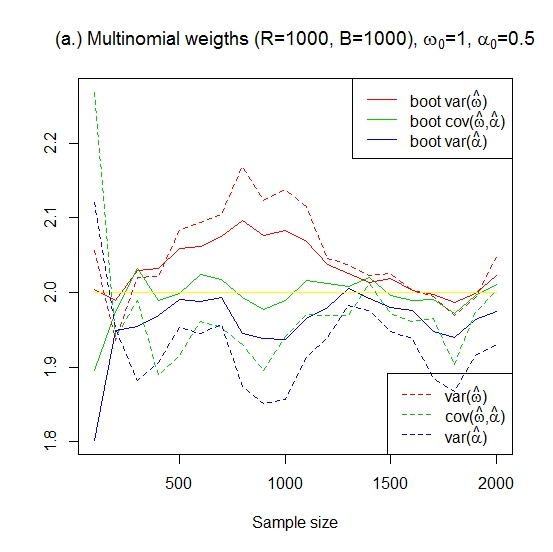

If we take multinomially distributed weights, then the scaling factor of the covariance matrix is , therefore the quotient of the two matrices by its elements must be near 2.

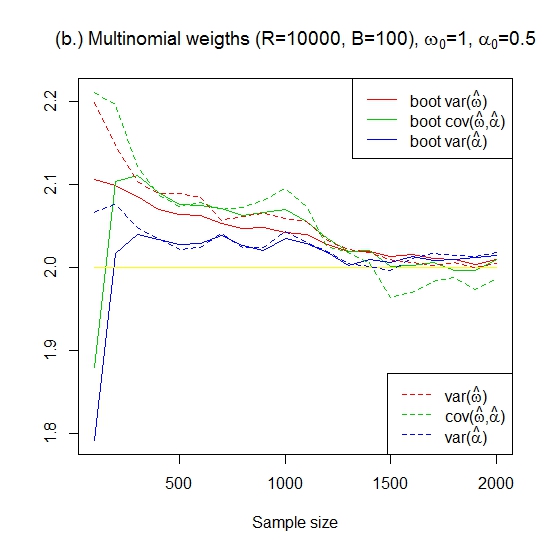

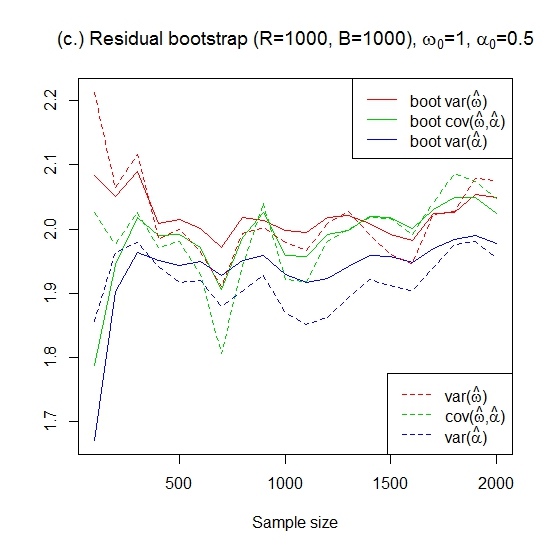

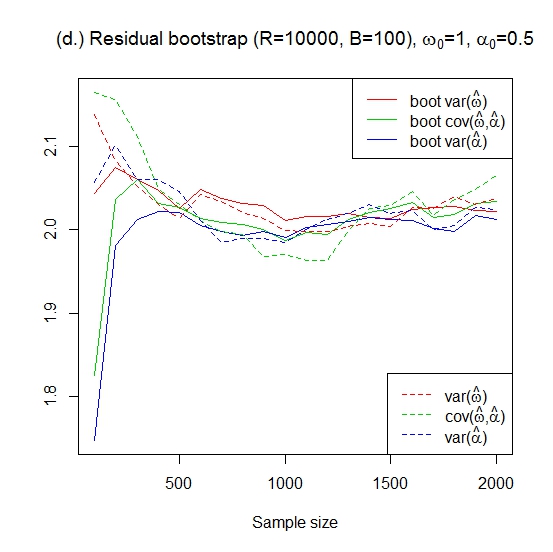

Figure 4 displays the convergence of the elements of the sample covariance matrix, divided element-wise by the theoretical covariance matrix (10), if the sample matrices are calculated with the multinomially weighted bootstrap (panels (a.) and (b.)) or with the residual bootstrap (panels (c.) and (d.)), for sample sizes ranging from 100 to 2000. Panel (a.) and (c.) show the convergence based on samples which were bootstrapped times, while the other two panels display simulations with and . The dashed lines are the sample covariance matrix values without bootstrap weights, divided by the theoretical values and scaled to 2.

Unfortunately in Theorem 5 there is not a swift convergence. In panel (a.) of Figure 4 we can’t see a straight convergence, the bootstrap can’t substantially improve the properties of the original samples, it only decreases the differences.

Panel (b.) of Figure 4 helps to understand the reason: the number of samples was too few. If we raise the number of samples to , and (for practical reasons)

decrease the bootstrap repetitions to , the convergence becomes quite good.

Looking at the simulations it is not obvious which of the two bootstrap methods is the better one.

Figure 4: Convergence of the sample covariance matrix, ARCH(1) process, and ; (a.) Weighted bootstrap with multinomial weights, =1000 and =1000; (b.) Weighted bootstrap with multinomial weights, =10000 and =100; (c.) Residual bootstrap, =1000 and =1000; (d.) Residual bootstrap, =10000 and =100

After that, we constructed 95% confidence intervals for the GARCH parameters with Gaussian innovations.

Table 1 contains the average coverage percentage of confidence intervals for the parameters and for different sample sizes (500, 1000, 2000) and using residual or weighted bootstrap methods, always compared to the Monte Carlo empirical confidence intervals.

For sample size of , the residual bootstrap outperformed the weighted bootstrap;

but for sample size 2000, the residual bootstrap performed mostly better then the residual bootstrap. Using the weighted bootstrap, the average coverage of the confidence intervals improved by increasing the sample size which can’t be stated in case of residual bootstrap.

Sample size

Method

Average coverage

Average coverage below

Average coverage above

Monte Carlo

95%

95%

2,5%

2,5%

2,5%

2,5%

500

RB

94.93

95.07

2.12

2.35

2.94

2.58

WB

94.19

94.23

2.66

2.29

3.15

3.47

1000

RB

95.47

95.52

2.61

1.99

1.92

2.49

WB

94.81

94.88

3.06

1.93

2.13

3.19

2000

RB

95.29

94.77

2.26

2.18

2.44

3.06

WB

94.74

95.07

2.62

2.21

2.64

2.72

Table 1: Average coverage

percentages of confidence intervals for the parameters and for sample sizes 500, 1000, 2000 and using residual bootstrap (RB) or weighted bootstrap (WB) methods.

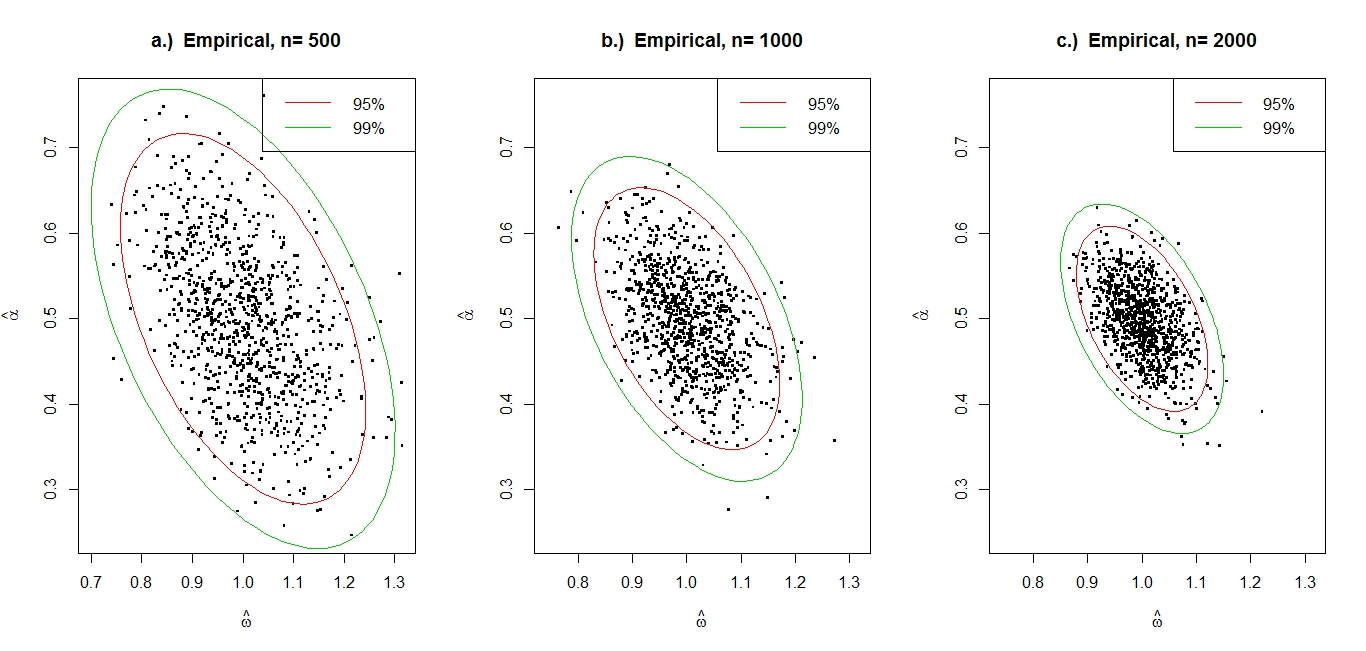

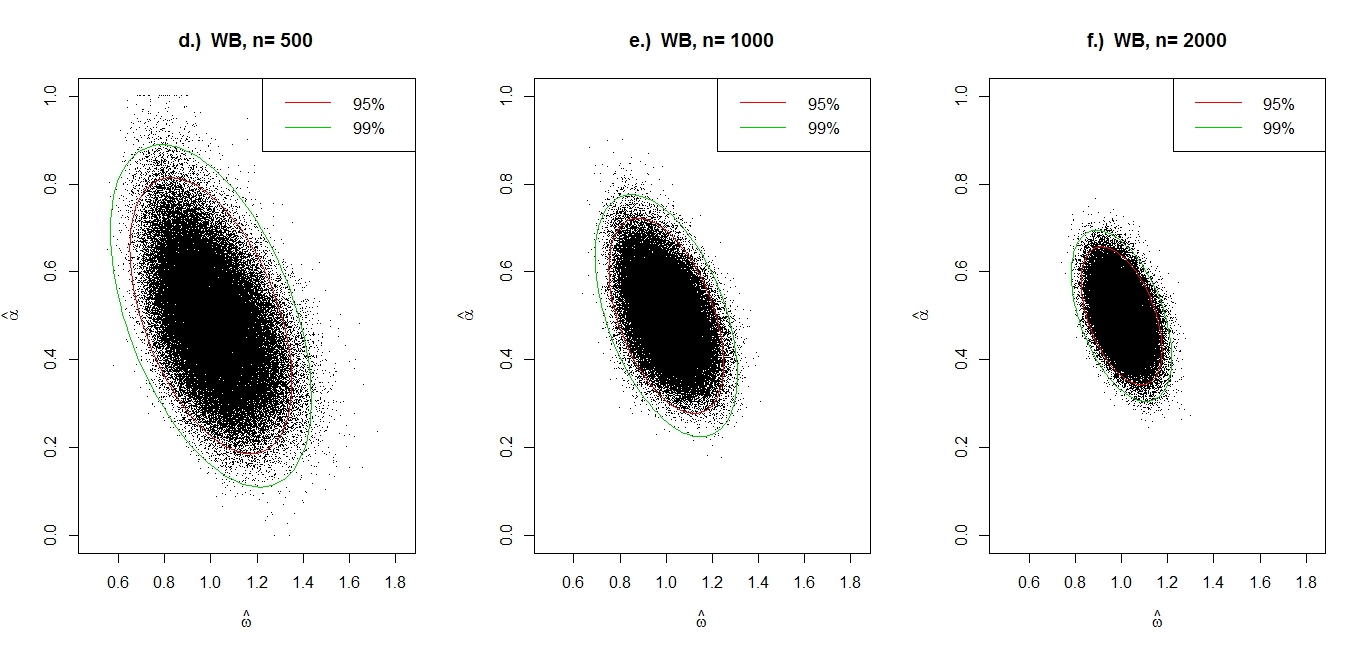

Using the limiting distributions (6) and (9) of the quasi-maximum likelihood estimator and its weighted bootstrap version, also confidence sets can be constructed. For the limiting distribution of the residual bootstrap QMLE, see Hall and Yao (2003). Table 2 reports the average coverage of the confidence sets, the row ’Empirical’ contains the 95% and 99% coverage of R=1000 samples, while the other two rows show the coverage of residual and weighted bootstrap QML estimates with samples and bootstrap replications. Note that in each case the weighted bootstrap QMLEs performed a bit better than the residual ones. Figure 5 represents the estimated pairs of parameters () and the 95% and 99% confidence sets – according to the limiting distribution – for different sample sizes (500, 1000, 2000). It can be seen that the confidence ellipses have a leaning longitudinal axis and the larger the sample size is, the smaller the ellipses become. The figures a.)–c.) were plotted

for samples and the figures d.)–f.) were plotted

for the weighted bootstrap QMLEs, bootstrapped times. Compared the points against the coverage sets, the coverage looks quite decent, and there are no clusters on the outside of the ellipses.

Method

95%

99%

95%

99%

95%

99%

Empirical

95.40

99.20

96.20

98.90

95.90

99.20

RB

95.84

99.12

95.97

99.19

96.02

99.24

WB

95.67

99.02

95.91

99.13

95.98

99.23

Table 2: Average coverage of the 95% and 99% confidence sets for sample sizes 500, 1000, 2000; using residual bootstrap (RB) or weighted bootstrap (WB) methods.

Figure 5: Pairs of estimated parameters () and the 95% and 99% confidence sets – according to the limiting distribution – for different sample sizes; empirical estimated parameters (a.), b.), c.)) and weighted bootstrap (WB) estimators (d.), e.), f.), ).

5 Conclusions

We have demonstrated that the multiplier bootstrap method reflects well the

properties of the original QMLE estimator, thus it may be used for investigating the

estimators in practical problems (we plan to come back to this issue in another paper soon).

Another important observation of our simulations is that the asymptotic results

presented in Sections 2 and 3 can be used for sample sizes

in the range of thousands only, as for smaller samples the deviations may still be

substantial.

It is also worth mentioning that we have found an interesting dependence between the

asymptotic covariance matrix and the parameter values themselves, which

should be taken into account in practical applications.

6 Acknowledgements

The work was supported by the European Union Social Fund (Grant Agreement No.TÁMOP

4.2.1/B-09/1/KMR-2010-0003).

7 Appendix

Proof of Theorem 6. We follow the proof of Francq and Zakoian (2004) and go into details only when changes are necessary. See the original proof in their

paper or in their book (Francq and Zakoian (2010)) on pages 156-159.

First, we introduce some notations to write the system of equations

in matrix form.

So we have

(11)

Let us denote by the open sphere with center and radius .

The proof consists of five steps and we also need a modification of the ergodic theorem.

(I.) The initial values are asymptotically irrelevant

(12)

Iterating (11), we get that for some appropriate and

In the estimation above we applied Markov’s inequality and Theorem 3.

Using the Borel-Cantelli lemma, we get

and

Finally, using Cesaro’s lemma, (14) and (15) are proved.

(II.) Identifiability of the parameter

For details, see Francq and Zakoian (2010), page 158.

(III.) The log likelihood function is integrable at and it has a unique minimum at the true value

It is easy to show that ,

because

The log likelihood function is integrable at :

The limit criterion is minimized at the true value

where the equality holds iff and as a consequence of

(II.), this is equivalent to

.

(IV.) For any , there exists a neighborhood such that

To prove this, we use (I.) and a consequence of the ergodic theorem.

In the last equation, we used that is an ergodic process.

The expression is monotonically increasing in , so is also monotonically increasing and using Beppo Levi’s theorem,

(V.) Last step of the proof, using the compactness of . For any neighborhood of ,

(16)

As is a compact set, by definition, there exist

open subsets of , for which

and

satisfy (IV.). So

As a consequence of (IV.) and (16), for large enough with probability 1.

This is true for any neighborhood , therefore

Proof of Theorem 7. We follow the proof of Francq and Zakoian (2004) and go into details only when changes are necessary. See the original proof in their

paper or in their book (Francq and Zakoian (2010)) on pages 159-168.

The Taylor-expansion of the function around is

where is between and .

Derivating, summarizing and multiplying this equation with , we get

where is between and .

We will show that

(17)

(18)

The proof consists of six steps.

(I.) Integrability of the second-order derivatives of at

As and is independent from , it is sufficient to show that

which is proven in Francq and Zakoian (2010), on pages 160-162.

(II.) J is invertible and The invertibility of is verified in Francq and Zakoian (2010), on page 163.

Using (I.), and the independence between and , we have

Then we obtain

(III.) Uniform integrability of the third-order derivatives of at : There exists a neighborhood of such that, for all ,

As and is independent from , it is sufficient to show that

which is proven in Francq and Zakoian (2010), on pages 163-165.

(IV.) The initial values are asymptotically irrelevant:

(19)

(20)

Using the results of Francq and Zakoian (2010) (pages 165-166) we have

So we obtain the estimate

Markov’s inequality, the independence between , and imply that, for

all ,

where .

To show (19), it is sufficient to prove that :

(V.) Using the martingale CLT (or Lindeberg’s CLT), we prove that

(21)

Let and

for all .

So for every , is a square integrable martingale difference.

Let us denote with , therefore the process

is stationary and ergodic.

As a consequence, using B6 for Bernstein’s theorem

We also have for all

At the second equality we used the stationarity of the process.

Using the martingale CLT on the process and then the

Cramér-Wold theorem, (21) is proved.

(VI.) Using the second order derivative of the Taylor expansion of , it can be seen that

At last, if we combine (IV.), (V.),(VI.) and apply Slutsky’s lemma on the first order derivative of

the Taylor expansion of , (7) is proved.

References

Barbe and Bertail (1995)

P. Barbe and P. Bertail.

The weighted bootstrap, volume 98.

Springer, 1995.

Berkes and Horvath (2004)

I. Berkes and L. Horvath.

The efficiency of the estimators of the parameters in GARCH

processes.

The Annals of Statistics, 32(2):633–655,

2004.

Berkes et al. (2003)

I. Berkes, P. Kokoszka, et al.

GARCH processes: structure and estimation.

Bernoulli, 9(2):201–227, 2003.

Bhattacharya and Bose (2012)

A. Bhattacharya and A. Bose.

Resampling in time series models.

Arxiv preprint arXiv:1201.1166, 2012.

Chen et al. (2011)

B. Chen, Y.R. Gel, N. Balakrishna, and B. Abraham.

Computationally efficient bootstrap prediction intervals for returns

and volatilities in ARCH and GARCH processes.

Journal of Forecasting, 30(1):51–71,

2011.

Corradi and Iglesias (2008)

V. Corradi and E.M. Iglesias.

Bootstrap refinements for QML estimators of the GARCH (1, 1)

parameters.

Journal of Econometrics, 144(2):500–510,

2008.

Francq and Zakoian (2004)

C. Francq and J.M. Zakoian.

Maximum likelihood estimation of pure GARCH and ARMA-GARCH

processes.

Bernoulli, 10(4):605–637, 2004.

Francq and Zakoian (2010)

C. Francq and J.M. Zakoian.

GARCH models: structure, statistical inference and financial

applications.

Wiley, 2010.

Hall and Yao (2003)

P. Hall and Q. Yao.

Inference in ARCH and GARCH models with heavy–tailed errors.

Econometrica, 71(1):285–317, 2003.

Hansen and Lunde (2005)

P.R. Hansen and A. Lunde.

A forecast comparison of volatility models: does anything beat a

GARCH (1, 1)?

Journal of applied econometrics, 20(7):873–889, 2005.

Horvath et al. (2004)

L. Horvath, P. Kokoszka, and G. Teyssiere.

Bootstrap misspecification tests for ARCH based on the empirical

process of squared residuals.

Journal of Statistical Computation and Simulation, 74(7):469–485, 2004.

Kojadinovic and Holmes (2011)

Yan J. Kojadinovic, I. and M. Holmes.

Fast large-sample goodness-of-fit tests for copulas.

Statistica Sinica, 21:841–871, 2011.

Ling (2007)

S. Ling.

Self-weighted and local quasi-maximum likelihood estimators for

ARMA-GARCH/IGARCH models.

Journal of Econometrics, 140(2):849–873,

2007.

Luger (2011)

R. Luger.

Finite-sample bootstrap inference in GARCH models with heavy-tailed

innovations.

Computational Statistics & Data Analysis, 2011.

Pascual et al. (2006)

L. Pascual, J. Romo, and E. Ruiz.

Bootstrap prediction for returns and volatilities in GARCH models.

Computational Statistics & Data Analysis, 50(9):2293–2312, 2006.

Peng and Yao (2003)

L. Peng and Q. Yao.

Least absolute deviations estimation for ARCH and GARCH models.

Biometrika, 90(4):967–975, 2003.

Præstgaard and Wellner (1993)

J. Præstgaard and J.A. Wellner.

Exchangeably weighted bootstraps of the general empirical process.

The Annals of Probability, 21(4):2053–2086, 1993.