Variance Swaps on Defaultable Assets and Market Implied Time-Changes

Abstract

We compute the value of a variance swap when the underlying is modeled as a Markov process time changed by a Lévy subordinator. In this framework, the underlying may exhibit jumps with a state-dependent Lévy measure, local stochastic volatility and have a local stochastic default intensity. Moreover, the Lévy subordinator that drives the underlying can be obtained directly by observing European call/put prices. To illustrate our general framework, we provide an explicit formula for the value of a variance swap when the underlying is modeled as (i) a Lévy subordinated geometric Brownian motion with default and (ii) a Lévy subordinated Jump-to-default CEV process (see Carr and Linetsky (2006)). In the latter example, we extend the results of Mendoza-Arriaga et al. (2010), by allowing for joint valuation of credit and equity derivatives as well as variance swaps.

1 Introduction

A variance swap (VS) is a forward contract written on the realized variance of an underlying . As is typical in derivatives literature, we define the realized variance over the interval as , the continuously sampled quadratic variation of the . Thus, at maturity the VS has a payoff (to the long side) of

| (1.1) |

The variance swap rate is determined at inception so that initial value of the VS is zero. Here, is the expectation under the risk-neutral pricing measure .

There are a number of reasons for which one may wish to enter into a VS agreement. First, a trader who delta-hedges a short position in a European option can limit his exposure to stochastic volatility risk by trading a VS (see, e.g., Carr and Schoutens (2008)). Second, a drop in the level of an underlying is often accompanied by an increase in the volatility of (the leverage effect). Thus, a long position in a VS serves as protection against a market crash. Such is the demand for VSs that, according to Jung (2006), the daily trading volume in equity index VSs reached 45 million USD vega notional in 2006 (vega measures the change in an option’s price caused by changes in volatility). On an annual basis, this corresponds to payments of more than 1 billion USD per percentage point of volatility (see Carr and Lee (2009)).

At the level of individual stocks there is yet another source for the leverage effect that is related to the default risk associated with the underlying firm. The credit-related leverage effect explains the interaction between market risk (return variance) and credit risk (default arrival). For instance, Cremers et al. (2008) show that CDS rates are correlated with both stock option implied volatility levels and the at-the-money slope of implied volatility. Similar results can be found in Consigli (2004). Carr and Wu (2010) study the interaction between the pricing of stock options and the pricing of credit default swaps. Specifically, they regress CDS spreads on stock option implied volatilities for four companies and find ’s ranging from 36-82%. More recently, Chang et al. (2012) verify not only that, on average, the returns in the CDS and stock markets are negatively correlated, but also that this correlation is higher (i.e., more negative) for high yield firms than it is for investment grade firms. This suggests that the credit-leverage effect is even stronger for companies with lower credit ratings. In summary, when the probability of default of a firm increases, its stock price tends to lose value while the option-implied volatility increases. In such a situation, it is common for investors to look for credit protection by taking long positions in deep out-of-the-money puts (see, e.g., Angelos (2009) and Carr and Wu (2010, 2011)). However, there is a side-effect in this hedging strategy. Though the investor’s objective is to minimize credit exposure, this strategy will increase his exposure to volatility due to the credit-equity leverage effect. This fact could also be seen from the turmoil experienced in the variance swap market when the stock market acutely dropped during the credit crisis of 2008-9 (see, e.g., Filipovic et al. (2013)). Hence, to summarize, in the pricing of variance swaps written on an individual stock, it is especially important to take into account default risk (and the credit-related leverage effect).

In his seminal paper, Neuberger (1990) showed that, when the underlying is modeled by a process with continuous sample paths, , (for simplicity, assume the risk-free rate of interest is zero) the fair value of is given by a European-style contract . Later, Carr and Madan (1998) showed that the contract (or in fact, any European-style derivative with a twice differentiable payoff) can be synthesized from a linear combination of calls and puts.111In fact, the replication result of Carr and Madan (1998) is independent of the continuity assumption of the price process. Thus, when -expiry calls and/or puts are available at every , the fair value of is uniquely determined by the implied volatility smile. Remarkably, this result is independent of any assumption about the volatility process . However, this result does rely on the continuity of sample paths of . The events of the recent (and ongoing) financial crisis underscore the need to include jumps in the underlying price process . The question naturally arises then: what is the fair value of when the price process is allowed to have discontinuous sample paths?

One possible answer to this question is given by Carr et al. (2012), who show that, when is modeled as a Lévy process time-changed by an absolutely continuous time-change, the fair value of is equal to a multiplier times the value of a log contract . Interestingly, the multiplier does not depend on the time-change process. While the value of does depend on the time-change through the contract, since the contract can be synthesized by a linear combination of calls, when one has full knowledge of the volatility smile, the value of can be determined in the framework of Carr et al. (2012) without any knowledge of the time-change process.

This last point cannot be emphasized enough. A parametric model for the time-change process would leave one open to model risk, as any misspecification of the time-change parameters would (in general) result in erroneous values of . By using knowledge of the volatility smile to construct the value of the contract, Carr et al. (2012) circumvent the need to parametrically model the time-change process. Thus, the risk of model misspecification is greatly reduced (though, some model risk still exists, since the multiplier depends on the choice of a specific Lévy process). An alternative and quite interesting approach to the joint pricing of volatility derivatives and index options in the presence of jumps is provided in Cont and Kokholm (2013).

In this paper, we consider the class of Lévy subordinated diffusion processes described in Mendoza-Arriaga et al. (2010). This class of models, like the class considered by Carr et al. (2012), allows for the underlying to experience both jumps and stochastic volatility. However, there are a few important differences between these two frameworks. In Carr et al. (2012), the background process is modeled as a Lévy process, which naturally includes the possibility of jumps, but does not include stochastic volatility. Stochastic volatility is added by time-changing the background process with a continuous increasing stochastic clock. In contrast, in Mendoza-Arriaga et al. (2010), the background process is modeled as a diffusion, which may include local stochastic volatility, but does not include jumps. Jumps are added by time-changing the background process with a Lévy subordinator. Additionally, the framework of Mendoza-Arriaga et al. (2010) allows for the possibility of a default event, whereas the framework of Carr et al. (2012) does not. While default may not be realistic for an index, it is certainly an important consideration for individual stocks as explained above.222A default event would cause to blow up. As such, we must amend our definition of a VS to account for this possibility. We will do this in Section 4. Finally, in Carr et al. (2012), the ratio of to the value of the contract is a constant , which is independent of the initial value of the underlying . However, empirical results from Carr et al. (2012) indicate that this ratio is not constant. In the Lévy subordinated diffusion setting of our paper, the ratio can, in general, depend on the initial value of the underlying. The reason for this difference is that Lévy processes are spatially homogeneous, whereas diffusion processes may have locally-dependent drift and diffusion coefficients.

Despite the differences between these frameworks, they share one desirable feature: when the background process is fixed and one has full knowledge of the volatility smile, the fair value of is robust to misspecification of the time-change process. In Carr et al. (2012), the effect that the time-change has on the value of is felt through the contract, which is constructed directly from European calls. In the framework of Mendoza-Arriaga et al. (2010), we will show that the Lévy subordinator can be inferred directly from the volatility smile. Once the subordinator is obtained, it can be used to compute the fair value of (among other things).

The rest of this paper proceeds as follows. In Section 2 we describe the class of Lévy subordinated diffusion processes in detail. In Section 3 we introduce some mathematical tools, which we shall need to compute the price of a VS. In Section 4 we modify the payoff of a VS to account for the possibility that the underlying defaults (i.e., jumps to zero). We then derive a general expression for the value of the modified VS in the Lévy subordinated diffusion setting. In Section 5 we present some important results concerning generalized eigenfunction expansions. These results will be needed for the diffusion-specific VS computations provided in Section 6. In Section 7 we show that, by observing European call and put prices written on the underlying, one can uniquely determine (in a non-parametric way) the drift and Lévy measure of the subordinator that drives the underlying price process. In section 8 we implement the numerical methods developed in Sections 2-7. First, we extract the subordinator driving four different stocks by observing call and put prices. Then, we then use the extracted subordinator to compute VS rates. Finally, in Section 9, we provide some concluding remarks and discuss directions for future research.

2 Model

We assume frictionless markets, no arbitrage, and take an equivalent martingale measure (EMM) chosen by the market on a complete filtered probability space as given. All stochastic processes defined below live on this probability space, and all expectations are with respect to unless stated otherwise. As all of the processes considered below are Feller, the natural filtrations generated by these processes are right-continuous. We shall assume that all the (natural) filtrations defined throughout this Section are augmented to include the -null sets. In particular, this assumption holds for the subordinate filtration , which we describe at the end of this Section. For simplicity, we assume zero interest rates. All of our results can be easily extended to include deterministic interest rates.

As in Mendoza-Arriaga et al. (2010), we model the stock price dynamics under the risk-neutral pricing measure as a stochastic process defined by

| (2.1) |

Here, the background process is a scalar Feller diffusion, is a Lévy subordinator, is a scaling factor, which is needed to ensure that the asset price is a martingale, and is a positive random variable, which will be used to model a possible default event of the underlying . Below, we describe each of the above-mentioned elements in detail.

Background Feller process . We let be a time-homogeneous Markov diffusion process, starting from a positive value , which solves a stochastic differential equation (SDE) of the form

| (2.2) |

where

| and | (2.3) |

Here, and are the state-dependent instantaneous volatility and drift rate, is a constant, and is a standard Brownian motion. We assume that and are Lipschitz continuous on the interval for each (i.e., locally Lipschitz), and that and remain bounded as . We do not assume that and remain bounded as . Under these assumptions the process does not explode to infinity (i.e., infinity is a natural boundary for the diffusion process; see Borodin and Salminen (2002) p.14 for boundary classification of diffusion processes). We also assume that zero is either an (unattainable) natural boundary or an entrance boundary. If zero is a natural boundary the state space is given by . If zero is an entrance boundary, i.e., the process can be started at then it quickly moves to interior of to never hit zero again. Throughout this document we assume that the process always starts from a positive value , and hence the state space is also defined as . Under all our previous assumptions is the unique strong solution to the SDE (2.2). The transition function of the diffusion process started at defines a Feller semigroup acting on the space of functions continuous on and such that the limits and exist and are finite (Ethier and Kurtz (1986) p.366) by

| (2.4) |

The infinitesimal generator of is a second-order differential operator of the form

| (2.5) |

with the domain if zero is an inaccessible boundary (natural or entrance). We also note that the semigroup leaves the space of functions continuous on and having zero limits and invariant and is a Feller semigroup on it. Lastly, we denote by the completed natural filtration of the process .

The trigger event and the indicator process . Let be an exponential random variable, independent of , and define the trigger event time as

| (2.6) |

That is, is the first jump time of a doubly stochastic Poisson process with jump intensity given by the killing rate . Observe that the killing rate is added in the drift (2.3) to compensate for the killing (jump-to-default). This compensation will be needed in order to ensure that the stock price is a martingale. Moreover, since the process cannot reach zero from the interior of the state space, then the underlying stock price process cannot go to zero continuously, rather, it may only jump to zero from a strictly positive value. We denote by the Feynman-Kac semigroup associated with the killing rate :

| (2.7) |

is a (sub-Markovian) Feller semigroup on with the generator

| (2.8) |

with the domain . More precisely, . Since zero is an inaccessible boundary (natural or entrance) of the diffusion with killing at the rate it suffices to restrict the domain to whenever we start the process from the interior of , i.e., (cf. Borodin and Salminen (2002) pp.15ff).

Since the random variable is not -measurable, we introduce an indicator process in order to keep track of the event . The indicator process is defined by

| (2.9) |

Lastly, we denote by the (completed) natural filtration of the process .

The auxiliary bivariate process . As in Mendoza-Arriaga and Linetsky (2013) we define the auxiliary bivariate process with state space . The process is a Feller semimartingale in the enlarged filtration with ( is the smallest filtration that contains and in which is a stopping time). Moreover, any function is represented as,

| (2.10) |

As we shall see below, the function can be interpreted as a promised payoff function if the triggering event does not occur by time , while can be understood as a recovery payoff function if the triggering event occurs prior time .

The following theorem gives the Markovian characterization of the bivariate process .

Theorem 2.1.

(i) The bi-variate process is a Feller process with the Feller semigroup acting on according to:

| (2.11) |

where , is the Feller semigroup of the process (2.4) and is the corresponding Feynman-Kac semigroup (2.7).

(ii) The infinitesimal generator of the Feller semigroup is given by

| (2.12) |

| (2.13) |

where and are the generators of and , respectively.

(iii) If (i.e., is of the form (2.10) with ) and is the bi-variate process with and , then the process

| (2.14) |

is an -martingale.

Proof.

The proof can be found in Mendoza-Arriaga and Linetsky (2013). ∎

Similarly, the Doob-Meyer decomposition of is given in the following corollary.

Corollary 2.2.

The increasing process has the Doob-Meyer decomposition

| (2.15) |

with the predictable -compensator and -martingale

| (2.16) |

Proof.

The Lévy subordinator . A Lévy subordinator is a Lévy process with positive jumps and non-negative drift. For a standard reference on subordinators we refer the reader to Bertoin (2004). We require that be independent of and and satisfy . Every Lévy subordinator has the following Itô-Lévy decomposition

| (2.17) |

where is the drift of the subordinator and is a Poisson random measure with the property that, for any Borel set we have for some -finite measure on . The measure , which must satisfy , is referred to as the Lévy measure. The Laplace transform of a Lévy subordinator is given by

| (2.18) |

where is the transition function of the subordinator and is the Laplace exponent of , which can be computed explicitly from the Lévy-Kintchine formula

| (2.19) |

Note that the Laplace exponent is concave and increasing and satisfies (see Bertoin (1996), page 73). For any Borel set the process is a Poisson process with intensity . If the arrival rate of all jumps is finite then is a compound Poisson process. In this case, the distribution of jumps is . If then the subordinator is said to be an infinite activity subordinator.

We define the first passage process or right inverse process of as . Recall that is assumed to be independent of . Therefore, is independent of as well. We let be the natural filtration of the process .

The subordinate filtration , the auxiliary subordinate bivariate process , and the default time . Recall from our above discussion that , and correspond to the filtrations generated by the processes , , and , respectively, and that the filtration is the smallest filtration that contains and in which is an -stopping time. Similarly, we can define the filtration , with , to be the smallest filtration that contains and in which is an increasing family of -stopping times. Then the subordinate filtration is constructed by time-changing the filtration with the Lévy subordinator , i.e., . Observe that since is an -stopping time, then is the filtration containing all of the information of the bivariate process prior to the stopping time . Consequently, one can define the subordinate bivariate process by time-changing the bivariate process with the subordinator . This transformation is called Bochner’s subordination due to work on subordination of semigroups and their generators by Bochner (1949). The subordinate process is a Feller -semimartingale (see Mendoza-Arriaga and Linetsky (2013)).

From (2.9) we observe that, before subordination, the indicator process satisfies for all . On the other hand, after subordination, the subordinate indicator process satisfies for all for which (i.e., ). Therefore, in the credit-equity context one can define the default time by

| (2.20) |

Certainly, is the first passage time process of across the level and the identity holds (see Section 5.1.1 in Jeanblanc et al. (2009)). Hence, is the default indicator process. The characterization of the subordinate process is provided below in Section 3.

The stock price and the scaling constant . From Eq. (2.1) we observe that the dynamics of the stock price can be described by means of the subordinate bivariate process . Indeed, the stock price can be seen as a function which is decomposed according to (2.10) with the payoff function if no default occurs by time , and zero recovery if the firm defaults prior to time . That is,

| (2.21) |

The scaling constant is introduced to ensure that the asset is an -martingale. As shown in Mendoza-Arriaga et al. (2010), will be a martingale if and only if and , where the set is defined in Eq. (2.18). That is, assuming zero interest rates, for every , and for every . From the previous condition in we are free to choose any value of as long as . Hence, from this point onward we assume that . Observe that the underlying assumption is equivalent to modeling the stock price under absolute priority, which means that the stock holder has zero recovery in the event of default.

3 Markovian and Semimartingale Characterization of the Subordinate Process

Before proceeding with the calculation of the quadratic variation of the price process it is essential to describe the characteristics of the underlying stock process in terms of the subordinate bivariate process . For convenience, we summarize some of the key results of Section 3 in Mendoza-Arriaga and Linetsky (2013) who give the Markovian and semimartingale characterization of the process . We refer the reader to Mendoza-Arriaga and Linetsky (2013) for the corresponding proofs.

We begin by recalling some key results about subordination (in the sense of Bochner (1949)) of semigroups of operators in Banach spaces. The expression for the generator is due to Phillips (1952).

Theorem 3.1.

(Phillips (1952)) Let be a subordinator with Lévy measure , drift , Laplace exponent , and transition function . Let be a strongly continuous contraction semigroup of linear operators on a Banach space with infinitesimal generator .

Define

| (3.1) |

Then is a strongly continuous contraction semigroup of linear operators on called subordinate semigroup of with respect to the subordinator .

Denote the infinitesimal generator of by . Then the domain of is a core of and

| (3.2) |

Moreover, if is a Feller semigroup on , then the subordinate semigroup is also a Feller semigroup on .

Next, recall that if is not an absorbing boundary for the process with diffusion coefficient , drift and killing rate , then the transition kernels , , of the semigroups have densities with respect to the Lebesgue measure, where are jointly continuous in . This follows from the fact that any one-dimensional diffusion has a density with respect to the speed measure that is jointly continuous in (cf. McKean (1956) or Borodin and Salminen (2002) p.13). Under our assumptions, the speed measure is absolutely continuous with respect to the Lebesgue measure (cf. Borodin and Salminen (2002), p.17) and, hence, the semigroups have densities with respect to the Lebesgue measure. For , the transition kernel is conservative, i.e., . For the kernel is generally defective, i.e., . While our diffusion is non-negative, for future convenience we extend the transition densities from to by setting for all and for all and . Then, the Markovian characterization of the subordinate bivariate process can be obtained from Theorem 3.1 as follows.

Theorem 3.2.

(Markovian characterization of ) The bi-variate process is a Feller process with the Feller semigroup acting on by:

| (3.3) |

where , , and and are Feller semigroups obtained by subordination in the sense of Bochner from Feller semigroups and .

The infinitesimal generator of the Feller semigroup has the following representation:

| (3.4) |

where , , are generators of .

The generator has the following Lévy-Khintchine-type representations with state-dependent coefficients:

| (3.5) | ||||

| (3.6) |

where the state-dependent Lévy density is defined for all by

| (3.7) |

and satisfies the integrability condition for each (recall that we extended to by setting for ), the drift with respect to the truncation function is given by,

| (3.8) |

and the killing rate is given by

| (3.9) |

where .

If (i.e., is of the form (2.10) with ) and starts with and , then the process

| (3.10) |

is an -martingale.

Now we turn our attention to the semimartingale characterization of the process (see Jacod and Shiryaev (2002), p.76, for the definition of predictable characteristics of a semimartingale).

Theorem 3.3.

(Semimartingale characterization of ) The bi-variate -semimartingale has the following predictable characteristics. The predictable quadratic variation of the continuous local martingale component is:

| (3.11) |

( and since is purely discontinuous). The predictable process of finite variation associated with the truncation function is:

| (3.12) |

where the function is defined in Eq. (3.8) and is defined in Eq. (3.9). The compensator of the random measure associated to the jumps of is a predictable random measure on :

| (3.13) | ||||

| (3.14) |

where are the Lévy densities defined in Eq. (3.7) with , and is the Dirac measure charging .

The Lévy-Itô canonical representation of with respect to the truncation function is:

| (3.15) |

where the compensator of the random measure associated to the jumps of is a predictable random measure on :

| (3.16) |

The Doob-Meyer decomposition of is:

| (3.17) |

with the martingale and the predictable compensator given in Eq. (3.12), so that the -intensity is .

Lastly, we formulate the Itô formula for functions of the bi-variate process in a form convenient for our application. Observe also that the continuous local martingale part can be represented in terms of the Brownian motion as , which will be useful for our representation of the stock price process . Since for the stock price process is a martingale (hence, a special semimartingale) then it suffices to present the Itô formula for the case in which the process is a special semimartingale (see. Jacod and Shiryaev (2002), Definition 4.21, p.43).

Theorem 3.4.

(Itô Formula for ) Suppose starts from and . For any function with and (recall that zero is an unattainable boundary for the diffusion process starting at ), if is a special semimartingale, the Itô formula can be written in the following form:

| (3.18) | ||||

| (3.19) | ||||

| (3.20) | ||||

| (3.21) |

where we introduced a random measure associated to those jumps of that do not coincide with jump of ,

| (3.22) |

and its compensator measure

| (3.23) |

Here, is the random measure associated to the jumps of and is its compensator measure (3.16). The generator is given by Eq. (3.4).

4 Variance Swap Computation

Due to the semimartingale characterization of the process of Section 3 we are now in position to provide the characterization of the stock price process and to explicitly compute the value of variance swap rate . First, let us recall from Eq. (2.21) that the stock price can be seen as a function which is decomposed according to (2.10) with the payoff function if no default occurs by time , and zero recovery if the firm defaults prior to time . The following theorem formally characterizes the stock price process.

Theorem 4.1.

(Stock Price Process ) Let the stock price process be specified in terms of the bivariate process by the prescription , where and . Moreover, assume that the scaling factor satisfies where is the Laplace exponent (2.19) of the subordinator , and where is the constant drift of the background process (2.2)–(2.3) (the set is defined in Eq. (2.18)). Then, the stock price process is a martingale with canonical representation

| (4.1) |

where is the drift of the Lévy subordinator . The random measure corresponds to those jumps of that do not coincide with jump of the default indicator (see Eq. (3.22)). The Lévy density is defined in Eq. (3.7). is a Brownian motion and is the martingale (3.17) associated to .

Proof.

From the restrictions on and , the stock price is a discounted martingale (see, Mendoza-Arriaga et al. (2010), Section 4). In the presence of a constant interest rate and dividend yield , the stock price can be decomposed as , where is a martingale and where is predictable, and hence, it is a special semimartingale. Then, the canonical representation of follows from the Itô formula of Theorem 3.4 applied to the function defined by and . We further observe that the drift vanishes since

| (4.2) | ||||

| (4.3) | ||||

| (4.4) | ||||

| (4.5) | ||||

| (4.6) | ||||

| (4.7) |

In the third equality we used the fact that (cf. Linetsky (2006), Proposition 2.1). The fourth equality follows from the definition (2.19) of the Laplace exponent, which cancels from the condition . ∎

This canonical representation decomposes the stock price process into a purely discontinuous martingale of jumps prior to default with the compensator measure (observe from Eq. (3.23) that ), a continuous martingale component represented in terms of a Brownian motion, and a final jump to zero (the default term ). Clearly, the process is a jump-diffusion process whenever , and a purely discontinuous process for .

Next, we note that if the firm underlying were to default at some time in the interval , then the payoff of a traditional variance swap contract (1.1) would be infinite. To account for this possibility, we modify the floating leg of the VS so that it only accumulates quadratic variation prior to the default time . That is, the long side of a VS, under our modified definition, has a payoff of

| (4.8) |

Notice that, for an asset that cannot default, our modified definition of a VS coincides with the traditional definition of a VS. Meanwhile, for an asset that can default, our modified definition of a VS is guaranteed to have a finite payoff, since the floating leg of the modified VS only accumulates quadratic variation up the time just prior to default.

Using definition (4.8), the fair value of is the risk-neutral expectation of the floating leg

| (4.9) |

An explicit expression for the right-hand side of (4.9) is given in the following theorem.

Theorem 4.2.

Let be given by . Then the right-hand side of (4.9) is given by

| (4.10) |

Proof.

In view of Eq. (4.9), it suffices to first calculate the Lévy-Itô canonical representation of the function , which corresponds to a zero–recovery –contract on the stock price. That is, a contract that pays if no default occurs by time , and zero otherwise (i.e., we set ). Hence, the canonical representation of the pre-default –contract of can be obtained by means of an application of the Itô formula of Theorem 3.4 to the function ,

| (4.11) | ||||

| (4.12) | ||||

| (4.13) |

Observe that due to the default term the process jumps to zero at default, which is consistent with our selection of the function that has zero-recovery in case of default. Consequently, it describes the pre-default dynamics of and prevents it from exploding at default time. From (4.13) it is straightforward to compute the differential of the pre-default dynamics of ,

| (4.14) | ||||

| (4.15) | ||||

| (4.16) |

Finally, multiplying (4.16) by , observing that and a.s., integrating over the interval , taking an expectation, and using the fact that the random measure is a martingale measure, one arrives at (4.10). ∎

Next, we give an alternative formulation of the value of in terms of Feynman-Kac semigroups.

Proposition 4.3.

Proof.

From Theorem 3.2 we observe that . Therefore, the first term of Eq. (4.17) follows immediately. From Proposition 32.5 in Sato (1999), p.215, we know that if as , then . Since as , then to prove it suffices to show that as . Indeed, the latter holds true since for an arbitrary , we have as (cf., McKean (1956), Theorem 4.5). Therefore,

| (4.19) | |||

| (4.20) | |||

| (4.21) |

The rest follows from observing that . ∎

5 Spectral Expansions

In order for the results of Sections 3 and 4 to be useful, we need a practical way to construct the FK semigroups and as well as the associated transition densities and (recall that we had dropped the super-index , since we only need the case of ). Spectral theory, or more specifically, the theory of eigenfunction expansions, provides a straightforward method of constructing these operators and functions. Below, we review some useful results relating to eigenfunction expansions. A detailed description of the spectral theorem for self-adjoint operators in a Hilbert space is given in Appendix B.

Recall that the FK semigroup has infinitesimal generator (2.8). With we associate a scale density and speed density

| (5.1) |

where the point is arbitrarily chosen in . The generator (2.8) with domain

| (5.2) |

is a self-adjoint operator in the Hilbert space . 333 is dense in implies that has a unique self-adjoint extension with . We will not distinguish between and its extension . Therefore, we have spectral representations for the operators and , where is any Borel-measurable function.

Let and be the generalized eigenfunctions/values of . Note that, since is the generator of a contraction semigroup , the eigenvalues of are non-negative. The operator can be written as (for a general Banach space, when the generator is unbounded the latter is understood as a strong limit via the Yosida approximation (see Pazy (1983), Corollary 3.5)). Thus, using (B.5), for any we have

| (5.3) |

where indicates the complex conjugate of . The notation is shorthand for

| (5.4) |

where and are the discrete and continuous portions of the spectrum of respectively and is the Lebesgue measure.

Similarly, using the functional calculus of Theorem B.1, the subordinated semigroup defined in Eq. (3.1) can be obtained as,

| (5.5) |

where is the Laplace exponent of , defined in Eq. (2.19). One should mention that the recent book of Schilling et al. (2010) is an excellent reference for Bochner subordination of semigroups (for example, the last result above is obtained from their Remark 12.4, p.133).

5.1 Uniform convergence of the discrete spectrum

In general, when the spectrum is discrete, the spectral expansion (5.3) of the semigroup (and hence, ) leads to an infinite series. When the semigroup is of trace class, then it is possible to establish uniform convergence for the expansions as follows. Assume that the eigenvalues of satisfy the condition

| (5.6) |

so that the FK semigroup is trace class (see Section 7.2 of Davies (2007)). According to Theorem 7.2.5 of Davies (2007), if is trace class, then the eigenfunctions are continuous functions with the global estimate for all . Setting in (5.3) yields the transition density of the FK semigroup.

| (5.7) |

The sum on the right-hand side of (5.7) converges uniformly in and on compacts. This ensures that, in addition to the convergence, the eigenfunction expansion (5.3) converges uniformly in on compacts for all and . This follows from the Cauchy-Schwarz bound for the expansion coefficients , the eigenfunction estimate, and the trace class condition (5.6).

In this case, the spectral expansion for the subordinated FK semigroup can be obtained by conditioning on the subordinator . For any we have

| (5.8) |

where and is the Lévy exponent of the subordinator . If we assume that the Laplace exponent is such that

| (5.9) |

then the subordinated FK semigroup is trace class. If we further assume that the eigenfunctions of the FK semigroup have a bound independent of on each compact interval (that is, if there exist constants , which depend on the compact interval but are independent of , such that for all ) then, in addition to the convergence, the eigenfunction expansion of the subordinated FK semigroup (5.8) converges uniformly in on compacts for all and . As above, setting in (5.8) yields the transition density of the subordinated FK semigroup

| (5.10) |

The sum in (5.10) is uniformly convergent on compacts in and . Note that the semigroup corresponding to the JDCEV process of Section 6.2 is of trace class.

6 Examples

In this Section, we compute (4.10) explicitly (up to an integral with respect to the Lévy measure of the subordinator ), when the background Feller diffusion is modeled as (i) a geometric Brownian motion with constant killing rate and (ii) a Jump-to-default Constant Elasticity of Variance process.

6.1 Example: geometric Brownian motion with default

Perhaps the most widely recognized non-negative diffusion in finance is the geometric Brownian motion process (GBM). Here, we consider GBM with a constant killing rate, which is a diffusion of the form (2.2)-(2.3) with constant parameters and (excuse the abuse of notation). The generator of the FK semigroup and the corresponding speed density are given by

| (6.1) | ||||||

| (6.2) | ||||||

Most commonly, the FK transition density of GBM with default is written as

| (6.3) |

Due to the fact that (6.1) is a self-adjoint operator on the Hilbert space , with given by (6.2), the FK transition density also has an (generalized) eigenfunction expansion of the form (5.7). The eigenfunctions and eigenvalues of are given in the following Theorem.

Theorem 6.1 (GBM Eigenvalues and Eigenfunctions).

Proof.

Remark 6.2.

Remark 6.3.

When the underlying is given by (2.1) and the background diffusion is modeled as a GBM with default, the at-the-money skew of the model-induced implied volatility surface is controlled by . For jumps in will be preferentially downward, causing a negative at-the-money skew. For , jumps in will be preferentially upward, causing a positive at-the-money skew. As the skew for equity options is typically negative, it makes sense to choose .

We are now in position to compute (4.10) when is modeled as a GBM with default.

Proposition 6.4.

Let be a GBM process with default as described above. Then we have

| (6.6) |

and

| (6.7) |

Proof.

See Appendix A.1. ∎

6.2 Example: Jump-to-Default constant elasticity of variance

The Constant Elasticity of Variance (CEV) model of Cox (1975) is a non-negative diffusion of the form (2.2)-(2.3), where and

| (6.8) |

Here, is the volatility elasticity parameter and is the volatility scale parameter. The specification is consistent with the leverage effect (volatility increases when the stock price falls). For the CEV process hits zero with positive probability. In particular, for , the origin is an exit boundary. For the origin is a regular boundary specified as a killing boundary.

Carr and Linetsky (2006) extend the CEV model to include a possible jump-to-default. Their model is refereed to as jump-to-default CEV or, more succinctly, JDCEV. In the JDCEV framework, the jump to default has a killing rate which is an affine functions of the local variance

| (6.9) |

where and . Although for all default may only occur through a jump from a positive value. When the zero boundary is entrance for the JDCEV diffusion, and thus, the diffusion cannot reach zero from the interior of . The majority of the expressions developed in this Section hold for all . However, the credit-equity modeling framework developed in Sections 2–4 works exclusively for the case in which (i.e., the case in which zero is an entrance boundary). Therefore, one should keep in mind this restriction when applying the following more general results.

For a JDCEV diffusion, the generator of the FK semigroup and the corresponding speed density are given by

| (6.10) | ||||

| (6.11) |

The FK transition density for the JDCEV diffusion was obtained by Carr and Linetsky (2006)

| (6.12) |

where is the modified Bessel function of order , the constants and are given in (6.11) and

| (6.13) |

Due to the fact that the unique extension of is a self-adjoint operator in the Hilbert space with given by (6.11), the FK transition density (6.12) has an eigenfunction expansion of the form (5.7). The eigenfunctions and eigenvalues of are given in the following theorem, which is due to Mendoza-Arriaga and Linetsky (2010).

Theorem 6.5 (JDCEV Eigenvalues and Eigenfunctions).

Proof.

Remark 6.6.

We are now equipped to compute (4.10) when the background process is a JDCEV diffusion. We shall focus specifically on the case , since in this case, all of the relevant functions are in with given by (6.11). Thus, we can compute all the necessary expectations explicitly using the eigenfunction expansion techniques of Section 5.

Before computing the expectations in (4.10) it will be useful to give an analytical solution for the -th moment of the stock price

| (6.18) |

Proposition 6.7 (-th Moment).

Let the diffusion be a JDCEV process with parameters , , , and . Assume . Then, for , the expected value of the function is given by the eigenfunction expansion:

| (6.19) |

where is the Laplace exponent of the subordinator . The JDCEV eigenvalues and eigenfunctions , are given in theorem 6.5, and the expansion coefficients are given by:

| (6.20) |

where is the Pochhammer symbol. Also, the spectral expansion is uniformly convergent for all , absolutely convergent at , and uniformly convergent at if .

Proof.

The proof of part is obtained from Lemma 3.1 and Proposition 3.1 in Mendoza-Arriaga and Linetsky (2010). For part we note that the semigroup is of trace class. In addition, we note that for , the eigenfunctions satisfy the bound for some independent of although it may depend on the range (see inequality (27a) on p.54 of Nikiforov and Uvarov (1988)). Moreover, since the expansion coefficients satisfy the Cauchy-Schwartz bound, , then for any the spectral expansion of converges uniformly for all . That is, converges uniformly for all . In Appendix A.2 we show that the spectral expansion of also converges absolutely at . In addition, if , then the spectral expansion converges uniformly at . ∎

Proposition 6.8.

Let be a JDCEV process with parameters , , , and . Assume . Then we have

| (6.21) | |||

| (6.22) |

Proof.

The expectation in (6.22) can be written explicitly as

| (6.23) | |||

| (6.24) |

where the last equality is due to Proposition 6.7. One should note that if then the sum converges uniformly at and the integral can be done term by term. Otherwise, observe that: (a) the series inside the integral is absolutely convergent for all due to Proposition 6.7 (and continuous for all ), and (b) the Laplace exponent is increasing. Then, we can conclude that the resulting series (6.22) is also absolutely convergent, and hence the exchange of sum and integral is justified (i.e., we integrate term by term with for some and then take the limit as ). ∎

Proposition 6.9.

Let be a JDCEV process with parameters , , , and . Assume and . Then we have

| (6.25) | |||

| (6.26) | |||

| (6.27) | |||

| (6.28) | |||

| (6.29) |

where

| (6.30) | ||||

| (6.31) |

and (with no subscript on ) is the Polygamma function.

Proof.

We start by mentioning that the functions result from the integrals

| (6.32) |

which are available in Prudnikov et al. (1983), Eq. 2.19.6.1 and 2.19.6.3, pp.469. The restriction is imposed such that the sums converge absolutely at . Indeed, it is easy to show that for all we have and . Moreover, since the expansion of converges absolutely at due to Proposition 6.7, then each of the series also converge absolutely at . The rest of the proof consists of integrating term by term. Details are found in Appendix A.3. ∎

7 Market Implied Lévy Subordinators

Note that the value of (4.10) depends on the drift and Lévy measure of the Lévy subordinator . One could, of course, compute the value of by choosing a specific drift and Lévy measure . However, this parametric approach would lead to a considerable amount of model misspecification risk, as there is no guarantee that the chosen subordinator would induce European option prices consistent with those observed on the market. An alternative approach would be to use knowledge of (liquidly traded and efficiently priced) European call and put options to constrain one’s choice of Lévy subordinator. In this section we will show that, when the background diffusion is fixed, the drift and Lévy measure of the subordinator can be obtained non-parametrically from the implied volatility smile of -expiry European options. This approach greatly reduces model misspecification risk, as the obtained subordinator induces -expiry option prices that are consistent with those observed on the market.

Let be described by (2.1). We assume that background diffusion is given, but that the drift and Lévy measure of the Lévy subordinator are unknown. Denote by the price of a European call option with time to maturity and strike price . Note that the price of a call with strike price can be obtained from the price of a put with the same strike through put-call parity. We assume the existence of European call options at all strikes . While calls at all strikes do not trade in practice, Bondarenko (2003) shows how to estimate the value of call at any strike, given the value of calls at a discrete set of strikes.

Let be the transition density of under the risk-neutral pricing measure

| (7.1) |

Note that if and only if . Thus,

| (7.2) |

As Breeden and Litzenberger (1978) show, the transition density can be implied from a semi-infinite strip of call prices. We have

| (7.3) |

Differentiating both sides of (7.3) twice with respect to , and noting that , one obtains

| (7.4) |

Setting our the two expressions (7.2) and (7.4) for equal to each other yields

| (7.5) |

Multiplying both sides of (7.5) by and integrating with respect to , we obtain

| (7.6) | ||||

| (7.7) |

Note that we have used and . We solve (7.7) for

| (7.8) |

If there exists a Lévy subordinator independent of , which is capable of generating the prices of call options on the market, then its Laplace exponent, evaluated at is given by (7.8). 444In a working paper, Carr and Lee (2006) obtain using similar methods. The authors do not deal with Lévy subordinators specifically. Thus, we refer to with Laplace exponent (7.8) as the market implied Lévy subordinator.

Remark 7.1.

It is worth noting that, although one can theoretically compute with call prices available at all strikes , a more convenient expression for the integral in (7.8) can be obtained by integrating by parts twice 555Our thanks to Marco Avellaneda for pointing this out.

| (7.9) | ||||

| (7.10) |

We have the following limits

| (7.11) | ||||||

| (7.12) |

Hence, we find

| (7.13) |

Note that is a derivative with respect to the argument of whereas is a derivative with respect to . The advantage of using expression (7.13) rather than the integral in (7.8) is that the differential operators in (7.13) act on the eigenfunction rather than the call price . Derivatives of can be computed analytically, whereas derivatives of call prices must be computed numerically from market data.

Using (7.8) one can obtain the value of for all . This information is sufficient for constructing the FK transition density and the transition density of . However, to compute the value of we need the drift and the Lévy measure of the subordinator . As we show in the next two subsections, and can be obtained from limited knowledge of the map .

7.1 Example: the Geometric Brownian motion with default

We now develop in detail how to imply from options data, when the underlying diffusion is given by (6.2). In order to use (7.8) we need to obtain since it appears on both sides of the equations, and the eigenfunctions of the killed diffusion, which are given by (6.4). The Laplace exponent (7.8) is given in terms of the ratio,

| (7.14) |

Note that (7.8) simplifies to,

| (7.15) |

setting we find,

| (7.16) |

Now that we have obtained , we can compute the whole function with numerical integration. Moreover, we can use the same approach to derive the Laplace exponent of the Lévy subordinator for the JDCEV dynamics. However, in this case we need to solve numerically for .

7.2 Obtaining and from : the compound Poisson case

As noted in Section 2, when the subordinator is of the compound Poisson type, its Lévy measure can be written as the product of the net jump intensity times the jump distribution

| (7.17) |

In this scenario, the Lévy-Kintchine formula (2.19) can be written

| (7.18) |

where we have defined , the Laplace transform of the measure

| (7.19) |

The drift of the subordinator and the net jump intensity can now be obtained from by taking the following limits

| (7.20) | ||||

| (7.21) |

where we have used . After obtaining and , we use (7.18) to solve for

| (7.22) |

Note, because , equation (7.22) will not give us the value of for any (we know ). However, knowledge of for is not needed in order to uniquely determine . To see this, we need the following theorem.

Theorem 7.2 (Analyticity of the Laplace Transform).

Let . Let be a real, non-negative, non-decreasing function which satisfies and is of bounded variation on for every . If the integral

| (7.23) |

converges for all , then is analytic for all , and

| (7.24) |

Proof.

See Widder (1946), page 57, Theorem 5a. ∎

Remark 7.3.

A function that is analytic in a domain is uniquely determined over by its values along a line segment in .

Remark 7.4.

From (7.24), it is clear that is decreasing and convex.

Let where . If the continuous spectrum of is non-empty , equation (7.22) gives us a map of on some interval . The analytic extension of that map is unique and well-defined in throughout . If the continuous spectrum of is empty , then (7.22) gives us a map of at a countably infinite number of points in (i.e., the proper eigenvalues of ). In this case, the analytic extension of is still uniquely determined if is Lipschitz (see Bäumer and Neubrander (1994), Corollary 1.3)

| and | (7.25) |

If is not Lipschitz, the analytic continuation of is uniquely determined if we know the value of at equally spaced intervals, i.e., if, for , we know where for some and (see Widder (1946), Theorem 6.2). Note that the eigenvalues (6.15) of the JDCEV process are equally spaced.

From a practical standpoint, one cannot evaluate (7.22) at an infinite number of . Thus, in order to obtain from (7.22), one should seek to fit a positive, analytic, decreasing, convex function to a finite number of points of . Upon doing this, one can use the inverse Laplace transform (Bromwich integral) to obtain

| (7.26) |

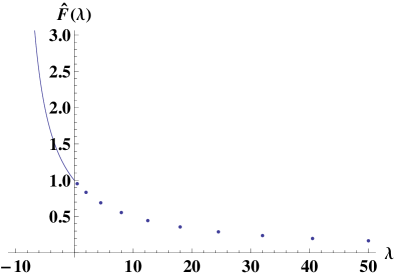

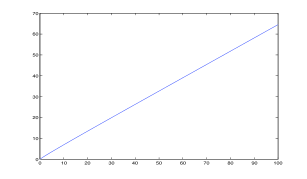

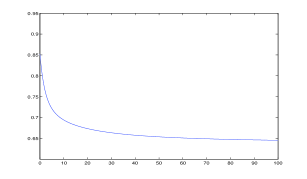

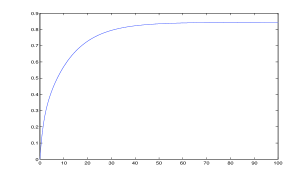

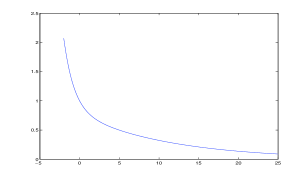

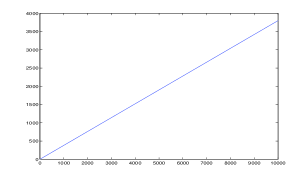

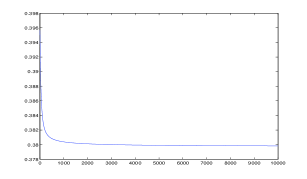

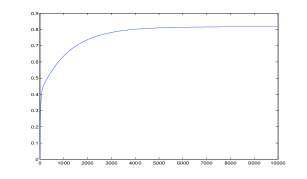

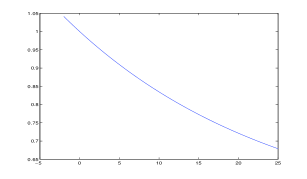

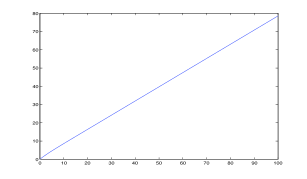

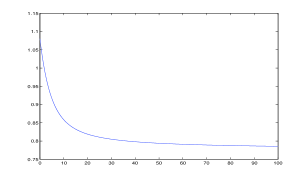

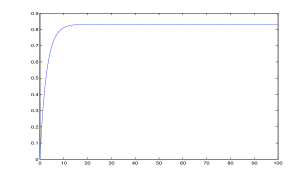

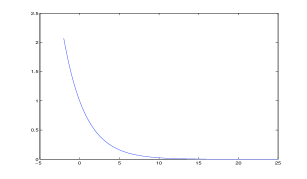

Here the constant is chosen so that the contour of integration lies to the right of all singularities of . Another option for obtaining is to numerically invert the Laplace transform . For a survey of numerical techniques for Laplace inversion we refer the reader to Davies and Martin (1979) and the references therein. Once is obtained, the Lévy measure is given by (7.17). In figure 1, we graphically illustrate how to obtain , and from knowledge of at a discrete set of points.

7.3 Obtaining and from : the general case

When the subordinator is not of the compound Poisson type, its drift can still be found using

| (7.27) |

To obtain we must introduce the tail of the Lévy measure

| (7.28) |

Following Bertoin (2004), pp. 7, we note that

| (7.29) |

where is the Laplace transform of the function . Depending on the nature of , equation (7.29) either gives us a map of along a line segment , in which case the analytic extension of is unique, or (7.29) gives us the value of at a countably infinite number of points. In this case, the analytic continuation of is uniquely determined if we know the value of at equally spaced intervals (the Lipschitz condition would not be satisfied for an infinite activity Lévy process). From a practical standpoint, one may seek to fit an analytic, decreasing, convex function to a finite number of points of . Upon doing this, one can obtain from the Bromwich integral

| (7.30) |

Finally, one obtains from

| (7.31) |

8 Empirical results

In this Section, we use the framework developed in Section 7 to imply from the market using call options on Apple, Google, Microsoft, and Facebook. We then use this information to compute Variance swap rates. Call option quotes were obtained on April 12, 2013 from Google Finance and have a maturity of 19 days. None of the firms payed dividends over the tenor of the option. For each individual symbol we implement the procedure described below.

In order to imply from the market, we must first fix a background diffusion . For simplicity, as in Section 6.1, we assume killed geometric Brownian motion dynamics for the background diffusion . The generator of is given in (6.1). In order to find the parameters (, , and ) of , we choose a range of parametric subordinators, and we fit the subordinated diffusion model to observed implied volatilities. Our calibration results reveal that is an order of magnitude smaller than . Therefore we assume . Next, to obtain the remaining parameters , we fit the killed GBM model (with no subordination) to observed implied volatilities. The results of this calibration fix and .

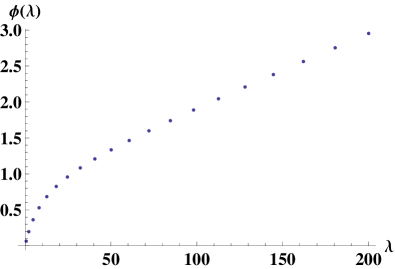

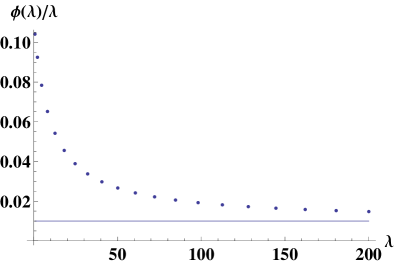

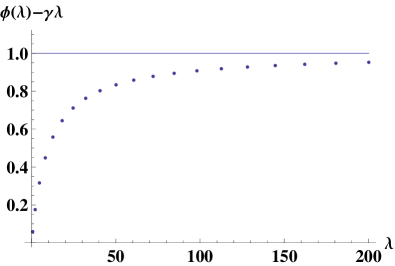

Having fixed a background process , we use equation (7.15) from Section 7.1 to derive the Laplace characteristic exponent of the unknown market subordinator. In order to obtain a continuum of call option prices (which are needed to compute the integral in (7.15)), we use the Stochastic Volatility Inspired (SVI) parametric family of Gatheral (2004) and Gatheral and Jacquier (2012) to interpolate the volatility smile. Note that the Laplace exponent is mathematically expected to be purely real. However, because we are projecting the density onto an imposed basis of eigenfunctions corresponding to the infinitesimal generator , we find that the market implied has an imaginary component. However, the imaginary component is significantly smaller than the real part of . Furthermore, we find that the real part of verifies the properties of characteristic functions.

In Figures 2 and 3, we plot the obtained (real part) of for the four stocks in our data set (Apple, Google, Microsoft, and Facebook). In the same Figures, we also plot and , which, using equations (7.20) and (7.21), enable us to identify the drift and net jump-intensity of the subordinator, and , which we obtain using (7.22). Note that the jump intensity appears to be finite for all four stocks (though, we emphasize that we did not assume this in our analysis). Next, we use (7.22) to derive . Finally, we obtain the Lévy measure of the subordinator using the Laplace transform inversion techniques of Davies and

Martin (1979). Having fully characterized the subordinator for each stock, we use Proposition 6.4 to compute variance swap rates. The results are given below.

| AAPL | FB | GOOG | MSFT | |

|---|---|---|---|---|

| 1M | 0.007821752 | 0.009443126 | 0.00649349 | 0.002771267 |

| 3M | 0.023352561 | 0.028183341 | 0.019121125 | 0.008281498 |

| 6M | 0.046369764 | 0.055932341 | 0.037197644 | 0.016466711 |

| 1Y | 0.091417487 | 0.11015411 | 0.070445294 | 0.032552754 |

9 Conclusion

In this paper we model the price process of an underlying as a Feller diffusion time changed by a Lévy subordinator. This class of models, first developed in Mendoza-Arriaga et al. (2010), allows for the underlying to experience jumps with a state-dependent Lévy measure, local stochastic volatility and a local stochastic default intensity.

The contribution of this paper is two-fold. First, we show how to compute the price of a VS contract in the general Lévy subordinated diffusion setting. Using our general formula, we perform specific VS computations when the background diffusion is modeled as (i) a GBM with default and a JDCEV process. Second, we show that the drift and Lévy measure of the Lévy subordinator that drives the price process can be obtained directly by observation of the -expiry volatility smile. By using call and put prices to uniquely determine the Lévy subordinator that drives the underlying price process, we reduce the risk of model misspecification.

Thanks

The authors would like to thank Stephan Sturm and Vadim Linetsky for their helpful comments on this work.

Appendix A Proofs

A.1 Proof of Proposition 6.4

Part is a straightforward computation

| (A.1) |

Part . Using Proposition 4.3 we have

| (A.2) | |||

| (A.3) | |||

| (A.4) | |||

| (A.5) |

where

| (A.6) | ||||

| (A.7) |

Inserting (A.6) and (A.7) into (A.5) yields

| (A.8) | ||||

| (A.9) | ||||

| (A.10) | ||||

| (A.11) | ||||

| (A.12) | ||||

| (A.13) |

In the second equality we have integrated with respect to and used integration by parts to move the off of the Dirac delta functions. Noting that

| (A.14) |

we find

| (A.15) | ||||

| (A.16) |

A.2 Computation of from Proposition 6.7

Part . Consider the series for . If for all the function satisfies the inequality for where the series , then the series converges uniformly (see Prudnikov et al. (1990), Section I.3.4.3, p.751). From the inequality (27a) on p.54 of Nikiforov and Uvarov (1988), we find that for some independent of . Therefore, we have

| (A.17) |

To show that the series converges, it is enough to show that for a large we have (see Prudnikov et al. (1990) Section I.3.2.19, p.751). Therefore, observe that

| (A.18) |

Thus

| (A.19) | ||||

| (A.20) |

Note that . Moreover, it can be verified that the term inside the bracket is less than for all (recall . This shows uniform convergence at for . To show that the series is absolutely convergent at it suffices to show that with (i.e., d’Alambert’s test for convergence). Equivalently, converges if as . Hence, analyzing the asymptotic behavior and noticing that for , we find that

| (A.21) |

Thus, we would like to test , where . First observe that

| (A.22) | ||||

| (A.23) |

Then, making use of the approximation , we find

| (A.24) |

which concludes the proof.

A.3 Proof of Proposition 6.9

First observe that from Proposition 4.3 we obtain,

| (A.25) | |||

| (A.26) | |||

| (A.27) | |||

| (A.28) |

where

| (A.29) | ||||

| (A.30) | ||||

| (A.31) |

Explicit representation of and are found using

| (A.32) |

and

| (A.33) |

Making the change of variable we obtain

| (A.34) | ||||

| (A.35) | ||||

| (A.36) |

and

| (A.37) | ||||

| (A.38) | ||||

| (A.39) | ||||

| (A.40) |

Now, we use the identity (where is the Kronecker delta) and the series expansion for the Generalized Laguerre polynomials () to obtain

| (A.41) |

and

| (A.42) | ||||

| (A.43) |

Similarly, we obtain

| (A.44) |

where is found by setting in (6.20). Also,

| (A.45) | ||||

| (A.46) |

and

| (A.47) | ||||

| (A.48) | ||||

| (A.49) |

Substituting the above expressions into Eq. (A.28) and using the relation (6.32) for , and as well as equations (6.30) and (6.31), we arrive to the final expression (6.29).

Appendix B Spectral Theorem

In this Appendix we summarize the theory of self-adjoint operators acting on a Hilbert space. A detailed exposition on this topic (including proofs) can be found in Reed and Simon (1980) and Rudin (1991).

Let be a Hilbert space with inner product . A linear operator is a pair where is a linear subset of and is a linear map . The adjoint of an operator is an operator such that , where

| (B.1) |

An operator is said to be self-adjoint in if

| (B.2) |

Throughout this Appendix, for any self-adjoint operator , we will assume that is a dense subset of . A densely defined self-adjoint operator is closed (see Rudin (1991), Theorem 13.9).

Given a linear operator , the resolvent set is defined as the set of such that the mapping is one-to-one and is continuous with . The operator is called the resolvent. The spectrum of an operator is defined as . We say that is an eigenvalue of if there exists such that the eigenvalue equation is satisfied

| (B.3) |

A function that solves (B.3) is called an eigenfunction of corresponding to . The multiplicity of an eigenvalue is the number of linearly independent eigenfunctions for which equation (B.3) is satisfied. The spectrum of an operator can be decomposed into two disjoint sets called the discrete and essential 666 The essential spectrum may be further decomposed into the continuous spectrum and the residual spectrum. It can be shown that the residual spectrum of an ordinary differential operator is empty (see Roach (1982), page 184). spectra: . For a normal operator , a number belongs to if and only if is an isolated point of and is an eigenvalue of finite multiplicity (see Rudin (1991), Theorem 12.29).

A projection-valued measure on the measure space is a family of bounded linear operators in that satisfies:

-

1.

and .

-

2.

is an orthogonal projection. That is, and is self-adjoint: .

-

3.

.

-

4.

If and for then , where the limit is in the strong operator topology.

-

5.

For every in the set function is a complex measure on .

Theorem B.1 (Spectral Representation Theorem).

There is a one-to-one correspondence between self-adjoint operators and projection-valued measures on , the correspondence being given by

| (B.4) |

If is a Borel function on then

| (B.5) |

Proof.

See Rudin (1991) Theorems 12.21 and 13.33. ∎

As a practical matter, if is a differential operator acting on a Hilbert space , where is an interval with endpoints , then the operators defined by (B.5) can be constructed by solving the proper and improper 777The term “improper” is used because the improper eigenvalues and the improper eigenfunctions since . eigenvalue problems

| proper: | (B.6) | ||||||||

| improper: | (B.7) |

For the improper eigenvalue problem one extends the domain of to include functions all functions for which the following boundedness conditions are satisfied

| (B.8) |

We will use Latin subscripts (e.g., ) to denote proper eigenfunctions/values and Greek subscripts (e.g., ) to denote improper eigenfunctions/values. When we do not wish to distinguish between proper and improper eigenfunctions/values we will write and with no subscript. We refer to and as generalized eigenfunctions/values.

After normalizing, the proper and improper eigenfunctions satisfy the following orthogonality relations

| (B.9) |

The operator in (B.5) is constructed as follows (see Hanson and Yakovlev (2002), Section 5.3.2)

| (B.10) | ||||

| (B.11) |

It is not always easy to evaluate divergent integrals of the form and verify that they are in fact delta functions . A method for directly obtaining properly normalised improper eigenfunctions can be found on page 238 of Friedman (1956).

|

|

|

|

| AAPL | (B.12) |

|

|

|

|

| FB | (B.13) |

|

|

|

|

| GOOG | (B.14) |

|

|

|

|

| MFST | (B.15) |

|

|

|

|

References

- Abramowitz and Stegun (1972) Abramowitz, M. and I. A. Stegun (1972). Handbook of Mathematical Functions: with Formulas, Graphs, and Mathematical Tables (10th ed.). New York: Dover Publications.

- Angelos (2009) Angelos, J. (2009, March). Deep Out-Of-The-Money Put Options: A Credit Derivative Market Alternative. Quick Reference Guide, Chigago Board Options Exchange.

- Bäumer and Neubrander (1994) Bäumer, B. and F. Neubrander (1994). Laplace Transform Methods for Evolution Equations. In Conferenze del Seminario di Matematica dell’Università di Bari, 259, Volume Swabian-Apulian Meeting on Operator Semigroups and Evolution Equations, Ruvo di Puglia, Italy, pp. 27–60.

- Bertoin (1996) Bertoin, J. (1996). Lévy Processes, Volume 121 of Cambridge Tracts in Mathematics. Cambridge, UK: Cambridge University Press.

- Bertoin (2004) Bertoin, J. (2004). Subordinators: Examples and Applications. In P. Bernard (Ed.), Lectures on Probability Theory and Statistics Ecole d’Ete de Probabilites de Saint-Flour XXVII - 1997, Volume 1717 of Lecture Notes in Mathematics: Mathematics and Statistics, pp. 1–97. Springer Berlin / Heidelberg.

- Bielecki and Rutkowski (2004) Bielecki, T. R. and M. Rutkowski (2004). Credit Risk: Modeling, Valuation and Hedging. Berlin: Springer-Verlag.

- Bochner (1949) Bochner, S. (1949). Diffusion Equation and Stochastic Processes. In Proceedings of the National Academy of Sciences, Volume 35 (7), pp. 368–370.

- Bondarenko (2003) Bondarenko, O. (2003). Estimation of Risk-Neutral Densities Using Positive Convolution Approximation. Journal of Econometrics 116(1-2), 85–112.

- Borodin and Salminen (2002) Borodin, A. and P. Salminen (2002). Handbook of Brownian Motion: Facts and Formulae. Probability and Its Applications. Basel, Switzerland.: Birkhauser Verlag AG, 2 Rev. Ed.

- Breeden and Litzenberger (1978) Breeden, D. T. and R. H. Litzenberger (1978). Prices of State-Contingent Claims Implicit in Option Prices. The Journal of Business 51(4), 621–651.

- Carr and Lee (2006) Carr, P. and R. Lee (2006, July). Quadratic Variation Derivatives with Skew. Working Paper.

- Carr and Lee (2009) Carr, P. and R. Lee (2009, May). Robust Replication of Volatility Derivatives. Preprint.

- Carr et al. (2012) Carr, P., R. Lee, and L. Wu (2012). Variance Swaps on Time-Changed Lévy Processes. Finance and Stochastics 16(2), 335–355.

- Carr and Linetsky (2006) Carr, P. and V. Linetsky (2006). A Jump to Default Extended CEV Model: An Application of Bessel Processes. Finance and Stochastics 10(3), 303–330.

- Carr and Madan (1998) Carr, P. and D. B. Madan (1998). Towards a Theory of Volatility Trading. In R. Jarrow (Ed.), Volatility: New Estimation Techniques for Pricing Derivatives. London, UK: Risk Books.

- Carr and Schoutens (2008) Carr, P. and W. Schoutens (2008). Hedging under the Heston Model with Jump-to-Default. International Journal of Theoretical & Applied Finance 11(4), 403–414.

- Carr and Wu (2010) Carr, P. and L. Wu (2010). Stock Options and Credit Default Swaps: A Joint Framework for Valuation and Estimation. Journal of Financial Econometrics 8(4), 409–449.

- Carr and Wu (2011) Carr, P. and L. Wu (2011). A Simple Robust Link Between American Puts and Credit Protection. The Review of Financial Studies 24(2), 473–505.

- Chang et al. (2012) Chang, J.-R., M.-W. Hung, and F.-T. Tsai (2012). Cross-Market Hedging Strategies for Credit Default Swaps under a Markov Regime-Switching Framework. The Journal of Fixed Income 22(2), 44–56.

- Consigli (2004) Consigli, G. (2004). Credit Default Swaps and Equity Volatility: Theoretical Modeling and Market Evidence. In Proceedings del Workshop su Portfolio Optimisation and Option Pricing, Venezia, pp. 45–70. Dipartamento di Matematica dell’Università Ca’Foscari.

- Cont and Kokholm (2013) Cont, R. and T. Kokholm (2013). A Consistent Pricing Model for Index Options and Volatility Derivatives. Mathematical Finance 23(2), 248 – 274.

- Cox (1975) Cox, J. C. (1975). Notes on Option Pricing I: Constant Elasticity of Variance Diffusions. Reprinted in The Journal of Portfolio Management, December 1996 23, 15–17.

- Cremers et al. (2008) Cremers, M., J. Driessen, P. Maenhout, and D. Weinbaum (2008). Individual stock-option prices and credit spreads. Journal of Banking & Finance 32(12), 2706–2715.

- Davies and Martin (1979) Davies, B. and B. Martin (1979). Numerical Inversion of the Laplace Transform: a Survey and Comparison of Methods. Journal of Computational Physics 33(1), 1–32.

- Davies (2007) Davies, E. B. (2007). Linear Operators and Their Spectra. Number 106 in Cambridge Studies in Advanced Mathematics. Cambridge University Press.

- Erdelyi (1953) Erdelyi, A. (1953). Higher Transcendental Functions, Volume II. New York: McGraw-Hill.

- Filipovic et al. (2013) Filipovic, D., E. Gourier, and L. Mancini (2013, March). Quadratic Variance Swap Models. Working paper.

- Friedman (1956) Friedman, B. (1956). Principles and Techniques of Applied Mathematics, Volume 280. New York: Wiley.

- Gatheral (2004) Gatheral, J. (2004). A Parsimonious Arbitrage-Free Implied Volatility Parameterization with Application to the Valuation of Volatility Derivatives. Presentation at Global Derivatives & Risk Management, Madrid.

- Gatheral and Jacquier (2012) Gatheral, J. and A. Jacquier (2012, April). Arbitrage-Free SVI Volatility Surfaces. Working paper.

- Hanson and Yakovlev (2002) Hanson, G. W. and A. B. Yakovlev (2002). Operator Theory for Electromagnetics: An Introduction. New York: Springer-Verlag.

- Jacod and Shiryaev (2002) Jacod, J. and A. N. Shiryaev (2002). Limit Theorems for Stochastic Processes (2nd. ed.), Volume 288 of Comprenhensive Studies in Mathematics. Berlin: Springer.

- Jeanblanc et al. (2009) Jeanblanc, M., M. Yor, and M. Chesney (2009). Mathematical Methods for Financial Markets. Springer Finance. London, UK: Springer.

- Jung (2006) Jung, J. (2006, August). Vexed by Variance. Risk Magazine, 41–43.

- Linetsky (2006) Linetsky, V. (2006). Pricing Equity Derivatives Subject to Bankruptcy. Mathematical Finance 16(2), 255–282.

- McKean (1956) McKean, H. P. (1956). Elementary Solutions for Certain Parabolic Partial Differential Equations. Transactions of the American Mathematical Society 82(2), 519–548.

- Mendoza-Arriaga et al. (2010) Mendoza-Arriaga, R., P. Carr, and V. Linetsky (2010). Time Changed Markov Processes in Credit-Equity Modeling. Mathematical Finance 20(4), 527–569.

- Mendoza-Arriaga and Linetsky (2010) Mendoza-Arriaga, R. and V. Linetsky (2010). Constructing Markov Processes with Dependent Jumps by Multivariate Subordination: Applications to Multi-Name Credit-Equity Modeling. Submitted for publication.

- Mendoza-Arriaga and Linetsky (2013) Mendoza-Arriaga, R. and V. Linetsky (2013). Time-Changed CIR Default Intensities with Two-Sided Mean-Reverting Jumps. To appear: Annals of Applied Probability.

- Neuberger (1990) Neuberger, A. (1990). Volatility Trading. Working Paper: London Business School.

- Nikiforov and Uvarov (1988) Nikiforov, A. and V. Uvarov (1988). Special Functions of Mathematical Physics: A Unified Introduction with Applications. Basel: Birkhäuser.

- Pazy (1983) Pazy, A. (1983). Semigroups of Linear Operators and Applications to Partial Differential Equations. N.Y., USA.: Springer-Verlag.

- Phillips (1952) Phillips, R. S. (1952). On the Generation of Semigroups of Linear Operators. Pacific Journal of Mathematics 2(3), 343–369.

- Prudnikov et al. (1983) Prudnikov, A. P., Y. A. Brychkov, and O. I. Marichev (1983). Integrals Series: Special Functions, Volume II of Integrals and Series. CRC Press.

- Prudnikov et al. (1990) Prudnikov, A. P., Y. A. Brychkov, and O. I. Marichev (1990). Integrals Series: More Special Functions, Volume III of Integrals and Series. CRC Press.

- Reed and Simon (1980) Reed, M. and B. Simon (1980). Methods of Modern Mathematical Physics (Revised ed.), Volume I: Functional Analysis. Academic Press.

- Roach (1982) Roach, G. F. (1982). Green’s Functions (2nd. ed.). Cambridge, UK: Cambridge University Press.

- Rudin (1991) Rudin, W. (1991). Functional Analysis (2nd. ed.). McGraw-Hill Science.

- Sato (1999) Sato, K. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge, UK.: Cambridge University Press.

- Schilling et al. (2010) Schilling, R. L., R. Song, and Z. Vondracek (2010). Bernstein Functions: Theory and Applications. Number 37 in De Gruyter studies in mathematics. Berlin: De Gruyter.

- Widder (1946) Widder, D. V. (1946). The Laplace Transform. New Jersey: Princeton University Press.