1 Introduction

A popular assumption in the valuation of financial options

via the numerical solution of partial differential equations

(PDEs) is the so-called linear boundary condition,

see, for example, [1, 10, 13, 14].

The linear boundary condition states that the second derivative

of the option value with respect to the underlying asset price

vanishes if the asset price gets large.

This condition represents a linear behavior of the option value

for large

asset prices, which can be seen to hold for a wide variety of

financial options.

In spite of its broad use in practice, only few rigorous

results have been derived in the literature up to now on the

stability and convergence of numerical discretizations if

the linear boundary condition is applied.

As it turns out, in the finite difference (FD) approach a

natural treatment of the linear boundary condition leads to

a downwind discretization of the advection term at

the relevant grid point; the details of which are given below

in this section.

Consequently, in the actual numerical solution one might

expect instability, or at least an adverse effect on the

convergence behavior.

It appears, however, that this is not observed in practice.

To our knowledge, the only theoretical stability

analysis in the literature up to now pertinent to the linear

boundary condition has been performed by Windcliff, Forsyth

& Vetzal [14].

These authors proved that for a common discretization of the

Black–Scholes PDE a necessary eigenvalue condition

for stability holds.

The objective of the present paper is to arrive at useful

sufficient conditions for stability and convergence

of discretizations when the linear boundary condition is

employed.

As far as we are aware, such conditions are lacking in the

current literature, but

they are clearly of much interest.

Consider the Black–Scholes PDE

|

|

|

(1.1) |

where and are given real constants that

denote the risk-neutral interest rate and the volatility,

respectively, and is the given maturity time of the

option.

The exact solution represents the

fair value of an option

if the underlying asset price equals at time .

For the numerical solution, one restricts in practice the

-domain to a boun-ded set

with fixed chosen sufficiently large.

The PDE (1.1) is complemented with initial and

boundary conditions.

In this paper, we consider at

the linear boundary condition

|

|

|

(1.2) |

At the lower boundary a standard Dirichlet condition is

taken,

which depends on the particular option.

The initial condition is given by the payoff of the option.

FD discretization of the initial-boundary value problem

for (1.1) on a general (non-uniform) grid

, with

mesh widths , leads to an initial value

problem for a system of ordinary differential equations

(ODEs),

|

|

|

(1.3) |

Here denotes a given real –matrix

and and , for , are given real

–vectors.

The vector is

directly given by

the payoff function

and depends on the Dirichlet condition at .

In this paper we

shall

deal with matrices of the form

|

|

|

|

|

(1.6) |

|

|

|

|

|

(1.14) |

where , , denote given real numbers.

The

–matrix

represents a natural discretization of the linear boundary

condition

(1.2).

It is determined

by the following approximations at the

grid points and :

|

|

|

(1.15) |

As in (1.1) is positive, the

approximation of

forms an upwind scheme at , but the same

approximation constitutes a downwind scheme at .

The latter

approximation

can be regarded as obtained from the second-order

central scheme for advection at with virtual point

and then replacing

by in view of the linear

boundary condition.

The discretization (1.15b) at

is identical to the one considered in [14].

The discretization (1.15a) at , on the

other hand,

appears to be new.

In particular, we approximate by zero at this point

instead of using the

standard second-order central scheme for diffusion.

The choice (1.15) yields a partial

decoupling between the FD solution at the grid points

and that at .

Concerning

the discretization on we make no assumptions

yet,

except that at each relevant grid point the stencil

belongs to – hence the structure

of the matrices and in (1.6).

The discretization (1.15) of the linear

boundary condition (1.2)

might be interpreted

as a Dirichlet-type condition, since the relevant subsystem

of ODEs involving the matrix is easily solved exactly

(cf. (2.3) below).

We

emphasize,

however, that the objective of this paper concerns

comparing the numerical solution to the exact solution of

the Black–Scholes PDE with the linear boundary condition

(1.2) at the upper boundary , and

not with a Dirichlet condition.

As it turns out, the analysis in the present situation, of

(1.2), encounters a variety of additional difficulties.

Our analysis commences with an investigation of the stability

of the FD discretization (1.3), (1.6).

This pertains to the derivation of rigorous bounds on the

norm of the matrix exponential .

We shall deal here with the maximum norm.

By and we denote the

maximum norm of real vectors and matrices, respectively.

An important tool is the logarithmic maximum norm,

which is defined for any square matrix by

|

|

|

where is the identity matrix of the same size as .

Upon writing a convenient formula

for the logarithmic maximum norm is

|

|

|

(1.16) |

A key property is given by the following theorem;

see e.g. [3, 7, 9, 11].

Theorem 1.1

Let . Then:

We note that we previously used the logarithmic norm in

analyzing the stability of discretizations of the

Black–Scholes and Heston PDEs when provided with

Dirichlet boundary conditions, see [5, 6, 12].

An outline of the rest of the paper is as follows.

In Section 2 we investigate the stability of

general semidiscretizations (1.3), (1.6)

of the Black–Scholes PDE with the linear boundary condition.

We

prove sharp upper and lower bounds for .

In Section 3 various well-known FD discretizations are

considered. For each discretization a practical sufficient

condition

is

obtained

such that the stability result of Section 2 holds.

In Section 4 we

derive a convergence estimate for

general semidiscretizations (1.3), (1.6)

of the Black–Scholes PDE with the linear boundary condition.

In Section 2 it was found that

is essentially inversely proportional to the mesh width

.

We prove however the positive result that this growth,

as tends to zero, generally

has no adverse effect on the convergence behavior.

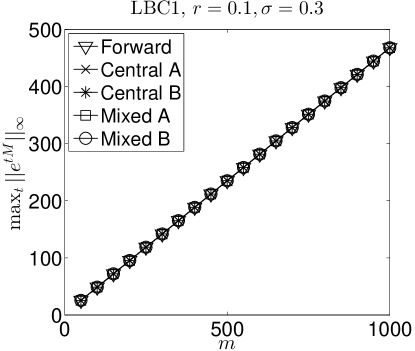

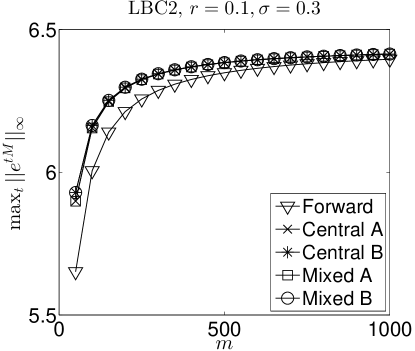

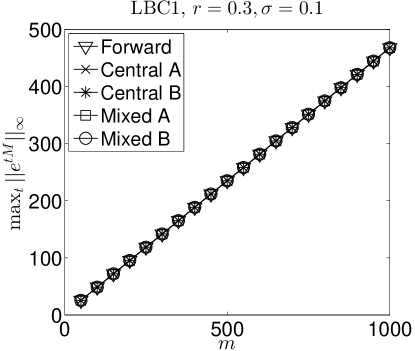

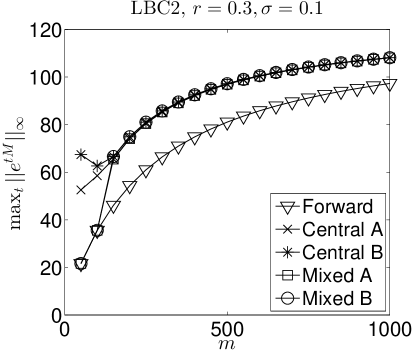

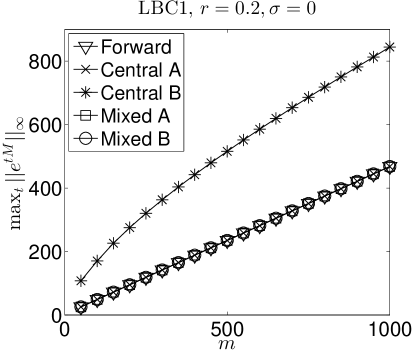

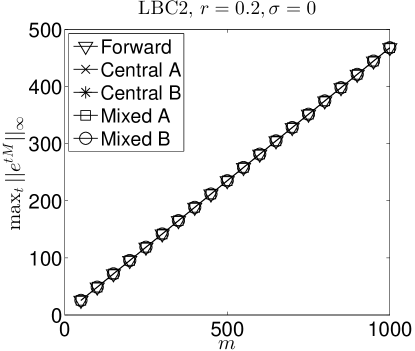

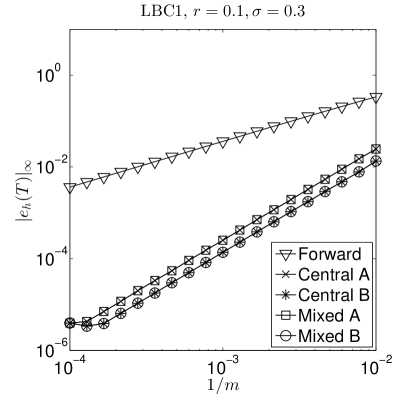

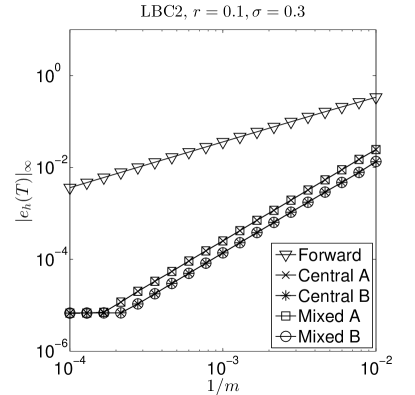

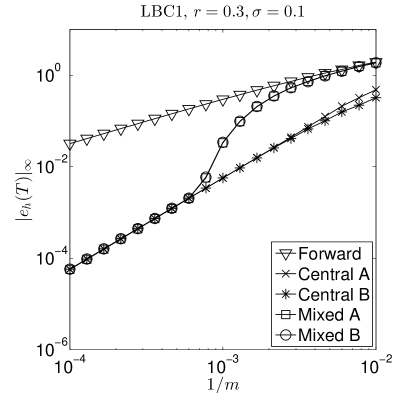

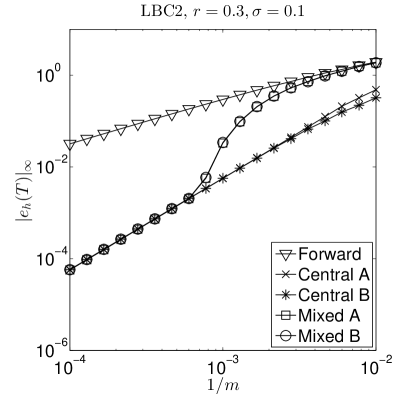

In Section 5 extensive numerical experiments

are presented regarding the stability and convergence

results of Sections 2, 4.

In Section 6 we consider the discretization

in time and prove stability and convergence results for

the popular family of -methods.

These results can be

regarded as

analogues of those obtained for the semidiscretization.

In Section 7 conclusions and issues for future

research are given.

2 A general stability theorem

In this section we consider general matrices of the form

(1.6) and derive a useful inclusion for the maximum

norm of for .

We start with three lemmas.

Lemma 2.1

It holds that

|

|

|

Proof

Consider the system of ODEs

|

|

|

with solution given by

|

|

|

(2.1) |

Let the vector be splitted into two parts,

|

|

|

where is an –vector and is a 2–vector.

In view of (1.6) one has

|

|

|

Thus and

|

|

|

|

|

|

|

|

|

|

|

|

Comparing with (2.1), the result of the lemma is obtained.

The next lemma gives the maximum norm of .

Lemma 2.2

It holds that

|

|

|

(2.2) |

Proof

The two eigenvalues of are and with corresponding eigenvectors

and .

Thus

|

|

|

which gives

|

|

|

(2.3) |

Hence,

|

|

|

It is readily seen that

|

|

|

Therefore,

|

|

|

Lemma 2.2 shows that for any given the

maximum norm of is essentially inversely proportional to

the mesh width .

The growth of as decreases corresponds

to the fact that at the grid point a downwind scheme is used

for the advection term in the Black–Scholes PDE.

Let denote the –dimensional unit vector

.

Lemma 2.3

If is invertible, and

, then

|

|

|

Proof (i) Consider first .

Define , i.e., .

Writing this gives

the system of equations

|

|

|

We prove by induction that .

In view of (1.16), the assumptions on imply that

all and .

Using this, yields

|

|

|

Next suppose for some .

We show that .

By (1.16) there holds

and consequently

|

|

|

We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This proves the induction step, and it follows that

.

Subsequently,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where it is used that .

Since the bound of the lemma

is obtained.

(ii) Consider next .

Define the matrix with .

There holds and thus we can

apply the result from part (i):

|

|

|

Taking the limit in this inequality

completes the proof.

The following theorem is the first main result of this paper.

It provides a tight inclusion of the maximum norm of

for matrices of the form (1.6) and reveals

that this norm is essentially inversely proportional to .

Theorem 2.4

If

|

|

|

(2.4) |

then

|

|

|

(2.5) |

Proof

We employ the formula for given by Lemma 2.1.

First, it is clear that

and by Lemma 2.2 the lower bound is directly obtained.

To prove the stated upper bound, we consider the maximum norm of

|

|

|

Using formula (2.3), it is readily shown that

|

|

|

(2.6) |

For any given real numbers , consider the

vector

|

|

|

A straightforward computation yields

|

|

|

Note that means .

In view of this and the assumptions of the theorem it holds

that both and are invertible and, by Theorem

1.1,

|

|

|

(2.7) |

Consequently, we have the bound

|

|

|

Now let represent any column vector of

. It is clear from (2.6) that

|

|

|

If , then the result of the theorem is

obvious; in fact

in this case.

Thus assume .

Then and application of Lemma

2.3 to both and yields

|

|

|

Since

|

|

|

it follows that

|

|

|

Using that has two columns, we arrive at the bound

|

|

|

(2.8) |

Finally, in view of Lemma 2.1,

|

|

|

By invoking (2.7), (2.8) and Lemma 2.2, the

upper bound of the theorem is obtained.

In Section 3,

applications of Theorem 2.4 to

various actual FD discretizations of the Black–Scholes PDE with

the linear boundary condition shall be discussed.

In Section 4 the stability results from the present

section shall

effectively be used

in the convergence analysis of FD discretizations.

In subsequent applications of Theorem 2.4 the

following lemma is useful.

Lemma 2.6

If satisfies the conditions

|

|

|

then is invertible and .

Proof

The conditions of the lemma directly

imply, by (1.16), that .

We

next show that is invertible.

Upon setting and

and

using that we obtain

|

|

|

|

|

|

Next, modify the matrix by subtracting column 1 from

columns .

This leads to

|

|

|

Clearly, if is invertible, then so is .

We prove that

|

|

|

Write . Then

is equivalent to the system of equations

|

|

|

(2.9) |

We distinguish three cases.

(a) Assume whenever .

Then , , for all .

Starting with the last equation of (2.9) and moving upwards,

one finds that

|

|

|

Substituting this into the first equation of (2.9) yields

|

|

|

It is easily seen that the coefficient of in the latter equation

is nonzero.

Thus , and consequently .

(b) Assume . Since and all

are nonzero, (2.9) directly yields that .

(c) Assume for certain .

This induces a natural partitioning of the matrix where each

diagonal block belongs to either case (a) or case (b) above.

Using this, it readily follows that if then .

4 A general convergence result

In this section we

prove a convergence result for general semidiscretizations

(1.3), (1.6) of the Black–Scholes PDE

with the linear boundary condition.

Let be the exact solution to (1.3),

(1.6) and, for , let

be the vector of the same size as given by

|

|

|

where is the exact solution to the initial-boundary

value problem for the Black–Scholes PDE (1.1) on

with linear boundary condition (1.2).

Define the spatial discretization error

|

|

|

and the spatial truncation error

|

|

|

A

standard approach to estimate spatial discretization

errors is to combine an estimate for the spatial truncation

errors with a stability bound, cf. e.g. [7].

However, a direct use of the bound on

from Theorem 2.4 does not lead to an optimal

result.

To obtain a useful result in the present situation where

the linear boundary condition is employed, we consider a

partitioning of the spatial truncation error vector into

two parts, corresponding to the intervals and

:

|

|

|

Using

the

individual stability bounds derived in Section 2,

we have as a preliminary result

Lemma 4.1

Assume (2.4) holds.

Then the spatial discretization error satisfies

|

|

|

Proof

From

|

|

|

|

|

|

|

|

|

|

one has

|

|

|

and, since ,

|

|

|

Lemma 2.1 yields

|

|

|

By (2.7), (2.8) and Lemma 2.2 the

following bounds hold whenever :

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Hence

|

|

|

Together with the integral representation above, this

gives the bound on the maximum norm of .

The following theorem forms the second main result of this

paper.

It gives a useful convergence estimate for general

semidiscretizations (1.3), (1.6)

of the Black–Scholes PDE with linear boundary condition.

Its

proof is obtained by combining Lemma 4.1 with

a bound for .

Theorem 4.2

Let be given and assume that on

the partial derivative exists and is continuous.

Define

|

|

|

(4.1) |

Assume (2.4) holds.

Then the spatial discretization error satisfies

|

|

|

Proof Write and .

Pertinent to the point we have

|

|

|

|

|

|

|

|

|

|

By Taylor’s theorem and using there

follows

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where

|

|

|

with certain in .

Substitution into the above formula yields

|

|

|

which readily leads to the estimate

|

|

|

Analogously, pertinent to the point , there holds

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

It thus follows that

|

|

|

and

|

|

|

(4.2) |

Application of Lemma 4.1 then gives the desired

estimate for .

The estimate of Theorem 4.2 for the spatial

discretization error consists of two contributions,

corresponding to the two intervals and

.

The first contribution is equal to the part of the spatial

truncation error pertinent to .

For any given FD discretization this can be estimated in a

standard way by Taylor expansion.

The second contribution is equal to

and depends on the partial derivative of the exact

option price near .

For a wide range of financial options it is plausible that

this contribution can be made arbitrarily small upon taking

the upper bound sufficiently

large (in the case of European call and put options this is

readily proved).

Theorem 4.2 thus expresses the useful result

that the contribution to spatial discretization error of the

semidiscretized linear boundary condition is

negligible, provided is sufficiently large.

Key to the proof is that the stability bounds derived in

Section 2 admit a growth of errors from the interval

that is at most inversely proportional to

but this growth is precisely offset by the factor

that arises in the part of the spatial truncation

error pertinent to this interval.

We note that

in Theorem 4.2 it is tacitly assumed

that the initial function is smooth, which has been

used for ease of

the analysis, but is often not fulfilled in

applications.

The numerical experiments in the subsequent section deal

with a nonsmooth initial function.

6 Time discretization

In this section we study the time discretization of

the semidiscrete system (1.3), (1.6)

by the well-known family of -methods, which

includes the popular Crank–Nicolson method (trapezoidal

rule) and implicit Euler method as special cases.

As noted in Section 1, the subsystem of

ODEs involving the matrix could be solved exactly,

but it is more interesting and useful, both from a

theoretical and practical point of view, to consider

the time discretization of the semidiscrete system

(1.3), (1.6) as a

whole.

Let parameter be given

and fixed.

Let step size with integer be

given and define ,

for .

The -method generates, in a successive way,

for an approximation to by

|

|

|

The choices and yield,

respectively, the Crank–Nicolson method and implicit

Euler method.

The above recurrence relation can be written as

|

|

|

(6.1) |

where is the so-called stability function of the method,

given by

|

|

|

and

|

|

|

for square matrices such that is invertible.

We first study the stability of the fully discrete process

(6.1).

The

subsequent two lemmas can be viewed as analogues of Lemmas

2.1, 2.2 for the semidiscrete

system.

Lemma 6.1

For there holds

|

|

|

where

|

|

|

(6.2) |

Proof

The formula is readily obtained by induction to and noting that

|

|

|

(6.3) |

Lemma 6.2

For there holds

|

|

|

Proof With the eigendecomposition of it is easily

verified that

|

|

|

and the rest of the proof is similar to that of

Lemma 2.2, using

.

Concerning the discretization on the spatial domain

we shall

assume

in the following that there exists a real constant ,

independent of the dimension and number of

time steps , such that

|

|

|

(6.4) |

In the literature much attention has been paid to

establishing (6.4), under a variety

of conditions on the matrix .

For the implicit Euler method () the neat

result is well-known that (6.4) is

fulfilled with whenever ,

cf. e.g. [4, 8].

Hence, this is guaranteed under the condition (2.4).

For all other time discretization methods, however,

the available results in the literature

implying

(6.4) with a constant

independent of and require, to the best

of our knowledge, stronger conditions on .

Notably, conditions on the resolvent, the numerical

range and

pseudospectra have been extensively

investigated in the literature,

cf. e.g. [9, 11].

Some of these results appear to be useful in our

current application,

but a verification of the

pertinent

conditions

on

is highly non-trivial.

As our main interest in this paper lies in

studying (the implications of) the discretized

linear boundary condition

on ,

which corresponds to the matrices

and , we shall leave the analysis of

(6.4) when

for future

research.

The next theorem can be regarded as a discrete analogue

to Theorem 2.4.

Theorem 6.3

If (2.4) and (6.4)

then for ,

|

|

|

with .

Proof

For any integer , let the rational

function be defined by

|

|

|

Consider the formula for

given by Lemma 6.1.

The lower bound on its maximum norm is clear by

Lemma 6.2.

To prove the upper bound, write

|

|

|

|

|

|

|

|

|

|

It holds that

|

|

|

(6.5) |

where .

Both columns of this matrix are of the form

|

|

|

with real numbers , independent of .

We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

By similar algebraic manipulations, there follows

|

|

|

|

|

|

Consequently,

|

|

|

(6.6) |

|

|

|

Continuing from here along the same lines as in the proof of

Theorem 2.4, and using the condition (6.4),

we arrive at

|

|

|

Together with Lemma 6.2, the stated upper

bound on now directly

follows.

In the subsequent convergence analysis of the process

(6.1), the matrix

|

|

|

arises.

By Lemma 6.1 and formula (6.3),

|

|

|

For the analysis below we need upper bounds on

the maximum norms of the constituent submatrices.

Putting , there holds

Lemma 6.4

If (2.4) and (6.4)

then for ,

|

|

|

(6.7) |

Proof The bound (6.7a) follows directly from

(6.4) and the fact that (2.4) implies

.

The bound (6.7b) is obtained using the same arguments

as in the proof of Lemma 6.2.

In order to prove (6.7c) we note that

|

|

|

and using this gives

|

|

|

(6.8) |

By (6.5) with ,

|

|

|

where .

If represents any of the two columns of this matrix,

then by a same argument as in the proof of Theorem

2.4 there follows

|

|

|

Consequently,

|

|

|

The proof of the bound (6.7d) is identical to that for

given above, except that needs to

be replaced by .

To prove the convergence result for the time discretization

process (6.1), we also need the following result.

Lemma 6.5

Assume (2.4) and (6.4)

hold.

Let be any given continuously

differentiable function and

|

|

|

Then there exists such that

for all :

|

|

|

(6.9) |

Proof Write and .

Let be such

that

|

|

|

Then the vector can be written as

|

|

|

For any rational function with there

holds

|

|

|

where .

Application of this matrix to , in the above form,

readily yields

|

|

|

Observe the important fact that there is no factor present here.

(a) The bound (6.9a) is obtained upon taking

and using .

(b) By formula (6.8),

|

|

|

Considering yields

|

|

|

with .

As in the proof of Theorem 2.4 we have

and,

together with , there follows

|

|

|

which completes the proof of (6.9b).

(c) By formula (6.2),

|

|

|

with .

Taking in the above general formula,

we get

|

|

|

where

|

|

|

It is convenient to set and

.

Then

and formula (6.6) directly gives

|

|

|

|

|

|

|

|

|

Using that and

yields

|

|

|

|

|

|

|

|

|

|

which proves the bound (6.9c).

As in Section 4,

let the vector be given by

|

|

|

where is the exact solution to the initial-boundary

value problem for the Black–Scholes PDE (1.1) on

with linear boundary condition (1.2).

The following theorem provides a useful estimate for

the space-time discretization error, defined by

|

|

|

It essentially states that the estimate for the spatial

discretization error from Theorem 4.2 remains

valid after time discretization up to a

term, where denotes the classical order of consistency

of the -method and is a constant independent

of the spatial grid and the time step.

Theorem 6.6

Let if and if

.

Assume that all partial derivatives of of orders

exist and are continuous on .

Let be given and let , be defined

by (4.1).

Assume (2.4) and (6.4) hold.

Then there exists a real constant (depending only on ,

, and ) such that

|

|

|

whenever , , ,

.

Proof Let the local space-time error in the -th

step of (6.1) be defined by

|

|

|

Subtracting (6.1) from this yields

|

|

|

(6.10) |

With the spatial truncation error

|

|

|

as defined in Section 4, one can express as

|

|

|

Inserting this into the definition of it readily

follows that

|

|

|

(6.11) |

The above formula for consists of two terms,

corresponding to the truncation error in space and the

truncation error in time.

In view of (6.10), we shall study

.

Concerning the first term, the bounds for the submatrices

of

given by Lemma 6.4 directly lead to

|

|

|

|

|

|

|

|

|

Invoking the estimate (4.2) for

this gives

|

|

|

|

|

|

|

|

|

where .

Concerning the second term, for the function

defined by

|

|

|

standard Taylor expansion shows that

|

|

|

with

|

|

|

|

|

|

where designates the maximum norm of

a real function on .

Using now Lemma 6.5 and the partitioning

|

|

|

it follows that

|

|

|

with

|

|

|

Combining the above bounds, we are led to

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|