From characteristic functions to implied volatility expansions

Abstract

For any strictly positive martingale for which has a characteristic function, we provide an expansion for the implied volatility. This expansion is explicit in the sense that it involves no integrals, but only polynomials in the log strike. We illustrate the versatility of our expansion by computing the approximate implied volatility smile in three well-known martingale models: one finite activity exponential Lévy model (Merton), one infinite activity exponential Lévy model (Variance Gamma), and one stochastic volatility model (Heston). Finally, we illustrate how our expansion can be used to perform a model-free calibration of the empirically observed implied volatility surface.

Keywords: Implied volatility expansions, exponential Lévy, affine class, Heston, additive process,

1 Introduction

While it is rare to find a martingale model for which the transition density is available in closed form (the Black-Scholes model being a notable exception), there is a veritable zoo of models for which the characteristic function is available explicitly (exponential Lévy models and affine models [9] for instance). The existence of an analytically tractable characteristic function allows for (vanilla) option prices to be computed quickly using (generalised) Fourier transforms [25, 26]. Every model contains unobservable parameters, which are usually calibrated to market data. This calibration procedure is typically performed using implied volatilities rather than option prices, the former being dimensionless. For a given model, one therefore has to compute (by finite difference, Monte Carlo or numerical integration) option prices first and then the corresponding implied volatilities by some root-finding algorithm. Both steps require sophisticated numerical tools and occasionally somewhat of an artistic touch. These are computationally expensive and render calibration a long and intensive task.

Over the past decade, many authors have focused on obtaining closed-form approximations for both option prices and implied volatilities, partly in order to speed up this calibration process. Perturbation methods have been used by Lorig and co-authors [28] (see also [10, 11, 13, 19]) to obtain such approximations for diffusion-type models. In extreme regions—where numerical schemes become less efficient—asymptotic expansions of densities and of implied volatilities have been obtained in [3, 7, 15, 20, 33] in the small-maturity case (both for diffusions and jump models) and in [22] for the large-time behaviour of affine stochastic volatility models. Roger Lee [24] pioneered the study of the tails of implied volatility, and more recent (model-dependent and model-free) results have appeared in [2, 7, 12, 17].

The goal of this paper is to derive an approximation for the implied volatility in any model whose characteristic function is available in closed form. This approximation contains no special function and does not require any numerical integration. It can therefore be used efficiently to accelerate the aforementioned calibration issue. The methodology follows and extends the previous works [23, 27] and is related to some extent to the works by Takahashi and Toda [32]. Indeed, by writing the characteristic function as a perturbation around the Black-Scholes characteristic function, our expansion has the form of a Black-Scholes price perturbed by some additional quantity (which we shall make precise later), which can then be turned into an expansion for the corresponding implied volatility.

The rest of the paper proceeds as follows: in Section 2, we provide a brief review of the characteristic function approach to option pricing and introduce some notations needed later in the paper. Section 3 contains the main results, namely a series expansion for the implied volatility. More precisely, we show (Section 3.1) that, whenever the characteristic function is available in closed-form, the European call price can be written as a regular perturbation around the Black-Scholes price. A similar result then holds for the implied volatility, as detailed in Sections 3.2 and 3.3. In Section 4 we numerically test our results and provide practical details about this implementation.

2 Notations and preliminary results

We consider here a given probability space ; all the processes studied will be -adapted. In particular will denote the stock price process, namely a -adapted martingale under the risk-neutral probability measure . The dynamics of may depend on some auxiliary process (), say some stochastic volatility. The starting point is assumed to be non-random. For simplicity and notational convenience, we will assume that and that the risk-free interest rate is zero.

2.1 Pricing via Fourier transforms

Let be the payoff function of a European call option on with strike : , and denote its (generalised) Fourier transform

The results obtained below for option prices remain valid for Put options with payoff , but we shall chiefly consider European call option prices unless otherwise stated. For any , define the moment explosions and . Since is a martingale, we have and . We shall further make the stronger assumption:

Assumption 1.

For any , and .

This assumption holds for most models in practice, and allows us to write the value of a call option as

| (1) |

where we write () for a complex number. Of course the function also depends on , the starting point of , but we shall omit it in the notations for clarity. In this paper, we consider models for which the characteristic function admits the representation

| (2) |

for some analytic function , satisfying for all (martingale property). From (1), this implies that the price of a call option may be written as (see also [25] or [26])

| (3) |

Several well-known models fit within this class

| (4) | |||||

| (5) | |||||

| (6) |

where is a Lévy triplet, are the spot characteristics of an additive process, the function is fully characterised by and the function satisfies a Riccati equation. For precise details on Lévy and affine processes, we refer the interested reader to the monograph by Sato [31] and the groundbreaking paper by Duffie, Filipović and Schachermayer [8].

2.2 Black-Scholes and implied volatility

Option prices are commonly quoted in units of implied volatility (rather than in units of currency) first because the latter is dimensionless, and second, because the shape and behaviour of the implied volatility provide more information than option prices. However, the implied volatility is scarcely available in closed form and has to be computed numerically via inversion of the Black-Scholes formula. We derive here a closed-form expansion for the implied volatility for models whose characteristic function is of the form (2). We begin our analysis by defining the Black-Scholes price and the implied volatility.

Definition 2.

The Black-Scholes price is given by

| (7) |

Remark 3.

Note that is the Lévy exponent of a Brownian motion with volatility and drift , so that (7) is the Fourier representation of the usual Black-Scholes price, more typically written as

| (8) |

where is the cumulative distribution function of a standard normal random variable.

Definition 4.

For any maturity , starting point and (log) strike , the implied volatility is defined as the unique non negative real solution to the equation , where is the (observed or computed) call option price with the same maturity and log strike.

Remark 5.

For any , the existence and uniqueness of the implied volatility can be deduced using the general arbitrage bounds for call prices and the monotonicity of (see [11, Section 2.1, Remark (i)]).

For any , , the function is analytic on , and hence for any and such that , the function at the point is given by its Taylor series:

| (9) |

where The interchange of the derivative and integral operators is justified by Fubini’s theorem. If one observes the option price , then the following proposition provides a way to compute the corresponding implied volatility.

Proposition 6.

For any , , let be defined (as a function of ) by , and let be some strictly positive real number. Then the following expansion holds:

| (10) |

Proof.

Since the function is strictly increasing on , analytic in a neighbourhood of and , the proposition follows from Lagrange Inversion Theorem [1, Equation 3.6.6]. ∎

Proposition 6 shows that, for every fixed , , , there exists some radius of convergence (depending on ) such that implies that , defined implicitly through the equation , is fully characterised by (10). This result however seems to be only of theoretical interest. Once the option value is known, computing the implied volatility inverting the Black-Scholes formula is a simple numerical exercise. Moreover, computing the implied volatility using (10) is not numerically efficient since the option price requires the computation of a (possibly highly oscillatory) Fourier integral. One may wish to use (10) to deduce some properties of the implied volatility, but then the proposition would benefit from precise error bounds when truncating the infinite sum. The rest of the paper focuses on developing a similar expansion, without the need for the (potentially computer-intensive) implementation of the value function .

3 Implied volatility expansions

3.1 Call prices as perturbations around Black-Scholes

For any and define the function by

where is the Black-Scholes characteristic function from Definition 2 and

| (11) |

Recall from Bochner theorem [29, Theorem 4.2.2] that a complex-valued function is a characteristic function if and only if it is non-negative definite and . Therefore is a well-defined characteristic function for any , and we can associate to it a (unique up to indistinguishability) stochastic process , starting at , which is a true martingale. The price of a call option written on thus reads

| (12) |

Let denote the implied volatility corresponding to the option price . Since and , the implied volatility corresponding to the option price is given by . We now seek an expression for . The first step is to show that can be written as a power series in , whose first term corresponds to the Black-Scholes call price with volatility . To this end, we first expand as

and deduce a series representation for in (12):

| (13) |

for any , where the application of Fubini’s theorem is justified since is finite. Note in particular that .

3.2 Series expansion for implied volatility

From (13), it is clear that is an analytic function of (we have explicitly provided its power series representation). Since the composition of two analytic functions is also analytic [5, Section 24, p. 74], the expansion (9) implies that is an analytic function and therefore has a power series expansion in , which we write , where . The following proposition provides an expansion formula for the coefficients .

Proposition 7.

Fix , , and let denote the radius of convergence of the expansion (10). If for all , then the following expansion holds:

| (14) |

The right-hand side only involves for , so that the sequence can be determined recursively.

Proof.

Let us fix some and . Taylor expanding around the point we obtain

In order to recover the implied volatility from Definition 4, we need to equate the Black-Scholes call price above and the option value in (13), and collect terms of identical powers of :

| (15) | |||||||

| (16) | |||||||

Solving the above equations for the sequence , we find at the zeroth order and for any , the order is given by (14). ∎

Remark 8.

Explicitly, up to we have

| (17) |

where all the functions and are evaluated at .

Remark 9.

Having served its purpose, we now dial up to one. The implied volatility is then given by , where is a fixed positive constant and where the sequence is given by (14).

3.3 Simplification of the expressions for

The expression for the coefficients () in (14) is not straightforward to apply; one needs to compute first the Fourier integrals () via (13), then all the terms of the form (). We provide now a more explicit approximation—without integrals or special functions—for . The key to this simplification is that all the terms and () in (14) can actually be expressed in terms of derivatives of with respect to , the starting point of the log stock price process. Indeed, the classical Black-Scholes relation between the Delta, the Gamma and the Vega for call options, , implies that the derivative can be expressed as a sum of terms of the form . We shall also use the equality , which holds for any polynomial (and actually for any analytic function—simply take to be its power series). We first start with the following theorem, which provides an approximation for the coefficients in (13) as a differential operator acting on .

Theorem 10.

Fix some and . If the power series holds in a complex neighbourhood of the origin, then for any integer , defined in (13) can be written as , where

| (18) |

and where only contains derivatives (with respect to ) of of order higher than .

Remark 11.

Note that the power series for in the theorem starts at , which follows from the fact that the process is conservative. This expansion holds as soon as all the moments of exist and for small enough, which is valid under Assumption 1.

Proof.

Assume that the power series for holds around the origin, where the coefficients read

| (19) |

The martingale condition implies , and hence

| (20) | ||||

| (21) |

Let now be the truncation of the series (21) at the -th order, i.e.

| (22) |

and define the operator acting on by

| (23) |

where is a closed set within the radius of convergence of , and the integral is nothing else than the remainder of the series expansion around the point . Hence for any , in (13) can be written as

| (24) | ||||

| (25) | ||||

| (26) | ||||

| (27) |

where

| (28) | ||||

| (29) |

From the decomposition (22), we can write , where the coefficients are defined in (19). We can now compute

| (30) |

which is precisely the expression given in (18). Regarding , since for any , there exists such that , we have , where denotes the radius of convergence of . The sequence is (eventually) decreasing and the sum tends to zero as tends to infinity, so that the sum can be made arbitrarily small. We then obtain

| (31) | ||||

| (32) |

One can then readily check that the sum behaves as as tends to zero. Therefore, contains derivatives (with respect to ) of of at least order . ∎

Expression (18) motivates the following definition:

Definition 12.

For any integers , and for fixed we define the -th order approximation of the implied volatility as

| (33) |

where, for any , is defined as

| (34) |

Note that is obtained from by replacing in (14) by its th order approximation . The following theorem, proved in Appendix A, is the main result of this paper and provides and explicit expression (not involving the derivatives of Black-Scholes) for the -th order approximation of the implied volatility.

Theorem 13.

Example 14.

To illustrate how the above theorem works in practice, we compute explicitly. Fix and write . Equation (18) implies

| (39) | ||||

| (40) |

Next, using Proposition 20 we have

| (41) | ||||

| (42) | ||||

| (43) |

with defined in (35). From Proposition 19 we then have , where . Therefore, recalling that we obtain

| (44) | ||||

| (45) |

Lastly, from (33)-(34) we have

| (46) |

The explicit expression for can be obtained by inserting (41), (43) and (45) into (46).

4 Numerical implementation: discussions and examples

We now focus on the practical implementation of the results above, namely Theorem 13. Section 4.1 proposes a smoothing procedure to further enhance the applicability of our methodology. In Sections 4.2 and 4.3, we implement our implied volatility expansion in two exponential Lévy models (Merton and Variance Gamma) and one stochastic volatility model (Heston).

4.1 Smoothing with the SVI parameterisation

Option data is often noisy and limited by the number of strikes at which options are liquidly traded. In [14], Jim Gatheral introduces the following Stochastic Volatility Inspired (SVI) parameterisation:

| (47) |

for any maturity , where , , , . By fitting the SVI parameterisation to noisy option data, one is able to create a smooth implied volatility smile, which then can be used to interpolate implied volatility between strikes and extrapolate implied volatility to strikes which are not traded. The density corresponding to a given implied volatility parameterisation can be computed via the Breeden-Litzenberger formula [4]: . An implied volatility smile is said to be free of butterfly arbitrage if the corresponding density is non-negative: . Let be the implied volatility smile corresponding to a given SVI parameterisation (47). In general, SVI parameterisation (47) is not guaranteed to be free of butterfly arbitrage. However, for a given set of SVI parameters , one can easily verify that the corresponding density is non-negative, and therefore free of butterfly arbitrage. This and recent arbitrage-free SVI parameterisations have recently been studied in [16] and [18], and we refer the interested reader to these papers for more details. As we shall see in the examples considered in Section 4, for finite , the approximate implied volatility derived in Section 2.2 has a tendency to oscillate around the true implied volatility (see Figures 1, 2 and 3). Taking to be the true implied volatility could lead to arbitrage opportunities. In order to prevent this, we propose to smooth the implied volatility approximation by fitting the SVI parameterisation to it. That is, given a model for the underlying and a time to maturity , we first compute the approximate implied volatility as a function of -strike , and then fit an arbitrage-free SVI parameterisation to over some range of strikes, usually chosen to be a symmetric interval around .

4.2 Exponential Lévy models

Suppose that is a Lévy process with Lévy triplet . Then its characteristic function reads

where the drift is constrained by the martingale condition : . From the expansion we can write

with and , for any . The existence of is equivalent to the finiteness of the th moment of by [31, Theorem 25.3], which is clearly satisfied under Assumption 1. Hence, the coefficients in (19) are given by

| (48) |

We examine two exponential Lévy models in detail—the Merton model [30] and the Variance Gamma model [6]—whose Lévy measures are given by:

| (49) | |||||

| (50) |

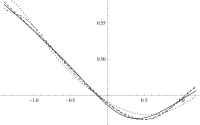

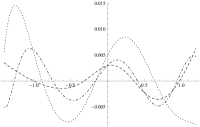

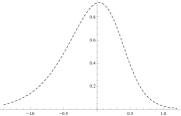

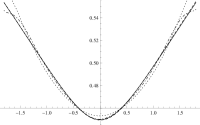

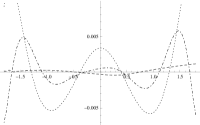

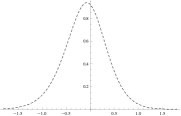

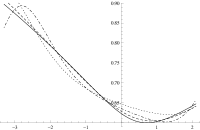

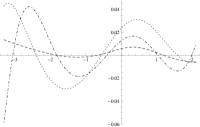

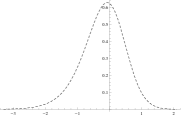

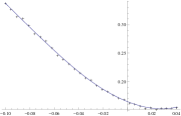

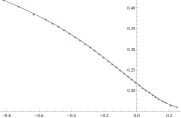

where , . The Merton model is a finite-activity Lévy process (), whereas the Variance Gamma model has infinite activity (). For infinite activity Lévy processes, one typically takes the diffusion component to be zero, namely . We now examine the accuracy of the implied volatility expansion above in these models: the Merton model in Figure 1 and the Variance Gamma in Figure 2. For each of these two sets of plots, we fix some parameters, and draw the implied volatility approximations with for the Merton model and for the Variance-Gamma one, and . We also plot the SVI smoothing of as well as the true implied volatility. The true option price is computed by a quadrature of the inverse Fourier transform representation (1), and the true implied volatility is computed by numerical inversion of the Black-Scholes formula (we use a simple Newton-Raphson algorithm). We also plot the total errors between each approximation (and with SVI smoothing) and the true implied volatility. As discussed above, the implied volatility approximation oscillates around the true implied volatility . However, the relative error corresponding to is less than one percent for nearly all log-moneyness to maturity ratios (LMMRs) satisfying for both models, which is well within the implied volatility bid-ask spread of S&P options. Furthermore, the relative error of with SVI smoothing is about one half percent for all . As a no-arbitrage consistency check, we also plot the density corresponding to the SVI fit. The parameters for each model are as follows:

| Merton model: | (51) | |||

| Variance Gamma model: | (52) |

4.3 The Heston model

In the Heston model [21], the risk-neutral dynamics of are given by

with , , and where and are two standard Brownian motions with correlation . Its characteristic function reads , where

Unlike the exponential Lévy setting, there is no simple general formula for the coefficients . However, from (19), one can compute

| (53) | ||||

| (54) |

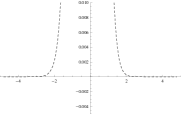

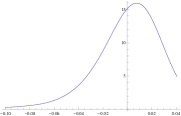

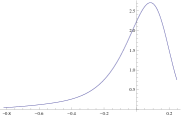

Higher order terms are easily computed using any mathematical software, and are omitted here for clarity. In Figure 3, we plot the function with and , a calibrated SVI to and the true implied volatility (computed exactly as for the Lévy models above). We also plot the relative errors between each approximation (and the SVI smoothing of ) and the true implied volatility. Again the approximation oscillates around the true implied volatility, but the relative error of is less than two percent for nearly all LMMRs satisfying , and that of with SVI smoothing is roughly one percent for all . As before, we also plot the density corresponding to the calibrated SVI parameterisation as a no-arbitrage consistency check. We use the following set of parameters: , , , , , , , .

4.4 Model-free calibration

As noted previously, the model-specific dependence of the approximate implied volatility expansion is entirely captured by the coefficients . This simple structure allows for a model-free calibration of the implied volatility surface. Assume one observes implied volatilities for maturities and , where and are two integers. We shall assume for simplicity that the number of available strikes is the same for each maturity. We suggest the following procedure:

-

(i)

Let be the quoted implied volatility for an option with maturity and strike .

-

(ii)

Let be the approximate implied volatility for an option with maturity and strike computed using the approximation (33).

-

(iii)

At each maturity , leave and as free parameters. Fit to the market’s -maturity implied volatility smile by minimising .

-

(iv)

As an initial guess, use the largest quoted implied volatility at each maturity for , and .

Remark 15.

With and , step (iii) is instantaneous using Mathematica’s FitTo or Matlab’s lsqnonlin for instance.

We test this procedure on SPX index options from January 4, 2010 with and . The results for three separate maturities (, , years) are given on Figure 4. The calibrated parameters are ( is a shorthand notation for ):

| 0.033 | 0.382 | -1.64E-3 | -1.00E-6 | 1.64E-6 | 1.89E-8 | 8.62E-10 | 5.22E-12 | 1.40E-13 |

|---|---|---|---|---|---|---|---|---|

| 0.70 | 0.659 | -1.31E-1 | -5.00E-3 | 2.40E-3 | 4.24E-4 | 6.96E-5 | 2.88E-6 | 4.83E-7 |

| 1.45 | 0.436 | -8.35E-2 | -1.22E-2 | 1.68E-3 | -6.26E-5 | 3.42E-5 | -1.77E-6 | 3.96E-7 |

Remark 16.

If the stock price is an exponential Lévy model, then (48) implies that and should be constant. If this is not so, then exponential Lévy models are probably not the best dynamics to describe the underlying.

Remark 17.

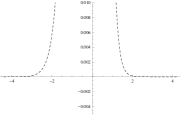

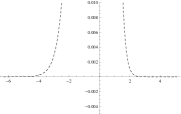

Our whole methodology is based on approximating the characteristic function of a process by a truncated version of its expansion with respect to some small parameter. In essence, this truncation tends to ignore the tail behaviour (high-order terms in the expansion) of the process, and hence, even though the resulting volatility expansion is accurate around the money, there is no reason why it should be so in the tails. The latter, however, are usually not observable in practice, so that this should be of lesser concern for practical implementation. This in particular means that, should one plot the densities corresponding to the fit in Figure 4, the latter may become negative in the tails (hence allowing for arbitrage opportunities). In our calibration example (Figure 4), the density does remain non-negative though. If however it was to become negative, one could perform an SVI fit, as explained in Section 4.1, or, even better, use the fully no-arbitrage SVI version developed in [16].

Acknowledgments

M. Lorig acknowledges financial support from Imperial College London, and both authors are grateful to Claude Martini and Zeliade Systems for their useful comments and for indicating to us the availability of CBOE data. The authors would also like to thank an anonymous referee, whose suggestions improved both the mathematical quality and readability of this manuscript.

Appendix A Proof of Theorem 13

From (34) we observe that involves both and . Theorem 13 will follow directly from Definition 12, and Propositions 19 and 20, both of which provide explicit expressions for these quantities. In all the statements and results below, we shall consider , and define . Furthermore, we recall that, for any , denotes the -th Hermite polynomial from Theorem 13. We first start with the following lemma.

Lemma 18.

For any integers , we have

| (55) |

Proof.

From the Black-Scholes call price formula (8) we clearly obtain , where . Now, for any integers and , we have

| (56) | ||||

| (57) |

The lemma then follows from the identity and from

| (58) | ||||

| (59) |

∎

Proposition 19.

The identity

| (60) |

holds, where the coefficients are defined recursively by and for .

Proof.

Proposition 20.

The following equality holds:

References

- Abramowitz and Stegun [1964] Abramowitz, M. and I. Stegun (1964). Handbook of mathematical functions with formulas, graphs, and mathematical tables, Volume 55. Dover publications.

- Benaim and Friz [2009] Benaim, S. and P. Friz (2009). Regular variation and smile asymptotics. Math. Finance 19(1), 1–12.

- Berestycki et al. [2004] Berestycki, H., J. Busca, and I. Florent (2004). Computing the implied volatility in stochastic volatility models. Communications on Pure and Applied Mathematics 57 (10), 1352–1373.

- Breeden and Litzenberger [1978] Breeden, D. T. and R. H. Litzenberger (1978). Prices of state-contingent claims implicit in option prices. The Journal of Business 51(4), 621–651.

- Brown and Churchill [1996] Brown, J. and R. Churchill (1996). Complex variables and applications, Volume 7. McGraw-Hill New York, NY.

- Carr et al. [1998] Carr, P., D. Madan, and E. Chang (1998). The Variance Gamma process and option pricing. European Finance Review 2(1), 79–105.

- Deuschel et al. [2014] Deuschel, J., P. Friz, A. Jacquier, and S. Violante (2014). Marginal density expansions for diffusions and stochastic volatility, part II: Applications. Communications on Pure and Applied Mathematics 67(2), 321–350.

- Duffie et al. [2003] Duffie, D., D. Filipović, and W. Schachermayer (2003). Affine processes and applications in finance. Annals of Applied Probability 13 (3), 984–1053.

- Duffie et al. [2000] Duffie, D., J. Pan, and K. Singleton (2000). Transform analysis and asset pricing for affine jump-diffusions. Econometrica 68(6), 1343–1376.

- Fouque et al. [2003] Fouque, J.-P., G. Papanicolaou, R. Sircar, and K. Sølna (2003). Singular perturbations in option pricing. SIAM J. Applied Mathematics 63(5), 1648–1665.

- Fouque et al. [2011] Fouque, J.-P., G. Papanicolaou, R. Sircar, and K. Solna (2011). Multiscale Stochastic Volatility for Equity, Interest-Rate and Credit Derivatives. Cambridge University Press.

- Friz et al. [2011] Friz, P., S. Gerhold, A. Gulisashvili, and S. Sturm (2011). Refined implied volatility expansions in the heston model. Quantitative Finance 11 (8), 1151–1164.

- Fukasawa [2011] Fukasawa, M. (2011). Asymptotic analysis for stochastic volatility: Edgeworth expansion. Electronic Journal of Probability 16, 764–791.

- Gatheral [2004] Gatheral, J. (2004). A parsimonious arbitrage-free implied volatility parameterization with application to the valuation of volatility derivatives. Presentation at Global Derivatives & Risk Management, Madrid.

- Gatheral et al. [2012] Gatheral, J., E. Hsu, P. Laurence, C. Ouyang, and T. Wang (2012). Asymptotics of implied volatility in local volatility models. Mathematical Finance 22 (4), 591–620.

- Gatheral and Jacquier [2014] Gatheral, J. and A. Jacquier (2014). Arbitrage-free svi volatility surfaces. Quantitative Finance 14(1), 59–71.

- Gulisahsvili and Stein [2010] Gulisahsvili, A. and E. Stein (2010). Asymptotic behavior of the stock price distribution density and implied volatility in stochastic volatility models. Applied Mathematics & Optimization 61 (3), 287–315.

- Guo et al. [2012] Guo, G., A. Jacquier, C. Martini, and L. Neufcourt (2012). Generalised arbitrage-free svi volatility surfaces. arXiv:1210.7111.

- Hagan et al. [2002] Hagan, P., D. Kumar, A. Lesniewski, and D. Woodward (2002). Managing smile risk. Wilmott Magazine, 84–108.

- Henry-Labordère [2008] Henry-Labordère, P. (2008). Analysis, geometry and modeling in finance. Chapman and Hill / CRC.

- Heston [1993] Heston, S. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6(2), 327–343.

- Jacquier et al. [2013] Jacquier, A., M. Keller-Ressel, and A. Mijatović (2013). Large deviations and stochastic volatility with jumps: asymptotic implied volatility for affine models. Stochastics 85(2), 321–345.

- Jacquier and Lorig [2013] Jacquier, A. and M. Lorig (2013). The smile of certain Lévy-type models. SIAM Journal on Financial Mathematics 4(1), 804–830.

- Lee [2004] Lee, R. (2004). The moment formula for implied volatility at extreme strikes. Mathematical Finance 14(3), 469–480.

- Lewis [2001] Lewis, A. (2001). A simple option formula for general jump-diffusion and other exponential Lévy processes. Preprint available at SSRN:282110.

- Lipton [2002] Lipton, A. (2002). The vol smile problem. Risk (February), 61–65.

- Lorig [2013] Lorig, M. (2013). The exact smile of certain local volatility models. Quantitative Finance 13(6), 897–905.

- Lorig et al. [2014] Lorig, M., S. Pagliarani, and A. Pascucci (2014). Explicit implied vols for multifactor local-stochastic vol models. ArXiv preprint arXiv:1306.5447.

- Lukacs [1970] Lukacs, E. (1970). Characteristic functions (2nd edition). Hafner Pub. Co. New York, NY.

- Merton [1976] Merton, R. (1976). Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics 3(1), 125–144.

- Sato [1999] Sato, K. (1999). Lévy processes and infinitely divisible distributions. Cambridge University Press.

- Takahashi and Toda [2013] Takahashi, A. and M. Toda (2013). Note on an extension of an asymptotic expansion scheme. To appear in International Journal of Theoretical and Applied Finance 16(5).

- Tankov [2010] Tankov, P. (2010). Pricing and hedging in exponential lévy models: review of recent results. In Paris-Princeton Lecture Notes in Mathematical Finance.