Spectra of random graphs with arbitrary expected degrees

Abstract

We study random graphs with arbitrary distributions of expected degree and derive expressions for the spectra of their adjacency and modularity matrices. We give a complete prescription for calculating the spectra that is exact in the limit of large network size and large vertex degrees. We also study the effect on the spectra of hubs in the network, vertices of unusually high degree, and show that these produce isolated eigenvalues outside the main spectral band, akin to impurity states in condensed matter systems, with accompanying eigenvectors that are strongly localized around the hubs. We also give numerical results that confirm our analytic expressions.

I Introduction

The topology of complex networks, such as social, biological, and technological networks, can be represented in matrix form using an adjacency matrix or any of several other related matrices such as the graph Laplacian or the modularity matrix Newman03d ; Boccaletti06 . The spectral properties of these matrices—their eigenvalues and eigenvectors—are related to a range of network features of scientific interest, including optimal partitions Fiedler73 ; PSL90 , percolation properties BBCR10 , community structure Newman06b ; Fortunato10 , and the behavior of network dynamical processes such as random walks, current flow, diffusion, and synchronization Arenas08 ; BBV08 . As a result, the study of network spectra has been the subject of considerable research effort for some years. This effort has taken a number of forms. One has been the study of the spectra of empirically observed networks, which can be calculated by numerical means for networks of size up to hundreds of thousands of vertices Arenas08 ; FDBV01 . Another, which is the topic of this paper, is the study of the spectra of model networks. A fundamental question we would like to answer is how particular structural features of networks are reflected in network spectra, and model networks provide an ideal setting in which to investigate this question.

Some results in this area have been known for a long time. For example, the very simplest of network models, the Poisson random graph, studied as far back as the 1950s by Erdős, Rényi, and others SR51 ; ER60 , has a symmetric adjacency matrix whose elements are independent identically-distributed random variables. Such matrices are known, subject to some conditions but regardless of the precise distribution of their elements, to have a universal spectrum obeying the Wigner semicircle law, and eigenvectors that are distributed isotropically at random, except for the leading eigenvalue and eigenvector, whose values are governed by the Perron–Frobenius theorem and the average degree of the network arnold1971wigner ; furedi1981eigenvalues ; anderson2010introduction ; bai2010spectral ; vanMieghem11 ; erdos2011spectral ; tao2011topics ; tao2012random .

As we have come to understand in the last decade, however, the random graph is a poor model for the structure of real-world networks. In particular, the frequency distribution of the degrees of vertices in the random graph is Poissonian, while the degree distribution of most real-world networks is highly right-skewed, often having a power-law or exponential tail of “hubs” with degree far above the mean. Luckily, it turns out to be possible to create generalizations of the basic random graph that incorporate arbitrary degree distributions, including skewed distributions, the best-known such model being the so-called configuration model Bollobas80 ; MR95 . The configuration model is solvable exactly for many of its structural properties, including its complete component structure MR95 ; MR98 ; NSW01 and percolation properties CEBH00 ; CNSW00 , and the results have led us to a better understanding of the profound effect the degree distribution has on network topology.

In this paper we study the spectral properties of the configuration model. Motivated by recent developments in random matrix theory, we derive a simple recipe for calculating the spectrum of the adjacency matrix of the model. We show that the spectrum is composed of three fundamental elements, all of which have clear correlates in the structure of the network. The elements are: (1) the leading eigenvalue, which is dictated primarily by the average network degree; (2) a continuous band or “bulk spectrum,” analogous to the Wigner semicircle but taking a different shape; and (3) in some but not all cases, additional eigenvalues outside of the continuous band which correspond to the hubs in the network and which have eigenvectors that are strongly localized about those hubs.

In addition to our analytic developments, we also confirm the form and behavior of each of these elements with numerical calculations on example networks generated using the configuration model.

A number of previous authors have examined the spectral properties of the configuration model. Farkas et al. FDBV01 performed numerical calculations on large samples generated using the model and demonstrated that there are clear deviations from the semicircle law for non-Poisson choices of the degree distribution, and especially for power-law distributions. Dorogovtsev et al. DGMS03 gave an analytic route to the full spectrum, though their method is complex, involving the solution of a nonlinear integral equation containing Bessel functions, which at present can only be done approximately. Chung et al. CLV03 gave a rigorous derivation of the expected value of the largest eigenvalue in the spectrum in the limit of a dense network. Our calculations extend these studies by providing a simple derivation of the full spectrum which is exact in the limit of large vertex degrees and confirms earlier findings while shedding new light on features of the spectrum and their implications for network structure.

II The model

In this paper we study the spectral properties of the configuration model—or, more precisely, a slight variant of the model, as we now describe.

The configuration model is a model of an undirected random graph with a specified number of vertices and a given degree sequence. In this model one first specifies a degree sequence, meaning one specifies the degree of each of the vertices. Let the degree of vertex be denoted and let us visualize the degree as ends or “stubs” of edges emerging from the vertex. Then the configuration model is defined as the ensemble of pairwise matchings of stubs in which every matching appears with equal probability. That is, a configuration model network with the given degree sequence is generated by repeatedly choosing two stubs uniformly at random from those available and joining them together to form a complete edge. This process continues until all stubs have been joined and no unattached stubs remain. (For this to work, the number of stubs must be even, and hence the model is defined only for degree sequences whose sum is even.)

The configuration model provides a way to generate networks that have any degree sequence we desire while being essentially random in other respects—there are no correlations or long-range structure in the configuration model ensemble.

A crucial feature of the configuration model for our purposes will be the expected number of edges between a vertex pair. It is straightforward to show, given the degree sequence, that the expected number of edges between vertices and is equal to in the limit of large network size, where is the number of edges in the network. Note that it is possible to generate networks with multi-edges—pairs of vertices connected by more than one parallel edge. The actual number of edges between vertices and is multinomially distributed with mean .

However, edges in the configuration model are not statistically independent. Since the degrees of vertices are fixed, the presence of an edge from vertex to vertex makes it less likely that there will be an edge from to any other vertex, and hence edges that share a common end are correlated. When degree is large the correlations become small and the multinomial distribution of edge number becomes approximately Poisson, but for networks with finite average degree the correlations will always be present and may be significant.

These correlations make analysis of the model more difficult and so in this paper we consider a modified model in which the number of edges between each pair of vertices is defined to be an independent random variable with mean and value drawn from a Poisson distribution with that mean. In this model, becomes the expected degree of vertex and is the expected total number of edges. When degrees become large, which is the primary regime that we consider in this paper, the actual degrees will be narrowly peaked about their expected values, so the properties of the variant model and the standard configuration model, including the spectral properties that we study, become the same. This model (or slight variants of it) has been studied previously by a number of authors, notably Chung and Lu CL02b , with whose work it is perhaps most strongly associated.

In this paper we consider networks in the limit of large size with expected vertex degrees drawn from a fixed probability density , so that is the fraction of vertices with expected degree in the interval from to . (Note that expected degree need not be an integer, although one is free to choose it to have integer values if one wishes.) More precisely, we consider a sequence of networks of increasing size with fixed expected degrees and additional degrees drawn from as becomes larger. Thus for finite the expected degree of any particular vertex remains constant as becomes large and the empirical degree distribution converges to in the large- limit.

The adjacency matrix of a network generated according to this model is the symmetric matrix with integer elements equal to the number of edges between vertices and . Our primary goal in this paper is to calculate the average spectrum of the adjacency matrix within the model ensemble, which we do in two stages. We write the matrix as

| (1) |

where is the ensemble average of , which has elements , and is the deviation from that average. Our approach is first to calculate the spectrum of the matrix , whose elements are, by definition, independent random variables with zero mean, although crucially they are are not identically distributed. Once we have the spectrum of then the spectrum of is calculated from it in a separate step.

The matrix is of interest in its own right. It has elements

| (2) |

This matrix is known as the modularity matrix, and forms the basis for one of the most widely used methods for detecting modules or communities in networks Newman06b ; Fortunato10 . The methods described in this paper thus give us the spectra of both the adjacency matrix and the modularity matrix.

Note that the elements of the modularity matrix have variance the same as the elements of the adjacency matrix which, since they are Poisson distributed, have variance equal to their mean . Hence

| (3) |

which will be important shortly.

III Spectrum of the modularity matrix

As discussed in the previous section, we will first calculate the spectrum of the modularity matrix , defined by Eq. (2), then calculate the spectrum of the adjacency matrix from it in a separate step. We begin by developing some fundamental notions concerning random variables that will be important for our derivations.

Suppose we have two independent random variables, and , ordinary scalar variables, with probability densities and . What is the probability that their sum will have a particular value ? The answer to this question is well known and simple. The probability density for is

| (4) |

which is the convolution of the two distributions. Similarly we can ask for the probability that the product has value , which is given by the multiplicative convolution

| (5) |

A scalar random variable can be thought of as the single eigenvalue of a random matrix. A matrix is diagonal by definition and its one eigenvalue is trivially equal to its one element. A natural generalization of the convolution results above is to ask what their equivalent is for larger random matrices, , , and so forth, where we will confine ourselves to symmetric matrices, so that the eigenvalues are real. That is, if we know the probability density of the eigenvalues—the so-called spectral density—of two independent symmetric random matrices, what is the spectral density of their sum or product? The answer is no longer a simple convolution, because matrices do not in general commute, so what is the appropriate generalization? Unfortunately, this question does not have a straightforward answer because it turns out that a knowledge of the spectral densities alone is not enough. In general one needs to know the distribution of the entire matrices to calculate the spectral density of their sum or product. There is, however, one case in which relatively simple results apply, which is when the eigenvectors of the two matrices are themselves random and uncorrelated.

Recall that the eigenvectors of a symmetric matrix are orthogonal—for an matrix they define a set of orthogonal axes in an -dimensional vector space. Thus if we have two random symmetric matrices, the eigenvectors of one can always be transformed into the eigenvectors of the other by a suitable rotation and/or reflection—in other words by a suitable unitary transformation. If for different choices of the random matrices the transformations needed to do this are distributed isotropically—if all possible such transformations are equally likely—then the random matrices are said to be free. Loosely, one can say that two random matrices are free if the angle between their eigenvectors is also random. The mathematics of free random variables has been developed extensively since the 1990s and is known by the name of free probability theory voiculescu1992free .

The crucial observation now is the following: for free matrices the spectral density of their sum or product is a function only of the individual spectral densities. It turns out that one no longer needs to know the entire distribution of the matrices themselves and well-defined generalizations of the convolution equations, Eqs. (4) and (5), exist. For the sum of two matrices the appropriate generalization is known as the free convolution or free additive convolution; for the product of matrices it is the free multiplicative convolution. Thus if two symmetric random matrices have spectral densities and , then the spectral density of their product is the free multiplicative convolution

| (6) |

where denotes the convolution. Although this defines the convolution in principle, it does not tell us how to calculate it. We will come to that in a moment, but first let us return to the configuration model and see why this is a useful result.

We wish to calculate the spectral density of the modularity matrix , which for an undirected network is a symmetric random matrix whose elements have zero mean but different variances, equal to —see Eq. (3). Let us define a normalized modularity matrix by

| (7) |

where is the diagonal matrix with elements . has elements , so that each is divided by a factor proportional to its standard deviation and hence, though not identically distributed, all elements now have the same variance, equal to . So long as the vertex degrees are large, matrices with this property are known to have an eigenvector basis oriented isotropically at random and to have spectral density obeying the Wigner semicircle law arnold1971wigner ; furedi1981eigenvalues ; anderson2010introduction ; bai2010spectral ; vanMieghem11 ; erdos2011spectral ; tao2011topics ; tao2012random , which for our particular matrix takes the form

| (8) |

where is the average degree in the network. The requirement that vertex degrees be large is necessary because deviations from the semicircle law are known to arise for very sparse matrices RB88 . For small degrees, therefore, the results given here will only be approximate.

Now consider an eigenvalue of the modularity matrix itself, satisfying where is the corresponding eigenvector. Multiplying by , writing , and defining , this can also be written

| (9) |

In other words the modularity matrix has the same eigenvalues as the matrix , which is the product of the diagonal matrix , which by definition has spectral density equal to the degree distribution , and the symmetric matrix , with spectral density given by Eq. (8).

But it is precisely to the products of such random matrices that Eq. (6) relates, and hence, applying that equation, we arrive at the principal result of this paper: the spectral density of the modularity matrix for a network with arbitrary expected degrees is equal to the free multiplicative convolution of the degree distribution with the Wigner semicircle. That is, the spectral density is given by

| (10) |

where is the distribution of expected degrees and is given by Eq. (8).

This result is of immediate practical utility. Numerical methods exist for computing free multiplicative convolutions efficiently rao2008polynomial ; olver2012numerical , which means we can use existing numerical packages to compute spectral densities easily and rapidly for a wide range of degree distributions.

For the purposes of the present paper, however, we would like to know more. In particular, we would like explicit formulas for calculating the spectral density in the general case. Unfortunately, the free multiplicative convolution has no simple expression for matrices of finite size, but in the limit of large size—which is also the limit of a large network—suitable expressions do exist. Specifically, for a spectral density we can define a function

| (11) |

which is called the Cauchy transform of . Then if is the free multiplicative convolution of two other distributions and as in Eq. (10), it can be shown that

| (12) |

where denotes the functional inverse of , and and are defined by analogy with (11):

| (13) |

Substituting Eq. (8) into the second of these, we have

| (14) |

The ambiguity in the sign of the square root arises because of a branch cut in the evaluation of the integral, but it can be shown that the final result for the free convolution never depends on the choice of sign rao2007multiplication . Here we take the negative sign, since it makes some of the following steps cleaner. Rearranging for as a function of we then find that the functional inverse is

| (15) |

and substituting into (12) we get

| (16) |

Evaluating this equation at the point gives , which can be rearranged to read

| (17) |

For convenience we define and Eq. (17) becomes

| (18) |

or, more simply,

| (19) |

If we can solve this equation for then the Cauchy transform of , Eq. (11), is given by . To recover itself from the Cauchy transform we note that for real and

| (20) |

which is a Lorentzian of width and area 1, and hence in the limit as becomes equal to a delta-function:

| (21) |

Thus

| (22) |

This is the Stieltjes–Perron inversion formula. Setting it tells us that the spectral density of the configuration model is given by

| (23) |

where the imaginary part is taken in the limit as tends to the real line from above.

Equations (19) and (23) give us a complete recipe for calculating the spectrum of the modularity matrix. We note that equations equivalent to these have been derived in other contexts in the literature on random matrices. See for example the results on band matrices in Refs. molchanov1992limiting ; shlyakhtenko1996random ; anderson2006clt ; casati2009wigner ; bai2010limiting .

III.1 Example solutions

The solution of Eqs. (19) and (23) relies on our being able to compute the integral in Eq. (19), whose difficulty depends on the particular choice of degree distribution. To give an example where the calculation is straightforward, consider the standard Poisson random graph, for which all vertices have the same expected degree and hence . Substituting into (19) and solving the resulting quadratic equation gives

| (24) |

so that the spectral density is

| (25) |

which recovers the standard semicircle distribution for the random graph.

As a more general example, consider any distribution where the degrees take a set of discrete values , as they do for any integer-valued degree distribution of the type commonly considered for network models. Then , where the coefficients satisfy . Then, from Eq. (19),

| (26) |

where we have used . Thus is the root of a polynomial of degree . For instance, if there are two discrete values of the expected degree, then

| (27) |

which can be rearranged to give the cubic equation

| (28) |

Of the three solutions to this equation one is always real, and hence (in light of Eq. (23)) cannot give the spectral density. The remaining two are complex conjugates and so give results that differ only in sign, the positive sign being the one we are looking for.

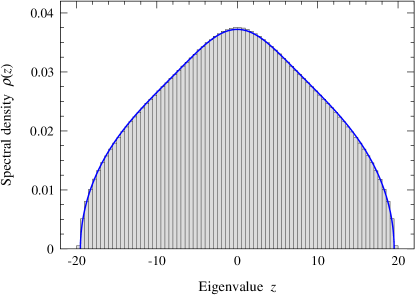

Figure 1 shows a plot of the resulting spectral density, Eq. (23), as a function of for the case , , and . The figure shows strong departure from the semicircle law. Also shown are the results of direct numerical calculations of the spectra of simulated networks with the same degree distribution and the agreement between the analytic and numerical results is good.

III.2 Features of the spectral density

We can invoke additional properties of the free convolution to better understand the spectrum of the modularity matrix. Consider, for instance, the case where the expected degree distribution has compact support, meaning that there are hard upper and lower limits to the expected degree a vertex may have. (The lower limit is trivial, since degrees must be non-negative, but the upper limit is not.) Since the semicircle distribution, Eq. (8), also has compact support, the spectral density of the modularity matrix is then a convolution of two compact distributions. In this scenario it can be shown that the bulk spectrum of the modularity matrix will also have compact support bai2010limiting . Furthermore, given this observation we can show that the spectrum will generically exhibit a sharp square-root decay at its edges. To see this, note that the central function in our theory is the solution for of an equation of the form where is given and

| (29) |

(See Eq. (19).) From Eq. (23) we know that is complex within the spectral band and real outside it and hence the edge of the band is the point at which complex solutions to disappear. For analytic such a disappearance corresponds to the point at which an extremum of with respect to crosses the zero line. Denoting this point by and performing an expansion about it to leading order in both and , we then have

| (30) |

the terms in and vanishing at the extremum. In the limit as we approach the band edge, therefore, the equation takes the form

| (31) |

and hence, within the band, we have for some real constant . Then the spectral density, Eq. (23), is

| (32) |

where is another real constant. A similar argument implies square-root behavior at the lower edge of the spectrum as well. The square-root form can be seen, for example, in the vertical sides of the spectrum in Fig. 1.

We can also calculate the behavior of as from above, for which Eq. (31) implies

| (33) |

with the same real constant as before. Note that this implies that the limiting value of at the band edge is generically finite, but that the slope diverges. This has important consequences for “hub” vertices—those with unusually high degree—whose effect on the spectrum displays a phase transition behavior that depends crucially on the functional form of . We discuss hub vertices in detail in Section VI.

These results apply for the case where the expected degree distribution is bounded. In cases where it is not we expected the spectral density of the modularity matrix to be similarly unbounded, having no band edge and generically inheriting the worst-case tail behavior of . Similar observations have been made previously by Chung et al. CLV03 for a different matrix, the graph Laplacian. They note that a normalized version of the Laplacian, akin to our normalized modularity matrix , should display a semicircle distribution, but that the Laplacian itself should have a spectrum that inherits the tail behavior of the degree distribution.

IV The resolvent and the Stieltjes transform

In the previous section we calculated the spectral density of the modularity matrix for the configuration model. It is possible to calculate many other properties of the spectrum as well, as we now show. Our starting point for these calculations is the so-called resolvent matrix, which is the matrix function , where is the identity. As we will see, a knowledge of the ensemble average of the resolvent allows us to calculate many things, including the spectral density of the adjacency matrix, the leading eigenvalue of the adjacency matrix, and the effect on the spectrum of network hubs.

It also gives us an alternative, though perhaps less elegant, derivation of the results for the modularity matrix in the previous section. The spectral density of the modularity matrix can be defined as

| (34) |

where are the eigenvalues of the matrix. Substituting for the delta-function from Eq. (21), we get the so-called Plemelj–Sokhotski formula

| (35) |

Via a change of basis, the sum on the right-hand side is equal to the trace of the matrix , and hence is the limit where goes to the real line of . In other words, the spectral density depends on the trace of the resolvent, and its average over the ensemble of model networks is given by the average of this quantity:

| (36) |

The normalized trace is called the Stieltjes transform of .

The two most common ways to calculate the Stieltjes transform are either to expand the matrix in powers of and take the trace term by term, or to write the trace in terms of derivatives of a Fresnel integral and then employ the replica trick EJ76 . Here, however, we take a different approach inspired by work of Bai and Silverstein bai1999methodologies ; bai2010spectral that allows us to calculate the average of the full resolvent.

The resolvent is the inverse of a matrix whose off-diagonal elements are zero-mean random variables. Consider a general such matrix and let us write it in terms of its first rows and columns, plus the last row and column, thus:

| (37) |

Thus is the matrix with the th row and column removed, and is the th column minus its last element .

Now consider the vector , where . Let us break into its first elements and its last element , where clearly . Then we have and hence

| (38) |

The first equation tells us that

| (39) |

and substituting this result into the second gives

| (40) |

To make further progress we assume that is narrowly peaked about its average value in the limit of large system size, meaning its variance about that value vanishes as becomes large. We will for the moment take this assumption as given, but it can be justified using results for concentration of measure of random quadratic forms karoui2011geometric , which apply provided vertex degrees are large (so that our results, like those of Section III, will be exact only for large degrees).

If is narrowly peaked then the average of the reciprocal on the right-hand side of (40) is equal to the reciprocal of the average and

| (41) |

Furthermore, if is narrowly peaked then the average of Eq. (39) is since is independent of and . But the elements of are equal to and hence

| (42) |

for . By the same method we can derive expressions for the inverse of with any row and column removed and hence show that

| (43) |

and

| (44) |

In other words, is a diagonal matrix when is large, with diagonal elements given by Eq. (43).

But if this is true of , then by the same argument it must also be true of . Hence, noting that is independent of , we have

| (45) |

Returning now to Eq. (36), the role of the matrix in our problem is played by . As we noted earlier, the elements of the modularity matrix (and hence also the elements of the vector ) have mean zero and variance . Hence in Eq. (45) and

| (46) |

where is the diagonal matrix with elements and is the same matrix with the th row and column removed.

However, if tends to a well-defined limit as the network becomes large, then in this limit it must equal —the omission, or not, of the th row and column makes a vanishing difference for large . Hence (43) becomes

| (47) |

where we have made use of the fact that . At the same time, the off-diagonal elements of are zero by Eq. (44), so the average of the resolvent matrix is diagonal, a result that will be crucial for several following developments.

Without loss of generality, we now label the vertices of our network in order of increasing expected degree, and for convenience we define functions and of the continuous variable thus:

| (48) |

Then for large Eq. (47) becomes

| (49) |

where is the average degree, as previously.

The spectral density, Eq. (36), is related to by

| (50) |

where

| (51) |

which is just the ensemble average of the Stieltjes transform. To calculate , we define the additional quantity

| (52) |

where we have used Eq. (49). Since we have labeled our vertices in order of increasing degree, is by definition the th-lowest degree in the network, or equivalently it is the functional inverse of the cumulative distribution function defined by

| (53) |

where is the expected degree distribution. Thus, changing variables from to , Eq. (52) can be written

| (54) |

or as either of the equivalent forms

| (55) |

where the (correctly normalized) probability distribution

| (56) |

is known as the excess degree distribution in the networks literature. This distribution, which arises often in the theory of networks, is the probability that the network vertex reached by following an edge has an expected number of edges attached to it other than the one we followed to reach the vertex. (The distribution looks slightly different from the form usually given NSW01 because it is expressed in terms of expected degree rather than actual degree.)

If we can solve Eq. (55) for then we can calculate by substituting Eq. (49) into Eq. (51) and again changing variables from to , to get

| (57) |

This equation is similar in form to Eq. (55), but note that it is the ordinary degree distribution that appears in the numerator, not the excess degree distribution.

Alternatively, and more directly, we can calculate by multiplying both sides of (49) by the right-hand denominator, integrating, and rearranging, to get

| (58) |

Combining this result with Eq. (50) now gives us the spectral density:

| (59) |

where the imaginary part is, if necessary, calculated as the limit where tends to the real line from above.

V Spectrum of the adjacency matrix

In the previous sections we have derived the spectral density of the modularity matrix. To calculate the corresponding quantity for the adjacency matrix we make use of an argument of CDF09 ; BN11 as follows. The adjacency matrix can be written in terms of the modularity matrix as , where is the -element vector with elements . Hence any eigenvalue/vector pair of the adjacency matrix satisfies

| (60) |

which can be rearranged to read

| (61) |

Multiplying by , we then find that

| (62) |

Expanding as a linear combination of the eigenvectors of , this result can be written

| (63) |

where are the eigenvalues of the modularity matrix.

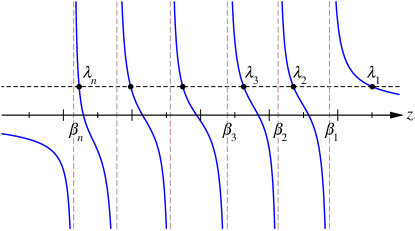

The solutions of this equation can be visualized as in Fig. 2. The solid curves represent the left-hand side of the equation, which has poles as shown at for all . The dashed horizontal line represents the 1 on the right-hand side and the points at which it intercepts the curves are the solutions for of (63), which are the eigenvalues of the adjacency matrix. If we number the eigenvalues of both and in order from largest to smallest, the geometry of Fig. 2 implies that the eigenvalues must satisfy an interleaving condition of the form . In the limit of large , where the spectral density of the modularity matrix becomes a smooth function and the eigenvalues are arbitrarily closely spaced, this implies that , so that asymptotically the spectral density of the adjacency matrix is the same as that of the modularity matrix.

The only exception is the highest eigenvalue of the adjacency matrix , which is bounded below by , but unbounded above. To calculate this value we average (62) over the ensemble and recall, as demonstrated in Section IV, that is diagonal, and hence

| (64) |

Combining this result with (62) and using Eq. (48) we then have

| (65) |

Taking Eq. (49), multiplying by the right-hand denominator and a further factor of , then integrating over , we get

| (66) |

And combining this result with Eq. (65) and noting that , we have

| (67) |

The solution of this equation for gives us the leading eigenvalue of the adjacency matrix.

For the Poisson random graph, for example, this result, in combination with Eq. (24), tells us that the leading eigenvalue takes the value . This is not a new result—it is well known in the literature—but it is comforting to see that the formalism works.

For the two-degree model of Eq. (27), we can use (67) to eliminate from (27) and get

| (68) |

which gives us a cubic equation for . For the parameter values used in Fig. 1, for example, , , and , we find that the leading eigenvalue of the adjacency matrix is A numerical calculation for the same parameters is in good agreement, giving for an average over 100 systems of size .

For the case of general degree distribution, we can use (67) to eliminate in Eq. (55) to get

| (69) |

An exact solution to this equation requires us to perform the integral, but one can derive an approximate solution by expanding the denominator of the integrand:

| (70) |

or

| (71) |

where denotes an average over the excess degree distribution of Eq. (56). If , where is the largest degree in the network, and noting that , we have

| (72) |

or

| (73) |

to leading order, where we have made use of . This result was derived previously by other means by Chung et al. CLV03 .

VI Network hubs

The picture developed in the previous sections is one in which the spectrum of the adjacency matrix has two primary components: a single leading eigenvalue plus a continuous band of lower eigenvalues, which it shares with the modularity matrix.

Let us examine more closely the continuous band and concentrate on the case of the modularity matrix, which is simpler since it has only the band and no separate leading eigenvalue. Consider the eigenvalues that lie at the topmost edge of the band, which are the highest eigenvalues of the modularity matrix. These eigenvalues are normally associated with good bisections of the network into “communities”—if a good bisection exists then there will be a corresponding high-lying eigenvalue whose eigenvector’s elements describe the split Newman06b .

As we now argue, however, there is another mechanism that generates high-lying eigenvalues, namely the presence of hubs in the network—vertices of unusually high degree—and the highest eigenvalues in the spectrum of the modularity matrix, and also the lowest, are often due to these hubs, while those corresponding to communities are somewhat smaller. As we will see, for hubs of sufficiently high degree, these eigenvalues can split off from the continuous band in a manner reminiscent of impurity states in condensed matter physics. In effect, the hub acts as an impurity in the network.

To see how the addition of a hub to a network produces a high-lying eigenvalue, let the hub be vertex and let once again be the modularity matrix without the th vertex (i.e., with the th row and column removed), so that the full modularity matrix looks like this:

| (75) |

Now, in an argument analogous to that of the previous section, consider an eigenvector of this matrix . Then the eigenvector equation can be multiplied out to give the equations

| (76) | ||||

| (77) |

The first of these can be rearranged to give

| (78) |

Then multiplying by and using the second equation gives

| (79) |

Now we note that the th element of is an independent random variable with variance and we can average over the ensemble and apply Eq. (45) to rewrite the left-hand side, giving

| (80) |

where is the diagonal matrix with elements as before, is the same matrix with the th row and column removed, and we have made use of the fact that . We note, as previously, that if the quantity tends to a limit as the network becomes large, then that limit is equal to the function defined in Eq. (52). Thus the eigenvalue satisfies

| (81) |

Substituting this expression into Eq. (55) and rearranging, we get an explicit expression for the eigenvalue thus:

| (82) |

This calculation also extends to the case where there is more than one hub in the network. Because the hub is treated no differently from any other network vertex, the same arguments apply if we add a second hub, or more, after the first. Equation (82) will give the correct eigenvalue for each hub separately.

Once again, our ability to actually solve for the value of will depend on whether we can do the integral in Eq. (82) (although one could also evaluate the integral numerically). In the special case where the hub degree is much larger than the expected degree of any of the other vertices, so that in the denominator of the integrand, the expression simplifies to

| (83) |

and hence .

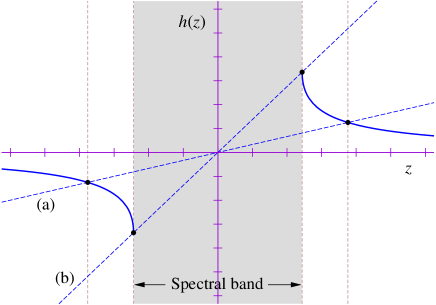

The solutions of Eq. (81) can be represented graphically as in Fig. 3. The curves in the figure represent the function and the diagonal lines represent . The point where the two cross give the eigenvalues. As the figure shows, when the expected degree of the th vertex is large enough, the equation has two solutions, one for low and one for high and both given by Eq. (82), that are separate from the continuous spectrum of eigenvalues we calculated in Section III.

How high a degree does a hub have to have to generate eigenvalues of this kind? The answer can be seen from Fig. 3— must be large enough for the line to intercept the curve of . Thus there is a critical value of , represented by the steeper diagonal in the figure, below which the hub eigenvalues vanish. Below this point, the highest eigenvalue will fall at the edge of the continuous band as normal and there will be no special hub eigenvalue. We can derive an expression for the transition point by observing that, as shown in Section III.2, the slope of diverges at the band edge, which implies that . Differentiating Eq. (82) and setting the result to zero, we find that the critical value of is the solution of

| (84) |

For example, in the case of the Poisson random graph this implies that the transition takes place at the point where , i.e., when . Thus we must have for the hub to have an effect on the spectrum.

This gives us a working definition of what we mean by a “hub” in a network. It depends, not surprisingly, on the degree distribution of the rest of the network—what it takes to stand out in a crowd depends on the rest of the crowd. But in the Poisson random graph, for instance, a hub is a hub, in spectral terms, if its degree is greater than twice the average in the rest of the network. This is a somewhat surprising result, given that vertices of high degree are easily spotted long before this point is reached, at least for large . Since the standard deviation of the degree distribution is , a vertex with degree twice the mean is standard deviations above the mean, which is a large number for large .

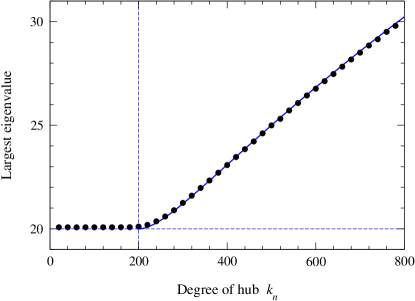

Nonetheless, the result does appear to be correct. Figure 4 shows the results of numerical calculations of the largest eigenvalue of the modularity matrix for a Poisson random graph with a single additional hub of expected degree , as a function of . As the figure shows, the eigenvalue obeys Eq. (82) quite closely until falls below (the vertical dashed line). Past this point, the leading eigenvalue assumes the same value as in a standard Poisson random graph with no hub (the horizontal line), even though the hub may still be present.

Putting together our principal observations, we have now developed quite a complete picture of the spectrum of the configuration model. We expect the spectrum to have two main parts, plus a third when the degree distribution implies the presence of hubs:

-

1.

There is a single eigenvalue given by the solution of Eq. (67), which will normally be the leading eigenvalue.

-

2.

There is a continuous band, given by Eq. (23). For bounded degree distributions the band will also be bounded, both above and below, and have edges that decay to zero as a square root.

-

3.

If there are hubs in the network, then there will be additional eigenvalues outside the band at both ends, given by Eq. (82). Each hub contributes two eigenvalues, one at each end of the band.

VI.1 Localization around hubs

One can also look at the eigenvector corresponding to a hub eigenvalue, which turns out to be heavily localized around the hub vertex. All the elements of the eigenvector, except for the element corresponding to the hub itself, are given in terms of by Eq. (78). For given , the expected value of the th component is

| (85) |

where we have once again made use of the fact that is diagonal (see Eq. (44)).

The th element of the vector takes the value for vertices that are connected to the hub and for those that are not. Hence, in the limit of large , eigenvector elements corresponding to neighbors of the hub will be of order a constant, with expected value

| (86) |

with given by Eq. (82), while the remaining elements will be of order .

The value of can be determined by insisting that the complete eigenvector be normalized. Using Eq. (78) we can write the normalization condition in the form

| (87) |

When we average over the ensemble we have, by analogy with Eq. (46),

| (88) |

and hence (87) implies that

| (89) |

where denotes the first derivative of , and we are assuming once again that the vector element is narrowly peaked about its expected value. Note that is negative at both the positive and negative band edges, and diverges to as we approach the band edge. Thus as we approach the transition at the which the hub eigenvalue disappears.

The results above apply to the hub eigenvectors at both ends of the spectral band, there being two eigenvalues for each hub vertex, one at either end, as shown in the previous section. Both eigenvectors will have a single element of order 1 in the position corresponding to the hub itself, elements of order in the positions corresponding the neighbors of the hub (see Eq. (86)), and all other elements of order . In other words, the both eigenvectors are strongly localized in the neighborhood of the hub. The only qualitative difference between the two eigenvectors is in the sign of the elements corresponding to the neighbors which, because of Eq. (86), will have the same sign as for the positive eigenvalue and the opposite sign for the negative one.

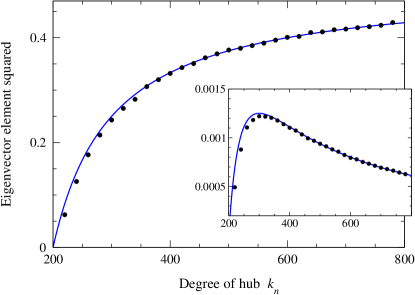

As an example, consider again the Poisson random graph, for which is given by Eq. (24) and is given by Eq. (82) to be , so that and the expected values of the eigenvector elements at both ends of the spectrum satisfy

| (90) |

in the limit of large network size. Figure 5 shows a comparison of these predictions with numerical results for actual networks. As the figure shows, the agreement is once again good, although, as with some of the other calculations, there are small disparities close to the transition at which the hub eigenvalue meets the band edge (which is at in this case).

VII Conclusions

In this paper we have studied the spectra of the adjacency and modularity matrices of random networks with given expected degrees. Our principal findings are that the spectral densities of the adjacency and modularity matrices are the same in the limit of large system size, except that the adjacency matrix has an additional highest eigenvalue, and that the spectral densities are given by the free multiplicative convolution of the degree distribution with a Wigner semicircle distribution. We have confirmed these results with numerical studies of actual networks generated according to the model. The spectra show strong departures from the classical semicircle law, in agreement with numerical studies by previous authors.

We have also studied the effect of network hubs, vertices of unusually high degree, and find that when their degree is sufficiently large these give rise to eigenvalues outside the main band of the spectrum, akin to impurity states in condensed matter systems. We have derived an explicit formula for these hub eigenvalues and we show that the corresponding eigenvectors are strongly localized around the hubs themselves.

In addition to their relevance to partitioning, community structure, and dynamical systems on networks, the techniques developed here could form a starting point for spectral calculations in more elaborate networks. There has, for instance, been recent interest in the spectral properties of community structured networks CGO09 ; NN12 , but calculations have been limited to models with Poisson degree distribution. Applications of the methods presented here to such networks could lead to new results for structured networks with nontrivial degree distributions.

Acknowledgements.

The authors thank Lenka Zdeborova for useful conversations. This work was funded in part by the National Science Foundation under grants CCF–1116115 and DMS–1107796 and by the Army Research Office under MURI grant W911NF–11–1–0391.References

- (1) M. E. J. Newman, The structure and function of complex networks. SIAM Review 45, 167–256 (2003).

- (2) S. Boccaletti, V. Latora, Y. Moreno, M. Chavez, and D.-U. Hwang, Complex networks: Structure and dynamics. Physics Reports 424, 175–308 (2006).

- (3) M. Fiedler, Algebraic connectivity of graphs. Czech. Math. J. 23, 298–305 (1973).

- (4) A. Pothen, H. Simon, and K.-P. Liou, Partitioning sparse matrices with eigenvectors of graphs. SIAM J. Matrix Anal. Appl. 11, 430–452 (1990).

- (5) B. Bollobás, C. Borgs, J. Chayes, and O. Riordan, Percolation on dense graph sequences. Annals of Probability 38, 150–183 (2010).

- (6) M. E. J. Newman, Modularity and community structure in networks. Proc. Natl. Acad. Sci. USA 103, 8577–8582 (2006).

- (7) S. Fortunato, Community detection in graphs. Phys. Rep. 486, 75–174 (2010).

- (8) A. Arenas, A. Díaz-Guilera, J. Kurths, Y. Moreno, and C. Zhou, Synchronization in complex networks. Physics Reports 469, 93–153 (2008).

- (9) A. Barrat, M. Barthélemy, and A. Vespignani, Dynamical Processes on Complex Networks. Cambridge University Press, Cambridge (2008).

- (10) I. J. Farkas, I. Derényi, A.-L. Barabási, and T. Vicsek, Spectra of “real-world” graphs: Beyond the semicircle law. Phys. Rev. E 64, 026704 (2001).

- (11) R. Solomonoff and A. Rapoport, Connectivity of random nets. Bulletin of Mathematical Biophysics 13, 107–117 (1951).

- (12) P. Erdős and A. Rényi, On the evolution of random graphs. Publications of the Mathematical Institute of the Hungarian Academy of Sciences 5, 17–61 (1960).

- (13) L. Arnold, On Wigner’s semicircle law for the eigenvalues of random matrices. Probability Theory and Related Fields 19, 191–198 (1971).

- (14) Z. Füredi and J. Komlós, The eigenvalues of random symmetric matrices. Combinatorica 1, 233–241 (1981).

- (15) G. Anderson, A. Guionnet, and O. Zeitouni, An Introduction to Random Matrices. Cambridge University Press, Cambridge (2010).

- (16) Z. Bai and J. Silverstein, Spectral Analysis of Large Dimensional Random Matrices. Springer, Berlin (2010).

- (17) P. van Mieghem, Graph Spectra for Complex Networks. Cambridge University Press, Cambridge (2011).

- (18) L. Erdos, A. Knowles, H. Yau, and J. Yin, Spectral statistics of Erdős–Rényi graphs I: Local semicircle law. Preprint arXiv:1103.1919.

- (19) T. Tao, Topics in Random Matrix Theory. American Mathematical Society, Providence, RI (2012).

- (20) T. Tao and V. Vu, Random matrices: The universality phenomenon for Wigner ensembles. Preprint arXiv:1202.0068.

- (21) B. Bollobás, A probabilistic proof of an asymptotic formula for the number of labelled regular graphs. European Journal of Combinatorics 1, 311–316 (1980).

- (22) M. Molloy and B. Reed, A critical point for random graphs with a given degree sequence. Random Structures and Algorithms 6, 161–179 (1995).

- (23) M. Molloy and B. Reed, The size of the giant component of a random graph with a given degree sequence. Combinatorics, Probability and Computing 7, 295–305 (1998).

- (24) M. E. J. Newman, S. H. Strogatz, and D. J. Watts, Random graphs with arbitrary degree distributions and their applications. Phys. Rev. E 64, 026118 (2001).

- (25) R. Cohen, K. Erez, D. ben-Avraham, and S. Havlin, Resilience of the Internet to random breakdowns. Phys. Rev. Lett. 85, 4626–4628 (2000).

- (26) D. S. Callaway, M. E. J. Newman, S. H. Strogatz, and D. J. Watts, Network robustness and fragility: Percolation on random graphs. Phys. Rev. Lett. 85, 5468–5471 (2000).

- (27) S. N. Dorogovtsev, A. V. Goltsev, J. F. F. Mendes, and A. N. Samukhin, Spectra of complex networks. Phys. Rev. E 68, 046109 (2003).

- (28) F. Chung, L. Lu, and V. Vu, Spectra of random graphs with given expected degrees. Proc. Natl. Acad. Sci. USA 100, 6313–6318 (2003).

- (29) F. Chung and L. Lu, The average distances in random graphs with given expected degrees. Proc. Natl. Acad. Sci. USA 99, 15879–15882 (2002).

- (30) D. Voiculescu, K. Dykema, and A. Nica, Free Random Variables, Volume 1. American Mathematical Society, Providence, RI (1992).

- (31) G. J. Rodgers and A. J. Bray, Density of states of a sparse random matrix. Phys. Rev. B 37, 3557–3562 (1988).

- (32) N. Rao and A. Edelman, The polynomial method for random matrices. Foundations of Computational Mathematics 8, 649–702 (2008).

- (33) S. Olver and R. Nadakuditi, Numerical computation of convolutions in free probability theory. Preprint arXiv:1203.1958.

- (34) N. Rao and R. Speicher, Multiplication of free random variables and the -transform: The case of vanishing mean. Electronic Communications in Probability 12, 248–258 (2007).

- (35) S. Molchanov, L. Pastur, and A. Khorunzhii, Limiting eigenvalue distribution for band random matrices. Theoretical and Mathematical Physics 90, 108–118 (1992).

- (36) D. Shlyakhtenko, Random Gaussian band matrices and freeness with amalgamation. International Mathematics Research Notices 20, 1013–1025 (1996).

- (37) G. Anderson and O. Zeitouni, A CLT for a band matrix model. Probability Theory and Related Fields 134, 283–338 (2006).

- (38) G. Casati and V. Girko, Wigner’s semicircle law for band random matrices. Random Operators and Stochastic Equations 1, 15–22 (2009).

- (39) Z. Bai and L. Zhang, The limiting spectral distribution of the product of the Wigner matrix and a nonnegative definite matrix. Journal of Multivariate Analysis 101, 1927–1949 (2010).

- (40) S. F. Edwards and R. C. Jones, The eigenvalue spectrum of a large symmetric random matrix. J. Phys. A 9, 1595–1603 (1976).

- (41) Z. Bai, Methodologies in spectral analysis of large-dimensional random matrices: A review. Statist. Sinica 9, 611–677 (1999).

- (42) N. Karoui and H. Koesters, Geometric sensitivity of random matrix results: Consequences for shrinkage estimators of covariance and related statistical methods. Preprint arXiv:1105.1404.

- (43) M. Capitaine, C. Donati-Martin, and D. Féral, The largest eigenvalues of finite rank deformation of large Wigner matrices: Convergence and nonuniversality of the fluctuations. Annals of Probability 37, 1–47 (2009).

- (44) F. Benaych-Georges and R. R. Nadakuditi, The eigenvalues and eigenvectors of finite, low rank perturbations of large random matrices. Advances in Mathematics 227, 494–521 (2011).

- (45) S. Chauhan, M. Girvan, and E. Ott, Spectral properties of networks with community structure. Phys. Rev. E 80, 056114 (2009).

- (46) R. R. Nadakuditi and M. E. J. Newman, Graph spectra and the detectability of community structure in networks. Phys. Rev. Lett. 108, 188701 (2012).