Predicting the time at which a Lévy process attains its ultimate supremum

Abstract

We consider the problem of finding a stopping time that minimises the -distance to , the time at which a Lévy process attains its ultimate supremum. This problem was studied in [13] for a Brownian motion with drift and a finite time horizon. We consider a general Lévy process and an infinite time horizon (only compound Poisson processes are excluded. Furthermore due to the infinite horizon the problem is interesting only when the Lévy process drifts to ). Existing results allow us to rewrite the problem as a classic optimal stopping problem, i.e. with an adapted payoff process. We show the following. If has infinite mean there exists no stopping time with a finite -distance to , whereas if has finite mean it is either optimal to stop immediately or to stop when the process reflected in its supremum exceeds a positive level, depending on whether the median of the law of the ultimate supremum equals zero or is positive. Furthermore, pasting properties are derived. Finally, the result is made more explicit in terms of scale functions in the case when the Lévy process has no positive jumps.

Keywords: Lévy processes, optimal prediction, optimal stopping.

Mathematics Subject Classification (2000): 60G40, 62M20

1 Introduction

This paper addresses the question of how to predict the time a Lévy process attains its ultimate supremum with an infinite time horizon. (Due to the jumps a Lévy process can experience, the word “attains” is used here in a slightly broader sense than when the driving process is continuous, cf. Section 3). That is, we aim to find a stopping time that is closest (in sense) to the time the Lévy process attains its ultimate supremum. This is an example of an optimal prediction problem. It is related to classic and well-studied optimal stopping problems. However, the key difference is that the payoff process is not adapted to the filtration generated by the driving stochastic process. Indeed, in our case, the time the Lévy process attains its ultimate supremum is not known (with absolute certainty) at any (finite) time . However, as time progresses, more information about the time of the ultimate supremum becomes available. Examples of optimal prediction problems where this is not the case include the “hidden target” type problems studied in [29].

In recent years optimal prediction problems have received considerable attention, see e.g. [18, 11, 13, 32, 29, 2, 17, 4, 14, 16, 12]. One reason is that such problems have found applications in fields such as engineering, finance and medicine. Prominent examples concern the optimal time to sell an asset (in finance) or the optimal time to administer a drug (in medicine).

The papers referred to above are mainly concerned with optimal prediction problems driven by Brownian motion (with drift), particularly with a finite time horizon. Some exceptions are [2] which deals with random walks, [16] with mean-reverting diffusions and [4] which deals with spectrally positive stable processes. The same problem as we consider was studied in [13], however for a Brownian motion with drift and a finite time horizon. In that paper it is also postulated that for a general Lévy process the structure of the solution is the same as they found for the Brownian motion with drift. See also Remark 10.

In this paper, the driving process is a general Lévy process drifting to , i.e. a.s. (otherwise the problem we consider is trivial as we will briefly point out in the sequel). We are interested in solving

| (1.1) |

where is the time attains its ultimate supremum (cf. Section 3 for details) and the infimum is taken over all stopping times with respect to the filtration generated by . Following [13, 32], due to the stationarity and independence of the increments of , (1.1) can be expressed as an optimal stopping problem driven by the reflected process given by for all , where denotes the running supremum of . This allows us to show the following. If has infinite mean then (1.1) is degenerate in the sense that it equals . Now suppose has finite mean. If the law of the ultimate supremum has an atom in of size at least then is optimal in (1.1). Otherwise, the infimum in (1.1) is attained by the first time enters an interval for some strictly larger than the median of the law of . We derive pasting properties and in the special case that is spectrally negative we obtain (semi-)explicit expressions for (1.1) and in terms of so-called scale functions.

Note that the problem (1.1) with a finite time horizon (rather than an infinite time horizon as we consider) is potentially more interesting from the point of view of applications. However, it is also considerably more challenging than the infinite horizon case. As motivated in [13] (cf. also Remark 10) it should be expected that in the finite horizon case the optimal stopping time is of the form the first time that the reflected process exceeds some time-dependent curve. For a Brownian motion with drift as considered in [13], this curve is specified only implicitly as the solution to a nonlinear integral equation. Their proof relies on first reducing the optimal prediction problem to an optimal stopping problem (also with a finite horizon, cf. their Lemma 2), which is then solved by the well-known technique of representing the value function of the optimal stopping problem and the time-dependent curve determining the optimal stopping time as a system with a PDE in a domain that has a free boundary.

Hence, if for a Brownian motion with drift in the finite horizon case the optimal stopping time can only be implicitly characterised, it should not be expected to be anything more explicit when a more general Lévy process drives the problem. As outlined above, in the infinite horizon case we derive rather explicit results, in particular for spectrally one-sided Lévy processes. (However, our results should also lead to rather explicit results for the large family of meromorphic Lévy processes (cf. [21]) for instance). In the finite horizon case, Lemma 2 from [13] still applies and then any of the available approximation techniques for finite expiry optimal stopping problems driven by Lévy processes could be used. See for instance [20], [24], [25] and [26]. For a Canadisation based method (cf. [20] and the references therein) the results in this paper should prove useful as that method consists of solving a recursive sequence of optimal stopping problems, each of which is a variation of the infinite horizon problem.

The rest of this paper is organised as follows. In Section 2 we discuss some preliminaries and some technicalities to be used later on. In Section 3 we introduce our main result, Theorem 8. Section 4 is then dedicated to the proof of Theorem 8. In Section 5 we discuss the case that has infinite mean. We make our results more explicit in the case that is spectrally negative in Section 6. In that section we also work out the examples of a Brownian motion with drift, a Brownian motion with drift plus negative jumps and a drift plus negative jumps. Finally, in the Appendix we collect the proofs of the lemmas discussed in Section 2.

2 Preliminaries

Let be a Lévy process starting from defined on a filtered probability space , where is the filtration generated by which is naturally enlarged (cf. Definition 1.3.38 in [8]). Recall that a Lévy process is characterised by stationary, independent increments and paths which are right continuous and have left limits, and its law is characterised by the characteristic exponent defined through for all and . According to the Lévy–Khintchine formula there exist , and a measure (the Lévy measure) concentrated on satisfying (the tuple is usually refered to as the Lévy triplet) such that

We denote the running supremum at time by for all , so that is the ultimate supremum of . As is well known (see e.g. Theorem 12 on p.167 in [7]), we have

| (2.1) |

In Section 3, we look at the problem of predicting the time of the ultimate supremum of , which is defined as

(cf. the discussion in Section 3). If is not compound Poisson then we have

| (2.2) |

Indeed, making use of the Sparre–Andersen identity (cf. Lemma 15 on p. 170 in [7])

where the last equality holds since the set is a singleton when is not compound Poisson, see e.g. p. 158 of [22].

We shall soon see that the presence of an atom at in the law of plays a prominent role. Such an atom is related to (ir)regularity upwards. In fact, by denoting

| (2.3) |

is said to be regular upwards if a.s. – i.e. if enters immediately after starting from ; otherwise (then a.s.) is said to be irregular upwards. Similarly, is said to be regular (resp. irregular) downwards if is regular (resp. irregular) upwards. Theorem 6.5 in [22] classifies regularity upwards in terms of the Lévy triplet. It is a well-known rule of thumb that the value function of an optimal stopping problem driven by exhibits so-called smooth or continuous pasting dependent on whether this property holds or not, see e.g. [1] and the references therein (see also the main result of this paper, Theorem 8). We state four lemmas which will be of help to us to optimally predict the maximum of a Lévy process. The proofs of these lemmas can be found in the Appendix.

The following lemma concerns the connection between an atom at of the law of and (ir)regularity upwards.

Lemma 1.

Suppose is not a compound Poisson process and drifts to . The law of has an atom in if and only if is irregular upwards.

The next lemma allows us to conclude that when is not compound Poisson, the atom in identified in the above Lemma 1 is the only possible atom in the law of . Recall that is said to creep upwards if for some (and then all) it holds that . For instance, all Lévy processes with a Gaussian component and those of bounded variation with a positive drift creep upwards, see e.g. Theorem 7.11 in [22].

The next lemma concerns continuity properties of the distribution function of .

Lemma 2.

Suppose is not a compound Poisson process (still drifting to ). The distribution function of is continuous on . Furthermore, if creeps upwards then is Lipschitz continuous on .

Note that the above result is not sharp: there are obvious examples of Lévy processes not creeping upwards for which is nevertheless Lipschitz on , for instance when is a compound Poisson process with positive, exponentially distributed jumps plus a negative drift. In this case, when so that a.s. it holds (by Lemma 1 above) while has a positive, bounded and continuous density on (cf. Theorem 2 in [28]). For an interesting study of the law of the supremum of a Lévy process we refer to [10].

Remark 3.

Some examples of Lévy processes with two-sided jumps for which the density of is known (semi-)explicitly are Lévy processes with arbitrary negative jumps and phase-type positive jumps (cf. [28]) and the class of so-called meromorphic Lévy processes which have jumps consisting of a possibly infinite mixture of exponentials (cf. [21]). If has no positive jumps it is well known that follows an exponential distribution (cf. Section 6), while if has no negative jumps, scale functions may be used to describe the law of (cf. [22]).

We conclude with two technical results that will be of use later.

Lemma 4.

Recall the notation (2.3). Suppose that is regular downwards, then for any

Lemma 5.

Let be any Lévy process drifting to . Denote . Furthermore, for any denote by (resp. ) the measure (resp. expectation operator) under which starts from . Consider for and the optimal stopping problem

Then there is an so that for all .

3 Predicting the time of the ultimate supremum

Define the time where the ultimate supremum of the Lévy process is (first) attained by , that is

where we understand . Note that “attained” is used in a loose sense here. Indeed, if has negative jumps it might happen that the ultimate supremum is never attained. However, the above definition ensures that we have on the event while on the event . Furthermore, when is not a compound Poisson process, the set is a singleton as already mentioned in Section 2.

Our aim in this section is to find a stopping time as close as possible to , that is, we consider the optimal stopping problem

| (3.1) |

where the infimum is taken over all -stopping times.

The trichotomy of a Lévy process at infinity (see Theorem 7.1 in [22]) states that either , or a.s. In the latter two cases we have a.s. and hence (3.1) is degenerate. Henceforth in this section we assume that

| drifts to and has finite mean | (3.2) |

(we will deal with the case that has infinite mean in Proposition 17). Recall that these properties were discussed in Section 2.

Note that as and this standing assumption implies that without loss of generality we can consider the infimum in (3.1) over all stopping times with finite mean.

Recall that we denote by the distribution function of . We introduce for any the process , which is reflected in its running supremum, started from , that is

Note that for any , is a strong Markov process which drifts to (as does so). Later on, we shall also be using the following stopping times for :

| (3.3) |

Following [13] Lemma 2 and [32] Lemma 1, we rewrite the expectation in (3.1) as an expectation involving an -adapted process which will allow us to apply standard optimal stopping techniques. We include the proof here for completeness.

Proposition 6.

For any stopping time with finite mean we have that

Proof.

We have

Applying Fubini’s Theorem twice we deduce that

Furthermore, for any ,

where denotes an independent copy of . We conclude that when has finite mean

∎

Hence, by defining a function on as

| (3.4) |

we have that an optimal stopping time for is also optimal in (3.1). Therefore, let us analyse the function .

Inspecting the integrand in (3.4) makes it clear that a quantity of interest is the (lower) median of the law of , that is:

If , that is if , it is easy to see it is optimal to stop immediately. Indeed, we have the following result.

Proposition 7.

The time is optimal in (3.4) for all if and only if . In this case for all .

Proof.

Suppose . This implies for all , and, in particular, also (by right continuity). Hence for all and the result follows. Next suppose . We have

since a.s. by right continuous paths of and on . ∎

We now turn our attention to the more interesting case . Note that it is still possible that has a discontinuity in (but with size strictly less than ). Recall our standing assumptions that drifts to and has finite mean. Recall also that Lemma 2 states that is Lipschitz continuous on at least when creeps upwards. In the result below we denote by and the left and right derivative of , respectively.

Theorem 8.

Suppose that is not a compound Poisson process and is such that . Then there exists a such that an optimal stopping time in (3.4) is given by

Furthermore is a non-decreasing, continuous function satisfying the following:

-

(i)

if is regular downwards and is Lipschitz continuous on , then and (smooth pasting);

-

(ii)

if is irregular downwards, then is the unique solution on to the equation

Furthemore, when exists and is positive on , smooth pasting does not hold, i.e. .

Remark 9.

As the median of the distribution plays an important role in our main result, it is interesting to compare this with the “median rule” in [29]. There, the so-called “hidden target” is a random variable which is taken to be independent of the underlying process (which is assumed to be continuous in [29]) and the aim is to stop as close as possible (in the sense described in [29]) to this hidden target. It turns out there that it is optimal to stop as soon as the hits the median of the hidden target. In our setting, the target clearly depends on the whole path of and here it turns out that , i.e. we should wait a bit longer than just the first hitting time of the median (at least with with positive probability).

Remark 10.

In [13] it was postulated that the same problem we consider here but with a finite rather than an infinite time horizon is solved by the first time the process exceeds a time dependent boundary. As the time dependency of the boundary is a consequence of the finite horizon, this would in the case of an infinite time horizon naturally extend to the first time the process exceeds a (time independent) level. Indeed, the above Theorem 8 confirms this observation.

4 Proof of Theorem 8

As the proof of Theorem 8 is rather long, we break it into a number of lemmas which we prove in this section. We still have the standing assumption (3.2). Throughout this section we denote the payoff process for any by

so that . Note that for any , since drifts to , also drifts to . Furthermore, recall the notation introduced in (3.3), and for we write for the last time is in the interval , i.e.

We start with a technical result.

Lemma 11.

For any we have .

Proof.

Note that , where is the time the final excursion of leaves . As we assume that has a finite mean, the post-maximum process has the same law as conditioned to stay positive (see for example Proposition 4.4 in [27] or Theorem 3.1 in [6]). Therefore, is the last passage time over the level of conditioned to stay positive. From p.357 in [15] and Lemma 4 in [5] we know that is equal in distribution to , where denotes the first passage time of over level and denotes the time of the last maximum of prior to time . Therefore

where the last inequality holds since drifts to (see for example [7] Proposition 17 on p. 172). ∎

Next, we derive some properties of .

Lemma 12.

The function is non-decreasing with for all . In particular, for any .

Proof.

From the monotonicity of in and it is clear that is non-decreasing. For any we have . In particular, take some and let . Then for all and hence , where the last inequality uses that by right continuity of paths we have a.s.

Furthermore,

and using Lemma 11 it follows that . The monotonicity of implies that for all . ∎

The following result is helpful to prove continuity of .

Lemma 13.

There exists a (sufficiently large) such that for all

Proof.

We first show that there exists a such that

| (4.1) |

For this, denote and

Note that

Using this together with a dynamic programming argument and that for all (cf. Lemma 12) it follows (note that in below computation we consider w.l.o.g. only stopping times which are finite a.s.)

Appealing to Lemma 5 with and , the ultimate right-hand side is equal to which indeed vanishes for all (with and as defined in Lemma 5). Hence, if we set we indeed arrive at (4.1).

Using (4.1) together with another dynamic programming argument and we can now derive the result:

∎

Next, we use the result above to show the continuity of .

Lemma 14.

The function is continuous.

Proof.

From the above Lemma 13 we know we may write

| (4.2) |

Since is a continuous process and

| (4.3) |

(note that the last inequality follows for instance from Lemma 11) it is clear that the infimum in (4.2) is attained. As is continuous on (cf. Lemma 2) it is uniformly continuous on . Take any . Let be such that for all with it holds . For any we have, where is the optimal stopping time when starting from and we use for all :

establishing the continuity of as . ∎

The continuity of allows us to show that an optimal stopping time for is given by the first time the reflected process exceeds a certain threshold.

Lemma 15.

Denoting , we have that for any the stopping time

attains the infimum in .

Proof.

Following the usual arguments from general theory for optimal stopping (see e.g. Theorem 2.4 on p. 37 in [30] for details), taking into account (4.3) and the fact that is continuous, an optimal stopping time for is given by . Here denotes the the Snell envelope of which satisfies on account of the Markov property of :

The last lemma in this section concludes the proof. It concerns the smoothness of the function at and an expression for if is irregular downwards.

Lemma 16.

We have the following.

-

(i)

If is regular downwards and is Lipschitz continuous on , then there is smooth pasting at i.e. .

-

(ii)

If is irregular downwards, then is the unique solution on to the equation

Furthemore, if exists and is positive on smooth pasting does not hold, i.e. .

In both cases above we have .

Proof.

Consider case (i). As is non-decreasing, for it suffices to show that

| (4.4) |

For any we know from Lemma 15

and hence, if is a Lipschitz constant of

We now show that . For this, suppose we had . We will show that this violates the smooth pasting we have just established. For all small enough we have

| (4.5) |

As this ensures that and hence a dynamic programming argument yields

The first integral in the above expectation is non-positive due to (4.5) and hence

Appealing to Lemma 4 and using that we see that this implies , which is the required contradiction.

Now consider case (ii). Note that we have a.s. for all (as is irregular downwards and as ). For any we have and hence by a dynamic programming argument we may write

Letting and using that for all we see (recall is continuous)

| (4.6) |

By continuity of we have and hence the above right-hand side vanishes. Furthermore, since the integrand is monotone in and for we have , the inequality being strict with positive probability, it is clear that is the unique element in for which the right-hand side of (4.6) vanishes.

It is clear that . Indeed if we had then by continuity of this would imply . However the right hand side of (4.6) is strictly negative for on account of the following facts: it holds that for , for and a.s.

Finally, let us show that smooth pasting does not hold when has a positive derivative on . Indeed, we have for any

and using (4.6) we get

Dividing by and applying Fatou’s Lemma yields

| (4.7) |

As on the event we see that the right-hand side in (4.7) is indeed strictly positive since is. ∎

5 The case that has infinite mean

In this section we show that in the case when has infinite mean, it is impossible to find a stopping time which has finite -distance to . This is intuitively not very surprising given Theorem 8. Indeed, suppose we approximate in a suitable sense by a sequence of Lévy processes, indexed by say, for each of which the corresponding time of the ultimate supremum has finite mean. For each element in the sequence, a stopping time minimising the -distance to is the first time the reflected process exceeds a level . Suppose the ’s have a limit . If is finite then the limit of the optimal stopping times, say , is the first time the reflected process associated with exceeds the level . However this would mean that has finite mean and hence . On the other hand, if is infinite then a.s. and hence still .

We will prove the following result by introducing an independent, exponentially time horizon.

Proposition 17.

Suppose as before that is not a compound Poisson process and drifts to . Suppose now that . Then (3.1) is degenerate, i.e. for all stopping times it holds .

Proof.

For any , let denote an exponentially distributed random variable with mean , independent of . (For convenience we denote the joint law of and also by ). Furthermore, for any random time we denote

Let us assume that a stopping time exists with and derive a contradiction. First, note that since a.s. as and for all (this is readily checked from the definition of and ) dominated convergence yields

| (5.1) |

Now, using that for any we have

the same reasoning as in Proposition 6 yields for any stopping time

| (5.2) |

To examine the right-hand side of (5.2), define the function on as

| (5.3) |

Note that the mappings for any fixed and for any fixed are non-decreasing. Furthermore for any

| (5.4) |

and hence is a bounded function taking values in . It is straightforward to adjust slightly the arguments from the proof of Lemma 14 (using (5.4)) to see that is a continuous function. Following the same arguments as in the proof of Lemma 15, the Snell envelope of the process defined as

satisfies

for any . Therefore general theory of optimal stopping dictates that a stopping time minimising the right-hand side of (5.2) and, equivalently, which is optimal for , is given by

| (5.5) |

where for all . Note that the final step uses the monotonicity of in . (Cf. Theorem 2.4 on p. 37 in [30] for details.) Note that the monotonicity of implies that is non-increasing.

Now we are ready to return to our main argument. Taking the infimum over in (5.2) yields

where the infimum in the left-hand side (and in ) is attained by as defined in (5.5). Letting in this equation it follows on account of (5.1) and so that as .

Next, we show that this implies

| for any we have as . | (5.6) |

Indeed, suppose this were not the case, i.e. that exists with as such that for some and all . The monotonicity of then implies for all and . Hence for all

where the stopping time in the right-hand side has finite mean due to the fact that drifts to (see Lemma 11). However, due to (5.3) it holds that , violating as . Hence (5.6) holds.

For any we see from (5.6) together with the monotonicity of that

and consequently

This implies that

| (5.7) |

Indeed, one way to see that (5.7) holds is the following. Fix some . For an arbitrary pick so that . Then

and as all the terms in the final right-hand side vanish except for the second, which is bounded above by the arbitrarily chosen .

Remark 18.

If has infinite mean a possibility is to replace the -distance by a more interesting function. An alternative would for instance be to consider

as done in [17].

6 Spectrally negative Lévy processes

One special case for which the results from Theorem 8 can be expressed more explicitly is when is spectrally negative, i.e. when the Lévy measure is concentrated on but is not the negative of a subordinator. In this section is assumed to be spectrally negative. Further details of the definitions and properties used in this section can be found in [22] Chapter 8. It is worth recalling at this point that the relationship between the problem we set out to solve, i.e. (1.1), and the function which was defined in (3.4) and analysed in Theorem 8 is

In particular, the stopping time that is optimal for (cf. Theorem 8) is also optimal for our original problem (1.1).

Let be the Laplace exponent of , i.e.

Then exists at least on , it is strictly convex and infinitely differentiable with and . Denoting by the right inverse of , i.e. for all

the ultimate supremum follows an exponential distribution with parameter (with the usual convention that a.s. when ). It follows that

| (6.1) |

If the properties in (6.1) hold then the assumptions in Theorem 8 are satisfied. Indeed, implies that drifts to (recall (2.1)), and any compound Poisson process with no positive jumps is the negative of a subordinator which is excluded from the definition of spectrally negative. Furthermore, as follows an exponential distribution with parameter we have . Finally, Corollary 8.9 in [22] yields

which is finite when , implying that has finite mean (recall (2.2)).

Next, we briefly introduce scale functions. The scale function associated with is defined as follows: it satisfies for while on it is continuous, strictly increasing and characterised by its Laplace transform:

Furthermore on the left and right derivatives of exist. Note that in this case is regular (resp. irregular) downwards when is of unbounded (resp. bounded) variation. For ease of notation we shall assume that has no atoms when is of bounded variation, which guarantees that . Also, when is of unbounded variation it holds that with (see [23]), otherwise where is the drift of .

For several families of spectrally negative Lévy processes allows a (semi-)explicit representation, see [19] and the references therein. Scale functions are a natural tool for describing several types of fluctuation identities. Relevant for this paper is that the potential measure of the reflected process starting from killed at leaving the interval , i.e.

can also be expressed in terms of scale functions (cf. [22] Theorem 8.11):

Lemma 19.

When is spectrally negative the measure has a density on a version of which is given by

and only when is of bounded variation it has an atom at zero which is then given by

The results of Theorem 8 are expressed in terms of scale function as follows.

Corollary 20.

When is spectrally negative and satisfies any of the properties in (6.1), then is the unique solution on to the equation in :

| (6.2) |

and

| (6.3) |

Proof.

We have from Theorem 8 that , where we define

Now

Plugging in the result from Lemma 19 yields

If is of bounded variation, i.e. irregular upwards, continuity of requires in particular , which readily implies that solves (6.2) and that (6.3) holds, since for and . If is of unbounded variation, i.e. regular upwards, the smooth pasting condition at (cf. Theorem 8 (i)) again readily implies that solves (6.2) and (6.3) holds, since in this case for , and .

Finally it remains to show that (6.2) has at most one solution. This is straightforward since the function defined by

satisfies , for (here ) and for . ∎

We conclude with some explicit examples.

Example 21.

Let be a Brownian motion with drift, i.e. for and where is a standard Brownian motion. The Laplace exponent is given by

It is straightforward to check that and

Plugging this into Corollary 20 shows that is the unique solution of the equation in

and

Example 22.

In this example we consider the jump-diffusion , where is a standard Brownian motion, is a Poisson process with intensity , is a sequence of i.i.d. exponentially distributed random variables with parameter , and where and . The Laplace exponent of is given by

Choosing the parameters such that we see that has roots , and , with

Furthermore

where

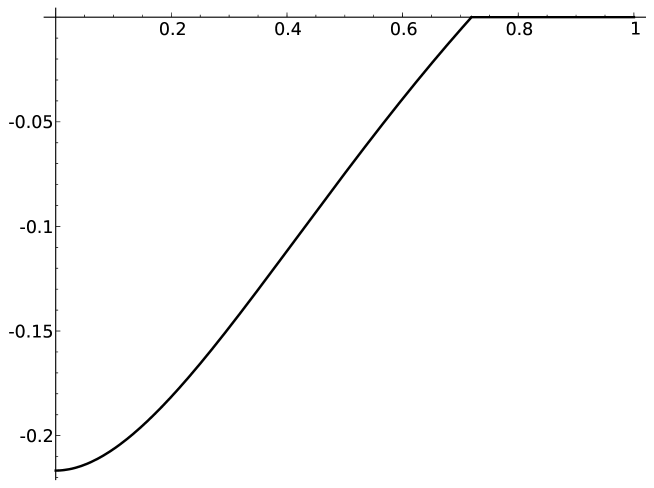

as follows directly from the definition (see also [3]). Plugging this into (6.2) and (6.3) (together with ) leads to Figure 1. Note that Figure 1 also illustrates smooth pasting at (cf. Theorem 8 (i)).

For comparison, if we set and take the resulting process is irregular downwards. In this case we have and

This setting is illustrated in Figure 2. Note that indeed the plot illustrates there is no smooth pasting at (cf. Theorem 8 (ii)).

Acknowledgements

The authors are very grateful to Jenny Sexton for useful suggestions and discussion as well as to two anonymous referees for the helpful comments.

Appendix

Here we prove the four lemmas from Section 2.

Proof of Lemma 1.

For any let be a random variable independent of following an exponential distribution with mean . From the Wiener–Hopf factorisation (see in particular part (ii) and (iii) of Theorem 6.16 in [22] e.g.) we know that for any

Then

hence if and only if

Proof of Lemma 2.

From Wiener–Hopf theory we know that is equal in law to , where is the ascending ladder height process and is an exponentially distributed random variable independent of and with parameter , where denotes the Laplace exponent of the ladder process (see e.g. Chapter 6 in [22] for further details). The Laplace exponent of given by

can be expressed as

where is the drift and the Lévy measure satisfies .

From [7] Proposition 17 on p. 172 and Theorem 19 on p. 175 it follows that creeping upwards is equivalent to , and if this is the case has a bounded, continuous and positive density on .

Henceforth suppose , while it remains to show that is continuous on when is not a compound Poisson process. If it is not difficult to see that is continuous, cf. Theorem 5.4 (i) in [22]. Let now . Then is a compound Poisson process (with jump distribution times a constant). In this case and hence in particular is irregular upwards by the above Lemma 1. Denote by the ladder height process of which is a subordinator (without killing as drifts to ). Note that cannot be a compound Poisson process, because if it were then by the same argument as above would be irregular downwards in addition to irregular upwards and hence would be compound Poisson which we excluded. So either or (or both) must hold, which in turn implies (analogue to above, cf. Theorem 5.4 (i) in [22]) that the renewal measure of given by

has no atoms. The so-called equation amicale inversée from [33] reads

and shows that has no atoms since has no atoms. Hence, is compound Poisson with a continuous jump distribution. It is now a straightforward exercise to find an expression for the law of (by conditioning on the number of jumps experiences before ) and to deduce that the continuous jump distribution guarantees that the distribution function of is continuous on . ∎

Proof of Lemma 4.

From p.10 (see the display in the middle of that page) in [9] we know that

where denotes the excursion measure, the height of a generic excursion and is the renewal function of the downward ladder height process , i.e.

This function is subadditive (as is easily seen using the Markov property) and satisfies when is regular downwards. As is not a constant function, it also holds that

Indeed, if this limsup were , then which would imply that would be the zero function since is non-decreasing and for any

This concludes the proof of Lemma 4. ∎

Proof of Lemma 5.

Denote . We break the proof up in three steps, by considering the cases where is regular dowards, a subordinator and irregular downwards, respectively.

Step 1. Let us assume that is regular downwards. Note that we may equivalently write where for . For any let be a continuous non-increasing function so that for and for . Define the process as

and define . Take some . As we have for any stopping time

so that by monotone and dominated convergence . It is readily checked that this implies

| (A.2) |

Fix some . It is straightforward to check that is continuous. Indeed for any we have

| (A.3) | |||||

where is an optimal stopping time for the optimal stopping problem

Now, note that the right-hand side (A.3) vanishes as on account of the assumption that is regular downwards. (In general the infimum in might not be attained, however in such a case the above argument still applies using a sequence of stopping times instead of ). Furthermore, can be written as a continuous function of the Markov process and is integrable since has finite mean due to the fact that drifts to (see for example [7] Proposition 17 on p. 172). These facts ensure that the general theory of optimal stopping applies and thus an optimal stopping time for is given by

| (A.4) |

cf. [30] Corrolary 2.9 on p. 46. Indeed, using the (lower) Snell envelope of yields for any

Since

we retrieve that the optimal stopping time for as dictated by the general theory of optimal stopping, namely coincides with .

Now, as for and is non-increasing it follows that

for some . Let . Then the result follows on account of (A.2) provided we show . For this, suppose we had . Along a subsequence such that we would have

| (A.5) |

since the second expectation above remains bounded while for the first expectation we have

However (A.5) is impossible since for all , and hence this step is done.

Step 2. As an intermediate step, let us now assume that is a subordinator, i.e. is a Lévy process with non-decreasing paths. We also assume the drift of is strictly positive. As a consequence, drifts to , is regular upwards and for all . Note that we may write

For any , let be defined as in Step 1 and define the process as

Furthermore set . Note we again have that for all as . Fix some . We have that is integrable since has finite mean, is a continuous function of the Markov process and is continuous which can be seen by the same argument as in Step 1 (thereby using that is regular upwards). The same argument as in Step 1 shows that the optimal stopping time for is again given by (A.4).

Fix some . For all such that we have either (or, equivalently, ) or . In the latter case, the monotonicity of the paths of and of the function imply . It follows that if we have

| (A.6) |

Take some (small) . Since is decreasing and tends to as there exists such that for all we have . We will show that for all satisfying this property we have . Indeed, take such and suppose we had . Then a subsequence exists along which . However (A.6) implies that for all such that we have which is a contradiction. Hence indeed and we conclude that the result of the lemma also holds when is a subordinator.

Step 3. Finally suppose that is irregular downwards – hence complementing Step 1. Then is necessarily of bounded variation and thus consists of a drift term plus the sum of its jumps (see equation (2.22) in [22]). Hence in particular a subordinator exists with strictly positive drift such that a.s. for all . From Step 2 above we know that the result holds for and it readily follows this means the result also holds for . ∎

References

- [1] Alili, L. and Kyprianou, A.E. (2005) Some remarks on first passage of Lévy processes, the American put and pasting principles. Ann. Appl. Probab. 15, 2062–2080.

- [2] Allaart, P. (2010) A general ‘bang-bang’ principle for predicting the maximum of a random walk. J. Appl. Probab. 47, 1072–1083.

- [3] Baurdoux, E.J. and Van Schaik, K. (2011) Further calculations for the McKean stochastic game for a spectrally negative Lévy process: from a point to an interval. J. Appl. Prob. 48, 200–216.

- [4] Bernyk, V. and Dalang, R.C. and Peskir, G. (2011) Predicting the Ultimate Supremum of a Stable Lévy Process with No Negative Jumps. Ann. Probab. 39, 2385–2423.

- [5] Bertoin, J. (1991) Sur la décomposition de la trajectoire d’un processus de Lévy spectralement positif en son infimum. Annales de l’I. H. P., section B 4, 537–547.

- [6] Bertoin, J. (1993) Splitting at the infimum and excursions in half-lines for random walks and Lévy processes. Stochastic Process. Appl. 47, 17–35.

- [7] Bertoin, J. (1996) Lévy Processes. Cambridge University Press.

- [8] Bichteler, K. (2002) Stochastic Integration with jumps. Cambridge University Press.

- [9] Chaumont, L. and Doney, R.A. (2005) On Lévy processes conditioned to stay positive. Electr. Journal Prob. 10, 948–961.

- [10] Chaumont, L. (2013) On the law of the supremum of Lévy processes. Ann. Probab., 41, 1191–1217.

- [11] Cohen, A. (2010) Examples of optimal prediction in the infinite horizon case. Statistics & Probability Letters 80, 950–957.

- [12] Du Toit, J. and Peskir, G. (2007) The Trap of Complacency in Predicting the Maximum. Ann. Probab. 35, 340–365.

- [13] Du Toit, J. and Peskir, G. (2008) Predicting the time of the ultimate maximum for Brownian motion with drift. Proc. Math. Control Theory Finance, 95–112.

- [14] Du Toit, J. and Peskir, G. (2009) Selling a Stock at the Ultimate Maximum. Ann. Appl. Probab. 19, 983–1014.

- [15] Duquesne, T. (2003) Path decompositions for real Lévy processes. Ann. I. H. Poincaré – PR 39 2, 339–370.

- [16] Espinosa, G.-E. and Touzi, N. (2012) Detecting the Maximum of a Mean-Reverting Scalar Diffusion. SIAM J. Control Optim. 50, 2543–2572.

- [17] Glover, K. and Hulley, H. and Peskir, G. (2013) Three-Dimensional Brownian Motion and the Golden Ratio Rule. Ann. Appl. Probab. 23, 895–922.

- [18] Graversen, S.E. and Peskir, G. and Shiryaev, A. N. (2001) Stopping Brownian motion without anticipation as close as possible to its ultimate maximum. Theory Probab. Appl. 45, 125–136.

- [19] Hubalek, F. and Kyprianou, A.E. (2010) Old and new examples of scale functions for spectrally negative Lévy processes. Sixth Seminar on Stochastic Analysis, Random Fields and Applications. Eds R. Dalang, M. Dozzi, F. Russo. Progress in Probability, Birkhäuser 119–146.

- [20] Kleinert, F. and Van Schaik, K. (2013) A variation of the Canadisation algorithm for the pricing of American options driven by Lévy processes. Submitted, arXiv:1304.4534.

- [21] Kuznetsov, A. and Kyprianou, A.E. and Pardo, J.C. (2012) Meromorphic Lévy processes and their fluctuation identities. Annals Appl. Prob. 22, 1101–1135.

- [22] Kyprianou, A.E. (2006) Introductory Lectures on Fluctuations of Lévy processes with Applications. Springer.

- [23] Lambert, A. (2000) Completely asymmetric Lévy processes confined in a finite interval. Ann. Inst.H. Poincaré Probab. Statist. 36, 251–274.

- [24] Levendorskii, S.Z., Kudryavtsev, O. and Zherder, V. (2006) The relative efficiency of numerical methods for pricing American options under Lévy processes. J. Comput. Finance 9, 69–97.

- [25] Maller, R.A., Solomon, D.H. and Szimayer, A. (2006) A multinomial approximation for American option prices in Lévy process models. Math. Finance 16, 613–633.

- [26] Matache, A.M., Nitsche, P.A. and Schwab, C. (2005) Wavelet Galerkin pricing of American options on Lévy driven assets. Quant. Finance 5, 403–424.

- [27] Millar, P. W. (1977) Zero-One Laws and the Minimum of a Markov Process. Transactions of the AMS 226, 365–391.

- [28] Mordecki, E. (2002) The distribution of the maximum of a Lévy process with positive jumps of phase-type. In: Proceedings of the Conference Dedicated to the 90th Anniversary of Boris Vladimirovich Gnedenko, Kyiv, pp. 309–316.

- [29] Peskir, G. (2012) Optimal Detection of a Hidden Target: The Median Rule. Stochastic Process. Appl. 122, 2249–2263.

- [30] Peskir, G. and Shiryaev, A.N. (2006) Optimal Stopping and Free-Boundary Problems. Birkhäuser Verlag.

- [31] Sato, K. (1999) Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press.

- [32] Urusov, M.A. (2005) On a property of the moment at which Brownian motion attains its maximum and some optimal stopping problems. Theory Probab. Appl. 49, 169–176.

- [33] Vigon, V. (2002) Votre Lévy rampe-t-il? Journal of the London Mathematics Society 65, 243–256.