Semiparametric stationarity tests based on adaptive multidimensional increment ratio statistics

Abstract

In this paper, we show that the adaptive multidimensional increment ratio estimator of the long range memory parameter defined in Bardet and Dola (2012) satisfies a central limit theorem (CLT in the sequel) for a large semiparametric class of Gaussian fractionally integrated processes with memory parameter . Since the asymptotic variance of this CLT can be computed, tests of stationarity or nonstationarity distinguishing the assumptions and are constructed. These tests are also consistent tests of unit root. Simulations done on a large benchmark of short memory, long memory and non stationary processes show the accuracy of the tests with respect to other usual stationarity or nonstationarity tests (LMC, V/S, ADF and PP tests). Finally, the estimator and tests are applied to log-returns of famous economic data and to their absolute value power laws.

Keywords: Gaussian fractionally integrated processes; Adaptive semiparametric estimators of the memeory parameter; test of long-memory; stationarity test; unit root test.

1 Introduction

Consider the set of fractionally integrated time series for by:

Assumption : is a time series if there exists a continuous function satisfying:

-

1.

if , is a stationary process having a spectral density satisfying

(1.1) -

2.

if , is a stationary process having a spectral density satisfying

(1.2)

The case is the case of long-memory processes, while short-memory processes are considered when and nonstationary processes when . ARFIMA processes (which are linear processes) or fractional Gaussian noises (with parameter ) are famous examples of processes satisfying Assumption . The purpose of this paper is twofold: firstly, we establish the consistency of an adaptive semiparametric estimator of for any . Secondly, we use this estimator for building new semiparametric stationary tests.

Numerous articles have been devoted to estimate in the case . The books of Beran (1994) or Doukhan et al. (2003) provide large surveys of such parametric (mainly maximum likelihood or Whittle estimators) or semiparametric estimators (mainly local Whittle, log-periodogram or wavelet based estimators). Here we will restrict our discussion to the case of semiparametric estimators that are best suited to address the general case of processes satisfying Assumption . Even if first versions of local Whittle, log-periodogramm and wavelet based estimators (see for instance Robinson, 1995a and 1995b, Abry and Veitch, 1998) are only considered in the case , new extensions have been provided for also estimating when (see for instance Hurvich and Ray, 1995, Velasco, 1999a, Velasco and Robinson, 2000,

Moulines and Soulier, 2003, Shimotsu and Phillips, 2005, Giraitis et al., 2003, 2006, Abadir et al., 2007 or Moulines et al., 2007). Moreover, adaptive versions of these estimators have also been defined for avoiding any trimming or bandwidth parameters generally required by these methods (see for instance Giraitis et al., 2000, Moulines and Soulier, 2003, or Veitch et al., 2003, or Bardet et al., 2008). However there still no exists an adaptive estimator of satisfying a central limit theorem (for providing confidence intervals or tests) and valid for but also for . This is the first objective of this paper and it will be achieved using multidimensional Increment Ratio (IR) statistics.

Indeed, Surgailis et al. (2008) first defined the statistic (see its definition in (2.3)) from an observed trajectory . Its asymptotic behavior is studied and a central limit theorem (CLT in the sequel) is established for inducing a CLT. Therefore, the estimator , where is a smooth and increasing function, is a consistent estimator of satisfying also a CLT (see more details below). However this new estimator was not totally satisfying: firstly, it requires the knowledge of the second order behavior of the spectral density that is clearly unknown in practice. Secondly, its numerical accuracy is interesting but clearly less than the one of local Whittle or log-periodogram estimators. As a consequence, in Bardet and Dola (2012), we built an adaptive multidimensional estimator (see its definition in (3.2)) answering to both these points

but only for

. This is an adaptive semiparametric estimator of and its numerical performances are often better than the ones of local Whittle or log-periodogram estimators.

Here we extend this preliminary work to the case . Hence we obtain a CLT satisfied by for all with an explicit asymptotic variance depending only on and this notably allows to obtain confidence intervals. The case is now studied and this offers new interesting perspectives: our adaptive estimator can be used for building a stationarity (or nonstationarity) test since is the “border number” between stationarity and nonstationarity.

There exist several famous stationarity (or nonstationarity) tests. For stationarity tests we may cite the KPSS (Kwiotowski, Phillips, Schmidt, Shin) test (see for instance Hamilton, 1994, p. 514) and LMC test (see Leybourne and McCabe, 2000). For nonstationarity tests we may cite the Augmented Dickey-Fuller test (ADF test in the sequel, see Hamilton, 1994, p. 516-528) and the Philipps and Perron test (PP test in the sequel, see for instance Elder, 2001, p. 137-146). All these tests are unit root tests, i.e. and roughly speaking, semiparametric tests based on the model with . A test about for a process satisfying Assumption is therefore a refinement of a basic unit root test since the case is a particular case of and the case a particular case of . Thus, a stationarity (or nonstationarity test) based on the

estimator of provides a more sensible test than usual unit root tests.

This principle of stationarity test linked to was also already investigated in many articles. We can notably cite Robinson (1994), Tanaka (1999), Ling and Li (2001), Ling (2003) or Nielsen (2004). However, all these papers provide parametric tests, with a specified model (for instance ARFIMA or ARFIMA-GARCH processes). More recently, several papers have been devoted to the construction of semi-parametric tests, see for in instance Giraitis et al. (2006), Abadir et al. (2007) or Surgailis et al. (2006).

Here we slightly restrict the general class to the Gaussian semiparametric class defined below (see the beginning of Section 2). For processes belonging to this class, we construct a new stationarity test which accepts the stationarity assumption when with a threshold depending on the type I error test and , while the new nonstationarity test accepts the nonstationarity assumption when . Note that also provides a test for deciding between short and long range dependency, as this is done by the V/S test (see details in Giraitis et al., 2003)

In Section 5, numerous simulations are realized on several models of time series (short and long memory processes).

First, the new multidimensional IR estimator is compared to the most efficient and famous semiparametric estimators for ; the performances of are convincing and equivalent to close to other adaptive estimators (except for extended local Whittle estimator defined in Abadir et al., 2007, which provides the best results but is not an adative estimator).

Secondly, the new stationarity and nonstationarity tests are compared on the same benchmark of processes to the most famous unit root tests (LMC, V/S, ADF and PP tests). And the results are quite surprising: even on AR or ARIMA processes, multidimensional IR and tests provide convincing results as well as tests built from the extended local Whittle estimator. Note however that ADF and PP tests provide results slightly better than these tests for these processes. For long-memory processes (such as ARFIMA processes), the results are clear: and tests are efficient tests of (non)stationarity while LMC, ADF and PP tests are not relevant at all.

Finally, we studied the stationarity and long range dependency properties of Econometric data. We chose to apply estimators and tests to the log-returns of daily closing value of classical Stocks and Exchange Rate Markets. After cutting the series in stages using an algorithm of change detection, we found again this well known result: the log-returns are stationary and short memory processes while absolute values or powers of absolute values of log-returns are generally stationary and long memory processes. Classical stationarity or nonstationarity tests are not able to lead to such conclusions. We also remarked that these time series during the “last” (and third) stages (after 1997 for almost all) are generally closer to nonstationary processes than during the previous stages with a long memory parameter close to .

The forthcoming Section 2 is devoted to the definition and asymptotic behavior of the adaptive multidimensional IR estimator of . The stationarity and nonstationarity tests are presented in Section 4 while Section 5 provides the results of simulations and application on econometric data. Finally Section 6 contains the proofs of main results.

2 The multidimensional increment ratio statistic

In this paper we consider a semiparametric class : for and define:

Assumption : is a Gaussian time series such that there exist , , and satisfying:

-

1.

if , is a stationary process having a spectral density satisfying for all

(2.1) -

2.

if , is a stationary process having a spectral density satisfying for all

(2.2)

Note that Assumption is a particular (but still general) case of the more usual set of fractionally integrated processes defined above.

Remark 1.

We considered here only Gaussian processes. In Surgailis et al. (2008) and Bardet and Dola (2012), simulations exhibited that the obtained limit theorems should be also valid for linear processes. However a theoretical proof of such result would require limit theorems for functionals of multidimensional linear processes difficult to be established.

In this section, under Assumption , we establish central limit theorems which extend to the case those already obtained in Bardet and Dola (2012) for .

Let be a process satisfying Assumption and be a path of . For any define

| (2.3) |

The statistic was first defined in Surgailis et al. (2008) as a way to estimate the memory parameter. In Bardet and Surgailis (2011) a simple version of IR-statistic was also introduced to measure the roughness of continuous time processes. The main interest of such a statistic is to be very robust to additional or multiplicative trends.

As in Bardet and Dola (2012), let with and , and define the random vector .

In the sequel we naturally extend the results obtained for to by the convention: (which changes nothing to the asymptotic results).

For , let be a standard fractional Brownian motion, i.e. a centered Gaussian process having stationary increments and such as . Now, using obvious modifications of Surgailis et al. (2008), for and , define the stationary multidimensional centered Gaussian processes such as for ,

| (2.6) |

and by continuous extension when :

with for , using the convention . Now, we establish a multidimensional central limit theorem satisfied by for all :

Proposition 1.

Assume that Assumption holds with and . Then

| (2.9) |

with where for ,

| (2.10) |

The proof of this proposition as well as all the other proofs is given in Section 6. As numerical experiments seem to show, we will assume in the sequel that is a definite positive matrix for all .

Now, this central limit theorem can be used for estimating . To begin with,

Property 2.1.

Let satisfying Assumption with and . Then, there exists a non-vanishing constant depending only on and such that for large enough,

| (2.14) | |||||

| and | (2.15) |

Therefore by choosing and such as when , the term can be replaced by in Proposition 1. Then, using the Delta-method with the function (the function is a increasing function), we obtain:

Theorem 1.

Let for . Assume that Assumption holds with and . Then if with and ,

| (2.18) |

This result is an extension to the case from the case already obtained in Bardet and Dola (2012). Note that the consistency of is ensured when but the previous CLT does not hold (the asymptotic variance of diverges to when , see Surgailis et al., 2008).

Now define

| (2.19) |

The function is and therefore, under assumptions of Theorem 1,

Thus, a pseudo-generalized least square estimation (LSE) of ican be defined by

with and denoting its transpose. From Gauss-Markov Theorem, the asymptotic variance of is smaller than the one of , . Hence, we obtain under the assumptions of Theorem 1:

| (2.22) |

3 The adaptive version of the estimator

Theorem 1 and CLT (2.22) require the knowledge of to be applied. But in practice is unknown. The procedure defined in Bardet et al. (2008) or Bardet and Dola (2012) can be used for obtaining a data-driven selection of an optimal sequence derived from an estimation of . Since the case was studied in Bardet and Dola (2012) we consider here and for , define

| (3.1) |

which corresponds to the sum of the pseudo-generalized squared distance between the points and PGLS estimate of . Note that by the previous convention, and . Then can be minimized on a discretization of and define:

Remark 2.

The choice of the set of discretization is implied by our proof of convergence of to . If the interval is stepped in points, with , the used proof cannot attest this convergence. However may be replaced in the previous expression of by any negligible function of compared to functions with (for instance, or with can be used).

From the central limit theorem (2.18) one deduces the following limit theorem:

Proposition 2.

Assume that Assumption holds with and . Then,

Finally define

and the estimator

| (3.2) |

(the definition and use of instead of are explained just before Theorem 2 in Bardet and Dola, 2012). The following theorem provides the asymptotic behavior of the estimator :

Theorem 2.

The convergence rate of is the same (up to a multiplicative logarithm factor) than the one of minimax estimator of in this semiparametric frame (see Giraitis et al., 1997). The supplementary advantage of with respected to other adaptive estimators of (see for instance Moulines and Soulier, 2003, for an overview about frequency domain estimators of ) is the central limit theorem (3.5) satisfied by . Moreover can be used for , i.e. as well for stationary and non-stationary processes, without modifications in its definition. Both this advantages allow to define stationarity and nonstationarity tests based on .

4 Stationarity and nonstationarity tests

Assume that is an observed trajectory of a process . We define here new stationarity and nonstationarity tests for based on .

4.1 A stationarity test

There exist many stationarity and nonstationarity test. The most famous stationarity tests are certainly the following unit root tests:

-

•

The KPSS (Kwiotowski, Phillips, Schmidt, Shin) test (see for instance Hamilton, 1994, p. 514);

-

•

The LMC (Leybourne, McCabe) test which is a generalization of the KPSS test (see for instance Leybourne and McCabe, 1994 and 1999).

We can also cite the V/S test (see its presentation in Giraitis et al., 2001) which was first defined for testing the presence of long-memory versus short-memory. As it was already notified in Giraitis et al. (2003-2006), the V/S test is also more powerful than the KPSS test for testing the stationarity.

More precisely, we consider here the following problem of test:

-

•

Hypothesis (stationarity): is a process satisfying Assumption with where and where .

-

•

Hypothesis (nonstationarity): is a process satisfying Assumption with where and where .

We use a test based on for deciding between these hypothesis. Hence from the previous CLT 3.5 and with a type I error , define

| (4.1) |

where (see (3.5)) and is the quantile of a standard Gaussian random variable .

Then we define the following rules of decision:

-

•

(stationarity) is accepted when and rejected when .

Remark 3.

In fact, the previous stationarity test defined in (4.1) can also be seen as a semi-parametric test versus with . It is obviously possible to extend it to any value by defining

From previous results, it is clear that:

Property 1.

Under Hypothesis , the asymptotic type I error of the test is and under Hypothesis , the test power tends to .

Moreover, this test can be used as a unit root test. Indeed, define the following typical problem of unit root test. Let , with , and an ARIMA with or . Then, a (simplified) problem of a unit root test is to decide between:

-

•

: and is a stationary ARMA process.

-

•

: and is a stationary ARMA process.

Then,

Property 2.

Under assumption , the type I error of this unit root test problem using decreases to when and the test power tends to .

4.2 A new nonstationarity test

Famous unit root tests are more often nonstationarity test. For instance, between the most famous tests,

-

•

The Augmented Dickey-Fuller test (see Hamilton, 1994, p. 516-528 for details);

-

•

The Philipps and Perron test (a generalization of the ADF test with more lags, see for instance Elder, 2001, p. 137-146).

Using the statistic we propose a new nonstationarity test for deciding between:

-

•

Hypothesis (nonstationarity): is a process satisfying Assumption with where and where .

-

•

Hypothesis (stationarity): is a process satisfying Assumption with where and where .

Then, the rule of the test is the following: Hypothesis is accepted when and rejected when where

| (4.2) |

Then as previously

Property 3.

Under Hypothesis , the asymptotic type I error of the test is and under Hypothesis the test power tends to .

As previously, this test can also be used as a unit root test where , with , and an ARIMA with or . We consider here a “second” simplified problem of unit root test which is to decide between:

-

•

: and is a stationary ARMA process.

-

•

: and is a stationary ARMA process..

Then,

Property 4.

Under assumption , the type I error of the unit root test problem using decreases to when and the test power tends to .

5 Results of simulations and application to Econometric and Financial data

5.1 Numerical procedure for computing the estimator and tests

First of all, softwares used in this Section are available on http://samm.univ-paris1.fr/-Jean-Marc-Bardet with a free access on (in Matlab language) as well as classical estimators or tests.

The concrete procedure for applying our MIR-test of stationarity is the following:

-

1.

using additional simulations (realized on ARMA, ARFIMA, FGN processes and not presented here for avoiding too much expansions), we have observed that the value of the parameter is not really important with respect to the accuracy of the test (less than on the value of ). However, for optimizing our procedure we chose as a stepwise function of :

and .

- 2.

5.2 Monte-Carlo experiments on several time series

In the sequel the results are obtained from generated independent samples of each process defined below. The concrete procedures of generation of these processes are obtained from the circulant matrix method, as detailed in Doukhan et al. (2003). The simulations are realized for different values of and and processes which satisfy Assumption :

-

1.

the usual ARIMA processes with respectively or and an innovation process which is a Gaussian white noise. Such processes satisfy Assumption or holds (respectively);

-

2.

the ARFIMA processes with parameter such that and an innovation process which is a Gaussian white noise. Such ARFIMA processes satisfy Assumption (note that ARIMA processes are particular cases of ARFIMA processes).

-

3.

the Gaussian stationary processes , such as its spectral density is

(5.1) with , and . Therefore the spectral density implies that Assumption holds. In the sequel we will use and , implying that the second order term of the spectral density is less negligible than in case of FARIMA processes.

Comparison of with other semiparametric estimators of

Here we first compare the performance of the adaptive MIR-estimator with other famous semiparametric estimators of :

-

•

is the adaptive global log-periodogram estimator introduced by Moulines and Soulier (2003), also called FEXP estimator, with bias-variance balance parameter . Such an estimator was shown to be consistent for .

-

•

is the extended local Whittle estimator defined by Abadir, Distaso and Giraitis (2007) which is consistent for . It is a generalization of the local Whittle estimator introduced by Robinson (1995b), consistent for , following a first extension proposed by Phillips (1999) and Shimotsu and Phillips (2005). This estimator avoids the tapering used for instance in Velasco (1999b) or Hurvich and Chen (2000). The trimming parameter is chosen as (this is not an adaptive estimator) following the numerical recommendations of Abadir et al. (2007).

-

•

is an adaptive wavelet based estimator introduced in Bardet et al. (2013) using a Lemarie-Meyer type wavelet (another similar choice could be the adaptive wavelet estimator introduced in Veitch et al., 2003, using a Daubechie’s wavelet, but its robustness property are slightly less interesting). The asymptotic normality of such estimator is established for (when the number of vanishing moments of the wavelet function is large enough).

Note that only is the not adaptive among the estimators.

Table 1, 2, 3 and 4 respectively provide the results of simulations for ARIMA, ARFIMA, ARFIMA and processes for several values of and .

| ARIMA | =-0.5 | =-0.7 | =-0.9 | =-0.1 | =-0.3 | =-0.5 |

|---|---|---|---|---|---|---|

| 0.163 | 0.265 | 0.640 | 0.093 | 0.102 | 0.109 | |

| 0.138 | 0.148 | 0.412 | 0.172 | 0.163 | 0.170 | |

| 0.125 | 0.269 | 0.679 | 0.074 | 0.078 | 0.120 | |

| 0.246 | 0.411 | 0.758 | 0.067 | 0.099 | 0.133 |

| ARFIMA(1,d,0) | =-0.5 | =-0.7 | =-0.9 | =-0.1 | =-0.3 | =-0.5 |

|---|---|---|---|---|---|---|

| 0.077 | 0.106 | 0.293 | 0.027 | 0.048 | 0.062 | |

| 0.045 | 0.050 | 0.230 | 0.046 | 0.046 | 0.040 | |

| 0.043 | 0.085 | 0.379 | 0.031 | 0.032 | 0.036 | |

| 0.080 | 0.103 | 0.210 | 0.037 | 0.044 | 0.054 |

| ARFIMA(0,d,0) | ||||||||

|---|---|---|---|---|---|---|---|---|

| 0.088 | 0.092 | 0.097 | 0.096 | 0.101 | 0.101 | 0.099 | 0.105 | |

| 0.144 | 0.134 | 0.146 | 0.152 | 0.168 | 0.175 | 0.165 | 0.157 | |

| 0.075 | 0.078 | 0.080 | 0.084 | 0.083 | 0.079 | 0.077 | 0.081 | |

| 0.071 | 0.079 | 0.087 | 0.088 | 0.087 | 0.085 | 0.069 | 0.076 |

| ARFIMA(0,d,0) | ||||||||

|---|---|---|---|---|---|---|---|---|

| 0.037 | 0.025 | 0.031 | 0.031 | 0.035 | 0.035 | 0.038 | 0.049 | |

| 0.043 | 0.042 | 0.043 | 0.042 | 0.055 | 0.054 | 0.046 | 0.147 | |

| 0.034 | 0.033 | 0.032 | 0.036 | 0.033 | 0.032 | 0.033 | 0.032 | |

| 0.033 | 0.032 | 0.031 | 0.023 | 0.023 | 0.038 | 0.039 | 0.041 |

| ARFIMA(1,d,1) | ||||||||

| ; | ||||||||

| 0.152 | 0.132 | 0.125 | 0.125 | 0.118 | 0.117 | 0.111 | 0.112 | |

| 0.138 | 0.137 | 0.144 | 0.155 | 0.161 | 0.179 | 0.172 | 0.170 | |

| 0.092 | 0.088 | 0.090 | 0.097 | 0.096 | 0.087 | 0.087 | 0.087 | |

| 0.173 | 0.154 | 0.152 | 0.148 | 0.139 | 0.132 | 0.105 | 0.098 |

| ARFIMA(1,d,1) | ||||||||

| ; | ||||||||

| 0.070 | 0.062 | 0.053 | 0.052 | 0.052 | 0.054 | 0.059 | 0.58 | |

| 0.038 | 0.042 | 0.041 | 0.050 | 0.052 | 0.054 | 0.045 | 0.150 | |

| 0.039 | 0.035 | 0.033 | 0.037 | 0.038 | 0.037 | 0.035 | 0.033 | |

| 0.049 | 0.057 | 0.056 | 0.053 | 0.051 | 0.050 | 0.048 | 0.050 |

| 0.140 | 0.170 | 0.201 | 0.211 | 0.209 | 0.205 | 0.210 | 0.202 | |

| 0.187 | 0.188 | 0.204 | 0.200 | 0.192 | 0.187 | 0.200 | 0.192 | |

| 0.177 | 0.182 | 0.190 | 0.184 | 0.174 | 0.179 | 0.196 | 0.189 | |

| 0.224 | 0.225 | 0.230 | 0.220 | 0.213 | 0.199 | 0.185 | 0.175 |

| 0.110 | 0.139 | 0.150 | 0.151 | 0.152 | 0.153 | 0.152 | 0.142 | |

| 0.120 | 0.123 | 0.132 | 0.131 | 0.132 | 0.127 | 0.134 | 0.155 | |

| 0.139 | 0.138 | 0.141 | 0.134 | 0.134 | 0.140 | 0.140 | 0.145 | |

| 0.170 | 0.173 | 0.167 | 0.165 | 0.167 | 0.166 | 0.164 | 0.150 |

Conclusions of simulations: In almost of cases (especially for ), the estimator provides the smallest among the semiparametric estimators even if this estimator is not an adaptive estimator (the bandwidth is fixed to be , which should theretically be a problem when , i.e. ). However, even for the process with , the estimator provides not so bad results (when , note that never provides the best results contrarly to what happens with the other processes sayisfying ). Some additional simulations, not reported here, realized with always for with , show that the of becomes the worst (the largest) among the of the other estimators. The estimator provide convincing results, almost the same performances than the other adaptive estimators and .

Comparison of MIR tests and with other famous stationarity or nonstationarity tests

Monte-Carlo experiments were done for evaluating the performances of new tests and and for comparing them to most famous stationarity tests (LMC and V/S, V/S replacing KPSS) or nonstationarity (ADF and PP) tests (see more details on these tests in the previous section).

We also defined a stationarity and nonstationarity test based on the extended local Whittle estimator following the results obtained in Abadir et al. (2007) (a very simple central limit theorem was stated in Corollary 2.1). Then, for instance, the stationarity test is defined by

with (and the nonstationarity test is built following the same trick).

-

•

for LMC test;

-

•

for V/S test;

-

•

for ADF test;

-

•

for PP test;

The results of these simulations with a type I error classically chosen to are provided in Tables 5, 6, 7 and 8.

| ARIMA | =-0.5 | =-0.7 | =-0.9 | =-0.1 | =-0.3 | =-0.5 |

| : Accepted | 1 | 1 | 0.37 | 0 | 0 | 0 |

| : Accepted | 1 | 1 | 0.25 | 0 | 0 | 0 |

| LMC: Accepted | 0.97 | 1 | 0.84 | 0.02 | 0 | 0 |

| : Accepted | 0.96 | 0.93 | 0.84 | 0.09 | 0.08 | 0.12 |

| : Rejected | 0.99 | 0.77 | 0.08 | 0 | 0 | 0 |

| : Rejected | 1 | 0.94 | 0 | 0 | 0 | 0 |

| ADF: Rejected | 1 | 1 | 1 | 0.06 | 0.04 | 0.04 |

| PP : Rejected | 1 | 1 | 1 | 0.06 | 0.03 | 0.02 |

| ARIMA | =-0.5 | =-0.7 | =-0.9 | =-0.1 | =-0.3 | =-0.5 |

| : Accepted | 1 | 1 | 0.91 | 0 | 0 | 0 |

| : Accepted | 1 | 1 | 1 | 0 | 0 | 0 |

| LMC: Accepted | 0.95 | 1 | 1 | 0 | 0 | 0 |

| : Accepted | 0.93 | 0.97 | 0.90 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 0.87 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 0.95 | 0 | 0 | 0 |

| ADF: Rejected | 1 | 1 | 1 | 0.09 | 0.01 | 0.04 |

| PP : Rejected | 1 | 1 | 1 | 0.07 | 0.01 | 0.04 |

| ARFIMA | ||||||||

| : Accepted | 1 | 1 | 1 | 1 | 0.72 | 0.09 | 0.01 | 0 |

| : Accepted | 1 | 1 | 1 | 1 | 0.53 | 0.02 | 0 | 0 |

| LMC: Accepted | 0 | 0.06 | 0.75 | 1 | 1 | 1 | 0.52 | 0 |

| : Accepted | 1 | 0.97 | 0.81 | 0.51 | 0.30 | 0.20 | 0.09 | 0.05 |

| : Rejected | 1 | 1 | 0.97 | 0.53 | 0.02 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 0.99 | 0.48 | 0.01 | 0 | 0 | 0 |

| ADF: Rejected | 1 | 1 | 1 | 0.98 | 0.60 | 0.24 | 0.06 | 0.01 |

| PP : Rejected | 1 | 1 | 1 | 1 | 0.90 | 0.43 | 0.05 | 0 |

| ARFIMA | ||||||||

| : Accepted | 1 | 1 | 1 | 1 | 0.08 | 0 | 0 | 0 |

| : Accepted | 1 | 1 | 1 | 1 | 0.06 | 0 | 0 | 0 |

| LMC: Accepted | 0 | 0.05 | 0.97 | 1 | 1 | 1 | 0.53 | 0 |

| : Accepted | 1 | 0.95 | 0.50 | 0.17 | 0.05 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 1 | 0.94 | 0 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 1 | 0.89 | 0 | 0 | 0 | 0 |

| ADF: Rejected | 1 | 1 | 1 | 1 | 0.88 | 0.53 | 0.07 | 0 |

| PP : Rejected | 1 | 1 | 1 | 1 | 1 | 0.75 | 0.07 | 0 |

| ARFIMA | ||||||||

| ; | ||||||||

| : Accepted | 1 | 1 | 1 | 0.95 | 0.47 | 0.11 | 0.01 | 0 |

| : Accepted | 1 | 1 | 1 | 0.98 | 0.31 | 0 | 0 | 0 |

| LMC: Accepted | 0.12 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| : Accepted | 1 | 0.96 | 0.78 | 0.54 | 0.34 | 0.18 | 0.09 | 0.05 |

| : Rejected | 1 | 1 | 0.84 | 0.23 | 0.01 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 0.96 | 0.21 | 0 | 0 | 0 | 0 |

| ADF: Rejected | 1 | 1 | 1 | 0.96 | 0.59 | 0.26 | 0.05 | 0.01 |

| PP : Rejected | 1 | 1 | 1 | 1 | 0.74 | 0.30 | 0.03 | 0 |

| ARFIMA | ||||||||

| ; | ||||||||

| : Accepted | 1 | 1 | 1 | 0.99 | 0.12 | 0 | 0 | 0 |

| : Accepted | 1 | 1 | 1 | 1 | 0.04 | 0 | 0 | 0 |

| LMC: Accepted | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| : Accepted | 1 | 0.95 | 0.61 | 0.22 | 0.07 | 0 | 0.01 | 0 |

| : Rejected | 1 | 1 | 1 | 0.67 | 0.01 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 1 | 0.86 | 0 | 0 | 0 | 0 |

| ADF: Rejected | 1 | 1 | 1 | 1 | 0.91 | 0.45 | 0.04 | 0 |

| PP : Rejected | 1 | 1 | 1 | 1 | 0.99 | 0.59 | 0.03 | 0 |

| : Accepted | 1 | 1 | 1 | 1 | 0.99 | 0.49 | 0.05 | 0.01 |

| : Accepted | 1 | 1 | 1 | 1 | 0.98 | 0.34 | 0.01 | 0 |

| LMC: Accepted | 0 | 0 | 0.13 | 0.86 | 1 | 1 | 0.82 | 0 |

| : Accepted | 1 | 1 | 0.93 | 0.69 | 0.42 | 0.25 | 0.16 | 0.09 |

| : Rejected | 1 | 1 | 1 | 0.93 | 0.37 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 1 | 0.98 | 0.23 | 0 | 0 | 0 |

| ADF: Rejected | 1 | 1 | 1 | 1 | 1 | 0.88 | 0.38 | 0.11 |

| PP : Rejected | 1 | 1 | 1 | 1 | 0.90 | 0.43 | 0.05 | 0 |

| : Accepted | 1 | 1 | 1 | 1 | 1 | 0.03 | 0 | 0 |

| : Accepted | 1 | 1 | 1 | 1 | 0.99 | 0 | 0 | 0 |

| LMC: Accepted | 0 | 0 | 0.39 | 1 | 1 | 1 | 1 | 0 |

| : Accepted | 1 | 0.99 | 0.79 | 0.29 | 0.11 | 0.04 | 0 | 0 |

| : Rejected | 1 | 1 | 1 | 0.99 | 0.82 | 0 | 0 | 0 |

| : Rejected | 1 | 1 | 1 | 1 | 0.30 | 0 | 0 | 0 |

| ADF: Rejected | 1 | 1 | 1 | 1 | 1 | 0.98 | 0.34 | 0.01 |

| PP : Rejected | 1 | 1 | 1 | 1 | 1 | 1 | 0.50 | 0.01 |

Conclusions of simulations: From their constructions, KPSS and LMC, V/S (or KPSS), ADF and PP tests should asymptotically decide the stationarity hypothesis when , and the nonstationarity hypothesis when . It was exactly what we observe in these simulations. For ARIMA processes with or (i.e. AR process when ), LMC, V/S, ADF and PP tests are more accurate than our adaptive MIR tests or tests based on , especially when . But when the tests computed from and provide however convincing results.

In case of processes with , the tests computed from and are clearly better performances than than classical stationarity tests ADF or PP which accept the nonstationarity assumption even if the processes are stationary when for instance. The results obtained with the LMC test are not at all satisfying even when another lag parameter is chosen. The case of the V/S test is different since this test is built for distinguishing between short and long memory processes. Note that a renormlized version of this test has been defined in Giraitis et al. (2006) for also taking account of the value of .

5.3 Application to the the Stocks and the Exchange Rate Markets

We applied the adaptive MIR statistics as well as the other famous long-memory estimators and stationarity tests to Econometric data, the Stocks and Exchange Rate Markets. More precisely, the following daily closing value time series are considered:

-

1.

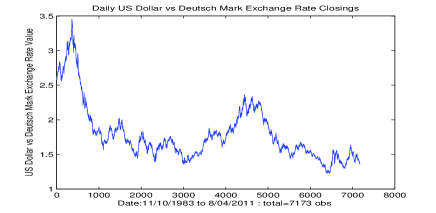

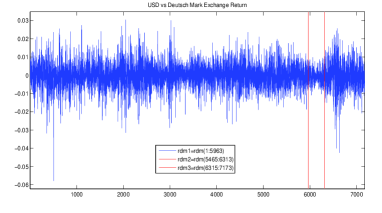

The USA Dollar Exchange rate in Deusch-Mark, from to ( obs.).

-

2.

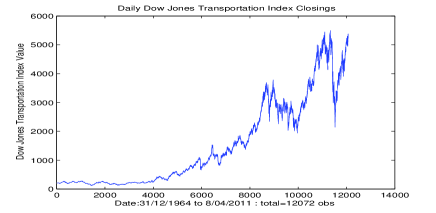

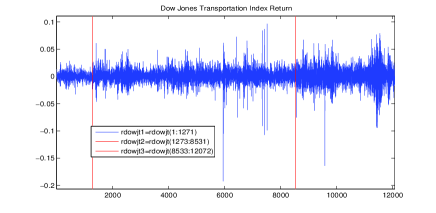

The USA Dow Jones Transportation Index, from to ( obs.).

-

3.

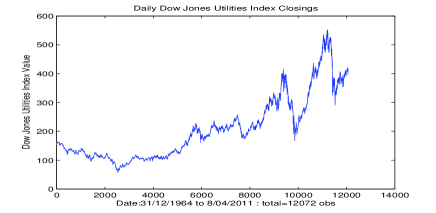

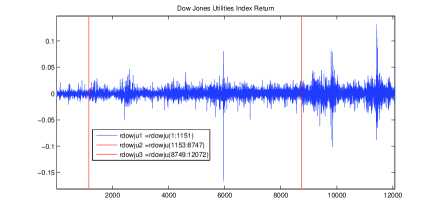

The USA Dow Jones Utilities Index, from to ( obs.).

-

4.

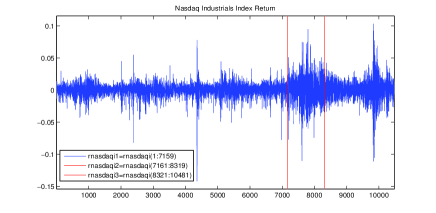

The USA Nasdaq Industrials Index, from to ( obs.).

-

5.

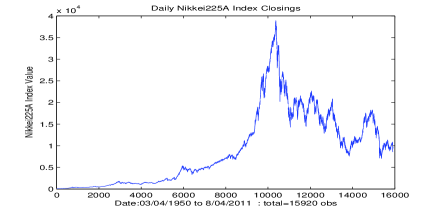

The Japan Nikkei225A Index, from to ( obs.).

We considered the log-return of this data and tried to test their stationarity properties. Since stationarity or nonstationarity tests are not able to detect (offline) changes, we first used an algorithm developed by M. Lavielle for detecting changes (this free software can be downloaded from his homepage: http://www.math.u-psud.fr/lavielle/programmeslavielle.html). This algorithm provides the choice of detecting changes in mean, in variance, …, and we chose to detect parametric changes in the distribution. Note that the number of changes is also estimated since this algorithm is based on the minimization of a penalized contrast. We obtained for each time series an estimated number of changes equal to which are the following:

-

•

Two breaks points for the US dollar-Deutsch Mark Exchange rate return are estimated, corresponding to the dates: 21/08/2006 and 24/12/2007. The Financial crisis of 2007-2011, followed by the late 2000s recession and the 2010 European sovereign debt crisis can cause such breaks.

-

•

Both the breaks points estimated for the US Dow Jones Transportation Index return, of the New-York Stock Market, correspond to the dates: 17/11/1969 and 15/09/1997. The first break change can be a consequence on transportation companies difficulties the American Viet-Nam war against communist block. The second change point can be viewed as a contagion by the spread of the Thai crisis in 1997 to other countries and mainly the US stock Market.

-

•

Both the breaks points estimated for the US Dow Jones Utilities Index return correspond to the dates: 02/06/1969 and 14/07/1998. The same arguments as above can justify the first break. The second at 1998 is probably a consequence of “the long very acute crisis in the bond markets,…, the dramatic fiscal crisis and Russian Flight to quality caused by it, may have been warning the largest known by the global financial system: we never went too close to a definitive breakdown of relations between the various financial instruments“(Wikipedia).

-

•

The two breaks points for the US Nasdaq Industrials Index return correspond to the dates: 17/07/1998 and 27/12/2002. The first break at 1998 is explained by the Russian flight to quality as above. The second break at 2002 corresponds to the Brazilian public debt crisis of 2002 toward foreign owners (mainly the U.S. and the IMF) which implicitly assigns a default of payment probability close to 100% with a direct impact on the financial markets indexes as the Nasdaq.

-

•

Both the breaks points estimated for the Japanese Nikkei225A Index return corresponds to the dates 29/10/1975 and 12/02/1990, perhaps as consequence of the strong dependency of Japan to the middle east Oil following 1974 or anticipating 1990 oil crisis. The credit crunch which is seen as a major factor in the U.S. recession of 1990-91 can play a role in the second break point.

Data and estimated instant breaks can be seen on Figure 1. Then, we applied the estimators and tests described in the previous subsection on trajectories obtained in each stages for the economic time series. These applications were done on the log-returns, their absolute values, their squared values and their -power laws with maximized for each LRD estimators. The results of these numerical experiments can be seen in Tables 9-13.

Conclusions of numerical experiments: We exhibited again the well known result: the log-returns are stationary and short memory processes while absolute values or power of log-returns are generally stationary but long memory processes (for this conclusion, we essentially consider the results of , and V/S tests since the other tests have been shown not to be relevant in the cases of long-memory processes). However the last and third estimated stage of each time series provides generally the largest estimated values of the memory parameter (for power law of log-returns) which are close to ; hence, for Nasdaq time series, we accepted the nonstationarity assumption.

r=(USD1 vs Deutsh-Mark Exchange Rate Return) Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S S S SM 5.5 -0.2 -0.031 0.059 0.057 -0.007 S S S S S S SM 3.4 0.1 0.034 0.169 0.122 -0.015 S S S S S S SM 5.3 -0.4 0.098 0.140 0.043 0.019

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S NS NS LM 9.5 1.8 0.294 0.301 0.344 0.275 S S NS S NS NS LM 3.6 1.1 -0.121 0.153 0.414 -0.038 S S S S NS NS LM 9.2 1.8 0.168 0.417 0.389 0.410

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S S S LM 289.5 10.7 0.081 0.258 0.298 0.078 S S S S NS S LM 8.7 2.3 -0.018 0.127 0.431 -0.096 S S S S NS S LM 81.3 7.1 0.035 0.411 0.336 0.428

(Non)Stationarity Test LRD Kurtosis Skewness ADF PP KPSS LMC =0.32 S S NS S NS NS SM 3.5 -0.5 0.321* 0.251 0.256 0.343 = 0.97 S S S S NS NS SM 8.7 1.1 0.293 0.301* 0.343 0.275 = 1.12 S S S S NS NS SM 13.7 2.3 0.302 0.300 0.345* 0.273 =0.77 S S S S NS NS SM 5.1 1.1 0.273 0.298 0.335 0.379* =0.05 S S NS NS S NS LM 27.9 -5.0 0.246* 0.078 -0.005 0.103 = 1.31 S S S S NS NS LM 4.9 1.5 -0.103 0.166* 0.446 -0.072 =1.50 S S S S NS S LM 5.8 1.8 -0.092 0.162 0.450* -0.082 =0.03 S S NS NS S NS LM 30.9 -5.4 0.239 0.113 -0.030 0.211* =0.63 S S NS NS NS NS LM 3.8 0.7 0.244* 0.354 0.333 0.097 = 1.44 S S S S NS NS LM 27.1 3.7 0.159 0.436* 0.387 0.441 = 1.19 S S S S NS NS LM 14.9 2.6 0.168 0.430 0.394* 0.430 = 2.90 S S S S NS S LM 223.4 13.3 0.053 0.291 0.233 0.475*

r=Dow Jones Transportation Index Return Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S S NS SM 4.6 0.0 0.218 0.174 0.098 0.198 S S S S S S SM 21.7 -0.8 0.053 0.002 0.008 -0.404 S S S S S S SM 8.3 -0.3 0.002 -0.015 -0.034 -0.038

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S NS NS LM 6.1 1.5 0.154 0.320 0.270 0.166 S S S S NS NS LM 57.3 4.4 0.322 0.260 0.240 0.168 S S S S NS NS LM 16.3 2.5 0.405 0.476 0.496 0.374

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S NS S LM 32.3 4.4 0.158 0.284 0.231 0.231 S S S S S NS LM 2301.5 39.9 0.334 0.122 0.093 0.118 S NS S S NS NS LM 459.0 15.5 0.416 0.452 0.434 0.356

(Non)Stationarity Test LRD Kurtosis Skewness ADF PP KPSS LMC = 1.83 S S S S NS S LM 25.0 3.8 0.252* 0.291 0.237 0.202 = 0.45 S S NS S NS NS LM 2.7 0.4 0.118 0.331* 0.290 0.047 = 0.36 S S NS S NS NS LM 2.9 -0.4 0.118 0.329 0.291* 0.237 = 0.03 S S NS S NS NS LM 12.8 -3.4 0.149 0.257 0.260 0.327* = 2.06 S S S S S NS LM 2551.6 42.6 0.355* 0.113 0.086 0.110 = 0.68 S S S S NS NS LM 10.6 1.6 0.308 0.276* 0.261 0.135 = 0.65 S S S S NS NS LM 9.2 1.4 0.303 0.276 0.261* 0.129 = 1.29 S S S S NS NS LM 246.8 10.1 0.330 0.227 0.200 0.504* = 0.66 S NS S S NS NS LM 5.4 1.1 0.444* 0.435 0.461 0.374 = 1.38 S S S S NS NS LM 64.8 5.2 0.402 0.492* 0.499 0.391 = 1.22 S S S S NS NS LM 36.2 3.8 0.400 0.489 0.502* 0.387 = 2.75 S S S S NS NS LM 1698.7 35.8 0.407 0.315 0.287 0.466*

r=Dow Jones Utilities Index Return Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S S S SM 7.3 0.6 0.191 0.037 -0.132 0.222 S S S S S S SM 43.2 -1.3 0.094 0.025 0.001 0.043 S S S S S S SM 13.0 0.0 0.026 0.024 0.001 -0.032

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S NS NS LM 11.9 2.4 0.283 0.287 0.316 0.225 S S S S NS NS LM 127.4 5.9 0.134 0.301 0.304 0.184 S S S S NS NS LM 25.5 3.4 0.417 0.559 0.484 0.595

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S NS S LM 63.1 6.7 0.250 0.253 0.212 0.270 S S S S NS NS LM 5322.4 67.8 0.130 0.100 0.100 0.100 S NS S S NS NS LM 289.6 14.0 0.510 0.468 0.423 0.513

(Non)Stationarity Test LRD Kurtosis Skewness ADF PP KPSS LMC S S NS S NS NS LM 3.3 -0.1 0.354* 0.262 0.327 0.145 S S S S NS NS LM 14.6 8.4 0.215 0.288* 0.308 0.234 S S NS S NS NS LM 4.5 0.8 0.311 0.276 0.336* 0.396 S S S S NS NS LM 4.8 1.0 0.310 0.278 0.336 0.398* S S S S S S LM 7320.6 84.9 0.165* 0.015 0.017 0.040 S S S S NS NS LM 9.1 1.2 0.113 0.330* 0.327 0.113 S S S S NS NS LM 13.0 1.6 0.117 0.330 0.327* 0.113 S S S S NS NS LM 4386.6 59.1 0.125 0.130 0.129 0.377* S NS S S NS NS LM 683.1 22.5 0.527* 0.394 0.344 0.426 S S S S NS NS LM 21.6 3.1 0.415 0.560* 0.483 0.544 S S S S NS NS LM 35.2 4.2 0.421 0.557 0.485* 0.364 S S S S NS NS LM 28.2 3.7 0.419 0.559 0.484 0.723*

r=Nasdaq Industrials Index Return Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S S S SM 20.7 -1.5 0.141 0.073 0.092 -0.202 S S S S S S SM 4.6 0.0 0.012 0.070 0.116 0.014 S S S S NS S SM 10.4 -0.3 0.045 0.078 0.082 -0.045

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S S NS SM 52.4 4.4 0.361 0.309 0.287 0.274 S S S S NS NS LM 7.4 1.6 0.284 0.532 0.504 0.385 S NS S NS NS NS LM 18.3 3.0 0.516 0.761 0.606 0.668

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S S NS SM 1356.8 31.4 0.381 0.146 0.114 0.100 S S S S NS NS LM 49.0 5.4 0.304 0.466 0.378 0.432 S NS S S NS NS LM 140.0 10.0 0.498 0.786 0.544 0.708

(Non)Stationarity Test LRD Kurtosis Skewness ADF PP KPSS LMC S S S S S NS LM 63.7 4.9 0.396* 0.304 0.281 0.325 S S S S NS NS LM 10.2 0.7 0.188 0.329* 0.325 0.293 S S S S NS NS LM 6.3 0.9 0.178 0.326 0.328* 0.275 S S S S NS NS LM 22.4 2.6 0.199 0.324 0.311 0.587* S S S S NS S LM 142.0 9.8 0.317* 0.374 0.276 0.263 S S S S NS NS LM 7.9 1.7 0.284 0.532* 0.501 0.388 S S NS S NS NS LM 4.2 0.9 0.300 0.517 0.517* 0.340 S S S S NS NS LM 39.8 4.8 0.299 0.479 0.395 0.432* S NS S S NS S LM 256.9 14.3 0.548* 0.272 0.479 0.669 S NS S S NS NS LM 89.1 7.7 0.504 0.801* 0.575 0.739 S NS S S NS NS LM 26.0 3.7 0.526 0.772 0.608* 0.671 S NS S S NS NS LM 36.0 4.5 0.532 0.782 0.606 0.760*

r=Nikkei 225A Index Return Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S S S SM 12.6 -0.6 0.083 0.067 0.084 0.022 S S S S S S SM 63.7 -2.3 -0.021 -0.016 -0.013 -0.039 S S S S S S SM 9.0 -0.1 0.033 0.047 -0.005 -0.015

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S NS NS LM 26.1 3.3 0.302 0.343 0.313 0.218 S S S S NS NS LM 150.9 7.5 0.196 0.346 0.304 0.321 S S S S NS NS LM 17.0 2.6 0.413 0.415 0.431 0.335

Segments (Non)Stationarity Test LRD Kurtosis Skewness Breaks ADF PP KPSS LMC S S S S NS NS LM 427.8 16.9 0.275 0.241 0.267 0.080 S S S S S NS LM 2610.8 48.0 0.230 0.146 0.154 0.117 S S S S NS NS LM 235.5 12.3 0.381 0.396 0.363 0.377

(Non)Stationarity Test LRD Kurtosis Skewness ADF PP KPSS LMC S S S S NS NS LM 149.8 9.0 0.323* 0.296 0.296 0.201 S S S S NS NS LM 15.4 4.4 0.286 0.345* 0.311 0.213 S S S S NS NS LM 27.1 3.4 0.303 0.342 0.313* 0.218 S S S S NS NS LM 74.8 6.1 0.273 0.322 0.307 0.622* S S S S S S LM 3487.4 58.3 0.252* 0.037 0.042 0.045 S S S S NS NS SM 55.5 4.1 0.180 0.353* 0.304 0.154 S S S S NS NS SM 87.1 5.3 0.186 0.352 0.305* 0.035 S S S S S NS SM 1697.1 35.8 0.221 0.220 0.222 0.465* S NS S S NS NS LM 35.7 4.1 0.467* 0.412 0.426 0.386 S S S S NS NS LM 11.0 2.0 0.429 0.415* 0.428 0.351 S S S S NS NS LM 17.0 2.6 0.413 0.415 0.431* 0.335 S NS S S NS NS LM 40.3 4.4 0.467 0.411 0.424 0.425*

6 Proofs

Proof of Proposition 1.

This proposition is based on results of Surgailis et al. (2008) and was already proved in Bardet et Dola (2012) in the case .

Mutatis mutandis, the case can be treated exactly following the same steps.

The only new proof which has to be established concerns the case since Surgailis et al. (2008) do not provide a CLT satisfied by the (unidimensional) statistic in this case. Let the standardized process defined Surgailis et al. (2008). Then, for ,

Denote as in (5.39) of Surgailis et al. (2008). Both inequalities (5.41) and (5.42) remain true for and

Now let . The Hermite rank of the function is and therefore the equation (5.23) of Surgailis et al. (2008) obtained from Arcones Lemma remains valid. Hence:

from Lemma (8.2) and then the equations (5.28-5.31) remain valid for all . Then for ,

with . ∎

Proof of Property 2.1.

As in Surgailis et al (2008), we can write:

Therefore an expansion of provides an expansion of when .

Step 1 Let satisfy Assumption . Then we are going to establish that there exist positive real numbers , and specified in (6.2), (6.3) and (6.4) such that for and with defined in (2.14),

Under Assumption and with defined in (6.16) in Lemma 6.16, it is clear that,

since . Now using the results of Lemma 6.16 and constants , and , , defined in Lemma 6.16,

1. Let , i.e. . Then

As a consequence,,

| (6.2) |

and numerical experiments proves that is negative for any and .

2. Let , i.e. . Then,

As a consequence,

| (6.3) |

and numerical experiments proves that is negative for any and .

3. Let , i.e. . Then,

As a consequence,

| (6.4) |

and numerical experiments proves that is negative for any and .

4. Let . Then,

Once again with Lemma 6.16:

As a consequence,

| (6.5) |

Step 2: A Taylor expansion of around provides:

Note that numerical experiments show that for any . As a consequence, using the previous expansions of obtained in Step 1 and since , then for all :

Proof of Theorem 1.

Using Property 2.1, if with and then and it implies that the multidimensional CLT (2.9) can be replaced by

| (6.9) |

It remains to apply the Delta-method with the function to CLT (6.9). This is possible since the function is an increasing function such that and for all . It achieves the proof of Theorem 1. ∎

Proof of Proposition 2.

See Bardet and Dola (2012). ∎

Proof of Theorem 2.

See Bardet and Dola (2012). ∎

Appendix

We first recall usual equalities frequently used in the sequel:

Lemma 6.1.

For all

-

1.

For , ;

-

2.

For , ;

-

3.

For , .

Proof.

These equations are given or deduced (using decompositions of and integration by parts) from (see Doukhan et al., p. 31).

∎

Lemma 6.2.

For , denote

| (6.10) |

Then, we have the following expansions when :

| (6.16) |

with the following real constants (which do not vanish for any on the corresponding set):

Proof.

The proof of these expansions follows the steps than those of Lemma 5.1 in Bardet and Dola (2012). Hence we write for ,

| (6.17) |

with

The expansions when of both the right hand sided integrals in (6.17) are obtained from Lemma 6.1. It remains to obtain the expansion of . Then, using classical trigonometric and Taylor expansions:

the expansions of can be obtained.

Numerical experiments show that , , and . ∎

References

- [1] Abadir, K.M., Distaso, W. and Giraitis, L. 2007. Nonstationarity-extended local Whittle estimation. J. Econometrics, 141, 1353-1384.

- [2] Abry, P., Veitch, D. and Flandrin, P. 1998. Long-range dependent: revisiting aggregation with wavelets. J. Time Ser. Anal. , 19, 253-266.

- [3] Bardet, J.M. and Bibi H. 2013. Adaptive semiparametric wavelet estimator and goodness-of-fit test for long-memory linear processes. Electronic Journal of Statistics, 7, 1-54.

- [4] Bardet, J.M., Bibi H. and Jouini, A. 2008. Adaptive wavelet-based estimator of the memory parameter for stationary Gaussian processes. Bernoulli, 14, 691-724.

- [5] Bardet, J.M. and Dola B. 2012. Adaptive estimator of the memory parameter and goodness-of-fit test using a multidimensional increment ratio statistic. Journal of Multivariate Analysis, 105, 222-240.

- [6] Bardet J.M. and Surgailis, D. 2011. Measuring the roughness of random paths by increment ratios. Bernoulli, 17, 749-780.

- [7] Beran, J. 1994. Statistics for Long-Memory Processes. Chapman and Hall, New York.

- [8] Doukhan, P., Oppenheim, G. and Taqqu M.S. (Editors) 2003. Theory and applications of long-range dependence, Birkhäuser.

- [9] Elder, J. and Kennedy, P.E. 2001. Testing for Unit Roots : What Should Students Be Taught? Journal of Economic Education, 32, 137-146.

- [10] Giraitis, L., Kokoszka, P. and Leipus, R. 2001. Testing for long memory in the presence of a general trend. J. Appl. Probab. 38, 1033-1054.

- [11] Giraitis, L., Kokoszka, P., Leipus, R. and Teyssière, G. 2003. Rescaled variance and related tests for long memory in volatility and levels. J. Econometrics, 112, 265-294.

- [12] Giraitis, L., Leipus, R. and Philippe, A. 2006. A test for stationarity versus trends and unit roots for a wide class of dependent errors. Econometric Th., 22, 989-1029.

- [13] Giraitis, L., Robinson P.M. and Samarov, A. 1997. Rate optimal semi-parametric estimation of the memory parameter of the Gaussian time series with long range dependence. J. Time Ser. Anal., 18, 49-61.

- [14] Giraitis, L., Robinson P.M., and Samarov, A. 2000. Adaptive semiparametric estimation of the memory parameter. J. Multivariate Anal., 72, 183-207.

- [15] Hamilton, J.D. 1994. Time Series Analysis, Princeton University Press, Princeton, New Jersey.

- [16] Henry, M. and Robinson, P.M. 1996. Bandwidth choice in Gaussian semiparametric estimation of long range dependence. In: Athens Conference on Applied Probability and Time Series Analysis, Vol. II, 220-232, Springer, New York.

- [17] Hurvich, C.M. and Ray, B.K. 1995. Estimation of the Memory Parameter for Nonstationary or Noninvertible Fractionally Integrated Processes. Journal of Time Series Analysis, 16, 17-41.

- [18] Hurvich, C.M. and Chen, W.W. 2000. An Efficient Taper for Potentially Overdifferenced Long-Memory Time Series. Journal of Time Series Analysis, 21, 155-180.

- [19] Iouditsky, A., Moulines, E. and Soulier, P. 2001. Adaptive estimation of the fractional differencing coefficient. Bernoulli, 7, 699-731.

- [20] Leybourne, S.J. and McCabe, B.P.M. 1994. A Consistent Test for a Unit Root. Journal of Business and Economic Statistics, 12, 157-166.

- [21] Leybourne, S.J. and McCabe, B.P.M. 1999. Modified Stationarity Tests with Data-Dependent Model-Selection Rules. Journal of Business and Economic Statistics, 17, 264-270.

- [22] Ling, S. and Li, W.K. 2001. Asymptotic Inference for nonstationary fractionally integrated autoregressive moving-average models. Econometric Theory, 17, 738-765.

- [23] Ling, S. 2003. Adaptive estimators and tests of stationary and non-stationary short and long memory ARIMA-GARCH models. J. Amer. Statist. Assoc., 92, 1184-1192.

- [24] Moulines, E., Roueff, F. and Taqqu, M.S. 2007. On the spectral density of the wavelet coefficients of long memory time series with application to the log-regression estimation of the memory parameter. J. Time Ser. Anal., 28, 155-187.

- [25] Moulines, E. and Soulier, P. 2003. Semiparametric spectral estimation for fractionnal processes. In P. Doukhan, G. Openheim and M.S. Taqqu editors, Theory and applications of long-range dependence, 251-301, Birkhäuser, Boston.

- [26] Nielsen, M.O. 2004. Efficient Likelihood Inference in Nonstationary Univariate Models. Econometric Theory, 20, 116-146.

- [27] Philipps, P.C.B. (1999). Discrete Fourier Transforms of Fractional Processes. Technical Report, Yale University.

- [28] Robinson, P.M. 1994. Efficient Tests of Nonstationary Hypotheses. Journal of the American Statistical Association, 89, 1420-37.

- [29] Robinson, P.M. 1995a. Log-periodogram regression of time series with long range dependence. The Annals of statistics, 23, 1048-1072.

- [30] Robinson, P.M. 1995b. Gaussian semiparametric estimation of long range dependence. The Annals of statistics, 23, 1630-1661.

- [31] Shimotsu, K. and Phillips, P.C.B. 2005. The Exact Local Whittle Estimation of Fractional Integration. The Annals of Statistics, 33, 1890-1933.

- [32] Surgailis, D., Teyssière, G., Vaičiulis, M. 2008. The increment ratio statistic. J. Multiv. Anal., 99, 510-541.

- [33] Tanaka, K. 1999. The Nonstationary Fractional Unit Root. Econometric Theory, 15, 549-582.

- [34] Veitch, D., Abry, P., Taqqu, M.S. 2003. On the Automatic Selection of the Onset of Scaling. Fractals, 11, 377-390.

- [35] Velasco, C. 1999a. Non-stationary log-periodogram regression. Journal of Econometrics, 91, 325-371.

- [36] Velasco, C. 1999b. Gaussian Semiparametric Estimation of Non-stationary Time Series. Journal of Time Series Analysis, 20, 87-127.

- [37] Velasco, C., Robinson, P. 2000. Whittle pseudo-maximum likelihood estimation for nonstationary time series. J. Am. Statist. Assoc., 95, 1229-1243.