A generalized mean-reverting equation and applications

Abstract.

Consider a mean-reverting equation, generalized in the sense it is driven by a -dimensional centered Gaussian process with Hölder continuous paths on (). Taking that equation in rough paths sense only gives local existence of the solution because the non-explosion condition is not satisfied in general. Under natural assumptions, by using specific methods, we show the global existence and uniqueness of the solution, its integrability, the continuity and differentiability of the associated Itô map, and we provide an -converging approximation with a rate of convergence (). The regularity of the Itô map ensures a large deviation principle, and the existence of a density with respect to Lebesgue’s measure, for the solution of that generalized mean-reverting equation. Finally, we study a generalized mean-reverting pharmacokinetic model.

Key words and phrases:

Stochastic differential equations, rough paths, large deviation principle, mean-reversion, Gaussian processesMSC2010 : 60H10.

Acknowledgements. Many thanks to my Ph.D. supervisor Laure Coutin for her precious help and advices. This work was supported by A.N.R. Masterie.

1. Introduction

Let be a -dimensional centered Gaussian process with -Hölder continuous paths on ( and ).

Consider the stochastic differential equation (SDE) :

| (1) |

where, is a deterministic initial condition, are deterministic constants and satisfies the following assumption :

Assumption 1.1.

The exponent satisfies : .

When the driving signal is a standard Brownian motion, equation (1) taken in the sense of Itô, is used in many applications. For example, it is studied and applied in finance by J-P. Fouque et al. in [6] for . The cornerstone of their approach is the Markov property of diffusion processes. In particular, their proof of the global existence and uniqueness of the solution at Appendix A involves S. Karlin and H.M. Taylor [10], Lemma 6.1(ii). Still for , the convergence of the Euler approximation is proved by X. Mao et al. in [17] and [25]. For , equation (1) is studied by F. Wu et al. in [25]. Recently, in [21], N. Tien Dung got an expression and shown the Malliavin’s differentiability of a class of fractional geometric mean-reverting processes.

Equation (1) is a generalization of the mean-reverting equation. In this paper, we study various properties of (1) by taking it in the sense of rough paths (cf. T. Lyons and Z. Qian [14]). Note that Doss-Sussman’s method could also be used since (1) is a -dimensional equation (cf. H. Doss [5] and H.J. Sussman [24]). A priori, even in these senses, equation (1) admits only a local solution because it doesn’t satisfy the non-explosion condition of [8], Exercice 10.56.

At Section 2, we state useful results on rough differential equations (RDEs) and Gaussian rough paths coming from P. Friz and N. Victoir [8]. Section 3 is devoted to study deterministic properties of (1). We show existence and uniqueness of the solution for equation (1), provide an explicit upper-bound for that solution and study the continuity and differentiability of the associated Itô map. We also provide a converging approximation with a rate of convergence. Section 4 is devoted to study probabilistic properties of (1) ; properties of the solution’s distribution, various integrability results, a large deviation principle and the existence of a density with respect to Lebesgue’s measure on for the solution of (1). Finally, at Section 5, we study a pharmacokinetic model based on a particular generalized mean-reverting (M-R) equation (inspired by K. Kalogeropoulos et al. [11]).

2. Rough differential equations and Gaussian rough paths

Essentially inspired by P. Friz and N. Victoir [8], this section provides useful definitions and results on RDEs and Gaussian rough paths.

In a sake of completeness, results on rough differential equations are stated in the multidimensional case.

In the sequel, denotes the euclidean norm on and the usual norm on .

Consider the set of subdivisions for and

Let be the step- tensor algebra over () :

For , is equipped with its euclidean norm , and the canonical projection on for any is denoted by .

First, let’s remind definitions of -variation and -Hölder norms ( and ) :

Definition 2.1.

Consider :

-

(1)

The function has finite -variation if and only if,

-

(2)

The function is -Hölder continuous if and only if,

In the sequel, the space of continuous functions with finite -variation will be denoted by :

The space of -Hölder continuous functions will be denoted by :

If it is not specified, these spaces will always be equipped with norms and respectively.

Remark. Note that :

Definition 2.2.

Let be a continuous function of finite -variation. The step- signature of is the functional such that for every and ,

Moreover,

is the step- free nilpotent group over .

Definition 2.3.

A map is of finite -variation if and only if,

where, is the Carnot-Caratheodory’s norm such that for every ,

In the sequel, the space of continuous functions from into with finite -variation will be denoted by :

If it is not specified, that space will always be equipped with .

Let’s define the Lipschitz regularity in the sense of Stein :

Definition 2.4.

Consider . A map is -Lipschitz (in the sense of Stein) if and only if is on , bounded, with bounded derivatives and such that the -th derivative of is -Hölder continuous ( is the largest integer strictly smaller than and ).

The least bound is denoted by . The map is a norm on the vector space of collections of -Lipschitz vector fields on , denoted by .

In the sequel, will always be equipped with .

Let be a continuous function of finite -variation such that a geometric -rough path exists over it. In other words, there exists an approximating sequence of functions of finite -variation such that :

When , a natural geometric -rough path over it is defined by :

| (2) |

We remind that if is a collection of Lipschitz continuous vector fields on , the ordinary differential equation , with initial condition , admits a unique solution.

That solution is denoted by .

Rigorously, a RDE’s solution is defined as follow (cf. [8], Definition 10.17) :

Definition 2.5.

A continuous function is a solution of with initial condition if and only if,

where, is the uniform norm on . If there exists a unique solution, it is denoted by .

Theorem 2.6.

Let be a collection of locally -Lipschitz vector fields on () such that : and are respectively globally Lipschitz continuous and -Hölder continuous on . With initial condition , equation admits a unique solution .

For a proof, see P. Friz and N. Victoir [8], Exercice 10.56.

For P. Friz and N. Victoir, the rough integral for a collection of -Lipschitz vector fields along is the projection of a particular full RDE’s solution (cf. [8], Definition 10.34 for full RDEs) : where,

and is the canonical basis of .

In particular, if and are two continuous functions, respectively of finite -variation and finite -variation with , the Young integral of with respect to is denoted by .

Remark. We are not developing the notion of full RDE in that paper because it is not useful in the sequel. As mentioned above, the reader can refer to [8], Definition 10.34 for details.

For a proof of the following change of variable formula for geometric rough paths, cf. [2], Theorem 53 :

Theorem 2.7.

Let be a collection of -Lipschitz vector fields on () and let be a geometric -rough path. Then,

Now, let state some results on -dimensional Gaussian rough paths :

Consider a stochastic process defined on and satisfying the following assumption :

Assumption 2.8.

is a -dimensional centered Gaussian process with -Hölder continuous paths on ().

In the sequel, we work on the probability space where , is the -algebra generated by cylinder sets and is the probability measure induced by on .

Remark. Since is a -dimensional Gaussian process, the natural geometric -rough path over it defined by (2) is matching with the enhanced Gaussian process for provided by P. Friz and N. Victoir at [8], Theorem 15.33 in the multidimensional case.

Finally, Cameron-Martin’s space of is given by :

with

Let be the map defined on by :

where,

with .

That map is a scalar product on and, equipped with it, is a Hilbert space.

The triplet is called an abstract Wiener space (cf. M. Ledoux [12]).

Proposition 2.9.

For , consider a random variable , continuously -differentiable (i.e. is continuously differentiable from into , for almost every ).

If satisfies Bouleau-Hirsch’s condition (i.e. a.s. for at least one such that , where :

then admits a density with respect to Lebesgue’s measure on .

Remarks :

-

(1)

Classically, Bouleau-Hirsch’s condition is not stated that way and involves Malliavin calculus framework. Consider the Malliavin derivative operator (cf. D. Nualart [20], Section 1.2), the reproducing kernel Hilbert space of the Gaussian process (cf. J. Neveu [19]), and the canonical isometry from into defined for example at N. Marie [18], Section 3.1. Bouleau-Hirsch’s condition for is .

On one hand, by Cauchy-Schwarz’s inequality, it is sufficient to show that there exists satisfying and . On the other hand, with Malliavin calculus methods, one can easily show that . -

(2)

About Bouleau-Hirsch’s criterion for , please refer to [20], Theorem 2.1.2.

3. Deterministic properties of the generalized mean-reverting equation

In this section, we show existence and uniqueness of the solution for equation (1), provide an explicit upper-bound for that solution and, study the continuity and differentiability of the associated Itô map. We also provide a converging approximation for equation (1).

Consider a function satisfying the following assumption :

Assumption 3.1.

The function is -Hölder continuous ().

Let be the natural geometric -rough path over defined by (2). Then, we put , which is a geometric -rough path over

by [8], Theorem 9.26.

Remark. For a rigorous construction of Young pairing, the reader can refer to [8], Section 9.4.

Then, consider the rough differential equation :

| (3) |

where is the map defined on by :

For technical reasons, we introduce another equation :

| (4) |

where, and

for every . The integral is taken in the sense of Young.

The map belongs to and is bounded with bounded derivatives on for every . Then, equation (4) admits a unique solution in the sense of Definition 2.5 by applying Theorem 2.6 up to the time

by assuming that .

Consider also the time , such that when .

3.1. Existence and uniqueness of the solution

As mentioned above, Section 2 ensures that equation (4) has, at least locally, a unique solution denoted . At Lemma 3.2, we prove it ensures that equation (3) admits also, at least locally, a unique solution (in the sense of Definition 2.5) denoted . In particular, we show that . At Proposition 3.3, we prove the global existence of by using the fact it never hits on . These results together ensures the existence and uniqueness of on .

Lemma 3.2.

Proof.

Consider the solution of (4) on , with initial condition .

The continuous function takes its values in on .

Since , the map is , bounded and with bounded derivatives.

Then, by applying the change of variable formula (Theorem 2.7) to and to the map between and :

Since , in the sense of Definition 2.5, is the solution of (3) on with initial condition . ∎

Proposition 3.3.

Proof.

Suppose that , put and consider the solution of (4) on (), with initial condition .

On one hand, note that by definition of :

for every . Then, since when :

| (5) |

for every .

Moreover, since is the Young integral of against , and is -Hölder continuous, is also -Hölder continuous (cf. [8], Theorem 6.8).

Together, equality (5) and the -Hölder continuity of imply :

On the other hand, the two terms of that sum are positive. Then,

| (6) | |||||

| (7) |

Since has been chosen arbitrarily, inequality (6) is true for every and implies :

So

| (8) | |||||

By inequalities (7) and (8) together :

| (9) |

If , then and

If , inequality (9) can be rewritten as

but and

Therefore, if , .

An immediate consequence is that :

Then, (4) admits a unique solution on by putting :

where, denotes the solution of (4) on for every .

By Lemma 3.2, equation (3) admits a unique solution on , matching with .

Finally, since is chosen arbitrarily, for locally -Hölder continuous, equation (3) admits a unique solution on by putting :

for every . ∎

Remarks and partial extensions :

-

(1)

Note that the statement of Lemma 3.2 holds true when , and up to the time , equation (3) has a unique explicit solution :

However, in that case, can belong to . Then, is matching with the solution of equation (3) only locally. It is sufficient for the application in pharmacokinetic provided at Section 5.

-

(2)

For every , equation (4) admits a unique solution on when :

(10) Indeed, for every ,

Then,

Since is continuous from into with :

Therefore,

(11) by inequality (10). Since the right-hand side of inequality (11) is not depending on , that hitting time is not belonging to .

By Lemma 3.2, equation (3) admits also a unique solution on when (10) is true. -

(3)

If , necessarily :

for every .

Then, when , and by [8], Theorem 6.8 :with .

Therefore, is defined on when .

3.2. Upper-bound for the solution and regularity of the Itô map

Under assumptions 1.1 and 3.1, we provide an explicit upper-bound for and, show continuity and differentiability results for the Itô map :

Proof.

Consider , the solution of (4) with initial condition and

On one hand, we consider the two following cases :

- (1)

-

(2)

If ; by definition of , and then, . Therefore,

On the other hand, by using the integration by parts formula, for every ,

because .

Therefore, by putting cases 1 and 2 together ; for every ,

| (13) |

That achieves the proof because, and the right hand side of inequality (13) is not depending on . ∎

Remark. In particular, by Proposition 3.4, does not explode when or/and .

Notation. In the sequel, for every ,

Proposition 3.5.

Under Assumption 1.1, for and , is a continuous map from into . Moreover, is Lipschitz continuous from into for every and .

Proof.

Consider and belonging to .

For , we put and where,

and, with notations of equation (4), is the map defined by :

We also put :

On one hand, we consider the two following cases :

-

(1)

Consider and suppose that .

Since and are continuous on by construction, for every , and then,Therefore,

Symmetrically, one can show that this inequality is still true when .

-

(2)

Consider ,

and suppose that .

Since and are continuous on by construction, for every , and then,Therefore,

Symmetrically, one can show that this inequality is still true when .

By putting these cases together and since the obtained upper-bounds are not depending on :

| (14) |

Then, is continuous from into .

For any -Hölder continuous function , from Lemma 3.2 and Proposition 3.3 :

Moreover, by [8], Proposition 6.12, is continuous from into itself. Therefore, is continuous from into by composition.

On the other hand, consider and . By Proposition 3.4, there exists such that :

Then, for every ,

by inequality (14). Since is Lipschitz continuous from bounded sets of into (cf. [8], Proposition 6.11), that achieves the proof. ∎

In order to study the regularity of the solution of equation (3) with respect to parameters characterizing the vector field , let’s denote by (resp. ) the solution of equation (3) (resp. (4)) up to .

Proof.

On one hand, consider , and :

because for every by Proposition 3.3.

Then, by Lemma 3.2 :

On the other hand, consider , , and such that : , and for every . As at Lemma 3.2, by the change of variable formula (Theorem 2.7), for every ,

because for every by Proposition 3.3.

Since for every by assumption, necessarily :

and

Therefore, it’s impossible, and for every , . ∎

Proof.

Let’s now show the continuous differentiability of the Itô map with respect to the initial condition and the driving signal :

Proposition 3.8.

Under Assumption 1.1, for and , is continuously differentiable from into .

Proof.

In a sake of readability, the space is denoted by .

Consider , ,

Since is continuous from into by Proposition 3.5 :

| (15) |

In particular, for every , the function is -valued with and

In [8], the continuous differentiability of the Itô map with respect to the initial condition and the driving signal is established at theorems 11.3 and 11.6. In order to derive the Itô map with respect to the driving signal at point in the direction , has to satisfy the condition to ensure the existence of the geometric -rough path over () provided at [8], Theorem 9.34 when . When , that condition can be dropped by (2). Therefore, since the vector field is on , is continuously differentiable from into .

In conclusion, since has been arbitrarily chosen, is continuously differentiable from into .

∎

3.3. A converging approximation

In order to provide a converging approximation for equation (3), we first prove the convergence of the implicit Euler approximation for equation (4) :

| (16) |

where, for , and while .

Remark. On the implicit Euler approximation in stochastic analysis, cf. F. Malrieu [15] and, F. Malrieu and D. Talay [16] for example.

The following proposition shows that the implicit step- Euler approximation is defined on :

Proof.

Let be the function defined on by :

On one hand, for every and , and for every ,

Then, increase on . Moreover,

Therefore, since is continuous on :

| (17) |

On the other hand, for every , equation (16) can be rewritten as follow :

| (18) |

In conclusion, by recurrence, equation (18) admits a unique strictly positive solution .

Necessarily, for .

That achieves the proof.

∎

For every , consider the function such that :

for every .

The following lemma provides an explicit upper-bound for . It is crucial in order to prove probabilistic convergence results at Section 4.

Lemma 3.10.

Under Assumption 3.1, for and :

Proof.

Similar to the proof of Proposition 3.4.

First of all, by applying (16) recursively between integers and a change of variable :

| (19) |

Consider and

For each , we consider the two following cases :

- (1)

-

(2)

If ; by definition of , for , and then, . Therefore, from equality (19) :

As at Proposition 3.4 :

| (21) | |||||

That achieves the proof because the right hand side of inequality (21) is not depending on . ∎

With ideas of A. Lejay [13], Proposition 5, we show that converges and provide a rate of convergence :

Theorem 3.11.

Proof.

It follows the same pattern that Proof of [13], Proposition 5.

Consider , and the solution of equation (4) with initial condition . Since is a subdivision of , there exists an integer such that .

First of all, note that :

| (22) |

where, for . Since is the solution of equation (4), and satisfy :

where,

In order to conclude, we have to show that is bounded by a quantity not depending on and converging to when goes to infinity :

On one hand, for every ,

because is -Hölder continuous with constant if and locally Lipschitz continuous otherwise, is -Hölder continuous and admits a strictly positive minimum on , and is Lipschitz continuous with constant . In particular, if ,

where .

Then, for ,

| (23) | |||||

On the other hand, for each integer between and , we consider the two following cases (which are almost symmetric) :

-

(1)

Suppose that . Then,

Therefore,

-

(2)

Suppose that . Then,

Therefore,

By putting these cases together :

| (24) |

By applying (24) recursively from down to :

| (25) | |||||

because and by inequality (23).

Moreover, from inequality (25), there exists such that for every integer ,

where,

In particular,

Then , and

In conclusion, from inequality (22) :

That achieves the proof because the right hand side of inequality (3.3) is not depending on and . ∎

Finally, for every and , consider .

The following corollary shows that is a converging approximation for with . Moreover, as the Euler approximation, it is just necessary to know , and, parameters and to approximate the whole path by :

Proof.

4. Probabilistic properties of the generalized mean-reverting equation

Consider the Gaussian process and the probability space introduced at Section 2. Under Assumption 2.8, almost every paths of are satisfying Assumption 3.1. Then, under assumptions 1.1 and 2.8, results of Section 3 hold true for , with deterministic initial condition .

This section is essentially devoted to complete them on probabilistic side. In particular, we prove that belongs to for every . We also show that the approximation introduced at Section 3 for is converging in for every .

Remark. Since is a -dimensional process, as mentioned at Section 2, there exists an explicit geometric -rough path over it, matching with the enhanced Gaussian process provided by P. Friz and N. Victoir at [8], Theorem 15.33. That explains why Assumption 2.8 is sufficient to extend deterministic results of Section 3 to .

4.1. Extension of existence results and properties of the solution’s distribution

On one hand, when , Proposition 4.1 extend remark 2 of Proposition 3.3 on probabilistic side. On the other hand, we study properties of the distribution of defined on , when is a -dimensional Gaussian process with locally -Hölder continuous paths, stationary increments and satisfies a self-similar property.

Proposition 4.1.

Proof.

Proposition 4.2.

Assume that is a -dimensional centered Gaussian process with locally -Hölder continuous paths, and there exists such that :

Under Assumption 1.1, for and , with any deterministic initial condition :

for every .

Proof.

Proposition 4.3.

Assume that is a -dimensional centered Gaussian process with locally -Hölder continuous paths, and there exists such that :

Under Assumption 1.1, for and , with any deterministic initial condition :

for every and , with :

Proof.

By Proposition 3.3, has almost surely continuous and strictly positive paths on . Then, by Theorem 2.7 applied to almost every paths of and to the map between and :

Therefore, for every , where,

because .

In conclusion, by applying Theorem 2.7 to almost every paths of and to the map :

for every and . ∎

Remark. Typically, mean-reverting equations driven by a fractional Brownian motion are concerned by propositions 4.2 and 4.3.

Proposition 4.4.

Consider , and a -dimensional fractional Brownian motion with Hurst parameter . Under Assumption 1.1, for every () :

Proof.

Consider and

where, .

Case 1 (). On one hand, since if and only if for every , and

then implies that :

Therefore,

for every .

On the other hand, since :

with

For every and every ,

and is a continuous, decreasing map. Then, for every ,

Therefore, by Lebesgue’s theorem :

and for every , almost surely.

Case 2 (). In that case, if and only if, for every . Then, with ideas of the first case :

for every .

Moreover, results on have been established for every and every at case 1 then, by Lebesgue’s theorem :

and for every , almost surely.

In conclusion, since by Lemma 3.2, for every , almost surely.

∎

4.2. Integrability and convergence results

Consider the implicit Euler approximation for the following SDE :

where,

for every .

Proposition 4.5.

Proof.

Corollary 4.6.

Proof.

4.3. A large deviation principle for the generalized M-R equation

We establish a large deviation principle for the generalized mean-reverting equation (as P. Friz and N. Victoir at [8], Section 19.4).

First of all, let’s remind basics on large deviations (for details, the reader can refer to [3]).

Throughout this subsection, assume that .

Definition 4.7.

Let be a topological space and let be a good rate function (i.e. a lower semicontinuous map such that is a compact subset of for every ).

A family of probability measures on satisfies a large deviation principle with good rate function if and only if, for every ,

where,

Proposition 4.8.

Consider and two Hausdorff topological spaces, a continuous map and a family of probability measures on .

If satisfies a large deviation principle with good rate function , then satisfies a large deviation principle on with good rate function such that :

for every .

That result is called contraction principle. The reader can refer to [3], Lemma 4.1.6 for a proof.

Consider the space of functions such that :

for every .

In the sequel, is equipped with and the Borel -field generated by open sets of the -Hölder topology. The same way, is equipped with and the Borel -field generated by open sets of the uniform topology.

Now, suppose that satisfies :

Assumption 4.9.

There exists such that :

Moreover, and is an abstract Wiener space.

Remarks :

-

(1)

The notion of abstract Wiener space is defined and detailed in M. Ledoux [12].

- (2)

Consider the stochastic differential equation :

| (27) |

where, is a deterministic initial condition, and satisfies Assumption 1.1.

Under assumptions 1.1 and 2.8, by propositions 3.3 and 4.5, equation (27) admits a unique solution belonging to for every .

Moreover, under Assumption 4.9, by Proposition 4.3 :

| (28) |

for every and .

In the sequel, assume that . Then, satisfies :

where, is the map defined on by :

Let show that satisfies a large deviation principle :

Proposition 4.10.

Proof.

Since by construction, Proposition 3.5 implies that is continuous from

On the other hand, under Assumption 4.9, by M. Ledoux [12], Theorem 4.5 ; satisfies a large deviation principle on with good rate function .

Therefore, since for every , by the contraction principle (Proposition 4.8), satisfies a large deviation principle on with good rate function .

∎

4.4. Density with respect to Lebesgue’s measure for the solution

Via Bouleau-Hirsch’s method, this subsection is devoted to show that admits a density with respect to Lebesgue’s measure on for every and every .

Notation. For two normed vector spaces and , the embedment of in is denoted by .

Throughout this subsection, assume that satisfies :

Assumption 4.11.

Cameron-Martin’s space of satisfies :

Example. A fractional Brownian motion with Hurst parameter satisfies Assumption 4.11.

Proposition 4.12.

Proof.

With notations of Proposition 3.8, by Proposition 2.9 and the transfer theorem, it is sufficient to show that satisfies Bouleau-Hirsch’s condition for any .

On one hand, by Proposition 3.8 (cf. Proof), is continuously differentiable from into . Then, is continuously differentiable on

By P. Friz and N. Victoir [8], Lemma 15.58, for almost every ,

Therefore, almost surely :

and is continuously -differentiable.

On the other hand, by Proposition 3.8, for every ,

In particular, for .

In conclusion, by Proposition 2.9, for every , and then , admit a density with respect to Lebesgue’s measure on respectively.

∎

5. A generalized mean-reverting pharmacokinetic model

We study a pharmacokinetic model based on a particular generalized mean-reverting equation (inspired by K. Kalogeropoulos et al. [11]).

In order to study the absorption/elimination processes of a given drug, the following deterministic mono-compartment model is classically used :

| (29) |

where :

-

•

is the dose administered to the patient at initial time.

-

•

is the volume of the elimination compartment (extra-vascular tissues).

-

•

is the rate of absorption in compartment . If the drug is administered by rapid injection, an IV bolus injection, it is natural to take .

-

•

is the rate of elimination in compartment , describing removal of the drug by all elimination processes including excretion and metabolism.

-

•

is the concentration of the drug in compartment at time .

Remark. About deterministic pharmacokinetic models, the reader can refer to Y. Jacomet [9] and N. Simon [23].

Recently, in order to modelize perturbations during the elimination processes, stochastic generalizations of (29) has been studied :

where, is a standard Brownian motion and the stochastic integral is taken in the sense of Itô. For example, in K. Kalogeropoulos et al. [11] :

with and .

However, these models aren’t realistic (cf. M. Delattre and M. Lavielle [4]), because the obtained process is too rough.

Since probabilistic properties of Itô’s integral aren’t particularly interesting in that situation, if the drug is administered by rapid injection, could be the solution of equation (1) with , and .

In order to bypass the difficulty of the standard Brownian motion’s paths roughness, one can take a Gaussian process satisfying Assumption 2.8 with close to . Typically, a fractional Brownian motion with a high Hurst parameter (cf. simulations below).

Precisely :

| (30) |

where the stochastic integral is taken pathwise, in the sense of Young. Moreover, since , we shown at Section 3 that until it hits zero, the solution of equation (30) is matching with the process defined by :

It is natural to assume that when the concentration hits 0, the elimination process stops. Then, we put where is a deterministic fixed time.

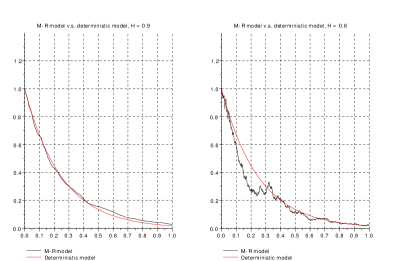

For example, let simulate that model with , , , and a fractional Brownian motion with Hurst parameter :

On one hand, remark that the stochastic model (black) keeps the trend of the deterministic model (red). On the other hand, remark that when the Hurst parameter is relatively close to (), perturbations in biological processes are taken in account by , but more realistically than for .

In the sequel, we also consider the process . Its covariance function is denoted by .

For clinical applications, parameters , and have to be estimated. Consider a dissection of for . We also put and for . The following proposition provides the likelihood function of which can be approximatively maximized with respect to the parameter by various numerical methods (not studied in this paper) :

Proof.

Since is a centered Gaussian process as a Wiener integral against ; is a centered Gaussian vector with covariance matrix . We denote by the natural density of with respect to Lebesgue’s measure on .

Consider an arbitrary Borel bounded map . By the transfer theorem :

by reduction to canonical form of quadratic forms.

Put for and . Then,

where, denotes the Jacobian of :

By applying that change of variable :

Therefore, with :

∎

Finally, consider a random time and a deterministic function satisfying the following assumption :

Assumption 5.2.

The function belongs to and there exists such that :

Let show the existence and compute the sensitivity of to variations of the initial concentration in compartment .

Proof.

First of all, the function is almost surely on and,

Consider and .

On one hand, since belongs to , from Taylor’s formula :

by Assumption 5.2.

On the other hand, since :

| (31) |

and

| (32) |

By Fernique’s theorem, the right hand sides of inequalities (31) and (32) belong to for every . Moreover, these upper-bounds are not depending on and .

Therefore, by Lebesgue’s theorem, is derivable at point and,

∎

There is probably many ways to use that result in medical treatments. For example, assume that modelize a part of patient’s therapeutic response to the administered drug. Proposition 5.3 provides a way to minimize the initial dose for an optimal response.

Remarks :

-

(1)

By the strong law of large numbers, there exists an almost surely converging estimator for that sensitivity.

-

(2)

For any , one can show the existence of a stochastic process defined on such that where, denotes the divergence operator associated to the Gaussian process . Then, has not to be derivable anymore by assuming that . It is particularly useful if is not continuous at some points.

We don’t develop it in that paper because the Malliavin calculus framework has to be introduced before. To understand that idea, please refer to E. Fournié et al. [7] in Brownian motion’s case and N. Marie [18].

References

- [1] R.J. Adler. An Introduction to Continuity, Extrema, and Related Topics for General Gaussian Processes. Institute of Mathematical Statistics, Lecture Notes-Monograph Series, Vol. 12, 1990.

- [2] L. Coutin. Rough Paths via Sewing Lemma. ESAIM : Probability and Statistics, doi:10.1051/ps/2011108.

- [3] A. Dembo and O. Zeitouni. Large Deviations Techniques and Applications. Applications of Mathematics, Vol. 38, New-York. Springer-Verlag, 1998.

- [4] M. Delattre and M. Lavielle. Pharmacokinetics and Stochastic Differential Equations : Model and Methodology. Annual Meeting of the Population Approach Group in Europe, 2011.

- [5] H. Doss. Liens entre équations différentielles stochastiques et ordinaires. C.R. Acad. Sci. Paris Ser. A-B, 283(13):Ai, A939-A942, 1976.

- [6] J. Feng, J-P. Fouque and R. Kumar. Small-Time Asymptotics for Fast Mean-Reverting Stochastic Volatility Models. arXiv (1009.2782), 2010.

- [7] E. Fournié, J-M. Lasry, J. Lebuchoux, P-L. Lions and N. Touzi. Applications of Malliavin Calculus to Monte-Carlo Methods in Finance. Finance Stochast. 3, 391-412, 1999.

- [8] P. Friz and N. Victoir. Multidimensional Stochastic Processes as Rough Paths : Theory and Applications. Cambridge Studies in Applied Mathematics, 120. Cambridge University Press, Cambridge, 2010.

- [9] Y. Jacomet. Pharmacocinétique. Cours et Exercices. Université de Nice, U.E.R. de Médecine, Service de pharmacologie expérimentale et clinique, Ellipses, 1989.

- [10] S. Karlin and H.M. Taylor. A Second Course in Stochastic Processes. Academic Press Inc., Harcourt Brace Jovanovich Publishers, 1981.

- [11] K. Kalogeropoulos, N. Demiris and O. Papaspiliopoulos. Diffusion-driven Models for Physiological Processes. International Workshop on Applied Probability (IWAP), 2008.

- [12] M. Ledoux. Isoperimetry and Gaussian Analysis. Ecole d’été de probabilité de Stain-Flour, 1994.

- [13] A. Lejay. Controlled Differential Equations as Young Integrals : A Simple Approach. Journal of Differential Equations 248, 1777-1798, 2010.

- [14] T. Lyons and Z. Qian. System Control and Rough Paths. Oxford University Press, 2002.

- [15] F. Malrieu. Convergence to Equilibrium for Granular Media Equations and their Euler Schemes. Annals of Applied Probability, Vol. 13, no. 2, 540-560, 2003.

- [16] F. Malrieu et D. Talay. Concentration Inequalities for Euler Schemes. Springer-Verlag, 355-371, 2006.

- [17] X. Mao, A. Truman and C. Yuan. Euler-Maruyama Approximations in Mean-Reverting Stochastic Volatility Model under Regime-Switching. Journal of Applied Mathematics and Stochastic Analysis, 2006.

- [18] N. Marie. Sensitivities via Rough Paths. arXiv (1108.0852), 2011.

- [19] J. Neveu. Processus aléatoires gaussiens. Presses de l’Université de Montréal, 1968.

- [20] D. Nualart. The Malliavin Calculus and Related Topics. Second Edition. Probability and Its Applications, Springer, 2006.

- [21] N. Tien Dung. Fractional Geometric Mean Reversion Processes. Journal of Mathematical Analysis and Applications, vol. 330. pp. 396-402, 2011.

- [22] M. Sanz-Solé and I. Torrecilla-Tarantino. A Large Deviation Principle in Hölder Norm for Multiple Fractional Integrals. arXiv (0702049), 2007.

- [23] N. Simon. Pharmacocinétique de population. Collection Pharmacologie médicale, Solal, 2006.

- [24] H.J. Sussman. On the Gap between Deterministic and Stochastic Ordinary Differential Equations. Ann. Probability, 6(1):19-41, 1978.

- [25] F. Wu, X. Mao and K. Chen. A Highly Sensitive Mean-Reverting Process in Finance and the Euler-Maruyama Approximations. Journal of Mathematical Analysis and Applications, 348(1). pp. 540-554, 2008.