Vine Constructions of Lévy Copulas

Abstract

Lévy copulas are the most general concept to capture jump dependence in multivariate Lévy processes. They translate the intuition and many features of the copula concept into a time series setting. A challenge faced by both, distributional and Lévy copulas, is to find flexible but still applicable models for higher dimensions. To overcome this problem, the concept of pair copula constructions has been successfully applied to distributional copulas. In this paper, we develop the pair construction for Lévy copulas (PLCC). Similar to pair constructions of distributional copulas, the pair construction of a -dimensional Lévy copula consists of bivariate dependence functions. We show that only of these bivariate functions are Lévy copulas, whereas the remaining functions are distributional copulas. Since there are no restrictions concerning the choice of the copulas, the proposed pair construction adds the desired flexibility to Lévy copula models. We discuss estimation and simulation in detail and apply the pair construction in a simulation study.

keywords:

Lévy Copula , Vine Copula , Pair Lévy Copula Construction , Multivariate Lévy ProcessesMSC:

[2010] 60G51 , 62H991 Introduction

Many financial and nonfinancial applications need multivariate models with jumps where the dependence of the jumps is captured adequately. To this end, Lévy processes have been applied in the literature. However, although the recently introduced concept of Lévy copulas enables modeling the dependence in Lévy processes in a multivariate setup, known parametric Lévy copulas are very inflexible in higher dimensions, i.e., they consist of very few parameters. In this paper, we show that, similar to the pair copula construction of distributional copulas going back to Joe [13], Lévy copulas may be constructed from a constellation of parametric bivariate dependence functions. Because these dependence functions may be chosen arbitrarily, the resulting Lévy copulas flexibly capture various dependence structures.

Lévy processes are stochastic processes with independent increments. They consist of a Brownian motion part and jumps. Due to the jumps, Lévy processes capture stylized facts observed in financial data as non-normality, excessive skewness, and kurtosis (see, e.g., Johannes [14]). At the same time, they stay mathematically tractable and allow for derivative pricing by change of measure theory. For these reasons, intensive research is conducted on the statistical inference of Lévy processes (see, e.g., Lee and Hannig [18] and the references therein).

The fundamental work for multivariate applications of Lévy processes is the seminal paper of Kallsen and Tankov [16], where the concept of Lévy copulas is introduced. This concept transfers the idea of distributional copulas to the context of Lévy processes. Distributional copulas (normally just referred to as copulas) are functions which connect the marginal distribution functions of random variables to their joint distribution function. They contain the entire dependence information of the random variables (see, e.g., Nelsen [19] for an introduction to copulas). In the same sense, the theory of Lévy copulas enables to model multivariate Lévy processes by their marginal Lévy processes and to choose a suitable Lévy copula for the dependence structure separately. For papers regarding the estimation of Lévy copulas in multivariate Lévy processes and applications see, e.g., the recent papers of Esmaeili and Klüppelberg [9, 10, 11] and references therein.

All papers involving Lévy copulas focus on rather small dimensions since higher-dimensional flexible Lévy copulas are difficult to construct. A similar effect has been observed during the first years of literature on distributional copulas, where mainly -dimensional distributional copulas have been analyzed. One solution regarding distributional copulas has been the development of very flexible pair constructions of copulas going back to Joe [13] and further developed in a series of papers (see, e.g., Bedford and Cooke [5] or Aas et al. [1]). In pair copula constructions, a -dimensional copula is constructed from bivariate copulas. Here, of the bivariate copulas model the dependence of bivariate margins, whereas the remaining bivariate copulas model certain conditional distributions, such that the entire -dimensional dependence structure is specified.

Lévy copulas are conceptually different from distributional copulas. While -dimensional distributional copulas are distribution functions on a hypercube, -dimensional Lévy copulas are defined on and relate to Radon measures. Therefore, the idea of pair constructions for copulas is not directly transferable to Lévy copulas and up to now it has not been clear whether it is possible at all. In this paper, we show that a pair copula construction of Lévy copulas (PLCC) is indeed possible. It also consists of bivariate dependence functions but only of them are Lévy copulas, while the remaining ones are distributional copulas. For statistical inference, we derive sequential maximum likelihood estimators for an arbitrary pair construction of Lévy copulas as well as a simulation algorithm. We analyze the applicability of the concept in a simulation study. The estimation and simulation algorithms show encouraging results in a finite sample setting.

The remainder of the paper is structured as follows. In Section 2.1, we review the theory of copulas for random variables and pair copula constructions of such copulas. In Section 2.2, we address the theory of Lévy processes and Lévy copulas. Our pair construction of Lévy copulas is derived in Section 3. In Section 4, we provide simulation as well as maximum likelihood estimation methods. Section 5 contains simulation studies probing the simulation and estimation algorithms in finite samples and Section 6 concludes.

2 Preliminaries

In this section, we briefly recall necessary theory on copulas, pair copulas, Lévy processes, and the Lévy copula concept.

2.1 Copulas and Pair Copula Construction

Let be a random vector with joint distribution function and continuous marginal distribution functions , . The copula of is the uniquely defined distribution function with domain and uniformly distributed margins satisfying

By coupling the marginal distribution functions to the joint one, the copula entirely determines the dependence of the random variables While many -dimensional parametric families of copulas exist, see, e.g., Nelsen [19], the families for the -dimensional case suffer from lack of flexibility. To overcome this problem, the concept of pair copula construction has been developed (see, e.g., Joe [13] for the seminal work or the detailed introductions in Aas et al. [1], Bedford and Cooke [5], and Berg and Aas [7]). In a pair copula construction, a -dimensional copula is constructed of bivariate copulas. Of these bivariate copulas, bivariate copulas directly model -dimensional margins of the copula , whereas the other bivariate copulas indirectly specify the remaining parts in terms of conditional distributions. Since the number of possible combinations grows rapidly with the dimension, Bedford and Cooke [5, 6] introduced a graphical model, called regular vines (R-vines), to describe the structures of pair copula constructions.

[colsep=1.5cm,rowsep=0.8cm] T1&

An example of a regular vine for the 3-dimensional case is given in Figure 1. It shows three dimensions (labeled 1,2 and 3) and two trees (labeled T1 and T2) of dependence functions. The first tree (T1) contains the two bivariate copulas, and modeling the dependence between dimensions 1 and 2 and dimensions 2 and 3, respectively. Thus, tree T1 completely determines these two bivariate dependence structures. It also indirectly determines parts of the dependence between dimensions 1 and 3, but not necessarily the entire dependence. For instance, if the pairs 1,2 and 2,3 are each correlated with 0.9, then 1 and 3 cannot be independent but their exact dependence is not specified. In particular, the conditional dependence of 1 and 3 given 2 is not specified. Therefore, in the second tree (T2), this bivariate conditional dependence is modeled with another copula, Together, the three bivariate copulas fully specify the dependence of the three dimensions. Since the choice of all three bivariate copulas is arbitrary, the vine structure provides a very flexible way to construct multidimensional copulas. In the -dimensional case, bivariate copulas are needed and arranged in trees (see, e.g., Joe [13]). There are special cases of regular vines, e.g., C-vines or D-vines (see, e.g., Aas et al. [1] for a more detailed introduction).

2.2 Lévy Processes and Lévy Copulas

Detailed information about Lévy processes may be found in Rosinski [20], Kallenberg [15] or Sato [21]. Introductions to Lévy copulas are given in Kallsen and Tankov [16] or Cont and Tankov [8]. Here, we give a very short overview of both.

Let be a probability space. A Lévy process is a stochastic process with stationary, independent increments starting at zero. Lévy processes can be decomposed into a deterministic drift function, a Brownian motion part and a pure jump process with a possibly infinite number of small jumps, see, e.g., Kallenberg [15], Theorem 15.4 (Lévy Itô decomposition). In this paper, we focus on spectrally positive Lévy processes, which are Lévy processes with positive jumps only. This facilitates the notation considerably and in many relevant cases it is sufficient to consider positive jumps only. However, all results of the paper may be extended to the general case. The characteristic function of the distribution of such an -valued spectrally positive Lévy process , at time , is given by the Lévy-Khinchin representation (see Kallenberg [15])

| (1) |

Here, corresponds to the drift part of the process and is the covariance matrix of the Brownian motion part at time The Lévy measure is a measure on which is concentrated on the positive domain with The Lévy measure completely characterizes the jump parts of the Lévy process, where for is the expected number of jumps per unit of time with jump sizes in A spectrally positive Lévy process with positive entrees of and is called subordinator. It has no negative increments.

An interesting example for a one-dimensional subordinator is the stable subordinator. It is heavy tailed and therefore suggested as a loss process for operational risk models. In Basawa and Brockwell [3], the Lévy measure of a stable subordinator on is defined by

where and .

Related to the Lévy measure, its tail integral is defined by (see, e.g., Definition 3.1 in Esmaeili and Klüppelberg [9])

The tail integral of a spectrally positive Lévy process uniquely determines its Lévy measure . We define the marginal tail integrals for any dimension of the multivariate Lévy process in a similar way. For one-dimensional spectrally positive Levy measures the tail integral is i.e., the expected number of jumps per unit of time with jump sizes larger or equal to For the one-dimensional stable subordinator, the tail integral can be explicitly calculated and inverted for ,

The inverse of the tail integral is needed for the simulation of the process.

Dependence of jumps of a multivariate Lévy process can be described by a Lévy copula which couples the marginal tail integrals to the joint one. A -dimensional Lévy copula is a measure defining function with margins for all and In particular, let denote the tail integral of a spectrally positive -dimensional Lévy process whose components have the tail integrals . Then, there exists a Lévy copula such that for all

| (2) |

Conversely, if is a Lévy copula and are marginal tail integrals of spectrally positive Lévy processes, Equation (2) defines the tail integral of a -dimensional spectrally positive Lévy process and are the tail integrals of its components. Both statements are often called the Sklar’s theorem for Lévy copulas and are proved, e.g, in Cont and Tankov [8].

In this paper, we focus on Lévy copulas for which the following assumption holds.

Assumption 1.

Let be a Lévy copula such that for every nonempty,

| (3) |

This is a rather weak assumption on the Lévy copula and is assumed in many papers, e.g., in Tankov [22]. It means that the Lévy copula has no new information at the points which is not already contained in the limit for We need it since it ensures a bijection between a Lévy copula on and a positive measure on with one-dimensional Lebesgue margins. This measure is given by

| (4) |

where with , component-wise, and refers to the -volume of the -box which is defined as

The sum is taken over all vertices of and

Furthermore, any positive measure on with Lebesgue margins uniquely defines a Lévy copula on that satisfies Assumption 1 by

and by setting

These results are proved, e.g., in Section 4.5 in Kingman and Taylor [17].

An example for a Lévy copula which is used later in the paper is the Clayton Lévy copula. For spectrally positive, 2-dimensional Lévy processes it is given on by

| (5) |

Here, determines the dependence of the jump sizes, where larger values of indicate a stronger dependence.

3 Pair Lévy Copulas

In this section, we present the pair construction of -dimensional Lévy copulas. In particular, we show that analogously to the pair construction of distributional copulas, functions of bivariate dependence may be arranged such that they define a -dimensional Lévy copula. In Sections 3.2 and 3.3, we provide illustrating examples how to construct multivariate pair Lévy copula constructions. Readers not interested in the technical parts may read these examples first.

3.1 Technical Part

The central theorem for the construction is Theorem 6. It states that two -dimensional Lévy copulas with overlapping -dimensional margins may be coupled to an -dimensional Lévy copula by a new, -dimensional distributional copula. Ensured by vine constructions (see Bedford and Cooke [6]) and starting at Theorem 6 therefore enables to sequentially construct Lévy copulas out of -dimensional dependence functions, i.e., -dimensional distributional copulas and Lévy copulas. Before we state the theorem, for convenience, we recall some definitions which can be found, e.g., in Ambrosio et al. [2].

Definition 1.

A positive measure on that is finite on compact sets is called a positive Radon measure.

Let and be measure spaces and let be a measurable function. For any measure on , we define the Push Forward Measure in by

Let be a positive Radon measure on and a function which assigns a finite Radon measure on to each . We say this map is -measurable if is -measurable for any .

Definition 2 (Generalized Product).

Let be a positive Radon measure on and a -measurable function which assigns a probability measure on to each . We denote by the Radon measure on defined by

where is any compact set.

We also need a theorem which states that a Radon measure may be decomposed into a a projection onto some of its dimensions and a probability measure. For a proof see Theorem 2.28 in Ambrosio et al. [2] and also the sentence after Corollary 2.29 there.

Theorem 1 (Disintegration).

Let be a Radon measure on , the projection on the first variables and . Let us assume that is a positive Radon measure, i.e., that for any compact set . Then, there exists a finite measure in such that is -measurable, is a probability measure almost everywhere in , and

this is for any where is any compact set.

We are now able to state the main theorem.

Theorem 2 (Pair Lévy Copula Composition).

Let and be two Lévy copulas on where is a Lévy copula on the variables and is a Lévy copula on the variables . Denote the corresponding measures on by and , respectively. Suppose that the two measures have an identical -dimensional margin on the variables .

Then, we can define a Lévy copula on by

where is the one-dimensional distribution function corresponding to the probability measure from the decomposition of into

is the one-dimensional distribution function corresponding to the probability measure from the decomposition of into

and is a distributional copula. Since Lévy copulas are functions on , we set for every nonempty,

| (6) |

The theorem, which is proved in the appendix, illustrates how to construct a -dimensional Lévy copula from two -dimensional Lévy copulas with a common margin. Applying the theorem recursively, these -dimensional Lévy copulas can be constructed from -dimensional ones. This can be repeated down to construct -dimensional Lévy copulas from bivariate ones. In higher dimensions, there are many ways for this procedure due to possible permutations of the dimensions and numerous possible pairwise combinations within the trees. The graphical visualization of the different resulting structures of pair construction is possibly by the concept of regular vines as developed in Bedford and Cooke [6]. Regular vines also help to construct pair Lévy copulas top-down. This means to start with bivariate Lévy copulas and to combine them successively to -dimensional Lévy copulas. The regular vine approach ensures that at each step the involved Lévy copulas have sufficiently overlapping margins, and that therefore the theorem can be applied. To illustrate this procedure, we give two detailed examples. The first example refers to the most simple case, a -dimensional Lévy copula. The second, 4-dimensional example then illustrates how to sequentially add dimensions to the pair copula construction.

3.2 Example: 3-dimensional Pair Lévy Copula Construction

A 3-dimensional example can be constructed applying Theorem 6 to combine two 2-dimensional Lévy copulas by a distributional copula. As in the usual pair copula construction for distributional copulas, in Figure 2 we use the vine concept to visualize the resulting dependence structure.

[colsep=1.5cm,rowsep=0.8cm] T1&

The bivariate dependence structures in the first tree are Lévy copulas, whereas the copula in the second tree is a distributional copula. From Theorem 6 follows that

is a Lévy copula, where is the one-dimensional distribution function corresponding to the probability measure from the decomposition of into

| (7) |

and is the one-dimensional distribution function corresponding to the probability measure from the decomposition of into

| (8) |

Remember that is the Radon measure corresponding to With Theorem 1 and the considerations after Assumption 1 we see that in Equation (7) is the Lebesgue measure. Analogously, is the Radon measure corresponding to and therefore in Equation (8) is the Lebesgue measure as well.

To check whether has the desired margins, we calculate

A similar procedure shows that

As expected, we do not get such a direct representation of the third bivariate margin

because this margin is not only influenced by the distributional copula but also by and . However, we can adjust the bivariate margin of the first and third dimension by changing without affecting the other two bivariate margins.

3.3 Example: 4-dimensional Pair Lévy Copula Construction

Considering dimensions, we need two -dimensional Lévy copulas with an identical -dimensional margin. Here, we reuse the Lévy copula from Example 3.2 for the first three dimensions. The second -dimensional Lévy copula is constructed in the same way and has the vine representation shown in Figure 3.

[colsep=1.5cm,rowsep=0.8cm] T1&

[colsep=1.4cm,rowsep=0.8cm] T1&

Notice that the Lévy copula is used in both -dimensional pair Lévy copulas. Therefore, the marginal Lévy copulas

are the same and we can apply Theorem 6 to construct a -dimensional Lévy copula with the vine representation shown in Figure 4 and

where is the one-dimensional distribution function corresponding to the probability measure from the decomposition of from the first pair Lévy copula into

The one-dimensional distribution function corresponds to the probability measure from the decomposition of from the second pair Lévy copula into

4 Simulation and Estimation

In this section we discuss the simulation of multivariate Lévy processes as well as the maximum likelihood estimation of the pair Lévy copula. We need the following assumption which is fulfilled by the common parametric families of the bivariate (Lévy) copulas.

Assumption 2.

In the following, we assume that all bivariate distributional and Lévy copulas are continuously differentiable.

4.1 Simulation

The simulation of multivariate Lévy processes built upon Lévy copulas bases on a series representation for Lévy processes and the following theorem.

Theorem 3.

Let be a Lévy measure on , satisfying , with marginal tail integrals , , Lévy copula with corresponding measure . Let be a sequence of independent and uniformly distributed random variables and be a Poisson point process on with intensity measure from the decomposition of

with being a probability measure. For any value of , we suppose that is a random variable with probability measure . Then, the process defined by

is a -dimensional Lévy process without a Brownian component and drift. The Lévy measure of is .

Proof: The proof is similar to the proof of Tankov [22], Theorem 4.3.

In practical simulations, the sum cannot be evaluated up to infinity and one omits very small jumps. The sequence is therefore only simulated up to a sufficiently large resulting in a large value of (see Rosinski [20] for this approximation). Note that large values of correspond to small values of the jumps , since the tail integral is decreasing.

Based on the pair copula construction of the Lévy copula, can be drawn conditionally on in a sequential way. For convenience, assume that the pair Lévy copula has a D-vine structure and that the dimensions are ordered from left to right. The dependence between and is then determined in the first tree of the pair construction by the bivariate Lévy copula , and the distribution function of given is derived in the following Proposition.

Proposition 1.

Let be a 2-dimensional Lévy copula with corresponding measure . Then, we can decompose

where is a probability measure and the distribution function for almost all is given by

Proof: This is a special case of Tankov [22], Lemma 4.2.

Inverting this distribution function allows the simulation of Now suppose that we have already simulated the variables , and we want to simulate the last variable We already know from Theorem 1 that the distribution of the last variable, given the first , is a specific probability distribution and therefore we are interested in the corresponding distribution function . Having found , we can again invert it and easily simulate a realization of a random variable with this distribution function. The next proposition provides within the pair construction of the Lévy copula.

Proposition 2.

Let and be a pair Lévy copula, the corresponding measure, the projection on the first variables, and the push forward measure. Then, we can decompose

where is a probability measure on with distribution function

-almost everywhere. Moreover, is continuously differentiable.

The proposition is proved in the appendix. Similar to Aas et al. [1], it shows how we can iteratively evaluate and invert the distribution function .

4.2 Maximum Likelihood Estimation

It is usually not possible to track Lévy processes in continuous time. Therefore, we have to choose a more realistic observation scheme. In the context of inference for pure jump Lévy processes, a common assumption is that it is possible to observe all jumps of the processes larger than a given (see, e.g., Basawa and Brockwell (1978, 1980) [3, 4] or Esmaeili and Klüppelberg [9]).

Following Esmaeili and Klüppelberg [11], we estimate the marginal Lévy processes separately from the dependence structure. That is, we use all observations with jumps larger than in a certain dimension and estimate the parameters of the one-dimensional Lévy process.

For the estimation of the dependence structure, i.e., the Lévy copula, we can use the fact that the process consisting of all jumps larger than in all dimensions is a compound Poisson process. We suppose that all densities of the marginal Lévy measures exist and we denote the parameter vectors of the Lévy copula and the marginal Lévy measures by , respectively. The likelihood function is given by

where , is the number of observed jumps, and is the density of . This result also holds for -dimensional marginal Lévy processes with and is stated in Esmaeili and Klüppelberg [10] for two dimensions.

A straightforward estimation approach would be maximizing the full likelihood function to estimate the dependence structure. This, however, is disadvantageous because of two reasons. The first reason is a numerical one. The likelihood function is not easy to evaluate if more than one parameter is unknown. The second reason is more conceptual. Since we can only use jumps larger than in all dimensions, we waste a tremendous part of the information about the dependence structure, especially if the dependence structure is weak. For weak dependence structures, the probability that two jumps are both larger than a threshold (conditioned that at least one jump exceeds the threshold) is lower than for strong dependence.

For both reasons, we estimate the parameters of the bivariate Lévy and distributional copulas of the vine structure sequentially. This is also common for pair copula constructions of distributional copulas (see, e.g., Hobæk Haff [12]). We make use of the estimated marginal parameters and start in the first tree, using all observations larger than in the first and second components to estimate the parameters of . We continue this procedure for all other Lévy copulas in the first tree. To estimate the parameter of , we use all observations larger than in dimensions one, two, and three, as well as the previously estimated marginal parameters of the first three dimensions and the parameters of and . This means that we proceed tree by tree and within the tree, copula by copula or Lévy copula by Lévy copula, respectively. In each step, we make use of the estimated parameters from the preceding steps.

To use the above likelihood for pair Lévy copula constructions, we have to know how to calculate the density of a pair Lévy copula.

Proposition 3.

Let be a pair Lévy copula of the following form

and the corresponding measure and suppose that the density of exists. Then the density of exists as well and has the form

This proposition is proved in the appendix and states that we can iteratively decompose the pair Lévy copula into bivariate building blocks and therefore evaluate the density function in an efficient manner.

In contrast to the computation of the density of the pair Lévy copula, it is not easy to evaluate a higher dimensional pair Lévy copula itself. This is no real drawback, since the value of is not needed in most cases. For the normalizing constant of the likelihood, however, has to be evaluated. For this step, we apply Monte Carlo methods. The code may be obtained from the authors on request, so that for convenience, we omit the details here.

5 Simulation Study

In order to evaluate the estimators, we conduct a simulation study with a -dimensional PLCC. To make the results comparable, all marginal Lévy processes are chosen to be stable Lévy processes with parameters and all bivariate Lévy copulas in the first tree are Clayton Lévy copulas (see Equation (5)) with parameter . The distributional copulas in the higher trees are all Gaussian copulas, i.e.,

where is the distribution function of the bivariate normal distribution with correlation parameter and the quantile function of the standard normal distribution.

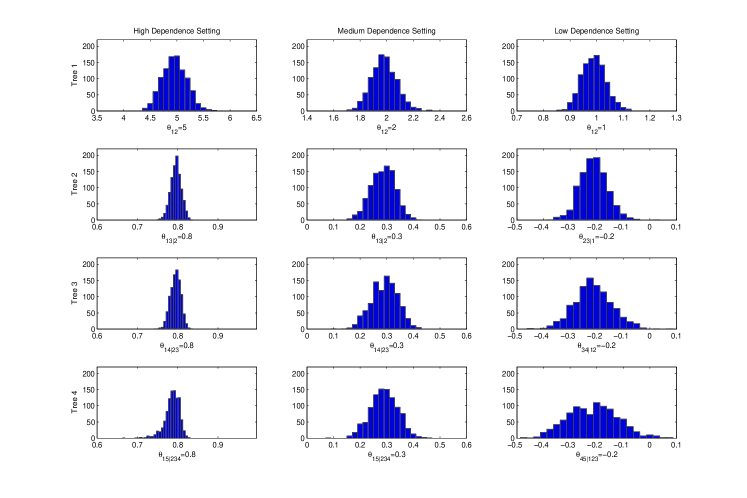

We analyze three different scenarios of dependence structures: high dependence (H), medium dependence (M) and low dependence (L). In scenarios H and M, we choose a D-vine structure of the PLCC, in scenario L a C-vine as it is numerically more appropriate for low dependencies. The D-vine structure refers to a structure where all dimensions in the lowest tree form a line and are each connected to the nearest neighbors, whereas the dimensions in a C-vine structure are connected to only one central dimension (see, e.g., Aas et al. [1]). Within a scenario, all Clayton Lévy copulas have the same parameter and all Gaussian copulas have the same parameter . The parameter values are summarized in Table 1.

| Scenario | Clayton Parameters | Gaussian Parameters |

|---|---|---|

| High dependence (H) | 5 | 0.8 |

| Medium dependence (M) | 2 | 0.3 |

| Low dependence (L) | 1 | -0.2 |

For each scenario, we simulate a realization of a 5-dimensional Lévy process over a time horizon . We then estimate the parameters of the process from the simulated data using our estimation approach. We choose two different thresholds and for jump sizes we can observe, i.e., we neglect jumps smaller than or respectively. Each simulation/estimation step is repeated 1000 times. The estimation results are reported in Tables 2 and 3. Shown are the true values of the parameters, the mean of the estimates of the 1000 repetitions and resulting estimates for bias and root mean square error (RMSE). Since the parameters in the different trees rely on different numbers of observation (the higher the tree, the more dimensions have to exceed the threshold at the same time) we also report the mean numbers of available jumps per tree.

Comparing the two tables, we see that the lower threshold leads to a higher number of jumps. We also find that weaker dependence leads to less co-jumps available for the estimation of higher trees than a stronger dependence. In all cases, the bias is very small. We find, however, that the RMSE is affected by the number of jumps available in certain trees as it increases with decreasing number of jumps. This effect is illustrated in Figure 5 in terms of histograms of the estimates.

| Tree | # Jumps | True Value | Mean | Bias | RMSE | |

|---|---|---|---|---|---|---|

| High Dep. | 1 | 870.61 | 5 | 5.0038 | ||

| 2 | 833.51 | 0.8 | 0.7987 | |||

| 3 | 814.39 | 0.8 | 0.7980 | |||

| 4 | 798.46 | 0.8 | 0.7890 | |||

| Med. Dep. | 1 | 707.18 | 2 | 2.0010 | ||

| 2 | 573.56 | 0.3 | 0.2983 | |||

| 3 | 498.45 | 0.3 | 0.2983 | |||

| 4 | 451.69 | 0.3 | 0.3001 | |||

| Low Dep. | 1 | 500.10 | 1 | 1.0016 | ||

| 2 | 267.36 | -0.2 | -0.1987 | |||

| 3 | 163.22 | -0.2 | -0.1992 | |||

| 4 | 113.91 | -0.2 | -0.2004 |

| Tree | # Jumps | True Value | Mean | Bias | RMSE | |

|---|---|---|---|---|---|---|

| High Dep. | 1 | 87.26 | 5 | 5.0403 | ||

| 2 | 83.63 | 0.8 | 0.7933 | |||

| 3 | 81.69 | 0.8 | 0.7810 | |||

| 4 | 80.10 | 0.8 | 0.7086 | |||

| Med. Dep. | 1 | 70.82 | 2 | 2.0312 | ||

| 2 | 57.47 | 0.3 | 0.2970 | |||

| 3 | 50.00 | 0.3 | 0.2844 | |||

| 4 | 45.37 | 0.3 | 0.2797 | |||

| Low Dep. | 1 | 50.21 | 1 | 1.0246 | ||

| 2 | 26.88 | -0.2 | -0.2019 | |||

| 3 | 16.42 | -0.2 | -0.1859 | |||

| 4 | 11.47 | -0.2 | -0.1378 |

6 Conclusion

Lévy copulas determine the dependence of jumps of Lévy processes in a multivariate setting with arbitrary numbers of dimensions. In dimensions larger than two, however, known parametric Lévy copulas are inflexible. In this paper, we develop a multidimensional pair construction of Lévy copulas from 2-dimensional dependence functions which are either Lévy copulas or distributional copulas. The resulting parametric Lévy copula has the desired flexibility, since every regular vine and every bivariate (Lévy) copula can be used in the PLCC. Applications of the concept can be found in operational risk modeling or risk management of insurance companies. In both fields, Lévy copula models have been proposed but their applicability was limited to low-dimensional cases. The pair construction solves these limitations and opens the way to high-dimensional applications. In this paper, simulation and estimation methods are evaluated in a simulation study.

Appendix A Proof of Theorem 6

For the proof of Theorem 6, we need a lemma which we state first.

Lemma 1.

Let be a positive Radon measure on , and -measurable measure-valued maps, where and are probability measures on with corresponding distribution functions and . Let be a 2-dimensional distributional copula and let be the probability measure defined by the distribution function on . Then, the map is -measurable.

Proof: By definition, the maps and are -measurable for any . This holds in particular for the intervals . Therefore, the maps and are -measurable for any . By definition of we have

for any rectangle . Since is a copula, it is continuous and therefore measurable. We get that is a composition of -measurable functions and therefore -measurable for any rectangle . Now that we have shown that is -measurable for any , we use the same argumentation as in the proof of Ambrosio, Fusco, and Pallara [2], Proposition 2.6, to show that is -measurable for any . Note that the set of intervals is closed under finite intersection, it is a generator of the -algebra , and there exists a sequence of these intervals such that . Denote the family of Borel sets such that is -measurable by . Obviously, . In order to use Ambrosio et al. [2], Remark 1.9, we have to show that the following conditions hold:

-

1.

, ,

-

2.

,, ,

-

3.

.

This is already shown in the first part in the proof of Ambrosio, Fusco, and Pallara [2], Proposition 2.26.

Now we are able to prove Theorem 6.

We show that the integral is well-defined in the first step. From Theorem 1 follows that is -measurable. By the definition of measure-valued maps, is -measurable for any and especially for any . Therefore,

is -measurable. With the same arguments, we see immediately that is -measurable for any . Since every copula is continuous, we can use the same arguments as in the proof of Lemma 1 to show that

is -measurable and that the integral is well-defined. To show that is indeed a Lévy copula, we have to check the properties of Tankov [22], Definition 3.3. We start by showing that is -increasing. In a first step, we show this property for any -box where all vertices lie in . For every let be the probability measure on defined by the distribution function . With Lemma 1 we know that is -measurable. By definition of

holds, and therefore

Since is a positive and well-defined measure,

In the next step, we denote and show that the limit in Equation (6) exists for any nonempty, . First, suppose that . Since we say w.l.o.g. that . Since is non-decreasing in every component, it suffices to show that

to prove that the limes exists. We use the dominated convergence theorem (e.g. Ambrosio, Fusco, and Pallara [2], Theorem 1.21) and the fact that for every distributional copula holds. For the inequality, we use the fact that Assumption 1 holds for the Lévy copula . Now, suppose that at least one element of is not in . W.l.o.g. then we have

Now that we have shown that the limit exists, it follows immediately that is -increasing on . To show that the Lévy copula has Lebesgue margins, we can again use the same equations as before and replace “” by “=” since in this case and therefore we can directly use Assumption 1.

Appendix B Proof of Proposition 2

Suppose that and are continuously differentiable. For any rectangle we get by Theorem 1

By the definition of the pair Lévy copula we see that

and therefore

holds -almost everywhere. The fact that this result does not only hold for fixed values of but for all is already shown in the proof of Tankov [22], Lemma 4.2. Since , are continuously differentiable and C is by Assumption 2 also continuously differentiable, we get immediately that is differentiable and

is a composition of continuous functions and therefore continuous. Finally, all bivariate Lévy copulas are by Assumption 2 continuously differentiable and therefore, the proposition follows by complete induction.

Appendix C Proof of Proposition 3

This statement follows from the definition of the pair Lévy copula construction, since

as stated.

References

- [1] Kjersti Aas, Claudia Czado, Arnoldo Frigessi, and Henrik Bakken. Pair-copula constructions of multiple dependence. Insurance: Mathematics and Economics, 44(2):182–198, 2009.

- [2] Luigi Ambrosio, Nicola Fusco, and Diego Pallara. Functions of Bounded Variation and Free Discontinuity Problems. Oxford University Press, 2000.

- [3] I.V. Basawa and P.J. Brockwell. Inference for gamma and stable processes. Biometrika, 65(1):129–133, 1978.

- [4] I.V. Basawa and P.J. Brockwell. A note on estimation for gamma and stable processes. Biometrika, 67(1):234–236, 1980.

- [5] Tim Bedford and Roger M. Cooke. Probability density decomposition for conditionally dependent random variables modeled by vines. Annals of Mathematics and Artificial Intelligence, 32(1-4):245–268, 2001.

- [6] Tim Bedford and Roger M. Cooke. Vines: A new graphical model for dependent random variables. The Annals of Statistics, 30(4):1031–1068, 2002.

- [7] Daniel Berg and Kjersti Aas. Models for construction of multivariate dependence: A comparison study. The European Journal of Finance, 15(7):639–659, 2009.

- [8] R. Cont and P. Tankov. Financial modelling with jump processes. 2004.

- [9] Habib Esmaeili and Claudia Klüppelberg. Parameter estimation of a bivariate compound poisson process. Insurance: Mathematics and Economics, 47(2):224–233, 2010.

- [10] Habib Esmaeili and Claudia Klüppelberg. Parametric estimation of a bivariate stable Lévy process. Journal of Multivariate Analysis, 102(5):918–930, 2011.

- [11] Habib Esmaeili and Claudia Klüppelberg. Two-step estimation of a multivariate Lévy process. preprint, 2011.

- [12] Ingrid Hobæk Haff. Comparison of estimators for pair-copula constructions. Journal of Multivariate Analysis, forthcoming, 2012.

- [13] Harry Joe. Families of -variate distributions with given margins and bivariate dependence parameters. Distributions with Fixed Marginals and Related Topics, pages 120–141, 1996.

- [14] M. Johannes. The economic and statistical role of jumps in continuous-time interest rate models. The Journal of Finance, 59:227–260, 2004.

- [15] Olav Kallenberg. Foundation of Modern Probability. Springer, 2002.

- [16] Jan Kallsen and Peter Tankov. Characterization of dependence of multidimensional Lévy processes using Lévy copulas. Journal of Multivariate Analysis, 97:1551–1572, 2006.

- [17] John Kingman and Samuel J. Taylor. Introduction to measure and probability. Cambridge University Press, Cambridge, 1966.

- [18] Suzanne S. Lee and Jan Hannig. Detecting jumps from Lévy jump diffusion processes. Journal of Financial Economics, 96(2):271–290, 2010.

- [19] R.B. Nelsen. An Introduction to Copulas. Springer, New York, 2nd edition, 2006.

- [20] J. Rosinski. Lévy Processes – Theory and Applications. In: Series Representation of Lévy Processes from the Perspective of Point Processes. Birkhäuser, Boston, 2001.

- [21] Ken-Iti Sato. Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press, Cambridge, 1999.

- [22] Peter Tankov. Simulation and option pricing in Lévy copula models. Unpublished manuscript, 2005.