Crises and collective socio-economic phenomena: simple models and challenges

Abstract

Financial and economic history is strewn with bubbles and crashes, booms and busts, crises and upheavals of all sorts. Understanding the origin of these events is arguably one of the most important problems in economic theory. In this paper, we review recent efforts to include heterogeneities and interactions in models of decision. We argue that the so-called Random Field Ising model (rfim) provides a unifying framework to account for many collective socio-economic phenomena that lead to sudden ruptures and crises. We discuss different models that can capture potentially destabilising self-referential feedback loops, induced either by herding, i.e. reference to peers, or trending, i.e. reference to the past, and that account for some of the phenomenology missing in the standard models. We discuss some empirically testable predictions of these models, for example robust signatures of rfim-like herding effects, or the logarithmic decay of spatial correlations of voting patterns. One of the most striking result, inspired by statistical physics methods, is that Adam Smith’s invisible hand can fail badly at solving simple coordination problems. We also insist on the issue of time-scales, that can be extremely long in some cases, and prevent socially optimal equilibria from being reached. As a theoretical challenge, the study of so-called “detailed-balance” violating decision rules is needed to decide whether conclusions based on current models (that all assume detailed-balance) are indeed robust and generic.

pacs:

Valid PACS appear hereI Introduction

Traditional economics treats the aggregate behaviour of a whole population through a “representative agent” approach, where the heterogeneous preferences of individual agents are replaced by average preferences curve. Agents are supposed to rationaly determine their action in isolation, with no reference whatsoever to the decision of others; in other words, interactions between agents are usually neglected. The need to account for interactions seems however quite compelling: imitation and social pressure effects must be responsible for the appearance of trends, fads and fashion or mass panic, that would be very difficult to understand if agents were really insensitive to the behaviour of others. 111As a recent anecdotal, but pittoresque piece of evidence: the explosion of “love-locks” on the Pont des Arts in Paris since 2008. Financial markets – and for that matter whole economies – are prone to crises and exhibit sudden discontinuities and crashes, even in the absence of any violent exogenous event. The idea that some crises are endogenously generated dates back to MacKay MacKay , Keynes Keynes and Minsky Minsky , with many more recent apostles – see e.g. Soros ; Akerlof ; Kirman_Book ; Sornette1 ; Sornette2 ; Risk . Collective effects can be the key to the success of a brand, a book or a movie Rodgers , or else of a new technology or a vaccination campaign. But they can also be detrimental and do lead to major catastrophes when imitation cascades are based on unreliable information or dangerous ideas, and when social pressure supersedes rational thinking. In any case, social imitation often leads to distortion and exaggeration, i.e. a decoupling between the cause and the effect, which in turn generates inequalities and concentration (or “condensation”) phenomena, see sections V.4, VII.1. These effects may grow ever stronger in our Internet and social network dominated societies.

From a theoretical point of view, interactions may indeed lead to an aggregate behaviour that is completely different from that implied by standard representative agent approaches Kirman_RA . Catastrophic events and discontinuities can occur at the macro level, when the behaviour of independent agents would be perfectly smooth and featureless. 222The converse is in fact also true: discontinuous behaviour at the agent level may end up being smoothed out at the macro level! Models of collective behaviour that illustrate those “surprises” on the way from micro to macro are of course familiar to statistical physicists – with Van der Waals and Weiss as early heroes Sethna_Book . Similar ideas started to develop in quantitative sociology in the seventies, with models introduced by Schelling (1971, 1973) Schelling and Granovetter (1978) Granovetter that are formally very close to spin models of magnets (see below, section IV.1). In fact, the analogy between magnetic polarization and opinion polarization was noted and formalized slightly earlier by a physicist (Weidlich) in 1971 Weidlich_1 who coined the word “Sociodynamics”, and slightly later by Galam, Gefen & Shapir (1982) Galam_0 , in a manifesto for “Sociophysics”.

As it is well known, interactions can lead to multiple equilibria and ergodicity breaking, which in turn lead to very interesting effects like “punctuated equilibrium”, hysteresis (or path dependence) and aging. These theoretical scenarios offer enticing metaphors for understanding economic systems as well, in particular the emergence of trust, norms and conventions. After all, a prosperous economy can only be achieved through efficient coordination and collaboration. Although anticipated by Keynes and pioneered by Föllmer in 1974 (again in the context of spin models! Follmer ), these ideas only really permeated into economics in the early nineties, partly nurtured by the Santa Fe meetings “The Economy As an Evolving Complex System” SantaFe1 ; SantaFe2 . As Kirman (1992-93) was forcefully arguing against the representative agent framework Kirman_RA and proposing his ‘ant’ recruitment model Kirman_ant , Brock and Durlauf wrote a series of remarkable papers Durlauf ; Brock_Hommes ; Brock using statistical mechanics methods to elicit the importance of social interactions in economics, emphasizing that the utility or payoff an individual receives depends directly on the choices of others. 333See also the earlier insightful paper by Becker Becker_restaurant . Although not yet fully mainstream, the field of “social dynamics” is now well appreciated 444The paper Discrete choice with social interactions by Brock and Durlauf Brock has 976 Google scholar citations at the time of writing. (see the books Becker_Book ; Durlauf_Book for enlightening discussions, BHW ; Chamley and references therein for another strand of literature on “herding” effects; see also Orlean ). In parallel, physicists have actively contributed to the field, with a variety of models for coordination, contagion, opinion formation, segregation, herding, etc. – see e.g. MG ; Fortunato ; Buchanan ; Ball for recent overviews of these endeavours.

The present paper is intended to be a personal, somewhat informal review, centred around the use of Random Field Ising models (rfim) as a generic model for crashes, opinion swings and discontinuities in a socio-economic context. The rfim provides a unifying framework and an enticing “story” for many disparate collective phenomena, including overnight trust evaporation such as that which occured after Lehman’s bankruptcy in 2008, or the persistence of cultural traits or habits, even when damaging for the community. 555Think for example of the tax-evasion culture in some countries, that has recently become an acute issue. Interestingly, some of the predictions are robust and can be quantitatively tested against data. We then discuss some theoretical limitations of the simplest (mean-field) version of the model. Three issues are, to our way of thinking, particularly relevant. One is the importance of history and memory in the preference of individual agents, in the absence of any interaction effects (this is called habit formation or “stickiness”) – see section VII.1. Another is the use of decision making rules (or selection probabilities) that have become standard in the above cited literature, and that amount to assuming what is called detailed-balance in the physics jargon – see section VI.2 for a precise definition. How much non detailed-balance rules would affect the qualitative features is very much an open problem (section VI.2). The third one concerns spatial effects, that should play a major role in some cases, as illustrated by election turnout statistics (section V.3). Finally, we cursorily discuss alternative (or rather, complementary) models of crashes and regime shifts based on feedback loops between past events and current decisions (sections VII.2, VII.3).

Many ideas in this paper have been “long and widely known”. However, they are only well known to those who know them well. Our experience is that even simple ideas may have a hard time permeating into other communities (the adoption models presented below could even be used to explain why! Helbing_boost ). Sometimes, a detailed translation helps. We hope that the present paper can serve this purpose and be a helpful exposition, in particular for students in physics and in economics interested by the issue of crises and collective phenomena.

II A generic binary choice model: the Random Field Ising Model

II.1 Set up of the model

The so-called ‘Random Field Ising Model’ (rfim) was proposed to model hysteresis loops and other anomalous properties of disordered magnets Sethna1 ; Sethna2 . The hysteresis loop problem is an example of a collective dynamics of flips (the individual magnetic spins) under the influence of a slowly evolving external solicitation. Depending on the parameters, the flips may take place smoothly, or be organized in intermittent bursts, or ‘avalanches’, leading to a specific acoustic pattern called Barkhausen noise. But because the model is so generic, it can be used as a simplified model for a host of other physical situations as well, such as earthquakes, fracture in disordered materials, failures in power grids, etc. These systems respond to the driving in a series of avalanches spanning a broad range of scales, which Sethna, Dahmen and Myers (2001) proposed to call “crackling noise” Sethna_nature .

As was originally proposed in Galam_0 ; Galam_1 , the model can also be transposed to represent binary decision situations under social pressure, and influenced by some global information (such as the price of a product or the quality of a technology) or by zeitgeist. This transposition was recently discussed in several socio-economical contexts in, e.g. QF ; Nadal1 ; Nadal2 ; Nadal3 ; Michard ; Harras (see Vives ; Marsili_Kirman ; Lorenz ; Holyst for variations on the theme). The model has a rich phenomenology. In particular, discontinuities appear in aggregate quantities when imitation effects exceed a certain threshold, even if the external solicitation varies smoothly with time. In this situation, the aggregate demand is a multi-valued function of the price Nadal1 . Below the threshold, on the other hand, the behaviour of “demand”, or of the average opinion, is smooth, but the natural trend can be substantially amplified and accelerated by peer pressure, possibly leading to sudden crises.

We will assume that each agent is confronted to a binary choice, the outcome of which is denoted by . This binary choice can be to vote or not to vote, or to vote yes or no in a referendum; it can be to buy or not to buy a certain good Nadal1 ; Nadal2 ; Nadal3 , to evade tax or not, to clap or to stop clapping at the end of concerts, etc. Michard . Textbook examples in sociology are to attend or not to attend a seminar Schelling , to join or not to join a riot Granovetter or a strike Galam_0 , to go or not to go to the crowded El Farol bar Arthur ; MG . Of course, examples can be multiplied ad libitum. We wish to add two more in view of their importance: one is to trust or not to trust. This encompasses a large number of situations that recently made the news: credit markets and credit ratings; trust in future economic prospects; trust in the validity of the models used to value derivative products Marsili_Kirman ; trust in the value of money itself, etc. The second is adopting or not an environment friendly technology (i.e. solar heating) which is individually costly but collectively valuable. This is closely related to the famous “tragedy of the commons” Hardin wherein individual short term interest is in conflict with long term collective welfare.

It is reasonable to assume that the decision of agent depends on three distinct factors:

-

•

(i) his personal inclination, preference or “willingness to pay/adopt”, measured by a real variable which we take to be time independent (but see section VII.1) and distributed according to a certain p.d.f . Large positive ’s means a strong a priori tendency to decide , and large negative ’s a strong bias towards .

-

•

(ii) public information, affecting all agents equally, such as objective information on the scope of the vote, the price of the product agents want to buy, the balance sheet of the banks, the advance of technology, etc. The influence of this time dependent common factor will be called the incentive field , again a real variable in .

-

•

(iii) social pressure or imitation effects; each agent is influenced by the previous decision made by a certain number of other agents in his “neighbourhood”, . The influence of on is taken to be , that adds to and . If , the decision of agent to buy (say) reinforces the attractiveness of the product for agent , who is now more likely to buy. This reinforcing effect can obviously lead to an unstable feedback loop, as discussed in section IV.2. If on the contrary , the action of agent deters agent from making the same choice. This “anti-conformist” or contrarian tendency, although rarer in human nature, can sometimes exist and be relevant. For example, buying can push the price up and discourage others from buying themselves. When both signs of coexist, one expects many metastable states with a very rich dynamics, see e.g. MM .

II.2 Decision rules

To sum up then, the overall perceived incentive of agent to choose over is

| (1) |

Now one has to specify a decision rule, given a certain value of the total incentive. The simplest rule is:

| (2) |

meaning that the decision to “buy” is reached whenever the incentive reaches a certain threshold value , which can be chosen without loss of generality to be zero. 666Any other -dependent value could have been chosen, since this simply amounts to shifting the value of idiosyncratic field .

However, the above decision rule is perhaps too deterministic and restrictive. One may imagine that agent could not pay attention to or misread the public information (which is often intrinsically ambiguous and hard to interpret) or else have a random, time dependent component in his preference (a sophisticated way of saying people can be fickle). 777The distinction between the two interpretations will be discussed again in section VI.1. A more general rule that is a standard in the choice/decision making literature (see section VI.1) is the so-called “logit rule” or “quantal response” which makes the decision a random variable, with probability:

| (3) |

where is a parameter that specifies the amount of noise (or “irrationality”) in the decision process, and is the analogue of inverse temperature in physics. When , incentives play no role and there is a random probability of the two decisions, whereas when , one recovers the deterministic rule given by Eq. (2).

It is in fact very natural to generalize slightly the above rule to keep some memory of the previous decision and allow for possibly time dependent incentives:

| (4) |

and

| (5) |

The coefficient can be interpreted as a probability to reconsider one’s past choice between and . When , all memory is lost and one recovers the previous rule Eq. (3).

These decision rules might at this stage appear as somewhat arbitrary, and guided by the fact that they will allow one to use directly Boltzmann-Gibbs measure and use results from statistical mechanics. We will comment on those rules below (sections VI.1,VI.2) – although considerable effort has been devoted to axiomatize decision theory Anderson_Palma , we feel that there is indeed some leeway here that might lead to interesting problems for future research.

II.3 The mean-field limit

If all , the above model is known in physics as the Random Field Ising model at temperature , and has been intensively studied in the last decades, in particular at (see e.g. Sethna1 ; Sethna2 ; Dhar ). In physics, natural networks of connections are -dimensional regular lattices, but other topologies, more natural in a socio-economic context such as the fully connected case, regular trees or random graphs have been studied as well. The qualitative phenomenology however does not depend much on the chosen topology, nor on the distribution of idiosyncratic fields , although quantitative details might be sensitive to these specifications. For simplicity, and in line with many previous papers Weidlich_1 ; Galam_0 ; Weidlich_review ; Brock ; Nadal1 ; Michard ; Nadal2 ; Nadal3 we will thus mostly restrict attention here to the “mean-field” case where , pairs. This does not mean that each agent consults all the other ones before making his mind, but rather than the average opinion , or total demand, becomes public information, and influences the behaviour of each individual agent. This is in fact a very realistic assumption in many cases: for example, the total sales of a book, or number of viewers of a movie, is certainly an important piece of information for the consumers. It is also thought that the evolution of the public opinion can be affected by polls or by confidence index, i.e. by a proxy of the average opinion Nadeau ; Stauffer ; Lux , and, indeed, this is the reason for certain countries banning opinion polls shortly before elections. In the case of financial markets, the price change itself can be seen, on a coarse-grained time scale, as an indicator of the aggregate demand (although the detailed relationship between the two might be quite subtle, see marketimpact ; Toth ). While this mean-field description may be very reasonable in certain settings, one expects that network/local effects may be relevant in other cases, for which the neighbourhood of agents is restricted to a more specific community. This locality might actually change quite a bit the features of the model (see section IV.2).

We now turn to an analysis of the rfim model in different limits, and try to summarize the salient results and their interpretation in a socio-economic context.

III The case of a homogeneous population: the Ising-Weidlich model

III.1 Dynamical equations and equilibrium

Let us start by analysing the case where , . Up to a shift in the public information field , one can always set . There are agents, and at time , the fraction of them who have chosen the alternative is . In the mean-field limit , the total incentive to choose over is simply:

| (6) |

If we speak of adopting individual solar heating, for example, can be interpreted as the immediate cost of installing a new heating system, whereas the term encapsulates both the expected cost decrease and technical improvements as more people shift to the new technology, and the social pressure that makes it “politically incorrect” to stick with hydrocarbon greedy devices.

Now, we use the dynamical updating rules given by Eqs. (4) above, and set . It is easy to show that the following probabilities hold for the evolution of the number of ‘adopters’, between and : 888It is interesting to notice that in Kirman’s ant recruitment model Kirman_ant , one rather has because change of opinions are supposed to happen during two-body “encounters” where one of the two convinces the second one to change his mind. In the present setting, encounters are not necessary.

| (7) |

From the above, one gets the evolution of the average and the square-average :

| (8) |

and

| (9) |

These equations were obtained in the present sociological context by Weidlich Weidlich_review , but are of course very standard in the context of the mean-field Ising model.

Taking infinitesimally small for convenience, and comparing with the predictions of the following Itô stochastic differential equation:

| (10) |

(where is the usual Brownian noise) one finds, by identification:

| (11) |

In order for this equation to be well behaved in the large limit, a change of time scale must be performed as (meaning that over a finite change of , a finite fraction of the population has been offered the possibility to switch). This finally leads to:

| (12) |

From now on, we will drop the tilde. Note that the scale of the noise goes down as with the population size.

The “equilibrium” state(s) of the system are such that , i.e. such that , leading to:

| (13) |

Setting , one recovers (as expected) the standard Curie-Weiss mean-field equation, re-derived by Brock and Durlauf Brock in the present framework: 999Note that there our choice of differs by a factor from the usual convention.

| (14) |

The solutions of that equation are well known. When , there is a critical value separating a high noise regime where agents shift randomly between the two choices, with . As first noted by Weidlich Weidlich_1 , a spontaneous “polarization” of the population occurs in the low noise regime , i.e. even in the absence of any individually preferred choice (i.e. ). When , one of the two equilibria is exponentially more probable than the other, and in principle the population should be locked into the most likely one: whenever and whenever . In the limit , the above equilibrium analysis suggests that as soon as (i.e. when the adoption cost is less than ), the whole population should move towards the “right” equilibrium .

Unfortunately, the equilibrium analysis is not sufficient to draw such an optimistic conclusion. A more detailed analysis of the dynamics is needed, which reveals that the time needed to reach equilibrium is exponentially large in the number of agents, and as noted by Keynes, in the long run, we are all dead. This situation is well-known to physicists, but is perhaps not so well appreciated in other circles – for example, it is not discussed in Brock . This is the main message of the present section, which would otherwise not be much more than a textbook exercise.

III.2 Potential barrier and metastability

Define a potential function such that . Up to an irrelevant additive constant, one finds

| (15) |

The analysis of is easy in the limit . Since is , one finds that as long as the potential has two minima situated, as expected, very close to and . The difference is equal to meaning, as explained above, that the equilibrium is indeed favored when . But there also appears an energy barrier between the two minima, situated at , which makes it hard for the system to crossover from the “bad” minimum to the “good” one. Using the above Langevin equation, Eq. (12), one finds that the time needed for the system, starting around , to reach is given by:

| (16) |

where is a numerical factor. The important point about this formula is the presence of the factor in the exponential. This means that whenever , the system should really be in the socially good minimum , but the time to reach it is exponentially large in the population size. In other words, it has no chance of ever getting there on its own for large populations. Only when reaches , i.e. when the adoption cost becomes zero will the population be convinced to shift to the socially optimal equilibrium – simply because is not a minimum anymore (note indeed that as ).

As decreases towards (i.e. as the noise in the decision process increases), the two minima get closer to each other and the barrier between then gets smaller, until hysteresis and polarization effects disappear altogether.

Let us summarize what happens in a situation where the cost of adopting a new technology, a new idea, or a socially beneficial attitude, decreases steadily as a function of time in our (so far) homogeneous population. When individual make near-optimal choices, the population as a whole will not adopt until , even if it would be optimal for the community as a whole to adopt as soon as – it would actually do so if one was prepared to wait an exponentially long time. As a function of time, one should see an extremely small number of adopters until the cost drops to zero, in which case the whole population finally shifts to the new paradigm. This is very different from the standard model of innovation diffusion, based on the following simple differential equation proposed by Bass in 1969 (Bass , and for a recent illuminating review Young ):

| (17) |

which says that the speed of adoption first increases with the number of people who have adopted. This equation leads to the famous “S-curve” for adoption. It predicts that the adoption speed is maximum when , at variance with the above scenario where the adoption speed abruptly increases when is still quite small. Note however that the discontinuity in time should be smoothed by the speed at which information about the behaviour of others is spreading; but when applied to financial markets, for example, this time can indeed be very short.

What are the solutions to escape from the “bad” equilibrium as soon as it becomes collectively profitable to move to the “good” one? Clearly, this is a coordination problem, which becomes hard to solve when is large. Apart from lowering the cost , the model above suggests at least three possibilities to make the barrier easier to cross: a) increase the variance term by coordinating the moves (instead of having independent decisions): this can be done through advertising campaigns, word of mouth, etc.; b) decrease , i.e. increasing the noise, for example when the information about the true costs is ambiguous; c) decrease , i.e. the number of people in direct interaction – people do not adopt because nobody else adopts. In physics, the existence of mutually inaccessible minima with different potentials is a pathology of mean-field models that disappears when the interaction is short-ranged. In this case, the transition proceeds through “nucleation”, i.e. droplets of the good minimum appear in space and then grow by flipping spins at the boundaries. This suggests an interesting policy solution when social pressure resists the adoption of a beneficial practice or product: subsidize the cost locally, or make the change compulsory there, so that adoption takes place in localized spots from which it will invade the whole population. The very same social pressure that was preventing the change will make it happen as soon as it is initiated somewhere.

Before leaving the homogeneous Ising-Weidlich model of this section, we would like to note that the solar heating example is in fact not be the best one, because the dynamics of the model assumes that choices are to some extent reversible, i.e. each agent can in principle flip back and forth between the two options. While this is clearly the case for opinions, tax-evasion, safe driving, trust, etc., it is harder to imagine that agents can easily switch between solar cells and heating oil – at least on short enough time scales to make the above description useful. The model in the next section is actually better suited for such irreversible choice situations.

IV The role of heterogeneities: scaling and avalanches

IV.1 The zero-temperature rfim and classical models of adoption

Let us now come back to the idea that agents are not clones and have different preferences or willingness to pay , distributed according to a certain p.d.f . The case where social pressure is absent, i.e. is very simple to analyse when . Call the cumulative distribution of , i.e. the probability that . The aggregate demand, or average opinion for a given incentive field is easily obtained as:

| (18) |

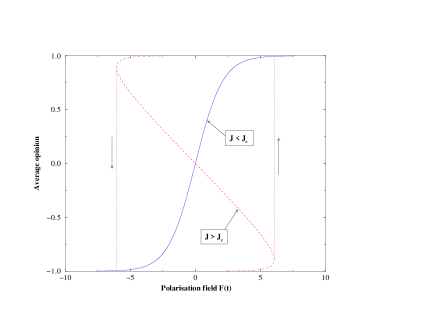

(The subscript means that here). As increases slowly from to , the average opinion evolves from to in a way that mirrors exactly the distribution of a priori opinions in the population. For a generic distribution of (for example, Gaussian), the opinion evolves smoothly as the polarization field is increased – see Fig. 1, blue line. If one interprets as minus the price of a product, and the price at which an agent is happy to buy, the total demand curve is clearly equal to the number of buyers, i.e.

| (19) |

which increases as the price decreases. For a unimodal distribution, will look like a smooth “S-curve” as the price decreases, or as the quality of the product increases. This is called the “moving equilibrium” model in the innovation diffusion literature Young .

The situation can change drastically when imitation is introduced. We keep here to a mean-field coupling to the average opinion, and comment on the robustness of the results later, section IV.6. This global feedback effect simply shifts to , leading to a self-consistent equation:

| (20) |

The threshold model of Schelling and Granovetter Schelling ; Granovetter is a particular case, although usually expressed slightly differently. As above, call the number of agents deciding to attend a seminar, or join a riot, etc. Each agent has a preference expressed as a conformity threshold: if the observed number exceeds an -dependent number that we set as , then agent joins as well the next time round. 101010In agreement with the above convention, large means that agent is more prone to join, i.e. his threshold is lower. This leads to a dynamical equation of the form:

| (21) |

The “equilibrium” value is given by the fixed point solution which coincides with Eq. (20) with . Eq. (20) contains as an extra degree of freedom, which allows one to treat both conformity and the moving equilibrium idea when is time dependent. Note that when all ’s are positive (which is the case of the mean-field model), decision changes are ‘irreversible’ when has a monotone evolution in time. In other words, if flipped from to at a certain moment in history, it will never flip back to later. This would not be true in the much richer (and more complicated) case where can take both positive and negative signs.

IV.2 Imitation vs. heterogeneity

Coming back to Eq. (20) when imitation is weak enough, one can expand the right hand side in powers of , leading to first order to:

| (22) |

This equation shows that the point where the slope of vs. is maximal coincides (for symmetric distributions) with the point where the speed of variation of opinion changes is maximally amplified: imitation leads to exaggeration. As imitation becomes stronger, the above perturbative expansion breaks down. Still, the maximum slope of vs. increases and finally diverges for a critical value , beyond which is a discontinuous function of (see Fig. 1, red line). Much as in the previous section, the self-consistent equation Eq. (20) has, for a range of , three solutions for , one of which being unstable (see Fig. 1). In an economic context, it means that the demand for a product can be a multi-valued function of price, i.e. the possible coexistence of a high demand and a low demand solution for the same price. This has been fully investigated in Nadal1 ; Nadal2 ; Nadal3 .

The solution chosen by the system depends on history. Suppose one starts with and (zero demand), and slowly increases to make the alternative choice more appealing. The average opinion will first follow the lower branch until it jumps discontinuously to the upper branch, for a certain threshold field (and symmetrically on the way back, at , as the field is decreased). Although Fig. 1 is qualitatively similar to the results of the previous section (which formally corresponds to , where is the width of the distribution ), there are many crucial differences. For example, the jump amplitude is not equal to but depends continuously on even when , and vanishes when as , where in mean-field or on tree-like graphs. Another difference is that the dynamics between and when the jump occurs is made of avalanches of different sizes, which we will discuss in section IV.4 below. A third difference is the existence of many more “equilibrium states”, beyond the ones corresponding to the protocol that we describe here (i.e. and all spins down at ). Other states can be reached, for example preparing the system with one will follow a totally different hysteresis loop as is increased. This “sensitivity to initial conditions”, or strong history dependence, makes the model quite appealing. 111111These effects, strictly speaking, disappear in finite dimensional lattices because of nucleation. But the time scales associated with nucleation may be so large that these metastable states still have a real existence.

What sets the critical value of the interaction parameter beyond which strong herding effects occur? Dimensional analysis immediately implies that where a numerical constant (perhaps infinite) that depends on the detailed shape of , and also on the topology of the graph. This means, as intuitively expected, that jumps and collective frenzy happen more easily in homogeneous populations (low ) than in strongly heterogeneous populations. Stability (of markets, democracies,…) requires diversity. For the mean-field model with a Gaussian , . If the graph is a regular tree, then whenever the number of neighbours is Dhar , but the transition disappears for a tree with 2 (i.e. a line) or 3 neighbours. For these little connected lattices, interaction effects are never strong and there is no hysteresis phase. On a two-dimensional square lattice with each bond of strength , the threshold is Vives_num and for a three-dimensional cubic lattice Sethna2 (both for a Gaussian ).

IV.3 Critical scaling

The vicinity of the critical point reveals interesting critical properties, to a large extent independent of the detailed form of . Noting the distance from criticality, one finds that the opinion slope takes a scaling form in a relatively wide region around of Sethna2 :

| (23) |

where the function can be computed explicitly Sethna_Dahmen ; Michard , and is universal. In particular, is a finite constant and . Eq. (23) means that the slope, as a function of , peaks at a maximum of order and remains large on a small window of field of order . In other words, the height of the peak behaves as an anomalous power of the width with . This is strikingly different from what is expected for any regular model, like the moving equilibrium model (), for which and , leading to . Interestingly, this leads to testable predictions, which only rely on the assumption that the external incentive field is a smooth function of time – see section V.1.

IV.4 Avalanches

If now one ‘zooms’ on finer details (on scale ) of the curve in the vicinity of , one discovers a very interesting structure. One finds that the evolution of is actually resolved in a succession of ‘avalanches’ of different sizes , where the first opinion change induces (through interactions) a second one, then a third one, etc. After the th one has flipped, the system is stable again, in the sense that for the current value of all ’s agree with the sign of the total incentives .

The statistics of the avalanches is in fact easy to understand in mean-field, because the dynamics maps into the well known critical branching process. When one agent flips from to , it induces a change of incentive for all other agents. For a given value of and , the agents that are on the verge of flipping have a preference precisely equal to . The average number of flips induced by the first one is thus given by Sethna_Dahmen :

| (24) |

Each of the newly converted agents can convert on average new ones, etc. In mean-field, this is equivalent to the Galton-Watson branching process with branching ratio GW . It is well known that when , avalanches are all of finite size, whereas when some avalanches will diverge and sweep the whole system. In the region of , the distribution of avalanche sizes is a truncated power-law:

| (25) |

Now, let us explain why corresponds to the critical point , . Eq. (20) can be written , with . One thus sees that the function must cut the first diagonal once for and three times for . The point must correspond to the case where is tangent to the first diagonal at the point of crossing. Therefore, at the critical point,

| (26) |

which is indeed equivalent to (see Eq. (24)). Interestingly, exactly the same scenario occurs in the so-called Fiber-Bundle model for fracture Hansen_fiber ; Rava , which is very close in spirit to the above models. In a nut-shell, the Fiber-Bundle model assumes initially intact fibers in parallel, subject to an external force that is equally distributed over all fibers. Fibers are heterogeneous, and when the force acting on the th one exceeds a certain threshold , the fiber breaks and the external force is redistributed over all remaining fibers. It is clear that the fraction of intact fibers obeys the following self consistent equation:

| (27) |

where is the distribution of fiber strengths. For , the above equation has generically two solutions that merge for and disappear for (i.e. the bundle breaks apart). Again, when the function has a slope equal to one at . The same analysis as above can be carried over for the avalanches in this model as well. 121212The exponent in the avalanche size distribution is the same as the one appearing in the first return time distribution of a one-dimensional random walk. Indeed, the critical branching process can be mapped onto that problem, see Sornette90s ; Hansen_fiber for more elaborations on this point.

This analysis offers an enticing microscopic picture of how large opinion swings actually develop in a population: as a branching process that generates avalanches. Most of them are small, but some may involve an extremely large number of individuals, without any particularly large change of external conditions (i.e. change in ). The power-law distribution that appears is tantalizing and might enable one to understand why bursts of activity and power-laws appear in the distribution of returns in financial markets, for example. But there is at present no convincing argument that would make this analogy sharp.

IV.5 Delays and trends

The above analysis assumes that the external incentive field varies extremely slowly, so that the state of the system can follow adiabatically the equilibrium condition Eq. (20). It may be useful to generalize the model to include lag effects, and to write the following time evolution equation Young :

| (28) |

where defines an equilibration time scale, i.e. the time needed for agents to adapt to the new piece of information that changed . If is very short compared to the evolution time of , we are back to the previous analysis. Otherwise, lag effects matter and could for example affect the avalanche size distribution for large .

Another potentially interesting generalisation is to include the influence of past trends. People are not only sensitive to the contemporaneous behaviour of others, they also take cues from past patterns. An obvious candidate is the speed at which has varied in the past, which may give a sense of urgency and adds to the external incentive . The simplest model that encodes this would be Eq. (28) with replaced by:

| (29) |

where is the time scale over which the past trend is computed and the strength of the coupling to past trends. This could be an interesting model for the dynamics of financial markets, similar to the one discussed in section VII.3. Other examples of feedback between past history and present decisions will also be reviewed there.

IV.6 Phase diagram for noisy decisions

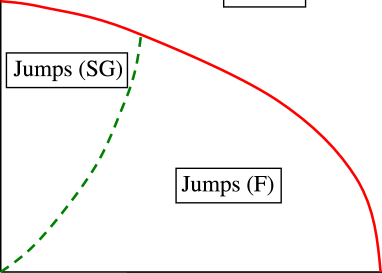

Before moving to more quantitative evidence for the type of effects that the rfim is supposed to capture, it is important to end the present section with a discussion of the role of the coefficient in the decision rules. Up to now, we considered that – i.e. decisions are ‘rational’ and conform to the overall incentive, . Introducing some amount of noise does not immediately destroy the above picture: for a given imitation strength , there is still a critical value of the heterogeneity below which jumps occur and above which the demand curve becomes smooth. Similarly, for a fixed , jumps remain until decision noise becomes larger than a -dependent value (i.e. for smaller than ). The situation is summarized in Fig. 2, which shows the region of the plane where jumps and hysteresis occur, located below the red line. Above that line (i.e. where heterogeneities and/or noise are strong enough, there is a single equilibrium and a unique demand/opinion curve). The model in section III.1 corresponds to the -axis of this graph (), whereas the results of the present section correspond to the -axis (). From the point of view of potential applications of the model, it is reassuring to see that the whole scenario predicted by the rfim, and in particular the transition between a “crisis” phase and a smooth phase, is quite robust against details (noise, network topology, shape of the probability distribution of preferences, etc.). 131313This universality was also noted and emphasized in Nadal2 ; Nadal3 . Finally, note that there is a second, green line in Fig. 2 Krzakala , separating a regime of strong history dependence where the number of equilibrium states is exponential in the number of agents and hysteresis sub-loops are stable, from a phase that is more similar to what happens in the homogeneous case , with a single (large) hysteresis loop. 141414For other recent examples of agent based models with an exponential number of equilibria, see Farmer_new ; Lucas .

IV.7 Summary

In summary, the transposition of the rfim to opinion/demand formation predicts that the average opinion evolves, as a function of the global solicitation, very differently if imitation effects are weak (in which case the evolution is smooth) or if imitation exceeds a certain threshold, in which case aggregate quantities are discontinuous and catastrophic avalanches may be triggered. More quantitatively, the model predicts that in generic situations, the speed of change should peak more and more as the critical point is approached. As a function of time, the speed of change exhibits a maximum of height and of width , the two being related by . This is very different from non-critical adoption models, such as the “moving equilibrium” model, for which . These predictions seem to be qualitatively and even quantitatively relevant in several instances that we describe in the next section.

V The rfim scenario: empirical evidence and possible applications

It is now a rather well established fact that people do not make decision in isolation but rely on the choice/opinion of others, see Raafat ; Baddeley for a detailed discussion and many references. Recent work includes in particular the artificial culture market of Salganik et al. Salganik , the analysis of earning forecasts by expert analysts Guedj , or the wisdom of crowds Helbing_crowds . Of course, anecdotal evidence concerning famous financial bubbles (like the tulip-mania in Amsterdam and other examples of ‘madness of crowds’ Thistime ) or famous fads & fashions (like Louis XIV’s wig, Catherine de Medicis’ forks and Richelieu’s rounded knives, etc.) make it quite obvious that social pressure can be disturbingly dominant. Keynes conceived imitation (herding) as a response to uncertainty and to the recognition of one’s own ignorance: people follow the crowd because they think (or fear) that the rest of the crowd might be better informed. 151515 Peyton Young in Durlauf_Book contrasts instrumental conformism, when it is beneficial to do what others do, to informational conformism, when we conform to what others do because it conveys information on best actions. The problem, we believe, is that often nobody really has any idea of what’s going on, so the “information” provided by the others actions is close to zero. Gigerenzer provides a complementary interpretation Gigerenzer ; Gigerenzer_Book : people tend to follow rules of thumb and routines. Imitation qualifies well as a ‘fast and frugal’ heuristic, which furthermore has minimal information costs. However, a recurrent problem has been to disentangle effects induced by direct imitations or social pressure from correlations that would appear just because people have the same information or the same cultural bias, etc. Manski

V.1 Some quantitive evidence

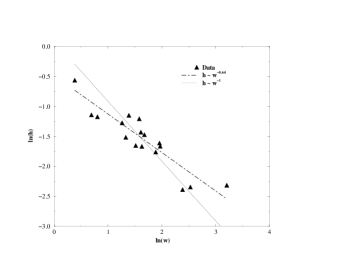

In that respect, the robust prediction of the rfim alluded to in the previous section allows one to test for the existence of herding effects with minimal extra assumptions. This is the program that we followed with Q. Michard in Michard . The idea was to compare the dynamics of the very same phenomenon (for example, the adoption of cell phones) in different countries, supposedly characterized by different imitation parameters, and different distributions of willingness to adopt. Still, assuming (a) that the speed of evolution of the external incentive field is similar in all countries, and (b) that the ratio is not too far from the critical value of the model 161616The rfim is actually well known to have a rather wide critical region, as emphasized in Sethna2 . then the scaling prediction Eq. (23) should hold, leading to a universal relation between the height and the width of the evolution speed , where is the speed of evolution of the external incentive field, assumed to be independent of the country or population. If the distance from the critical point varies across the set of available countries or crowds, should reveal peaks with different heights and widths, but all related by with if imitation is strong. 171717We emphasize again here that if , or if the variations were due to different speeds in different countries, one should observe . The way and are extracted from data is detailed in Michard . We gathered data concerning (a) the drop of birth rates in European countries in the second half of the XXth century Fertility (b) the increase of cell phones in Europe in the 90 s, (c) the way clapping dies out at the end of music concerts and (d) crime statistics in different US states in the period 1960-2000. Although social influence have been argued to be important in the latter case too JS , our data set did not show enough idiosyncratic variations across states to be exploited. In the first three cases, we find that our data fits well the picture suggested by the model, and that collective effects seem to be present, with indeed – see Fig. 3. The example of clapping is interesting because it is very close to being a controlled experiment Michard . In that case, we observed both continuous and abrupt endings, as predicted by the model. Challet et al. Unilever analyzed data from a Swiss on-line supermarket, and report for soap consumption. More data would be needed to ascertain the relevance of the rfim scenario in real situations. In particular a finer time resolution would allow one to test one of the crucial predictions of the model: the presence of bursts, or avalanches, with a truncated power-law distribution of sizes (see Eq. (25)). This would be a clear-cut signature of imitation cascades. 181818see also Cascades ; Cascades2 for experiments on information cascades and tip for some empirical evidence of tipping points in urban segregation phenomena. We also refer the reader to Blume for a review on “econometric” approaches to social phenomena.

V.2 Metaphors

In any event, the model has a huge narrative potential, and is well adapted to describe, qualitatively or quantitatively, many situations. For example, Nadal et al. Nadal1 ; Nadal2 ; Nadal3 have analyzed the model in great detail in the case of a product sold at price by a monopolist supplier, and in the presence of imitation effects on the demand side. They note that the monopolist has two different strategies: either to attract a large fraction of buyers at low prices or to target few buyers willing to pay high prices. There is again a first order transition where the optimal strategy switches abruptly from one to the other Nadal3 . They further note that, interestingly, the optimal price is generically just slightly below the price at which the high demand equilibrium disappears. A small change in the customers characteristics may lead to a decrease of this critical price. If this change is not anticipated by the seller, the posted price may become greater than the critical price, resulting in a collapse of the demand, and they relate this observation to Becker’s interpretation of the “crowded restaurant paradox” Becker_restaurant .

The sudden shift from the high demand branch to the low demand branch is also a natural mechanism for crashes in financial markets. We believe Risk , like many others, in the critical importance of trust as a determining factor for the prosperity of economies, and for securing well-functioning financial markets. Trust is a collective asset that allows efficient coordination and tremendously accelerates business. The most illuminating example is fiat money, that can only exist if people trust that a piece of paper will not be worthless tomorrow – and of course if everybody gives value to a dollar bill, the dollar bill is valuable. Clearly, money is more efficient than barter because it solves the otherwise daunting problem of matching individual preferences. On the other hand, because trust is an immaterial sentiment, it can evaporate overnight. Changing one’s mind can be instantaneous, the speed of change is not limited by physical constraints. This is one of the reason why crisis, crashes and bank runs can occur (this point of view is forcefully expressed in, e.g. Hosking ; Marsili_trust and refs. therein). Think for example of the sudden freezing of the money markets just after Lehman’s default: clearly, banks stopped lending because all other banks stopped lending. Credit means: “I believe (credo) that I will see my money back some day”, and this belief can disappear even if no destruction of wealth has physically taken place. Established trust is a situation where the subjective probability of default or of failure is very small.

Several quantitative models for trust collapse have been studied in the past few years, see e.g Marsili_trust ; Marsili_Kirman ; Lorenz ; Holyst and refs. therein. Some are directly related to the rfim, which can indeed be formulated as a model for trust cycles, associated to bubbles and busts, bank runs and hyper-inflation. Suppose that for some reason the world is in a euphoric state, corresponding to and – everybody trusts the system. Fiat money is considered as absolutely safe. Now, imagine that for some reason the objective trustworthiness of the system decreases. This could be due to a rise of inflation, or to over-valued prices of assets or houses that appear far above any reasonable fundamental value. This could also be due to political instability, or an increase in any measured or perceived risk. The most risk adverse individuals will act first and sell their assets, or take their money away from the bank, whereas most people firmly believe that the system is safe. 191919I personally know people who cashed their money just after Lehman’s default, and left their bank with a plastic bag full of bank notes. Still, these initial “irrational” reactions seed wariness in the minds of others – what if they were right? Maybe I should do the same? As dark clouds accumulate, it is easy to guess what will happen. Either imitation effects are small and people sell one by one their assets, leading to a slow decay of the stock markets or a soft landing of the business cycle. Or imitation is beyond the critical threshold and after an extended period where confidence is only maintained because everybody else is confident (as in a bubble), a small exogenous event (i.e. a small further decrease of ) may be enough to trigger global panic, i.e. crashes, bank runs, hyper-inflation, etc. Because the system is hysteretic, the fundamental information must grow back much beyond the point where the crisis occurred for people to regain confidence (see Fig. 1).

One can think about the model slightly differently. Imagine that the external world, captured by , is fixed, but that the imitation parameter can vary in time. This is quite realistic: in periods when uncertainty is small, people can rely on fundamental information to make a judgement. When uncertainty increases, it becomes more and more tempting to take one’s cue from the crowd. As increases past , an initially weakly polarized state can suddenly evolve towards (see Fig. 1). This is a kind of volatility feedback effect, where past volatility may trigger more herding effects, finally leading to a crash (see e.g. Cont ; Curty ; Harras ; Harras2 ).

V.3 Spatial effects

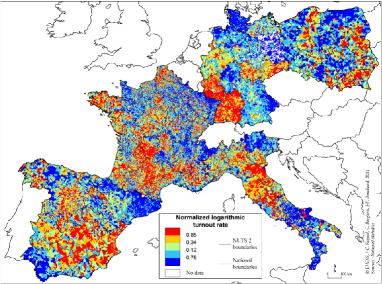

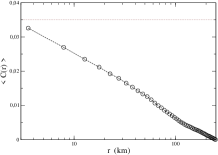

Another interesting topic is the spatial structure of the incentive field , which can be interpreted in the rfim setting as the average willingness (to pay/adopt/trust, etc..), around which an idiosyncratic component is added. It might be expected that on several issues, the average willingness strongly depends on regional characteristics and culture. One specific example for which spatially resolved data is available are elections. The simplest observable is the turnout rate, which reveals persistent patterns, both in time and in space – see Borghesi_election1 ; Borghesi_election2 and Fig. 4. Calling the turnout rate on a given election in a city located at , one can define the logarithmic turnout rate as:

| (30) |

The pattern of Fig. 4 suggests a non-trivial bahaviour of the spatial correlation of the field, which is found to decay roughly logarithmically with distance: 202020In the following expression, denotes an averaging over all positions .

| (31) |

as shown in Fig. 4, inset. This logarithmic dependence holds well for different elections and different countries, up to distances comparable to the size of the country Borghesi_election2 . Another striking observation is that the voting habits of the different regions seem to be extremely persistent historically Borghesi_election1 .

Assuming a logistic distribution for the idiosyncratic willingness to vote, one finds: 212121Note that here we neglect the immediate influence of others in the actual decision to vote, i.e. the interaction term. See the discussion of this point in Borghesi_election1 .

| (32) |

where is the (local) average willingness to vote. From the above identification, we conclude that this average willingness itself has logarithmic correlations in space and long-range correlations in time. This suggests the existence of a “cultural field” that keeps the memory independently of the presence of particular individuals.

A simple and rather natural idea is to decompose the time dependent incentive field as a sum of a -independent component (which measures the average interest in the election), a slowly varying “cultural” field that we want to model, and a white noise (in space) contribution , which models city-specific idiosyncraties and only has short-ranged spatial correlations Borghesi_election1 ; Borghesi_election2 . The cultural field should evolve due to (a) cultural “shocks” that contribute to changing the overall mood in a given city (such as the closing down of a factory or of a military base, important changes in population, etc.) and (b) diffusion, as a consequence of the exchange of ideas and opinions between nearby cities. Through human interactions, the cultural differences between nearby cities tend to narrow, leading to a Laplacian term in the evolution equation (in the continuum limit). We therefore proposed to write the following noisy diffusion equation for Borghesi_election1 ; Borghesi_election2 :

| (33) |

where measures the speed of diffusion of the cultural field 222222Taking the relevant inter-town distance to be km and the time for opinions to get closer to be a few months, one can estimate to be of the order of magnitude of a few hundreds km2 per year. and a white noise field. If cities were located on the nodes of a regular grid, it would be easy to show analytically that the stationary correlation function of the field decays as a logarithm of distance, as given by Eq. (31). However, the spatial distribution of cities in countries is in reality quite strongly heterogeneous, which leads to significant concavity when is plotted as a function of Borghesi_election2 . Quite remarkably, this concavity is very similar to what is observed for the empirical correlations Borghesi_election1 ; Borghesi_election2 , which tends to confirm that the long-range spatial correlations observed in election turnout rates can indeed be traced to the presence of an underlying cultural field with a diffusive dynamics.

While preparing this review, we discovered that a diffusion equation very similar to Eq. (33) was in fact proposed by Schweitzer and Hoylst in 2000 Schweitzer ; Schweitzer2 to model opinion formation. They call the “information field” and their equation can be written, in the present context, as:

| (34) |

The last term describes a coupling between the past realized turnout rates and the cultural field, i.e. large participation rates tend to motivate people to vote more the next time round. However, the presence of such a term in the diffusion equation would cut-off the logarithmic dependence of beyond a distance . Since this is not observed empirically, is probably large (20 years or more) – at least in the context of election participation.

The idea of a persistent cultural (or information) field that evolves according to a noisy diffusion equation seems quite important. If true, many other social phenomena like consumption habits, behavioral biases, etc. should exhibit long ranged (logarithmic) spatial correlations. More empirical work on the spatial correlations of these decisions, for example based on consumption data, in different situations and in different countries, would be very valuable – although the results on election turnout in many countries are already quite encouraging Borghesi_election2 .

V.4 Multiple choices

A generalisation of the rfim setting to multiple choices is interesting for obvious reasons: when in a bookstore, supermarket or record shop, the choice is not between two products but between thousands, or even millions of products. The same is true of the stock market – one can choose to invest in thousands of different stocks. Again, the choice of others is an important piece of information that we take into account before buying a book or deciding on a movie. It is plausible that herding effects play a role in the appearance of Pareto-tails in the measure of success (book sales, movie attendance, smart phones, etc.). A natural generalization of Eq. (2) to an M-choice situation reads Borghesi_choice :

| (35) |

where is the consumption of product by agent , and , and is the relative consumption of product , i.e.

| (36) |

The field describes the intrinsic attractivity of product , while is the willingness to pay of agent , to acquire product . As above, the coefficient measures the strength of social influence, and a factor is added to make sure that social influence remains of order unity when .

The most interesting question about such a model is to know whether the realized consumption is faithful, i.e. whether or not the actual choice of the different items reflects the ‘true preferences of individual agents, as would be the case in the absence of interactions (). Based on the phenomenology of the rfim, one expects that this will not be the case when is sufficiently large. The exact solution of the model in the limit indeed shows that a phase transition takes place for , where can be exactly computed in terms of the distribution of the s and the s, assumed to be IID random variables. For , strong distortions occur, meaning that the realized consumption will (i) “condense” into a small subset of all possible choices, (ii) violate the natural ordering of individual preferences and (iii) become history dependent: a particular initial condition determines the winners in an irreproducible and unpredictable way Marsili_Raf1 . Instead of all products getting a share of the market, some (but not necessarily the best ones, with large s) become ‘hits’ and attract a disproportionate number of buyers. This is a possible mechanism for the appearance of Pareto tails in most measures of success Zajdenweber ; Redner . Similar effects were observed in the artificial cultural market of Salganik et al. Salganik , which allowed them to conclude that increasing the strength of social influence increases both the inequality of market shares and the unpredictability of success (i.e. which products become winners).

The model can be transposed to other interesting situations, for example that of industrial production, for which one expects a transition between an archaic economy dominated by very few products and a fully diversified economy, as the dispersion of individual needs becomes larger as time passes.

VI Choice theory and decision rules

VI.1 The logit rule: arguments and extensions

The literature on choice theory is extremely vast and has been beautifully reviewed in Anderson_Palma (although the field has progressed since 1992). We want here to restrict to a few comments that may help to understand some of the problems at stake. In a nutshell, classical choice theory assumes that the probability to choose alternative in a set of different possibilities can be written as:

| (37) |

where is the “utility” of alternative and the “noise” parameter that allows one to interpolate between equiprobable choices () and utility maximisation (). Before discussing the arguments that have been put forth to justify the above “logit rule”, one should specify what one really means by “the probability to choose alternative ”. Two quite different interpretations can be found in the literature (see Anderson_Palma , pp. 30-33):

-

•

(1) One is that each agent, as a function of time, flips between different alternatives. At each time step the probability to choose is the above . This could be due to an imperfect knowledge of the utilities , or to “irrational” effects such as illusions and intuitions, cognitive limitations, etc. It could also be due to a truly time evolving context or environment, not described in the theory, but that randomly affects the relative utilities of the alternatives, in such a way that the perceived utility of agent at time is , where are time dependent random variables. In this interpretation, makes sense even for a single agent: it is the probability that, at a given instant of time he or she chooses .

-

•

(2) The second interpretation assumes that any given agent always makes the same choice, based on the maximisation of perceived utility , where are again random variables but now fixed in time. In this case, is the probability that a given agent in the population has forever chosen .

At the aggregate level, the two interpretations may look indistinguishable (see McFadden ), and this is indeed true for non-interacting (independent) agents. In the presence of interactions, however, the two formulations lead to different results for the aggregate behaviour (see section VI.2). The first interpretation corresponds to the -axis in the phase diagram of Fig.2, while the second corresponds to the -axis.

The proposed justifications for the exponential form of the probabilities in Eq. (37) are of three types Anderson_Palma : (a) axiomatic Anderson_Palma ; (b) based on specific assumptions about the random variables that affect the perceived utilities; (c) based on entropy arguments. On point (b): if the ’s are IID random variables with a Gumbel (double-exponential) distribution, then it is possible to show that the probability is indeed given by Eq. (37) McFadden . However, the deep reason for choosing a Gumbel distribution has remained elusive – the fact that the Gumbel distribution is max-stable does not seem to help (see however MG , pp 32-33). On point (c): one can argue that agents do not want to maximize the expected utility alone, but take into account the information cost (or the entropy) associated to the weights . As is well known, the maximisation of indeed directly yields Eq. (37). This has been called the variety seeking behaviour of agents in Anderson_Palma (pp. 78-79), and the exploration-exploitation compromise in Nadal_Kirman , which might account for some inherent uncertainty about the time stability of utilities (see also Marsili_Logit ). Still, all these arguments look a bit weak; 232323Other arguments, inspired by statistical physics, could go as follows Marsili_Logit : imagine a choice consisting in two sub-choices concerning issues in disjoint sets . These two sub-choices are furthermore assumed to be independent, i.e. the choice of an alternative in does not impact the utility of any of the alternatives in , and vice-versa. The utilities are therefore additive in that case: . Since the sub-choices are independent, one should also have . Looking for probabilities that depend on the total utility of the choice therefore selects the exponential form. One could also try to replicate the usual canonical construction of the Boltzmann weight, by arguing that a choice is never in isolation but interacts with many other choices, while the agent is only interested in the total utility. Sub-optimal choices (corresponding to a finite ) are allowed because they only have a small contribution to the total utility. However, these arguments are somewhat ad-hoc. the ultimate justification seems to be that the logit rule is mathematically very convenient Anderson_Palma , and allows one to use well known results in statistical physics because the logit rule is equivalent to the Boltzmann-Gibbs measure.

We will explore more the dynamical interpretation (1) above, which seems to us more realistic. People can change their minds and not make the same decision all the time, even when confronted to the very same information (see the discussion in Anderson_Palma ). The idea of introducing a “tremor” noise in the utility dates back to Thurstone Thurstone . If there is time correlations in the noise, and no learning or feedback from the past that induce some systematic evolution of the utilities, one can think of a dynamical model of decisions as the following Markov chain. At each time step, agent , having made choice , reviews his alternatives with probability and does not bother with probability . The possible alternatives are in a set . Often people do not even consider all alternatives simultaneously but sequentially, so just pick one possible , and decide whether it is worth going for that one. (We make this assumption to simplify the following discussion.) It is reasonable to postulate that the probability for this alternative to be adopted is equal to the probability that the noisy utility contributions are such that:

| (38) |

Alternative is therefore adopted with probability , where is the complementary cumulative distribution function of the noise differences. The time-dependent probabilities therefore obey the following Master equation:

| (39) |

As is well known, a sufficient condition for having Eq. (37) as the equilibrium (long time) solution of this equation is the so-called “detailed balance” equation: 242424One should of course keep in mind that the time needed to reach full equilibrium might be very large, or even infinite if there is a phase transition and ergodicity breaking – something that requires the number of states to be infinite.

| (40) |

and provided that all choices are reversible, i.e. , . Clearly, condition (40) is satisfied when corresponds to the logistic distribution:

| (41) |

but other distributions may be suitable as well. However, there is no a priori justification for imposing that the distribution of noise differences should have such a property. If the ’s are IID (or at least exchangeable), one can deduce in full generality that there is a function such that:

| (42) |

So expanding for small ’s one finds that the detailed balance condition is satisfied to first order with , but may be violated for higher orders in utility differences:

| (43) |

Not much is known about these non-detailed balance models. A natural conjecture is that for this particular class of models, for which the transition rates are functions of a utility (or energy) difference between the initial and final state, a quasi-equilibrium state is reached with no large scale currents. The robustness of the phase diagram and of the phase transitions to non-detailed balance terms (, , etc.) is of course a crucial issue.

The case of binary choice situations with no interactions between agents is clearly much simpler, and can be solved in full generality as:

| (44) |

and the introduction of a mean-field interaction leads to a self-consistent equation that generalizes the usual Curie-Weiss equation (Eq. (14) above):

| (45) |

It is clear that for generic concave functions this model still has a second order phase transition when , of the type discussed in section III.1 (where ). First order transitions can occur for more exotic shapes of .

But this point of view shows that there is no reason whatsoever to think that the noise parameter should be the same for all agents. Some may be more “rational” than others, meaning that a distribution of ’s could be needed – something that is unusual in physics. The interaction parameter could also be heterogeneous. The criterion for the appearance of hysteresis effects is, in the general case, , where the average is taken over the population.

VI.2 Non interacting vs. interacting agents, and coordination failure

It is worth dwelling a little more on the issue of detailed-balance decision rules in the presence of interactions. Call the choice made by agent and the joint distribution of the choices of the -agents at time , and the configuration of choices made by all agents. The time evolution of the population is a random walk in the space of choices, and is determined by the transition probabilities to go from configuration to configuration between and . Assume that at each time step, only one agent can change his choice. The set of accessible configurations from is made of all configurations that differ from by a single agent changing his choice. If every single agent uses a logit-rule to update his choice from to , with possibly dependent utilities , one finds for the transition probabilities:

| (46) |

Assuming individual choices are reversible in the above sense, do these transition probabilities obey detailed-balance? Superficially it seems to be so, but the presence of interactions can ruin the detailed-balance property. Detailed-balance is obeyed provided there exists a certain function that depends on the choice made by all agents, such that:

| (47) |

In this case, one indeed has:

| (48) |

such that the long-time equilibrium probabilities are given by the Boltzmann-Gibbs weight:

| (49) |

When agents are non interacting, in the sense that the utilities are independent of the choice made by others, then clearly:

| (50) |

When there are interactions, this is no longer true, and in fact it is in general not possible to construct such a function (the consequences of this impossibility will be discussed at the end of this section). A simple case where such a construction is possible, for example, is the binary choice situation where , and where the utilities take the following form:

| (51) |

with an arbitrary symmetric matrix. In this case, one can check by inspection that is given by:

| (52) |

One sees on this example that is not the sum of individual utilities. In fact:

| (53) |

The difference between these two quantities can have important consequences, as pointed out in the beautiful paper of Grauwin et al. Grauwin . They consider a variant of the Schelling model of segregation, where each agent is sensitive to the density of the neighbourhood in which he/she is living. Agents do not like living in derelict neighbourhoods () nor in overcrowded neighbourhoods (). Their incentive to live in a neighbourhood situated around is a certain function that has a maximum at ; for example and . The global utility is a functional of the density field and is given by:

| (54) |

where is the linear size of the city. Suppose that the size of the population is such that . It is in principle possible in this case to make everybody happy and reach the absolute maximum of the global utility of the population by having all neighbourhoods at , in which case , with .

Now, what will really happen if agents choose their neighbourhood based on their own utility? More precisely, let us assume that each agent can move from to with a probability given by the logit-rule, i.e.:

| (55) |

The function alluded to above is also a functional of , and according to the general principle expressed by Eq. (47), it should be such that, for all fields :

| (56) |

where we have assumed that the elementary area of a neighbourhood is normalized to one. The solution is:

| (57) |

where is an arbitrary constant. Therefore, unless is a constant, independent of (i.e. for non interacting agents), .

Now, the equilibrium probability is given by the Boltzmann-Gibbs measure: 252525We neglect here an entropic term, which is small when , see Grauwin for details.

| (58) |

with and is a Lagrange parameter ensuring that the average density is fixed to a certain . The most likely density configuration, for , is such that , . For the above symmetric piecewise linear choice for , one finds that the local density must be equal to with probability , and with probability , with such that , and such that:

| (59) |

is maximized. In the case where , the maximum is realized for , and when , it is realized for , but both solutions correspond to complete segregation, i.e. completely full () or completely empty () neighbourhoods! (The case where is degenerate, but any infinitesimally small departure from this case leads to segregation). Therefore, letting people optimize their own utility, to the detriment of the global well-being, leads to a disastrous situation. This is a stunning illustration of a case where Adam Smith’s invisible hand totally fails to bring the society to a global optimum.

Now, as proposed in Grauwin , coordination can be improved by making individuals conscious of the common good when they make their choice, by adding to the change of individual utility a term proportional to the extra cost in the global utility, i.e. change the logit-rule according to:

| (60) |

Since is already a functional of the density field, one can immediately see that the function adapted to the new choice update rule is given by:

| (61) |

Correspondingly, the equilibrium probability is now replaced by:

| (62) |

The most likely configuration can again be computed. One finds that it becomes the socially optimal solution and as soon as . As stressed by Grauwin et al., this model shows that the optimization strategy based on purely individual dynamics fails, illustrating the unexpected links between micromotives and macrobehavior. Making individuals aware of the costs of their choice for the society is, in some cases, useful to nudge the system into cooperation/coordination Nudge .

Note that the results of Grauwin et al. hold provided the decision rules obey detailed-balance. However, detailed-balance is, in the general case of interacting agents, the exception rather than the rule. Very few general results are known when detailed-balance is violated, see e.g. Jona-Lasinio ; CK ; Biroli , see also Burioni in the present context. Of course, some equilibrium will be reached after a long time, but there is no explicit construction of the equilibrium probability, similar to Eq. (49) above. One knows that in the general case, equilibrium currents are present. This is due to the fact that the probability to cycle ‘clockwise’ around a closed loop in decision space is different from the probability to cycle ‘counter-clockwise’ – except when detailed-balance is satisfied. Studying and interpreting these currents in a socio-economic context would be very interesting, in particular because these currents are known to considerably speed up the equilibration time in certain cases SG_asym ; CK , preventing the system from getting “trapped” in deep maxima of the function (the equivalent of deep energy wells in physics). For example, a natural extension of the model of Grauwin et al. that would exhibit equilibrium currents and (perhaps ?) mitigate segregation, would be quite appealing.

VII Imitation of the past and more instabilities

VII.1 Memory & Habit formation

Any realistic model of decision should in fact take into account that the utility/incentive of a given choice cannot be thought of as time independent. For example, it is hard to know how useful or interesting choice is without having tried it at least once (think about restaurants, for example). A simple way to model this would be to to assume that the perceived utility of choice , , is initially blurred by some estimation error that decays to zero as the total time spent choosing grows; for example YS :

| (63) |

where is the fraction of the time during which was chosen. In effect, this should be similar to having an effective parameter that increases over time. This is the equivalent, in physics, of an annealing process where the temperature slowly decreases with time.

As the relative utility of choices becomes better known to agents as time evolves, a second, more important effect might kick in: habit formation or “stickiness”. Often, past choices become more valuable only because they happened to be chosen. This can be for good reasons, like creating a loyalty relationship (such at the Marseilles fish market Kirman_fish ; WKH ), or because going to the same doctor makes that doctor know your personal problems better, etc. But it can also be because of high risk aversion (maybe another choice is better, but maybe it is much worse, so better stick to what I have) or sheer intellectual laziness. Hotel and restaurant chains are based on this strong universal principle: people often tend to prefer things they know.

This can be formalized as follows: define an indicator function , which is equal to if choice is made at time , and zero otherwise. The utility of choice at time for a given agent is written as:

| (64) |