Antti Knowleslabel=e1]knowles@math.ethz.ch

[Jun Yinlabel=e2]jyin@math.uwisc.edu

[

New York University and University of Wisconsin

Department of Mathematics

ETH Zürich

Rämistrasse 101

8092 Zürich

Switzerland

Department of Mathematics

University of Wisconsin

Madison, Wisconsin 53706

USA

(2014; 7 2012; 3 2013)

Abstract

We derive the joint asymptotic distribution of the outlier eigenvalues

of an additively deformed Wigner matrix . Our only assumptions on

the deformation are that its rank be fixed and its norm bounded. Our

results extend those of [The isotropic semicircle law and deformation of Wigner

matrices. Preprint] by admitting overlapping outliers

and by computing the joint distribution of all outliers. In particular,

we give a complete description of the failure of universality first

observed in [Ann. Probab.37 (2009) 1–47;

Ann. Inst. Henri Poincaré Probab. Stat.48 (1013) 107–133;

Free convolution with a semi-circular

distribution and eigenvalues of spiked deformations of Wigner matrices.

Preprint]. We also show that, under suitable

conditions, outliers may be strongly correlated even if they are far

from each other. Our proof relies on the isotropic local semicircle law

established in [The isotropic semicircle law and deformation of Wigner

matrices. Preprint]. The main technical achievement of the

current paper is the joint asymptotics of an arbitrary finite family of

random variables of the form .

15B52,

60B20,

82B44,

Random matrix,

universality,

deformation,

outliers,

doi:

10.1214/13-AOP855

keywords:

[class=AMS]

keywords:

††volume: 42††issue: 5

and

t1Supported in part by NSF Grant DMS-07-57425 Swiss National Science Foundation Grant 144662.

t2Supported in part by NSF Grant DMS-12-07961.

1 Introduction

In this paper, we study a Wigner matrix —a random

matrix whose entries are independent up to symmetry constraints—that

has been deformed by the addition of a finite-rank matrix belonging

to the same symmetry class as . By Weyl’s eigenvalue interlacing

inequalities, such a deformation does not influence the global

statistics of the eigenvalues as . Thus, the empirical

eigenvalue densities of the deformed matrix and the undeformed

matrix have the same large-scale asymptotics, and are governed by

Wigner’s famous semicircle law. However, the behavior of individual

eigenvalues may change dramatically under such a deformation. In

particular, deformed Wigner matrices may exhibit

outliers—eigenvalues detached from the bulk spectrum. They

were first investigated in FKoml for a particular rank-one

deformation. Subsequently, much progress

SoshPert , SoshPert2 , FP , CDMF1 , CDMF2 , CDMF3 , BGN , BGGM1 , BGGM2 , KY2 has

been made in the understanding of the outliers of deformed Wigner

matrices. We refer to SoshPert , SoshPert2 , KY2 for a more detailed

review of recent developments.

We normalize so that its spectrum is asymptotically given by the

interval . The creation of an outlier is associated with a

sharp transition, where the magnitude of an eigenvalue of

exceeds the threshold . As (resp., ) becomes larger than

, the largest (resp., smallest) nonoutlier eigenvalue of

detaches itself from the bulk spectrum and becomes an outlier. This

transition is conjectured to take place on the scale . In fact, this scale was established in

BBP , Pec , BV1 , BV2 for the special cases where is

Gaussian—the Gaussian Orthogonal Ensemble (GOE) and the Gaussian

Unitary Ensemble (GUE). We sketch the results of BBP , Pec , BV1 , BV2

in the case of additive deformations of GOE/GUE. For simplicity, we

consider rank-one deformations, although the results of

BBP , Pec , BV1 , BV2 cover arbitrary finite-rank deformations. Let

the eigenvalue of be of the form for some

fixed . In BBP , Pec , BV1 , BV2 , the authors proved

for any fixed the weak convergence

where denotes the largest eigenvalue of . In

particular, the largest eigenvalue of fluctuates on the scale

. Moreover, the asymptotics in of the law was

analysed in BBP , Pec , BV1 , BV2 , Bthesis : as (and

after an appropriate affine scaling), the law converges to

a Gaussian; as , the law converges to the

Tracy–Widom- distribution (where for GOE and for GUE), which famously governs the distribution of the largest

eigenvalue of the underformed matrix TW1 , TW2 .

The proofs of BBP , Pec use an asymptotic analysis of Fredholm

determinants, while those of BV1 , BV2 , Bthesis use an explicit

tridiagonal representation of ; both of these approaches rely

heavily on the Gaussian nature of . In order to study the phase

transition for non-Gaussian matrix ensembles, and in particular address

the question of spectral universality, a different approach is needed.

Interestingly, it was observed in CDMF1 , CDMF2 , CDMF3 that the

distribution of the outliers is not universal, and may depend on the

law of as well as the geometry of the eigenvectors of . The

nonuniversality of the outliers was further investigated in

SoshPert , SoshPert2 , KY2 .

In a recent paper KY2 , we considered finite-rank deformations of

a Wigner matrix whose entries have subexponential decay. The two main

results of KY2 may be informally summarized as follows.

{longlist}[(a)]

We proved that the nonoutliers of stick

to the extremal eigenvalues of the original Wigner matrix

with high precision, provided that each eigenvalue of

satisfies .

We identified the asymptotic distribution of a single

outlier, provided that (i) it is separated from the asymptotic

bulk spectrum by at least and (ii) it does not overlap with any other outlier

of . Here, two outliers are said to overlap if

their separation is comparable to the scale on which they

fluctuate; see Section 2.2 below for a precise

definition.

Note that the assumption (i) of (b) is optimal, up to the logarithmic

factor . Indeed, the extremal bulk eigenvalues

of are known KY2 , Theorem 2.7, to fluctuate on the scale

; for an eigenvalue of to be an outlier, therefore,

we require that its distance from the asymptotic bulk spectrum

be much greater than . See Section 2.2 below

for more details.

The goal of this paper is to extend the result (b) by obtaining a

complete description of the asymptotic distribution of the outliers.

Our only assumptions on the deformation are that its

rank be fixed and its norm bounded. (In particular, the eigenvalues of

may depend on in an arbitrary fashion, provided they remain

bounded, and its eigenvectors may be an arbitrary orthonormal family.)

Our main result gives the asymptotic joint distribution of all

outliers. Here, an outlier is by definition an eigenvalue of

whose classical location [see (7) below] is separated from

the asymptotic bulk spectrum by at least for some (large) constant . Our main result is given in

Theorem 2.11 below.

Thus, in this paper we extend the result (b) in two directions: we

allow overlapping outliers, and we derive the joint asymptotic

distribution of all outliers. The distribution of overlapping outliers

is more complicated than that of nonoverlapping outliers, as

overlapping outliers exhibit a level repulsion similar to that among

the bulk eigenvalues of Wigner matrices. This repulsion manifests

itself by the joint distribution of a group of overlapping outliers

being given by the distribution of eigenvalues of a small (explicit)

random matrix [see (17) below]. The mechanism

underlying the repulsion among outliers is therefore the same as that

for the eigenvalues of GUE: the Jacobian relating the

eigenvalue–eigenvector entries to the matrix entries has a Vandermonde

determinant structure, and vanishes if two eigenvalues coincide.

Several special cases of overlapping outliers have already been studied

in the works SoshPert , SoshPert2 , CDMF1 , CDMF2 , CDMF3 , which in

particular exhibited the level repulsion mechanism described above.

Due to this level repulsion, overlapping outliers are obviously not

asymptotically independent. A novel observation, which follows from our

main result, is that in general nonoverlapping outliers are not

asymptotically independent either; in this case the lack of

independence does not arise from level repulsion, but from a more

subtle interplay between the distribution of and the geometry of

the eigenvectors of . In some special cases, such as

GOE/GUE,

nonoverlapping outliers are, however, asymptotically independent. More

precisely, our main result (Theorem 2.11 below) shows

that two outliers may, under suitable conditions on and , be

strongly correlated in the limit , even if they are far

from each other (e.g., on opposite sides of the bulk spectrum).

Finally, we note that throughout this paper we assume that the entries

of have subexponential decay. We need this assumption because our

proof relies heavily on the local semicircle law and eigenvalue

rigidity estimates for , proved in EYY3 under the assumption

of subexponential decay. However, this assumption is not fundamental to

our approach, which may be combined with the recent methods for dealing

with heavy-tailed Wigner matrices developed in EKYY1 , EKYY2 , LY .

Moreover, the assumption that the norm of be bounded may be easily

removed; in fact, large eigenvalues of are easier to treat than

small ones.

We remark that recently Pizzo, Renfrew and Soshnikov

SoshPert , SoshPert2 took a different approach, and derived the

asymptotic distribution of a single group of overlapping outliers under

optimal tail assumptions on . On the other hand, in

SoshPert , SoshPert2 it is assumed that the eigenvalues of are

independent of and that its eigenvectors satisfy a condition which

roughly constrains them to be either strongly localized or delocalized.

1.1 Outline of the proof

As in KY2 , our proof relies on the isotropic local

semicircle law, proved in KY2 , Theorems 2.2 and 2.3. The

isotropic local semicircle law is an extension of the local

semicircle law, whose study was initiated in ESY1 , ESY3 . The

local semicircle law has since become a cornerstone of random matrix

theory, in particular in establishing the universality of Wigner

matrices ESY4 , ESY6 , EYY2 , EYY3 , TV1 , TV2 . The strongest versions of

the local semicircle law, proved in EYY3 , EKYY1 , give precise

estimates on the local eigenvalue density, down to scales containing

eigenvalues. In fact, as formulated in EYY3 , the

local semicircle law gives optimal high-probability estimates on the

quantity

(1)

where denotes the Stieltjes transform of Wigner’s semicircle law

and is the resolvent of .

The isotropic local semicircle law is a generalization of the local

semicircle law, in that it gives optimal high-probability estimates on

the quantity

(2)

where and are arbitrary deterministic

vectors. Clearly, (1) is a special case obtained from

(2) by setting and

, where denotes th

standard basis vector of .

As in the works SoshPert , SoshPert2 , KY2 , a major part of our

proof consists in deriving the asymptotic distribution of the entries

of . The main technical achievement of this paper is to obtain

the joint asymptotics of an arbitrary finite family of

variables of the form ,

whereby the spectral parameters of different entries may differ,

and are assumed to satisfy for some positive constant . The

question of the joint asymptotics of the resolvent entries occurs more

generally in several problems on deformed random matrix models, and we

therefore believe that the techniques of this paper are also of

interest for other problems on deformed matrix ensembles.

An important ingredient in our proof is the four-step strategy

introduced in KY2 . It may be summarized as follows: (i)

reduction to the distribution of the resolvent , (ii) the case of

Gaussian , (iii) the case of almost Gaussian , (iv) the case of

general . Steps (i)–(iii) in the current paper are substantially

different from their counterparts in KY2 ; this results from

treating an entire overlapping group of outliers simultaneously, as

well as from the need to develop an argument that admits an analysis of

the joint law of different groups. In fact, for pedagogical reasons,

first—in Sections 4–7—we give the

proof for the case of a single group of overlapping

outliers,333In the resolvent language, this means that the

spectral parameters of all the resolvent entries coincide. and

then—in Section 9.1—extend it to yield the full

joint distribution. In contrast to the steps (i)–(iii), step (iv)

survives almost unchanged from KY2 , and in

Section 7 we give an explanation of the required

modifications.

Another ingredient of our proof is a two-level partitioning of the

outliers combined with near-degenerate perturbation theory for

eigenvalues. Roughly, outliers are partitioned into blocks depending on

whether they overlap. In the finer partition, denoted by below

(see Definition 2.10), we regroup two outliers into the same

block if their mean separation is bounded by some large constant

(denoted by below) times the magnitude of their fluctuations. Due

to logarithmic error factors of the form that

appear naturally in high-probability estimates pervading our proof, we

shall require a second, coarser, partition, denoted by below

(see Definition 9.1). In , we regroup two

outliers into the same block if their mean separation is bounded by

times the magnitude of their fluctuations.

The link between and is provided by perturbation theory,

and is performed in Sections 8 (for a single group)

and 9 (for the full joint distribution).

2 Formulation of results

2.1 The setup

Let be an random matrix. We

assume that the upper-triangular entries are

independent complex-valued random variables. The remaining entries of

are given by imposing . Here denotes the Hermitian

conjugate of . We assume that all entries are centred, . In addition, we assume that one of the two following

conditions holds.

{longlist}[(ii)]

Real symmetric Wigner matrix: for all and

Complex Hermitian Wigner matrix:

We introduce the usual index of random matrix theory, defined

to be in the real symmetric case and in the complex Hermitian

case. We use the abbreviation GOE/GUE to mean GOE if is a real

symmetric Wigner matrix with Gaussian entries and GUE if is a

complex Hermitian Wigner matrix with Gaussian entries. We assume that

the entries of have uniformly subexponential decay, that is, that

there exists a constant such that

(3)

for all , and . Note that we do not assume the entries of

to be identically distributed, and we do not require any smoothness in

the distribution of the entries of .

We consider a deformation of fixed, finite rank . Let

be a deterministic matrix satisfying , and be a deterministic

diagonal matrix whose eigenvalues are nonzero. Both and depend

on . We sometimes also use the notation , where

are

orthonormal, as well as . We always assume

that the eigenvalues of satisfy

(4)

where is some fixed positive constant. We are interested in

the spectrum of the deformed matrix

The following definition summarizes our conventions for the spectrum of

a matrix. For our purposes, it is important to allow the matrix entries

and its eigenvalues to be indexed by an arbitrary subset of positive

integers.

Definition 2.1.

Let be a finite set of positive integers, and let be a Hermitian

matrix whose entries are indexed by elements of . We denote by

the family of eigenvalues of . We always order the eigenvalues so

that if .

By a slight abuse of notation, we sometimes identify with

the set . Thus, for

instance, denotes the distance

between and viewed as subsets of .

We abbreviate the (random) eigenvalues of and by

The following definition introduces a convenient notation for minors of

matrices.

Definition 2.2((Minors)).

For an matrix and a subset of integers, we define the matrix

We shall frequently make use of the logarithmic control parameter

(5)

The interpretation of is that of a slowly growing parameter

[note that for any and

large enough ]. Throughout this paper, every

quantity that is not explicitly a constant may depend on , with

the sole exception of the rank of the deformation, which is

required to be fixed. Unless needed, we consistently drop the argument

from such quantities.

We denote by a generic positive large constant, whose value may

change from one expression to the next. For two positive quantities

and , we use the notation to mean for some positive constant . Moreover, we

write if and if . Finally, for we set .

2.2 Heuristics of outliers

Before stating our results, we give a heuristic description of the

behavior of the outliers. An eigenvalue of satisfying

(6)

gives rise to an outlier located around its classical

location , where we defined, for ,

(7)

and

(8)

Condition (6) may be heuristically understood as

follows; for simplicity set and . The extremal

eigenvalues of that are not outliers fluctuate on the

scale (see KY2 , Theorem 2.7), the same scale as the

extremal eigenvalues of the undeformed matrix . For the largest

eigenvalue of to be an outlier, we require that

its separation from the asymptotic bulk spectrum , which is of

the order , be much greater than . This leads

to condition (6) by a simple expansion of

around 1.

The outlier associated with fluctuates on the

scale . Thus,

fluctuates on the scale if is

well-separated from the critical point , and on the scale

if is critical, that is, for some fixed . The outliers associated with and overlap if

their separation is comparable to or less than the scale on which they

fluctuate. The overlapping condition thus reads

(9)

for some (typically large) constant . Note that the factor

on the right-hand side could be replaced

with . Indeed, recalling

(6), it is not hard to check that

(9) for some is equivalent to

(9) with on the right-hand side replaced with

and the constant replaced with a constant .

Using (7) and recalling (6), we may

rewrite the overlapping condition (9) as

(10)

for some . As in (9), may be replaced with .

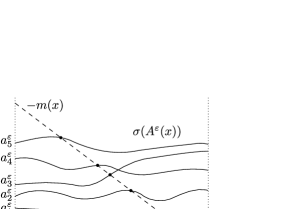

Figure 1 summarizes the general picture of outliers.

Figure 1: A general outlier configuration. We draw the outlier associated with using a black line marking its mean location

and a grey curve indicating its probability density. The breadth of the

curve associated with is of the order . Outliers

whose probability densities overlap satisfy (9) [or, equivalently,

(10)]. We do not draw the bulk eigenvalues,

which are contained in the grey bar.

2.3 The distribution of a single group

After these preparations, we state our results. We begin by defining a

reference matrix which will describe the distribution of a group of

overlapping outliers. Define the moment matrices and of through

Using the matrices and , we define the

deterministic functions

where , is an

matrix, and an matrix. Moreover, we define the

deterministic matrix

Remark 2.3.

Using Cauchy–Schwarz and assumption (3), it is easy

to check that , ,

and are uniformly bounded for satisfying (in the sense of quadratic forms).

Next, let be a positive sequence satisfying

. (Our result will be independent of

provided it satisfies this condition; see

Remark 2.4 below.) The sequence will serve as

a cutoff in the size of the entries of when computing the law of

: entries of smaller than give rise to an

asymptotically Gaussian random variable by the central limit theorem;

the remaining entries are treated separately, and the associated random

variable is in general not Gaussian. Thus, we define the matrix

through

For satisfying we define the matrix

(11)

Abbreviate

(12)

Note that is nothing but the covariance matrix of a GOE/GUE

matrix: if is an GOE/GUE matrix then

. We introduce an

Gaussian matrix , independent of , which is complex

Hermitian for and real symmetric for . The

entries of are centred, and their law is determined by the

covariance

Here is a term, that is,

needed to ensure that the right-hand side of (2.3) is a

nonnegative matrix. This nonnegativity follows as a

by-product of our proof, in which the right-hand side of

(2.3) is obtained from the covariance of an explicit random

matrix; see Proposition 6.1 below for more

details. Note that the term does not influence the

asymptotic distribution of .

Remark 2.4.

A different choice of , subject to , leads to the same asymptotic distribution for . This is an easy consequence of the central limit theorem

and the observation that the matrix entries

have covariance matrix .

Before stating our result in full generality, we give a special case

which captures its essence and whose statement is somewhat simpler.

Theorem 2.5

For large enough the following holds. Let

be a subset of consecutive integers, and fix . Suppose that

. Suppose moreover

that there is a constant such that

(14)

for all and, as ,

(15)

for all .

Define the rescaled eigenvalues

through

(16)

where we recall the definition (8) of . Let

denote the eigenvalues of the random

matrix

(17)

Then for any bounded and continuous function we have

The subset indexes outliers that belong to the same group of

overlapping outliers, as required by (14) [see also

(10) in the preceding discussion]. As required by

(15), the remaining outliers do not overlap with the

outliers indexed by .

Remark 2.6.

The reference point for the block is arbitrary and

unimportant. See Lemma 4.6 below and the comment

preceding it for a more detailed discussion.

Remark 2.7.

For the special case , Theorem 2.5

essentially444In fact, condition of KY2 analogous to

(15), equation (2.24) in KY2 , is slightly

stronger than (15). reduces to Theorem 2.14 of

KY2 . In addition, Theorem 2.5 corrects a

minor issue in the statement of Theorem 2.14 of KY2 , where the

variance of was not necessarily positive. Indeed, in the

language of the current paper, in KY2 the term in (11) was of the form , which

amounted to transferring a large Gaussian component from to

. This transfer was ill-advised as it sometimes resulted in

a negative variance for (which would however be compensated in the

sum by a large asymptotically Gaussian component in

).

The functions , , and

in (11) and (2.3) are in general nonzero in

the limit . They encode the nonuniversality of

the distribution of the outliers. Thus, the distribution of the

outliers may depend on the law of the entries of as well as on the

geometry of the eigenvectors .

In the GOE/GUE case, it is easy to check that is asymptotically Gaussian with covariance matrix

(18)

Moreover, if then the matrix

converges weakly to a Gaussian matrix with

covariance given by (18). In this case,

therefore, the nonuniversality is washed out. Thus, only outliers

separated from the bulk spectrum by a distance of order one

may exhibit nonuniversality.

If , then an appropriate

choice of yields as well

as a matrix whose covariance is asymptotically that of the

GOE/GUE case, that is, (18). Hence, in this case

the only manifestation of nonuniversality is the deterministic shift

given by .

It is possible to find scenarios in which each term of

(11) and (2.3) [apart from the trivial error

term in (2.3)] contributes in the limit .

This is, for instance, the case if and

do not depend on and , is not asymptotically , and an eigenvector satisfies as well as for some constant .

We refer to KY2 , Remarks 2.17–2.21, for analogous remarks,

where more details are given for the case .

Next, we give the asymptotic distribution of a group of overlapping

outliers in full generality. Thus, Theorem 2.9 below

holds for arbitrary sequences and

satisfying and (4).

Definition 2.8.

Let and be given. For and satisfying , define as the smallest subset of with the two following properties.

{longlist}[(ii)]

.

If for we have and

(19)

then either or .

The subset indexes those outliers that belong to the

same group of overlapping outliers as , where is a cutoff

distance used to determine whether two outliers are considered

overlapping. Note that is a set of consecutive

integers.

Theorem 2.9

For large enough the following holds. Let be

arbitrary, and let be bounded continuous functions,

where is a function on . Then there exist and such that for all and the following holds.

In order to describe the joint distribution of all outliers, we

organize them into groups of overlapping outliers, using a partition

whose blocks are defined using the subsets

from Definition 2.8.

Definition 2.10.

Let and be given, and fix and . We introduce a

partition555That is a partition follows from the

observation that if and only if . Therefore if and satisfy and then either or

.

on a subset of , defined as

We also use the notation and .

The indices in give rise to outliers, which are grouped into

the blocks of . Indices in do not give rise to outliers.

For , we define

(22)

We chose this value for definiteness, although any other choice of

with would do equally well.

Next, in analogy to (17), we define a reference matrix whose

eigenvalues will have the same asymptotic distribution as the

appropriately rescaled outliers .

Define the block diagonal matrix ,

where

In addition, we introduce a Hermitian, Gaussian matrix , that is, independent of

and whose entries have mean zero. It is block diagonal, , where the block is a matrix. The law of is determined by the covariance

where we defined

(Note that .) As in (2.3), the factor , whose contribution vanishes in the limit

, simply ensures that the right-hand side of (2.4)

defines a nonnegative matrix; this nonnegativity is an immediate

corollary of our proof in Section 9.1.

Next, in analogy to (16), we introduce the rescaled family

of outliers whose entries are defined by

(24)

where we recall the definition (8) of .

Moreover, for let denote the eigenvalues of the random matrix

and write . We may now state our main

result in its greatest generality.

Theorem 2.11

For large enough the following holds. Let be

arbitrary, and let be bounded continuous functions,

where is a function on . Then there exist and such that for all and we have

We conclude this section by drawing some consequences from

Theorem 2.11. In the GOE/GUE case, it is easy to see

that the law of the block matrix is asymptotically

Gaussian with covariance

In particular, we find that overlapping outliers repel each other

according to the usual random matrix level repulsion, while

nonoverlapping outliers are asymptotically independent.

In general outliers are not asymptotically independent, even if they do

not overlap. Such correlations arise from correlations between

different blocks of . There are two possible sources

for these correlations: the term in the

definition of , and the terms and

in the covariance (2.4) of the Gaussian matrix . Thus,

two outliers may be strongly correlated even if they are located on

opposite sides of the bulk spectrum.

3 Tools

The rest of this paper is devoted to the proofs of Theorems

2.5, 2.9 and 2.11.

Sections 3–8 are devoted to the proof

of Theorem 2.9; Theorem 2.5 is an

easy corollary of Theorem 2.9. Finally,

Theorem 2.11 is proved in Section 9 by

an extension of the arguments of

Sections 3–8.

We begin with a preliminary section that collects tools we shall use in

the proof. We introduce the spectral parameter

which will be used as the argument of Stieltjes transforms and

resolvents. In the following, we often use the notation and

without further comment. Let

denote the density of the local semicircle law, and

(25)

its Stieltjes transform. It is well known that the Stieltjes transform

satisfies the identity

(26)

It is easy to see that (26) and the definition

(7) imply

(27)

For , define

(28)

the distance from to the spectral edges . We have the simple

estimate

(29)

for . The following lemma collects some useful

properties

of .

Lemma 3.1

For , we have

(30)

Moreover,

(Here the implicit constants depend on .)

{pf}

The proof is an elementary calculation; see Lemma 4.2 in EYY2 .

The following definition introduces a notion of high probability that

is suitable for our needs.

Definition 3.2((High probability events)).

We say that an -dependent event holds with high

probability if there is some constant such that

(31)

for large enough .

Next, we give the key tool behind the proof of

Theorem 2.9: the Isotropic local semicircle

law. We use the notation for the components of a vector. We introduce the

standard scalar product . For , we define

the resolvent of through

The following result was proved in KY2 , Theorem 2.3.

Theorem 3.3((Isotropic local semicircle law outside of the spectrum))

Fix . There exists a

constant such that for large enough and any deterministic

we have with high probability

(32)

for all

Using (29) and Lemma 3.1, we find that the control

parameter in (32) may be written as

(33)

The following result provides sharp (up to logarithmic factors) large

deviations bounds on the locations of the outliers.

Theorem 3.4((Locations of the deformed eigenvalues))

There exists a constant such that, for large enough and under

condition (4), we have

(34)

with high probability provided that .

{pf}

This was essentially proved in KY2 , Theorem 2.7, by setting

there; see equation (2.20) of KY2 . Note that

Theorem 2.7 of KY2 has slightly stronger assumptions than

Theorem 3.4, requiring in addition that there be no

eigenvalues of satisfying . However, this assumption was only

needed for equation (2.21) of KY2 , and the proof from Section 6

of KY2 may be applied verbatim to (34) under

the assumptions of Theorem 3.4.

We shall often need to consider minors of , which are the content of

the following definition. It is a convenient extension of

Definition 2.2.

Definition 3.5((Minors and partial expectation)).

(i) For , we define

where . Moreover, we define the

resolvent of through

(ii) Set

When , we abbreviate by in the above

definitions; similarly, we write instead of .

(iii) For define the partial expectation

.

Next, we record some basic large deviations estimates from KY2 ,

Lemma 3.5.

Lemma 3.6((Large deviations estimates))

Let , be independent random

variables with zero mean and unit variance. Assume that there is a

constant such that

Then there exists a constant such

that, for any and any deterministic complex numbers and

, we have with high probability

(36)

(37)

(38)

We conclude this preliminary section by quoting a result on the

eigenvalue rigidity of . Denote by the classical locations of the eigenvalues of

, defined through

(39)

The following result was proved in EYY3 , Theorem 2.2.

Theorem 3.7((Rigidity of eigenvalues))

There exists a constant such that we have with high probability

for all .

4 Coarser grouping of outliers and reduction to the law of

For the following, we fix the sequences

and . It will sometimes be convenient to assume that

(40)

To that end, we invoke the following elementary result.

Lemma 4.1

Let be a sequence of nonnegative numbers and . The following statements are equivalent.

{longlist}[(ii)]

for large enough .

Each subsequence has a further subsequence along which .

We use Lemma 4.1 by setting to be the

left-hand side of (21). Using

Lemma 4.1, we therefore find that

Theorem 2.9 holds for arbitrary if it holds for

satisfying (40). From now on, we therefore assume without

loss of generality that (40) holds.

For the proof of Theorem 2.9, we need a new subset of

, denoted by , which is larger than or

equal to the subset from Definition 2.8.

Definition 4.2.

For satisfying (20), define

as the smallest subset of

with the two following properties.

{longlist}[(ii)]

.

If for we have and

(41)

then either or .

Here we use the notation .

Note that is a set of consecutive integers. Similar to

, the set indexes outliers that are close

to that indexed by , except that now the threshold used to

determine whether two outliers overlap is larger (

instead of the -independent ). This need to regroup outliers into

larger subsets arises from the perturbation theory argument in

Proposition 4.5 below. At the end of the proof,

in Section 8, we shall use perturbation theory a

second time to obtain a statement involving outliers in

instead of .

For the following, we introduce the abbreviation

so that (41) reads . We have the following elementary result.

Lemma 4.3

Let . If

and , then

For brevity, we fix satisfying (20), and

abbreviate and

when there is no risk of confusion.

The indices of and are separated in the following

sense.

Lemma 4.4

If and , then

(42)

If , then

(43)

{pf}

The bound (42) follows immediately from the

definition of . The bound (43) follows immediately

from Lemma 4.3 and the fact that is a set of at

most consecutive integers.

Since is diagonal, we may write

The matrix has dimensions and eigenvalues .

Define the region

(44)

From (20), (43) and Lemma 4.3

we get, for any , that

We therefore conclude that . For large enough a simple

estimate using the definition of and the bound

(34) yields for all

(45)

with high probability. In other words, houses with

high probability all of the outliers indexed by , and no other

eigenvalues of . Moreover, from

Theorem 3.7 we find that for large enough the

region contains with high probability no

eigenvalues of .

We may now state the main result of this section. Introduce the matrix

To shorten notation, for satisfying we often

abbreviate

Proposition 4.5

The following holds for large enough . Let

satisfy (20), and write . Then

for all we have

(46)

with high probability. [Recall Definitions 2.1 and

2.2 for the meaning of on the

left-hand side.]

{pf}

Our strategy for locating the outliers is based on the well-known fact

that is an eigenvalue of if and only

if has a zero eigenvalue (see, e.g., Lemma 6.1 of

KY2 ). Below, we develop a counting argument that finds the

eigenvalues of by analysing the behavior of each

eigenvalue of as varies. For our argument to work,

it is important that no two eigenvalues of

simultaneously cross the origin. [This condition is made precise in the

claim (4) below.] In order to rule out such coincidences, we

introduce additional randomness, by adding a small perturbation

, where has an absolutely continuous law.

The sole purpose of this perturbation is to exclude these coincidences

almost surely in the randomness of . This perturbation is

purely qualitative in the sense that may be

arbitrarily small; once the counting argument is concluded, we may

easily take and recover the claim for by a trivial continuity argument.

Thus, let be an Hermitian random matrix whose

upper-triangular entries are independent and have an absolutely

continuous law supported in the unit disc. Moreover, let be

independent of . Let . We shall prove the claim of

Proposition 4.5 for the matrix for small

enough (depending on ), instead of .

Define the matrix

(47)

From KY2 , Lemma 6.1, we get that is an

eigenvalue of if and only if

has a zero eigenvalue. Similar to

Proposition 7.1 in KY2 , we use perturbation theory to compare

the eigenvalues of with those of the block matrix

In order to apply perturbation theory, we must establish a lower bound

on the spectral gap

We find, for large enough and small enough (depending

on ), that with high probability

by Theorem 3.3, (29),

(33) and (20); in the second step we used

(42) and chose to be small enough

(depending on ); in the last step we chose to be large enough

(depending on ).

Next, Theorem 3.3, (29) and

(33) yield, with high probability,

(50)

for large enough and small enough (depending on ).

Define the regions

which are disjoint by (42). Using (49), we

find that for large enough and small enough

(depending on ) we have, with high probability,

Moreover, both and

have exactly eigenvalues in ; we denote these

eigenvalues by and , respectively.

We may now apply perturbation theory. Invoking

Proposition .1 using (4) and

(50) yields with high probability

(51)

for .

Next, we allow the argument of to vary in order

to locate the eigenvalues of . We recall

the following derivative bound from KY2 , Lemma 7.2: there is a

constant such that for large enough we have for all

-normalised , with high

probability,

(52)

(53)

By the definition (44) of , we find from

Lemma 4.3, (20) and (43) that

With these preliminary bounds, we may vary .

Let denote the continuous family of

eigenvalues of satisfying

for .

For the following argument, it is helpful to keep

Figure 2 in mind. We make the following claim:

()

We omit the details of the proof 666The claim (4)

reduces to the following statement. Let with and

be Hermitian matrices such that is deterministic and

depends smoothly on , and has an absolutely continuous law;

then, almost surely in , for all the matrix has at most one zero eigenvalue. Let denote the subset of

matrices with multiple eigenvalues at zero, so that is an algebraic

variety of codimension two. The claim therefore reduces to the

statement that the path almost surely

does not intersect , which is standard. of (4). Note

that the necessity for (4) to hold is the only reason we had

to introduce the additional randomness into .

Figure 2: The spectrum of for . For definiteness, we chose . The

region is delimited by dotted lines. The

eigenvalues of are labelled by black dots on the

-axis.

For definiteness, suppose for the following that . We claim

that for all we have with high probability

(18)

where denote the endpoints of the interval . Let us focus on the first estimate; the second one is proved

similarly. Let . Since

is increasing, we find that the left endpoint of is . From (56) and

Lemma .2, we find with high probability

in the second step we used ; the third step

holds for large enough and small enough (depending on

), by Lemma 4.3; the last step follows from (27). This concludes the proof of (18).

Recall that has with high probability

exactly eigenvalues in .

By continuity of the property (4) and

(18), we therefore get that the function intersects

each function , , exactly once in

. Let and denote by

the unique point (with high probability) in at

which .

From the definition of and (57) we get, with

high probability,

where in the second step we used (54), the fact that

, and the elementary bound

. [Recall

that by definition .]

Now we may use (51) and (4) to get

(20)

with high probability. Now we expand the left-hand side using the identity

(21)

which follows easily from (26); in the second step we

used Lemma 3.1. Differentiating again, we get . From (55), we therefore get

with high probability. Solving from

(4) and from (20), we

find for large enough with high probability

in the first step we estimated the error terms using by (21) and

(55); in the second step we used (20);

the last step follows by choosing large enough. Thus, we conclude

that

with high probability for small enough (depending on

). Taking completes the proof.

We conclude this section with a remark on the choice of the reference

point in Proposition 4.5. By

definition of , if then . Obviously, the distribution of the overlapping group of

outliers cannot depend on the

particular choice of . Nevertheless, the reference

matrix in

(46) depends explicitly on via

. This is not a contradiction, however, since a

different choice of leads to a reference matrix which only

differs from the original one by an error term of order ; this

difference may be absorbed into the error term on the right-hand side

of (46). We shall need this fact in

Section 9. The precise statement is as follows. (To

simplify notation, we state it without loss of generality for the case

.)

Lemma 4.6

Suppose that and that . Let

Then for large enough we have

where we abbreviated and .

{pf}

We write

with high probability; in the second step we wrote

and used (57) and Lemma 4.3, as well as

Theorem 3.3, (33),

(29), (21), and the fact that ; in the third step we used (7),

(27), and the assumption that is large enough; in the

last step we used that .

5 The Gaussian case

Suppose that satisfies (20). By

Proposition 4.5, in order to analyse the joint

distribution of the outliers with

, it suffices to analyse the distribution of

the eigenvalues of the matrix . In this section, we do

this under the assumption that the entries of are Gaussian, that

is, that is a GOE/GUE matrix.

Recall that may depend on . To simplify notation, in

Sections 5–7 we take , which allows us to drop subscripts and avoid minor

nuisances arising from the fact that may depend on . In

fact, this special case will easily imply the case of general ;

see Section 8.

The following definition is a convenient shorthand for the equivalence

relation defined by two random matrices of fixed size having the same

asymptotic distribution.

Definition 5.1.

For two sequences and of random matrices,

where is fixed, we write if

for all continuous and bounded .

Let be an GOE/GUE matrix

multiplied by . In other words, the covariances of are

given by

(23)

where was defined in (12). The following

proposition is the main result of this section. It provides the joint

distribution of the eigenvalues of , which, by

Proposition 4.5, immediately yields the

distribution of the -group of outliers under the assumption

that is a GOE/GUE matrix. However, since we are ultimately

interested in non-Gaussian , we shall not combine it

Proposition 4.5 directly, but instead use it as

an input for the more general case covered in Section 6.

Proposition 5.2

The following holds for large enough . Let

for some satisfying . Suppose moreover that is a GOE/GUE matrix. Then

{pf}

Throughout the proof, we drop the spectral parameter from

quantities such as . By unitary invariance of , we may

assume that , that is, is the

th standard basis vector of . By Schur’s complement

formula, we therefore get where

is the Hermitian matrix defined by

We now claim that

(24)

Bearing later applications in mind, we in fact prove, for any , that

(25)

with high probability. Applying (25) with to the minor

immediately yields (24). In order

to prove (25), we use Theorem 3.7 to get with

high probability

(26)

in the first step we estimated the contribution of by the

contribution of , and used that with high probability by

Theorem 3.7 and the assumption on (for large

enough ); in the second step we used the estimate

(27)

for , as follows from the definition of

. Similarly, setting , we find

with high probability. Indeed, using Lemma 3.6 we get

with high probability. In the last step we used (25), (4), and to get (dropping the upper indices to

simplify notation)

with high probability.

Using the bounds (29) and with high probability [as follows from

(3)], we may expand with (26) to get

with high probability. Let

denote the upper

block of . Thus we get

with high probability. In particular, for large enough we get

(31)

By definition, and are independent. What

therefore remains is to compute the asymptotic distribution of . We

claim that converges in law to an Gaussian matrix:

(32)

By the Cramér–Wold device, it suffices to show that

for any deterministic matrix satisfying and

if . To that end, we diagonalize

by writing

where is a unitary matrix and . Moreover, we

introduce the matrix . Since the entries of are i.i.d. Gaussians, is

orthogonal/unitary, and is independent of , we find

that . We conclude that

Note that is a family of i.i.d. random variables,

independent of , with variance .

Therefore,

with high probability for large enough , where we used (25).

Moreover, we have

with high probability for large enough , where in the second step we

used (25) and in the third step the estimate as follows by differentiating (21)

twice and from Lemma 3.1.

We conclude from the central limit theorem that

where we used the identity

as follows from (21) and (27). Thus,

(32) follows the identity

as follows from a from a simple variance calculation.

The next step of the proof is to consider the case where most entries

of are Gaussian. The exponent is used to define a

cutoff scale in the entries of , below which the corresponding

entries of are assumed to be Gaussian.

Proposition 6.1 will ultimately be fed into

Lemma 7.1 below, at which time we

shall choose to be large enough.

Proposition 6.1

The following holds for large enough . Let

for some satisfying . Let

. Suppose that the Wigner matrix satisfies

(33)

Then

where is a Gaussian matrix, independent of ,

with centred entries and covariance

{pf}

Throughout the proof, we drop the spectral parameter from

our notation.

{longlist}[Step 2.]

We start with some linear algebra in order to

write the matrix in a form amenable to analysis. Since for all we find that

We shall permute the rows of by using an permutation

matrix according to . It is

easy to see that we may permute the rows of by setting so that after the permutation we have

where:

{longlist}[(iii)]

is a matrix and an matrix,

for all

and ,

.

After the permutation , we may write as

where is a matrix, an

matrix, and an matrix with Gaussian

entries [as follows from (33)].

Next, we rotate the rows of by choosing a unitary matrix such that

where is an matrix that satisfies

(34)

Thus, we get

where denotes equality in distribution. Here we used the

unitary invariance of the Gaussian matrix .

Next, we decompose

where is an Gaussian matrix, an Gaussian matrix, and an Gaussian matrix. Moreover, is an matrix

and we have

Thus, we find

where

Here is a matrix satisfying ,

and is an matrix.

We claim that

(35)

with high probability (in the sense of matrix entries). In order to

prove (35), we write

and consider each block separately. For , we get using

(38)

with high probability. Similarly, (36) and

(37) yield

with high probability, where we used that . Next, from (36), (37) and

(38) we easily get

with high probability. This concludes the proof of (35).

Next, we define

and claim that

(37)

with high probability (in the sense of matrix entries). Since is an

GOE/GUE matrix that is independent of , (37) follows from

Theorem 3.3, (29),

(33) and (35).

For the following, we use the letter to denote any (random) error term satisfying with

high probability for some constant . We apply Schur’s complement

formula to get

where in the second step we expanded using (26) and

estimated the error term using (37), , and

with high

probability. Using , we get

Next, we rewrite the term so as to decouple the

randomness of from that of . From (35), we find

(38)

with high probability. Define the deterministic matrix

Next, we claim that there is a unitary matrix , which is -measurable, such that

(39)

with high probability. In order to prove (39), write

. Then (38) simply

states that the vectors form a

basis of an -dimensional subspace, which is orthonormal up to errors

of order with high probability. More precisely, we

choose a unitary matrix such that lies in the

direction of . Hence, by (38), we have with high probability. Note moreover that by

(38) we have with high probability for . Next, we

choose a unitary matrix that leaves invariant and

maximizes .

Hence, again by (38), we have with high probability. We continue in this

manner, at the th step choosing a unitary matrix that leaves

invariant and maximizes

. Finally,

we define . By construction, the estimate in

(39) holds. Moreover, since is deterministic, is

clearly -measurable. This concludes the proof of (39).

Using Theorem 3.3 and the fact that and

are independent, we therefore get from (39)

We conclude that

where we used that and that all

terms apart from are independent of .

Next, we compute

with high probability, where in the last step we used

Lemma 3.6 and. Using (34), we

rewrite

where we introduced the notation .

Thus, we conclude that

(40)

where

By definition, the random variables , ,

and are independent.

We compute the asymptotics of ,

, and . We begin with . We shall

apply Proposition 5.2 to the Gaussian matrix . Thus, in

Proposition 5.2 we replace with , with , and

by with . Since we find that . We therefore

conclude from Proposition 5.2 that

Here we used (27). Recall that is the rescaled GOE/GUE

matrix satisfying (23).

In order to deal with , we introduce, in analogy to

, the matrix whose entries are

defined by . In particular, since , we have

. Writing , we get

Next, we define the matrices

Note that, by definition, , and are independent. We now compute the covariances of the

matrices and . A simple calculation yields

where we defined

For example, let us prove the second identity for the case .

Using we find

The other cases are handled similarly. Moreover, since by definition we

have , the

central limit theorem implies that and converge to a Gaussian random matrix. Hence, the asymptotics of

and are governed entirely by their covariances

(6).

Similarly, is Gaussian with covariance

where we used (27). Using , we therefore conclude that

(42)

where is Gaussian with covariance

(43)

Next, we compute the asymptotics of

. We shall prove that is asymptotically Gaussian, and compute its covariance

matrix.

with high probability. Define the deterministic matrix

Exactly as after (6) we find that (6) and Gaussian

elimination imply that there is a unitary matrix , which is -measurable, such that

with high probability. Thus, we get

with high probability. Using that is independent of and ,

we therefore find

Defining the matrix

we therefore have

where

By definition, and are independent. Recalling

that , we find from the central

limit theorem that and are

each asymptotically Gaussian. Hence, it suffices to compute their

covariances. A straightforward computation yields

where we defined

[By a slight abuse of notation, we write by

identifying with the vector .]

We may now consider the sum . From (40), (42), (6), (6), and the definition of ,

we get

where is a Gaussian matrix, independent of ,

with covariance

Here we used that

as follows from the bilinearity of

as well as the identities , and .

Using that is a matrix with and , we easily

find that

Since , it is not hard to see that the errors on the

right-hand side of (6) are bounded from above (in the

sense of matrices) by the matrix . In particular, from (6) we get that the

matrix

is nonnegative, from which we conclude that the right-hand side of

(2.3) is nonnegative. This completes the proof. ∎\noqed

7 The general case

The general case follows from Proposition 6.1 and

Green function comparison. The argument is almost identical to that of

Section 7.4 in KY2 , and we only sketch the differences.

Let be an arbitrary real symmetric/complex

Hermitian Wigner matrix and a GOE/GUE matrix

independent of . For , define the subset

Define a new Wigner matrix

through

Thus, satisfies the assumptions of

Proposition 6.1. Let

Choose a bijective map . For denote

by the Hermitian matrix defined by

In particular, and . Let now satisfy . We write

and

Here denotes the matrix with entries . Hence we have , and the

matrices and differ only in the entries

and .

Next, we introduce the resolvents

Let . Set (as in KY2 , Section 7.4, we add a small

imaginary part to to ensure weak control on low-probability events)

and define

(47)

The quantities and are defined analogously with

replaced by and , respectively.

The following estimate is the main comparison estimate. It is very

similar to Lemma 7.13 of KY2 .

Lemma 7.1

Provided is a large enough constant, the following holds. Let be bounded with bounded derivatives

and be an arbitrary deterministic sequence of

matrices. Then

(49)

where satisfies ,

and

(50)

{pf}

The proof follows the proof of Lemma 7.13 of KY2 with cosmetic

modifications whose details we omit.

Using Lemma 7.1, we may now complete

the proof in the general case. The following proposition is the main

result of this section, and is the conclusion of the arguments from

Sections 5–7.

Proposition 7.2

The following holds for large enough . Let

for some satisfying . Then

where is the Gaussian matrix from

Proposition 6.1.

{pf}

The proof follows the proof of Theorem 2.14 in Section 7.4 of

KY2 with cosmetic modifications whose details we omit. The main

inputs are Proposition 6.1 and

Lemma 7.1. The imaginary part of the

spectral parameter is easily removed using

the estimate . The condition in

Lemma 7.1 can be relaxed to

by standard properties of weak convergence of measures.

We may now conclude the proof of Theorems 2.5 and

2.9. First, we note that Theorem 2.5

is an easy corollary of Theorem 2.9. We focus therefore

on the proof of Theorem 2.9.

Fix to be the constant from

Proposition 7.2. Fix

and define the subset

We assume that is a subsequence (i.e., infinite), for

otherwise the claim of Theorem 2.9 is vacuous. For

given , we introduce the partition

(51)

where the union ranges over subsets of satisfying , and

where and are the subsets from Definitions 2.8 and

4.2.

We shall prove the following result.

Proposition 8.1

Fix , and satisfying . Let be given, and let be bounded continuous functions, where is a function

on satisfying . Then

there exist constants and , both depending on

and , such that (21) holds for all and all satisfying .

Before proving Proposition 8.1, we note that it

immediately implies Theorem 2.9, since the partition

(51) ranges over a finite family containing

elements.

{pf*}

Proof of Proposition 8.1

From (45), we know that

contains with high probability precisely

outliers, namely . Following

(16), for we introduce the rescaled

eigenvalues

In order to identify the asymptotics of , we introduce the

matrices

Note that is random and deterministic. From

(46), (27) and (21), we get for

all that

(52)

with high probability. By Proposition 7.2 and

Remark 2.3, the family is tight.

We shall apply perturbation theory to the matrix . In order to do

so, we truncate by defining for . Then by tightness of there exists a such that

(54)

for all . For the truncated matrices, we find the spectral gap

where the constant only depends on in

(4); here in the last step we used (53). Proposition .1 therefore yields

(55)

We conclude that for there exists an and an , both depending

on and , such that for and satisfying we have

where in the first step we used (54), in the second

step (55) and dominated convergence, in the third

step (54) again, and in the last step

(52) and dominated convergence.

Proposition 8.1 now follows from

Proposition 7.2 applied to the matrix

In this final section, we extend the arguments of

Sections 4–8 to cover the joint

distribution of all outliers, and hence prove

Theorem 2.11.

We begin by introducing a coarser partition , defined

analogously to from Definition 2.10, except that

is replaced with from

Definition 4.2.

Definition 9.1.

Let and be given, and fix . We introduce a

partition777As in the footnote to Definition 2.10, it is

easy to see that is a partition.

on a subset of , defined as

We also use the notation .

It is immediate from Definitions 2.10 and 9.1

that and that for each

there is a (unique) such that

. In analogy to (22), we set for

definiteness

Note that for we have

(56)

The following result follows from

Proposition 4.5 and (21).

Proposition 9.2

The following holds for large enough . For any

and we have

(57)

with high probability.

As in Section 8, we may assume without loss of

generality that the partitions and are independent of

. [Otherwise partition

Since the union is over a finite family of subsets of , we may first fix and and then restrict ourselves

to .] As in the proof of

Proposition 8.1, we define for each the

matrix

The joint distribution of is described by the

following result, which is analogous to

Proposition 7.2.

We postpone the proof of Proposition 9.3 to

the next section, and finish the proof of Theorem 2.11

first. In order to identify the location of , we invoke

Proposition 9.2 and make use of the freedom

provided by Lemma 4.6 in order to change the

reference point at will. Thus,

Proposition 9.2 and

Lemma 4.6 yield, for any , ,

and containing , that

with high probability, where we used (21), (56)

and Lemma .2.

Next, for let denote the unique element of

that contains . For each , we introduce the

matrices

with high probability. By Proposition 7.2 and

Remark 2.3, is tight (in ). We

may now repeat verbatim the truncation and perturbation theory argument

from the proof of Proposition 8.1, following

(53). The conclusion is that there exists an and an

, both depending on and , such that for and we have

The claim now follows from Proposition 9.3

and the observation that. This

concludes the proof of Theorem 2.11.

What remains is to prove Proposition 9.3.

Clearly, it is a generalization of

Proposition 7.2. The proof of

Proposition 9.3 relies on the same

three-step strategy as that of

Proposition 7.2: the Gaussian case, the

almost Gaussian case and the general case.

We begin with the Gaussian case (generalization of

Section 5).

Proposition 9.4

Suppose that is a GOE/GUE matrix. Then for large enough we have

here is a family of independent Gaussian

matrices, where each is a matrix whose covariance is given by

(23).

{pf}

The proof is a straightforward extension of that of

Proposition 5.2, and we only indicate the

changes. For each argument , we use Schur’s complement

formula on the whole block . Thus, instead of

(5), we get

This gives

(60)

which is the appropriate generalization of (31). By definition,

is independent of the family of matrices

, and the submatrices , , are obviously independent. We may now repeat verbatim the

proof of (32) to get

Next, we consider the almost Gaussian case (generalization of

Section 6).

Proposition 9.5

Let . Suppose that the Wigner matrix satisfies

(62)

Define to be the matrix without the

shift arising from , that is, with

Then for large enough we have

(63)

{pf}

We start exactly as in the proof of

Proposition 6.1. We repeat the steps up to

(40) verbatim on the family of matrices , whereby all of the

reduction operations are performed simultaneously on each matrix

. Note that these matrices only differ

in the argument ; hence all steps of the reduction (and in

particular the quantities , , , , , ,

, , , , etc.) are the same for all matrices

. We take over the notation from the

proof of Proposition 6.1 without further comment.

Thus, we are led to the following generalization of (40):

(64)

where

(We deviate somewhat from the convention of Section 6 in

that, unlike there, we include the normalization factor, which depends

on , in the definition of the variables .) By definition,

the random matrices , , ,

and are independent. They are all block diagonal, and we

sometimes use the notation , etc., for their blocks. What remains is to identify

their individual asymptotic distributions.

The matrix is is easy: from

Proposition 9.4 we immediately get

where is defined as in

Proposition 9.4. The matrix is

dealt with in the same way as in the proof of

Proposition 6.1; we omit the details. By

definition, is Gaussian with mean zero. A short computation

yields the covariance

for , and . We may therefore

conclude that, similar to (42) and (6), we have

(65)

where is a block diagonal Gaussian

matrix with mean zero and covariance

for , and .

Next, we deal with and . By the central limit

theorem and the definition of , as in the proof of

Proposition 6.1, both of these matrices are

asymptotically Gaussian (with mean zero). The variances may be computed

along the same lines as in the proof of

Proposition 6.1. The result is, for , , , and , ,

as well as

Putting everything together, we get

(67)

where is a Gaussian block diagonal

matrix with mean zero that is independent of , and whose

covariance is given by

Similar to (6), we find using the definition of

and that the two last lines are asymptotic to . Thus,

we get

(68)

This concludes the proof.

In order to conclude the proof of

Proposition 9.3, we finally consider the

general case (generalization of Section 7). As in

Proposition 7.2, in the general case we get a

deterministic shift , where

(69)

The proof is similar to those of

Lemma 7.1 and

Proposition 7.2. We take over the setup and

notation from Section 7 up to, but not including,

(47). For each , we define the spectral

parameter and the matrix

(70)

we well as the

block diagonal matrix . The

quantities and are defined analogously with replaced by

and , respectively. The following is the main comparison

estimate, which generalizes

Lemma 7.1.

Lemma 9.6

Provided is a large enough constant, the following holds. Let be bounded with bounded derivatives and be

an arbitrary deterministic sequence of matrices. Then

(72)

where satisfies ,

the error term is defined in (50), and

is the block diagonal matrix

with blocks

(73)

{pf}

The proof of Lemma 7.1 may be taken

over almost verbatim, following the proof of Lemma 7.13 of KY2 .

The comparison estimate from

Lemma 9.6 yields the shift described

by . The precise statement is given by the following

proposition, which generalizes

Proposition 7.2.

Replacing with for , we conclude that for we have the equivalence

where

Moreover, from Lemma .2 below we find that

contains exactly eigenvalues of , for all . It is well known that the eigenvalues of are continuous in . We now claim that each such continuous

is in fact Lipschitz continuous with Lipschitz constant

Assuming this is proved, the claim immediately follows from .

In order to prove the Lipschitz continuity of , note that

is an eigenvalue of the matrix

Then the Lipschitz continuity of follows readily from

Lemma .2 below and the estimate

as follows from (2), the fact that for all , and the fact that is

Hermitian.

Lemma .2

Let and be square matrices, with Hermitian. Then the

spectrum of is contained in the closed -neighborhood

of the spectrum of .

{pf}

Using the identity we conclude that if then .

References

(1){barticle}[mr]

\bauthor\bsnmBaik, \bfnmJinho\binitsJ.,

\bauthor\bsnmBen Arous, \bfnmGérard\binitsG. and \bauthor\bsnmPéché, \bfnmSandrine\binitsS.

(\byear2005).

\btitlePhase transition of the largest eigenvalue for nonnull complex sample

covariance matrices.

\bjournalAnn. Probab.

\bvolume33

\bpages1643–1697.

\biddoi=10.1214/009117905000000233, issn=0091-1798, mr=2165575

\bptokimsref

\endbibitem

(2){barticle}[mr]

\bauthor\bsnmBenaych-Georges, \bfnmF.\binitsF.,

\bauthor\bsnmGuionnet, \bfnmA.\binitsA. and \bauthor\bsnmMaida, \bfnmM.\binitsM.

(\byear2011).

\btitleFluctuations of the extreme eigenvalues of finite rank deformations of

random matrices.

\bjournalElectron. J. Probab.

\bvolume16

\bpages1621–1662.

\biddoi=10.1214/EJP.v16-929, issn=1083-6489, mr=2835249

\bptokimsref

\endbibitem

(3){barticle}[mr]

\bauthor\bsnmBenaych-Georges, \bfnmF.\binitsF.,

\bauthor\bsnmGuionnet, \bfnmA.\binitsA. and \bauthor\bsnmMaida, \bfnmM.\binitsM.

(\byear2012).

\btitleLarge deviations of the extreme eigenvalues of random deformations of

matrices.

\bjournalProbab. Theory Related Fields

\bvolume154

\bpages703–751.

\biddoi=10.1007/s00440-011-0382-3, issn=0178-8051, mr=3000560

\bptnotecheck year\bptokimsref

\endbibitem

(4){barticle}[mr]

\bauthor\bsnmBenaych-Georges, \bfnmFlorent\binitsF. and \bauthor\bsnmNadakuditi, \bfnmRaj Rao\binitsR. R.

(\byear2011).

\btitleThe eigenvalues and eigenvectors of finite, low rank perturbations of

large random matrices.

\bjournalAdv. Math.

\bvolume227

\bpages494–521.

\biddoi=10.1016/j.aim.2011.02.007, issn=0001-8708, mr=2782201

\bptokimsref

\endbibitem

(5){bmisc}[author]

\bauthor\bsnmBloemendal, \bfnmAlexander\binitsA.

(\byear2011).

\bhowpublishedFinite rank perturbations of random matrices and their

continuum limits. Ph.D. thesis, Univ. Toronto, Canada.

\bptokimsref

\endbibitem

(6){barticle}[mr]

\bauthor\bsnmBloemendal, \bfnmAlex\binitsA. and \bauthor\bsnmVirág, \bfnmBálint\binitsB.

(\byear2013).

\btitleLimits of spiked random matrices I.

\bjournalProbab. Theory Related Fields

\bvolume156

\bpages795–825.

\biddoi=10.1007/s00440-012-0443-2, issn=0178-8051, mr=3078286

\bptnotecheck year\bptokimsref

\endbibitem

(7){bmisc}[auto:STB—2013/10/14—10:36:11]

\bauthor\bsnmBloemendal, \bfnmAlex\binitsA. and \bauthor\bsnmVirág, \bfnmBálint\binitsB.

(\byear2013).

\bhowpublishedLimits of spiked random matrices II.

Preprint. Available at arXiv:\arxivurl1109.3704.

\bptokimsref

\endbibitem

(8){barticle}[mr]

\bauthor\bsnmCapitaine, \bfnmMireille\binitsM.,

\bauthor\bsnmDonati-Martin, \bfnmCatherine\binitsC. and \bauthor\bsnmFéral, \bfnmDelphine\binitsD.

(\byear2009).

\btitleThe largest eigenvalues of finite rank deformation of large Wigner

matrices: Convergence and nonuniversality of the fluctuations.

\bjournalAnn. Probab.

\bvolume37

\bpages1–47.

\biddoi=10.1214/08-AOP394, issn=0091-1798, mr=2489158

\bptokimsref

\endbibitem

(9){barticle}[mr]

\bauthor\bsnmCapitaine, \bfnmM.\binitsM.,

\bauthor\bsnmDonati-Martin, \bfnmC.\binitsC. and \bauthor\bsnmFéral, \bfnmD.\binitsD.

(\byear2012).

\btitleCentral limit theorems for eigenvalues of deformations of Wigner

matrices.

\bjournalAnn. Inst. Henri Poincaré Probab. Stat.

\bvolume48

\bpages107–133.

\biddoi=10.1214/10-AIHP410, issn=0246-0203, mr=2919200

\bptnotecheck year\bptokimsref

\endbibitem

(10){bmisc}[auto:STB—2013/10/14—10:36:11]

\bauthor\bsnmCapitaine, \bfnmM.\binitsM.,

\bauthor\bsnmDonati-Martin, \bfnmC.\binitsC.,

\bauthor\bsnmFéral, \bfnmD.\binitsD. and \bauthor\bsnmFévrier, \bfnmM.\binitsM.

\bhowpublishedFree convolution with a semi-circular

distribution and eigenvalues of spiked deformations of Wigner matrices.

Preprint. Available at arXiv:\arxivurl1006.3684.

\bptokimsref

\endbibitem

(11){barticle}[mr]

\bauthor\bsnmErdős, \bfnmLászló\binitsL.,

\bauthor\bsnmKnowles, \bfnmAntti\binitsA.,

\bauthor\bsnmYau, \bfnmHorng-Tzer\binitsH.-T. and \bauthor\bsnmYin, \bfnmJun\binitsJ.

(\byear2012).

\btitleSpectral statistics of Erdős–Rényi grraphs II:

Eigenvalue spacing and the extreme eigenvalues.

\bjournalComm. Math. Phys.

\bvolume314

\bpages587–640.

\biddoi=10.1007/s00220-012-1527-7, issn=0010-3616, mr=2964770

\bptnotecheck year\bptokimsref

\endbibitem

(12){barticle}[mr]

\bauthor\bsnmErdős, \bfnmLászló\binitsL.,

\bauthor\bsnmKnowles, \bfnmAntti\binitsA.,

\bauthor\bsnmYau, \bfnmHorng-Tzer\binitsH.-T. and \bauthor\bsnmYin, \bfnmJun\binitsJ.

(\byear2013).

\btitleSpectral statistics of Erdős–Rényi graphs I: Local

semicircle law.

\bjournalAnn. Probab.

\bvolume41

\bpages2279–2375.

\biddoi=10.1214/11-AOP734, issn=0091-1798, mr=3098073

\bptnotecheck year\bptokimsref

\endbibitem

(13){barticle}[mr]

\bauthor\bsnmErdős, \bfnmLászló\binitsL.,

\bauthor\bsnmPéché, \bfnmSandrine\binitsS.,

\bauthor\bsnmRamírez, \bfnmJosé A.\binitsJ. A.,

\bauthor\bsnmSchlein, \bfnmBenjamin\binitsB. and \bauthor\bsnmYau, \bfnmHorng-Tzer\binitsH.-T.

(\byear2010).

\btitleBulk universality for Wigner matrices.

\bjournalComm. Pure Appl. Math.

\bvolume63

\bpages895–925.

\biddoi=10.1002/cpa.20317, issn=0010-3640, mr=2662426

\bptokimsref

\endbibitem

(14){barticle}[mr]

\bauthor\bsnmErdős, \bfnmLászló\binitsL.,

\bauthor\bsnmSchlein, \bfnmBenjamin\binitsB. and \bauthor\bsnmYau, \bfnmHorng-Tzer\binitsH.-T.

(\byear2009).

\btitleSemicircle law on short scales and delocalization of eigenvectors for

Wigner random matrices.

\bjournalAnn. Probab.

\bvolume37

\bpages815–852.

\biddoi=10.1214/08-AOP421, issn=0091-1798, mr=2537522

\bptokimsref

\endbibitem

(15){barticle}[mr]

\bauthor\bsnmErdős, \bfnmLászló\binitsL.,

\bauthor\bsnmSchlein, \bfnmBenjamin\binitsB. and \bauthor\bsnmYau, \bfnmHorng-Tzer\binitsH.-T.

(\byear2010).

\btitleWegner estimate and level repulsion for Wigner random matrices.

\bjournalInt. Math. Res. Not. IMRN

\bvolume3

\bpages436–479.

\biddoi=10.1093/imrn/rnp136, issn=1073-7928, mr=2587574

\bptokimsref

\endbibitem

(16){barticle}[mr]

\bauthor\bsnmErdős, \bfnmLászló\binitsL.,

\bauthor\bsnmSchlein, \bfnmBenjamin\binitsB. and \bauthor\bsnmYau, \bfnmHorng-Tzer\binitsH.-T.

(\byear2011).

\btitleUniversality of random matrices and local relaxation flow.

\bjournalInvent. Math.

\bvolume185

\bpages75–119.

\biddoi=10.1007/s00222-010-0302-7, issn=0020-9910, mr=2810797

\bptokimsref

\endbibitem

(17){barticle}[mr]

\bauthor\bsnmErdős, \bfnmLászló\binitsL.,

\bauthor\bsnmYau, \bfnmHorng-Tzer\binitsH.-T. and \bauthor\bsnmYin, \bfnmJun\binitsJ.

(\byear2011).

\btitleUniversality for generalized Wigner matrices with Bernoulli

distribution.

\bjournalJ. Comb.

\bvolume2

\bpages15–81.

\biddoi=10.4310/JOC.2011.v2.n1.a2, issn=2156-3527, mr=2847916

\bptokimsref

\endbibitem

(18){barticle}[mr]

\bauthor\bsnmErdős, \bfnmLászló\binitsL.,

\bauthor\bsnmYau, \bfnmHorng-Tzer\binitsH.-T. and \bauthor\bsnmYin, \bfnmJun\binitsJ.

(\byear2012).

\btitleRigidity of eigenvalues of generalized Wigner matrices.

\bjournalAdv. Math.

\bvolume229

\bpages1435–1515.

\biddoi=10.1016/j.aim.2011.12.010, issn=0001-8708, mr=2871147

\bptnotecheck year\bptokimsref

\endbibitem

(19){barticle}[mr]

\bauthor\bsnmFéral, \bfnmDelphine\binitsD. and \bauthor\bsnmPéché, \bfnmSandrine\binitsS.

(\byear2007).

\btitleThe largest eigenvalue of rank one deformation of large Wigner

matrices.

\bjournalComm. Math. Phys.

\bvolume272

\bpages185–228.

\biddoi=10.1007/s00220-007-0209-3, issn=0010-3616, mr=2291807

\bptokimsref

\endbibitem

(20){barticle}[mr]

\bauthor\bsnmFüredi, \bfnmZ.\binitsZ. and \bauthor\bsnmKomlós, \bfnmJ.\binitsJ.

(\byear1981).

\btitleThe eigenvalues of random symmetric matrices.

\bjournalCombinatorica

\bvolume1

\bpages233–241.

\biddoi=10.1007/BF02579329, issn=0209-9683, mr=0637828

\bptokimsref

\endbibitem

(21){bmisc}[auto:STB—2013/10/14—10:36:11]

\bauthor\bsnmKnowles, \bfnmA.\binitsA. and \bauthor\bsnmYin, \bfnmJ.\binitsJ.

\bhowpublishedThe isotropic semicircle law and deformation of Wigner

matrices. Preprint. Available at

arXiv:\arxivurl1110.6449. Comm. Pure Appl. Math. To appear.

\bptokimsref

\endbibitem

(22){bmisc}[auto:STB—2013/10/14—10:36:11]

\bauthor\bsnmLee, \bfnmJ. O.\binitsJ. O. and \bauthor\bsnmYin, \bfnmJ.\binitsJ.

\bhowpublishedA necessary and sufficient condition for edge

universality of Wigner matrices, Preprint. Available at

arXiv:\arxivurl1206.2251.

\bptokimsref

\endbibitem

(23){barticle}[mr]

\bauthor\bsnmPéché, \bfnmS.\binitsS.

(\byear2006).