Asymptotic Joint Distribution of Extreme Eigenvalues of the Sample Covariance Matrix in the Spiked Population Model

Dai Shi111Institute of Computational and Mathematical Engineering, Stanford University, Stanford, 94305

Abstract

In this paper, we consider a data matrix where all the columns are i.i.d. samples being dimensional complex Gaussian of mean zero and covariance . Here the population matrix is of finite rank perturbation of the identity matrix. This is the “spiked population model” first proposed by Johnstone in [18]. As but , we first establish in this paper the asymptotic distribution of the smallest eigenvalue of the sample covariance matrix . It also exhibits a phase transition phenomenon proposed in [1] — the local fluctuation will be the generalized Tracy-Widom or the generalized Gaussian to be defined in the paper.

Moreover we prove that the largest and the smallest eigenvalue are asymptotically independent as .

Key Words: Spiked population model, asymptotic independence of the extreme eigenvalues

1 Introduction

Suppose we have independently and identically distributed samples , each of which is an dimensional complex-valued vector. Here is the sample size and is the dimension of our data. We can then form the data matrix and further define its sample covariance matrix

In this paper we are interested in the asymptotic joint distribution of the largest and the smallest eigenvalues of the matrix . Below is the assumptions of our model.

•

All the data vectors are independently and identically distributed following the complex Gaussian distribution of mean zero and covariance matrix . Here is a non-random positive definite matrix.

•

but their ratio is a fixed amount in the interval .

•

We denote to be the eigenvalues of the matrix . Then we assume that all of the ’s are equal to one except for only finite of them. That is, there exist fixed integers which are independent of such that

and

The model defined above is the (complex) “spiked population model” proposed in [18]. The unit eigenvalues represent pure noise, while the spiked eigenvalues represent true information. In real applications, we will encounter such models quite often. In mathematical imaging (see [21]), the observed spectrum of the sample covariance matrix indeed has some detached eigenvalues, representing the possible scatterers in the region. As another example, in mathematical finance (see [22]), each column of our data matrix represents the correlated return of each stock. The sample correlation matrix has some spiked large eigenvalues, representing the main factors driving the market, and some small eigenvalues, representing the linear dependence of these factors. Other possible applications include, but not restricted to, speech recognition (see [23]), physics mixture (see [24]) and statistical learning (see [25]).

We define as the eigenvalues of the sample covariance matrix , where . In the null case where , a lot of properties are known. The empirical measure of , denoted by , will almost surely converge in distribution to the Marčenko-Pastur law (see [10]), whose density is defined by

(1.1)

where and . The support of the density, , is often called the Marčenko-Pastur sea. Regarding the largest eigenvalue and the smallest eigenvalue of the sample covariance matrix , German first proved that almost surely in [11] and later Silvertein proved that almost surely in [12]. That is to say, the largest and the smallest eigenvalues will converge to the corresponding edges of the Marčenko-Pastur law. For a second order approximation, Johansson in [15] proved that , properly scaled and centered, will converge weakly to the Tracy-Widom law. Baker, Forrester and Pearce in [17] also proved the similar result for the smallest eigenvalue. More precisely, we have

(1.2)

(1.3)

Here is the cdf of the Tracy-Widom law, i.e. where is the Airy operator on with kernel defined later in (1.8). Later we will explain why has this zero subscript. We note that most of these results are universal, as is proved in [14], [19] and [20], to list a few.

For the spiked population model where , the phenomenon becomes much more interesting. Recent research found that the non-null eigenvalues tend to pull the extreme sample eigenvalues out of the Marčenko-Pastur sea , provided that they are larger or smaller than certain thresholds. In [3] Baik and Silverstein proved the almost sure limits of the extreme sample eigenvalues pulled out by the spikes. He proved that for fixed , if the largest -th population eigenvalue is greater than , then the largest -th sample eigenvalue satisfies

(1.4)

If is less than or equal to the threshold , then which is just the right edge of the Marčenko-Pastur sea. The same is true for the smallest eigenvalues. If then (1.4) also holds for replaced by . Otherwise almost surely. Note that this includes the case where some of the ’s are the same. In this case, the corresponding ’s just converge to the same limit specified in (1.4). We call these eigenvalues “packed”.

But what is the second order approximation? Baik, Ben Arous and Péche in [1] observed the phase transition phenomenon of the asymptotic distribution of the largest sample eigenvalue . They proved that if (i.e., when is pulled out of the sea), then the local fluctuation of will be asymptotically the same as the largest eigenvalue of a GUE matrix, where is algebraic multiplicity of . On the other hand if then follows the generalized Tracy-Widom law defined in Definition 1.1. Moreover, in [4] Bai and Yao obtained the joint local fluctuation of the packed sample eigenvalues which are pulled out — when suitably centered and scaled, they are asymptotically the same distributed as some unitary Gaussian random matrix.

We note that similar results can also be obtained for perturbed GUE case, see [2] and [6]. In [4], [5] and [7] the authors also got the similar results for real Gaussian case or even universal case.

However, none of these results deal with joint distribution of the largest and the smallest sample eigenvalues in our spiked population model. Intuitively they should be independent. Indeed, the distance between the two extreme eigenvalues is at least , i.e., the width of the Marčenko-Pastur sea. For this large distance, the repulsion force between eigenvalues is very weak. As a result, asymptotically they will fluctuate freely, without interacting each other at all.

For a brief history, in [8] Bianchi, Debbah and Najim first established the independence for the GUE case. Their method is based on bounding the expansion of the Fredholm determinant.

Later Bornermann in [9] used operator theory to give a much simpler proof. In [16] a different approach relying on PDE can also be found.

In this paper, the two branches of the results are combined. Here we establish the asymptotic distribution of , i.e., the largest and the smallest eigenvalues. More precisely, we have two results. The first one is for the asymptotic distribution of the smallest eigenvalue. Here we also observe the same phase transition phenomenon as in [1]. We proved that, when suitably centered and scaled, the local fluctuation of the smallest eigenvalue will be similar to the largest one discussed above. As a second result, we prove that as , the largest and the smallest eigenvalues will be asymptotically independent. From this we can easily establish the asymptotic joint distribution of .

1.1 Main Results

To state our maim theorems, we need to define a few functions. They first appeared in [1]. In that paper Baik, Ben Arous and Péché also discussed some properties of them.

For any integer , we define

(1.5)

(1.6)

Here the contour is from to such that the point lies above the contour. As an immediate observation, is just the Airy function, denoted by

(1.7)

with the same contour as above. We can also define the Airy kernel

(1.8)

Furthermore, we define as the integral operator on with the kernel .

Definition 1.1

Given an integer , is defined to be

(1.9)

where is the inner product in .

Remark 1.1

As is shown in [1], is a distribution function. Moreover, is just the basic Tracy-Widom law. Hence for general can be regarded as a generalization of the Tracy-Widom law.

Definition 1.2

For , we define the distribution function as

(1.10)

to be the distribution function of the largest eigenvalue of a standard GUE matrix.

Remark 1.2

When , is just the density of a standard Gaussian. Hence we can regard as a generalization of the Gaussian distribution.

Having defined our key distribution functions and , we can state our main theorems below.

Theorem 1.1

For the spiked population model defined above, the smallest eigenvalue of the sample covariance matrix has the following asymptotic distribution, depending on whether the smallest eigenvalue of the true covariance matrix is small enough or not.

1.

If for some , and the other ’s lie in a compact subset of , then as

(1.11)

2.

If for some , and the other ’s lie in a compact subset of , then as

(1.12)

Our next theorem states that as , the largest and the smallest eigenvalues of the sample covariance matrix are asymptotically independent of each other.

To state it more rigorously, we assume that , for some , and the rest of the ’s lie in a compact subset of . We define such that

(1.13)

For , we define the centered and the scaled version of them. Define

(1.16)

(1.19)

to be the centered and the scaled version of . Then we have the following theorem regarding the asymptotic distribution of .

Theorem 1.2

Under the assumption of the spiked population model, as

Remark 1.3

Since or is the asymptotic distribution of and , Theorem 1.2 also tells us that are asymptotically independent.

Possible applications of our result include data analysis. Suppose we have a large data matrix . The question is to determine whether the samples are i.i.d. drawn from a Gaussian distribution of a given spiked covariance matrix . For example, when we just want to determine whether our data matrix is pure noise. One possible way is test the hypothesis is to see whether the largest and smallest eigenvalues are close to their asymptotic limit. But here we are testing the null hypothesis using two criteria, involving both and . Hence we need their joint distribution to carry on the hypothesis testing. Another possible application involves the local fluctuation of condition numbers. They are both discussed in Section 2.

The rest of the paper is organized as follows. A sketch of the proof will be provided in section 1.1. In section 2 we will discuss some applications of the result. In section 3 we will represent the probability in a determinantal form, which will be the basis for future proofs. Section 4 and 5 will be devoted to prove Theorem 1.1 under the two cases. The proof of Theorem 1.2 can be found in section 6. Finally Section 7 serves the conclusion of the whole paper.

1.2 Sketch of the proof

First let’s focus on the smallest eigenvalue.

The basic idea is to calculate the large limit of the density of . Since in our model, the distribution of each sample is Gaussian, we can write down the density explicitly in (3.1). Due to some trick proposed first by Tracy and Widom in [15], we can further write the density into the form of a Fredholm determinant , where the kernel of the operator is defined in (3.14). We note that the kernel can be written as two contour integrals. By designing our contours carefully and by the saddle point analysis, we can finally obtain the asymptotic limit of the kernels, or the limit of the operator itself under the trace norm. Since the determinant is a locally Lipschitz function of the operator under the trace norm, we have our desired limit.

For proving the asymptotic independence, our strategy is the same. We write the joint distribution of into a determinantal form in (3.2), where the operator can be written as a block matrix. We prove that under the correct scaling, the diagonal blocks will have a non-trivial limit, while the off-diagonal blocks will converge to zero, both under the trace norm. Hence will converge to a block diagonal matrix. The independence result follows easily from the trivial fact that the determinant of a diagonal matrix equals to the product of the determinants of its diagonal blocks.

2 Applications

In this section we will discuss some applications of Theorem 1.2. In subsection 2.1 we will talk about the asymptotic distribution of condition numbers of a data matrix. In subsection 2.2 some application in hypothesis testing will be discussed.

2.1 Distribution of Condition Numbers

As a simple consequence of Theorem 1.2, we can get the asymptotic fluctuation of the ratio , which is the square of the condition number of the original data matrix . More precisely, we have the following Corollary.

Corollary 2.1

Let be the condition number of the original data matrix . With the definition of in (1.13), we have the following four results.

1.

If , then

(2.1)

2.

If , then

(2.2)

3.

If , then

(2.3)

4.

If , then

(2.4)

Here are two independent random variables with distribution specified in their subscripts. The convergences in (2.1 – 2.4) all mean convergence in distribution.

Proof.

Here we just prove the corollary for case 1. By in (1.16) and (1.19) we have

(2.5)

In (2.5) the first factor will converge to one in probability. By Theorem 1.2 the random variable in the bracket will convergence to the right hand side of (2.1). By Slutsky’s lemma our proof is complete. The proofs for the other three cases are the same.

∎

2.2 Hypothesis Testing

In this section we discuss one way to test whether the columns of the data matrix are i.i.d. samples from complex normal distribution of mean zero and covariance matrix . This is our null hypothesis to be tested. Note that sometimes our goal is just to test whether our data is just pure noise, where we have . But the method discussed in this subsection can be generalized to any other covariance matrix as long as it is of finite rank perturbation of the identity.

To save space, here we just discuss the case where . The method for other cases can also be very similarly obtained.

By Theorem 1.2, we know that will converge to and , respectively. Intuitively, if the observed two extreme eigenvalues of the sample covariance matrix deviates from the two limits by a large amount, then probably we should reject the null hypothesis. However, here we are testing the null hypothesis using two criteria. We claim that should be close to and should be close to . Thus we need to calculate the joint distribution of the two. Hence our Theorem 1.2 plays an important role here — it claims that they are asymptotically independent.

Here’s our method to test the null hypothesis, step by step.

1.

Form the sample covariance matrix from the data matrix . Then calculate the observed maximum and minimum eigenvalue of it, denoted by .

2.

Use (1.16) and (1.19) to calculate the centered and scaled version of , denoted by .

3.

Calculate our statistic . If where is a pre-determined confidence level, then we reject the hypothesis. Otherwise we accept it.

3 Determinantal Form of the Distribution

In this section we will derive the determinantal form of the distribution of the extreme eigenvalues. This formula will be the basis for future saddle point analysis from Section 4 to 6. From now on, we will always denote as some positive constants independent of . Their value may vary from line to line, but they are always constants.

For notational convenience, we define for . Then if ’s are distinct, the joint probability density of can be written as the following form

(3.1)

for some constant . Here is the Vandermonde determinant. If some of the ’s coincide, we interpret (3.1) using the L’Hópital’s rule.

For any two real numbers , let be two disjoint intervals on such that

Moreover, we define and we denote as the probability that there are no eigenvalues in the set . That is,

Our first proposition gives a determinantal representation of . This determinant form will turn out to be an invaluable formula for future analysis.

Proposition 3.1

We have

(3.2)

where for is the integral operator on with the kernel

(3.3)

Here are two pre-fixed constants such that

(3.4)

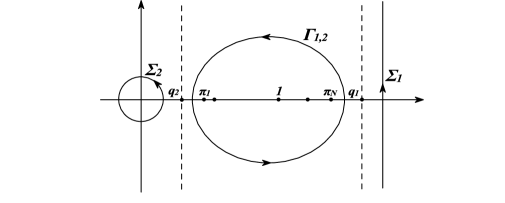

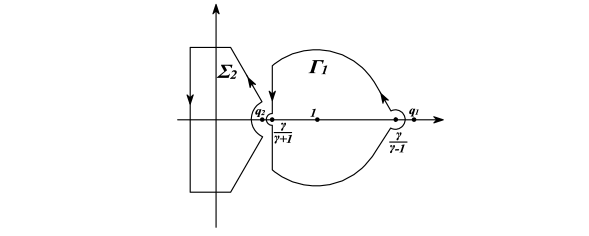

Moreover is the contour on enclosing and lying in the strip

is a vertical line from bottom to top for . is counter clockwise circle enclosing the origin and lies in . These contours are sketched in Figure 1.

Figure 1: Graph for the contours and

Remark 3.1

Here can be any constants as long as (3.4) is satisfied. They will not affect the determinant in (3.2).

Proof.

The proof is almost the same to the one in [1]. Thus we just point out our major differences. The rest will be quite sketchy.

Since we have an explicit expression for the probability density (3.1), we can express into the following (for details, see (66) of [1]).

Here is the indicator function of the set and is defined to be

If we define , then we can show that

Now we define and for . Here are two pre-fixed constant such that condition (3.4) is satisfied.

Then we observe .

We also define the operators by

Then we can re-write as

(3.5)

Please note that is an operator on and is a constant independent of . We note that can be also regarded as an operator on . Recall that . With and , will converge to zero. Hence take in (3.5) gives .

Now we note that is isomorphic to under the trivial isomorphism

Thus, under the isomorphism, (3.5) can be further written as

(3.6)

Here is an operator on . Following the rest of the proof of Proposition 2.1 in [1], we can obtain that, for ,

(3.7)

Here and are the contours defined in Proposition 3.1. The only difference is that in our case, instead of using equation (76) in [1], we used

for both , as long as is large enough.

∎

If we consider the special case of Proposition 3.1 when and , then we arrive at the following Corollary.

Corollary 3.1

We have

(3.8)

where is the integral operator on with the kernel defined in (3.3).

As the first goal of this paper, we will focus on the distribution of the smallest eigenvalue . Due to Corollary 3.1, we can in turn analyze the asymptotic behavior of the operator .

First we note that the kernel function can be simplified. Since the contour is always on the left of , then we have . Hence we have

where and are constants that will be defined later. Under such change of variables

where

(3.14)

Here

(3.15)

(3.16)

Under the assumption that only of these ’s are not one, we can further write as

(3.17)

(3.18)

Here

(3.19)

where the function is defined in the principal branch.

According to the discussion in [1], we just need to find suitable limiting functions and a constant such that, for any in a compact set,

(3.20)

(3.21)

In the following two sections we will use the saddle point analysis on to realize our promise.

In this section we will prove Theorem 1.1 for the case . Since in this section and the next section we will focus on only defined above, thus we temporarily drop all the subscript one, for notational simplicity. For example, instead of writing , we will write . Note that these are only valid in this and the next section.

We assume that for some (recall ),

and the rest of the ’s are in a compact subset of . The rest of the job is to provide a saddle point analysis of and .

In this case, we can define our constants to be

(4.1)

Here is a pre-fixed smaller number and will be later shown to be the saddle point of . We also define

(4.2)

Then our can be written as

(4.3)

(4.4)

Our constant in this case is defined to be

(4.5)

Finally, as we promised in (3.17) and (3.18), our and are defined as

(4.6)

(4.7)

Here is the contour from to such that lies on the left hand side of the contour. is the contour from to .

The main target of this section is to prove the following Proposition.

Proposition 4.1

Assume that and are bounded below. That is, assume that there exists some such that . Then

1.

There exists some constant such that uniformly for ,

(4.8)

2.

There exists some constant such that uniformly for ,

(4.9)

In order to prove Proposition 4.1, we perform the saddle point analysis on defined in (3.19) by . Through some very simple calculation, we find that

(4.10)

Hence is the saddle point of . Since is negative, the steepest descent direction for appearing in is with angle to the real axis. The steepest descent direction for in is with angle to the real axis. Let’s analyze first.

4.1 Analysis of

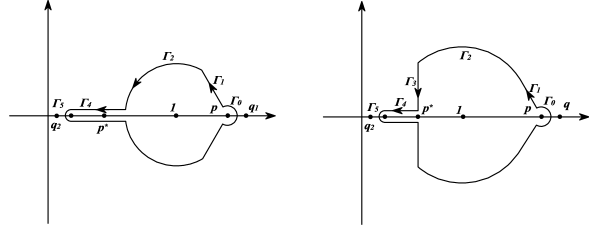

To carry out an saddle point analysis, we need to define our contour for first. In the following we only define in the upper half of the complex plane. The part in the lower half is just of a reflection with respect to the real axis. Let where

where is the small constant appeared in the definition for in (4.1). Define to be the arc centered at the point and connects the endpoint of . We define

(4.11)

Figure 2: The Contours . Case 1: Left. Case 2: Right.

For the definition of the rest of the contours, we need to split it into two cases.

•

Case 1. If does not intersect the vertical line , then is defined to be a horizontal line just above the real axis, i.e.

(4.12)

for some small fixed constant . We also require that should connect the endpoint of and the point . is a quarter circle centering at , with radius , just connecting . For a graph of the contour, please refer to the left part of Figure 2.

•

Case 2. If intersects the vertical line , then we just define to be the part of that line, connecting the endpoint of and heading downward. We add into our contour. The definition for and are exactly the same as that in Case 1. For a graph for this case, please refer to the right part of Figure 2.

We choose the contour in such a specific way to establish the following lemma.

Lemma 4.1

In both cases, is monotonously decreasing when travels along the path , provided that we choose small enough. For we have

where is the intersection of and .

Proof.

We divide the proof into several parts.

•

In for . Then

Everything is positive except the quadratic term . When is taken to be its largest possible value , the quadratic term achieves it maximum, which is . Hence we get

•

In we have for taking value in a subset of . The is some constant. We have

(4.13)

But we can calculate . Hence .

•

In , we note that can be represented as for some real parameter . We then have

Since is decreasing as travels along , we conclude that is decreasing.

•

For , can be represented as for some small constant and real parameter .

We note that for

Moreover is continuous for around zero, uniformly for all if lies in a compact subinterval of , which is indeed the case if . Hence we can choose small enough so that

.

∎

Now we are ready to find an asymptotic expression for the integral

(4.14)

As in [1], we first fix some small, then we decompose where

(4.15)

We can also define where is the image of under the map, and . We can also set

(4.16)

Here is the part of the integral (4.14) on and the definitions for and in (4.16) are similar.

Our strategy to prove (4.8) in Proposition 3.1 is as follows.

•

By saddle point analysis, the integral of in should be concentrated on the point . Hence and should be negligible, as is proved in Lemma 4.2.

•

For the integral of near , we prove in Lemma 4.3 that the difference is small.

Now we discuss how we should choose . First, by some very basic calculus we obtain that, if , then for we have

We note that is bounded above and below for . Moreover since

, we have

for some constants and . Hence from (4.23) we have

for some constant and for large enough. The statement for is proved in [1].

∎

Now in order to prove (4.8) in Proposition 4.1, we just need to prove

for some constant and for large enough. First using change of variables in (3.20) for , we know

(4.24)

Let where and . We can define to be the integral in (4.24) on and . Similarly we can define and . The following lemma completes the proof of the first part of Proposition 4.1.

Lemma 4.3

For some constant and for large enough, we have

(4.25)

Proof.

Assume to be large enough so that . For , By (4.19) we have that is bounded. Also

(4.26)

Also because has no singularities or zeros around ,

Thus

Since we have

(4.27)

the integrand in (4.27) is bounded above by . But the integral region is . Hence the first part is (4.25) is true.

For the second part, we have for . By (4.19), . Like (4.26) we have

where in the second step we use the change of variables .

∎

4.2 Analysis of

This time we use the saddle point analysis for to prove (4.9) in Proposition 4.1. Since most of the analysis will be similar to that of the previous part, we just outline the key steps.

The contour of in is graphed in Figure 3. Here where

Figure 3: The Contour in .

As in the previous section, we choose in such a way that the following lemma holds.

Lemma 4.4

is monotonously increasing as travels along . Moreover, for (here ), we have

(4.28)

for some constant , where is the interception of and .

Proof.

•

For , for some . Then

It is straight forward to verify that the right hand side is positive for .

•

For , . Then

for some constant , uniformly for all .

Hence we have

∎

As in the last subsection, we can also define to satisfy (4.18). Similarly we can also define

Similarly, from the decomposition of and we can also decompose and into

Because of (4.30) and (4.31), the following lemma holds true. Since the proof is similar to that of Lemma 4.2, we just provide the outlines. The only different part is that now our is an infinite contour.

Lemma 4.5

If is bounded below, i.e., for some fixed , then there exists some constant and such that for we have

(4.32)

uniformly for .

Proof.

The result for is proved in [1]. We just provide a brief proof about . The only difference from the previous subsection is that now is not of finite length. First since , we obtain, similar to Lemma 4.2, that

for some , uniformly for . We decompose into where , are the integral of (4.4) on and . Since is of finite length, we can take the same procedure as in the previous subsection to prove that

After showing that is negligible, we then turn to analyze , we can decompose where . Also we can use the same rule to write .

From this we can similarly decompose

As a analog of Lemma 4.3, we have the following lemma. The proof is similar and thus we just omit that.

Lemma 4.6

For some constant and for large enough, we have

(4.33)

uniformly for bounded below.

As a final remark, Lemma 4.5 and Lemma 4.6 together implies the second part of Proposition 4.1.

4.3 Finishing the proof

By (3.8) in Corollary 3.1 and by the scaling in (3.13) we obtain

(4.34)

where is an integral operator on with kernel

for defined in (4.6) and (4.7). By the same argument in section 3.3 of [1], we can prove that the Fredholm determinant in (4.34) is just . This finishes the proof.

In this part, we analyze the limiting distribution of the smallest sample eigenvalue when there are some “true” eigenvalues being smaller than the critical point .

We assume that for some ,

We also assume that the rest of the ’s are in a compact subset of . In this case, our constants are

(5.1)

Here is a pre-fixed smaller number. We note here that due to some very simple algebra we can verify that is a real number. Again, we define

(5.2)

The function is now

(5.3)

(5.4)

The constant is defined to be

(5.5)

Finally, like the previous section, we define our and to be

(5.6)

(5.7)

where

oriented from bottom to top. We note that the integral on in (5.7) also equals to the integral on the imaginary axis, from bottom to top.

Again, in this section, our main goal is to prove the following proposition.

Proposition 5.1

Assume are bounded below, then

1.

There exists some constant , such that uniformly for

(5.8)

2.

There exists some constant , such that uniformly for

(5.9)

In order to prove this proposition, we also need the saddle point analysis on . Note that with the choice of in (5.1), the two saddle points are and . It is not hard to know

(5.10)

and

(5.11)

In subsection 5.1 we use the residue theorem to provide an asymptotic analysis for in (5.8), and in subsection 5.2, a saddle point analysis around will provide us a good approximation for in (5.9). Finally, in subsection 5.3 we finish the proof.

5.1 Analysis of

By the residue theorem we have

(5.12)

where

(5.13)

and is a contour inclosing but excluding . We will later choose explicitly, based on which we will prove that the integral on is negligible. Hence the main contribution of (5.12) is the residue in (5.13).

The following lemma gives an approximation of .

Lemma 5.1

For bounded below, uniformly there exists constants and such that for all

Proof.

The proof is almost the same as that in [1].

First by expanding and on around we obtain

where is a analytic function around . Moreover all the coefficient in the Taylor expansion of around are bounded in . Hence we obtain

(5.14)

Here is a polynomial of of degree at most , and all the coefficients of are bounded in . Due to the factor in (5.14) we complete the proof.

∎

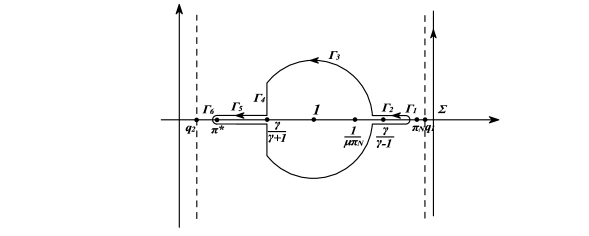

To keep our promise our next step is to prove that the second term in (5.12) is negligible. This is done in Lemma 5.3. But before that, we need to choose our contour explicitly. Again, our contour is symmetric with respect to the real axis thus we just define the upper part. We take where the ’s will be defined below. For a graph of the contour please refer to Figure 4.

Figure 4: The Contours and

•

Take such that . Moreover take some to be a sufficiently small constant. We take to be the quarter-circle centered at , with radius . Here is a small constant.

•

Take . We define

•

Define to be the arc centered at with radius . Using some simple algebra, we can verify that with our choice of , the real part of the intersection of and is between and , provided that is small enough.

•

If , we just define to be the vertical line joining and . This is shown in Figure 4. If , then we just exclude in the definition of , connecting and directly as we did in the previous section.

•

Take , we define

•

We finally define to be the quarter-circle centered at with radius .

Our analysis of replies heavily on the following lemma.

Lemma 5.2

There exists some constant such that

Proof.

Similar to Lemma 4.1, we also divide the proof into several parts.

•

In , can be represented as . We note that when ,

and

Thus is strictly decreasing for traveling on the real axis to . Moreover is continuous for around zero, uniformly for all lying in a compact subset of . Thus we can choose to be sufficiently small such that for some constant ,

•

In , for in a subset of . Then

with our choice of . Hence is decreasing in .

•

In (if it exists), . With exactly the same calculation as that of Lemma 4.1, we can prove that is decreasing in .

•

in , can be represented as , just as that in . This time when , and

With the same argument as that in , we can choose sufficiently small such that

∎

Based on Lemma 5.2, our next lemma establishes that the integral along in (5.12) is negligible, which finishes the proof of (5.8) in Proposition 5.1.

Lemma 5.3

There exists some and such that uniformly for and for

Now we follow the same proof as that in Lemma 4.3 thus we just list the key steps. We can prove

where is defined by . Further . Thus, by the change of variables in (5.22) we obtain

for some constant .

∎

5.3 Finishing the proof

Using the same steps as in [1], with minor modifications, we can prove

(5.23)

where is the -th probabilists’ Hermite polynomial, that is,

Thus the kernel has the desired form, as is proved by [1]. We omit the steps.

6 Independence of the extreme eigenvalues

In this section we will prove that the largest eigenvalue and the smallest eigenvalue are asymptotically independent. In Section 4 and Section 5 we dropped the subscript one for notational convenience. In this section, however, we will consider both the maximum and the minimum eigenvalue. Hence we need these subscripts to distinguish them.

Note that we have four cases here.

•

Case 1. and .

•

Case 2. and .

•

Case 3. and .

•

Case 4. and .

Since the proofs for all the cases are almost exactly the same, thus here we just prove the theorem for case 1.

where the operators are defined in (3.3). Our first observation is that for any constant , we will have

(6.8)

(6.11)

We will leave the constant as an normalization constant, to be defined later.

As the next step, to ensure the probability to be non-trivial, we need to take the proper scaling of and .

Under the case 1, define

(6.12)

Here and are defined in (4.1). The constant parameter and are defined in [1] by

(6.13)

Our next step is analyze . Let’s take as an example. As we did in (3.13 – 3.18), consider the kernel , with the change of variables

we know that is equivalent to defined in (3.14). The analysis for the other ’s are the same. Finally we can arrive at the following equation.

(6.14)

Here

is the proper scaling of and the is the integral operator from to where and . The kernels on the diagonal are

(6.15)

(6.16)

with defined by (3.15) and (3.16). The appeared in (6.15) are defined in [1] by

(6.17)

(6.18)

In Section 4 we have already shown that will tend to the desired limit at the speed of as tends to infinity. In [1], Baik, Ben Arous and Péché showed that will also tend to the desired form at the speed of . That is to say, the diagonal part in (6.14) has the non-trivial limit because of the correct scaling in (6.12). In order to prove that and are asymptotically independent, our strategy is to show that the off-diagonal terms and in (6.14), properly scaled, will tend to zero. Hence the matrix in (6.14) will tend to a diagonal matrix. Since the determinant of a diagonal matrix equals to the product of the determinant of its diagonal parts, the joint probability is approximately . Now we carry on our strategy in details.

First consider the off-diagonal terms in (6.14). First define the constant

(6.19)

( and the functions will be defined below).

Using the change of variables as we did in (3.13 – 3.18), we get

(6.20)

(6.21)

Here

(6.22)

(6.23)

(6.24)

(6.25)

The function are defined by

(6.26)

(6.27)

and the parameter are defined by

(6.28)

From some simple calculation, we know that are the saddle point of and , respectively. Below we will perform our saddle point analysis on and . Let’s start from first. In Figure 5 we plot the contour and in (6.20). The contour is defined in Figure 2, Section 4. Moreover the contour is defined in [1]. We quote their definition below.

Figure 5: The Contour and .

Define where

where is a pre-fixed constant which is sufficiently large and independent of .

The intuition of the proof is as follows. The saddle point of is respectively. Moreover in our contour we leave the saddle points along the steepest decent direction, in (6.20) the integral on will be mostly concentrated on the point and the integral on will be mostly concentrated on the point . But by our choice of the constant , and will be bounded at these two saddle points. Moreover around these two points will also be bounded. Hence due to the factor in front of the integral of (6.20), will tend to zero, at the speed of . To paraphrase our intuition into a rigorous proof, we will arrive at the following lemma.

Lemma 6.1

These exist some constant such that uniformly for , we have

(6.29)

(6.30)

Proof.

Here we just prove (6.29) as the proof for (6.30) will be similar.

Let’s define to a sufficiently small constant independent of . Just like what we did in Section 4 and 5, we decompose the contour by , by

We first analyze . By Lemma 4.1 we know that is decreasing on . Hence there exist some constant such that

(6.31)

For we can also deduce the same result. From Lemma 3.2 in [1], we have

(6.32)

For , we note three results proved before. (1) by the definition of the contour; (2) is bounded; and (3) is bounded. These three results, together with (6.31) give that

(6.33)

for some constant .

Now we proceed to prove

(6.34)

Similar to (4.18 – 4.21), we can choose small enough such that for ,

(6.35)

Actually in [1] the authors proved that (6.35) holds as long as

Now for ,

(6.36)

since that is bounded and that is bounded for . From (6.36) we obtain (6.34) directly. Having analyzed the behavior of on and , our next step is to prove that they decay exponentially fast on and . Let’s take as an example. The proof of will be similar. Indeed, by the second part of (6.31) and by the fact that is bounded, we obtain

(6.37)

Similar results for can also be obtain.

As the last step in proving our lemma, we have

(6.38)

Here

(6.39)

and are just the integral of (6.39) on and , respectively.

In , and , we have is bounded above. Hence by (6.33) and (6.34) we have

(6.40)

For , . We just use the trivial bound for some constant , by the definition of our contour. Hence by (6.37) and (6.36) we get

(6.41)

With similar analysis, we can prove that (6.41) also holds for and . Note that in (6.38) we have an extra in front of the integral. This finishes the proof of (6.29) in our lemma.

∎

As a simple consequence, Theorem 1.2 holds. Here’s the rest of the proof for the theorem.

for some constant . Here is the trace norm of the operator. Since the Fredholm determinant is a locally Lipchitz continuous function with respect to the trace norm, from (6.14) we obtain

∎

7 Conclusion

In this paper, we studied the spiked population model to establish two results: (1) the asymptotic distribution of the smallest eigenvalue of the sample covariance matrix, and (2) that the largest and the smallest eigenvalues are independent. Our approach is based on the convergence of operators under the trace norm.

For the smallest eigenvalue, when the spike is weak (all above the threshold ), the local fluctuation is of order , and will converge to the generalized Tracy-Widom law under the correct scaling. When the spike is strong enough to pull the smallest eigenvalue out of the Marčenko-Pastur sea, it wil fluctuate at the order of , following the generalized Gaussian distribution. We also proved that the largest and smallest eigenvalues are independent. Combined with the asymptotic behavior of proposed in [1], we can establish the joint distribution of .

References

[1]J. Baik, G. Ben Arous, S. Péché,

Phase transition of the largest eigenvalue for nonnull complex sample covariance matrices,

Ann. Prob. 33 (5) 1643-97, 2005.

[2]S. Péché,

The largest eigenvalue of small rank perturbations of hermitian random matrices,

Prob. Theory Relat. Fields, 134 127-173, 2006.

[3]J. Baik, J. W. Silverstein,

Eigenvalues of large sample covariance matrices of spiked population models,

J. Multivariate Analysis 97 1382-1408, 2006.

[4]Z. D. Bai, J. F. Yao,

Central limit theorems for eigenvalues in a spiked population model,

Ann. de l’Institut Henri Poincaré – Prob. et Stat. 44 (3) 447-474, 2008.

[5]D. Paul,

Asymptotics of sample eigenstructure for a large dimensional spiked covariance matrix model,

Statistica Sinica 17 1617-42, 2007.

[6]D. Féral, S. Péche,

The largest eignvalue of rank one deformation of large Wigner matrices,

Comm. Math. Phys. 272 185-228, 2007.

[7]M. Capitaine, C. Donati-Martin, D. Féral,

The largest eigenvalues of finite rank deformation of large Wigner matrices: Covergence and nun-universality of the fluctuations,

Ann. Prob. 37 (1) 1-47, 2009.

[8]P. Bianchi, M. Debbah, J. Najim,

Asymptotic independence in the spectrum of the gaussian unitary ensemble,

Elect. Comm. in Prob. 15 376-395, 2010.

[9]F. Bornermann,

Asymptotic independence of the extreme eigenvalues of gaussian unitary ensemble,

J. Math. Phys. 51 023514, 2010.

[10]V. A., Marcěnko, L. A. Pastur,

Distribution of eigenvalues for some sets of random matrices,

Math. USSR Sb. 1 457-486, 1967.

[11]S. Geman,

A limit theorem for the norm of random matrices,

Ann. Prob. 8 (2) 252-261, 1980.

[12]J. W. Silverstein,

The smallest eigenvalue of a large dimensional wishart matrix,

Ann. Prob. 13 (4) 1364-1368, 1985.

[13]K. Johansson,

Shape uctuations and random matrices,

Comm. Math. Phys. 209 437 476, 2000.

[14]Z. D. Bai, Y. Q. Yin,

Limit of the smallest eigenvalue of a large dimensional sample covariance matrices,

Ann. Prob. 21 1275-94, 1993.

[15]C. Tracy, H. Widom,

Correlation functions, cluster functions and spacing distributions for random matrices,

J. Stat. Phys., 92 (5-6) 809-835, 1998.

[16]Basor, Chen, Zhang,

PDEs satisfied by extreme eigenvalues distributions of GUE and LUE,

Random Matrices: Theory and Applications, 1 (1) 1150003, 2012.

[17]T. Baker, P. Forrester, P. Pearce,

Random matrix ensembles with an effective extensive external charge,

J. Phys. A 31 6087 6101, 1998.

[18]I. Johnstone,

On the distribution of the largest eigenvalue in principal components analysis,

Ann. Stat. 29 (2) 295 327, 2001.

[19]Y. Q. Yin,

Limiting spectral distribution for a class of random matrices,

J. Multivariate Anal. 20 50-68, 1986.

[20]Z. D. Bai, Y. Q. Yin, P. R. Krishnaiah,

On the limit of the largest eigenvalue of the large dimensional sample covariance matrix,

Prob. Theory and Related Fields 78 509-521, 1988

[21]E. Telatar,

Capacity of multi-antenna gaussian channels,

European Trans. Telecommunications 10 (6) 585-595, 1999.

[22]L. Lalous, P. Cizeau, M. Potters, J. Bouchaud,

Random matrix theory and financial correlations,

Internat. J. Theoret. Appl. Finance 3 (3) 391-397, 2000.

[23]A. Buja, T. Hastie, R. Tibshirani,

Penalized discriminant analysis,

Ann. Stat. 23 73-102, 2995.

[24]R. Sear, J. Cuesta,

Instabilities in complex mixtures with a large number of components,

Phys. Rev. Lett. 91 (24) 245701, 2004.

[25]D. Hoyle, M. Rattray,

Limiting form of the sample covariance eigenspectrum in PCA and kernel PCA,

Advances in Neural Information Processing Systems NIPS 16, 2003.