An intermediate distribution between Gaussian and Cauchy distributions

Abstract

In this paper, we construct an intermediate distribution linking the Gaussian and the Cauchy distribution. We provide the probability density function and the corresponding characteristic function of the intermediate distribution. Because many kinds of distributions have no moment, we introduce weighted moments. Specifically, we consider weighted moments under two types of weighted functions: the cut-off function and the exponential function. Through these two types of weighted functions, we can obtain weighted moments for almost all distributions. We consider an application of the probability density function of the intermediate distribution on the spectral line broadening in laser theory. Moreover, we utilize the intermediate distribution to the problem of the stock market return in quantitative finance.

Keywords: intermediate distribution; Gaussian distribution; Cauchy distribution; q-Gaussian distribution; weighted moment; spectral line broadening; stock market return

1 Introduction

In statistics, the Gaussian distribution is a standard distribution satisfying the central limit theorem; the Cauchy distribution, also called the Lorentzian distribution, however, typically fails to be tamed by the central limit theorem [1]. In the meantime, these two kinds of distributions both belong to infinitely divisible distributions [2, 3, 4]. They have some similarities, such as unimodality, symmetry and the same domain of definition. Such similar properties are so attractive that stimulate one to find an intermediate distribution to link up the Gaussian and the Cauchy distribution. The Student-t distribution [5] is the first distribution that realizes the purpose linking the two distributions. Nevertheless the Student-t distribution is not the unique one. In this paper, we provide another kind of distribution linking the Gaussian and the Cauchy distribution.

First, we introduce an intermediate distribution which can reduce to the Gaussian and the Cauchy distribution at some certain values of a parameter. Second, instead of conventional moments, we consider the weighted moment of a distribution. Many distributions have no moments since the moment of such distributions diverges. To seek moments, a weighted moment is introduced. By the weighted moment, rather than the conventional moment, one can calculate the moment in almost all kinds of distributions, such as Gaussian, Cauchy, and Student-t distributions and the distribution provided in the present paper. Third, we give two applications of the intermediate distribution: one is in laser theory and the other is in quantitative finance.

Specifically, as is well known, each probability density function (PDF) corresponds a characteristic function uniquely through a Fourier transformation [6, 7, 8], which enlightens one to construct a PDF starting from a characteristic function. From this viewpoint, we provide a distribution that bridges the gap between the Gaussian and the Cauchy distribution by analyzing their characteristic functions in this paper.

Next, we introduce a weighted moment, because the conventional moment fails to converge in many distributions [6], e.g., the Cauchy distribution does not have conventional moments. Nevertheless, the moment is one of the most important concepts in statistics. Many properties are reflected by each order moment, such as deviations and variances. If a distribution does not have moments, it makes difficulties to discuss the properties described by the moment. Therefore, we consider the weighted moment to overcome such a defect. We, specifically, discuss two types of weighted moments in this paper.

When considering complex systems, the concept of generalized distribution is widely discussed. An important generalization of the Gaussian distribution is the Tsallis distribution [9, 10, 11] (the Student-t distribution mentioned above is a special case of the Tsallis distribution). Recent researches show that a dissipative optical lattice system will display the Tsallis distribution [12]. In quantitative physics, it is shown that one can construct stock price models based on the Tsallis distribution [13]. In addition, some other kinds of generalized statistics and the applications are also discussed in the literature [14, 15].

Furthermore, we suggest an application of the intermediate distribution on spectral line broadening in laser theory. The homogeneous broadening due to collisions and spontaneous emissions is approximated by the Cauchy distribution, and the inhomogeneous broadening due to Doppler effects is approximated by the Gaussian distribution [16]. Since the two kinds of broadenings exist simultaneously, we suggest to use the intermediate distribution to describe the spectral line broadening. In general, a realistic system always cannot be exactly described by an ideal theoretical model. Therefore, some intermediate models are suggested to describe complex systems. For example, it is found that a magnetic system obeys a kind of intermediate statistics rather than Bose-Einstein statistics [17]. Moreover, some composite particles composed of some fermions may behave like bosons and obey Bose-Einstein statistics when they are far from each other; when they come closer together, however, the fermions in the composite particles can feel each other, and the statistics of the composite particles will deviate from exact Bose-Einstein statistics [18]. Such a composite-particle system will obey a certain kind of intermediate statistics. For this reason, some intermediate theories are considered [19, 20, 21, 22].

At last, we apply the intermediate distribution to describe the stock market return in quantitative finance. The stock market return is the return that we obtain from stock market by buying and selling stocks or get dividends by the company whose stock you hold. Stock market returns include two parts: capital gain and dividend income. In the Black-Scholes stock option pricing model [23] and the capital asset pricing model (CAPM) [24, 25, 26], the stock market price is assumed to follow lognormal distribution, which means that stock market returns follow the Gaussian distribution. Nevertheless, in real world, stock market returns disobey the Gaussian distribution. The characteristics of stock market return distribution is sharp peak and fat tails. The intermediate distribution can fit the stock market return better than the Gaussian distribution. Moreover, in the fitting results, we also compare the intermediate distribution with the q-Gaussian distribution, which generalizes the Gaussian distribution in statistics [27]. The distribution of the stock market return plays a fundamental role in pricing theory. Based on the intermediate distribution, we can price the stock price and the option in line with the realistic.

The structure of this paper is as follows. In section 2, an intermediate distribution linking the Gaussian and the Cauchy distribution is constructed. In section 3, the weighted moment and some properties of the moment are discussed. In section 4, a function is introduced to link the intermediate and the Gaussian distribution smoothly. In section 5, an application of the intermediate distribution to spectral line broadening in laser theory is discussed. In section 6, the intermediate distribution is utilized to fit the probability density function with respect to the stock market return. The conclusion and outlook are given in Section 7.

2 The Construction of the intermediate distribution

In this section, we introduce an intermediate distribution. The PDF of the intermediate distribution is

| (1) |

and the corresponding characteristic function is

| (2) |

Such a distribution will recover the Gaussian and the Cauchy distribution when and , respectively.

In the following, we deduce the PDF and the corresponding characteristic function in detail.

2.1 The characteristic function of the intermediate distribution

At the earliest, the unique general formula for any characteristic function of infinitely divisible distribution with finite variance was found by Kolmogorov. Levy and Khintchine generalized Kolmogorov’s result and discovered the famous Levy-Khintchine formula [4, 6, 8, 28]. The Levy-Khintchine formula is also valid to all infinitely divisible distributions.

According to the Levy-Khintchine formula, all characteristic functions of infinitely divisible distributions can be represented by [4, 6, 8, 28]

| (3) |

where is a real constant and is a real, bounded, and nondecreasing function of . Different ’s generate different distributions.

What we want to do is to introduce a function linking Gaussian and Cauchy distributions. We construct the function as

| (4) |

Obviously is a real, bounded, and nondecreasing function of from to . Because satisfies the requirements of the Levy-Khintchine formula, it corresponds to a characteristic function of a certain distribution. The function recovers the characteristic functions of Gaussian and Cauchy distributions when and , respectively:

| (5) |

| (6) |

where is the step function. In this paper, the intermediate distribution is generated from in Eq. (4).

2.2 The PDF of the intermediate distribution

Now, we deduce the PDF of the intermediate distribution corresponding to the characteristic function given by Eq. (2).

Facilitating the inverse Fourier transformation, we rewrite as

| (12) |

Then, performing the inverse Fourier transformation to gives

| (13) |

where is the generalized incomplete gamma function. Here is a real function of , because the two parts in the braces are complex conjugate and can be rewritten as a manifest real form as Eq. (1).

When and , the intermediate distribution given by Eq. (1) reduces to the Gaussian distribution

| (14) |

and the Cauchy distribution

| (15) |

respectively.

3 The weighted moment

In this section, we introduce weighted moments and discuss their behaviors.

The reason why we consider the weighted moment is that the conventional moment diverges in many distributions, such as the Cauchy distribution. To obtain and compare the moment between different distributions, we introduce the weighted function to seek a convergent moment. A parameter is used to adjust the weighted function. When the parameter takes a certain value, the weighted function reduces to and coincides with the conventional one. Specifically, we discuss the weighted moment with the cut-off weighted function and the exponential weighted function.

The moment is one of the essential concepts in statistics. It is because that the even order moment, especially the second order moment, reflects the deviation of a quantity that is estimated. It is inconvenient for us to analyze the deviation of this quantity that a distribution does not have the even order moments. Moreover, the mean value of a quantity can be expanded as a series of the moments since the quantity can be technically expanded as a power series.

3.1 The moment and the weighted moment

In this section, we introduce the weighted moment.

The central moment in statistics is defined as

| (16) |

Note that one also considers another kind of moment, the origin moment with , in statistics. We can easily find that the value of the origin moment depends on the central site of the distribution, while the central moment is independent on the site . Thus, the central moment is more natural than the origin moment. We will only discuss the central moment in this paper.

If is an even function, the Cauchy principal value of the odd order moments vanishes

| (17) |

The even order moment reads

| (18) |

The Gaussian distribution has all even order central moments:

| (19) |

where is the Euler gamma function. As is well known, the Cauchy distribution, however, does not has central moments. The intermediate distribution given by Eq. (1), like the Cauchy distribution, has no central moments. The -th moment of Eq. (1)

| (20) |

diverges, because the integral does not converge on .

In order to find a quantity to play the role of moments to the distribution which does not have moments, we define a weighted moment as

| (21) |

by introducing a symmetrical weighted function . Since and are symmetrical, the Cauchy principal value of the odd order moments vanishes, and, then, only the even order moment

| (22) |

needs to be considered.

In the following, we consider two weighted functions.

3.2 The weighted moment with the cut-off weighted function

In this section, we consider a cut-off weighted function,

| (23) |

The even order weighted moment with the weighted function (23) is then

| (24) |

which reduces to the moment Eq. (16) when .

Finally, we can obtain the cut-off weighted moments, .

The weighted moment of the intermediate distribution:

| (25) |

Here, , , is the generalized hypergeometric function, and the integral

| (26) |

is used.

The weighted moment of the Cauchy distribution:

| (27) |

The weighted moment of the Gaussian distribution:

| (28) |

When , the cut-off weighted moment of the Gaussian distribution reduces to the moment Eq. (19).

3.3 The weighted moment with the exponential weighted function

In this section, we consider the exponential weight function defined as

| (29) |

The even order weighted moment with the weighted function (29) is then

| (30) |

which reduces to the moment Eq. (16) when .

Finally, we obtain the exponential weighted moments, .

The weighted moment of the intermediate distribution:

| (31) |

The weighted moment of the Cauchy distribution:

| (32) |

The weighted moment of the Gaussian distribution:

| (33) |

When , the weighted moment of the Gaussian distribution reduces to the moment Eq. (19).

4 An alternative construction of the intermediate distribution

In this section, we suggest another construction of the PDF of the intermediate distribution, which links the intermediate distribution and the Gaussian distribution smoothly.

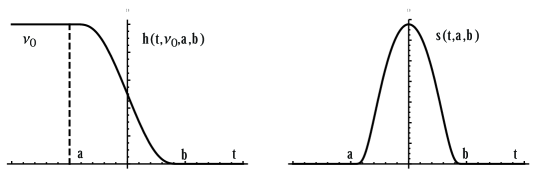

In the PDF of the intermediate distribution, Eq. (1), the points is a removable singularity. According to the analysis in the above section, the behavior of the moment depends on the value of the parameter . The distribution have no moments unless so that the intermediate distribution, Eq. (1), reduces to the Gaussian distribution. What we want to do is to seek a certain way that when the parameter runs smoothly from a constant to , the distribution travels smoothly from the intermediate distribution to the Gaussian distribution. Especially, when , the distribution will travel smoothly from the Cauchy distribution to the Gaussian distribution.

Specifically, we insert a smooth function into the PDF of the intermediate distribution, Eq. (1), and then have

| (34) |

where the function is [29, 30]

| (35) |

with , and

| (36) |

The figures of and are shown in Figure 1.

When , , and the PDF Eq. (34) reduces to the Gaussian PDF. When and , , the PDF Eq. (34) reduces to the Cauchy PDF. When runs from to , the distribution travels from the intermediate distribution to the Gaussian distribution smoothly. Especially, when , the distribution travels from the Cauchy distribution to the Gaussian distribution.

5 Application to the problem of the spectral line broadening in laser theory

In this section, we apply the intermediate distribution introduced in the present paper to the spectral line broadening in laser theory.

In laser theory, the spectral line broadening is a phenomenon due to photons emitted or absorbed in a narrow frequency range. The spectral line broadening of laser can be approximated by a distribution. The Cauchy distribution and Gaussian distribution are often used to describe the broadening: the Cauchy distribution is used to describe the homogeneous broadening; the Gaussian distribution is used to describe the inhomogeneous broadening. Nevertheless, the homogeneous and inhomogeneous broadening exist simultaneously. That is to say, in a system, the broadening is neither homogeneous nor inhomogeneous, but between homogeneous and inhomogeneous. Therefore, we need a function to describe the mixed broadening. In this paper, we suggest that, instead of the Gaussian and the Cauchy distribution, one can use an intermediate distribution to describe the spectral line broadening.

In the semiclassical approach of spectral line broadening in laser system, the material and the light are described by quantum mechanics and the Maxwell equations, respectively, to calculate the interaction between the medium and the light [31]. Under the electric dipole approximation, the rate of absorption and stimulated emission of the medium between two energy levels is [16]

| (37) |

where is the refractive index of the material, is the vacuum permittivity, is the electric dipole moment, is the energy density of the light, is the frequency coinciding with the interval of two energy levels defined by . The function in Eq. (37) can be expressed by a probability density distribution using to describe the broadening near the frequency . It is clear that the rate of absorption and stimulated emission is determined by the function .

If the life time of the system at a certain energy level is infinite, reduces to , where is the Dirac delta function. In a realistic system, the life time of an excited state is finite. There are many kinds of factors effecting on a laser system, such as collisions, spontaneous emission, Doppler effect, etc. These factors lead to the broadening, and make deviate from . This can be directly measured in experiments [32]. We usually use full width at half maximum of to describe the effect of the broadening. The reciprocal of full width at half maximum indicates the life time of the level.

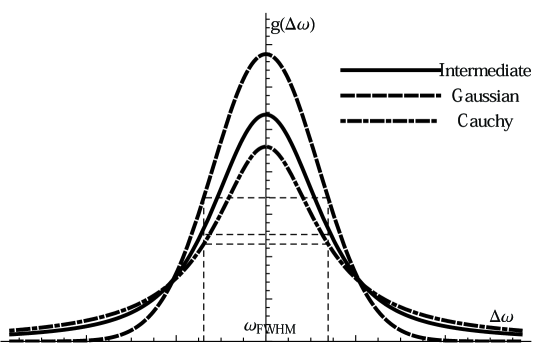

There are two kinds of mechanisms in spectral line broadening in a laser system [33]. One is homogeneous which arises from collisions and spontaneous emission, and it can be described by the Cauchy distribution. The other is inhomogeneous broadening which arises from the Doppler effect and the dislocation of the material. The Doppler broadening can be described by the Gaussian distribution, but the broadening caused by the dislocation has no proper expression. In general, homogeneous and inhomogeneous broadenings appear in a laser system simultaneously. Therefore, the function is actually between the Cauchy and Gaussian PDF.

Since the intermediate distribution given by Eq. (1) is between the Gaussian and the Cauchy distributions, we suggest that one can use the intermediate PDF, Eq. (1), to describe the function . Specifically, take

| (38) |

where is defined by the Eq. (1). The parameters and play the roles of fitting constants. The line shape of the broadenings which have the same full width at half maximum is shown in Figure 2.

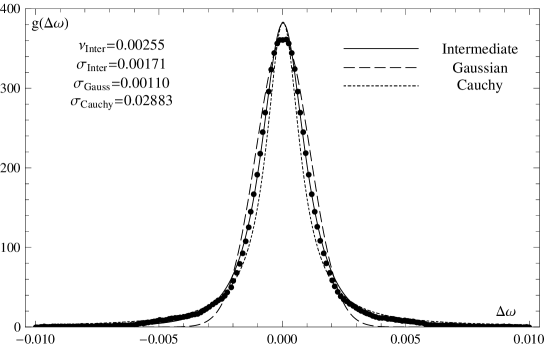

We import a set of data of hydrogen Zeeman-Stark line broadening from Figure 2 (b) in Ref. [34] and fit them with the intermediate, Cauchy, and Gaussian distribution, respectively. The data and the fitting results are plotted in Figure 3. From the fitting results, the intermediate distribution describes the line broadening better than the Gaussian and the Cauchy distribution.

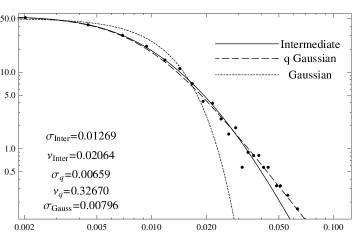

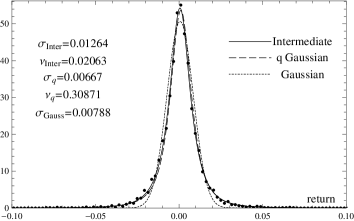

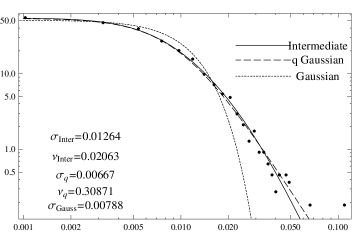

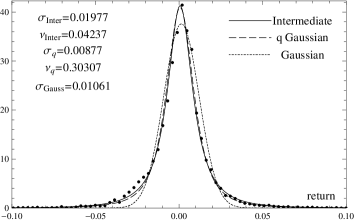

6 Application to stock market returns

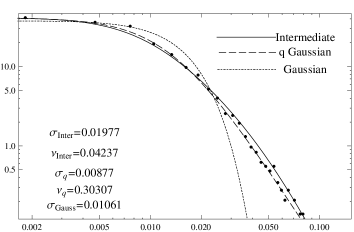

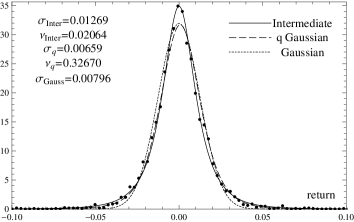

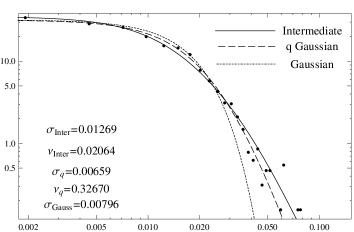

Gaussian distributed return is one of the most important assumptions in quantitative finance [24, 25, 26]. The key reason why we make this assumption is that the Gaussian distribution is easy to handle and we can get a lot of analytical results. The Gaussian distribution assumption, however, has got much criticism for its failure to describe the real world. Stock market returns in real world have sharp peak and fat tails distribution, which means that the probability of stock market crash is high. If we take the Gaussian distribution, the stock market crash is almost impossible to happen. Nevertheless, the stock market crash is not far away from us, like the Great Depression and the Black Thursday. We know that the Gaussian distribution does not have those characteristics. Thus we deem that the Gaussian distribution is a poor model of stock market return, and it is inappropriate to use the Gaussian distribution to describe the stock market. In this section, the market return is fitted by the intermediate distribution. We use S&P 500 price index, Dow Jones index, Nasdaq composite index, and Nikkei 225 index. The daily stock prices are obtained from Wind Database – a staple financial database. All those indexes are price index, and we compute the return from this formula

where is the return and is the stock price.

The q-Gaussian distribution is an important distribution, which has wide-ranging applications in various research scopes, as well as financial physics [35, 36, 37]. The q-Gaussian distribution is derived from the minimum Tsallis entropy [38, 39]

| (39) |

with the constraints of normalization of probability and a constant variance . The probability density function of the q-Gaussian distribution is

| (40) |

where and the q-exponential function is . When , the q-Gaussian distribution returns to the Gaussian distribution, Eq. (14).

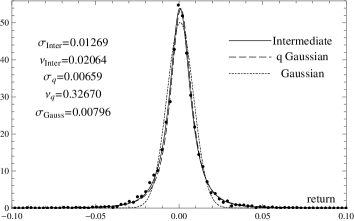

Making use of the intermediate, the q-Gaussian and the Gaussian distribution to fit the data, we plot the results in Figure 4-7. We can find that the intermediate and the q-Gaussian distribution are much better than the Gaussian distribution. The real data have sharp peak and fat tails and the intermediate and the q-Gaussian distribution both give good fits to this phenomenon. From these figures we can also find that the intermediate distribution is somewhat more suitable to describe the peak of the data of stock market returns, especially for the Nikkei index, and the log-log plots indicate that the q-Gaussian distribution describes the fat tails better than the intermediate distribution.

(a) (b)

(a) (b)

(a) (b)

(a) (b)

7 Conclusions and outlook

In this paper, we construct an intermediate distribution between the Gaussian and the Cauchy distribution. We provide the PDF and the corresponding characteristic function of the intermediate distribution. The moment, on the one hand, is used to show the mean value and the deviation to the mean value; on the other hand, is used as the terms of a series of a quantity. Because many kinds of distributions have no moment, we introduce the weighted moment. We calculate the weighted moment with the cut-off and the exponential weighted function, specifically. With the help of a smooth function, we give another expression of the intermediate distribution.

As an application, the spectral line broadening in laser theory can be approximated by a PDF. Since the homogeneous and inhomogeneous broadenings exist simultaneously, we suggest to describe the line shape function by the intermediate PDF, instead of the Cauchy or the Gaussian PDF. The intermediate distribution is not only useful in spectral line broadening of laser but maybe more attractive in financial physics [40, 41, 42]. A number of theoretical and empirical studies indicate that the majority of financial data are estimated as sharp peak and fat tails PDFs, but the Gaussian distribution is not general enough to account the excess kurtosis [43, 44, 45]. Our result shows that the intermediate and q-Gaussian distribution, however, comparing with the Gaussian distribution, are more suitable for fitting the financial data. The fitting results show that the intermediate distribution is somewhat more suitable to describe the kurtosis and the q-Gaussian distribution is more suitable to describe the tails, respectively. Such results show that the intermediate distribution, like the q-Gaussian distribution, can also be utilized in financial physics. In further study, we can use the intermediate distribution to price the option, and get the true value of the option. Option is one kind of derivatives which is the core of pricing theory. We also can price other derivatives whose price is based on the stock market return.

Acknowledgements This work is supported in part by NSF of China under Grant No. 11075115.

References

- [1] B.V. Gnedenko, A.N. Kolmogorov, 1949 Limit Theorems for Sums of independent Random Variables, Translated from Russian by Addison-Wesley, 1968.

- [2] S.M. Samuels, Positive-Integer-Valued Infinitely Divisible Distribution, Department of Statistics, Division of mathematical Sciences, Purdue University, 1975.

- [3] E.A. Novikov, Phys. Rev. E 50 (1994) R3303.

- [4] K. Sato, Levy Processes and Infinitely Divisible Distributions, Cambridge University Press, Cambridge, 1999.

- [5] V.C. Preda, Ann. Inst. Statist. Math. 34 (1982) 335.

- [6] L.E. Reichl, A Modern Course in Statistical Physics, 2nd edn, Wiley, New York, 1998.

- [7] Z.-S. She, E.C. Waymire, Phys. Rev. Lett. 74 (1995) 262.

- [8] D.W. Stroock, Probability Theory: An Analytic View, 2nd edn, Cambridge University Press, Cambridge, 2010.

- [9] C. Tsallis, R.S. Mendes, A.R. Plastino, Physica A 261 (1998) 534.

- [10] C. Tsallis, A. Rapisarda, A. Pluchino, E.P. Borges, Physica A 381 (2007) 143 .

- [11] A. Rodríguez, V. Schwämmle, C. Tsallis, J. of Stat. Mech. (2008) P09006.

- [12] P. Douglas, S. Bergamini, F. Renzoni. Phys. Rev. Lett. 96 (2006) 110601.

- [13] L. Borland, Phys. Rev. Lett. 89 (2002) 098701.

- [14] E. Van der Straeten, C. Beck, Phys. Rev. E 78 (2008) 051101.

- [15] E. Van der Straeten, C. Beck, Physica A, 390 (2011) 951.

- [16] O. Svelto, Principles of Lasers, 5th edn, Springer, New York, 2010.

- [17] W.-S. Dai, M. Xie, J. Stat. Mech. P04021 (2009).

- [18] Y. Shen, W.-S. Dai, M. Xie, Phys. Rev. A 75 (2007) 042111.

- [19] W.-S. Dai, M. Xie, Ann. Phys. (NY) 309 (2004) 295.

- [20] G. Gentile, Nuovo Cim. 17 (1940) 493.

- [21] W.-S. Dai, M. Xie, J. Stat. Mech. P07034 (2009).

- [22] W.-S. Dai, M. Xie, Physica A 331 (2004) 497.

- [23] F. Black, M. Scholes, Journal of Political economy 81 (1973) 637.

- [24] W. Sharpe, Journal of Finance 19 (1964) 425.

- [25] J. Lintner, Review of Economics and Statistics 47 (1965) 13.

- [26] J. Mossin, Econometrica 34 (1966) 768.

- [27] C. Tsallis, J. Stat. Phys. 52 (1988) 479.

- [28] D. Applebaum, Levy Processes and Stochastic Calculus, 2nd edn, Cambridge University Press, Cambridge, 2009.

- [29] S.S. Chern, W.H. Chen, K.S. Lam, Lectures on differential geometry,World Scientific, Singapore, 1999.

- [30] B.A. Dubrovin, A.T. Fomenko and S.P. Novikov, Modern Geometry — Methods and Applications, Part 2, Springer, Berlin, 1985.

- [31] U. Fano, Phys. Rev. 124 (1961) 1866.

- [32] M. Hanif, M. Aslam, M. Riaz, S.A. Bhatti, M.A. Baig, J. Phys. B 38 (2005) S65.

- [33] C.E. Webb, J.D.C. Jones, Handbook of Laser Technology and Applications, Volume I, IOP Publishing, London, 2004.

- [34] J.Rosato, D. Boland, M.Difallah, Y.Marandet, R. Stamm, International Journal of Spectroscopy (2010) Article ID 374372.

- [35] A.-H. Sato, J. Phys.: Conf. Ser. 201 (2010) 012008.

- [36] A.-H. Sato, Phys. Rev. E 69 (2004) 047101.

- [37] V. Gontis, J. Ruseckas, A. Kononovičius, Physica A 389 (2010) 100.

- [38] M. Gell-Mann, C. Tsallis, Nonextensive Entropy Interdisciplinary Applications, Oxford University Press, New York, 2004.

- [39] H. Suyari, Physica A 368 (2006) 63.

- [40] J.B. McDonald, W.K. Newey, Econometrics Theory 4 (1988) 428.

- [41] R.J. Smith, The Economic Journal 107 (1997) 503.

- [42] H.K. Ryu, Journal of Econometrics 56 (1993) 397.

- [43] D.X. Li, H.J. Turtle, Journal of Business and Economic Statistics 18 (2000) 174.

- [44] R.F. Engle, Econometrica 50 (1982) 987.

- [45] S.Y. Park, A.K. Bera, Journal of Econometrics 150 (2009) 219.