Yard-Sale exchange on networks: Wealth sharing and wealth appropriation.

Abstract

Yard-Sale (YS) is a stochastic multiplicative wealth-exchange model with two phases: a stable one where wealth is shared, and an unstable one where wealth condenses onto one agent. YS is here studied numerically on 1d rings, 2d square lattices, and random graphs with variable average coordination, comparing its properties with those in mean field (MF). Equilibrium properties in the stable phase are almost unaffected by the introduction of a network. Measurement of decorrelation times in the stable phase allow us to determine the critical interface with very good precision, and it turns out to be the same, for all networks analyzed, as the one that can be analytically derived in MF. In the unstable phase, on the other hand, dynamical as well as asymptotic properties are strongly network-dependent. Wealth no longer condenses on a single agent, as in MF, but onto an extensive set of agents, the properties of which depend on the network. Connections with previous studies of coalescence of immobile reactants are discussed, and their analytic predictions are successfully compared with our numerical results.

I Introduction

Wealth exchange models, initially proposed to investigate the

emergence of wealth inequality PCDP96 in human societies, have

recently became a subject of intense research CYCEWD05 ; YRCSM09 ,

following the availability of massive amounts of statistical data

describing commercial exchange, as well as wealth and income

distributions in different contexts Note1 .

Conservative stochastic exchange models were first used by

Angle ATST86 , who considered the spontaneous buildup of wealth

differences among equally able agents. In Angle’s initial model,

wealth concentration is a consequence of an explicit statistical

advantage favoring richer agents. In other words, the “rich get

richer” phenomenon is assumed explicitely in the exchange rules.

Later work showed HFTM02 ; SSMW03 ; IGACBR04 ; MGIWCI07 ; MMAE11 that

an explicit advantage favoring the rich is not necessary for wealth

concentration to appear. Wealth concentration can develop even if the

poor have an explicit statistical advantage. This rather

counterintuitive result, which has only recently been

stressed MGIWCI07 ; MMAE11 in the Econophysics literature, arises

when the amount at stake in each transaction is proportional to the

poorest agent’s wealth, e.g in the so-called Yard-Sale (YS)

models IKRWDI98 ; HFTM02 ; SSMW03 ; IGACBR04 ; SPWATM04 ; MGIWCI07 ; MMAE11 .

Yard Sale is an example of Multiplicative Stochastic Exchange, so

named because the wealth of the poorest intervening agent is

multiplied by a random number after the exchange MMAE11 . Under

YS dynamics, in the long run all wealth may end up in the hands of one

lucky agent, even if each pairwise transaction is statistically biased

in favor of the poorest of the two intervening agents. Therefore,

favoring the poor may not suffice to avoid wealth concentration, if the

bias in their favor is not strong enough. Interestingly, YS rules

constitute a realistic (although highly simplified) microscopic model

for the wealth exchange process occurring during commercial

interaction, or trade HFTM02 ; SSMW03 ; SPWATM04 . This suggests

that the conditions for the spontaneous creation of enormous wealth

differences for no reason other than luck TF01 , are built into

the commercial exchange rules, even if these rules may superficially

appear to favor the poor. Because of the possibility of

counterintuitive properties such as this one, and because of their

relevance for real world commercial exchange, it is clearly of

interest to understand the phenomenology of multiplicative exchange

models thoroughly.

In simple versions of YS, pairs of agents ’bet’ for a fraction of the wealth of the poorest of them, who has a probability to win the bet. Depending on and , long-term evolution can give rise either to a nontrivial equilibrium wealth distribution or to condensation of the whole wealth in the hands of just one agent. We call the resulting phases, respectively the wealth-sharing (or stable) and the wealth-appropriation (or unstable) phase. To date, most results for this model concern the full-mixture (or Mean-Field) case. However, commercial exchange is often determined by geographical, social or other constraints, which are ignored in the fully mixed approximation. Usually, a given agent can only exchange wealth with a reduced subset of other agents who are “close” to him by some measure of distance. These constraints can be described, at the simplest level, by means of a network in which nodes are economic agents and edges represent their possible interactions. It is reasonable to expect the topological properties of this network of allowed interactions to have a strong impact upon the general properties of wealth exchange processes occurring on them.

Recent work SBTOT03 ; GLFTP04 ; GD-MAIBT07 explores the network of commercial interactions among nations, or “World Trade Web” SBTOT03 . These studies make it clear that the topology of interaction networks is strongly correlated with the dynamical and static properties of the resulting wealth exchange process taking place on those networks Note2 . Numerical investigations SFAS01 ; GLWDO04 ; GLEON08 of the Bouchaud-Mezard BMWCI00 ; SPWATM04 model (BMM) on networks, find wealth distributions that change from lognormal to power-law when the connectivity is increased, for reasons that are easily understood. However, the BMM, while being an interesting solvable model, considers linear exchange (the amount exchanged is proportional to wealth differences), which is not very realistic SPWATM04 . On the other hand, the BMM includes both exchange and nonconservative processes (such as investment), and it is precisely from the interplay between the two that the network’s connectivity becomes important in the above studies.

The aim of this work is to analyze network effects for a realistic

model of pure conservative commercial exchange. Although real

economic systems involve nonconservative wealth-modifying processes as

well, it is important to first understand the properties of the

individual wealth-affecting mechanisms in isolation. In this work, we

study the Yard-Sale (YS) model on networks. Our network-restricted

version of YS is defined as follows: At each timestep, every agent

interacts (exchanges wealth according to YS rules) with another agent

that is randomly chosen among its neighbors, i.e. among those

agents for which a link exists. The interaction network is

fixed in time. Therefore, a pair of agents not connected by a link

will never interact directly. If the coordination number is

roughly the same for all nodes, each agent engages in two interactions

per timestep, on average. We consider here one-dimensional chains and

two-dimensional square lattices with nearest-neighbor links and

periodic boundary conditions, as well as Erdős-Rényi Random

Graphs BRG01 with variable coordination . In the limit

, the Random Graph becomes a complete graph, and

every pair has the same probability to interact. This is the

full-mixture case.

We focus on the identification of network-specific effects, i.e. the

extent to which the static and dynamic properties of the YS model,

when implemented on a network, depart from those in full-mixture. Our

results show that, while the stable wealth distribution is

mildly network-dependent, the location of the interface

that delimits the stable phase remains the same as in the full-mixture

case, for all networks considered in this work. The critical line

is therefore universal, in the sense defined in the context

of the theory of phase transitions. Dynamical properties, as for

example decorrelation times, on the other hand, do depend on the

network. Decorrelation times, which in this case are a measure of

“social mobility” of agents, are found to diverge at the interface

with the unstable phase. This divergence is used to locate the

critical line with high precision.

In the unstable, or wealth-appropriation, phase, dynamical as well as long-time properties of YS are found to be strongly network-dependent. The most important difference with full-mixture is in this case that, on a network, complete condensation in the hands of one agent no longer occurs. On a network, instead, in the long run an extensive set of “locally rich” agents (LRA) appears, each connected only to extremely impoverished agents. This leads to the effective cessation of all exchange activity, a phenomenon similar to dynamical freezing. This freezing onto a disordered final state is observed in the whole unstable phase. The properties of the final set of LRAs, and their final wealth distribution, depend on the network topology, as well as upon and . We discuss the connections between the appearance of a set of locally rich agents and the process of coalescence (or coagulation) of immobile reactants BVNR99 ; AGNN01 ; AO04 on networks. These connections provide analytical predictions for the number of LRAs on Random Graphs, which are consistent with our own numerical results. By increasing the average connectivity of a network, the number of LRAs onto which wealth condenses is decreased, until, in the limit , which is the full-mixture case, only one LRA remains, i.e full condensation is recovered.

This article is organized as follows. Section II recalls some results for YS in full-mixture. In Section III, numerical results on networks in the stable phase are presented and compared with full mixture results. In particular, decorrelation times are used in this section to locate the interface with high precision. Wealth appropriation dynamics on networks is studied in Section IV, where it is found that wealth condenses onto an extensive number of locally rich agents (LRA). Their number and wealth distribution are analyzed in this section. Finally, Section V offers a discussion of our results.

II Yard-Sale in full-mixture

Consider wealth exchange for a pair of agents and with before interaction, according to the following YS rules. The agents bet for an amount . The poorest agent () wins the bet with probability , in which case and , or looses the bet with probability , in which case and . The wealth of the poor agent is therefore multiplied by a random factor , which equals with probability and with probability . Long-term evolution under these rules gives rise either to a stable wealth distribution or to condensation, depending on and .

The location of the critical line below which condensation occurs can be derived as follows MGIWCI07 ; MMAE11 . The wealth of a very poor agent undergoes a Random Multiplicative Process RRMP90 with multiplier at each timestep. After a large number of timesteps, the appropriate central tendency estimator for is its geometric average , where

| (1) |

If , there will be a systematic transference of wealth from poorer to richer agents. This is the wealth-appropriation, or unstable, phase. In this phase, wealth differences among agents are amplified in time, until the whole wealth ends up in the hands of a single (in full-mixture) agent in the long run MGIWCI07 ; MMAE11 .

If , the system is in the wealth-sharing, or stable, phase. Wealth is transferred from richer to poorer agents, which tends to “iron out” wealth fluctuations. In the long run, the distribution of wealth reaches a nontrivial equilibrium form , which depends on and .

By the heuristic argument above, the critical interface separating stable and unstable phases is given by , or

| (2) |

A more rigorous analysis MGIWCI07 ; MMAE11 , involving the master

equation for in the full-mixture approximation, confirms

(2).

Notice that the average return of the poorest agent MMAE11 is

positive whenever . There is thus a region

where complete wealth concentration occurs, i.e. poor agents

impoverish further, despite the average return of poor agents being

positive.

II.1 The stable phase

II.1.1 Time correlations

A dynamical characterization that is useful in the stable phase is the relaxation timescale for equilibrium fluctuations. The excess wealth , where is the average per agent wealth, gives the amount by which the wealth of an agent departs from average at time . The correlation function at time , averaged over timesteps, is then defined as

| (3) |

We use here the normalized correlation function , which equals one for and decays as

| (4) |

for large . A small value of means that being richer or poorer than average at a given time has little predictive power timesteps later. Therefore, measures the “mobility”, in the wealth scale, of a typical agent over a time horizon of timesteps. The timescale over which converges to zero measures the amount of time needed for full “social mixture” (decorrelation from initial wealths, or loss of memory). In a statistical mechanics context, is the relaxation time needed for the decay of equilibrium wealth-fluctuations, or “decorrelation time”. Borrowing from the theory of equilibrium phase transitions SITP87 ; BDFTTO02 , one expects to diverge as the critical interface is approached from above, as

| (5) |

where the dynamical exponent can be a function of eventually. As shown later, the numerical estimation of allows a very precise determination of the location of the interface.

II.2 The unstable phase

II.2.1 Ranked wealths

When , the system is in the unstable phase, wealth differences are amplified in time and this eventually leads to condensation in the fully mixed case. In the whole unstable phase, the decorrelation time is infinite. Therefore an agents’ position in the wealth scale becomes frozen, in the long run. In other words, social mobility is suppressed in the appropriation phase.

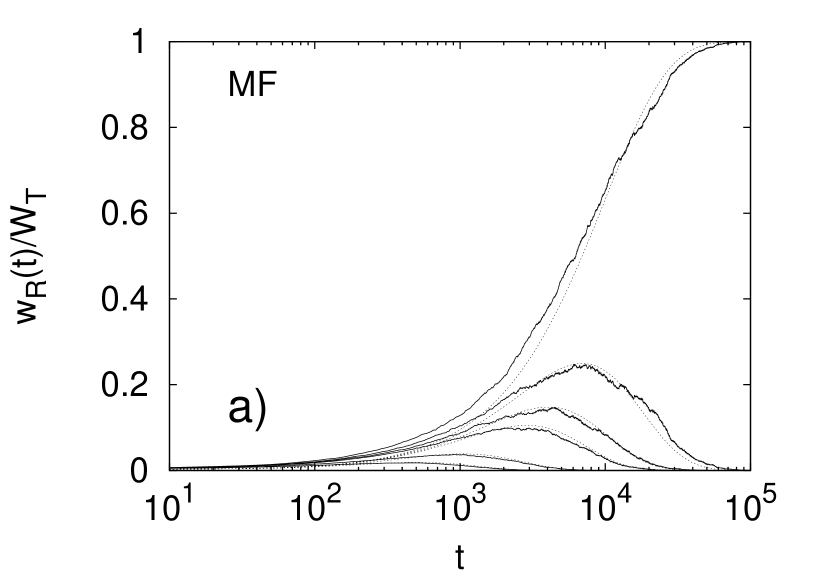

A dynamical analysis of the unstable phase MMAE11 for the fully-mixed system shows that the typical wealth of an agent with rank Note3 at time is , which, after normalizing for a total wealth reads

| (6) |

This expression is valid at long times, when ranks no longer change as a result of economic exchange. At any fixed time, the ranked-wealth distribution is thus exponential in rank. Accordingly, the transient wealth distribution is of the form . Fig. 1a compares (6) with numerical results.

II.2.2 Condensation criteria

In numerical simulations, a practical criterion is necessary to define wealth condensation within predefined limits. We use for this purpose the ratio , involving the wealths of the richest and second-richest agents in the system. This ratio is one for evenly distributed wealth, and goes to zero when all wealth condenses onto a single agent. An alternative useful measure of condensation is the normalized second moment

| (7) |

which is similar to the participation ratio in localization studies. is of order if wealth is more or less evenly distributed among agents, and goes to one upon condensation onto a single agent. Therefore, approximates the number of economically active agents in the system, as much as the inverse participation ratio estimates the number of sites over which a normal mode, or an electron, spreads.

II.2.3 Condensation timescales

The timescale for convergence towards the condensed state is an interesting property that quantifies the dynamics in the unstable phase. This timescale can be estimated theoretically, in the full-mixture case. Using (6) one has that , with

| (8) |

From (1) and (2), we see that . Therefore, the condensation timescale diverges as

on approach to the critical interface.

Simple analysis of (6) shows that attains its

maximum value at time , and goes

exponentially fast to zero afterwards for all . This is

understood in the following terms. During the condensation process in

the unstable phase, an agent with rank systematically extracts

wealth from poorer agents (those with ) and transfers some of it

to richer agents (those with ). As long as the wealth of poorer

agents so allows, his balance will be positive, so his wealth will at

first increase. But this increase happens at the expense of poorer

agents, and for times these will have exhausted their

wealth. Continued transference of wealth upwards (to richer agents)

will in turn make the agent with rank impoverish as well.

Therefore, each rank goes bankrupted at a specific timescale. Poorer

ranks (of order ) do so at times of order , while richer

ones (of order one) take time . The second-richest agent

goes bankrupted at time , leaving a single rich agent

to account for most of the wealth. This justifies our identifying of

as the timescale needed for complete condensation. The entire

process of enrichment followed by bankruptcy for the different ranks

is visualized in Fig. 1.

III Network YS in the stable phase

In this section, results from numerical simulations for 1d rings, 2d

square lattices with periodic boundaries, Erdős-Rényi Random

Graphs, and full-mixture, are described and compared with analytic

predictions for the full-mixture case. Starting from an even

distribution of wealth among the agents, the system is first

equilibrated during timesteps before measurements are

taken. The required number of equilibration steps is determined by

measuring for a series of increasing values, until it

is found to no longer depend on . System sizes from

to agents are considered.

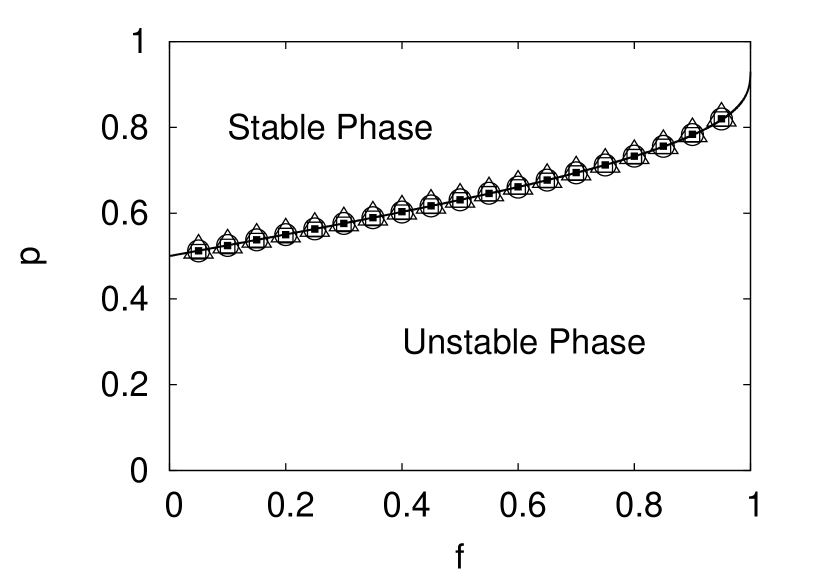

We first describe how the critical line is determined

numerically in this work. Firstly, after equilibrating the system as

described above, correlation functions are measured in the

stable phase for many pairs and for each network considered.

Once is known for each pair and for each network,

(4) is fitted to these data, from where estimates for the

relaxation times are obtained. As expected, is

found to diverge on approach to a critical value that

delimits the stable phase from below. By next fitting

(5) to our data for , we can obtain very

precise estimates for , the location of this divergence. Our

results are shown in Fig. 2. The critical values so found

are, in all cases, consistent with the full-mixture prediction

(Eq. (2)) within numerical errors, suggesting that , for all networks considered.

The above result differs from expectations based on the theory of

equilibrium phase transitions. In that case, for a given interacting

system, critical parameters as e.g the critical temperature, do depend

on the network, i.e. are not universal. The analogous parameter for

Yard-Sale is the critical probability , which, within our

numerical errors, seems to be network-independent and the same as in

the full-mixture, or Mean-Field, case. We therefore propose that the

critical interface (2) derived for the full-mixture case is

exact on any singly-connected network.

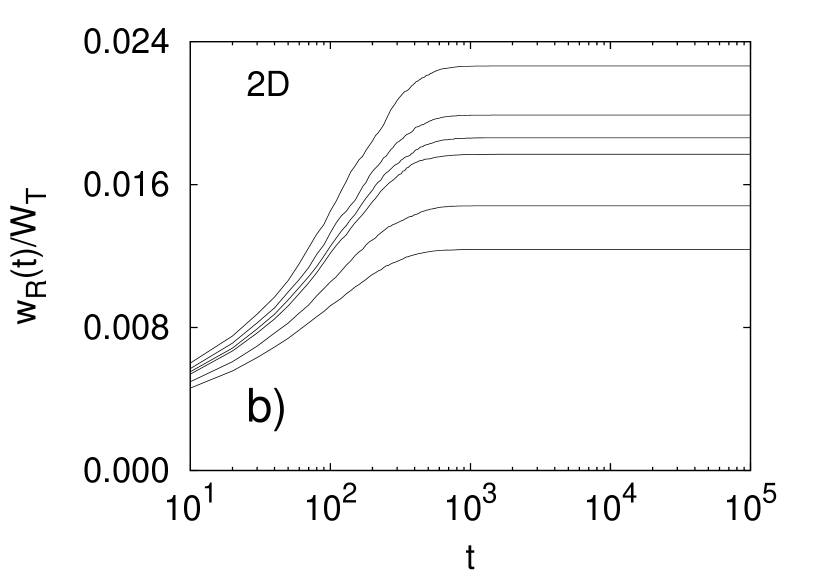

Equilibrium wealth distributions in the stable

phase () where measured (not shown) for all

networks considered in this work, for several pairs , and

compared with full-mixture. We found that is network-dependent,

although differences with full-mixture are minor. Relaxation

timescales, on the other hand, are found to be strongly

network-dependent, which is reasonable since the paths through which

wealth can flow are dictated by network topology. As expected,

relaxation to equilibrium takes longer on 1d rings, because there are

lesser paths for wealth to flow, and it is fastest in the full-mixture

case.

IV Network YS in the unstable phase

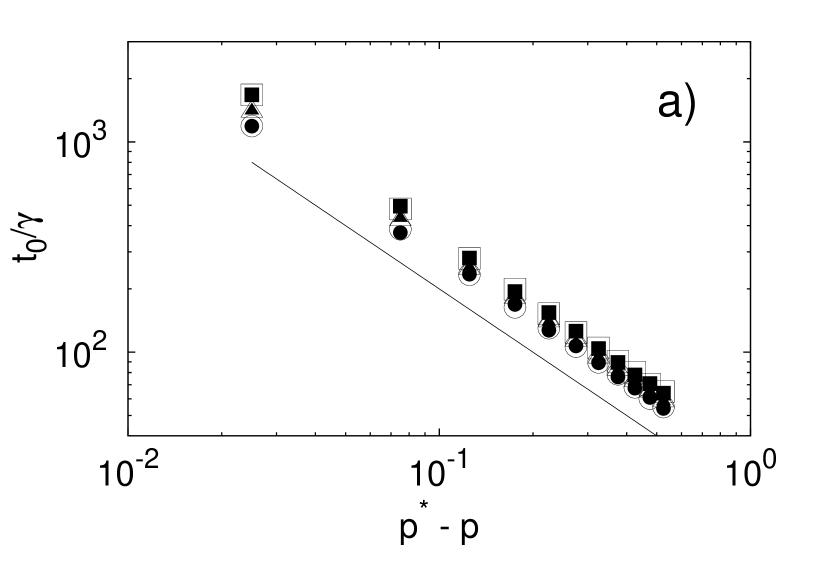

In the fully mixed case, whenever the system is in the unstable phase , where is given by (2), all wealth ends up being owned by a single rich agent in the long run. This process is called wealth condensation MMAE11 ; MGIWCI07 . For numerical purposes, in this work we assume that the system is completely condensed when . The time needed for this limit to be reached is measured and averaged over condensation histories. Results for in the complete-graph limit (full mixture) are displayed in Fig. 3a (open and filled circles), and are found to behave as , in entire accordance with the theoretical result (8) for full-mixture.

For network-restricted Yard-Sale in the unstable phase, complete wealth condensation onto a single agent is no longer observed. Instead, in the long run, the whole wealth condenses onto an extensive set of locally rich agents (LRA). A locally rich agent is defined to be one who is richer than any of its neighbors. Agents who are non-LRA impoverish steadily in the long run, because in the unstable phase there is a systematic transference of wealth from poor to rich agents. For long times, each LRA is only connected to agents whose wealth is extremely small. Wealth exchange is then effectively suppressed, leading to dynamical freezing, onto a disordered final state.

IV.1 Condensation times

At long times, there is a clear scale separation between the wealth of each LRAs and those of its neighbors, the latter going exponentially to zero in time. We assume that the final set of LRAs has been irreversibly frozen, and that wealth exchange has effectively stopped, when each LRA is richer than its richest neighbor by a factor of at least . This criterion generalizes the one we adopted for full-mixture, and reduces to it whenever there is condensation, in which case there is only one LRA.

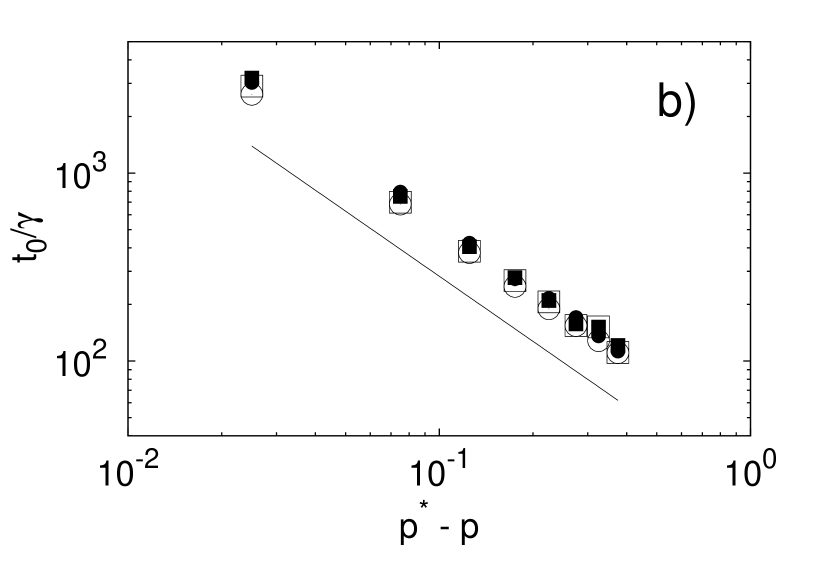

Fig. 3a shows condensation times divided by coordination , for Random Graphs with variable link density . The case (circles) is the complete graph, or full-mixture case. Condensation times are seen to diverge at the interface as , that is, the exponent of this divergence does not depend on and is the same as for full-mixture. Our results also show that is roughly proportional to , which is consistent with Eq. (8) for the full-mixture limit, in which case .

Fig. 3b shows for 1d and 2d networks, where . The exponent in seems to be slightly larger for these finite-dimensional networks. Although is arguably dimension-dependent, the quality of our data does not allow us to resolve the difference between and . Our best estimate is in one and two dimensions.

IV.2 Locally Rich Agents

Clearly, any set of LRAs with arbitrary wealths, surrounded by impoverished agents is a fixed point of the dynamics. There is thus a non-denumerable multiplicity of fixed points, among which the wealth exchange dynamics chooses one stochastically. The statistical properties of these fixed points, as for example the average number of LRAs, and their wealth distribution, depend on the parameters of the model, as well as on the topology of the network, among other things. A detailed study of these properties is beyond the scope of this work. However, some of the most relevant properties of LRAs, namely their number and wealth distribution, will be briefly discussed in the following.

IV.2.1 Number of LRAs

Once the above described criterion for the formation of a set of LRAs is satisfied, the dynamics is stopped, and the properties of LRAs are determined. Measurements are averaged over repetitions of the condensation history, for each case.

Condensation of wealth onto a reduced set of agents is a consequence of the unstable nature of the dynamics for . There is a systematic transfer of wealth from poor to rich, which in turn increases wealth differences. The strength of this instability is given by (Eq. (1)), and becomes zero right at the interface . Close to this interface, where is small, wealth appropriation by the richer agents happens very slowly. Wealth has then more time to migrate to richer agents, before the dynamics comes to a halt. One therefore expects the process of wealth concentration onto a single rich agent to happen more completely there, than deep inside the unstable phase, where dynamical arrest takes place in a short time. One could then expect the average number of LRAs to decrease on approach to the interface.

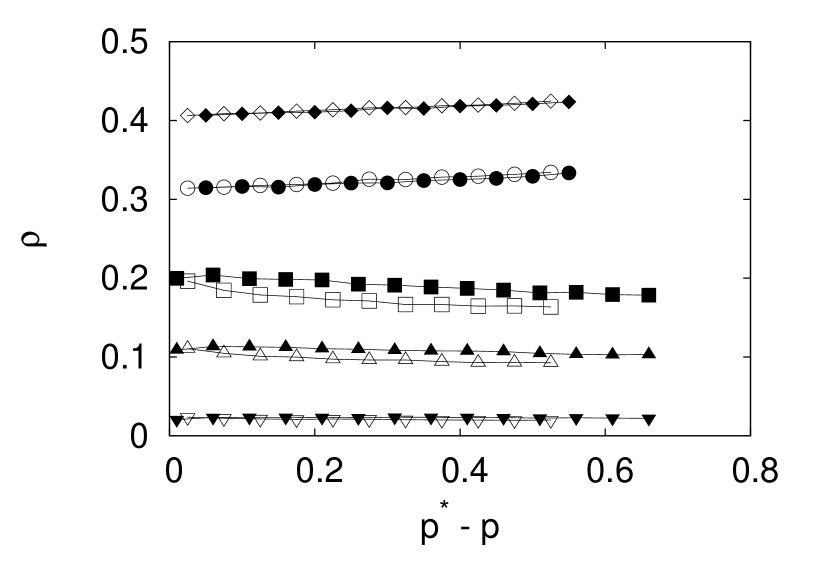

However, our results, displayed in Fig. 4, show that, for a given network, the final density of LRAs depends only very mildly on the exchange parameters or . In other words, the number of LRAs is roughly the same in the whole unstable phase, and is only determined by the network’s properties (see Section IV.2.2). For 1d rings and 2d square lattices, there is even no observable -dependence in Fig. 4.

IV.2.2 Analytical prediction for

By definition, no two LRAs are connected to each other. Therefore, a set of LRAs constitutes an independent set BRG01 of the graph. A partition of a graph into independent sets constitutes a coloring. We thus conclude that long-term YS evolution in the appropriation phase identifies colorings of the network.

Since, as our numerical results suggest (see Fig. 4), the

number of LRAs is not strongly dependent on and , one can

obtain useful information by studying the particular case ,

, which is analytically tractable to some extent. In this

particular case, whenever two agents interact, the winner is chosen at

random. If the richest agent wins, he gets the whole wealth of the

loosing agent, who is in turn rendered inactive. A similar process is

studied in the context of “coagulation” or “coalescence” of immobile reactants on a

network BVNR99 ; AGNN01 ; AO04 . Analytical descriptions for the

density of the active species ( is the inert species), which in

our case is the final density of LRA, have been provided for these, as

well as for related models KVA81 ; MPA93 that consider

“annihilation” as well.

In particular, Abad AO04 provides explicit expressions for the

final density of active agents on 1d and 2d lattices, as well

as on Bethe Lattices with coordination . If is the

initial density of active sites, the final density on a Bethe lattice

is

| (9) |

For large , this gives for , and if .

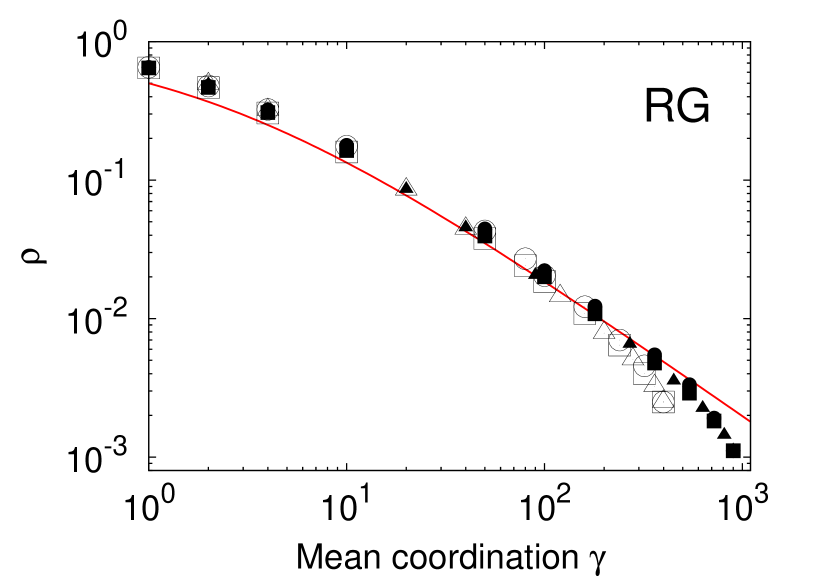

A comparison between (9) and our own numerical results on

Random Graphs (RG) with average coordination is shown in

Fig. 5. Notice that all sites on a Bethe lattice have

neighbors, while this is satisfied only on average for Random Graphs.

Therefore, a perfect coincidence is not expected. Nevertheless, an

acceptable similarity between our numerical results and (9)

is found.

The 1d case is obtained from (9) in the limit , and equals for as is our case. Our numerical result in 1d is approximately ( Fig. 4), somewhat larger than this analytic prediction. Abad’s two-dimensional approximate result is for , again slightly smaller than our numerical results on 2d square lattices, shown in Fig. 4.

These results show that the dynamical process of multiplicative wealth concentration on networks has features in common with annihilation and coalescence KVA81 ; MPA93 ; BVNR99 ; AGNN01 ; AO04 of immobile reactants. Furthermore, it was in the context of those models that the failure of the MF approximation to predict the final density of active species was first noticed. While MF predicts a zero asymptotic density of the active species, on generic networks a finite value is found. This parallels our observation that, while in full mixture wealth condenses onto a single agent, on networks it does so onto an extensive set of agents.

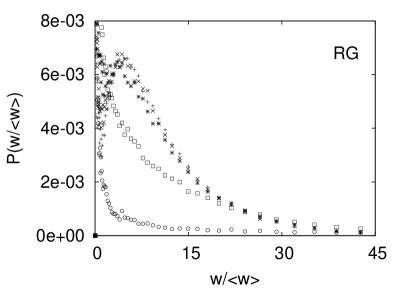

IV.2.3 Wealth distribution of LRAs

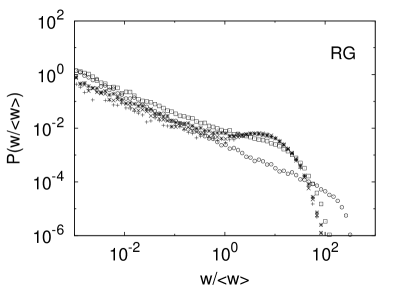

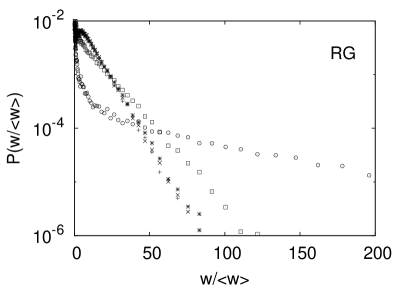

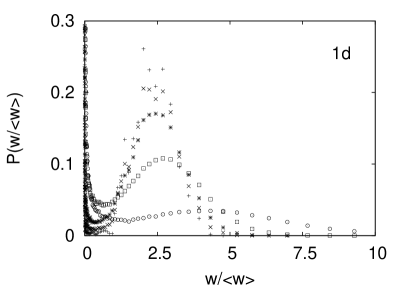

Wealth distributions of LRAs in the frozen state are displayed in

Fig. 6 for 1d and RG with . Wealth

distributions on 2d lattices were also measured (are not shown) and

found to be qualitatively similar to those in 1d. In all three cases,

the minimum in for suggests the

existence of two sets of LRAs with different properties. For the sake

of this analysis, the population of LRAs is divided in two groups

according to their wealth. Those with wealth ,

have a roughly normal wealth distribution in 1d and 2d, and an

exponential wealth distribution on Random Graphs. We call these “type

1” LRAs. In addition to those, LRAs with , have

wealths distributed according to a power-law that

extends down to zero. These we call “type 2” LRAs.

We have measured (not shown) the numbers of type 1 and 2 LRAs versus

time for all networks with various parameter values. For values

that are not too close to the interface, freezing occurs rapidly, and

the final number and cumulative total wealth of type 2 LRAs turns out

to be almost negligible compared to those of type 1. In other words,

most LRAs are type 1, i.e. have wealths larger than average in the

frozen state. Additionally, the wealths of type 1 LRAs are found to

have a narrow distribution if not too close to the interface. Very

close to the interface, i.e. for , on the other hand, a

significant amount of conversion from type 1 to type 2 occurs before

the frozen state is reached. During this process, the number of type 1

LRAs drops steadily, while the total number of LRAs stays almost

constant or increases slowly. Conversion from type 1 to type 2 means

that a large number of LRAs, despite being richer than their

neighbors, can still loose a significant fraction of their wealth,

which in the end goes to the few remaining type 1 LRAs. This is

possible because close to the interface (Eq. (1)) is

small, and therefore being richer does not ensure a strong statistical

advantage.

On approach to the interface, wealth distributions of LRAs develop

long tails for large wealth, and the power-law behavior is seen to extend to the right. Therefore, the distinction

between the wealth distributions of type 1 and type 2 LRAs is blurred

in this limit. Near the interface, a single LRA ends up owning a

significant fraction of the whole wealth. Therefore, even though the

total number of LRAs remains approximately constant when the interface

is approached, most of them will only have negligible wealth in the

end. Therefore, we conclude that wealth condenses onto a single rich

agent, on any connected network, when the system is unstable but very

close to the critical interface .

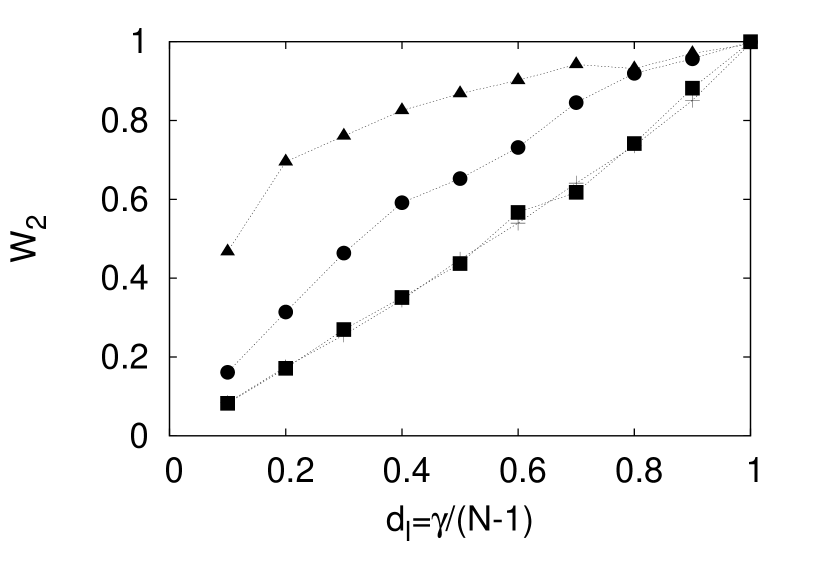

In the case of Random Graphs, condensation onto a single agent occurs

in the whole unstable phase only in the complete graph limit, i.e. in

the limit . A measure of wealth

condensation is provided by (see Eq. (7)). A plot of at

freezing versus link density is shown in

Fig. 7. These data show that full condensation in the

whole unstable phase only happens in the complete-graph limit. Inside

the unstable phase, wealth is distributed among all LRAs roughly

uniformly. Unless the system is really close to the interface, one has

. This result can be understood as follows. In the

frozen state, as shown in Fig. 6, wealth is

distributed exponentially among the resulting

locally rich agents. If there are locally rich agents and

the rest have zero wealth, Eq. (7) can be rewritten as , where is the variance

of the wealth distribution of the LRAs. For the particular case of an

exponential distribution, and therefore

. As discussed in Section IV.2.2, the

density of LRA is approximately for large

. Therefore , which renders

as observed numerically for points not too

close to the interface (Fig. 7).

V Discussion of results

Yard-Sale

(YS) IKRWDI98 ; HFTM02 ; SSMW03 ; IGACBR04 ; SPWATM04 ; MGIWCI07 ; MMAE11

is a simple but realistic model for commercial exchange that presents

two phases: a stable (or wealth-sharing) phase where wealth is

distributed and an unstable (or wealth-appropriation) one where wealth

concentrates in the hands of a few agents. We have numerically studied

the static and dynamic properties of YS on several types of networks,

comparing them to those in the full-mixture (or mean-field)

approximation. Equilibrium wealth distributions on networks,

in the stable phase, are found to be very similar to those in

full-mixture. Measuring decorrelation times , which in the

this model can be interpreted as “social mobility” times, we are

able to very precisely locate the interface that separates the wealth

sharing from the wealth appropriation phases

(Fig. 2). Our numerical results strongly suggest that the

critical interface derived in the full-mixture

approximation (Eq. (2)) is exact on any network.

An important result is the observation that, for network YS in the

unstable phase, wealth does not condense onto a single agent as it

does in the fully mixed case, but onto an extensive set of locally

rich agents (LRA) instead. These LRAs form an independent

set BRG01 in the network, and therefore define a coloring of

it. The final density of agents with nonzero wealth is thus finite on

networks, while it is zero for full mixture. In recent related

work S-MHRCFI11 , it was proposed that the emergence of many

locally rich agents might be due to multiple-connectedness of the

network, suggesting that, on networks made of just one connected

component, global condensation onto one agent would eventually occur.

This expectation is not confirmed by our results, which show that an

extensive number of LRAs remain, in the whole unstable phase, on

singly-connected networks as well. It is only in the limit of a

complete graph, which is the fully mixed case, or, (on any network) in

the limit (i.e. right at the interface), that

condensation onto a single agent is observed.

We have discussed previously unnoticed connections between wealth

condensation in YS and earlier studies of

annihilation KVA81 ; MPA93 or

coalescence BVNR99 ; AGNN01 ; AO04 of immobile reactants, a related

statistical problem where the distinction between network results and

mean-field ones (i.e. zero vs nonzero final density of LRAs) was first

noticed BVNR99 ; AGNN01 . With the help of these connections, we

have been able to compare our own numerical results (Figs. 4

and 5) with analytic predictions AO04 for

the remaining density of wealth-possessing agents on several networks.

A good coincidence is found throughout the entire unstable

phase. Furthermore, by using analytical expressions for the density of

remaining LRAs on Random Graphs, we were able to explain our numerical

results (Fig. 7) showing that

on Random Graphs, deep inside the unstable phase.

Surprisingly, the density of LRAs is essentially constant in the whole

unstable phase, although their wealth distribution is not. Their

wealth distribution is roughly homogeneous, i.e. has a relatively

narrow distribution, except when extremely close to the interface. A

particularity that deserves further attention is the fact that the

wealth distribution of LRAs in the frozen state is nearly normal in

one and two dimensions, but exponential on Random Graphs

(Fig. 6)

Very close to the interface that delimits the unstable phase from

above, however, wealth is no longer homogeneously distributed among

the LRAs, but develops a long right tail of the form

until, at the interface itself, only one rich agent remains, which

owns the whole systems’ wealth. Therefore, on the interface itself,

condensation onto a single agent is again observed, on any

network. However, the time needed for condensation diverges in this

limit, in contraposition to the full mixture case, where wealth

condenses onto a single agent in finite time.

We have found that YS models only show strongly network-dependent

properties when the system’s parameters are in the unstable

phase. In the light of this result, the correlations between

topological properties and wealth distributions that have been

recently observed in experimental studies of global commercial

networks SBTOT03 ; GLFTP04 ; GD-MAIBT07 , may be interpreted as

suggesting that the international trade system is itself in the

unstable phase. In other words, that the microscopic exchange rules

for international trade are such that favor systematic wealth

appropriation by larger agents. Other evidences of this possibility

have been recently found by analyzing the distribution of per-capita

gross domestic products Note4 .

On the other hand, as already said in the introduction, global wealth

distributions depend on processes other than conservative

exchange. The generation of wealth by endogenous processes, for

example, acts as a source of wealth that would avoid freezing in the

unstable phase. A system under unstable exchange, in the presence of

wealth creation by endogenous processes, would reach a

quasi-stationary state in which wealth is produced everywhere and then

channeled towards richer agents by the exchange processes.

Acknowledgements.

The authors wish to thank the warm hospitality of the Statistical Mechanics group in Centro Atómico Bariloche, Argentina, where this work was started. Computer time provided by CGSTIC-CINVESTAV on “Xiuhcoatl” hybrid supercomputing cluster made this work possible. R. B. G. Acknowledges financial support from CONACYT.References

- (1) V. Pareto. Cours d’Economie Politique. Droz, Geneve, 1896.

- (2) A. Chatterjee, S. Yarlagadda, and B. K. Chakrabarti, editors. Econophysics of Wealth Distributions. Springer-Verlag, Milan, Italy, 2005.

- (3) V. M. Yakovenko and J. B. Rosser. Colloquium: Statistical mechanics of money, wealth, and income. Rev. Mod. Phys., 81:1703–1725, 2009.

-

(4)

See for example

http://en.wikipedia.org/wiki/Distribution_of_wealth. - (5) J. Angle. The surplus theory of social stratification and the size distribution of personal wealth. Social Forces, 65:293–326, 1986.

- (6) B. Hayes. Follow the money. Am. Scientist, 90:400–405, 2002.

- (7) S. Sinha. Stochastic maps, wealth distribution in random asset exchange models and the marginal utility of relative wealth. Phys. Scr., T106:59–64, 2003.

- (8) J. R. Iglesias, S. Goncalves, G. Abramson, and J. L. Vega. Correlation between risk aversion and wealth distribution rid b-3753-2010. Physica A, 342:186–192, 2004.

- (9) C. F. Moukarzel, S. Goncalves, J. R. Iglesias, M. Rodriguez-Achach, and R. Huerta-Quintanilla. Wealth condensation in a multiplicative random asset exchange model. Eur. Phys. J.-Spec. Top., 143:75–79, 2007.

- (10) C. F. Moukarzel. Multiplicative asset exchange with arbitrary return distributions. J. Stat. Mech.-Theory Exp., page P08023, 2011.

- (11) S. Ispolatov, P. L. Krapivsky, and S. Redner. Wealth distributions in asset exchange models. Eur. Phys. J. B, 2:267–276, 1998.

- (12) N. Scafetta, S. Picozzi, and B. J. West. A trade-investment model for distribution of wealth. Physica D, 193:338–352, 2004.

- (13) Nassim N. Taleb. Fooled by Randomness: The Hidden Role of Chance in the Markets and in Life. W. W. Norton & Company, 1st edition, October 2001.

- (14) M. A. Serrano and M. Boguñá. Topology of the world trade web rid b-7795-2011. Phys. Rev. E, 68:015101, 2003.

- (15) D. Garlaschelli and M. I. Loffredo. Fitness-dependent topological properties of the world trade web. Phys. Rev. Lett., 93:188701, 2004.

- (16) D. Garlaschelli, T. Di Matteo, T. Aste, G. Caldarelli, and M. I. Loffredo. Interplay between topology and dynamics in the world trade web rid e-9961-2010. Eur. Phys. J. B, 57:159–164, 2007.

- (17) For a review, see e.g. M. A. Serrano, D. Garlaschelli, M. Boguñá, and M. Loffredo, 2010, The World Trade Web: Structure, evolution and modeling. in Complex Networks, edited by G. Caldarelli, in Encyclopedia of Life Support Systems (EOLSS).

- (18) W. Souma, Y. Fujiwara, and H. Aoyama. Small-World Effects in Wealth Distribution. eprint arXiv:cond-mat/0108482, August 2001.

- (19) D. Garlaschelli and M. I. Loffredo. Wealth dynamics on complex networks. Physica A, 338:113–118, 2004.

- (20) D. Garlaschelli and M. I. Loffredo. Effects of network topology on wealth distributions. J. Phys. A-Math. Theor., 41:224018, 2008.

- (21) J. P. Bouchaud and M. Mezard. Wealth condensation in a simple model of economy. Physica A, 282:536–545, 2000.

- (22) Béla Bollobás. Random Graphs. Cambridge University Press, Cambridge, 2nd edition, 2001.

- (23) F. Baras, F. Vikas, and G. Nicolis. Reaction-controlled cooperative desorption in a one-dimensional lattice: A dynamical approach. Phys. Rev. E, 60(4, Part a):3797–3803, OCT 1999.

- (24) E. Abad, P. Grosfils, and G. Nicolis. Nonlinear reactive systems on a lattice viewed as Boolean dynamical systems. Phys. Rev. E, 63(4, Part 1), APR 2001.

- (25) E. Abad. On-lattice coalescence and annihilation of immobile reactants in loopless lattices and beyond. Phys. Rev. E, 70(3, Part 1), SEP 2004.

- (26) S. Redner. Random multiplicative processes - an elementary tutorial. Am. J. Phys., 58(3):267, March 1990.

- (27) H. Eugene Stanley. Introduction to Phase Transitions and Critical Phenomena. International Series of Monographs on Physics. Oxford University Press, 1987.

- (28) J. J. Binney, N. J. Dowrick, A. J. Fisher, and M. E. J. Newman. The Theory of Critical Phenomena: An introduction to the Renormalization Group. Oxford Science Publications. Oxford University Press, New York, 2002.

- (29) An agent has rank if its wealth is the -th largest in the population.

- (30) V. M. Kenkre and H. M. Vanhorn. Annihilations of stationary particles on a lattice. Phys. Rev. A, 23(6):3200–3206, 1981.

- (31) S. N. Majumdar and V. Privman. Annihilation of immobile reactants on the Bethe lattice. J. Phys. A-Math. Gen. , 26(16):L743–L748, Aug. 21 1993.

- (32) C. H. Sanabria-Montana, R. Huerta-Quintanilla, and M. Rodriguez-Achach. Class formation in a social network with asset exchange. Physica A, 390:328–340, 2011.

- (33) C. Moukarzel, “Per-capita GDP and nonequilibrium wealth-concentration in a model for trade”, 2011, to be published.