The Fast Cauchy Transform and Faster Robust Linear Regression111A conference version of this paper appears under the same title in the Proceedings of the 2013 ACM-SIAM Symposium on Discrete Algorithms.

Abstract

We provide fast algorithms for overconstrained regression and related problems: for an input matrix and vector , in time we reduce the problem to the same problem with input matrix of dimension and corresponding of dimension . Here, and are a coreset for the problem, consisting of sampled and rescaled rows of and ; and is independent of and polynomial in . Our results improve on the best previous algorithms when , for all except ; in particular, they improve the running time of Sohler and Woodruff (STOC, 2011) for , that uses asymptotically fast matrix multiplication, and the time of Dasgupta et al. (SICOMP, 2009) for general , that uses ellipsoidal rounding. We also provide a suite of improved results for finding well-conditioned bases via ellipsoidal rounding, illustrating tradeoffs between running time and conditioning quality, including a one-pass conditioning algorithm for general problems.

To complement this theory, we provide a detailed empirical evaluation of implementations of our algorithms for , comparing them with several related algorithms. Among other things, our empirical results clearly show that, in the asymptotic regime, the theory is a very good guide to the practical performance of these algorithms. Our algorithms use our faster constructions of well-conditioned bases for spaces and, for , a fast subspace embedding of independent interest that we call the Fast Cauchy Transform: a distribution over matrices , found obliviously to , that approximately preserves the norms: that is, with large probability, simultaneously for all , , with distortion , for an arbitrarily small constant ; and, moreover, can be computed in time. The techniques underlying our Fast Cauchy Transform include fast Johnson-Lindenstrauss transforms, low-coherence matrices, and rescaling by Cauchy random variables.

1 Introduction

Random sampling, random projection, and other embedding methods have proven to be very useful in recent years in the development of improved worst-case algorithms for a range of linear algebra problems. For example, Gaussian random projections provide low-distortion subspace embeddings in the norm, mapping an arbitrary -dimensional subspace in into a -dimensional subspace in , with , and distorting the norm of each vector in the subspace by at most a constant factor. Importantly for many applications, the embedding is oblivious in the sense that it is implemented by a linear mapping chosen from a distribution on mappings that is independent of the input subspace. Such low-distortion embeddings can be used to speed up various geometric algorithms, if they can be computed sufficiently quickly. As an example, the Fast Johnson Lindenstrauss transform (FJLT) is one such embedding; the FJLT is computable in time, using a variant of the fast Hadamard transform [1]. Among other things, use of the FJLT leads to faster algorithms for constructing orthonormal bases, regression, and subspace approximation, which in turn lead to faster algorithms for a range of related problems including low-rank matrix approximation [12, 20, 10].

In this paper, we use and extensions of these methods to provide faster algorithms for the classical regression problem and several other related problems. Recall the overconstrained regression problem.

Definition 1.

Given a matrix , with , a vector , and a norm , the regression problem is to find an optimal solution to:

| (1) |

In this paper, we are most interested in the case , although many of our results hold more generally, and so we state several of our results for general . The regression problem, also known as the Least Absolute Deviations or Least Absolute Errors problem, is especially of interest as a more robust alternative to the regression or Least Squares Approximation problem.

It is well-known that for , the regression problem is a convex optimization problem; and for and , it is an instance of linear programming. Recent work has focused on using sampling, projection, and other embedding methods to solve these problems more quickly than with general convex programming or linear programming methods. Most relevant for our work is the work of Clarkson [6] on solving the regression problem with subgradient and sampling methods; the work of Dasgupta et al. [7] on using well-conditioned bases and subspace-preserving sampling algorithms to solve general regression problems; and the work of Sohler and Woodruff [24] on using the Cauchy Transform to obtain improved embeddings, thereby leading to improved algorithms for the regression problem. The Cauchy Transform of [24] provides low-distortion embeddings for the norm, and thus it is an analog of the Gaussian projection for . It consists of a dense matrix of Cauchy random variables, and so it is “slow” to apply to an arbitrary matrix ; but since it provides the first analog of the Johnson-Lindenstrauss embedding for the norm, it can be used to speed up randomized algorithms for problems such as regression and subspace approximation [24].

In this paper, we provide fast algorithms for overconstrained regression and several related problems. Our algorithms use our faster constructions of well-conditioned bases for spaces; and, for , our algorithms use a fast subspace embedding of independent interest that we call the Fast Cauchy Transform (FCT). We also provide a detailed empirical evaluation of the FCT and its use at computing well-conditioned bases and solving regression problems.

The FCT is our main technical result, and it is essentially an analog of the FJLT. The FCT can be represented by a distribution over matrices , found obliviously to (in the sense that its construction does not depend on any information in ), that approximately preserves the norms of all vectors in . That is, with large probability, simultaneously for all , , with distortion , for an arbitrarily small constant ; (see Theorem 2); and, moreover, can be computed in time. We actually provide two related constructions of the FCT (see Theorems 1 and 2). The techniques underlying our FCTs include FJLTs, low-coherence matrices, and rescaling by Cauchy random variables.

Our main application of the FCT embedding is to constructing the current fastest algorithm for computing a well-conditioned basis for (see Theorem 3). Such a basis is an analog for the norm of what an orthonormal basis is for the norm, and our result improves the result in [24]. We also provide a generalization of this result to constructing well-conditioned bases (see Theorem 10). The main application for well-conditioned bases is to regression: if the rows of are sampled according to probabilities derived from the norms of the rows of such a basis, the resulting sample of rows (and corresponding entries of ) are with high probability a coreset for the regression problem; see, e.g., [7]. That is, for an input matrix and vector , we can reduce an regression problem to another regression problem with input matrix of dimension and corresponding of dimension . Here, and consist of sampled and rescaled rows of and ; and is independent of and polynomial in . We point out that our construction uses as a black box an FJLT, which means that any improvement in the running time of the FJLT (for example exploiting the sparsity of ) results in a corresponding improvement to the running times of our regression.

Based on our constructions of well-conditioned bases, we give the fastest known construction of coresets for regression, for all , except . In particular, for regression, we construct a coreset of size that achieves a -approximation guarantee (see Theorem 4). Our construction runs in time, improving the previous best algorithm of Sohler and Woodruff [24], which has an running time. Our extension to finding an well-conditioned basis also leads to an time algorithm for a -approximation to the regression problem (see Theorem 11), improving the algorithm of Dasgupta et al. [7]. For , extensions of our basic methods yield improved algorithms for several related problems. For example, we actually further optimize the running time for to (see Theorem 5). In addition, we generalize our result to solving the multiple regression problem (see Theorem 6); and we use this to give the current fastest algorithm for computing a -approximation for the subspace approximation problem (see Theorem 7).

In addition to our construction of well-conditioned bases (see Theorem 10) and their use in providing a -approximation to the regression problem (see Theorem 11), we also provide a suite of improved results for finding well-conditioned bases via ellipsoidal rounding for general problems, illustrating tradeoffs between running time and conditioning quality. These methods complement the FCT-based methods in the sense that the FCT may be viewed as a tool to compute a good basis in an oblivious manner, and the ellipsoid-based methods provide an alternate way to compute a good basis in a data-dependent manner. In particular, we prove that we can obtain an ellipsoidal rounding matrix in at most time that provides a -rounding (see Theorem 9). This is much faster than the algorithm of Lovász [19] that computes a -rounding in time. We also present an optimized algorithm that uses an FJLT to compute a well-conditioned basis of in time (see Theorem 10). When , these rounding algorithms are competitive with or better than previous algorithms that were developed for .

Finally, we also provide the first empirical evaluation for this class of randomized algorithms. In particular, we provide a detailed evaluation of a numerical implementation of both FCT constructions, and we compare the results with an implementation of the (slow) Cauchy Transform, as well as a Gaussian Transform and an FJLT. These latter two are -based projections. We evaluate the quality of the well-conditioned basis, the core component in all our geometric algorithms, on a suite of matrices designed to test the limits of these randomized algorithms, and we also evaluate how the method performs in the context of regression. This latter evaluation includes an implementation on a nearly terabyte-scale problem, where we achieve a relative-error approximation to the optimal solution, a task that was infeasible prior to our work. Among other things, our empirical results clearly show that, in the asymptotic regime, the theory is a very good guide to the practical performance of these algorithms.

Since this paper is long and detailed, we provide here a brief outline. We start in Section 2 with some preliminaries, including several technical results that we will use in our analysis and that are of independent interest. Then, in Section 3, we will present our main technical results for the Fast Cauchy Transform; and in Section 4, we will describe applications of it to well-conditioned basis construction and leverage score approximation, to solving the regression problem, and to solving the norm subspace approximation problem. Then, in Section 5, we describe extensions of these ideas to general problems. Section 6 will contain a detailed empirical evaluation of our algorithms for -based problems, including the construction of well-conditioned bases and both small-scale and large-scale regression problems. Section 7 will then contain a brief conclusion. For simplicity of presentation, the proofs of our main results have been moved to Appendices A through J.

2 Preliminaries

Let be an input matrix, where we assume and has full column rank. The task of linear regression is to find a vector that minimizes with respect to , for a given and norm . In this paper, our focus is mostly on the norm, although we also discuss extensions to , for any . Recall that, for , the norm of a vector is , defined to be for . Let denote the set ; and let and be the th row vector and th column vector of , respectively. For matrices, we use the Frobenius norm , the -operator (or spectral) norm , and the entrywise norm . (The exception to this is , where this notation is used for the spectral norm and the entrywise 2-norm is the Frobenius norm.) Finally, the standard inner product between vectors is ; are standard basis vectors of the relevant dimension; denotes the identity matrix; and refers to a generic constant whose specific value may vary throughout the paper.

Two Useful Tail Inequalities.

The following two Bernstein-type tail inequalities are useful because they give tail bounds without reference to the number of i.i.d. trials. The first bound is due to Maurer [22], and the second is an immediate application of the first.

Lemma 1 ([22]).

Let be independent random variables with , and define . Then, for any ,

Lemma 2.

Let be i.i.d. Bernoulli random variables with probability , and let , where , with and . Then, for any ,

Proof.

The proof is a straightforward application of Lemma 1 to . ∎

Sums of Cauchy Random Variables.

The Cauchy distribution, having density , is the unique -stable distribution. If are independent Cauchys, then is distributed as a Cauchy scaled by . The Cauchy distribution will factor heavily in our discussion, and bounds for sums of Cauchy random variables will be used throughout. We note that the Cauchy distribution has undefined expectation and infinite variance.

The following upper and lower tail inequalities for sums of Cauchy random variables are proved in Appendix A. The proof of Lemma 3 is similar to an argument of Indyk [15], though in that paper the Cauchy random variables are independent. As in that paper, our argument follows by a Markov bound after conditioning on the magnitudes of the Cauchy random variable summands not being too large, so that their conditional expectations are defined. However, in this paper, the Cauchy random variables are dependent, and so after conditioning on a global event, the expectations of the magnitudes need not be the same as after this conditioning in the independent case.

Lemma 4 is a simple application of Lemma 1, while Lemma 5 was shown in [7]; we include the proofs for completeness.

Lemma 3 (Cauchy Upper Tail Inequality).

For , let be (not necessarily independent) Cauchy random variables, and with . Let . Then, for any ,

Remark. The bound has only logarithmic dependence on the number of Cauchy random variables and does not rely on any independence assumption among the random variables. Even if the Cauchys are independent, one cannot substantially improve on this bound due to the nature of the Cauchy distribution. This is because, for independent Cauchys, , and the latter sum is itself distributed as a Cauchy scaled by . Hence for independent Cauchys, .

Lemma 4 (Cauchy Lower Tail Inequality).

For , let be independent Cauchy random variables, and with and . Let . Then, for any ,

An Sampling Lemma.

We will also need an “-sampling lemma,” which is an application of Bernstein’s inequality. This lemma bounds how norms get distorted under sampling according to probabilities. The proof of this lemma is also given in Appendix A.

Lemma 5 ( Sampling Lemma).

Let and suppose that for , . For , define , and let be a random diagonal matrix with with probability , and otherwise. Then, for any (fixed) , with probability at least ,

where

3 Main Technical Result: the Fast Cauchy Transform

In this section, we present the Fast Cauchy Transform (FCT), which is an -based analog of the fast Johnson-Lindenstrauss transform (FJLT). We will actually present two related constructions, one based on using a quickly-constructable low-coherence matrix, and one based on using a version of the FJLT. In both cases, these matrices will be rescaled by Cauchy random variables (hence the name Fast Cauchy Transform). We will also state our main results, Theorems 1 and 2, which provides running time and quality-of-approximation guarantees for these two FCT embeddings.

3.1 FCT1 Construction: via a Low-coherence Matrix

This FCT construction first preprocesses by a deterministic low-coherence “spreading matrix,” then rescales by Cauchy random variables, and finally samples linear combinations of the rows. Let be a parameter governing the failure probability of our algorithm. Then, we construct as

where:

-

has each column chosen independently and uniformly from the standard basis vectors for ; we will set the parameter , where controls the probability that our algorithms fail and is a suitably large constant;

-

is a diagonal matrix with diagonal entries chosen independently from a Cauchy distribution; and

-

is a block-diagonal matrix comprised of blocks along the diagonal. Each block is the matrix , where is the identity matrix, and is the normalized Hadamard matrix. We will set . (Here, for simplicity, we assume is a power of two and is an integer.)

(For completeness, we remind the reader that the (non-normalized) matrix of the Hadamard transform may be defined recursively as follows:

The normalized matrix of the Hadamard transform is then equal to ; hereafter, we will denote this normalized matrix by .) Heuristically, the effect of in the above FCT construction is to spread the weight of a vector, so that has many entries that are not too small. (This is discussed in Lemma 7 in the proof of Theorem 1 below.) This means that the vector comprises Cauchy random variables with scale factors that are not too small; and finally these variables are summed up by , yielding a vector , whose norm won’t be too small relative to . For this version of the FCT, we have the following theorem. The proof of this theorem may be found in Appendix B.

Theorem 1 (Fast Cauchy Transform (FCT1)).

There is a distribution (given by the above construction) over matrices , with , such that for an arbitrary (but fixed) , and for all , the inequalities

| (2) |

hold with probability , where

Further, for any , the product can be computed in time.

Setting to a small constant, since and , it follows that in the above theorem.

Remark.

The existence of such a satisfying bounds of the form (2) was established by Sohler and Woodruff [24]. Here, our contribution is to show that can be factored into structured matrices so that the product can be computed in time. We also remark that, in additional theoretical bounds provided by the FJLT, high-quality numerical implementations of variants of the Hadamard transform exist, which is an additional plus for our empirical evaluations of Theorem 1 and Theorem 2.

Remark.

Our proof of this theorem uses a tail bound for in terms of and , where is any positive vector in , and is the matrix used in our FCT construction. where are anti-correlated random variables. To get concentration, we independently bounded in our proof which required to obtain the high probability result; this resulted in the bound .

3.2 FCT2 Construction: via a Fast Johnson-Lindenstrauss Transform

This FCT construction first preprocesses by a FJLT and then rescales by Cauchy random variables. Recall that is a parameter governing the failure probability of our algorithm; and let be a generic arbitrarily small positive constant (whose value may change from one formula to another). Let , , and , where the parameters are appropriately large constants. Then, we construct as

where:

-

is a matrix of independent Cauchy random variables; and

Informally, the matrix reduces the dimensionality of the input space by a very small amount such that the “slow” Cauchy Transform of [24] can be applied in the allotted time. Then, since we are ultimately multiplying by , the results of [24] still hold; but since the dimensionality is slightly reduced, the running time is improved. For this version of the FCT, we have the following theorem. The proof of this theorem may be found in Appendix C.

Theorem 2 (Fast Cauchy Transform (FCT2)).

There is a distribution (given by the above construction) over matrices , with , such that for arbitrary (but fixed) , and for all , the inequalities

hold with probability , where . Further, for any , the product can be computed in time.

Setting to be a small constant and for , , and can be computed in time. Thus, we have a fast linear oblivious mapping from from that has distortion on any (fixed) -dimensional subspace of .

Remark. For , FCT2 gives a better dependence of the distortion on , but more generally FCT2 has a dependence on . This dependence arises because the random FJLT matrix does not give a deterministic guarantee for spreading out a vector whereas the low coherence matrix used in FCT1 does give a deterministic guarantee. This means that in using the union bound, we need to overcome a factor of .

Remark. The requirement is set by the restriction in Lemma 9 in the proof of Theorem 2. In the bound of Theorem 2, , where arises from Theorem 12, which originally appeared in [24]. If a stronger version of Lemma 9 can be proved that relaxes the restriction , then correspondingly the bound of Theorem 2 will improve.

Remark. This second construction has the benefit of being easily extended to constructing well-conditioned bases of , for ; see Section 5.

4 Algorithmic Applications in of the FCT

In this section, we describe three related applications of the FCT to -based problems. The first is to the fast construction of an well-conditioned basis and the fast approximation of leverage scores; the second is a fast algorithm for the least absolute deviations or regression problem; and the third is to a fast algorithm for the norm subspace approximation problem.

4.1 Fast Construction of an Well-conditioned Basis and Leverage Scores

We start with the following definition, adapted from [7], of a basis that is “good” for the norm in a manner that is analogous to how an orthogonal matrix is “good” for the norm.

Definition 2 ( Well-conditioned Basis (adapted from [7])).

A basis for the range of is -conditioned if and for all , . We will say that is well-conditioned if and are low-degree polynomials in , independent of .

Remark. An Auerbach basis for is -conditioned, and thus we know that there exist well-conditioned bases for . More generally, well-conditioned bases can be defined in any norm, using the notion of a dual norm , and these have proven important for solving regression problems [7]. Our focus in this section is the norm, for which the dual norm is the norm, but in Section 5 we will return to a discussion of extensions to the norm.

Our main algorithm for constructing an well-conditioned basis, FastL1Basis, is summarized in Figure 1. This algorithm was originally presented in [24], and our main contribution here is to improve its running time. We note that in step 3, we do not explicitly compute the product of and , but rather just return and with the promise that is well-conditioned. The leading order term in our running time to compute is , while in [24] it is , or with fast matrix multiplication, .

Given an matrix , let be any projection matrix such that for any ,

| (3) |

For example, it could be constructed with either of the FCT constructions described in Section 3, or with the “slow” Cauchy Transform of [24], or via some other means. After computing the matrix , the FastL1Basis algorithm of Figure 1 consists of the following steps: construct and an such that , where has orthonormal columns (for example using a QR-factorization of ); and then return .

FastL1Basis: 1: Let be an matrix satisfying (3), e.g., as constructed with one of the FCTs of Section 3. 2: Compute and its QR-factorization: , where is an orthogonal matrix, i.e., . 3: Return

The next theorem and its corollary are our main results for the FastL1Basis algorithm; and this theorem follows by combining our Theorem 2 with Theorems 9 and 10 of [24]. The proof of this theorem may be found in Appendix D.

Theorem 3 (Fast Well-conditioned Basis).

Corollary 1.

If is obtained from the FCT2 construction of Theorem 2, then the resulting is an -conditioned basis for , with and , with probability . The time to compute the change of basis matrix is , assuming and is a fixed constant.

Remark. Our constructions that result in satisfying (3) do not require that ; they only require that have rank , and so can be applied to any having rank . In this case, a small modification is needed in the construction of , because , and so we need to use instead of . The running time will involve terms with . This can be improved by processing quickly into a smaller matrix by sampling columns so that the range is preserved (as in [24]), which we do not discuss further.

The notion of a well-conditioned basis plays an important role in our subsequent algorithms. Basically, the reason is that these algorithms compute approximate answers to the problems of interest (either the regression problem or the subspace approximation problem) by using information in that basis to construct a nonuniform importance sampling distribution with which to randomly sample. This motivates the following definition.

Definition 3 ( Leverage Scores).

Given a well-conditioned basis for the range of , let the -dimensional vector , with elements defined as be the leverage scores of .

Remark. The name leverage score is by analogy with the leverage scores, which are important in random sampling algorithms for regression and low-rank matrix approximation [21, 20, 10]. As with regression and low-rank matrix approximation, our result for regression and subspace approximation will ultimately follow from the ability to approximate these scores quickly. Note, though, that these -based scores are not well-defined for a given matrix , in the sense that the norm is not rotationally invariant, and thus depending on the basis that is chosen, these scores can differ by factors that depend on low-degree polynomials in . This contrasts with , since for any orthogonal matrix spanning a given subspace leads to the same leverage scores. We will tolerate this ambiguity since these leverage scores will be used to construct an importance sampling distribution, and thus up to low-degree polynomial factors in , which our analysis will take into account, it will not matter.

4.2 Fast Regression

Here, we consider the regression problem, also known as the least absolute deviations problem, the goal of which is to minimize the norm of the residual vector . That is, given as input a design matrix , with , and a response or target vector , compute

| (4) |

and an achieving this minimum. We start with our main algorithm and theorem for this problem; and we then describe how a somewhat more sophisticated version of the algorithm yields improved running time bounds.

4.2.1 Main Algorithm for Fast Regression

Prior work has shown that there is a diagonal sampling matrix with a small number of nonzero entries so that satisfies

where is an optimal solution for the minimization in (4); see [7, 24]. The matrix can be found by sampling its diagonal entries independently according to a set of probabilities that are proportional to the leverage scores of . Here, we give a fast algorithm to compute estimates of these probabilities. This permits us to develop an improved algorithm for regression and to construct efficiently a small coreset for an arbitrary regression problem.

In more detail, Figure 2 presents the FastCauchyRegression algorithm, which we summarize here. Let . First, a matrix satisfying (3) is used to reduce the dimensionality of to and to obtain the orthogonalizer . Let be the resulting well-conditioned basis for the range of . The probabilities we use to sample rows are essentially the row-norms of . However, to compute explicitly takes time, which is already too costly, and so we need to estimate without explicitly computing . To construct these probabilities quickly, we use a second random projection —on the right. This second projection allows us to estimate the norms of the rows of efficiently to within relative error (which is all we need) using the median of independent Cauchy’s, each scaled by . (Note that this is similar to what was done in [10] to approximate the leverage scores of an input matrix.) These probabilities are then used to construct a carefully down-sampled (and rescaled) problem, the solution to which will give us our approximation to the original problem.

FastCauchyRegression: 1: Let and construct , an matrix satisfying (3) with replaced by . (If is a vector then .) 2: Compute and its QR factorization, . (Note that has orthonormal columns.) 3: Let be a matrix of independent Cauchys, with . 4: Let and construct . 5: For , compute 6: For and , compute probabilities 7: Let be diagonal with independent entries: 8: Return that minimizes w.r.t. (using linear programming).

The next theorem summarizes our main quality-of-approximation results for the FastCauchyRegression algorithm of Figure 2. It improves the algorithm of [24], which in turn improved the result in [7]. (Technically, the running time of [24] is , where is any constant larger than the exponent for matrix multiplication; for practical purposes, we can set .) Our improved running time comes from using the FCT and a simple row-norm estimator for the row-norms of a well-conditioned basis. The proof of this theorem may be found in Appendix E.

Theorem 4 (Fast Cauchy Regression).

Given are , , and . FastCauchyRegression constructs a coreset specified by the diagonal sampling matrix and a solution vector that minimizes the weighted regression objective . The solution satisfies, with probability at least ( is a constant),

Further, with probability , the entire algorithm to construct runs in time

where is the time to solve an -regression problem on vectors in dimensions, and if FCT2 is used to construct then .

Remarks. Several remarks about our results for the regression problem are in order.

- •

-

•

A natural extension of our algorithm to matrix-valued right hand sides gives a approximation in a similar running time for the -norm subspace approximation problem. See Section 4.3 for details.

-

•

We can further improve the efficiency of solving this simple regression problem, thereby replacing the running time term in Theorem 4 with , but at the expense of a slightly larger sample size . The improved algorithm is essentially the same as the FastCauchyRegression algorithm, except with two differences: is chosen to be a matrix of i.i.d. Gaussians, for a value ; and, to accommodate this, the size of needs to be increased. Details are presented in Section 4.2.2.

4.2.2 A Faster Algorithm for Regression

Here, we present an algorithm that improves the efficiency of our regression algorithm from Section 4.2.1; and we state and prove an associated quality-of-approximation theorem. See Figure 3, which presents the OptimizedFastCauchyRegression algorithm. This algorithm has a somewhat larger sample size than our previous algorithm, but our main theorem for this algorithm will replace the running time term in Theorem 4 with a term.

OptimizedFastCauchyRegression: 1: Let and construct , an matrix satisfying (3) with replaced by . 2: Compute and its QR factorization, . (Note that has orthonormal columns.) 3: Set the parameters 4: Let be a matrix of independent standard Gaussians. 5: Construct . 6: For , compute 7: For compute probabilities 8: Let be diagonal with independent entries: 9: Return that minimizes w.r.t. (using linear programming).

The intuition behind the OptimizedFastCauchyRegression algorithm is as follows. The -th entry will be a -mean Gaussian with variance . Since the row has -dimensions, the norm and norm only differ by . Hence, at the expense of some factors of in the sampling complexity , we can use sampling probabilities based on the norms. The nice thing about using norms is that we can use Gaussian random variables for the entries of rather than Cauchy random variables. Given the exponential tail of a Gaussian random variable, for a with fewer columns we can still gurantee that no sampling probability increases by more than a logarithmic factor. The main difficulty we encounter is that some sampling probabilities may decrease by a larger factor, even though they do not increase by much – however, one can argue that with large enough probability, no row is sampled by the algorithm if its probability shrinks by a large factor. Therefore, the behavior of the algorithm is as if all sampling probabilities change by at most a factor, and the result will follow. Here is our main theorem for the OptimizedFastCauchyRegression algorithm. The proof of this theorem may be found in Appendix F.

Theorem 5 (Optimized Fast Cauchy Regression).

Given are , , and . OptimizedFastCauchyRegression constructs a coreset specified by the diagonal sampling matrix and a solution vector that minimizes the weighted regression objective . The solution satisfies, with probability at least ,

Further, with probability , the entire algorithm to construct , runs in time

where is the time to solve an -regression problem on vectors in dimensions, and if FCT2 is used to construct then

Note that our algorithms and results also extend to multiple regression with , a fact that will be exploited in the next section.

4.3 norm Subspace Approximation

Finally, we consider the norm subspace approximation problem: Given the points in the matrix and a parameter , embed these points into a subspace of dimension to obtain the embedded points such that is minimized. (Note that this is the analog of the problem that is solved by the Singular Value Decomposition.) When , the subspace is a hyperplane, and the task is to find the hyperplane passing through the origin so as to minimize the sum of distances of the points to the hyperplane. In order to solve this problem with the methods from Section 4.2, we take advantage of the observation made in [5] (see also Lemma 18 of [24]) that this problem can be reduced to related regressions of onto each of its columns, a problem sometimes called multiple regression. Thus, in Section 4.3.1, we extend our “simple” regression algorithm to an “multiple” regression algorithm; and then in Section 4.3.2, we show how this can be used to solve the norm subspace approximation problem.

4.3.1 Generalizing to Multiple Regression

The multiple regression problem is similar to the simple regression problem, except that it involves solving for multiple right hand sides, i.e., both and become matrices ( and , respectively). Specifically, let and . We wish to find which solves

Although the optimal can clearly be obtained by solving separate simple regressions, with for , one can do better. As with simple regression, we can reformulate the more general constrained optimization problem:

To recover multiple regression, we set and , in which case the constraint set is .

A detailed inspection of the proof of Theorem 4 in Section 4.2 (see Appendix E for the proof) reveals that nowhere is it necessary that be a vector, i.e., the whole proof generalizes to a matrix . In particular, the inequalities in (9) continue to hold, since if they hold for every vector , then it must hold for a matrix because . Similarly, if Lemma 13 continues to hold for vectors then it will imply the desired result for matrices, and so the only change in all the algorithms and results is that the short dimension of changes from to . Thus, by shrinking by an additional factor of , and taking a union bound we get a relative error approximation for each individual regression. We refer to this modified algorithm, where a matrix is input and the optimization problem in the last step is modified appropriately, as FastCauchyRegression, overloading notation in the obvious way. This discussion is summarized in the following theorem.

Theorem 6 (Fast Cauchy Multiple Regression).

Given , , a matrix and , FastCauchyRegression constructs a coreset specified by the diagonal sampling matrix and a solution that minimizes the weighted multiple regression objective . The solution satisfies, with probability at least ,

Further, with probability , the entire algorithm to construct , runs in time

where is the time to solve -regression problem on the same vectors in dimensions, and if FCT2 is used to construct , then .

Remarks. Several remarks about our results for this multiple regression problem are in order.

-

•

First, we can save an extra factor of in in the above theorem if all we want is a relative error approximation to the entire multiple regression and we do not need relative error approximations to each individual regression.

-

•

Second, when it is interesting that there is essentially no asymptotic overhead in solving this problem other than the increase from to ; in general, by preprocessing the matrix , solving regressions on this same matrix is much quicker than solving separate regressions. This should be compared with regression, where solving regressions with the same takes (since the SVD of needs to be done only once), versus a time of for separate regressions.

-

•

Third, we will use this version of multiple regression problem, which is more efficient than solving separate -simple regressions, to solve the -subspace approximation problem. See Section 4.3.2 for details.

4.3.2 Application to norm Subspace Approximation

Here, we will take advantage of the observation made in [5] that the norm subspace approximation problem can be reduced to related regressions of onto each of its columns. To see this, consider the following regression problem:

This regression problem is fitting (in the norm) the th column of onto the remaining columns. Let be an optimal solution. Then if we replace by , the resulting vectors will all be in a dimensional subspace. Let be with replaced by . The crucial observation made in [5] (see also Lemma 18 of [24]) is that one of the is optimal—and so the optimal subspace can be obtained by simply doing a hyperplane fit to the embedded points. So,

When viewed from this perspective, the -norm subspace approximation problem makes the connection between low-rank matrix approximation and overconstrained regression. (A similar approach was used in the case to obtain relative-error low-rank CX and CUR matrix decompositions [11, 21].) We thus need to perform constrained regressions, which can be formulated into a single constrained multiple regression problem, which can be solved as follows: Find the matrix that solves:

where the constraint set is . Since the constraint set effectively places an independent constraint on each column of , after some elementary manipulation, it is easy to see that this regression is equivalent to the individual regressions to obtain . Indeed, for an optimal solution , we can set .

Thus, using our approximation algorithm for constrained multiple regression that we described in Section 4.3.1, we can build an approximation algorithm for the -norm subspace approximation problem that improves upon the previous best algorithm from [24] and [5]. (The running time of the algorithm of [24] is , where and is any constant.) Our improved algorithm is basically our multiple regression algorithm, FastCauchyRegression, invoked with and (NULL). The algorithm proceeds exactly as outlined in Figure 2, except for the last step, which instead uses linear programming to solve for that minimizes with respect to . (Note that the constraints defining are very simple affine equality constraints.) Given , we define and compute where is with the column replaced by . It is easy to now show that is a -approximation to the dimensional subspace approximation problem. Indeed, recall that is optimal and the optimal error is for some ; however, for any :

where (a) is from the -optimality of the constrained multiple regression as analyzed in Appendix E and (b) is because attained minimum error among all . This discussion is summarized in the following theorem.

Theorem 7.

Given ( points in dimensions), there is a randomized algorithm which outputs a -approximation to the -norm subspace approximation problem for these points with probability at least . Further, the running time, with probability , is

5 Extensions to , for

In this section, we describe extensions of our methods to , for . We will first (in Section 5.1) discuss norm conditioning and connect it to ellipsoidal rounding, followed by a fast rounding algorithm for general centrally symmetric convex sets (in Section 5.2); and we will then (in Section 5.3) show how to obtain quickly a well-conditioned basis for the norm, for any and (in Section 5.4) show how this basis can be used for improved regression. These results will generalize our results for from Sections 4.1 and 4.2, respectively, to general .

5.1 norm Conditioning and Ellipsoidal Rounding

As with regression, regression problems are easier to solve when they are well-conditioned. Thus, we start with the definition of the norm condition number of a matrix .

Definition 4 ( norm conditioning).

Given an matrix , let

Then, we denote by the norm condition number of , defined to be:

For simplicity, we will use , , and when the underlying matrix is clear.

There is a strong connection between the norm condition number and the concept of an -conditioning developed by Dasgupta et al. [7].

Definition 5 (-conditioning (from [7])).

Given an matrix and , let be the dual norm of , i.e., . Then is -conditioned if (1) , and (2) for all , . Define as the minimum value of such that is -conditioned. We say that is well-conditioned if , independent of .

The following lemma characterizes the relationship between these two quantities.

Lemma 6.

Given an matrix and , we always have

Proof.

To see the connection, recall that

and that

Thus, is -conditioned and . On the other hand, if is -conditioned, we have, for all ,

and

Thus, . ∎

Although it is easier to describe sampling algorithms in terms of , after we show the equivalence between and , it will be easier for us to discuss conditioning algorithms in terms of , which naturally connects to ellipsoidal rounding algorithms.

Definition 6.

Let be a convex set that is full-dimensional, closed, bounded, and centrally symmetric with respect to the origin. An ellipsoid is a -rounding of if it satisfies , for some , where means shrinking by a factor of .

To see the connection between rounding and conditioning, let and assume that we have a -rounding of : . This implies

If we let , then we get

Therefore, we have . So a -rounding of leads to a -conditioning of .

5.2 Fast Ellipsoidal Rounding

Here, we provide a deterministic algorithm to compute a -rounding of a centrally symmetric convex set in that is described by a separation oracle. Recall the well-known result due to John [17] that for a centrally symmetric convex set there exists a -rounding and that such rounding is given by the Löwner-John (LJ) ellipsoid of , i.e., the minimal-volume ellipsoid containing . However, finding this -rounding is a hard problem. To state algorithmic results, suppose that is described by a separation oracle and that we are provided an ellipsoid that gives an -rounding for some . In this case, the best known algorithmic result of which we are aware is that we can find a -rounding in polynomial time, in particular, in calls to the oracle; see Lovász [19, Theorem 2.4.1]. This result was used by Clarkson [6] and by Dasgupta et al. [7]. Here, we follow the same construction, but we show that it is much faster to find a (slightly worse) -rounding. The proof of this theorem may be found in Appendix G.1.

Theorem 8 (Fast Ellipsoidal Rounding).

Given a centrally symmetric convex set centered at the origin and described by a separation oracle, and an ellipsoid centered at the origin such that for some , it takes at most calls to the oracle and additional time to find a -rounding of .

Applying Theorem 8 to the convex set , with the separation oracle described via a subgradient of and the initial rounding provided by the “” matrix from the QR decomposition of , we improve the running time of the algorithm used by Clarkson [6] and by Dasgupta et al. [7] from to while maintaining an -conditioning. The proof of this theorem may be found in Appendix G.2.

Theorem 9.

Given an matrix with full column rank, it takes at most time to find a matrix such that .

5.3 Fast Construction of an Well-conditioned Basis

Here, we consider the construction of a basis that is well-conditioned for . To obtain results for general that are analogous to those we obtained for , we will extend the FCT2 construction from Section 3.2, combined with Theorem 8.

Our main algorithm for constructing a -well-conditioned basis, the FastLpBasis algorithm, is summarized in Figure 4. The algorithm first applies block-wise embeddings in the norm, similar to the construction of FCT2; it then uses the algorithm of Theorem 8 to compute a -rounding of a special convex set and obtain the matrix . It is thus a generalization of our FastL1Basis algorithm of Section 4.1, and it follows the same high-level structure laid out by the algorithm of [10] for computing approximations to the leverage scores and an well-conditioned basis.

FastLpBasis: 1: Let , , and be an Fast Johnson-Lindenstrauss matrix, the same as the matrix in the FCT2 construction. 2: Partition along its rows into sub-matrices of size , denoted by , compute for , and define 3: Apply the algorithm of Theorem 8 to obtain a -rounding of : . 4: Output .

The next theorem is our main result for the FastLpBasis algorithm. It improves the running time of the algorithm of Theorem 9, at the cost of slightly worse conditioning quality. However, these worse factors will only contribute to a low-order additive term in the running time of our regression application in Section 5.4. The proof of this theorem may be found in Appendix H.

Theorem 10 (Fast Well-conditioned Basis).

For any with full column rank, the basis constructed by FastLpBasis (Figure 4), with probability at least , is well-conditioned with . The time to compute is .

5.4 Fast Regression

Here, we show that the overconstrained regression problem can be solved with a generalization of the algorithms of Section 4.2 for solving regression; we will call this generalization the FastLpRegression algorithm. In particular, as with the algorithm for regression, this FastLpRegression algorithm for the regression problem uses an well-conditioned basis and samples rows of with probabilities proportional to the norms of the rows of the corresponding well-conditioned basis (which are the analogs of the leverage scores). As with the FastCauchyRegression, this entails using—for speed—a second random projection applied to —on the right—to estimate the row norms. This allows fast estimation of the norms of the rows of , which provides an estimate of the norms of those rows, up to a factor of . We use these norm estimates, e.g., as in the above algorithms or in the sampling algorithm of [7]. As discussed for the running time bound of [7], Theorem 7, this algorithm samples a number of rows proportional to . This factor, together with a sample complexity increase of needed to compensate for error due to using , gives a sample complexity increase for the FastLpRegression algorithm while the leading term in the complexity (for ) is reduced from to . We modify Theorem 7 of [7] to obtain the following theorem.

Theorem 11 (Fast Regression).

Given , , and , there is a random sampling algorithm (the FastLpRegression algorithm described above) for regression that constructs a coreset specified by a diagonal sampling matrix , and a solution vector that minimizes the weighted regression objective . The solution satisfies, with probability at least , the relative error bound that for all . Further, with probability , the entire algorithm to construct runs in time

where with , and is the time to solve an regression problem on vectors in dimensions.

6 Numerical Implementation and Empirical Evaluation

In this section, we describe the results of our empirical evaluation. We have implemented and evaluated the Fast Cauchy Transforms (both FCT1 and FCT2) as well as the Cauchy transform (CT) of [24]. For completeness, we have also compared our method against two -based transforms: the Gaussian Transform (GT) and a version of the FJLT. Ideally, the evaluation would be based on the evaluating the distortion of the embedding, i.e., evaluating the smallest such that

where is one of the Cauchy transforms. Due to the non-convexity, there seems not to be a way to compute, tractably and accurately, the value of this . Instead, we evaluate both -based transforms (CT, FCT1, and FCT2) and -based transforms (GT and FJLT) based on how they perform in computing well-conditioned bases and approximating regression problems.

6.1 Evaluating the Quality of Well-conditioned Bases

We first describe our methodology. Given a “tall and skinny” matrix with full column rank, as in Section 4.1, we compute well-conditioned bases of : , where is one of those transforms, and where and are from the QR decomposition of . Our empirical evaluation is based on the metric . Note that is scale-invariant: if is -conditioned with , is -conditioned, and hence . This saves us from determining the scaling constants when implementing CT, FCT1, and FCT2. While computing is trivial, computing is not as easy: it requires solving linear programs:

Note that this essentially limits the size of the test problems in our empirical evaluation: although we have applied our algorithms to much larger problems, we must solve these linear programs if we want to provide a meaningful comparison by comparing our fast -based algorithms with an “exact” answer. Another factor limiting the size of our test problems is more subtle and is a motivation for our comparison with -based algorithms. Consider a basis induced by the Gaussian transform: , where is a matrix whose entries are i.i.d. Gaussian. We know that with high probability. In such case, we have

and

Hence . Similar results apply to the FJLTs that work on an entire subspace of vectors, e.g., the Subsampled Randomized Hadamard Transform (SRHT) [28]. In our empirical evaluation, we use SRHT as our implementation of FJLT, but we note that similar running times hold for other variants of the FJLT [4]. Table 1 lists the running time and worst-case performance of each transform on conditioning, clearly showing the cost-performance trade-offs. For example, comparing the condition number of GT or FJLT, , with the condition number of CT, , we will need to see the advantage of CT over -based algorithms (e.g., should be at least at the scale of when is ). To observe the advantage of FCT1 and FCT2 over -based transforms, should be relatively even larger.

| time | ||

|---|---|---|

| CT | ||

| FCT1 | ||

| FCT2 | ||

| GT | ||

| FJLT |

Motivated by these observations, we create two sets of test problems. The first set contains matrices of size and the second set contains matrices of size . We choose the number of rows to be powers of to implement FCT2 and FJLT in a straightforward way. Based on our theoretical analysis, we expect -based algorithms should work better on the first test set than -based algorithms, at least on some worst-case test problems; and that this advantage should disappear on the second test set. For each of these two sizes, we generate four test matrices: is randomly generated ill-conditioned matrix with slightly heterogeneous leverage scores; is randomly generated ill-conditioned matrix with strongly heterogeneous leverage scores; and and are two “real” matrices chosen to illustrate the performance of our algorithms on real-world data. In more detail, the test matrices are as follows:

-

•

, where is a diagonal matrix whose diagonals are linearly spaced between and , is a Gaussian matrix, is a diagonal matrix whose diagonals are linearly spaced between and , and is a Gaussian matrix. is chosen in this way so that it is ill-conditioned (due to the choice of ) and its bottom rows tend to have high leverage scores (due to the choice of ).

-

•

, where is a Gaussian matrix. The first rows tend to have very high leverage scores because missing any of them would lead to rank deficiency, while the rest rows are the same from each other and hence they tend to have very low leverage scores. is also ill-conditioned because we have , where is very large.

- •

-

•

, the leading submatrix of the TinyImages matrix created by Torralba et al. [26]. The original images are in RGB format. We convert them to grayscale intensity images, resulting a matrix of size .

To implement FCT1 and FCT2 for our empirical evaluations, we have to fix several parameters in Theorems 2 and 1, finding a compromise between theory and practice. We choose except for GT. We choose and for FCT1, and for FCT2. Although those settings don’t follow Theorems 2 and 1 very closely, they seem to be good for practical use. Since all the transforms are randomized algorithms that may fail with certain probabilities, for each test matrix and each transform, we take independent runs and show the first and the third quartiles of in Tables 2 and 3.

| 1.93e+04 | 7.67e+05 | 8.58 | 112 | |

| CT | [10.8, 39.1] | [10.4, 41.7] | [10.2, 33] | [8.89, 42.8] |

| FCT1 | [9.36, 21.2] | [15.4, 58.6] | [10.9, 38.9] | [11.3, 40.8] |

| FCT2 | [12.3, 32.1] | [17.3, 76.1] | [10.9, 43] | [11.3, 42.1] |

| GT | [6.1, 8.81] | [855, 1.47e+03] | [5.89, 8.29] | [6.9, 9.17] |

| FJLT | [5.45, 6.29] | [658, 989] | [5.52, 6.62] | [6.18, 7.53] |

| 4.21e+05 | 2.39e+06 | 36.5 | 484 | |

| CT | [90.2, 423] | [386, 1.44e+03] | [110, 633] | [150, 1e+03] |

| FCT1 | [113, 473] | [198, 1.1e+03] | [114, 765] | [127, 684] |

| FCT2 | [134, 585] | [237, 866] | [106, 429] | [104, 589] |

| GT | [27.4, 31] | [678, 959] | [28.8, 32.3] | [29.4, 33.5] |

| FJLT | [19.9, 21.2] | [403, 481] | [21.4, 23.1] | [21.8, 23.2] |

The empirical results, described in detail in Tables 2 and 3, conform with our expectations. The specifically designed -based algorithms perform consistently across all test matrices, while the performance of -based algorithms is quite problem-dependent. Interestingly, though, the -based methods often perform reasonably well: at root, the reason is that for many input the leverage scores are not too much different than the leverage scores. That being said, the matrix clearly indicates that -based methods can fail for “worst-case” input; while the -based methods perform well for this input.

On the first test set, -based algorithms are comparable to -based algorithms on , , and but much better on . The differences among -based algorithms are small. In terms of conditioning quality, CT leads FCT1 and FCT2 by a small amount on average; but when we take running times into account, FCT1 and FCT2 are clearly more favorable choices in this asymptotic regime. On the second test set, -based algorithms become worse than -based on , , and due to the increase of and the decrease of . All the algorithms perform similarly on ; but -based algorithms, involving Cauchy random variables, have larger variance than -based algorithms.

|

|

|

|

6.2 Application to Regression

Next, we embed these transforms into fast approximation of regression problems to see how they affect the accuracy of approximation. We implement the FastCauchyRegression algorithm of Section 4.2, except that we compute the row norms of exactly instead of estimating them. Although this takes time, it is free from errors introduced by estimating the row norms of , and thus it permits a more direct evaluation of the regression algorithm. Unpublished results indicate that using approximations to the leverage scores, as is done at the beginning of the FastCauchyRegression algorithm, leads to very similar quality-of-approximation results.

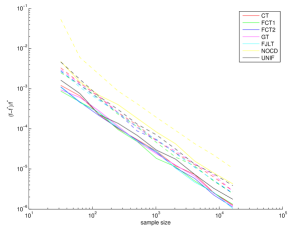

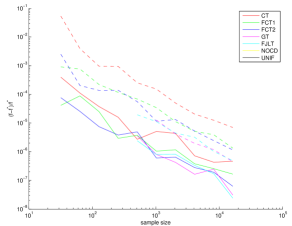

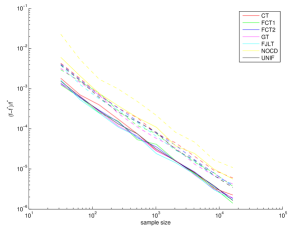

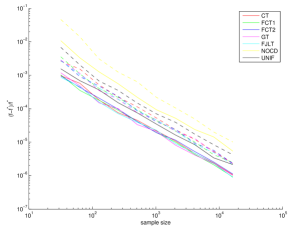

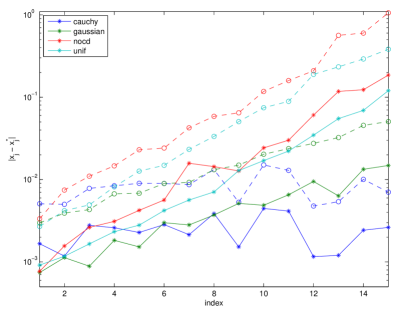

We generate a matrix of size and generate the right-hand sides , where is a Gaussian vector, and is a random vector whose entries are independently sampled from the Laplace distribution and scaled such that . Then, for each row , with probability we replace by to simulate corruption in measurements. On this kind of problems, regression should give very accurate estimate, while regression won’t work well. For completeness, we also add uniform sampling (UNIF) and no conditioning (NOCD) into the evaluation. Instead of determining the sample size from a given tolerance, we accept the sample size as a direct input; and we choose sample sizes from to .

The results are shown in Figure 5, where we draw the first and the third quartiles of the relative errors in objective value from independent runs. If the subsampled matrix is rank-deficient, we set corresponding relative error to to indicate a failure. We remove relative errors that are larger than from the plot in order to show more details. As expected, we can see that UNIF and NOCD are certainly not among reliable choices; they failed (either generating rank-deficient subsampled problems or relative errors larger than ) completely on . In addition, GT and FJLT failed partially on the same test. Empirically, there is not much difference among -based algorithms: CT works slightly worse than FCT1 and FCT2 on these tests, which certainly makes FCT1 and FCT2 more favorable. (One interesting observation is that we find that, in these tests at least, the relative error is proportional to instead of . At this time, we don’t have theory to support this observation.) This coupled with the fact that leverage scores can be approximated more quickly with FCT1 and FCT2 suggests the use of these transforms in larger-scale applications of regression.

6.3 Evaluation on a Large-scale Regression Problem

Here, we continue to demonstrate the capability of sampling-based algorithms in large-scale applications by solving a large-scale regression problem with imbalanced and corrupted measurements. The problem is of size , generated in the following way:

-

1.

The true signal is a standard Gaussian vector.

-

2.

Each row of the design matrix is a canonical vector, which means that we only estimate a single entry of in each measurement. The number of measurements on the -th entry of is twice as large as that on the -th entry, . We have billion measurements on the first entry while only million measurements on the last. Imbalanced measurements apparently create difficulties for sampling-based algorithms.

-

3.

The response vector is given by

where is the -th row of and are i.i.d. samples drawn from the Laplace distribution. measurements are corrupted to simulate noisy real-world data. Due to these corrupted measurements, regression won’t give us accurate estimate, and regression is certainly a more robust alternative.

Since the problem is separable, we know that an optimal solution is simply given by the median of responses corresponding to each entry.

The experiments were performed on a Hadoop cluster with cores. Similar to our previous test, we implemented and compared Cauchy-conditioned sampling (CT), Gaussian-conditioned sampling (GT), un-conditioned sampling (NOCD), and uniform sampling (UNIF). Since only has non-zeros, CT takes time instead of , which makes it the fastest among CT, FCT1, and FCT2 on this particular problem. Moreover, even if is dense, data at this scale are usually stored on secondary storage, and thus time spent on scanning the data typically dominates the overall running time. Therefore, we only implemented CT for this test. Note that the purpose of this test is not to compare CT, FCT1, and FCT2 (which we did above), but to reveal some inherent differences among conditioned sampling (CT, FCT1, and FCT2), conditioned sampling (GT and FJLT), and other sampling algorithms (NOCD and UNIF). For each algorithm, we sample approximately () rows and repeat the sampling times, resulting approximate solutions. Note that those approximate solutions can be computed simultaneously in a single pass.

We first check the overall performance of these sampling algorithms, measured by relative errors in -, -, and -norms. The results are shown in Table 4.

| CT | [0.008, 0.0115] | [0.00895, 0.0146] | [0.0113, 0.0211] |

|---|---|---|---|

| GT | [0.0126, 0.0168] | [0.0152, 0.0232] | [0.0184, 0.0366] |

| NOCD | [0.0823, 22.1] | [0.126, 70.8] | [0.193, 134] |

| UNIF | [0.0572, 0.0951] | [0.089, 0.166] | [0.129, 0.254] |

Since the algorithms are all randomized, we show the first and the third quartiles of the relative errors in independent runs. We see that CT clearly performs the best, followed by GT. UNIF works but it is about a magnitude worse than CT. NOCD is close to UNIF at the first quartile, but makes very large errors at the third. Without conditioning, NOCD is more likely to sample outliers because the response from a corrupted measurement is much larger than that from a normal measurement. However, those corrupted measurements contain no information about , which leads to NOCD’s poor performance. UNIF treats all the measurements the same, but the measurements are imbalanced. Although we sample measurements, the expected number of measurements on the last entry is only , which downgrades UNIF’s overall performance.

We continue to analyze entry-wise errors. Figure 6 draws the first and the third quartiles of entry-wise absolute errors, which clearly reveals the differences among conditioned sampling, conditioned sampling, and other sampling algorithms.

While UNIF samples uniformly row-wise, CT tends to sample uniformly entry-wise. Although not as good as other algorithms on the first entry, CT maintains the same error level across all the entries, delivering the best overall performance. The -based GT sits between CT and UNIF. conditioning can help detect imbalanced measurements to a certain extent and adjust the sampling weights accordingly, but it is still biased towards the measurements on the first several entries.

To summarize, we have shown that conditioned sampling indeed works on large-scale regression problems and its performance looks promising. We obtained about two accurate digits ( relative error) on a problem of size by passing over the data twice and sampling only rows in a judicious manner.

7 Conclusion

We have introduced the Fast Cauchy Transform, an -based analog of fast Hadamard-based random projections. We have also demonstrated that this fast -based random projection can be used to develop algorithms with improved running times for a range of -based problems; we have provided extensions of these results to ; and we have provided the first implementation and empirical evaluation of an -based random projection. Our empirical evaluation clearly demonstrates that for large and very rectangular problems, for which low-precision solutions are acceptable, our implementation follows our theory quite well; and it also points to interesting connections between -based projections and -based projections in practical settings. Understanding these connections theoretically, exploiting other properties such as sparsity, and using these ideas to develop improved algorithms for high-precision solutions to large-scale -based problems, are important future directions raised by our work.

References

- [1] N. Ailon and B. Chazelle. The fast Johnson-Lindenstrauss transform and approximate nearest neighbors. SIAM Journal on Computing, 39(1):302–322, 2009.

- [2] N. Ailon and E. Liberty. Fast dimension reduction using Rademacher series on dual BCH codes. In Proceedings of the 19th Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1–9, 2008.

- [3] S. Arora, E. Hazan, and S. Kale. A fast random sampling algorithm for sparsifying matrices. In Proceedings of the 10th International Workshop on Randomization and Computation, pages 272–279, 2006.

- [4] H. Avron, P. Maymounkov, and S. Toledo. Blendenpik: Supercharging LAPACK’s least-squares solver. SIAM Journal on Scientific Computing, 32:1217–1236, 2010.

- [5] J. P. Brooks and J. H. Dulá. The L1-norm best-fit hyperplane problem. Applied Mathematics Letters, 26(1):51–55, 2013.

- [6] K. Clarkson. Subgradient and sampling algorithms for regression. In Proceedings of the 16th Annual ACM-SIAM Symposium on Discrete Algorithms, pages 257–266, 2005.

- [7] A. Dasgupta, P. Drineas, B. Harb, R. Kumar, and M. W. Mahoney. Sampling algorithms and coresets for regression. SIAM Journal on Computing, (38):2060–2078, 2009.

- [8] D. Donoho and X. Huo. Uncertainty principles and ideal atomic decomposition. IEEE Transactions on Information Theory, 47:2845 – 2862, 2001.

- [9] D. Donoho and P. Stark. Uncertainty principles and signal recovery. SIAM Journal on Applied Mathematics, 49:906 – 931, 1989.

- [10] P. Drineas, M. Magdon-Ismail, M. W. Mahoney, and D. P. Woodruff. Fast approximation of matrix coherence and statistical leverage. In Proceedings of the 29th International Conference on Machine Learning, 2012.

- [11] P. Drineas, M. W. Mahoney, and S. Muthukrishnan. Relative-error CUR matrix decompositions. SIAM Journal on Matrix Analysis and Applications, 30:844–881, 2008.

- [12] P. Drineas, M. W. Mahoney, S. Muthukrishnan, and T. Sarlós. Faster least squares approximation. Numerische Mathematik, 117(2):219–249, 2010.

- [13] R. Gribonval and M. Nielsen. Sparse representations in unions of bases. IEEE Transactions on Information Theory, 49:3320–3325, 2003.

- [14] M. Gu and S. C. Eisenstat. A stable and efficient algorithm for the rank-one modification of the symmetric eigenproblem. SIAM Journal on Matrix Analysis and Applications, 15(4):1266–1276, 1994.

- [15] P. Indyk. Stable distributions, pseudorandom generators, embeddings, and data stream computation. Journal of the ACM, 53(3):307–323, 2006.

- [16] P. Indyk. Uncertainty principles, extractors, and explicit embeddings of into . In Proceedings of the 39th Annual ACM Symposium on Theory of Computing, pages 615–620, 2007.

- [17] F. John. Extremum problems with inequalities as subsidiary conditions. In Studies and Essays presented to R. Courant on his 60th Birthday, pages 187–204. 1948.

- [18] D. M. Kane and J. Nelson. Sparser Johnson-Lindenstrauss transforms. In Proceedings of the 23rd Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1195–1206, 2012.

- [19] L. Lovász. Algorithmic Theory of Numbers, Graphs, and Convexity. CBMS-NSF Regional Conference Series in Applied Mathematics 50. SIAM, Philadelphia, 1986.

- [20] M. W. Mahoney. Randomized algorithms for matrices and data. Foundations and Trends in Machine Learning. NOW Publishers, Boston, 2011. Also available at: arXiv:1104.5557.

- [21] M. W. Mahoney and P. Drineas. CUR matrix decompositions for improved data analysis. Proc. Natl. Acad. Sci. USA, 106:697–702, 2009.

- [22] A. Maurer. A bound on the deviation probability for sums of non-negative random variables. Journal of Inequalities in Pure and Applied Mathematics, 4(1):Article 15, 2003.

- [23] P. Paschou, J. Lewis, A. Javed, and P. Drineas. Ancestry informative markers for fine-scale individual assignment to worldwide populations. Journal of Medical Genetics, page doi:10.1136/jmg.2010.078212, 2010.

- [24] C. Sohler and D. P. Woodruff. Subspace embeddings for the -norm with applications. In Proceedings of the 43rd Annual ACM Symposium on Theory of Computing, pages 755–764, 2011.

- [25] M. J. Todd. On minimum volume ellipsoids containing part of a given ellipsoid. Mathematics of Operations Research, 7(2):253–261, 1982.

- [26] A. Torralba, R. Fergus, and W. T. Freeman. 80 million tiny images: A large data set for nonparametric object and scene recognition. IEEE Transactions on Pattern Analysis and Machine Intelligence, 30(11):1958–1970, 2008.

- [27] J. A. Tropp. Topics in Sparse Approximation. PhD thesis, UT-Austin, 2004.

- [28] J. A. Tropp. Improved analysis of the subsampled randomized Hadamard transform. Adv. Adapt. Data Anal., 3(1-2):115–126, 2011.

Appendix A Proofs of Technical Cauchy Lemmas

A.1 Proof of Lemma 3 (Cauchy Upper Tail Inequality)

The proof uses similar techniques to the bounds due to Indyk [15] for sums of independent clipped half-Cauchy random variables. Fix (we will choose later) and define the events

and . Note that . Using the pdf of a Cauchy and because , we have that:

By a union bound, . Further, , hence . We now bound . First, observe that

Next, since , we have that

Finally, by using the pdf of a Cauchy, , and so

We conclude that

By Markov’s inequality and because , we have:

The result follows by setting .

A.2 Proof of Lemma 4 (Cauchy Lower Tail Inequality)

To bound the lower tail, we will use Lemma 1. By homogeneity, it suffices to prove the result for . Let . Clearly and so defining , we have that and . Thus, we have that

where the last step holds by Lemma 1 for . Using the distribution of the half-Cauchy, one can verify using standard techniques that by choosing , and , so and . It follows that and the result follows.

A.3 Proof of Lemma 5 ( Sampling Lemma)

First, observe that , and since , . Next, observe that

because when , that row must be sampled, and so does not contribute to the deviation. So, we only need to analyze the RHS of the above equation. From now on, we only consider those with , in which case , where . Let be the (positive) random variable ; either or

where we defined . We can also obtain a bound for :

where, in the last inequality, we used the upper bound for and we further upper bounded by summing over all . Let with ; the standard Bernstein bound states that

Plugging in our bounds for and , we deduce that

The lemma follows after some simple algebraic manipulations.

Appendix B Proof of Theorem 1 (Fast Cauchy Transform (FCT1))

Preliminaries.

Before presenting the proof, we describe the main idea. It follows a similar line of reasoning to [24], and it uses an “uncertainty principle” (which we state as Lemma 7 below).

The uncertainty principle we prove follows from the fact that the concatenation of the Hadamard matrix with the identity matrix is a dictionary of low coherence. For background, and similar arguments to those we use in Lemma 7 below, see Section 4 of [16]. In particular, see Claim 4.1 and Lemma 4.2 of that section.

To prove the upper bound, we use the existence of a -conditioned basis and apply to this basis to show that cannot expand too much, which in turn means that cannot expand too much (for any ). To prove the lower bound, we show that the inequality holds with exponentially high probability, for a particular ; and we then use a suitable -net to obtain the result for all .

Main Proof.

We now proceed with the proof of Theorem 1. We will first prove an upper bound (Proposition 1) and then a lower bound (Proposition 2); the theorem follows by combining Propositions 1 and 2.

Proposition 1.

With probability at least , for all , , where .

Proof.

Let be a -conditioned basis (see Definition 2 below) for the column space of , which implies that for some we can write . Since if and only if , it suffices to prove the proposition for . By construction of , for any , , and so

Thus it is enough to show that . We have

where . We will need bounds for for , and . For any vector , we represent by its blocks of size , so and . Recall that , and observe that . By explicit calculation,

Since , it follows that

Applying this to for yields

| (5) |

since because is -conditioned.

The entry of is which is a Cauchy scaled by . So,

where are dependent Cauchy random variables. Using , we obtain:

Hence, we can apply Lemma 3 with and to obtain

Setting the RHS to , it suffices that . Thus, with probability at least ,

∎

Before we prove the lower bound, we need the following lemma which is derived using a sparsity result for matrices with unit norm rows and low “coherence,” as measured by the maximum magnitude of the inner product between distinct rows ( is a matrix with low coherence). This result mimics results in [9, 8, 13, 27, 16].

Lemma 7.

For and any , .

Proof.

We can assume , and so . Let be rows of , with of them coming from and from . where is a symmetric block matrix where the entries in are , and so .

Now, given any , we set with , and choose to be the rows corresponding to the components of having largest magnitude, with being the rows with indices in . Then , and so the entry in with smallest magnitude has magnitude at most . We now consider . Since , ; further, all components have magnitude at most (as all the components of have smaller magnitude than those of ). is minimized by concentrating all the entries into as few components as possible. Since the number of non-zero components is at least , giving these entries the maximum possible magnitude results in

(where we used ). We are done because ∎

We now prove the lower bound. We assume that Proposition 1 holds for , which is true with probability at least for as defined in Proposition 1. Then, by a union bound, both Propositions 1 and 2 hold with probability at least

( and are from Proposition 1). Since , by choosing for large enough , the final probability of failure is at most , because .

Proposition 2.

Proof.

First we will show a result for fixed , summarized in the next lemma.

Lemma 8.

Given this lemma, the proposition follows by putting a -net on the range of (observe that the range of has dimension at most ). This argument follows the same line as in Sections 3 and 4 of [24]. Specifically, let be any fixed (at most) dimensional subspace of (in our case, is the range of ). Consider the -net on with cubes of side . There are such cubes required to cover the hyper-cube ; and, for any two points inside the same -cube, . From each of the -cubes, select a fixed representative point which we will generically refer to as ; select the representative to have if possible. By a union bound and Lemma 8,

We will thus condition on the high probability event that for all . For any with , let denote the representative point for the cube in which resides ( as well). Then .

where the last inequality holds using Proposition 1. By choosing and recalling that , we have that , with probability at least

All that remains is to prove Lemma 8. As in the proof of Proposition 1, we represent any vector by its blocks of size , so and . Let ,

We have that , and

We conclude that , which intuitively means that is “spread out.” We now analyze . (Recall that , where ).

is a Cauchy random variable scaled by . Further, because each column of has exactly one non-zero element, the for are independent. Thus, the random variables and have the same distribution. To apply Lemma 4, we need to bound and . First,

where the last inequality is because is a standard basis vector. To bound , we will show that is nearly uniform. Since is a weighted sum of independent Bernoulli random variables (because and are independent for ), we can use Lemma 2 with and , and so and ; setting in Lemma 2:

By a union bound, none of the exceed with probability at most . We assume this high probability event, in which case . We can now apply Lemma 4 with and to obtain

By a union bound, with probability at least . Scaling both sides by gives the lemma. ∎

Running Time.

The running time follows from the time to compute the product for a Hadamard matrix , which is time. The time to compute is dominated by computations of , which is a total of time. Since is diagonal, pre-multiplying by is and further pre-multiplying by takes time , the number of non-zero elements in (which is ). Thus the total time is as desired.

Appendix C Proof of Theorem 2 (Fast Cauchy Transform (FCT2))

Preliminaries.

We will need results from prior work, which we paraphrase in our notation.

Definition 7 (Definition 2.1 of [2]).

For , a distribution on real matrices has the Manhattan Johnson-Lindenstrauss property (MJLP) if for any (fixed) vector , the inequalities

holds with probability at least (w.r.t. ), for global constants .

Remark. This is the standard Johnson-Lindenstrauss property with the additional requirement on . Essentially it says that is a nearly uniform, so that .

Lemma 9 (Theorem 2.2 of [2]).

Let be an arbitrarily small constant. For any satisfying , there exists an algorithm that constructs a random matrix that is sampled from an MJLP distribution with . Further, the time to compute for any is .

We will need these lemmas to get a result for how an arbitrary subspace behaves under the action of , extending Lemma 9 to every , not just a fixed . In the next lemma, the 2-norm bound can be derived using Lemma 9 (above) and Theorem 19 of [18] by placing a -net on and bounding the size of this -net. (See Lemma 4 of [3].) The Manhattan norm bound is then derived using a second -net argument together with an application of the 2-norm bound. The constants and in this lemma are from Definition 7; and the in Lemmas 9 and 10, with the constants and from Definition 7, is the same used in our FCT2 construction for . We present the complete proof of Lemma 10 in Appendix J.

Lemma 10.

Let be any (fixed) dimensional subspace of , and an matrix sampled from a distribution having the MJLP property. Given , let . Then, with probability at least , for every ,

We also need a result on how the matrix of Cauchy random variables behaves when it hits a vector . The next theorem is Theorem 5 of [24]. For completeness and also to fix some minor errors in the proof of [24], we give a proof of Theorem 12 in Appendix I.

Theorem 12.

Let be an arbitrary (fixed) subspace of having dimension at most , and an matrix of i.i.d. Cauchy random variables with for large enough constant . Then, with probability at least , and for all ,

where .

Note that for fixed to some small error probability, , and the product in the theorem above can be computed in time

Main Proof.