Adaptive Execution: Exploration and Learning of Price Impact

Abstract

We consider a model in which a trader aims to maximize expected risk-adjusted profit while trading a single security. In our model, each price change is a linear combination of observed factors, impact resulting from the trader’s current and prior activity, and unpredictable random effects. The trader must learn coefficients of a price impact model while trading. We propose a new method for simultaneous execution and learning – the confidence-triggered regularized adaptive certainty equivalent (CTRACE) policy – and establish a poly-logarithmic finite-time expected regret bound. This bound implies that CTRACE is efficient in the sense that the -convergence time is bounded by a polynomial function of and with high probability. In addition, we demonstrate via Monte Carlo simulation that CTRACE outperforms the certainty equivalent policy and a recently proposed reinforcement learning algorithm that is designed to explore efficiently in linear-quadratic control problems.

Key words: adaptive execution, price impact, reinforcement learning, regret bound

1 Introduction

A large block trade tends to ‘‘move the market’’ considerably during its execution by either disturbing the balance between supply and demand or adjusting other market participants’ valuations. Such a trade is typically executed through a sequence of orders, each of which pushes price in an adverse direction. This effect is called price impact. Because it is responsible for a large fraction of transaction costs, it is important to design execution strategies that effectively manage price impact. In light of this, academics and practitioners have devoted significant attention to the topic [Bertsimas and Lo [1998], Almgren and Chriss [2000], Kissell and Glantz [2003], Obizhaeva and Wang [2005], Moallemi et al. [2008], Alfonsi et al. [2010]].

The learning of a price impact model poses a challenging problem. Price impact represents an aggregation of numerous market participants’ interpretations of and reactions to executed trades. As such, learning requires ‘‘excitation’’ of the market, which can be induced by regular trading activity or trades deliberately designed to facilitate learning. The trader must balance the short term costs of accelerated learning against the long term benefits of an accurate model. Further, given the continual evolution of trading venues and population of market participants, price impact models require retuning over time. In this paper, we develop an algorithm that learns a price impact model while guiding trading decisions using the model being learned.

Our problem can be viewed as a special case of reinforcement learning. This topic more broadly addresses sequential decision problems in which unknown properties of an environment must be learned in the course of operation (see, e.g., Sutton and Barto ). Research in this area has established how judicious investments in decisions that explore the environment at the expense of suboptimal short-term behavior can greatly improve longer-term performance. What we develop in this paper can be viewed as a reinforcement learning algorithm; the workings of price impact are unknown, and exploration facilitates learning.

In reinforcement learning, one seeks to optimize the balance between exploration and exploitation – the use of what has already been learned to maximize rewards without regard to further learning. Certainty equivalent control (CE) represents one extreme where at any time, current point estimates are assumed to be correct and actions are made accordingly. This is an instance of pure exploitation; though learning does progress with observations made as the system evolves, decisions are not deliberately oriented to enhance learning.

An important question is how aggressively a trader should explore to learn a price impact model. Unlike many other reinforcement learning problems, in ours a considerable degree of exploration is naturally induced by exploitative decisions. This is because a trader excites the market through regular trading activity regardless of whether or not she aims to learn a price impact model. This activity could, for example, be triggered by return-predictive factors, and given sufficiently large factor variability, the induced exploration might adequately resolve uncertainties about price impact. Results of this paper demonstrate that executing trades to explore beyond what would naturally occur through exploitation can yield significant benefit.

Our work is constructive: we propose the confidence-triggered regularized adaptive certainty equivant policy (CTRACE), pronounced ‘‘see-trace,’’ a new method that explores and learns a price impact model alongside trading. CTRACE can be viewed as a generalization of CE, which at each point in time estimates coefficients of a price impact model via least-squares regression using available data and makes decisions that optimize trading under an assumption that the estimated model is correct and will be used to guide all future decisions. CTRACE deviates in two ways: (1) regularization is applied in least-squares regression and (2) coefficients are only updated when a certain measure of confidence exceeds a pre-specified threshold and a minimum inter-update time has elapsed. Note that CTRACE reduces to CE as the regularization penalty, the threshold, and the minimum inter-update time vanish.

We demonstrate through Monte Carlo simulation that CTRACE outperforms CE. Further, we establish a finite-time regret bound for CTRACE; no such bound is available for CE. Regret is defined here to be the difference between realized risk-adjusted profit of a policy in question and one that is optimal with respect to the true price impact model. Our bound exhibits a poly-logarithmic dependence on time. Among other things, this regret bound implies that CTRACE is efficient in the sense that the -convergence time is bounded by a polynomial function of and with high probability. We define the -convergence time to be the first time when an estimate and all the future estimates following it are within an -neighborhood of a true value with probability at least . Let us provide here some intuition for why CTRACE outperforms CE. First, regularization enhances exploration in a critical manner. Without regularization, we are more likely to obtain overestimates of price impact. Such an outcome abates trading and thus exploration, making it difficult to escape from the predicament. Regularization reduces the chances of obtaining overestimates, and further, tends to yield underestimates that encourage active exploration. Second, requiring a high degree of confidence reduces the chances of occasionally producing erratic estimates, which regularly arise with application of CE. Such estimates can result in undesirable trades and/or reductions in the degree of exploration.

It is also worth comparing CTRACE to a reinforcement learning algorithm recently proposed in Abbasi-Yadkori and Szepesvàri [2010] which appears well-suited for our problem. This algorithm was designed to explore efficiently in a broader class of linear-quadratic control problems, and is based on the principle of optimism in the face of uncertainty. Abbasi-Yadkori and Szepesvàri [2010] establish an regret bound that holds with probability at least , where denotes time and some logarithmic terms are hidden. Our bound for CTRACE is on expected regret and exhibits a dependence on of . We also demonstrate via Monte Carlo simulation that CTRACE dramatically outperforms this algorithm.

To summarize, the primary contributions of this paper include:

-

(a)

We propose a new method for simultaneous execution and learning – the confidence-triggered regularized adaptive certainty equivalent (CTRACE) policy.

-

(b)

We establish a finite-time expected regret bound for CTRACE that exhibits a poly-logarithmic dependence on time. This bound implies that CTRACE is efficient in the sense that, with probability , the -convergence time is bounded by a polynomial function of and .

-

(c)

We demonstrate via Monte Carlo simulation that CTRACE outperforms the certainty equivalent policy and a reinforcement learning algorithm recently proposed by Abbasi-Yadkori and Szepesvàri [2010] which is designed to explore efficiently in linear-quadratic control problems.

The organization of the rest of this paper is as follows: Section 2 presents our problem formulation, establishes existence and uniqueness of an optimal solution to our problem, and defines performance measures that can be used to evaluate policies. In Section 3, we propose CTRACE and derive a finite-time expected regret bound for CTRACE along with two properties: inter-temporal consistency and efficiency. Section 4 is devoted to Monte Carlo simulation in which the performance of CTRACE is compared to that of two benchmark policies. Finally, we conclude this paper in Section 5. All proofs are provided in Appendix. Detailed proofs are available upon request.

2 Problem Formulation

2.1 Model Description

Decision Variable and Security Position We consider a trader who trades a single security over an infinite time horizon. She submits a market buy or sell order at the beginning of each period of equal length. represents the number of shares of the security to buy or sell at period and a positive (negative) value of denotes a buy (sell) order. Let denote the trader’s pre-trade security position before placing an order at period . Therefore, .

Price Dynamics The absolute return of the security is given by

| (1) |

We will explain each term in detail as we progress. This can be viewed as a first-order Taylor expansion of a geometric model

over a certain period of time, say, a few weeks in calendar time, which makes this approximation reasonably accurate for practical purposes. Although it is unrealistic that the security price can be negative with positive probability, our model nevertheless serves its practical purpose for the following reasons: Our numerical experiments conducted in Section 4 show that price changes after a few weeks from now have ignorable impacts on a current optimal action. In other words, optimal actions for our infinite-horizon control problem appear to be quite close to those for a finite-horizon counterpart on a few week time scale. Furthermore, it turns out that in simulation we could learn a unknown price impact model fast enough to take actions that are close to optimal actions within a few weeks. Thus, learning based on our price dynamics model could also be justified. We will give concrete numerical examples later to support these notions.

Price Impact The term represents ‘‘permanent price impact’’ on the security price of a current trade. The permanent price impact is endogenously derived in Kyle [1985] from informational asymmetry between an informed trader and uninformed competitive market makers, and in Rosu [2009] from equilibrium of a limit order market where fully strategic liquidity traders dynamically choose limit and market orders. Huberman and Stanzl [2004] prove that the linearity of a time-independent permanent price impact function is a necessary and sufficient condition for the absence of ‘‘price manipulation’’ and ‘‘quasi-aribtrage’’ under some regularity conditions.

The term indicates ‘‘transient price impact’’ that models other traders’ responses to non-informative orders. For example, suppose that a large market buy order has arrived and other traders monitoring the market somehow realize that there is no definitive evidence for abrupt change in the fundamental value of the security. Then, they naturally infer that the large buy order came merely for some liquidity reason, and gradually ‘‘correct’’ the perturbed price into what they believe it is supposed to be by submitting counteracting selling orders. The dynamics of in (1) indicates that the impact of a current trade on the security price decays exponentially over time, which is considered in Obizhaeva and Wang [2005] that incorporate the dynamics of supply and demand in a limit order market to optimal execution strategies. In Gatheral [2010], it is shown that the exponentially decaying transient price impact is compatible only with a linear instantaneous price impact function in the absence of ‘‘dynamic arbitrage.’’

Observable Return-Predictive Factors We assume that there are multiple observable return-predictive factors that affect the absolute return of the security as in Garleanu and Pedersen [2009]. Those factors could be macroeconomic factors such as gross domestic products (GDP), inflation rates and unemployment rates, security-specific factors such as P/B ratio, P/E ratio and lagged returns, or prices of other securities that are correlated with the security price. In our price dynamics model, denotes these factors and denotes factor loadings. The term represents predictable excess return or ‘‘alpha.’’ We assume that is a first-order vector autoregressive process where is a stable matrix that has all eigenvalues inside a unit disk and is a martingale difference sequence adapted to the filtration . We further assume that is bounded almost surely, i.e. for all for some deterministic constant , and being positive definite and independent of .

Unpredictable Noise The term represents random fluctuations that cannot be accounted for by price impact and observable return-predictive factors. We assume that is a martingale difference sequence adapted to the filtration , and independent of , , and for any . Also, being independent of . Finally, each is assumed to be sub-Gaussian, i.e., for some .

Policy A policy is defined as a sequence of functions where maps the trader’s information set at the beginning of period into an action . The trader observes and at the end of period and thus her information set at the beginning of period is given by . A policy is admissible if generated by satisfies . A set of admissible policies is denoted by .

Objective Function The trader’s objective is to maximize expected average ‘‘risk-adjusted’’ profit defined as

where the first term indicates change in book value and the second term a quadratic penalty for her non-zero security position in the next period that reflects her risk aversion. is a risk-aversion coefficient that quantifies the extent to which the trader is risk-averse.

Assumptions The following is a list of assumptions on which our analysis is based throughout this paper. Let . We will make two more assumptions as we progress.

Assumption 1.

-

(a)

The price impact coefficients are unknown to the trader. Note that they can be learned only through executed trades.

-

(b)

The factor loadings are known to the trader. This is a reasonable assumption since they can be learned by observing prices without any transaction.

-

(c)

The decaying rates of the transient price impact are known to the trader and all the elements are distinct. In practice, they are definitely not known a priori. However, it can be handled effectively for practical purposes by using a sufficiently dense with a large so that potential bias induced by modeling mismatch can be greatly reduced at the expense of increased variance, which can be reduced by regularization.

-

(d)

for some component-wise and some . The constraint is imposed to capture non-zero execution costs in practice. Note that is compact and convex.

Notations and denote the -norm and the Frobenius norm of a matrix, respectively. and denote and , respectively. For a symmetric matrix , means that is positive definite and means that is positive semidefinite. indicates the smallest eigenvalue of . of a matrix indicates the entry of in the th row and in the th column. of a vector indicates the th entry of . of a vector denotes a diagonal matrix whose th diagonal entry is . denotes the th column of and indicates a segment of the th column of from the th entry to the th entry. denotes an indicator function on the event .

2.2 Existence of Optimal Solution

Now, we will show that there exists an optimal policy among admissible policies that maximizes expected average risk-adjusted profit. For convenience, we will consider the following minimization problem that is equivalent to maximize expected average risk-adjusted profit.

We call the negative of average risk-adjusted profit ‘‘average cost.’’ This problem can be expressed as a discrete-time linear quadratic control problem

where , , , ,

Note that is strictly positive but is not necessarily positive semidefinite. Therefore, special care should be taken in order to prove the existence of an optimal policy. We start with a well-known Bellman equation for average-cost linear quadratic control problems

| (2) |

where denotes a differential value function and denotes minimum average cost. It is natural to conjecture . Plugging it into (2), we can obtain a discrete-time Riccati algebraic equation

| (3) |

with a second-order optimality condition . The following theorem characterizes an optimal policy among admissible policies that minimizes expected average cost, and proves existence and uniqueness of such an optimal policy.

Theorem 1.

For any , there exists a unique symmetric solution to (3) that satisfies and where and denotes a spectral radius. Moreover, a policy with is an optimal policy among admissible policies that attains minimum expected average cost .

For ease of exposition, we define some notations: denotes a unique symmetric stabilizing solution to (3) with . denotes a gain matrix for an optimal policy with , denotes a closed-loop system matrix with , and denotes a linear mapping from to a regressor used in least-squares regression for learning price impact, i.e. . Having these notations, we make two assumptions about as follows. Indeed, we can verify through closed-form solutions that these assumptions hold in a special case which will be discussed in Subsection 2.3.

Assumption 2.

-

(a)

There exists such that for any .

-

(b)

and for any

Using Assumption 2, we can obatin an upper bound on uniformly over and .

Lemma 1.

For any , there exists being independent of such that for all . Thus, is finite. For any fixed , where . Moreover, .

Note that Lemma 1 can be applied only when is fixed over time. From now on, we assume without loss of generality otherwise we can always set to be greater than .

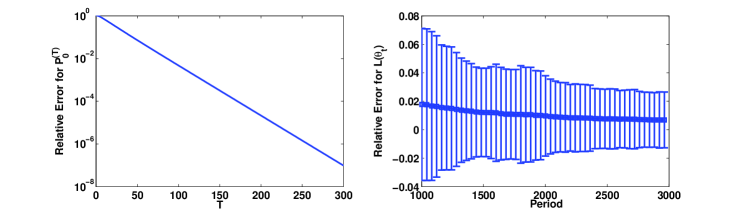

Finally, we present concrete numerical examples that support the validity of our price model as an approximation of the geometric model for practical purposes. As we discussed earlier, our numerical experiments conducted in Section 4 show that our infinite-horizon control problem could be approximated accurately by a finite-time control problem with a time horizon on a few week time scale. To be more precise, we define relative error for as where denotes a coefficient matrix of a quadratic value function at period for a finite-horizon control problem with a terminal period , and denotes a coefficient matrix of a quadratic value function for our infinite-horizon control problem. As shown in Figure 1, the relative error for appears to decrease exponentially in and the relative error for is almost where corresponds to 3.8 trading days.

Furthermore, we could learn unknown fast enough to take actions that are close to optimal actions on a required time scale. An action from a current estimate could be quite close to an optimal action even if estimation error for the current estimate is large, especially in cases where a few ‘‘principal components’’ of with large directional derivatives with respect to are learned accurately. To be more precise, we define relative error for as

where is a stationary process generated by and . The relative error for indicates how different an action from an estimate is than an optimal action from the true value . Figure 1 shows how the relative error for evolves over time with two-standard-error bars when ’s are obtained from a new policy that we will propose in Section 3. As you can see, all the approximate 95%-confidence intervals lie within range after Period 2500 that corresponds to 32 trading days. It implies that actions from estimates learned over a few weeks could be sufficiently close to optimal actions.

2.3 Closed-Form Solution: A Single Factor and Permanent Impact Only

When we consider only the permanent price impact and a single observable factor, we can derive an exact closed-form and as follows.

Although this is a special case of our general setting, we can get useful insights into the effect of permanent price impact coefficient on various quantities. Here are some examples:

-

•

and are strictly decreasing in .

-

•

, .

-

•

, .

-

•

The expected average risk-adjusted profit is strictly decreasing in .

-

•

, .

2.4 Performance Measure: Regret

In this subsection, we define a performance measure that can be used to evaluate policies. For notational simplicity, let , and . Using (3), we can show that

First, we define pathwise regret of a policy at period as where and with . In other words, the pathwise regret of a policy at period amounts to excess costs accumulated over periods when applying relative to when applying the optimal policy . By definition of , the pathwise regret of a policy at period can be expressed as

Second, we define expected regret of a policy at period as . Taking expectation of pathwise regret, we can obtain a more concise expression for expected regret because the last two terms vanish by the law of total expectation. Hence, we have

Finally, we define relative regret of a policy at period as where is minimum expected average cost for . Our choice of performance measure will be either expected regret or relative regret in the rest of this paper.

3 Confidence-Triggered Regularized Adaptive Certainty Equivalent Policy

Our problem can be viewed as a special case of reinforcement learning, which focuses on sequential decision-making problems in which unknown properties of an environment must be learned in the course of taking actions. It is often emphasized in reinforcement learning that longer-term performance can be greatly improved by making decisions that explore the environment efficiently at the expense of suboptimal short-term behavior. In our problem, a price impact model is unknown, and submission of large orders can be considered exploratory actions that facilitate learning.

Certainty equivalent control (CE) represents one extreme where at any time, current point estimates are assumed to be correct and actions are made accordingly. Although learning is carried out with observations made as the system evolves, no decisions are designed to enhance learning. Thus, this is an instance of pure exploitation of current knowledge. In our problem, CE estimates the unknown price impact coefficients at each period via least-squares regression using available data, and makes decisions that maximize expected average risk-adjusted profit under an assumption that the estimated model is correct. That is, an action for CE is given by where with a regressor .

An important question is how aggressively the trader should explore to learn . Unlike many other reinforcement learning problems, a fairly large amount of exploration is naturally induced by exploitative decisions in our problem. That is, regular trading activity triggered by the return-predictive factors excites the market regardless of whether or not she aims to learn price impact. Given sufficiently large factor variability, the induced exploration might adequately resolve uncertainties about price impact. However, we will demonstrate by proposing a new exploratory policy that executing trades to explore beyond what would naturally occur through the factor-driven exploitation can result in significant benefit.

Now, let us formally state that exploitative actions triggered by the return-predictive factors induce a large degree of exploration that could yield strong consistency of least-squares estimates. It is worth noting that pure exploitation is not sufficient for strong consistency in other problems such as Lai and Wei [1986] and Chen and Guo [1986].

Lemma 2.

For any , let , and . Also, let denote a unique solution to . Then,

| (4) |

Moreover, we can show that is continuous on by proving uniform convergence of to on . Continuity leads to which will be used later.

Corollary 1.

is continuous on and .

Lemma 2 implies that increases linearly in time a.s. asymptotically. In addition, we can obtain a similar result for a finite-sample case: There exists a finite, deterministic constant such that grows linearly in time for all with probability at least . This is a crucial result that will be used for bounding above ‘‘-convergence time’’ later. It is formally stated in the following lemma.

Lemma 3.

For any , let , and . Then, there exists an event such that on with

Furthermore, we can extend Lemma 2 in such a way that still increases to infinity linearly in time for time-varying adapted to as long as remains sufficiently close to a fixed for all . Here, denotes a -algebra generated by and is -measurable for each .

Lemma 4.

Consider any and adapted to such that

for all and any . Let , and . Then,

Similarly to Lemma 3, we can obtain a finite-sample result for Lemma 4. This result will provide with a useful insight into how our new exploratory policy operates in the long term.

It is challenging to guarantee that all estimates generated by CE are sufficiently close to one another uniformly over time so that Lemma 4 and Lemma 5 can be applied to CE. In particular, CE is subject to overestimation of price impact that could be considerably detrimental to trading performance. The reason is that overestimated price impact discourages submission of large orders and thus it might take a while for the trader to realize that price impact is overestimated due to reduced ‘‘signal-to-noise ratio.’’ To address this issue, we propose the confidence-triggered regularized adaptive certainty equivalent policy (CTRACE) as presented in Algorithm 1. CTRACE can be viewed as a generalization of CE and deviates from CE in two ways: (1) regularization is applied in least-squares regression, (2) coefficients are only updated when a certain measure of confidence exceeds a pre-specified threshold and a minimum inter-update time has elapsed. Note that CTRACE reduces to CE as the regularization penalty and the threshold tend to zero, and the minimum inter-update time tends to one.

Regularization induces active exploration in our problem by penalizing the -norm of price impact coefficients as well as reduces the variance of an estimator. Without regularization, we are more likely to obtain overestimates of price impact. Such an outcome attenuates trading intensity and thereby makes it difficult to escape from the misjudged perspective on price impact. Regularization decreases the chances of obtaining overestimates by reducing the variance of an estimator and furthermore tends to yield underestimates that encourage active exploration.

Another source of improvement of CTRACE relative to CE is that updates are made based on a certain measure of confidence for estimates whereas CE updates at every period regardless of confidence. To be more precise on this confidence measure, we first present a high-probability confidence region for least-squares estimates from Abbasi-Yadkori et al. [2011].

Proposition 1 (Corollary 10 of Abbasi-Yadkori et al. [2011]).

This implies that for any

By definition, CTRACE updates only when . typically dominates for large because it increases linearly in , and is inversely proportional to the squared estimation error . That is, CTRACE updates only when confidence represented by exceeds the specified level . From now on, we refer to this updating scheme as confidence-triggered update. Confidence-triggered update makes a significant contribution to reducing the chances of obtaining overestimates of price impact by updating ‘‘carefully’’ only at the moments when an upper bound on the estimation error is guaranteed to decrease.

The minimum inter-update time in Algorithm 1 can guarantee that the closed-loop system from CTRACE is stable as long as is sufficiently large. Meanwhile, there is no such stability guarantee for CE. The following lemma provides with a specific uniform bound on .

Lemma 6.

Under CTRACE with

Confidence-triggered update yields a good property of CTRACE that CE lacks: CTRACE is inter-temporally consistent in the sense that estimation errors are bounded with high probability by monotonically nonincreasing upper bounds that converge to zero almost surely as time tends to infinity. The following theorem formally states this property.

Theorem 2 (Inter-temporal Consistency of CTRACE).

Let be estimates generated by CTRACE with , and . Then, the th update time in Algorithm 1 is finite a.s. Moreover, on the event where

and is monotonically nonincreasing for all with a.s.

Moreover, we can show that CTRACE is efficient in the sense that its -convergence time is bounded above by a polynomial of , and with probability at least . We define -convergence time to be the first time when an estimate and all the future estimates following it are within an -neighborhood of with probability at least . If is sufficiently small, we can apply Lemma 4 and Lemma 5 to guarantee that increases linearly in with high probability after -convergence time and thereby confidence-triggered update occurs at every periods. This is a critical property that will be used for deriving a poly-logarithmic finite-time expected regret bound for CTRACE. By Theorem 2, it is easy to see that the -convergence time of CTRACE is bounded above by where is defined as

The following theorem presents the polynomial bound on the -convergence time of CTRACE.

Theorem 3 (Efficiency of CTRACE).

Finally, we derive a finite-time expected regret bound for CTRACE that is quadratic in logarithm of elapsed time using the efficiency of CTRACE and Lemma 5.

Theorem 4 (Finite-Time Expected Regret Bound of CTRACE).

If is CTRACE with , and , then for any and all ,

where , ,

Note that , and are all . Therefore, it is not difficult to see that the expected regret bound for CTRACE is .

4 Computational Analysis

In this section, we will compare via Monte Carlo simulation the performance of CTRACE to that of two benchmark policies: CE and a reinforcement learning algorithm recently proposed in Abbasi-Yadkori and Szepesvàri [2010], which is referred to as AS policy from now on. AS policy was designed to explore efficiently in a broader class of linear-quadratic control problems and appears well-suited for our problem. It updates an estimate only when the determinant of is at least twice as large as the determinant evaluated at the last update, and selects an element from a high-probability confidence region that yields maximum average reward. In our problem, AS policy can translate to update an estimate with at each update time . Intuitively, the smaller price impact, the larger average profit, equivalently, the smaller which is the negative of average profit. In light of this, we restrict our attention to solutions to of the form where denotes a constrained least-squares estimate to with regularization. The motivation is to reduce the amount of computation needed for AS policy otherwise it would be prohibitive. Indeed, the minimum appears to be attained always with the smallest such that , which is provable in the special case considered in Subsection 2.3. Note that can be viewed as a measure of aggressiveness of exploration: means no extra exploration and smaller implies more active exploration.

| 6 | 2 | ||

|---|---|---|---|

| Trading interval | 5 mins | Initial asset price | $50 |

| Half-life of | [5, 7.5, 10, 15, 30, 45] mins | Half life of factor | [10, 40] mins |

| [ 0.50, 0.63, 0.71, 0.79, 0.89, 0.93 ] | diag([0.707, 0.917]) | ||

| ($/share) | [0, 6, 0, 3, 7, 5] | ($/share) | |

| (annualized vol. = 10%) | diag([1, 1]) | ||

| [0.006, 0.002] | |||

| ( 38 trading days) | Sample paths | 600 |

Table 1 summarizes numerical values used in our simulation. The signal-to-noise ratio (SNR), which is defined as under , is 0.058 and the optimal average profit is $765.19 per period. and are sampled independently from Gaussian distribution even though is assumed to be bounded almost surely for the theoretical analysis. In fact, it turns out that the use of Gaussian distribution for does not make a noticeable difference from a bounded case. The regularization coefficient , the confidence-triggered update threshold , the minimum inter-update time and the significance level are chosen via cross-validation with realized profit: For CTRACE, , and . For AS policy, and . The reason for smaller and large for AS policy is to keep the radius of confidence regions small because the exploration done by AS policy tends to be more than necessary and thus costly.

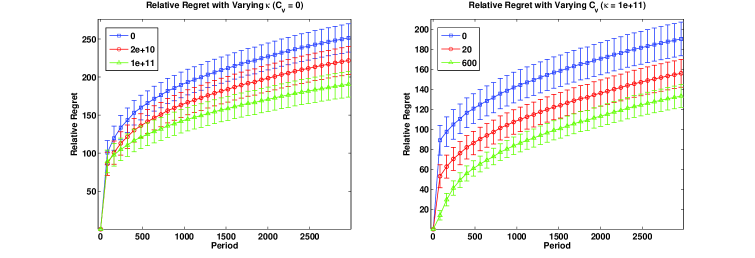

The left figure in Figure 2 illustrates improvement of relative regret due to regularization. It shows the relative regret of CTRACE with varying and fixed , i.e. no confidence-triggered update. The vertical bars indicate two standard errors in both directions, that is, approximate 95% confidence intervals. It is clear that the relative regret is reduced as CTRACE regularizes more, and the improvement from no regularization to is statistically significant with approximate 95% confidence level. The right figure in Figure 2 shows improvement achieved by confidence-triggered update with varying but fixed . As you can see, update based on confidence makes a substantial contribution to reducing relative regret further. The improvement from to is statistically significant with approximate 95% confidence level.

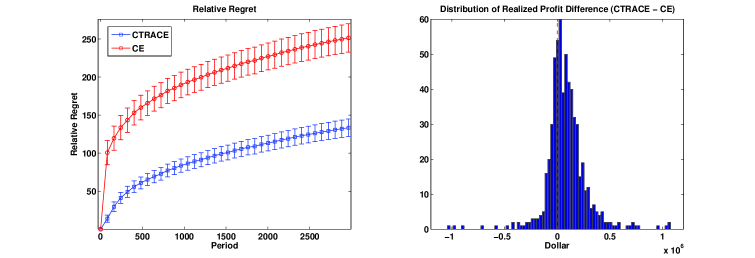

As shown on the left of Figure 3, CTRACE clearly outperforms CE in terms of relative regret and the difference is statistically significant with approximate 95% confidence level. The dominance stems from both regularization and confidence-triggered update as shown in Figure 2. The figure on the right shows an empirical distribution of difference between realized profit of CTRACE and that of CE over 600 sample paths. Much more realizations are located to the right with respect to zero profit. It implies that CTRACE tends to make more profit than CE more frequently.

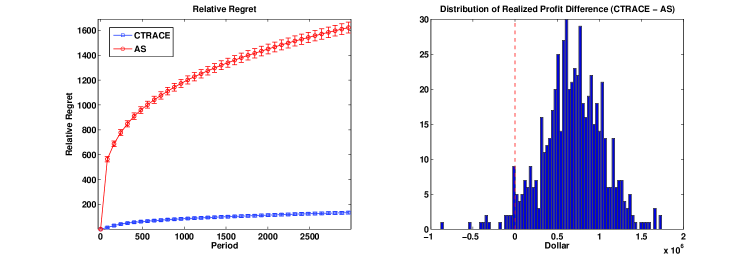

Finally, we compare performance of CTRACE to that of AS policy in Figure 4. The left figure shows that CTRACE outperforms AS policy even more drastically than CE in terms of relative regret, and the superiority is statistically significant with approximate 95% confidence level. On the right, you can see an empirical distribution of difference between realized profit of CTRACE and that of AE over 600 sample paths. It is clear that CTRACE is more profitable than AS policy in most of the sample paths. This illustrates that aggressive exploration performed by AS policy is too costly. The reason is that AS policy is designed to explore actively in situations where pure exploitation done by CE is unable to identify a true model. In our problem, however, a great degree of exploration is naturally induced by observable return-predictive factors and thus aggressiveness of exploration suggested by AS policy turns out to be even more than necessary. Meanwhile, CTRACE strikes a desired balance between exploration and exploitation by taking into account factor-driven natural exploration.

5 Conclusion

We have considered a dynamic trading problem where a trader maximizes expected average risk-adjusted profit while trading a single security in the presence of unknown price impact. Our problem can be viewed as a special case of reinforcement learning: the trader can improve longer-term performance significantly by making decisions that explore efficiently to learn price impact at the expense of suboptimal short-term behavior such as execution of larger orders than appearing optimal with respect to current information. Like other reinforcement learning problems, it is crucial to strike a balance between exploration and exploitation. To this end, we have proposed the confidence-triggered regularized adaptive certainty equivalent policy (CTRACE) that improves purely exploitative certainty equivalent control (CE) in our problem. The enhancement is attributed to two properties of CTRACE: regularization and confidence-triggered update. Regularization encourages active exploration that accelerates learning as well as reduces the variance of an estimator. It helps keep CTRACE from being a passive learner due to overestimation of price impact that abates trading. Confidence-triggered update allows CTRACE to have monotonically nonincreasing upper bounds on estimation errors so that it reduces the frequency of overestimation. Using these two properties, we derived a finite-time expected regret bound for CTRACE of the form . Finally, we have demonstrated through Monte Carlo simulation that CTRACE outperforms CE and a reinforcement learning policy recently proposed in Abbasi-Yadkori and Szepesvàri [2010].

As extention to our current model, it would be interesting to develop an efficient reinforcement learning algorithm for a portfolio of securities. Another interesting direction is to incorporate a prior knowledge of particular structures of price impact coefficients, e.g. sparsity, to an estimation problem. It is worth considering other regularization schemes such as LASSO.

Appendix A Proofs

Proof of Theorem 1 Since the evolution of is not affected by , and , it is not difficult to see that there exists a desired for our stochastic control problem if there exists with the same properties for a deterministic control problem having no and . Let denote reduced coefficient matrices for the deterministic problem of appropriate dimensions. Now, is controllable and this problem is a special case of the problem considered in Molinari [1975]. By Theorem 1 in Molinari [1975], there exists a desired if for all on the unit circle where

In our problem, it is not difficult to check that for any , and ,

and . Therefore, the desired result follows. Noting an upper block diagonal structure of the original closed-loop system matrix , we can easily see that the stability for the deterministic problem carries over to our original problem. The uniqueness of a stabilizing solution follows from the stability. For the optimality of , we can use the same proof in Chapter 4 of Bertsekas [2005]. ∎

Proof of Lemma 1 By Theorem 1, for all . Since is a compact set and Assumption 2-(a) implies the continuity of and , it follows that and . Therefore, by Theorem in Buchanan and Parlett [1966], uniformly converges to zero matrix. That is, for any , there exists being independent of such that for all . Also, by continuity of and compactness of . For any , it is easy to see that by definition of and . Since ,

Since , it follows that . ∎

Proof of Lemma 2 For notational simplicity, let , and . The almost-sure convergence in (4) follows from Lemma 2 in Anderson and Taylor [1979]. It is easy to see that is full-rank since . Therefore, it is sufficient to show that is positive definite. Since is a stable matrix and , where . Thus, it is sufficient to show that is full-rank. First, we will show that is linearly independent. We can show by induction that where and . Since each is a polynomial of degree and its leading coefficient is all , we can transform into Vandermonde matrix through elementary row operations. Thus, is nonsingluar. Now, suppose for some . By definition of and , it implies . Then, by nonsingularity of , we may conclude . Therefore, and we may conclude that is full-rank. ∎

Proof of Corollary 1 By Assumption 2-(a), is continuous on and so are and . Uniform convergence of to on follows from the fact that for any

Since is continuous in for all , the limiting matrix is continuous in component-wise. Thus, so is . Finally, is continuous on . Since and is a compact set, it follows from its continuity that . ∎

Proof of Lemma 3 Let denote an elementary vector whose entries are all zero except for th entry being one and . Since , is an almost-surely bounded martingale difference process adapted to and thus it is conditionally sub-Gaussian with Hence, if we use a special case of Corollary 1 in Abbasi-Yadkori et al. [2011] with for all , then for all and any

Using and , it follows from the union bound that where and

On the above event, and . We can rewrite as

Repeating times a process of left-multiplying both sides with , right-multiplying with and adding the resulting inequality into the original one side-by-side, we obtain

Note that and . Taking limit over and using these two inequalities, we have with probability at least

Setting and , we have for all . It is easy to show that Similarly, from , we can obtain for all

Since , it follows that and thus . ∎

Proof of Lemma 4 For notational convenience, let , , , , and . By definition of and , Since can be expressed as , we have

Then, we can show that

It follows that

Taking on both sides, Likewise, we can show that ∎

Proof of Lemma 5 Using the same techniques in the proof of Lemma 3 and Lemma 4, we can obtain that on the event with ,

Proof of Lemma 6 Using for and , we can show by induction that for all . For any , Finally, . ∎

Proof of Theorem 2 Given , it is easy to show that . Using and Proposition 1, we can show that on the event for any

For any , . It is easy to show through elementary calculus that is strictly decreasing in if . ∎

Proof of Theorem 3 Using for all , we can show that

Suppose for contradiction that . Let be the last update time less than . Then, there is no update time in the interval by definition of and . By definition of and Lemma 3,

It is clear that . Consequently, is eligible for a next update time after . It implies that but this is a contradiction. ∎

References

- Abbasi-Yadkori and Szepesvàri [2010] Y. Abbasi-Yadkori and C. Szepesvàri. Regret bounds for the adaptive control of linear quadratic systems. In 24th Annual Conference on Learning Theory. JMLR: Workshop and Conference Proceedings, 2010.

- Abbasi-Yadkori et al. [2011] Y. Abbasi-Yadkori, D. Pal, and C. Szepesvàri. Online least squares estimation with self-normalized processes: An application to bandit problems. Working paper, 2011.

- Alfonsi et al. [2010] A. Alfonsi, A. Schied, and A. Schulz. Optimal execution strategies in limit order books with general shape functions. Quantitative Finance, 10:143–157, 2010.

- Almgren and Chriss [2000] R. Almgren and N. Chriss. Optimal control of portfolio transactions. Journal of Risk, 3:5–39, 2000.

- Anderson and Taylor [1979] T. W. Anderson and J. B. Taylor. Strong consistency of least squares estimates in dynamic models. The Annals of Statistics, 7:484–489, 1979.

- Bertsekas [2005] D. P. Bertsekas. Dynamic programming and optimal control, volume 2. Athena Scientific, Belmont, MA, 3rd edition, 2005.

- Bertsimas and Lo [1998] D. Bertsimas and A. W. Lo. Optimal control of execution costs. Journal of Financial Markets, 1:1–50, 1998.

- Buchanan and Parlett [1966] M. L. Buchanan and B. N. Parlett. The uniform convergence of matrix powers. Numerische Mathematik, 9(1):51–54, 1966.

- Chen and Guo [1986] H. Chen and L. Guo. Convergence rate of least squares identification and adaptive control for stochastic systems. International Journal of Control, 44:1459–1476, 1986.

- Garleanu and Pedersen [2009] N. Garleanu and L. H. Pedersen. Dynamic trading with predictable returns and transaction costs. Working paper, 2009.

- Gatheral [2010] J. Gatheral. No-dynamic-arbitrage and market impact. Quantitative Finance, 10:749–759, 2010.

- Huberman and Stanzl [2004] G. Huberman and W. Stanzl. Price manipulation and quasi-arbitrage. Econometrica, 74(4):1247–1276, 2004.

- Kissell and Glantz [2003] R. Kissell and M. Glantz. Optimal Trading Strategies: Quantitative Approaches for Managing Market Impact and Trading Risk. Amacom Books, 2003.

- Kyle [1985] A. S. Kyle. Continuous auctions and insider trading. Econometrica, 53(6):1315–1335, 1985.

- Lai and Wei [1986] T. L. Lai and C. Wei. Extended least squares and their applications to adaptive control and prediction in linear systems. IEEE Transactions on Automatic Control, 31:898–906, 1986.

- Moallemi et al. [2008] C. C. Moallemi, B. Park, and Van Roy B. Strategic execution in the presence of an uninformed arbitrageur. forthcoming in Journal of Financial Markets, 2008.

- Molinari [1975] B. P. Molinari. The stabilizing solution of the discrete algebraic riccati equation. IEEE Transactions on Automatic Control, 20(3):396–399, 1975.

- Obizhaeva and Wang [2005] A. Obizhaeva and J. Wang. Optimal trading strategy and supply/demand dynamics. Working paper, 2005.

- Rosu [2009] I. Rosu. A dynamic model of the limit order book. Review of Financial Studies, 22:4601–4641, 2009.

- [20] R. S. Sutton and A. G. Barto. Reinforcement learning: An introduction.