Hölder regularity and series representation of a class of stochastic volatility models

Antoine Ayache and Qidi Peng

Université Lille 1

Abstract

Let be an arbitrary continuously differentiable deterministic function such that is bounded by a polynomial.

In this article we consider the class of stochastic volatility models in which , the logarithm of the price process, is of the form , where denotes an arbitrary centered Gaussian

process whose trajectories are, with probability , Hölder continuous functions of an arbitrary order , and where is a standard Brownian motion independent on .

First we show that the critical Hölder regularity of a typical trajectory of is equal to . Next we provide for

such a trajectory an expression as a random series which converges at a geometric rate in any Hölder space of an arbitrary order ; this expression is obtained through the expansion of the random function on the Haar basis. Finally, thanks to it, we give an efficient iterative

simulation method for .

Running Title: Series representations of stochastic volatility models

Key Words: Haar system, Hölder spaces, Gaussian processes, fractional and multifractional Brownian motions.

Stochastic volatility models are extensions of the

well-known Black and Scholes model. Hull and White [15] and

other authors working in the field of mathematical finance (see for instance [22]

and [18]), introduced them starting in the mid-80s, in order to account for

volatility effects of exogenous arrivals of information on the price of an underlying asset. Later, for making such models to be

more realistic, it has been proposed (see for example [10, 11, 13, 14, 21])

to replace the Brownian motion governing the volatility in them, by a more

flexible stochastic process. That is why, in this article we consider the general class of stochastic volatility models, in which the stochastic process denoting the logarithm of the price of an underlying asset, is defined for each time , as,

(1.1)

where

•

denotes an arbitrary real-valued centered Gaussian process whose trajectories are, with probability ,

Hölder continuous functions of an arbitrary order i.e. there is a positive and finite random variable such

that one has for almost all and for all ,

(1.2)

it is worth noticing that, thanks to the Gaussianity of , the random variable can be chosen in such a way that all its moments are finite.

•

is an arbitrary deterministic real-valued continuously differentiable function on the real line, which satisfies as well as its derivative , for all ,

(1.3)

where and are two constants (non depending) on .

•

denotes a standard Brownian motion independent on the process . Observe that thanks to these assumptions, the stochastic integral in (1.1) is well-defined, moreover, conditional on the -algebra,

(1.4)

is a centered Gaussian process with a covariance function given, for all , by,

(1.5)

Observe that the models in (1.1) are generalizations of the multifractional stochastic volatility models introduced in [2], which in turn extend the

fractional stochastic volatility models studied in [13, 14]. Recall that a multifractional stochastic volatility model is defined

through (1.1) in which denotes a multifractional Brownian motion [6, 20], in other words, roughly speaking, a fractional Brownian motion with a smooth time-varying Hurst parameter ; a survey on the latter Gaussian process can be found in [1] for instance, also we refer to [7, 8, 9] for some interesting applications of it in the field of finance. Recall that the main feature of a multifractional stochastic volatility model, is that the local roughness of the volatility process ,

in other words its pointwise Hölder exponent (see (2.1) for a definition of this exponent), can be prescribed via the Hurst functional parameter and thus is allowed to change over time (that is from point to point).

The remaining of the paper is structured in the following way. In section 2, we show that there exists a modification of , also denoted by

, whose trajectories belong, with probability , to any Hölder space of an arbitrary order ; on the other hand, under the assumption

that vanishes only on a Lebesgue negligible set, we show that the pointwise

Hölder exponent of , at any point such that , is almost surely equal to ; observe that, under the same

assumption on , the latter result implies that, with probability , the trajectories of fail to belong to when and is not an almost surely vanishing process (i.e. we do not have for all , almost surely, ).

In section 3, by expanding the random function on the Haar basis of , we introduce a random series representation of

, for which the convergence holds at a geometric rate, almost surely in , for all

. Finally, thanks to the latter nice representation of , we give in section 4 an iterative algorithm which allows to efficiently simulate this process.

2 Hölder regularity of the log price process

Let us first recall the definition of a Hölder space of order .

Definition 2.1

For any , the Hölder space

is defined as the Banach space of the continuous real-valued functions which satisfy,

It is equipped with the norm,

(2.1)

where

Observe that reduces to the usual Banach space of real-valued continuous functions over . The main goal of this section is to prove the following two theorems.

Theorem 2.1

Let be the stochastic process defined in (1.1), then there exists a modification of , also denoted by , such that, with probability , for all , the trajectories of belong to the Hölder space .

Recall that when a trajectory of an arbitrary real-valued stochastic process

is a continuous and non-differentiable function at a point , then , the pointwise Hölder exponent of at , is defined as,

(2.2)

Theorem 2.2

Let be the modification of the process introduced in Theorem 2.1 and let be the corresponding pointwise Hölder exponent; then, under the assumption that vanishes only on a Lebesgue negligible set, one has,

(2.3)

Observe that a straightforward consequence of Theorem 2.1 is that, one has for all ,

(2.4)

Therefore, for obtaining Theorem 2.2, it is sufficient to show that Theorem 2.1 holds and that, under the assumption that vanishes only on a Lebesgue negligible set, one has,

(2.5)

The proof of Theorem 2.1 mainly relies on the following two lemmas. Observe that the first one whose proof can be found in [16] for instance, is a refined version of the usual Kolmogorov criterion allowing to show that a stochastic process has a modification with almost surely continuous trajectories; also observe that the second one, which can easily be proved, is a standard result on centered real-valued Gaussian random variables.

Lemma 2.3(Kolmogorov-Centsov criterion)

Assume that the positive real number is arbitrary and fixed. Let be

an arbitrary stochastic process such that for all , one has,

where , and are three positive constants. Then there exists a

modification of denoted by , whose trajectories are

with probability , Hölder functions of any arbitrary order ; in other words,

Lemma 2.4(equivalence of Gaussian moments)

Let be an arbitrary centered real-valued Gaussian random variable. Then for

all positive real number , one has,

(2.6)

where denotes the positive constant, only depending on , defined as,

being the usual ”Gamma function”, defined as , for all .

Proof of Theorem 2.1: Let be arbitrary and fixed, we assume that the positive real number has been chosen

in such a way that

(2.7)

Recall that the -algebra has been defined in (1.4) and that

conditionally on it, the stochastic process has a centered Gaussian distribution with a covariance function given by (1.5).

Therefore, one has, for any real number and for each ,

observe that is an almost surely finite random variable, since the trajectories of are, with probability continuous functions.

The Gaussianity of the latter process as well as the almost sure finiteness of , imply that (see [17] for instance), all the moments of this random variable are finite as well, namely, for each real number , one has,

(2.11)

Next, one sets,

(2.12)

observe that is an almost surely finite random variable since is a continuous function, moreover, in view of (1.3) and (2.11) all its moments

are finite, namely, for each real number , one has,

(2.13)

Next, combining (2) with (2.10) and (2.12), one gets that,

where ; observe that the finiteness of the latter constant is due to (2.13). Finally, putting together (2.15), (2.7), and Lemma 2.3 in which one takes and , one obtains the theorem.

From now on, our goal is to show that Relation (2.5) holds, to this end one needs the following lemma.

Lemma 2.5

Assume that is arbitrary and fixed. Let is an arbitrary sequence of non

vanishing real numbers which converges to and satisfies, for every , . Then,

(i)

for all fixed , conditional on the -algebra defined in (1.4), the random variable

has a centered Gaussian distribution with a variance given by,

(ii)

moreover, under the assumptions that does not vanish except on a Lebesgue negligible set and , one has, almost surely,

Proof of Lemma 2.5: Part follows from (2) and the fact that conditionally on , the stochastic process has a centered Gaussian distribution. Let us now prove that Part holds.

The Mean Value Theorem, implies that, that there is a real number which belongs to the interval

and satisfies,

(2.16)

thus, using the almost sure continuity of the random function , one gets that,

(2.17)

Next, observe that the assumptions that vanishes only on Lebesgue negligible set and that , imply that,

almost surely,

Now, we are in position to prove Relation (2.5).

Proof of Relation (2.5): Our proof is inspired by that of Proposition 2.4 in [4]. It consists in showing that for all fixed , there exists a sequence of non vanishing real numbers converging to which satisfies:

(2.19)

To this end, it is sufficient to prove that there exists a sequence of non vanishing real numbers converging to which satisfies:

(2.20)

where the notation ”” means that the convergence to holds in probability. Indeed, assuming that (2.20) is satisfied, then one can extract from a subsequence denoted by such that one has (2.19).

Let us now prove (2.20). Denote by an arbitrary sequence of non vanishing real numbers converging to and such that for all .

Observe that, one has, for all real number ,

Thus, combining (2.22) with (2.23) one obtains that,

(2.24)

Finally, in view of (2) and (2.24), using the dominated convergence theorem, it follows that (2.20) holds.

3 Random series representation of via the Haar basis

In order to state the main result of this section, we need to introduce some notations.

•

We denote by the usual Lebesgue Hilbert of the square integrable real-valued deterministic functions over .

•

The Haar orthonormal basis of (see for example [19, 12, 23]), is the

sequence of the functions:

defined as

(3.1)

and

(3.2)

where is the indicator function of an arbitrary set .

•

We denote by the underlying probability space, that is

the probability space on which the processes , and

are defined; moreover, for the sake of simplicity, we assume that this space has been chosen in such a way that: for all

, Relation (1.2) holds and for each . Also, we denote by

the sequence of standard independent Gaussian random variables defined, on this space as,

(3.3)

and

(3.4)

Observe that, similarly to Lemma 2 in [3], one can show that there exist

an event of probability , and a positive random variable of finite moment of any order,

such that one has for all , all and all ,

(3.5)

we note in passing that the proof of this important inequality, mainly relies on Borel-Cantelli Lemma.

•

is the stochastic

field defined for all as,

(3.6)

thus, the process defined in (1.1) can be expressed as,

(3.7)

Observe that (3.6), (2.10), (2.12), imply that for all ,

(3.8)

where the last inequality results from the continuity of the functions and .

•

We denote by the stochastic process defined for all

, as,

(3.9)

moreover, for all and , we denote by the stochastic process defined for all

, as,

(3.10)

Observe that it follows from (3.9), (3.10),

(3.8), (3.1) and (3.2), that for

all and for all ,

(3.11)

and for all and ,

(3.12)

Now we are in position to state the main result of this section:

Theorem 3.1

Let be arbitrary and fixed. For all and , one sets,

(3.13)

In view of (3.11) and (3.12) the trajectories of the process belong to the Hölder space since they are in fact Lipschitz functions; moreover, there exist an event of probability and a positive random variable of finite moment of any order, such that one has for

all and ,

(3.14)

where is the usual norm on (see Definition 2.1) and where has been introduced in

(1.2).

In order to prove the latter theorem we need some preliminary results. The following lemma is a weak version of Theorem 3.1.

Lemma 3.2

We use the same notations as in Theorem 3.1. Let be arbitrary and fixed. When goes to , the random variable

converges to the random variable in the Hilbert space , namely, one has,

(3.15)

As a straightforward consequence, there exist an event of probability included in (recall that is the event of probability on which (3.5) holds) and a subsequence (a priori depending on ) such that for all ,

one has,

(3.16)

Proof of Lemma 3.2: Let be as in (3.6). Observe that in view of (3.8), for all fixed , the function belongs to . By expanding the latter function on the Haar basis, one obtains that,

(3.17)

where the coefficients and have been defined respectively in (3.9) and

(3.10). A priori the series in (3.17) is convergent in the norm, namely,

(3.18)

where, for each , is the partial sum defined, for all , as,

(3.19)

Let us show that this series, is also convergent in the

norm, that is,

(3.20)

In order to show that (3.20) holds, we will use the dominated convergence theorem. It follows from (3.17), (3.19), Parseval formula and

(3.8), that for all ,

thus, in view of (3.18) and (2.13), we are allowed to derive (3.20) by making use of the dominated convergence theorem.

Finally, observe that, (3.7), (3.3), (3.4), (3.13), (3.19), (1.4), and the isometry property of Wiener integral, entail that, one has almost surely, for all ,

Proof of Lemma 3.3: First observe that

(3.23) easily results from (3.2), (3.6) and

(3.10). Let us now prove that (3.21) holds, so we assume that . For all , we set

(3.24)

Then, using (3.2), (3.6),

(3.10) and (3.24), it follows that can be

expressed as an increment of order of the function :

namely, when , one has,

(3.25)

Next, applying the Mean Value Theorem to the function

on the interval , it follows from (3.25) and (3.24), that there

exists such that

(3.26)

then, applying the same theorem to the function , on the

compact interval whose endpoints are

and

, one obtains, in view of (3.26) and (2.10), that,

(3.27)

where

Observe that the continuity of the functions and , implies that is a finite random variable, moreover (1.3) and (2.11) entail that all its moments are finite as well. Next, combining (3.27) with (1.2), one gets

(3.21). Let us now show that (3.22) holds. It follows from (3.2), (3.6) and (3.10) that

where the random variable has been defined in (2.12); thus we obtain (3.22).

Lemma 3.4

Let be an arbitrary fixed positive real number. There is a constant , only depending on , such that for all ,

satisfying , one has

Proof of Lemma 3.4: The derivative over of the positive function is equal

to

Let us set . When , then the function is increasing on ; thus taking , it follows that the lemma holds. When , then the latter function is increasing on and decreasing on ; thus setting

one obtains the lemma.

Now we are in position to prove Theorem 3.1.

Proof of Theorem 3.1: First notice that it is sufficient to show that

for all (recall that is the event of probability on which (3.5) holds), and one has,

(3.28)

Indeed, (3.28) implies that is a Cauchy

sequence in the Banach space and, as consequence, it converges, in this space, to some limit

denoted by . Next let be the event

of probability defined as

where

is the event introduced in Lemma 3.2 when . Thus it follows from the latter lemma, that for each and all one has ; this is equivalent to , since and are continuous function. Then, letting in (3.28), goes to while fixed, one gets (3.14).

From now on, our goal will be to show that (3.28) holds. To this end, in view of (2.1), it is sufficient to prove that there exist two positive random variables and of finite moment of any order, such that one has for all , and

,

(3.29)

and

(3.30)

We will only show that (3.29) is satisfied, since (3.30) can be

obtained in the same way. Let be two arbitrary and fixed real numbers belonging

to the interval . Observe that in view of (3.13), using the triangle inequality, one has,

(3.31)

Let us now give appropriate bounds for

(3.32)

and derive form them (3.29). We denote by the unique integer such that

(3.33)

Also for all and , we denote by the unique integer

belonging to such that

(3.34)

with the convention that

(3.35)

Observe that when ,

(3.36)

being the integer part function. Also, observe that (3.32), (3.23), and the fact that does not when (see (3.25)), imply that

(3.37)

Let us now study the following two cases: and . First assume that , then

(3.33) implies that and, as a consequence that

. When,

, it follows from (3.37), (3.5) and (3.12), that

where . When, , putting together (3.37), (3.5), (3.12), (3.22) and the fact that , one obtains that,

where and . Thus, we have

shown that there is a positive random variable of finite moment of any order, non depending on , , and , such that for all , one has,

Therefore, in view of (3.33), for each integer satisfying , one has,

(3.38)

Next, it follows from (3.38), the inequality (see (3.33)) and Lemma 3.4 (in which one

takes , and ), that

(3.39)

where

being the constant introduced in Lemma 3.4. Let us now study the case where . Observe that in this case, in view of Relations (3.33) and (3.34), one necessarily has and

(3.40)

Also observe that, using (3.35), (3.36) and (3.40), one obtain that

Thus (3.42) and (3.40) imply that for all , one has,

(3.43)

where . Next, observe that one has for ,

(3.44)

where the constant

Thus combining (3.43) with (3), it follows that for all , one has,

(3.45)

where . Let us now show that, for all , one has,

(3.46)

where , is the constant introduced in Lemma 3.4 and has been introduced

in (3.39). It is clear that (3.45) implies

that (3.46) holds when , so from now on, we assume that and that is an arbitrary nonnegative integer satisfying .

It follows from (3.45) that

Then using Lemma 3.4 (in which one takes , and ), one obtains that

(3.47)

Next combining (3.47) with (3.39), it follows that (3.46) holds in the case where . Finally

(3), (3.32) and (3.46) imply that (3.29) is satisfied.

4 Simulation of via the Haar multiresolution analysis

Our algorithm for simulating mainly relies on Theorem 3.1 which allows to approximate , for large enough,

by the process defined in (3.13) as a finite of sum. First we will give an expression for the latter process which makes it rather easy to simulate, to this end, we need to introduce some notations.

•

For all fixed integers and , the function is defined as,

(4.1)

•

For all fixed integer , we denote by the finite sequence of independent standard

Gaussian random variables defined as,

(4.2)

•

For all fixed integers and , the stochastic process is defined for all

, as,

The following proposition provides a nice expression for the process .

Proposition 4.1

For all fixed integer , let be the stochastic process defined in (3.13). Then one has for all , almost

surely,

(4.4)

Observe that, Relation (4.4), also holds almost surely for all and (i.e. this relation is satisfied on an event of

probability which does not depend on and ), since the trajectories of the processes

and , are with probability , continuous functions.

Proof of Proposition 4.1: The main ingredient of the proof is the Haar multiresolution analysis (see for example [19, 12, 23]) of the Hilbert space ; that is the increasing (in the sense of the inclusion) sequence of the finite dimensional subspaces of defined as,

and for all integer ,

where the orthonormal functions and have been introduced respectively in (3.1) and in (3.2).

Relations (3.17) and (3.19) imply that for every fixed and , the function

, can be viewed as the orthogonal projection (in the sense of the usual inner product of ) of the function , on the space . On the other hand, it is known (see for example [19, 12, 23]) that, the finite sequence,

forms an orthonormal basis of . Therefore, in view of (4.3), one has, for all ,

(4.5)

Finally, using the fact that,

as well as Relations (3.19), (3.4), (4.5) and (4.2),

one obtains (4.4).

Now, we are ready to describe the main step of our algorithm for simulating .

Main steps of our algorithm for simulating :

(1)

We take large enough and we simulate the finite sequence

of the standard independent Gaussian random variables defined in (4.2).

(2)

We simulate

observe that in the case where the centered Gaussian process is a multifractional Brownian motion; such a simulation can be done by making use of one of the efficient methods described in [5].

(3)

Noticing that, for all , and , Relations (4.1), (4.3) and (3.6) imply that,

we approximate the latter integral, by the Riemann sum

(4.6)

On the other hand, observe that (4.1), (4.3) and (3.6) entail that for each ,

(4)

Thus, in view of (4.4), for all , we approximate by

(4.7)

Then we simulate

by using the fact that

(4.8)

and the induction relation, for all ,

(4.9)

Observe that (4.8) and (4.9) easily result from (4.6) and (4.7).

(5)

Finally, by interpolating the points

we obtain a stochastic process which, in view of Theorem 3.1, satisfies the following property: for all fixed

, there exists a random variable of finite moment of any order, such that one has, almost surely, for all big enough,

where is the usual norm on the Hölder space .

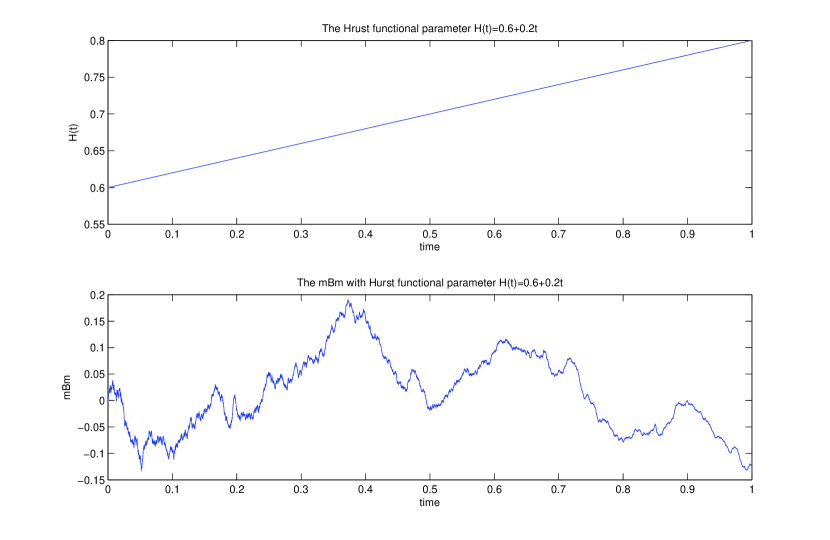

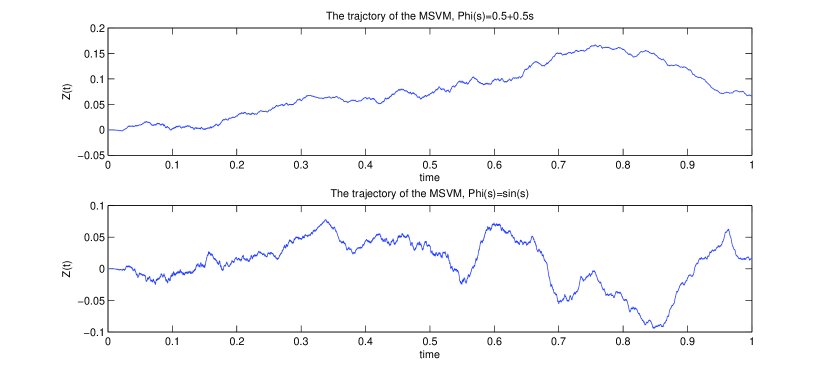

Figure 1: Graph of the function such that for all , and a simulation of a trajectory of a multifractional Brownian motion with Hurst functional parameter .Figure 2: Simulation, in the case where for all , and also in the case where

for all , of a trajectory of the log price process generated through (1.1) by the multifractional Brownian motion

in Figure 1. The shapes of these two simulated trajectories tend to confirm the fact that the pointwise Hölder exponent of does not change from one place to another and is equal to (see Theorem 2.2).

References

[1]

A. Ayache.

Du mouvement brownien fractionnaire au mouvement brownien

multifractionnaire.

Technique et science informatiques, (20-9):1133–1152, 2001.

[2]

A. Ayache and Q. Peng.

Stochastic volatility and multifractional brownian motion.

Stochastic Differential Equations and Processes. Proceedings

SAAP, Springer-Verlag, 7:211–237, 2011.

[3]

A. Ayache and M.S. Taqqu.

Multifractional processes with random exponent.

Publ. Mat., 2(49):459–486, 2005.

[4]

A. Ayache and J. Lévy Véhel.

The generalized multifractional brownian motion.

Statistical Inference for Stochastic Processes, 1-2(3):7–18,

2000.

[5]

O. Barrière.

Synthèse et estimation de mouvements browniens multifractionnaires

monodimensionnels et bidimensionnels. etude de processus à régularité

prescrite.

Ph.D. Thesis, École Centrale de Nantes, 2007.

[6]

A. Benassi, S. Jaffard, and D. Roux.

Gaussian processes and pseudodifferential elliptic operators.

Rev. Mat. Iberoam., 1(13):19–81, 1997.

[7]

S. Bianchi.

Pathwise identification of the memory function of the memory function

of multifractional brownian motion with application to finance.

Int. J. Theoret. Appl. Finance, 2(8):255–281, 2005.

[8]

S. Bianchi and A.Pianese.

Multifractional properties of stock indices decomposed by filtering

their pointwise hölder regularity.

Int. J. Theoret. Appl. Finance, 6(11):567–595, 2008.

[9]

S. Bianchi, A.Pianese, and A.Pantanella.

Modeling stock prices by the multifractional brownian motion: an

improved estimation of the pointwise regularity.

To appear in Quantitative Finance, (11):567–595, 2010.

[10]

F. Comte and E. Renault.

Long memory continuous time models.

J. Econom., (73):101–150, 1996.

[11]

F. Comte and E. Renault.

Long memory in continuous-time stochastic volatility models.

Math. Finance, (8):291–323, 1998.

[12]

I. Daubechies.

Ten lectures on wavelets.

CBMS-NSF series, SIAM Philadelphia, 61, 1992.

[13]

A. Gloter and M. Hoffmann.

Stochastic volatility and fractional brownian motion.

Prépublication du laboratoire de Probabilités & Modèles

Aléatoires des Universités Paris 6 & Paris 7, (746), 2002.

[14]

A. Gloter and M. Hoffmann.

Stochastic volatility and fractional brownian motion.

Stoch. Proc. Appl., (113):143–172, 2004.

[15]

J. Hull and A. White.

The pricing of options on assets with stochastic volatilities.

J. Finance, (3):281–300, 1987.

[16]

I. Karatzas and A.V. Shreve.

Brownian motion and stochastic calculus.

Springer, pages 281–300, 1987.

[17]

M. Ledoux and M. Talagrand.

Probability in banach spaces.

Springer, seccond printing, pages 83–96, 2010.

[18]

A. Melino and S.M. Turnbull.

Pricing foreign currency options with stochastic volatility.

J. Econom., (45):239–265, 1990.

[19]

Y. Meyer.

Wavelets and operators.

Cambridge University Press, 1:191–209, 1992.

[20]

R.F. Peltier and J. Lévy Véhel.

Multifractional brownian motion : definition and preliminary results.

Rapport de recherche de l’INRIA, (2645):239–265, 1995.

[21]

M. Rosenbaum.

Estimation of the volatility persistence in a discretely observed

diffusion model.

Stoch. Proc. Appl., (118):1434–1462, 2008.

[22]

L. Scott.

Option pricing when the variance changes randomly: Estimation and an

application.

J. Financial Quantit. Anal., (22):419–438, 1987.

[23]

P. Wojtaszczyk.

A mathematical introduction to wavelets.

London Mathematical Society Texts, Cambridge University Press,

37:1183–1212, 1997.

Antoine Ayache and Qidi Peng: U.M.R. CNRS 8524, Laboratoire Paul

Painlevé, Bât. M2, Université Lille 1, 59655 Villeneuve d’Ascq Cedex, France.

E-mails: Antoine.Ayache@math.univ-lille1.fr, Qidi.Peng@math.univ-lille1.fr